Quantum Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

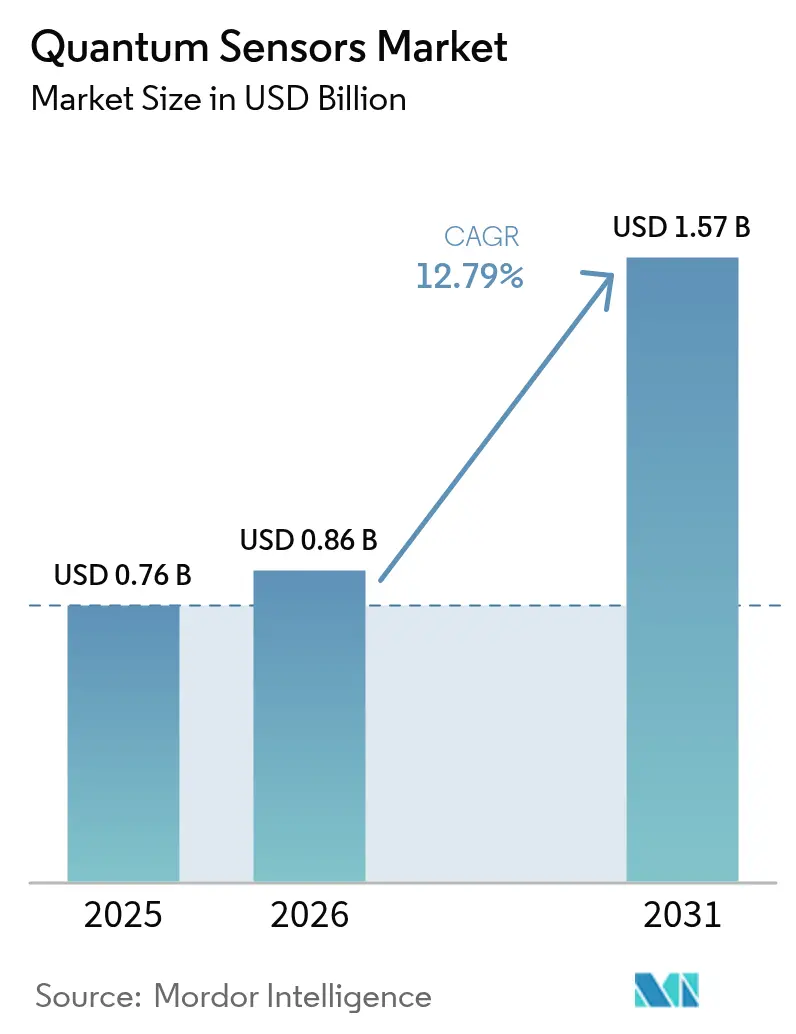

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.57 Billion |

| Growth Rate (2026 - 2031) | 12.79% CAGR |

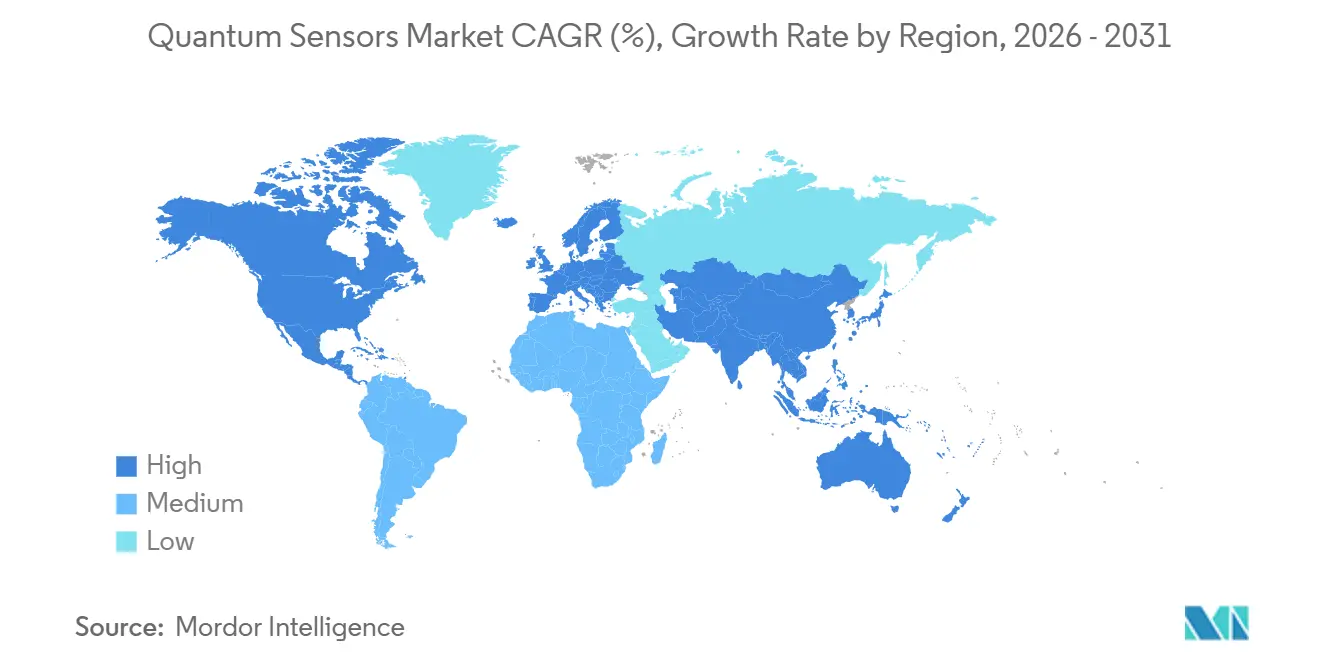

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

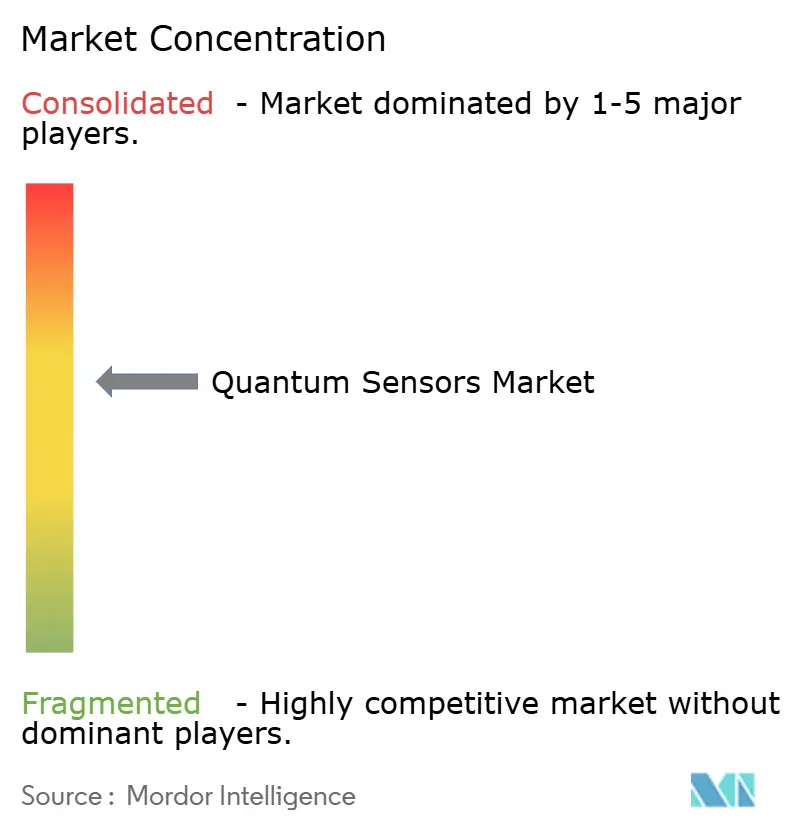

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Quantum Sensors Market Analysis by Mordor Intelligence

The quantum sensors market size is expected to grow from USD 0.76 billion in 2025 to USD 0.86 billion in 2026 and is forecast to reach USD 1.57 billion by 2031 at a 12.79% CAGR over 2026-2031. Defense-funded positioning, navigation, and timing upgrades dominate early volumes, yet commercial telecom synchronization, autonomous navigation, and satellite constellations are widening the addressable base. Venture funding channeled toward chip-scale atomic clocks and nitrogen-vacancy (NV) diamond magnetometers is shrinking unit costs, while wafer-scale fabrication is shortening production lead times. Governments in the United States, China, Japan, and Europe are underwriting pilot deployments that validate ruggedized field performance, accelerating the transition from laboratory prototypes to revenue-generating products. Regulatory scrutiny around export-controlled quantum hardware remains a moderating factor, but industry players report smoother license workflows as standards bodies formalize interface, calibration, and cybersecurity protocols.

Key Report Takeaways

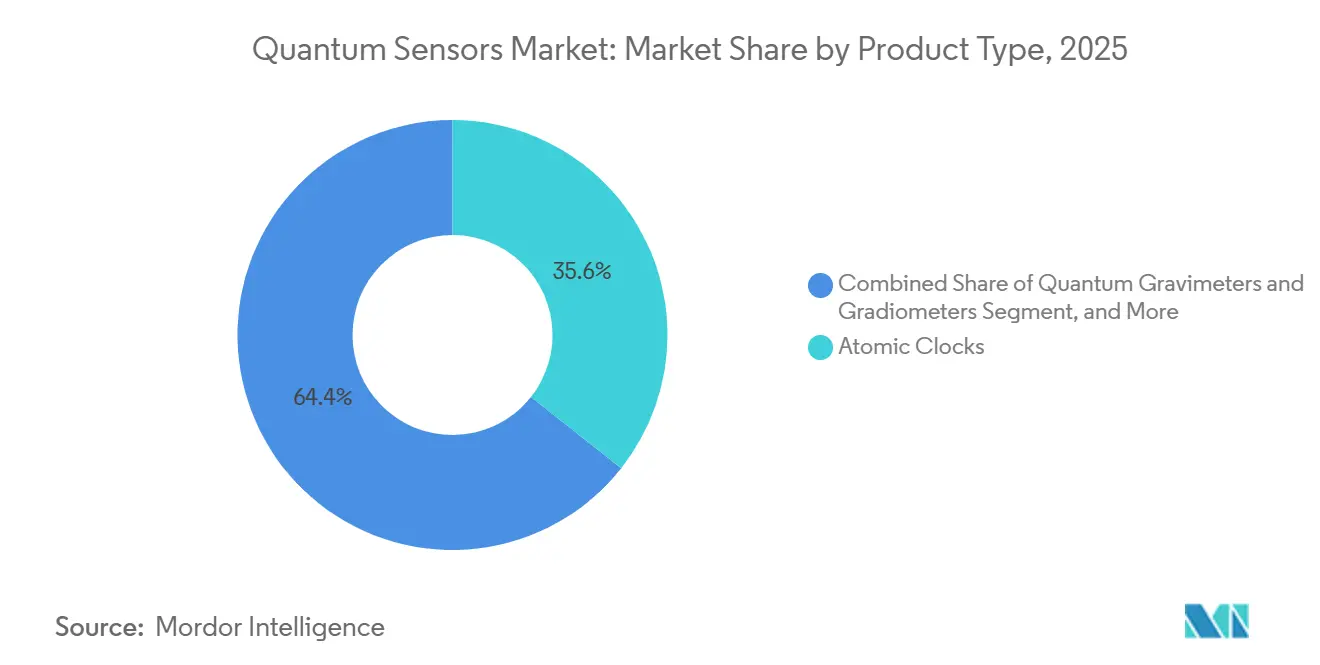

- By product type, atomic clocks led with 35.63% revenue share in 2025; quantum gravimeters and gradiometers are projected to expand at a 13.96% CAGR through 2031.

- By sensing mechanism, cold-atom interferometry accounted for 39.78% of the quantum sensors market share in 2025, while NV-diamond sensors are advancing at a 13.74% CAGR to 2031.

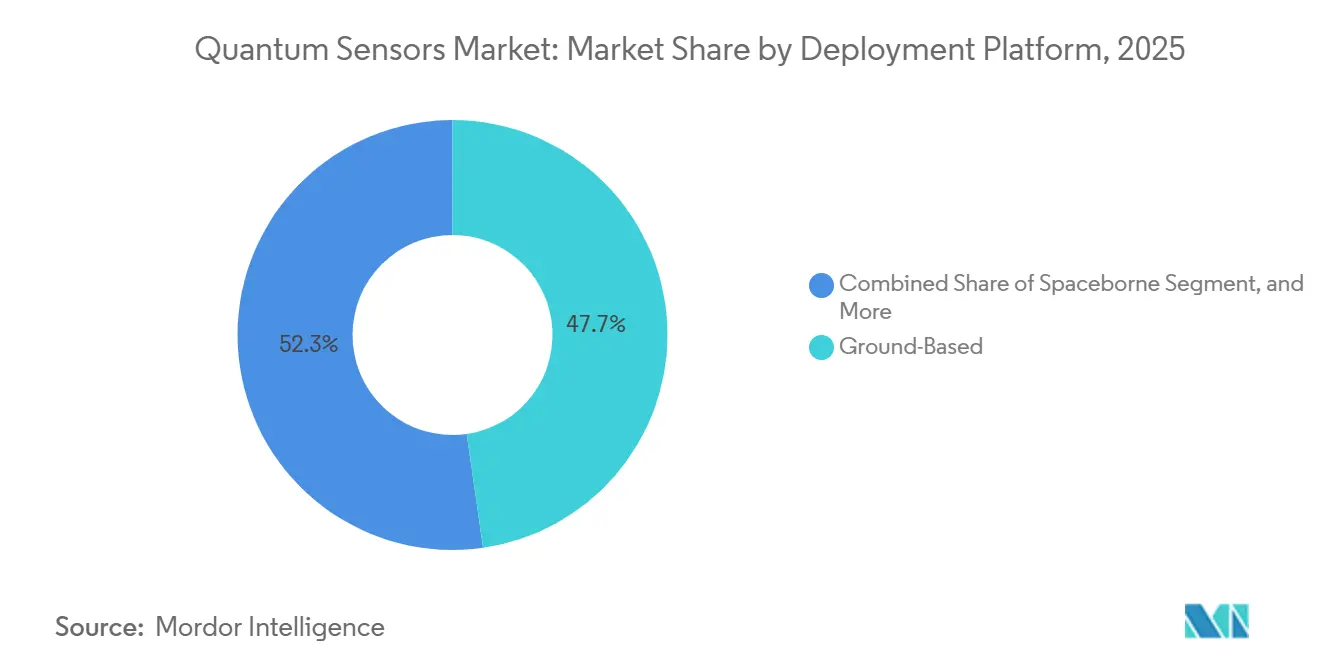

- By deployment platform, ground-based systems accounted for 47.74% of the quantum sensor market in 2025; spaceborne installations are projected to grow at a 13.54% CAGR through 2031.

- By end-user, defense and security captured a 42.37% share in 2025, whereas space and satellite applications recorded the highest projected CAGR at 13.93% through 2031.

- By geography, North America dominated at 38.91% revenue share in 2025, while Asia-Pacific is forecast to post a 13.77% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Quantum Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Defense Funding for Quantum PNT | +2.8% | North America, Europe, Asia-Pacific (China, India) | Medium term (2-4 years) |

| National Quantum Initiatives and Budgets | +2.5% | Global, concentrated in U.S., EU, China, Japan | Long term (≥ 4 years) |

| Demand for High-Precision Autonomous Navigation | +2.2% | North America, Europe, Asia-Pacific (Japan, South Korea) | Medium term (2-4 years) |

| Commercial Rollout of Quantum Clocks in Telecom and Datacenters | +1.9% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Spaceborne Climate-Monitoring Gravimeters | +1.6% | Global, led by ESA, NASA, JAXA missions | Long term (≥ 4 years) |

| Wafer-Scale Fabrication Drives Cost Decline | +1.4% | Global, manufacturing hubs in North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Defense Funding for Quantum PNT

U.S. defense allocations reached USD 877 million in fiscal 2025 for quantum science, with large tranches earmarked for cold-atom inertial sensors and optical atomic clocks to harden navigation against GPS jamming.[1]U.S. Department of Defense, “Quantum Science Budget FY 2025,” DEFENSE.GOV The United Kingdom and NATO partners are issuing multiyear contracts for quantum gravimeters that locate underground structures without satellite links. China’s Strategic Support Force is integrating NV-diamond magnetometers into anti-submarine warfare prototypes, leveraging room-temperature operation to cut maintenance burdens. India’s 2024 quantum roadmap finances indigenous atomic clocks for the NavIC constellation, reflecting a broader pivot toward supply-chain sovereignty.

National Quantum Initiatives and Budgets

The EU Quantum Flagship reserved EUR 1 billion (USD 1.13 billion) for application-ready sensing platforms through 2028, bundling healthcare, mobility, and space projects under unified milestones. Japan’s 2025 supplementary budget set aside JPY 45 billion (USD 310 million) for spaceborne gravimeters tasked with monitoring volcanic activity. Australia, South Korea, and Canada operate similar schemes that shoulder risk for domestic startups, anchor first-of-a-kind deployments, and establish national performance benchmarks.

Demand for High-Precision Autonomous Navigation

Bosch demonstrated a quantum inertial measurement unit with 0.01-degree-per-hour drift, enabling autonomous trucks to navigate tunnels and dense urban cores without satellite correction.[2]Bosch, “Quantum Inertial Measurement Unit,” BOSCH.COM The U.S. Federal Aviation Administration is trialing cold-atom interferometers on urban air mobility routes where skyscraper multipath corrupts GNSS signals. Japanese pilot programs plan to embed quantum sensors into rural shuttle fleets to maintain centimeter-grade accuracy along poorly mapped roads.

Commercial Rollout of Quantum Clocks in Telecom and Datacenters

International Telecommunication Union standard G.8272.1, released in 2024, codifies quantum-clock specs for 5G and 6G timing, unlocking procurement budgets across carriers.[3]International Telecommunication Union, “ITU-T G.8272.1 Recommendation,” ITU.INT Microchip Technology shipped its 10,000th chip-scale atomic clock in 2025, claiming 1×10⁻¹² stability in a sub-50 cm³ package. Hyperscale cloud providers report 40% fewer database-conflict events after swapping GPS-disciplined oscillators for quantum references.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Deployment and Maintenance Costs | -1.8% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Environmental Sensitivity of Cold-Atom Systems | -1.3% | Airborne and mobile platforms worldwide | Medium term (2-4 years) |

| Alkali-Vapor Cell Supply-Chain Bottlenecks | -0.9% | Manufacturing centers in North America and Europe | Short term (≤ 2 years) |

| Export-Control Restrictions on Quantum Tech | -0.7% | Cross-border sales from U.S., EU, China to restricted entities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Deployment and Maintenance Costs

Cold-atom gravimeters command list prices of USD 500,000-2 million, and life-cycle upkeep, including laser replacement, vacuum maintenance, and calibration,n adds 15-20% annually, delaying breakeven for oil, gas, and mining buyers. Healthcare pilots in magnetoencephalography weigh USD 3-5 million systems against USD 1 million superconducting alternatives, slowing hospital adoption. Until wafer-scale integration cuts the bill of materials by an order of magnitude, mainstream adoption remains gated to high-value verticals.

Environmental Sensitivity of Cold-Atom Systems

Airborne gravimeters require active vibration isolation with a bandwidth exceeding 100 Hz, adding mass that trims aircraft survey range. U.S. Army road trials showed 60% coherence-time degradation in vehicle-mounted accelerometers under off-road conditions, forcing computational overhead for real-time error compensation. Space missions are subject to radiation-induced decoherence, prompting ESA to test hardened laser systems on the 2027 CARIOQA mission.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Atomic Clocks Sustain Leadership While Gravimeters Surge

Atomic clocks contributed 35.63% of 2025 revenue, buoyed by telecom, satellite navigation, and financial time-stamping. The quantum sensors market size attributed to clocks is projected to reach USD 0.55 billion by 2031 as chip-scale designs penetrate edge-network gear. Quantum gravimeters and gradiometers are forecast to expand at a 13.96% CAGR, lifting their share of the quantum sensors market above 20% by 2031, driven by demand from oil, gas, and geothermal exploration.

Microchip's 2025 module, which integrates laser diodes, vapor cells, and control ASICs, achieves an 80% reduction in size and power consumption, highlighting a trend towards component standardization in clocks. In contrast, gravimeters are still tailored to individual specifications, facing 12-18 month lead times and requiring vendor-specific calibration. This lack of interoperability has made conservative energy firms hesitant to adopt them.

By Sensing Mechanism: Cold-Atom Dominance Faces NV-Diamond Momentum

In 2025, cold-atom interferometers accounted for 39.78% of total sales, solidifying their dominance in high-precision gravimetry and Positioning, Navigation, and Timing (PNT) contracts. These devices are increasingly favored for their ability to deliver unparalleled accuracy in measuring gravitational fields, which is critical for applications such as geophysics, oil and gas exploration, and navigation systems. Meanwhile, NV-diamond devices are set to seize an 18% share of the quantum sensor market by 2031. This growth is fueled by the rising demand for miniaturized magnetometers, which are highly sought after in defense applications for detecting submarines and in biomedical sectors for advanced imaging and diagnostics.

Laser cooling underpins unmatched precision, yet size, weight, and power penalties hinder mobile use. NV-diamond sensors operate at room temperature and tolerate vibration, with Element Six cutting synthetic-diamond wafer prices 40% in 2025. Rydberg-atom, optomechanical, and SQUID modalities occupy smaller niches focused on RF sensing, consumer wearables, and ultra-low-field biomagnetism, respectively.

By Deployment Platform: Ground Installations Hold Scale, Spaceborne Growth Accelerates

In 2025, national metrology institutes and fixed seismic arrays adopted quantum references, leading ground-based nodes to capture 47.74% of the revenue. These nodes play a critical role in ensuring precise measurements and enhancing the reliability of quantum sensors. Meanwhile, buoyed by satellite timing and climate-monitoring missions, spaceborne payloads are set to expand at a robust 13.54% CAGR, aiming for a 25% share of the quantum sensor market by 2031. The increasing demand for accurate data in space-based applications is driving this growth trajectory.

Microgravity enhances atom interrogation times, amplifying sensitivity and enabling more precise measurements. ESA’s CARIOQA gravimeter, slated for 2027, aims for a precision of 1 milligal, which could significantly improve geophysical studies and resource exploration. Concurrently, NASA’s Deep Space Atomic Clock has demonstrated an impressive stability of 2×10⁻¹⁶ over extended multiyear orbits, showcasing its potential for deep-space navigation and timekeeping. While airborne and marine deployments may lag in adoption, they are increasingly pivotal for applications such as mineral surveys and submarine navigation, where traditional methods face limitations. These deployments are expected to gain strategic importance as advancements in quantum sensor technology continue to unfold.

By End-User: Defense Still Commands, Space and Satellite Posts Fastest Gains

Defense and security sectors generated 42.37% of total revenue in 2025, driven by significant investments in multi-theater Positioning, Navigation, and Timing (PNT) system upgrades. These advancements highlight the growing emphasis on enhancing operational capabilities in complex and diverse environments. Meanwhile, space and satellite operators are poised to experience the industry's fastest growth rate, with a projected CAGR of 13.93%. This growth is expected to elevate their share of the quantum sensor market to USD 0.34 billion by 2031, reflecting the increasing adoption of advanced technologies in space exploration and satellite operations.

While U.S. and European defense budgets focus on developing GPS-denied navigation systems and magnetic-anomaly detection technologies to strengthen national security, satellite constellations are undergoing a transition. These constellations are integrating onboard quantum clocks, a move aimed at reducing their reliance on ground stations and enhancing the precision of satellite-based systems. In the commercial sector, oil, gas, and mining companies are leveraging gravimeters to optimize resource exploration, achieving a 30-40% reduction in exploratory drilling costs. Concurrently, neurology centers are actively testing NV-diamond magnetoencephalography, a cutting-edge tool designed to improve the accuracy of epilepsy focalization, showcasing the expanding applications of quantum sensors in healthcare.

Geography Analysis

North America anchors demand through robust defense spending, National Institute of Standards and Technology clock programs, and Silicon Valley venture capital pipelines. U.S. federal contracts bridge technology-readiness gaps, while Canadian research hubs push NV-diamond magnetometry for mining and telecom applications. The region’s installed base creates a service ecosystem for calibration, spares, and upgrade cycles, reinforcing supplier lock-in.

Asia-Pacific records the fastest revenue trajectory as China, Japan, and India escalate sovereign positioning and climate-monitoring missions. Chinese Academy of Sciences’ 2024 orbital gravimeter demonstrated sub-milligal Earth-observational capability, spurring provincial governments to co-fund downstream analytics startups. Japan’s quantum innovation hub links universities and industry, focusing on Rydberg-atom sensors to monitor electromagnetic spectrum congestion across dense urban corridors. India advances chip-scale atomic-clock manufacturing to curb reliance on imports and bolster the resilience of its regional navigation system.

Europe maintains technological parity through coordinated EU funding, but procurement fragmentation among member states tempers volume scaling. Germany and France co-lead cold-atom gravimeter prototypes for renewable-energy exploration, while the United Kingdom channels commercialization vouchers toward laser-component specialists. Niche applications in geothermal mapping and railway tunnel inspection are driving incremental demand. South America, the Middle East, and Africa remain in pilot-project mode, focusing on mineral exploration in Chile and offshore oil surveys in the Gulf of Oman. Vendor outreach focuses on leasing models to offset high capital costs and align with resource-royalty cash flows.

Competitive Landscape

The quantum sensors market hosts a blend of diversified industrial incumbents and venture-backed specialists. Honeywell International and Robert Bosch convert legacy aerospace and automotive channels into early mover advantage for photonic accelerometers and quantum inertial measurement units, bundling hardware with analytics to defend pricing. Infleqtion, AOSense, and Muquans compete on performance in defense and space contracts where 1-femtotesla sensitivities and micro-gal gravimetry eclipse cost concerns.

Cost-down pressure is mounting. SiTime’s 2025 MEMS-quantum hybrid oscillator achieves 1×10⁻¹¹ stability at one-tenth price, threatening mid-tier atomic-clock suppliers. Element Six scales synthetic-diamond wafers to commodity pricing, empowering new entrants in room-temperature magnetometry. Teledyne e2v doubles global vapor-cell output by adding a Grenoble line, unclogging a component bottleneck that had been throttling chip-scale atomic-clock growth.

Intellectual property positions are tightening: Honeywell held 47 awarded patents on optomechanical accelerometers by December 2025, and Bosch holds patents covering thermal-management schemes critical to mobile cold-atom devices. Export-control regimes under the Wassenaar Arrangement complicate cross-border scaling, granting regional champions breathing room but also constraining total addressable revenue in geographies with restricted end-users.

Quantum Sensors Industry Leaders

AOSense Inc.

Robert Bosch GmbH

Microchip Technology Inc.

Campbell Scientific Inc.

LI-COR Biosciences Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Infleqtion secured a USD 15 million U.S. Air Force Research Laboratory contract to build airborne quantum magnetometers targeting 1 femtotesla sensitivity.

- December 2025: Honeywell Quantinuum integrated a photonic accelerometer into an automotive-grade inertial navigation system, entering OEM qualification.

- November 2025: European Space Agency awarded EUR 22 million (USD 24.9 million) to Airbus Defence and Space and Muquans for a CARIOQA spaceborne gravimeter.

- October 2025: Robert Bosch confirmed 2027 series production for quantum inertial measurement units in autonomous trucks.

Global Quantum Sensors Market Report Scope

The Quantum Sensors Market Report is Segmented by Product Type (Atomic Clocks, Quantum Magnetometers, Quantum Accelerometers and Gyroscopes, Quantum Gravimeters and Gradiometers, PAR Quantum Sensors, Other Product Types), Sensing Mechanism (Cold-Atom Interferometry, Nitrogen-Vacancy (NV) Diamond, Rydberg-Atom Electric-Field Sensors, Optomechanical/Photonic Sensors, Superconducting Quantum Interference Sensors), Deployment Platform (Ground-Based, Airborne, Spaceborne, Marine/Sub-Surface), End-User (Defense and Security, Space and Satellite, Oil, Gas and Mining, Healthcare and Life Sciences, Transportation and Automotive, Telecom and Datacenters), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Atomic Clocks |

| Quantum Magnetometers |

| Quantum Accelerometers and Gyroscopes |

| Quantum Gravimeters and Gradiometers |

| PAR Quantum Sensors |

| Other Product Types |

| Cold-Atom Interferometry |

| Nitrogen-Vacancy (NV) Diamond |

| Rydberg-Atom Electric-Field Sensors |

| Optomechanical / Photonic Sensors |

| Superconducting Quantum Interference Sensors |

| Ground-Based |

| Airborne |

| Spaceborne |

| Marine / Sub-Surface |

| Defense and Security |

| Space and Satellite |

| Oil, Gas and Mining |

| Healthcare and Life Sciences |

| Transportation and Automotive |

| Telecom and Datacenters |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Atomic Clocks | ||

| Quantum Magnetometers | |||

| Quantum Accelerometers and Gyroscopes | |||

| Quantum Gravimeters and Gradiometers | |||

| PAR Quantum Sensors | |||

| Other Product Types | |||

| By Sensing Mechanism | Cold-Atom Interferometry | ||

| Nitrogen-Vacancy (NV) Diamond | |||

| Rydberg-Atom Electric-Field Sensors | |||

| Optomechanical / Photonic Sensors | |||

| Superconducting Quantum Interference Sensors | |||

| By Deployment Platform | Ground-Based | ||

| Airborne | |||

| Spaceborne | |||

| Marine / Sub-Surface | |||

| By End-User | Defense and Security | ||

| Space and Satellite | |||

| Oil, Gas and Mining | |||

| Healthcare and Life Sciences | |||

| Transportation and Automotive | |||

| Telecom and Datacenters | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is revenue growing in the quantum sensors market?

The market is set to rise from USD 0.86 billion in 2026 to USD 1.57 billion by 2031 at a 12.79% CAGR.

Which product type currently earns the most money?

Atomic clocks lead with 35.63% of 2025 revenue, driven by telecom and satellite timing demand.

What is the strongest growth opportunity by end-user?

Space and satellite operators are projected to post a 13.93% CAGR through 2031 as constellations adopt onboard quantum clocks and gravimeters.

Which region will add the most new sales?

Asia-Pacific is forecast to achieve a 13.77% CAGR, closing the gap with North America by 2031.

What main barrier slows wider adoption?

High acquisition and maintenance costs, especially for cold-atom systems, remain the largest commercial hurdle.

Page last updated on: