Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 23.16 Billion |

| Market Size (2031) | USD 30.02 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turbine Control System Market Analysis by Mordor Intelligence

The Turbine Control System Market size was valued at USD 21.98 billion in 2025 and estimated to grow from USD 23.16 billion in 2026 to reach USD 30.02 billion by 2031, at a CAGR of 5.36% during the forecast period (2026-2031).

Aging thermal fleets, the need to integrate variable renewable generation, and the electricity-hungry rise of AI data centers are the headline forces underpinning this steady expansion. Utilities have accelerated control-system retrofits to transform 1990-era plants into agile assets able to switch from baseload to cycling duty in minutes. Developers of offshore wind farms are simultaneously demanding adaptive pitch-and-yaw algorithms that preserve blade integrity despite constantly shifting sea states. Meanwhile, data-center operators favor aeroderivative gas turbines that can start, ramp, and stop more than ten times per day without breaching strict NOx limits. Together, these trends foster an environment in which advanced controllers, field devices, and software analytics are viewed less as discrete products and more as a tightly woven orchestration layer that keeps diverse turbine fleets safe, efficient, and cyber-secure.

Key Report Takeaways

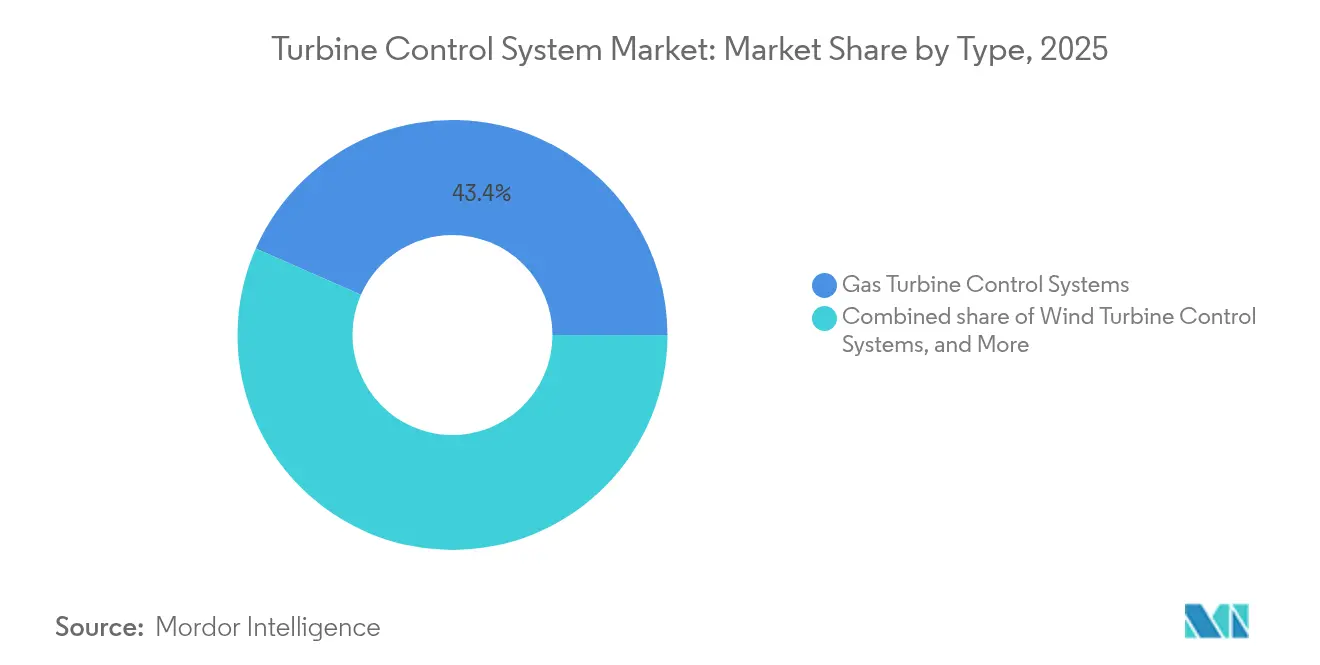

- By type, gas turbine systems held 43.40% of the turbine control systems market share in 2025, while wind turbine solutions are projected to lead growth at a 7.16% CAGR through 2031.

- By function, speed-control platforms accounted for 31.95% of the turbine control systems market size in 2025; vibration and emissions solutions are set to expand at a 6.05% CAGR to 2031.

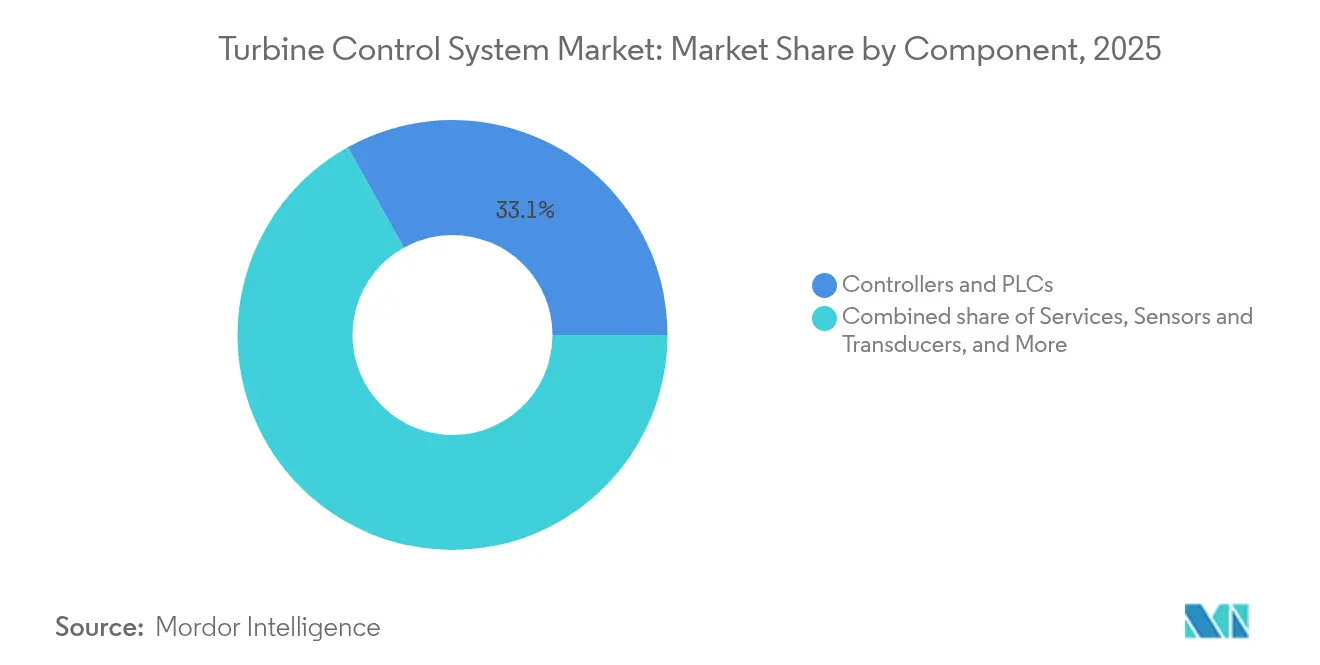

- By component, controllers and PLCs dominated the market with a 33.10% revenue share in 2025, whereas services are poised to record the fastest growth of 6.78% CAGR through 2031.

- By end-user, power-generation utilities commanded 46.40% share of the turbine control systems market size in 2025, while independent service providers are forecast to rise at a 6.45% CAGR.

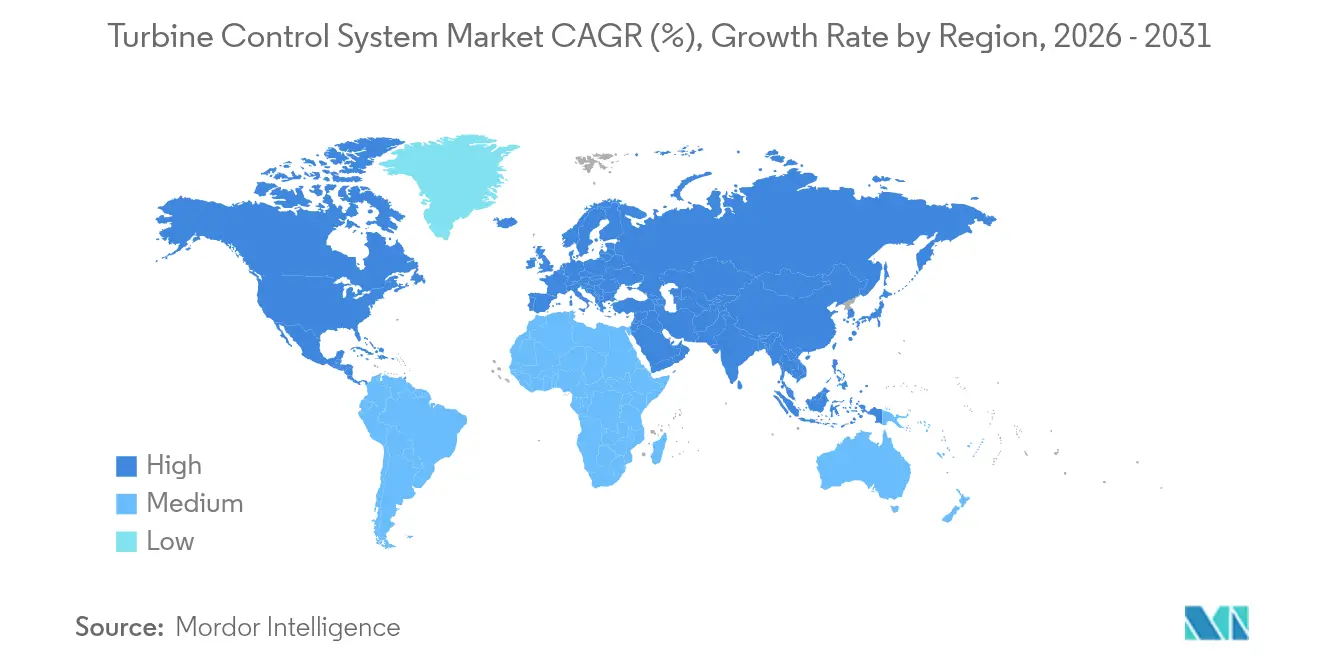

- By geography, the Asia-Pacific region controlled 38.05% of the turbine control systems market share in 2025 and is projected to advance at a 5.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Turbine Control System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Modernization of aging thermal fleets | +1.2% | North America, Europe, Global | Medium term (2-4 years) |

| Expansion of wind capacity | +0.8% | APAC, Europe, Global | Long term (≥ 4 years) |

| Reliability push in global gas-turbine fleet | +0.7% | North America, Middle East, Global | Short term (≤ 2 years) |

| AI data-center peak-demand surges | +0.9% | North America, APAC, Europe | Short term (≤ 2 years) |

| Digital-twin-enabled predictive maintenance | +0.6% | Developed markets, Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Wind Capacity Requiring Advanced Pitch & Yaw Controls

Modern 15-MW offshore turbines operate with rotor diameters exceeding 240 m, magnifying aerodynamic loads and structural fatigue. Their control software, therefore, blends pitch, yaw, and torque commands in 20-millisecond cycles to balance power extraction against blade strain. Grid codes in Europe and China add another layer by compelling wind farms to contribute frequency support, forcing controllers to momentarily reduce active power to emulate spinning inertia(1)Institution of Engineering and Technology, “Coordinated Frequency Regulation by DFIG Wind Power Plants,” theiet.org . Floating installations raise the bar again, as the nacelle must coordinate with mooring-line dynamics in real-time. Suppliers armed with high-fidelity aeroelastic models and edge-computing processors are capturing share in this fast-growing slice of the turbine control systems market.

Reliability Push in Global Gas-Turbine Fleet

As combined-cycle blocks transition from baseload to peaker duty, hot-section parts experience increased temperature cycling and potential flame instability. Mitsubishi Heavy Industries’ A-CPFM platform integrates machine learning into the combustion loop, enabling the controller to fine-tune fuel splits and eliminate vibration-driven trips —a feature now validated at the 600 MW Jackson facility in Mississippi(2)Mitsubishi Heavy Industries, “Best Innovation 2024 Awards,” mhi.com . Hydrogen blending introduces further complexity because the flame speed and calorific value differ from those of pure methane; therefore, control logic must track these variables to prevent auto-ignition events. Plant owners, especially in the Middle East, where water desalination relies on cogeneration units, are prioritizing software retrofits that ensure greater than 99% availability.

AI Data-Center Peak-Demand Surges Driving Fast-Ramp Controls

Hyperscale campuses built to train large language models have energy-use profiles that swing by hundreds of megawatts in a single hour. GE Vernova’s LM2500XPRESS package responds with full speed, no-load in under 5 minutes, and achieves rated power in less than 10 minutes, while maintaining emission levels far below those of legacy diesel backups(3)GE Vernova, “Rack ’Em Up,” gevernova.com . Control firmware orchestrates fuel delivery, variable bleed valves, and starter-motor cut-over, allowing the turbine to synchronize with the grid without thermal shock. Several US utilities have negotiated power-purchase agreements that allow these units to export surplus electricity during valley periods, turning data-center turbines into grid-support assets and further stimulating the turbine control systems market.

Digital-Twin-Enabled Predictive Maintenance

Digital twins ingest SCADA feeds, historical trip data, and physics-based models to calculate real-time health indices for bearings, blades, and combustion liners. GE’s steam-turbine twin detected a 0.02 mm bearing deviation three weeks before vibration levels crossed alarm thresholds, enabling a planned 12-hour outage instead of a forced multi-day shutdown(4)GE, “The Catch,” ge.com . Wind-farm owners overlay similar twin outputs with lidar data to forecast blade-root bending loads, thereby extending inspection intervals. The insight that a USD 200,000 software subscription can avert a USD 1 million lost-generation event is driving a 7.0% services CAGR within the turbine control systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining fossil CAPEX as renewables scale | -0.9% | Global, with Europe and North America leading transition | Long term (≥ 4 years) |

| Cyber-security & integration complexity in brown-field retrofits | -0.5% | Global, with developed markets most affected | Medium term (2-4 years) |

| Stricter grid-code inertia limits constraining ramp algorithms | -0.4% | Europe and North America, with APAC adoption following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Fossil CAPEX as Renewables Scale

European utilities such as Vattenfall have sold or mothballed coal and gas assets to unlock capital for offshore wind and battery projects. These divestments lower the addressable base for new turbine control installations. Remaining fossil operators funnel budgets into only the most necessary upgrades—chiefly emissions-compliance and flexible-operation retrofits—rather than full control-room overhauls. The net effect is a shift from green-field hardware awards to brown-field optimization contracts, which tempers overall revenue expansion even as it boosts demand for software licensing and field-service expertise within the turbine control systems industry.

Cyber-Security & Integration Complexity in Brown-Field Retrofits

North American utilities governed by NERC CIP standards must isolate operational-technology networks from corporate domains. On a 1995-era steam plant, this can require installing new fiber rings, firewalls, and intrusion-detection appliances before a modern controller is even powered up. Firms specializing in industrial-control security estimate that cyber-hardening can increase a straightforward retrofit’s capital cost by 50% and add six months to the schedule(5)Industrial Defender, “AI Race Brings Energy Reliability Back into Spotlight,” industrialdefender.com . For cash-constrained plant owners, these hurdles sometimes defer or downscale projects, restraining the near-term momentum of the turbine control systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Gas Dominance Amid Wind Acceleration

Gas platforms supplied 43.40% of the turbine control systems market in 2025, a lead built on their dual role as baseload anchors and rapid-response units when renewable output sags. Machine-learning-infused combustion control now trims start-up fuel consumption by up to 10%, a saving eagerly adopted by merchant-plant operators exposed to volatile spot prices. Conversely, wind solutions are projected to climb a 7.16% CAGR slope between 2026 and 2031, driven by 20 GW per year of global offshore additions that require multi-axis control to handle wake interactions and grid-support duties. The steam and hydro categories, while mature, continue to experience moderate spending, particularly where pumped-storage hydropower is repurposed for long-duration energy storage.

A second factor sustaining gas leadership is hydrogen readiness. OEMs are shipping software updates that adjust firing-temperature maps and diluent-flow curves if blend ratios exceed 30%. Owners of GE 7F and Siemens SGT-800 fleets are therefore opting for incremental control-platform upgrades rather than full hardware swaps. Wind, by contrast, is embracing distributed-edge processors mounted directly in the nacelle so that feedback loops stay below 5 ms despite limited offshore bandwidth. Those architecture shifts are drawing IT-oriented entrants into the turbine control systems market.

By Function: Speed-Control Leadership with Emerging Functions Growth

Speed control represented 31.95% of 2025 revenues, reflecting its universality across steam, gas, hydro, and wind machines. Even so, auxiliary packages such as vibration suppression, combustion emissions, and cyber-intrusion monitoring will together post a 6.05% CAGR. Emissions modules are trending from simple lookup tables toward adaptive neural-network regulators that balance NOx targets, ramp rates, and fuel blends in real-time. Pressure-control logic, critical in once-through steam generators, is also being upgraded, with new algorithms coordinating variable-speed feed-water pumps to dampen drum-level oscillations. Across all functions, the guiding pattern is convergence: a single high-availability PLC now hosts multiple advanced applications that once required separate controllers, streamlining footprint and maintenance.

The turbine control systems market size attributed to these emerging functions is poised to surpass USD 6.18 billion by 2031 as grid-code revisions tighten inertia, frequency-ride-through, and black-start requirements. For fleet managers, bundling advanced functions into a single license simplifies compliance audits, thereby further boosting adoption.

By Component: Controllers Dominance with Services Acceleration

Controllers and PLCs accounted for 33.10% of the turbine control systems market size in 2025, as every architecture—whether legacy or new—still relies on a deterministic execution engine. The narrative, however, is shifting toward lifecycle economics. Services tied to installation, application engineering, and cybersecurity patching will expand at a 6.78% CAGR through 2031, outpacing hardware growth. Vendors such as Woodward embed security certificates at the chip level, then sell annual maintenance contracts that push firmware updates whenever vulnerability databases flag new exploits. Sensors and transducers, though less glamorous, also evolve; eddy-current probes are giving way to fiber-optic strain gauges that survive higher temperatures at hydrogen-fired turbines. HMI and SCADA suites are transitioning to HTML5 thin-client interfaces, allowing for cloud-hosted historian analytics without compromising response times.

In aggregate, these developments reflect an irreversible shift: customers no longer ask for a “panel of controllers” but for an integrated performance-management stack that spans from field devices to the enterprise cloud. Component makers must therefore broaden their portfolios or risk being relegated to commodity status within the turbine control systems industry.

By End-user Industry: Utilities Leadership with Service Provider Growth

Utilities owned 46.40% of the installed turbine control value in 2025, owing to their stewardship of most large thermal and renewable fleets. Yet those same utilities increasingly outsource complex failure analysis and cyberwatch functions to independent service providers (ISPs) that can mobilize multidisciplinary task forces. ISPs are thus projected to notch a 6.45% CAGR through 2031. Oil-and-gas players remain important as they deploy gas turbines for LNG compression, but CAPEX cycles there hinge heavily on global commodity prices. Process industries utilize medium-pressure steam turbines for cogeneration; their control needs center on precise steam quality management that balances process heat with power sale opportunities.

Marine and aviation users represent a niche but technologically demanding customer base. Rolls-Royce’s MT30 gas turbines must change load at up to 10 MW/min while keeping shaft speed within ±0.1%; accordingly, the embedded control logic weighs mere kilograms yet equals land-based counterparts in functional breadth. Lessons learned at sea then migrate back into land-based designs, underscoring cross-sector innovation loops that invigorate the turbine control systems market.

Geography Analysis

The Asia-Pacific region commanded 38.05% of 2025 revenue and is projected to expand at a 5.78% annual rate through 2031. Chinese offshore wind auctions now stipulate grid-forming capability, prompting developers to specify multi-function controllers right at the bidding stage. India’s renovation and modernization program for ~44 GW of subcritical coal units also generates new orders for the turbine control systems market. Southeast Asian countries, particularly Thailand, following its 5,300 MW Bang Pakong CCGT milestone, procure high-efficiency J-class gas turbines whose control suites synchronize eight units across a single 500 kV bus.

North America remains the second-largest region, buoyed by data-center clustering in Texas, Virginia, and Alberta. Local utilities collaborate with turbine OEMs to co-develop “black-park” modes so that aeroderivative units can island sensitive IT loads during grid faults, a capability that commands sizeable service premiums in the turbine control systems industry. Environmental agencies’ emphasis on the methane-to-hydrogen transition further accelerates control-software spending, as existing turbines must receive logic capable of handling variable Wobbe-index fuels.

Europe places a strong emphasis on flexible operations and cyber-resilience. Germany’s grid operator now rewards fast frequency response of less than 2 seconds, encouraging retrofitted steam units to implement over-fire logic plus advanced governor-valve sequencing. Simultaneously, the EU NIS2 regulation adds legal teeth to cybersecurity obligations, prompting plant owners to adopt monitored firewalls and anomaly-detection analytics. These factors sustain software and services revenue even though green-field fossil builds are rare.

In the Middle East and Africa, combined-cycle and mechanical-drive projects for desalination and midstream gas continue to be active. High ambient temperatures and dust necessitate control algorithms that anticipate compressor surge margins and automate inlet-bleed cooling sequences to prevent compressor surge. South American growth centers on Brazil’s pumped-storage assets, which now engage four-quadrant turbines that alternate between generation and motoring, requiring sophisticated transitions that only the latest controllers can coordinate.

Regulatory Landscape

Compliance requirements for turbine control systems increasingly combine turbine-specific performance standards with mandatory cyber and grid-reliability rules. In hydropower, the International Electrotechnical Commission (IEC) updated key references in September 2024 with IEC 60308:2024 (testing of hydraulic turbine governing systems) and IEC 61362:2024 (guidelines for specification of hydraulic turbine governing systems), which feed into procurement specifications for governors, sensors, and acceptance testing.

In North America, cybersecurity requirements for bulk electric system assets remain a direct buying driver for control and SCADA upgrades. NERC Critical Infrastructure Protection (CIP) standards advanced further in 2026, with CIP-003-9 becoming effective in April 2026 and CIP-012-2 becoming effective in July 2026. FERC approval of CIP-008-7.1 in March 2026 reinforced incident reporting and response expectations for cyber assets connected to generation and control centers. These rules expand retrofit scope beyond controllers, increasing the need for segmentation, access controls, and auditable configuration management across turbine control environments.

Competitive Landscape

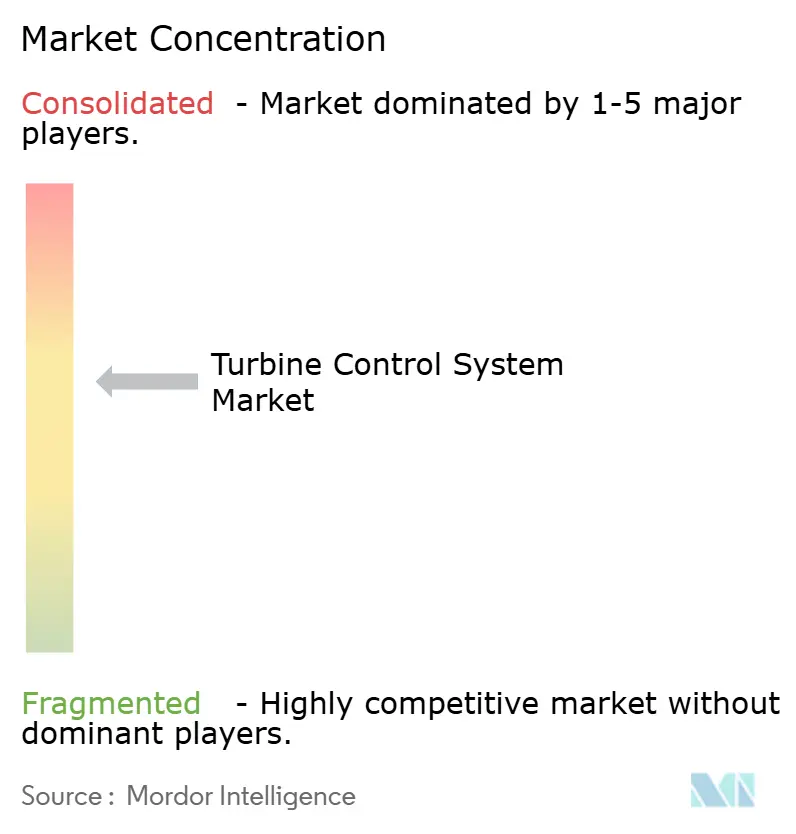

The industry structure exhibits moderate concentration, with the top five vendors capturing just over 60% of 2024 sales, leaving ample room for niche software and cybersecurity players. ABB’s buyout of Siemens Gamesa’s power-electronics arm expanded its renewables control suite, giving it a turnkey path from generator converter through SCADA cloud. GE Vernova leverages a 10,000-unit installed base to upsell digital-twin subscriptions, claiming that users achieve a 2% fuel savings within six months. Siemens Energy pairs its T3000 controller with modular edge devices, allowing customers to add hydrogen-blend logic without replacing the rack. Emerson, for its part, integrates Ovation DCS with API-compliant safety-instrumented systems, targeting oil and gas operators who must meet dual mandates for process safety and cyber hardening.

Emergent competitors specialize in AI acceleration. Several start-ups ingest controller data into large transformer models to predict, within one-hour horizons, when gusts will hit an offshore array or when filter differential pressure will curb gas-turbine output. Users pilot these features in parallel with OEM twins, disaggregating vendor lock-in. Cyber-security firms also gain traction; Industrial Defender markets managed-detection services that overlay existing OT data without touching safety loops, easing compliance with NERC CIP v7.

Many equipment suppliers are thus repositioning themselves as solution integrators. Mitsubishi Heavy Industries banners its M-Edge platform, promising a cradle-to-grave package of controllers, twin units, and a maintenance workforce for JAC-class gas turbines. The differentiation pathway is increasingly running through software IP and service responsiveness, rather than metallurgical feats alone, sharpening competition while enlarging the overall turbine control systems market.

Turbine Control System Industry Leaders

ABB Ltd.

Emerson Electric Co

General Electric Company

Siemens Energy AG

Mitsubishi Heavy Industries

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Modernization programs are creating whitespace for software-defined upgrades that extend legacy turbines while meeting newer flexibility, emissions, and cybersecurity requirements. Modular control architectures that support incremental changes are drawing attention as many operators prioritize targeted retrofits, such as governor logic, vibration and emissions packages, and cybersecurity hardening, rather than full control-room replacement. Platform ecosystems such as GE Vernova Mark VIe and Siemens Energy Omnivise T3000 fit this shift by packaging unit control, plant-level integration, and digital enablement into deployments designed for brownfield constraints.

Fuel flexibility and cycling operation also point to opportunity areas where control IP, rather than hardware alone, drives supplier differentiation. ETN Global highlighted advanced turbine control systems in its March 2026 R&D Recommendation Report as a critical enabler for integrating hydrogen, methanol, and renewable fuels into power-generation fleets, reinforcing demand for automated tuning and combustion dynamics management. Siemens Energy filed a March 2026 patent describing objective-based turbine control that uses real-time dynamic models to balance load demands with component remaining useful life, aligning with customer emphasis on controllers that coordinate ramping, maintenance planning, and lifetime consumption in a single optimization loop.

Recent Industry Developments

- July 2026: Emerson released the Ovation Curation Tool, synchronization software for power and water control systems that manages version control and change history between production systems and digital twins. The release supports lifecycle services around turbine control environments where configuration drift and patch governance are major operational risks.

- December 2025: Mitsubishi Heavy Industries and Mitsubishi Electric completed functional testing of a jointly developed next-generation gas turbine control system aimed at thermal power plants, with commercialization targeted in fiscal year 2026. The milestone supports a refreshed control offering focused on higher flexibility and multi-fuel operation, a recurring requirement as gas fleets move toward cycling duty and hydrogen blending.

- October 2024: Mitsubishi Power completed Thailand's 5,300 MW Bang Pakong combined-cycle project with eight JAC gas turbines under unified digital control. The project showed how multi-unit coordination on shared electrical infrastructure raises the value of integrated turbine control suites for ramping, synchronization, and plant-wide optimization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the turbine control systems market is defined as revenues earned from hardware, software, and related services that monitor and control turbine operation, including speed, load, temperature, and pressure control, across major turbine applications.

Scope exclusions: the sizing excludes the turbine itself and major balance-of-plant equipment. It also excludes general plant automation that is not directly tied to turbine control and protection functions.

Segmentation Overview

- By Type

- Steam Turbine Control Systems

- Gas Turbine Control Systems

- Wind Turbine Control Systems

- Hydro Turbine Control Systems

- By Function

- Speed Control

- Load Control

- Temperature Control

- Pressure Control

- Other Functions

- By Component

- Controllers and PLCs

- Sensors and Transducers

- HMI and SCADA Software

- Actuators and Valves

- Services (Installation, Retrofit, Cyber-security)

- By End-user

- Power Generation Utilities

- Oil and Gas (Upstream, Midstream, Downstream)

- Process Industries (Chemicals, Paper, Metals)

- Marine and Aviation

- Independent Service Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with mapping where turbine control demand comes from, then linking it to measurable activity such as new capacity additions and maintenance cycles. We relied on public energy and industry sources such as IEA electricity and power generation statistics, U.S. EIA capacity and generation data, Eurostat energy balances, World Bank macro indicators, and IRENA renewable and wind deployment releases to anchor the demand pool by region.

To convert that demand pool into an addressable control systems value, secondary reading was used to understand typical control architecture, replacement timing, and service intensity for gas, steam, and wind turbines. This included peer reviewed engineering journals, turbine safety and grid-code publications, patent databases for control and condition monitoring themes, company annual reports and investor decks, and trade association websites to understand the installed base context. Paid subscriptions that support company financials and intelligence, news and financials tracking, and patent databases were used selectively to fill gaps and cross-check trends. The desk sources listed here are illustrative only, and other public references were also used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on validating how control systems are bought and priced in real projects, and on confirming what share of spend sits in upgrades versus new installations. We spoke with OEM-side specialists, independent service providers, EPC and plant engineering teams, and utility and industrial operators across key regions. This clarified retrofit rates, service attachment, and the practical split between hardware and software spend.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 53% |

| Mid tier: 53% | Functional/Unit leaders: 37% | EMEA: 29% |

| Smaller Players: 18% | Managers: 51% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand reconstruction that starts from the operating and new-build turbine base, then applies penetration and spend factors for turbine-specific control and protection needs. For each major turbine type, we used indicators such as annual capacity additions, installed base by region, typical overhaul and retrofit cycles, service intensity for control upgrades, and the mix shift toward digital control, remote monitoring, and cybersecurity add-ons.

Those totals were checked with selective bottom-up approximations, where supplier revenue splits, sampled project pricing, and volume assumptions (for example, control cabinet and PLC counts per unit and typical service bundle rates) helped confirm that the market total was directionally consistent. Where bottom-up detail was missing in smaller geographies, gaps were handled by applying region-level ratios tied to installed base and commissioning activity, then reviewed again during primary validation.

For forecasting, scenario analysis was used alongside simple multivariate regression to connect demand to forward drivers such as power generation additions, gas turbine order activity, wind repowering cycles, and industrial production trends. Forecasts were then adjusted with expert feedback when policy or fuel-price shifts were expected to change project timing. We kept the model repeatable so inputs can be traced back to clear variables rather than one-off assumptions.

Data Validation & Update Cycle

Validation is done through multiple checks, where model outputs are compared with independent signals such as regional capacity build plans, turbine fleet age profiles, and service activity patterns reported by operators and service firms. Outliers are flagged, and the underlying drivers are re-reviewed, followed by a second pass that checks for unit consistency, currency timing, and double counting between software, hardware, and services.

Before sign-off, analysts re-contact sources when there is a large variance against observed installation or retrofit momentum in a region, or when a policy change is likely to move spending between years. Reports are refreshed annually, and interim updates are made when material events occur, such as major capacity program announcements or sharp changes in turbine ordering. Right before delivery, a final review pass is completed so clients receive the most current view available.

Mordor Intelligence's Turbine Control Systems Market Size Compared With Other Published Estimates

Published market values for turbine control systems can vary because each publisher draws the line differently around what gets counted. They also use different base years and handle currency timing differently. Even when the same end market is discussed, the split between new installations and retrofits, and how software and service revenues are treated, can change the final number.

In practice, the biggest gaps usually come from whether wind turbine controls are included alongside gas and steam, whether services like commissioning and ongoing upgrades are fully counted, and how fast average selling prices are assumed to move with digitalization and cybersecurity demand. A second driver is refresh cadence, where older estimates may not fully reflect the recent mix shift toward retrofit projects and life extension work, which can be uneven by region and by turbine age.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 23.16 B (2026) | |

| Global Consultancy A | USD 19.50 B (2024) | Uses an earlier base year and a shorter forecast window, and the definition tends to emphasize core turbine control hardware, which can understate service and upgrade revenues when retrofit activity is high. |

| Industry Publisher B | USD 18.70 B (2022) | Anchors the market to an older year and leans more toward power-plant applications, which can leave out parts of wind-related control spend and some recurring software and modernization bundles. |

The spread in figures mainly comes from year selection and what is counted beyond the control unit itself, especially services and modernization packages. By explicitly separating turbine-linked control and protection functions from wider plant automation, and then validating retrofit rates and service attachment through interviews, the sizing stays traceable to the demand pool and keeps category overlap lower. This approach is applied consistently by Mordor Intelligence.

Key Questions Answered in the Report

What is the current size of the turbine control systems market and how fast is it growing?

The market stands at USD 23.16 billion in 2026 and is projected to expand to USD 30.02 billion by 2031, reflecting a 5.36% CAGR.

Which turbine type contributes the highest revenue today?

Gas-turbine control systems lead with 43.40% market share because they serve both baseload and fast-ramping peaking roles.

Which geographic region is the largest and fastest-growing?

Asia-Pacific accounts for 38.05% of revenue in 2025 and is advancing at a 5.78% CAGR, driven by China’s offshore wind build-out and India’s thermal-plant retrofits.

What is the single biggest functional category within turbine control platforms?

Speed-control solutions hold 31.95% of 2025 revenue, reflecting their universal need across gas, steam, wind and hydro turbines.

How are digital twins influencing purchasing decisions?

Operators adopt digital-twin analytics to detect early faults, avoid unplanned outages and cut fuel use, which is fueling a 6.78% CAGR in services tied to turbine control systems.

Why are AI data centers important for future demand?

Hyperscale AI campuses require turbines that can start and ramp in minutes, prompting new orders for aeroderivative units equipped with advanced fast-response controls.

Page last updated on: