Organic Rankine Cycle Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

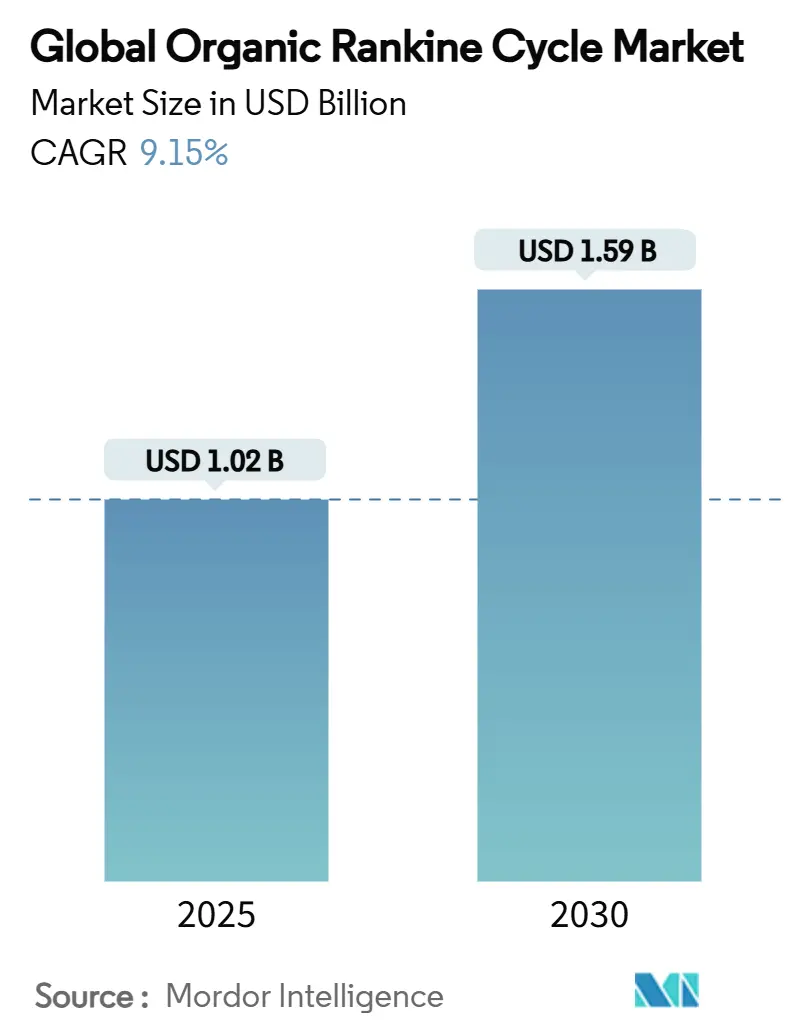

| Market Size (2025) | USD 1.03 Billion |

| Market Size (2030) | USD 1.59 Billion |

| Growth Rate (2025 - 2030) | 9.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Rankine Cycle Market Analysis by Mordor Intelligence

The Global Organic Rankine Cycle Market size is estimated at USD 1.02 billion in 2025, and is expected to reach USD 1.59 billion by 2030, at a CAGR of 9.15% during the forecast period (2025-2030).

Rapid policy momentum around industrial decarbonization, stricter emission rules for heat-intensive sectors, and rising investment in low-temperature renewable power collectively underpin this steady expansion of the Organic Rankine Cycle market. Uptake is strongest where waste-heat obligations and clean-electricity incentives converge, such as in the United States' Production Tax Credit, Canada’s 30% Clean Technology Investment Tax Credit, and the European Union’s Clean Industrial Deal. Growth is further reinforced by geothermal build-outs in Kenya, Indonesia, and the Philippines, which increasingly specify binary-cycle equipment, as well as by data-center operators that now view waste-heat-to-power modules as a route to lower operating costs and Scope 2 emissions.

Key Report Takeaways

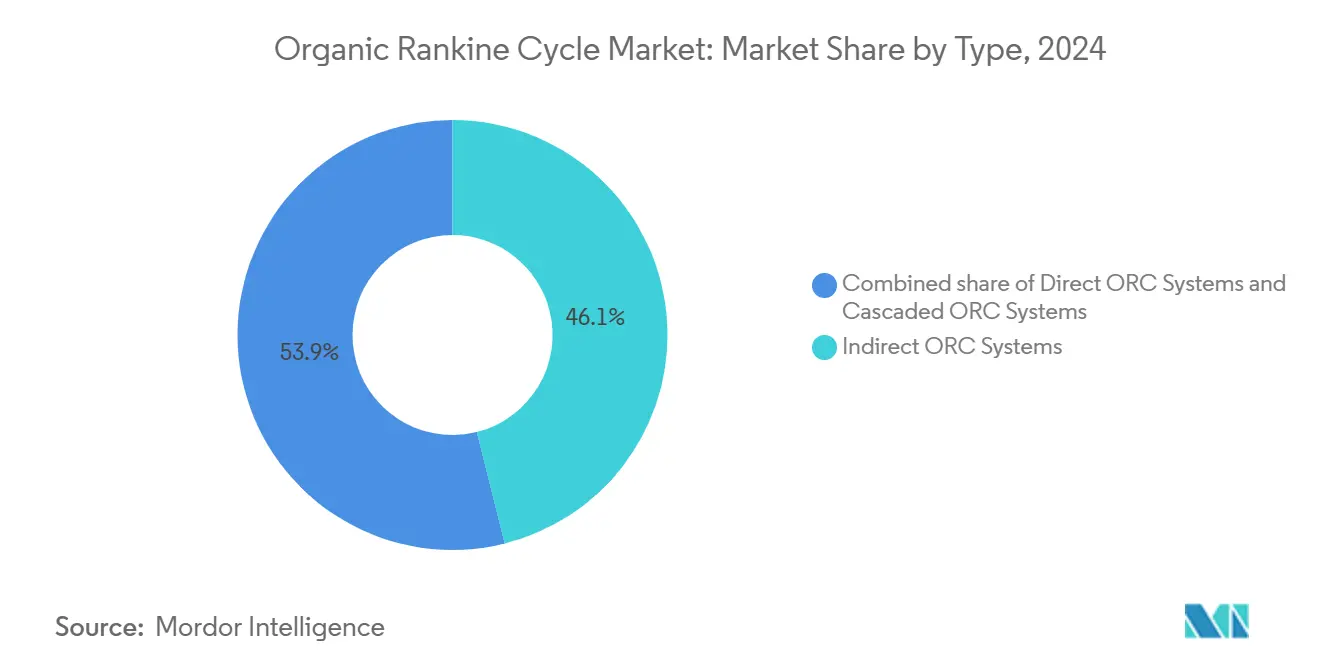

- By type, indirect systems led the 2024 landscape with 46.1% of the Organic Rankine Cycle market share, while cascaded systems are projected to post the fastest 14.4% CAGR through 2030

- By working fluid, siloxanes commanded 40.7% share of the Organic Rankine Cycle market size in 2024; super-critical CO₂ alternatives are expanding at a 12.8% CAGR to 2030, supported by tighter F-gas curbs.

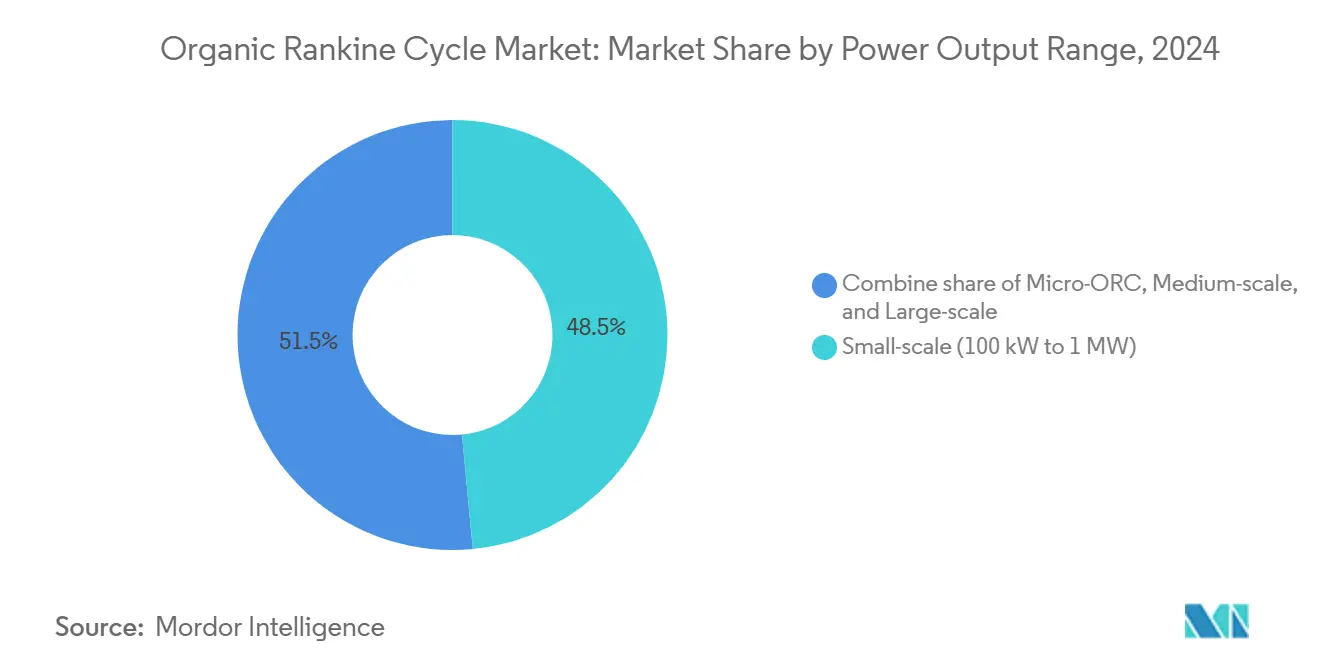

- By power output range, small-scale units between 100 kW and 1 MW accounted for 48.5% of the Organic Rankine Cycle market size in 2024, whereas sub-100 kW micro units are advancing at an 11.7% CAGR to 2030

- By application, waste-heat recovery held 46.5% of the Organic Rankine Cycle market share in 2024; marine and transport retrofits are expected to log a 13.3% CAGR, the fastest across all applications.

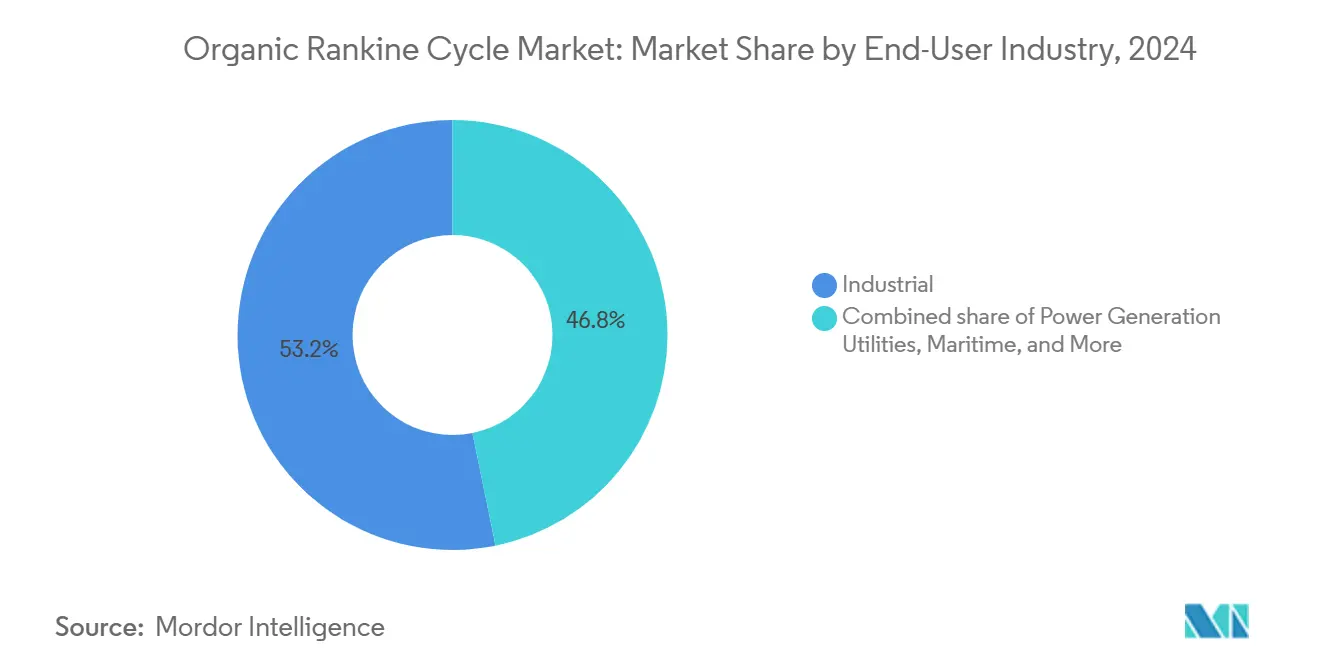

- By end-user industry, industrial facilities accounted for 53.2% of 2024 demand, while data-center customers are on track for a 15.6% CAGR, the top growth rate among end-users.

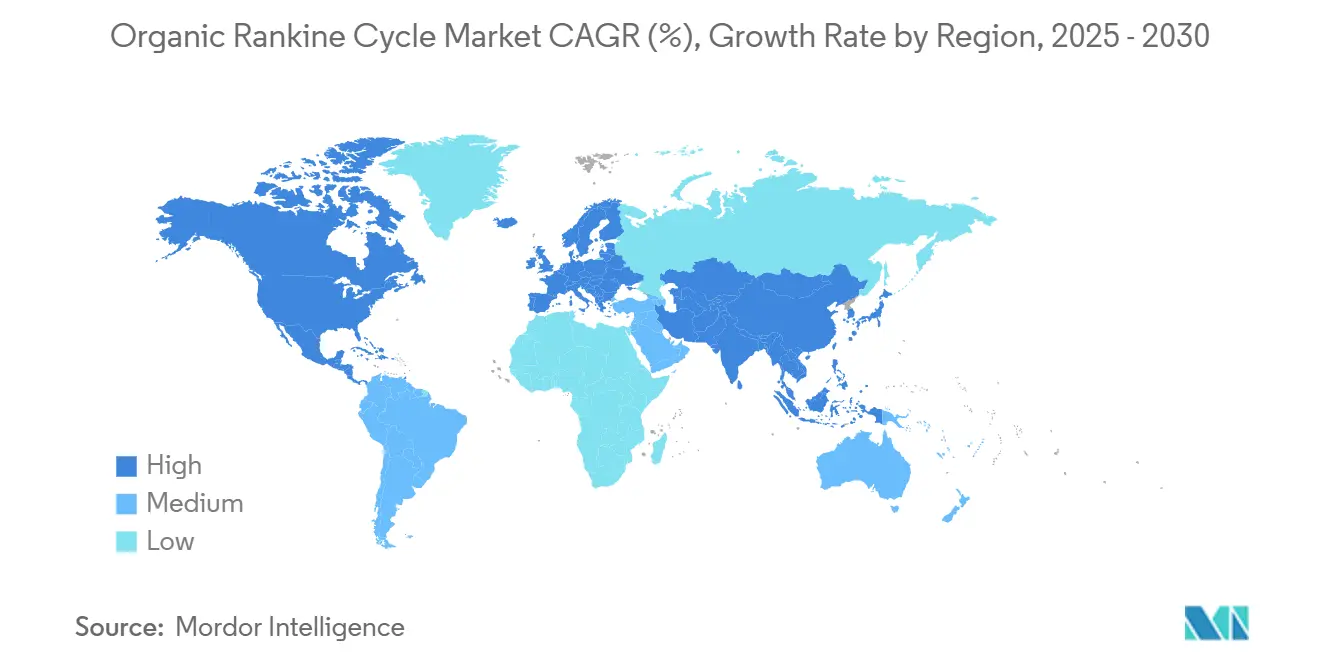

- By geography, North America accounted for 42.9% of the market share in 2024, while the Asia-Pacific region drove market growth, registering a CAGR of 13.9% through 2030.

Global Organic Rankine Cycle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter emission rules accelerate waste-heat recovery | +2.1% | EU, North America, global spill-over | Medium term (2-4 years) |

| Geothermal and biomass capacity expansion | +1.8% | Asia-Pacific core, Latin America & Africa emerging | Long term (≥4 years) |

| Subsidies & feed-in tariffs for distributed plants | +1.5% | North America & EU, rolling into APAC | Short term (≤2 years) |

| Industrial decarbonization targets | +1.7% | Global, early adoption in OECD | Medium term (2-4 years) |

| Falling cost of next-generation HFO fluids | +1.0% | Global | Short term (≤2 years) |

| IMO rules driving LNG-carrier retrofits | +0.9% | Global shipping lanes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent emission regulations accelerating industrial waste-heat recovery projects

The Carbon Border Adjustment Mechanism now obliges importers to report embedded emissions, pressuring steel and cement producers to deploy on-site power recovery through Organic Rankine Cycle market solutions.(1)Source: European Commission, “Implementing Regulation 2023/1773,” europa.eu In the United States, the phasedown of hydrofluorocarbons has nudged plant operators toward natural-refrigerant ORC systems that avoid leak-detection penalties.(2)Source: Federal Register, “Phasedown of Hydrofluorocarbons,” federalregister.gov Studies show that a single ORC retrofit can trim cement-plant CO₂ output by up to 30%, a scale of reduction that meets several jurisdictions’ permitting thresholds. Because the rule sets have hard compliance dates, the Organic Rankine Cycle market is shifting from optional energy-efficiency projects to mandatory license-to-operate investments.

Rapid growth in geothermal & biomass power installations

Global geothermal capacity reached 16,318 MW in 2024, with binary ORC units accounting for roughly one-quarter of that total. Kenya’s 105 MW Menengai complex illustrates the appeal: modular plants financed by multilateral banks deliver firm power with a lower land footprint than flash systems. The Philippines commissioned a 28.9 MWe binary addition that transforms residual heat into 253,000 MWh of extra output, cutting 72,200 t of CO₂ annually. Similar projects are currently under appraisal across Indonesia, Latin America, and Eastern Africa, where resource mapping has been enhanced thanks to advances in electromagnetic imaging. The Organic Rankine Cycle market gains a long-tail flow of equipment orders as these new wells come online.

Government subsidies & feed-in tariffs for distributed ORC plants

Thirty-percent refundable credits in Canada now apply to all qualified ORC gear and can reach higher rates when job-quality thresholds are met. Parallel incentives under U.S. Sections 45Y and 48E lock in production- or investment-based support for zero-emission generators commissioned after 2025. Italy’s FER X decree and Spain’s quarterly remuneration updates likewise stabilize cash flows for sub-5 MW renewable units, allowing industrial hosts to finance Organic Rankine Cycle market projects without utility backing. The cumulative effect is a global pipeline of smaller distributed schemes that previously struggled to clear hurdle rates.

Industrial decarbonization targets in energy-intensive sectors

Cement, steel, and chemical producers are now publishing roadmaps aligned with national net-zero laws, raising interest in hybrid heat platforms that combine electric boilers, thermal storage, and ORC power blocks. Demonstration plants show that integrating waste heat and renewable sources for 150-250 °C processes could avoid nearly 19 million t CO₂ annually across European industry. These same enterprises also evaluate super-critical CO₂ loops because of their compact turbines and refrigerant-free operation. Policy deadlines and corporate pledges are redefining capital-budget priorities, placing Organic Rankine Cycle market technology squarely in line for near-term replacement cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX compared with steam Rankine systems | -1.8% | Global, with higher impact in price-sensitive emerging markets | Short term (≤ 2 years) |

| Shortage of skilled EPC contractors for megawatt-scale ORCs | -1.2% | Global, with acute shortages in North America and Europe | Medium term (2-4 years) |

| Supply bottlenecks for high-temperature seals & expanders | -0.9% | Global, with manufacturing concentrated in Europe and Asia | Medium term (2-4 years) |

| Regulatory uncertainty over PFAS-based refrigerants | -0.7% | North America & EU, with spillover effects to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High upfront CAPEX compared with steam Rankine systems

Large-frame steam cycles maintain an installed-cost edge at higher outputs, especially where import tariffs inflate component expenses. Inflation has lifted quotation prices for turbines and shell-and-tube heat exchangers, stretching payback periods for some mid-cap manufacturers. Governments partly offset this hurdle through investment credits and accelerated depreciation, but smaller firms with weaker balance sheets still need concessional lending to adopt Organic Rankine Cycle market solutions.

Shortage of skilled EPC contractors for megawatt-scale ORCs

An aging workforce in welding, electrical fitting, and turbine installation constrains project throughput, particularly in regions where utility solar and wind programs already absorb a significant portion of the available labor pool. While technical colleges and trade alliances expand certification programs, the lead time to train field crews exceeds the near-term construction surge expected for Organic Rankine Cycle industry projects. Vendors respond by standardizing modules and simplifying commissioning steps to cut on-site labor hours.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Indirect dominance with cascaded acceleration

In 2024, indirect circuits, where thermal oil isolates the process fluid, secured 46.1% of the Organic Rankine Cycle market. Their robustness at 300-400 °C keeps maintenance needs low in cement and petrochemical loops. Over the forecast period, cascaded arrangements are expected to grow at a 14.4% CAGR as operators seek a multi-stage recovery that boosts net electrical yield by 10-15% compared to single-stage designs. Cascaded adoption spreads fastest in steel mills with multiple heat-grade streams; however, direct systems retain relevance in geothermal prospects, where brine compatibility reduces capital expenditure and piping costs.

Second-generation cascaded packages also provide redundancy: if an upper stage is offline, the lower stage continues to produce power, thereby preserving uptime. This operational resilience is critical where continuous process lines cannot risk total plant outages, thereby securing a durable market share for cascaded designs within the Organic Rankine Cycle market.

By Working Fluid: Siloxanes still lead, super-critical CO₂ on rise

Siloxanes captured 40.7% of the 2024 demand, thanks to their chemical stability across the 200-350 °C range and negligible ozone-depletion potential. Yet regulatory cost pressure is shifting selections; European F-gas quotas have inflated high-GWP refrigerant prices tenfold since 2014.(3)Source: Green Cooling Initiative, “High GWP Refrigerants Face Soaring Prices,” green-cooling-initiative.org Vendors now promote natural fluids, propane, butane, pentane, and super-critical CO₂, the latter poised for a 12.8% CAGR through 2030 within the Organic Rankine Cycle market.

Super-critical CO₂ turbines operate on a denser working fluid, enabling compact footprints that are attractive to data-center rooftops and offshore platforms. Manufacturers point to modular skids weighing under 5 t per 250 kW gross, representing a step change compared with legacy R-245fa cycles. As PFAS limits extend, early movers that certify seals and gaskets for CO₂ will gain procurement preference in regulated markets.

By Power Output Range: Sub-1 MW units dominate, micro scale outpaces

Units rated 100 kW-1 MW held 48.5% of the Organic Rankine Cycle market size in 2024, largely because this bracket aligns with clinker-cooler and glass-furnace waste-heat streams. However, micro-ORC packages below 100 kW are expanding at an 11.7% CAGR as co-location with edge data rooms and telecom hubs becomes mainstream.(4)Source: Infinity Turbine, “ORC and Supercritical CO2,” infinityturbine.com Modular water-cooled condensers integrate with existing HVAC, slashing incremental site works.

Conversely, machines with a capacity of 1-5 MW serve municipal biomass and district-heating loops, while those with a capacity greater than 5 MW are typically found in flash-to-binary geothermal retrofits. As capital markets favor smaller ticket sizes with quick revenue starts, sub-MW growth is expected to contribute to overall shipment volumes, even if megawatt-scale projects retain a larger share of aggregate megawatts.

By Application: Waste-heat recovery at core, marine retrofits surge

Waste-heat capture accounted for 46.5% of 2024 revenue, reflecting clear energy-savings paybacks across both ferrous and non-ferrous smelters. The marine category is forecast to log a 13.3% CAGR to 2030 as LNG carriers adopt cryogenic CO₂ Capture skids paired with ORC bottoming cycles, which remove 90% of stack emissions.(5)Source: MDPI, “Decarbonization and Energy Efficiency of FSRU,” mdpi.com Geothermal additions continue steady growth, while biomass projects benefit from feed-in tariffs in Europe and Japan.

Solar-thermal hybrids emerge where high-flux troughs or Fresnel reflectors can raise ORC inlet temperatures during peak insolation, thereby boosting capacity factors without the need for costly battery storage. District-heating operators in Sweden and the Netherlands retrofit Organic Rankine Cycle market units to supply low-carbon power and thermal energy through the same heat-exchanger network, exemplifying multi-vector value.

By End-user Industry: Industrial plants lead, data centers fastest

Industrial process owners contributed 53.2% of 2024 shipments, leveraging ORC loops to turn furnace exhaust into electricity and chilled water. Data-center builders rank as the fastest riser, with a 15.6% CAGR, driven by AI-server heat densities that exceed 1,500 W per rack unit. Pilot sites in Italy now dispatch heat equal to 3,300 t CO₂ saving per year to district networks, illustrating cross-sector co-benefits.(6)Source: Retelit, “Avalon 3 Heat Recovery Project,” retelit.it

Utility companies maintain geothermal and biomass portfolios, while oil and gas operators deploy trailer-mounted packages on compressor-station exhaust. Maritime engine builders design embed-ready interfaces, indicating that shipyards will specify ORC compatibility upfront rather than as a later retrofit. The broadening customer base underscores the versatility of the Organic Rankine Cycle market across traditional and digital infrastructures.

Geography Analysis

North America accounted for 42.9% of 2024 revenue, primarily driven by federal tax incentives that treat ORC plants as zero-emission generators. (7)Source: Bureau of Energy Efficiency, “Renewable Consumption Obligations,” beeindia.gov.in State-level clean-heat standards further reward installations at cement and glass facilities, and geothermal approvals in Utah and Nevada proceed under streamlined permits. Nevertheless, domestic component tariffs can elongate paybacks for large steel-sourced turbine housings.

Europe follows with a robust uptake driven by the EUR 1 billion Industrial Decarbonization Bank pilot and the Net-Zero Industry Act's manufacturing targets. F-gas restrictions accelerate fluid substitutions, shifting procurement toward propane and super-critical CO₂. Nordic data-center clusters utilize district-heating grids for surplus heat sales, thereby deepening the penetration of Organic Rankine Cycle market equipment in both power and thermal applications.

The Asia-Pacific region shows the strongest outlook with a 13.9% CAGR. India's Renewable Consumption Obligations, which stipulate 29.91% non-fossil power for 2024-25, steer sugar mills and textile plants to adopt sub-5 MW ORC blocks. The Philippines and Indonesia continue to expand their geothermal build-outs, standardizing binary modules. Kenya's Menengai project exemplifies African progress and signals to investors that multilateral finance is available for similar prospects in the Rift Valley. This region presents the largest future addressable Organic Rankine Cycle market with high process-heat intensity in chemicals and metals.

Competitive Landscape

The Organic Rankine Cycle market remains moderately consolidated. Turboden, Ormat, and Exergy combine captive turbine manufacturing with long-term service contracts, giving them lifecycle-cost advantages. Ormat booked USD 829 million in revenue for 2023 and plans to increase installed capacity to 2.3 GW by 2026 through geothermal and waste-heat projects. Turboden collaborates with Fervo Energy on advanced geothermal loops, expanding reach into closed-loop reservoirs. Exergy advances radial-outflow turbine geometry to raise isentropic efficiency by up to 5 percentage points in low-pressure applications.

Emerging vendors like Infinity Turbine focus on super-critical CO₂ micro units for data-center and desalination niches. Major OEMs, such as GE Vernova and Siemens Energy, license expander technology but often partner with specialist integrators for the balance-of-plant scope. Competitive differentiation is increasingly driven by working-fluid compliance, modularity, and digital performance monitoring, ensuring 98% uptime or higher.

Strategic alliances proliferate: Rolls-Royce and ASCO unite their carbon-capture expertise with ORC power blocks for on-site valorization of recovered CO₂. Ansaldo Energia positions its AE-T100 microturbine family as a drop-in replacement for aging CHP units, bundling 10-year O&M. As policy visibility improves, financiers grow comfortable underwriting merchant-revenue models, reinforcing the trajectory toward a stable yet innovation-rich Organic Rankine Cycle industry.

Organic Rankine Cycle Industry Leaders

Turboden S.p.A.

Ormat Technologies Inc.

Exergy S.p.A.

Kaishan Compressor Co. Ltd.

ElectraTherm Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: European Commission allocated EUR 1 billion to the Industrial Decarbonization Bank pilot, funding high-temperature waste-heat and thermal-storage projects that favor ORC integration.

- June 2025: Canada enacted Clean Economy Investment Tax Credits covering 30% of qualified ORC equipment cost, with enhanced rates for projects meeting prevailing-wage provisions.

- May 2025: Ormat Technologies reported a record USD 150.3 million adjusted EBITDA for Q1 2025 and acquired the 20 MW Blue Mountain geothermal plant for USD 88 million to expand its binary portfolio.

- February 2025: U.S. Treasury finalized rules for technology-neutral clean-electricity production credits, offering stable pathways for ORC plants placed in service after 2025.

Global Organic Rankine Cycle Market Report Scope

| Direct ORC Systems |

| Indirect ORC Systems |

| Cascaded ORC Systems |

| Hydrocarbons (Pentane, Butane) |

| Siloxanes (D4, D5) |

| Refrigerants (R245fa, R1233zd-E) |

| Super-critical CO2 |

| Aromatics (Toluene, Benzene) |

| Micro ORC (Below 100 kW) |

| Small-scale (100 kW to 1 MW) |

| Medium-scale (1 to 5 MW) |

| Large-scale (Above 5 MW) |

| Waste Heat Recovery |

| Geothermal Power |

| Biomass Power Generation |

| Solar Thermal |

| Marine and Transport |

| District Heating |

| Industrial (Cement, Steel, Glass, Chemicals) |

| Power Generation Utilities |

| Oil and Gas (Up/Mid-stream) |

| Commercial and District Energy |

| Maritime |

| Data Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Direct ORC Systems | |

| Indirect ORC Systems | ||

| Cascaded ORC Systems | ||

| By Working Fluid | Hydrocarbons (Pentane, Butane) | |

| Siloxanes (D4, D5) | ||

| Refrigerants (R245fa, R1233zd-E) | ||

| Super-critical CO2 | ||

| Aromatics (Toluene, Benzene) | ||

| By Power Output Range | Micro ORC (Below 100 kW) | |

| Small-scale (100 kW to 1 MW) | ||

| Medium-scale (1 to 5 MW) | ||

| Large-scale (Above 5 MW) | ||

| By Application | Waste Heat Recovery | |

| Geothermal Power | ||

| Biomass Power Generation | ||

| Solar Thermal | ||

| Marine and Transport | ||

| District Heating | ||

| By End-user Industry | Industrial (Cement, Steel, Glass, Chemicals) | |

| Power Generation Utilities | ||

| Oil and Gas (Up/Mid-stream) | ||

| Commercial and District Energy | ||

| Maritime | ||

| Data Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Organic Rankine Cycle market be by 2030?

Forecast value stands at USD 1,591.32 million in 2030, reflecting a 9.15% CAGR from 2025-2030.

Which ORC system type is growing fastest?

Cascaded configurations are projected to advance at a 14.4% CAGR, outpacing direct and indirect designs.

Why are data-center operators adopting ORC units?

They convert server waste heat into electricity and district-heating output, improving energy efficiency while cutting CO₂ emissions.

Which region shows the strongest growth outlook?

Asia-Pacific is expected to register a 13.9% CAGR, buoyed by geothermal build-outs and renewable consumption mandates.

What is the main barrier to wider ORC deployment?

Higher upfront capital costs compared with steam Rankine cycles, especially in price-sensitive markets, remain the key hurdle.

Which working fluid is gaining preference under new refrigerant rules?

Super-critical CO₂ is attracting interest due to zero global-warming potential and compact turbine size.

Page last updated on: