Heat Recovery Steam Generator Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 2.02 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

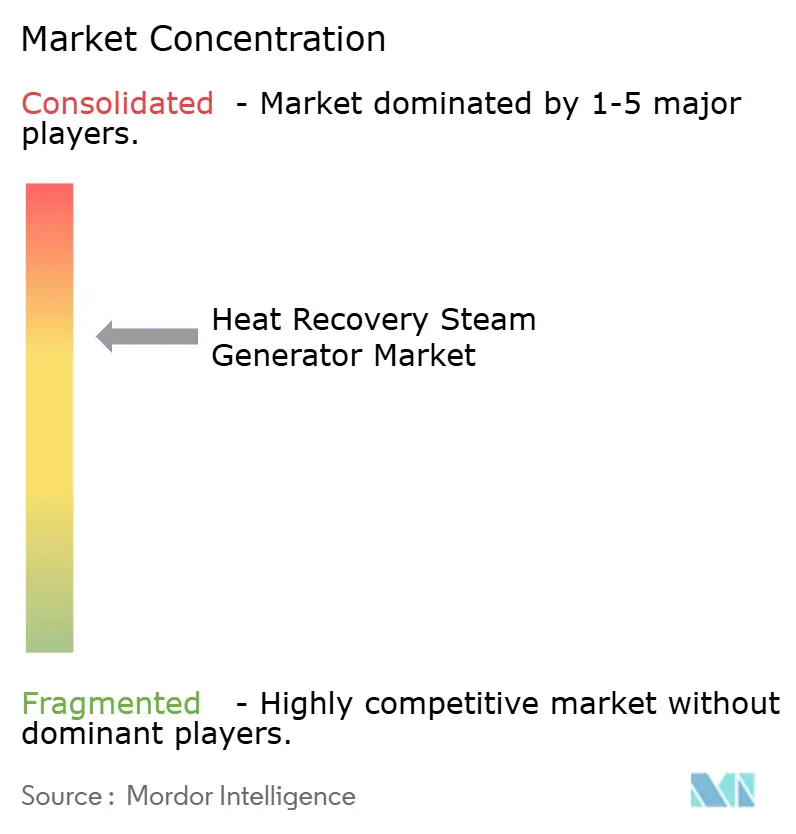

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heat Recovery Steam Generator Market Analysis by Mordor Intelligence

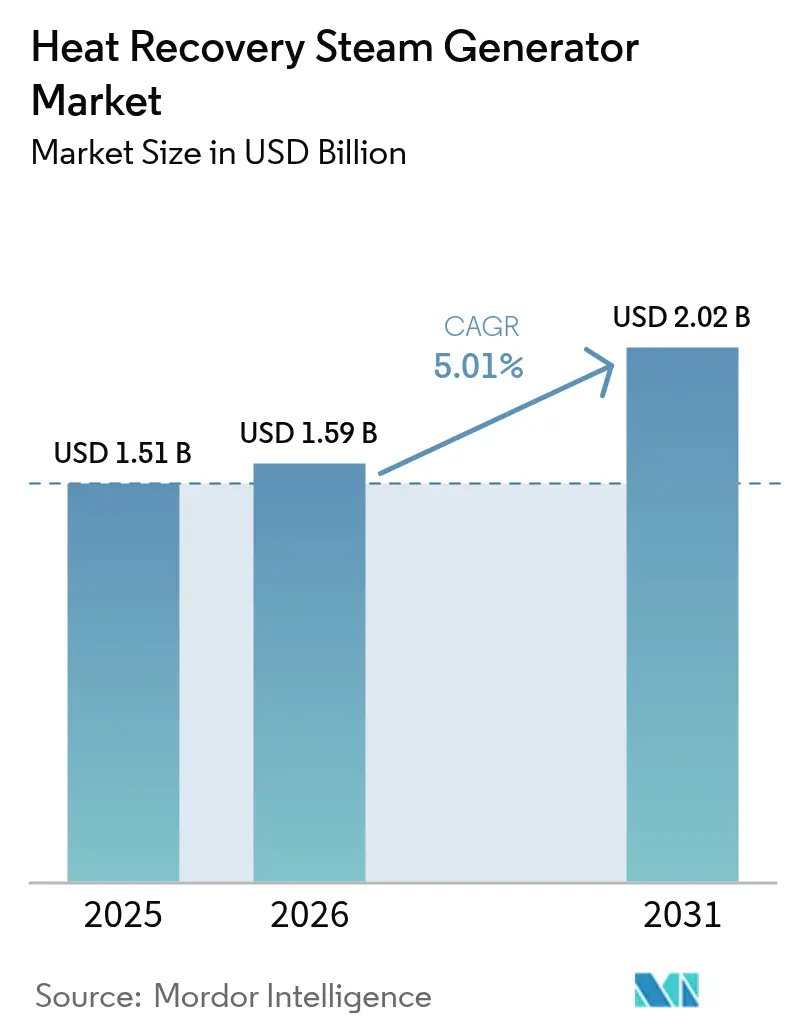

The Heat Recovery Steam Generator market size is expected to grow from USD 1.51 billion in 2025 to USD 1.59 billion in 2026 and is forecast to reach USD 2.02 billion by 2031 at 5.01% CAGR over 2026-2031.

Demand resilience is anchored in rising combined-cycle gas-turbine (CCGT) additions, stricter industrial emissions regulations, and the operational cost advantage of harvesting waste heat in power and process industries. Manufacturers are prioritizing flexible, hydrogen-ready designs that can cycle frequently without compromising reliability. Parallel investments in carbon-capture-ready CCGT plants widen the addressable base, while modular LNG, refining, and data-center micro-cogeneration projects create new pockets of opportunity. Supply-chain tightness around high-pressure drums, finned-tube modules, and skilled fabrication labor is lengthening delivery schedules, reinforcing the value proposition of vendors with integrated manufacturing footprints and long-term service programs.

Key Report Takeaways

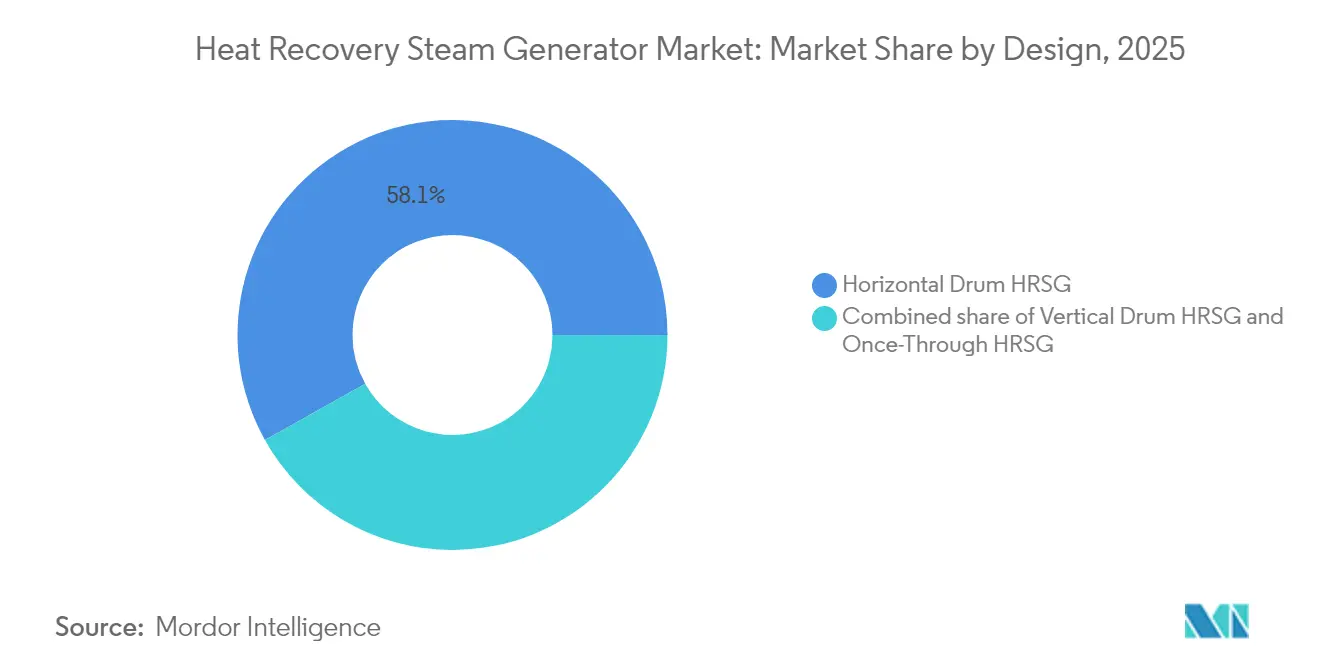

- By design, horizontal drum HRSGs commanded 58.12% share of the heat recovery steam generator market size in 2025, while once-through technology is forecast to accelerate at 6.46% CAGR through 2031.

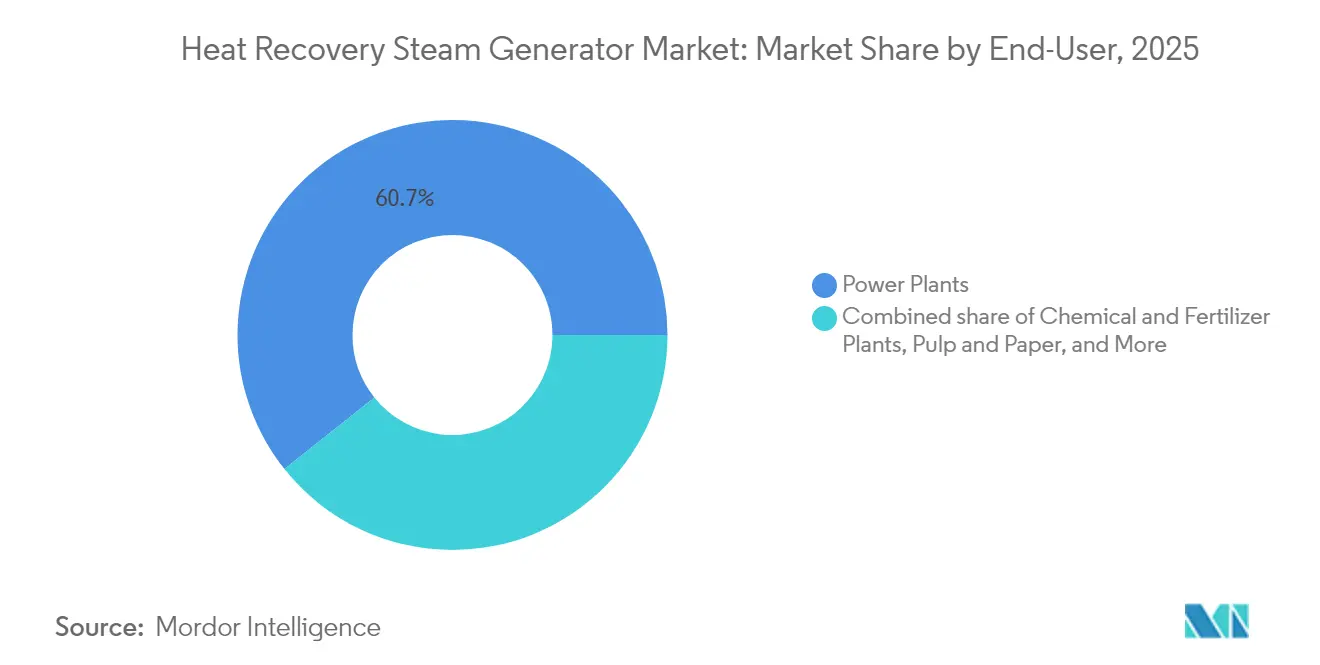

- By end user, power plants held 60.72% of the heat recovery steam generator market share in 2025, whereas chemical and fertilizer facilities are projected to register the highest CAGR of 6.12% from 2026 to 2031.

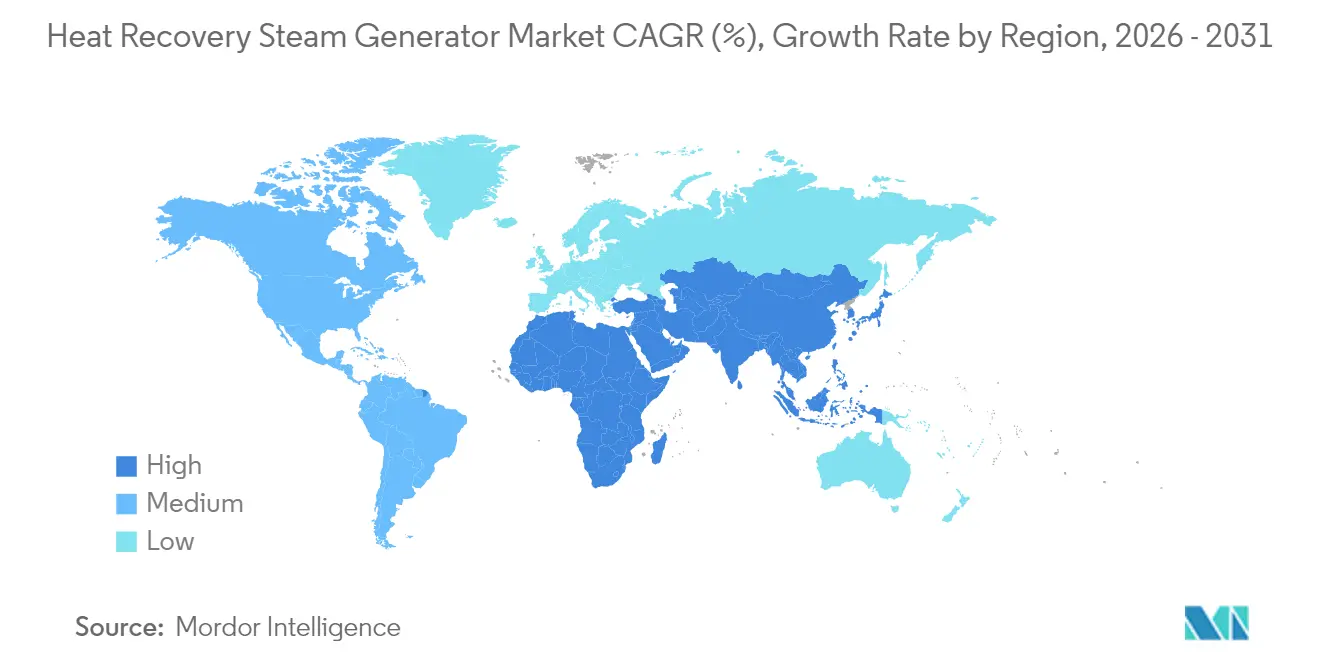

- By geography, the Asia-Pacific region led with a 42.55% revenue share in 2025; it is expected to outpace others at a 5.73% CAGR through 2031.

- GE Vernova, Siemens Energy, and Mitsubishi Power collectively accounted for over 45% of shipments in 2024, underscoring a moderately concentrated supplier landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Heat Recovery Steam Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of CCGT capacity pipeline | 1.20% | Global, with concentration in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Industrial emission-reduction mandates | 0.90% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Operational-cost pressure in O&G & chemicals | 0.70% | Global, particularly Middle East and North America | Short term (≤ 2 years) |

| CO₂-capture integration boosting low-pressure steam demand | 0.60% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Modular LNG plants adopting compact HRSGs | 0.40% | Global, with focus on Qatar, Australia, and US Gulf Coast | Medium term (2-4 years) |

| Data-center micro-cogeneration deployment | 0.30% | North America and Europe, early adoption in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of CCGT Capacity Pipeline

Global developers anticipate commissioning more than 18.7 GW of new combined-cycle capacity in the United States by 2028, with parallel multigigawatt programs also advancing in Saudi Arabia, Qatar, and China.[1]U.S. Energy Information Administration, “Annual Energy Outlook 2025,” eia.gov Project sponsors are specifying HRSGs that tolerate wider exhaust-gas temperatures from hydrogen-capable turbines and integrate exhaust-gas recirculation to cut carbon-capture costs by 6%.[2]GE Vernova, “Enhancing CCGT Efficiency with Exhaust Gas Recirculation,” gevernova.com As turbine backlogs extend to 2029, utilities are placing early equipment orders, shifting the competitive advantage toward vendors with captive module fabrication capabilities. The robust pipeline provides multi-year revenue visibility for the heat recovery steam generator market, although schedule risk remains tied to turbine availability and financing milestones. Design complexity is trending upward because owners demand rapid starts, part-load efficiency, and materials resilience under high-hydrogen combustion gases.

Industrial Emission-Reduction Mandates

The US Environmental Protection Agency now requires 90% CO₂ abatement for long-run coal and new baseload gas plants by 2032, prompting industrial campuses to retrofit or build cogeneration plants centered on HRSG technology.[3]United States Environmental Protection Agency, “New Source Performance Standards for Fossil-Fuel-Fired Power Plants,” epa.gov European chemical producers, exemplified by BASF’s 160 MW heat-pump-steam complex in Germany, illustrate how mandates convert environmental compliance into energy-efficiency investments. Facilities pursuing net-zero pathways incorporate triple-pressure HRSGs that feed both process steam and solvent-based capture units. Chemical and fertilizer operators seek configurations compatible with amine regeneration loads, enabling them to comply without jeopardizing throughput. Early movers who master permitting and technology integration benefit from lower lifetime compliance costs and potential carbon credit upside.

Operational-Cost Pressure in O&G & Chemicals

Volatile LNG price expectations near USD 13 per million British thermal units for 2025 squeeze margins for refineries and petrochemical plants.[4]Institute for Energy Economics and Financial Analysis, “Gas Price Volatility and LNG Affordability,” ieefa.org Installing turbine-HRSG cogeneration schemes yields fuel savings of USD 5 million per year for a 12 MWe module and achieves up to 100% energy efficiency improvements over fired boilers. Operators also monetize surplus electricity during market peaks, turning cost centers into revenue contributors. Flexibility remains critical; plant managers prefer once-through HRSGs that track variable steam loads without drum-level constraints. These economics underpin a sustained flow of retrofit awards, particularly in US Gulf Coast petrochemical corridors and Middle East refining hubs.

CO₂-Capture Integration Boosting Low-Pressure Steam Demand

Carbon-capture pilots that pair molten-carbonate fuel cells with HRSGs show 90% CO₂ removal while raising net plant output by 42% versus amine systems. Capture solvers demand stable low-pressure steam, a profile naturally provided by multi-pressure HRSGs, thereby displacing auxiliary boilers. Steam-methane reformer complexes utilizing sequential combustion and HRSG heat recovery can achieve a thermal efficiency of 38.9%, producing hydrogen and power within a shared capture scheme. Industrial clusters in Alberta and Rotterdam, which pool CO₂ pipelines, amplify economies of scale, reinforcing HRSG adoption curves through 2030. Vendors offering integrated capture-ready drums and space allowances command pricing premiums yet face minimal short-term competition due to engineering barriers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX & long pay-back vs alternatives | -0.80% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Gas-price volatility dampening CCGT FIDs | -0.60% | Global, with regional variations based on gas supply dynamics | Short term (≤ 2 years) |

| Materials corrosion under high-H₂ turbine exhaust | -0.40% | Global, affecting hydrogen-ready installations | Medium term (2-4 years) |

| Limited skilled HRSG fabrication capacity | -0.30% | Global, concentrated in manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX & Long Pay-Back vs Alternatives

The typical CCGT equipped with a triple-pressure HRSG costs USD 0.25 million per MW more than an open-cycle plant, extending payback periods to 8-12 years in low-capacity-factor grids. Developers in Southeast Asia and Africa face higher financing spreads, tilting procurement toward less efficient but cheaper OCGT sets. Growth in the heat recovery steam generator market, therefore, tends to favor jurisdictions that offer capacity payments or energy-efficiency incentives. Multilateral lenders attempt to bridge the gap with green-bond frameworks, yet disbursement timelines can delay order intake.

Gas-Price Volatility Dampening CCGT FIDs

Commodity swings triggered by geopolitical tensions push gas-forward curves into steep contango, unsettling revenue models for merchant CCGT assets. Lenders raise debt-service coverage ratios, and independent power producers defer final investment decisions, directly reducing near-term HRSG bookings. Integrated utilities with regulated cost recovery remain less exposed; however, even they are reevaluating project timings to align with contracted LNG supplies. Price volatility also clouds the competitiveness of gas-to-power in renewables-heavy grids, periodically shifting preference toward battery storage or demand-side management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Design: Once-Through Flexibility Gains Ground

Once-through HRSGs, although still a minority, are projected to grow at a 6.46% CAGR through 2031, while drum-type systems accounted for 58.12% of the 2025 revenue. Horizontal drum units retain dominance in base-load CCGT blocks because they provide consistent steam purity and proven durability. Vertical drums serve space-constrained retrofit sites, particularly inside refineries. The heat recovery steam generator market size for once-through units is projected to rise from USD 0.49 billion in 2026 to USD 0.67 billion by 2031, reinforcing supplier focus on quick-start architectures. Startup curves of under 30 minutes enable plant operators to chase peak pricing windows, whereas drum systems still average 60 to 90 minutes. Hydrogen-blend pilots indicate lower chloride-induced stress corrosion on once-through tube circuitry, positioning the design as a hedge against future fuel shifts. That said, water-quality demands remain stringent; owners are investing in condensate polishing skids to safeguard turbine blades.

Horizontal drum HRSGs will continue to dominate the larger slice of the heat recovery steam generator market, as mega-scale CCGT projects exceeding 800 MW tend to opt for familiar layouts and economies of scale. OEMs package triple-pressure with reheat trains to maximize combined-cycle output beyond 64% net efficiency, as validated by Thailand’s 5,300 MW M701JAC cluster. Enhancements, such as 3D-printed low-pressure economizer fins and advanced T91 steel headers, mitigate fatigue from cycling, thereby extending service intervals. Over the forecast horizon, incremental upgrades ask smart soot-blowing and infrared tube monitoring will prolong the competitive life of drum configurations, even as once-through units proliferate in mid-merit plants.

By End User: Chemicals Propel Incremental Demand

Power plants represented 60.72% of 2025 shipments, translating into a heat recovery steam generator market size of USD 0.92 billion. In contrast, chemicals and fertilizers posted the highest 6.12% CAGR, rising from USD 0.23 billion in 2026 to USD 0.31 billion in 2031. Chemical complexes pursue cogeneration revamps to offset gas cost spikes and comply with tightening carbon budgets. Ammonia producers retrofit single-pressure HRSGs on synthesis-gas turbines, shaving steam-reformer fuel by 12%. Refineries continue to anchor a stable demand base by replacing aging package boilers with turbine-HRSG trains that co-produce power and 55 bar steam. Data-center operators explore 5-10 MWe micro-cogeneration skids to cut scope-2 emissions while harvesting low-grade heat for absorption chillers.

Other industrial users, including those in the metals, pulp, and paper sectors, leverage HRSGs within biomass-hybrid systems to monetize process off-gases. Steelmakers in India integrate HRSGs with coke-oven gas turbines, achieving 25% internal power self-sufficiency. Food-grade CO₂ producers adopt HRSGs to supply reboiler duty for purification columns, capturing additional margin streams. Although power generation retains scale dominance, diversified industrial adoption underwrites a broader revenue plateau that protects suppliers from utility investment cyclicality.

Geography Analysis

Asia-Pacific continues to headline both market share and growth velocity. The region generated 42.55% of global 2025 revenue, and its 5.73% CAGR promises an incremental USD 0.22 billion by 2031, supported by multi-gigawatt CCGT expansions in China, India, Vietnam, and Thailand. China’s Huizhou hydrogen-ready CHP block exemplifies how developers future-proof assets for 50% H₂ firing, embedding once-through HRSGs with advanced fin-tube alloys. India’s national hydrogen mission is spurring the commissioning of cogeneration retrofits with dual-fuel turbines in Gujarat and Odisha. Japan’s fleet-renewal projects favor compact vertical-drum HRSGs for brownfield grid-balancing plants, aided by local content incentives.

North America leverages replacement cycles and emissions standards to sustain demand. The Environmental Protection Agency’s 90% CO₂ rule accelerates repowering of coal sites with CCGT-HRSG blocks that include spare pads for solvent regeneration exchangers. US Gulf Coast refineries embrace once-through HRSGs on aeroderivative turbines to hedge against LNG price volatility and carbon pricing proposals. Canada’s Alberta industrial carbon-capture hub contracts HRSG suppliers for waste-to-energy plants integrating post-combustion capture, expanding non-utility use cases.

Europe pursues decarbonization through high-efficiency, hydrogen-blend-capable HRSGs. Germany’s phase-out of unabated coal drives utilities to order triple-pressure, reheat systems with exhaust-gas recirculation for capture readiness. The Netherlands incentivizes combined heat-and-power upgrades in greenhouse horticulture, opening a niche segment for compact two-pressure HRSGs paired with small frame turbines. Supply-chain reliance on Asian pressure-part fabricators, however, exposes European projects to logistics delays, propelling interest in localized module assembly.

The Middle East records accelerating orders linked to Vision 2030 and industrial diversification. Saudi Arabia’s 7.2 GW CCGT pipeline specifies carbon-capture-ready HRSGs rated for 46 bar low-pressure steam to accommodate solvent regeneration, signaling design upgrades beyond conventional evaporator banks. Qatar’s North Field LNG expansion opts for compact HRSGs on aeroderivative turbines to maximize modular integration. United Arab Emirates utilities emphasize service contracts that guarantee 98% availability, funneling after-sales revenues to OEMs.

South America and Africa remain nascent but promising. Brazil tenders gas-fired thermal capacity to back solar and wind, including Bahia plants fitted with locally fabricated vertical-drum HRSGs to satisfy content rules. Nigeria and Mozambique evaluate small CCGT packages for industrial parks, but financing hurdles persist. Nonetheless, regional gas discoveries position both continents as long-term growth candidates once infrastructure matures.

Competitive Landscape

Market concentration is moderate. GE Vernova, Siemens Energy, and Mitsubishi Power combined accounted for more than 45% of 2024 shipments, leveraging complete turbine-to-stack portfolios and bundled long-term service agreements. These giants differentiate through digital performance suites, hydrogen-blend credentials, and experience integrating carbon-capture auxiliaries. GE Vernova’s USD 600 million US plant upgrade will increase heavy-duty turbine output to 70-80 units annually by 2026, strengthening its position in captive HRSG pairing. Siemens Energy bets on additive-manufactured burners and exclusive SMR steam turbine deals to widen the addressable markets beyond conventional thermal power.

Tier-two fabricators, such as BHI and Babcock & Wilcox, secure a share in regional turnkey contracts, especially where local content quotas are applied. BHI’s KRW 67 billion Fuji Electric partnership extends its presence in Japan, underpinning a backlog through 2031. Babcock & Wilcox’s 39% bookings rise in 2024 reflects diversified exposure across waste-to-energy and industrial decarbonization niches.

Supply scarcity in high-pressure finned-tube modules and a limited pool of ASME S-stamp workshops elevate barriers to entry. Some utilities now reserve fabrication slots years ahead, effectively locking out late entrants and encouraging vendor consolidation. Private-equity investors eye roll-up opportunities among specialized shops that build harps, transition ducts, and casing modules. Meanwhile, service revenues climb as operators sign performance-based contracts covering smart soot blowing, tube fouling analytics, and remote condition monitoring.

Strategic moves increasingly pivot on fuel flexibility. Vendors trial 100% hydrogen burners and ammonia-cracking inserts, anticipating post-2030 decarbonization mandates. Modular skid designs target LNG trains and data center cogeneration, where footprint and fast-track delivery outweigh the complexity of multiple pressures. Players able to bundle financing and lifecycle guarantees win bids in capital-constrained emerging markets, reinforcing the importance of downstream service ecosystems.

Heat Recovery Steam Generator Industry Leaders

General Electric (GE Vernova)

Siemens Energy AG

Mitsubishi Power

Thermax Ltd.

Nooter/Eriksen

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Duke Energy and GE Vernova agreed to procure up to 11 US-built 7HA turbines, underpinning GE Vernova’s USD 600 million domestic manufacturing expansion.

- April 2025: BHI secured a KRW 67 billion HRSG contract for Hokkaido Electric Power’s Ishikari Bay plant, extending delivery through Mar 2031.

- January 2025: GE Vernova 9HA turbines selected for YTL PowerSeraya’s 600 MW hydrogen-capable Singapore plant featuring triple-pressure reheat HRSG.

- October 2024: Mitsubishi Power completed a 5,300 MW natural-gas plant in Thailand with eight M701JAC units and HRSGs achieving 64% efficiency.

Global Heat Recovery Steam Generator Market Report Scope

The heat recovery steam generator market report includes:

| Horizontal Drum HRSG |

| Vertical Drum HRSG |

| Once-Through HRSG |

| Power Plants |

| Oil and Gas Facilities |

| Chemical and Fertilizer Plants |

| Metal and Mining |

| Pulp and Paper |

| Other Industrial Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Design | Horizontal Drum HRSG | |

| Vertical Drum HRSG | ||

| Once-Through HRSG | ||

| By End User | Power Plants | |

| Oil and Gas Facilities | ||

| Chemical and Fertilizer Plants | ||

| Metal and Mining | ||

| Pulp and Paper | ||

| Other Industrial Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the heat recovery steam generator market?

The market is valued at USD 1.59 billion in 2026 and is projected to reach USD 2.02 billion by 2031.

Which region dominates the heat recovery steam generator market?

Asia-Pacific leads with 42.55% revenue share in 2025 and also records the fastest 5.73% CAGR through 2031.

Which design type is growing fastest?

Once-through HRSG technology posts the highest 6.46% CAGR, driven by rapid-start capability and hydrogen-fuel readiness.

Why are chemical and fertilizer plants adopting HRSGs?

Stricter emission mandates and energy-cost pressures push these facilities to install HRSG-based cogeneration systems that cut fuel use and CO₂ output.

How does carbon-capture integration affect HRSG demand?

Capture processes require large volumes of low-pressure steam, making multi-pressure HRSGs the preferred source and expanding long-term demand.

Who are the major players in the heat recovery steam generator market?

GE Vernova, Siemens Energy, and Mitsubishi Power collectively hold over 45% of global shipments, supported by integrated turbine-to-stack offerings and long-term service agreements.

Page last updated on: