Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 40.46 Billion |

| Market Size (2031) | USD 54.14 Billion |

| Growth Rate (2026 - 2031) | 6.00% CAGR |

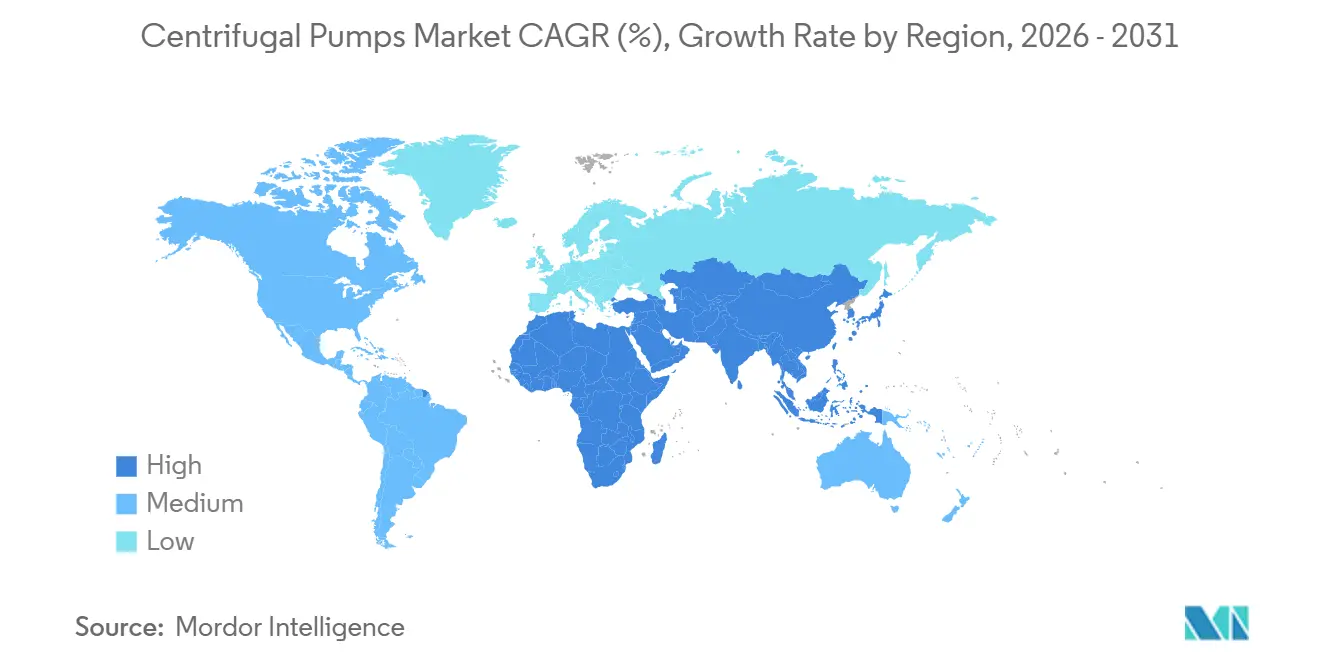

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

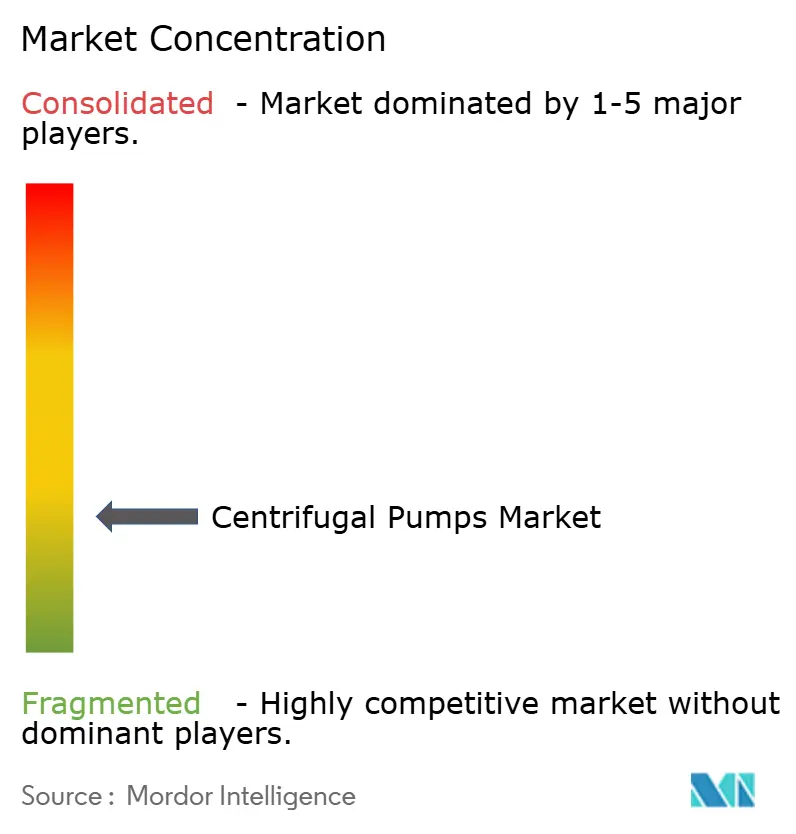

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Centrifugal Pumps Market Analysis by Mordor Intelligence

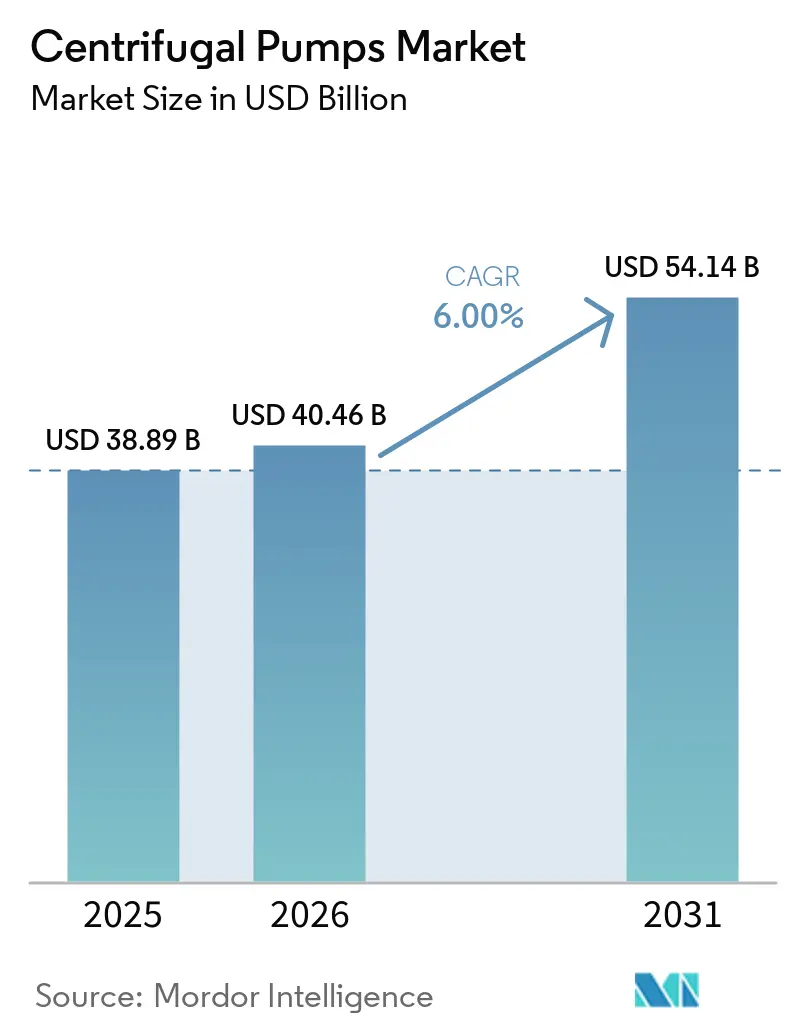

The Centrifugal Pumps Market size is projected to be USD 38.89 billion in 2025, USD 40.46 billion in 2026, and reach USD 54.14 billion by 2031, growing at a CAGR of 6% from 2026 to 2031.

Demand is shifting from routine replacements to compliance-driven upgrades as utilities, industrial processors, and infrastructure owners pursue energy-efficiency mandates, water-quality targets, and higher levels of automation. Single-stage units dominated revenue in 2025, yet multi-stage models are accelerating in desalination, boiler-feed, and reverse-osmosis installations that require pressures of 500–1,500 psi. Asia-Pacific remained the largest regional buyer in 2025, and fast-growing spending on municipal wastewater, irrigation modernization, and geothermal power keeps the region above the global growth trend. Competitive focus has moved to digital integration, with variable-frequency drives and condition-monitoring platforms cutting utility energy use by 25–30% and unplanned downtime by 15–20%.

Key Report Takeaways

- By stage, single-stage pumps captured 62.8% of the centrifugal pumps market share in 2025, while multi-stage products are forecast to expand at a 7.3% CAGR through 2031.

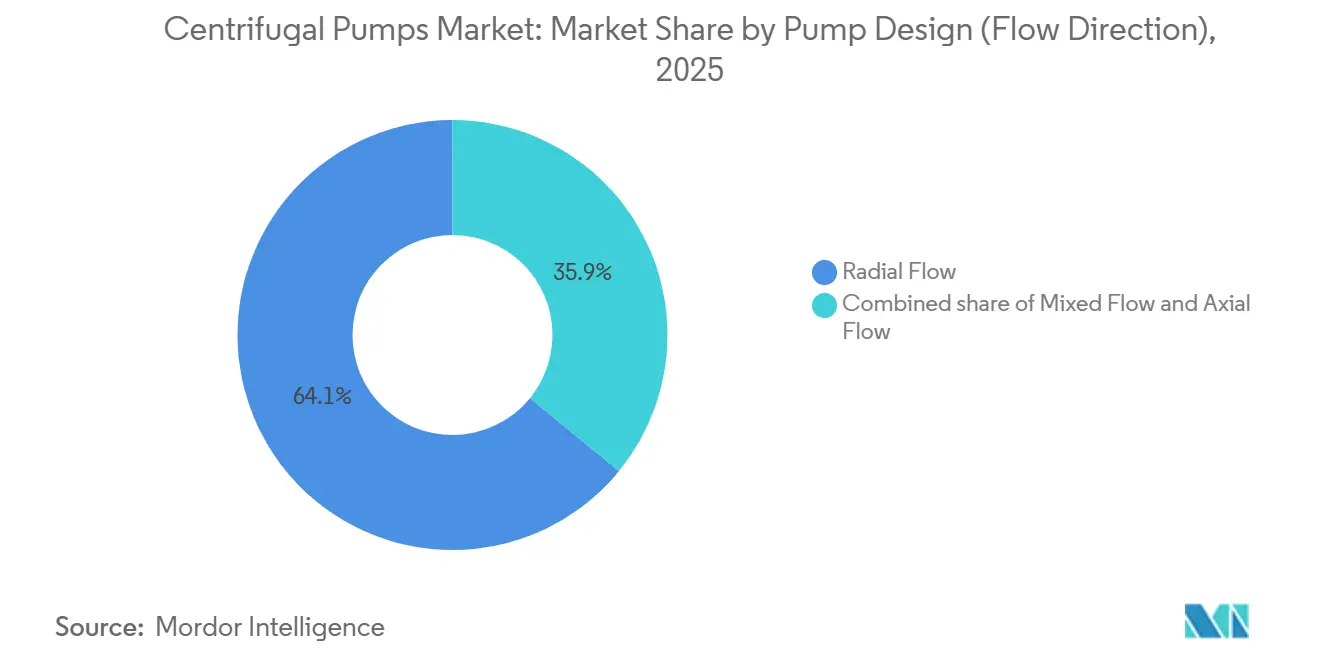

- By flow direction, radial-flow designs held 64.1% of 2025 revenue, but mixed-flow variants are growing at a 6.9% CAGR on flood-control and mining demand.

- By impeller type, enclosed designs accounted for 70.4% of shipments in 2025; semi-open impellers are advancing at a 7.0% CAGR because of slurry tolerance in mining and wastewater duties.

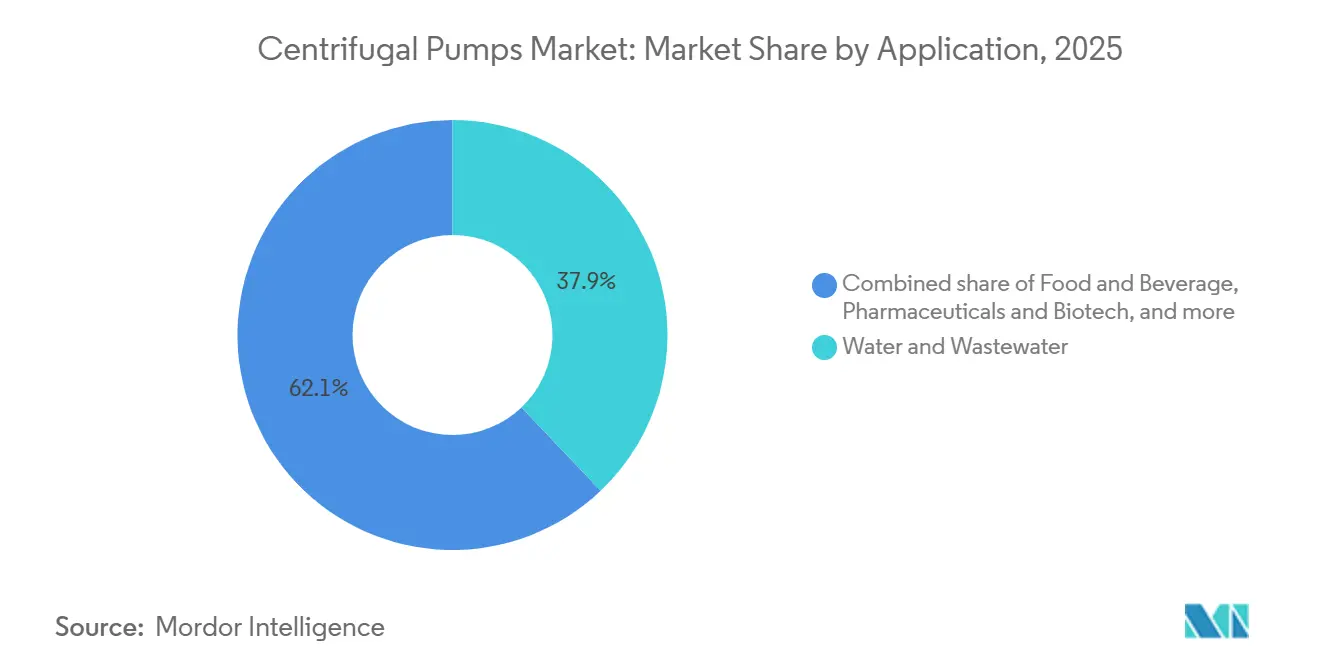

- By application, water and wastewater delivered 37.9% of 2025 revenue, yet food and beverage is the fastest segment with a 6.8% CAGR to 2031.

- By geography, Asia-Pacific contributed 50.3% of global revenue in 2025 and is expected to maintain a 6.4% CAGR, driven by China, India, and Southeast Asia.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Centrifugal Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wastewater infrastructure spending boom | +1.2% | Global, with concentration in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| HVAC retrofit wave in commercial buildings | +0.8% | North America & Europe, emerging in Asia-Pacific urban centers | Short term (≤ 2 years) |

| Oil & gas mid-stream capacity expansion | +0.9% | Middle East, North America (shale basins), Asia-Pacific (LNG terminals) | Medium term (2-4 years) |

| Power-generation build-outs, esp. CCGT | +0.7% | Asia-Pacific, Middle East, selective North America markets | Long term (≥ 4 years) |

| Modular skid pumps for data-centre cooling | +0.6% | North America, Europe, Asia-Pacific (hyperscale hubs) | Short term (≤ 2 years) |

| Hydrogen-ready liquid pumps for green H₂ projects | +0.5% | Australia, Middle East, Europe (North Sea corridor) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Waste-Water Infrastructure Spending Boom

Municipal and industrial treatment plants are in a capital-intensive upgrade cycle. The U.S. Environmental Protection Agency allocated USD 11.5 billion in 2024 through State Revolving Fund programs to modernize pump stations, membrane-bioreactor lines, and nutrient-removal assets[2]U.S. Environmental Protection Agency, “Clean Water State Revolving Fund Allotments,” epa.gov. The Clean Water State Revolving Fund disbursed USD 32.81 billion for advanced treatment and USD 2.255 billion for reuse projects, both of which depend on multi-stage pumps able to deliver 50–150 psi feed pressure. Utilities are replacing fixed-speed machines from the 1980s and 1990s with variable-speed units that cut energy use by 25–30%, saving USD 40,000–60,000 per 100-horsepower pump each year. PFAS remediation adds volume: 85% of EPA fiscal-year-2022 emerging-contaminant grants target per- and polyfluoroalkyl substances, driving demand for corrosion-resistant pumps that handle acidic regenerant streams. Outside the United States, the Philippines has earmarked PHP 438.4 billion (USD 8.5 billion) for irrigation projects that will install solar-powered single-stage units across 681,709 hectares.

HVAC Retrofit Wave in Commercial Buildings

Building owners are replacing legacy chilled-water pumps to satisfy tougher energy codes and refrigerant phasedown rules. The International Energy Agency identifies resilient cooling technologies such as ground-source heat pumps, chilled-water storage, and evaporative systems, all of which rely on centrifugal circulation pumps operating at 40–60 feet of head. Johnson Controls reports power-usage-effectiveness ratios of 1.18–1.24 for its cooling units, thanks in part to variable-speed pumps that trim parasitic energy 15–20% compared with constant-speed designs.[3]Johnson Controls, “Cooling Distribution Efficiency Case Study,” johnsoncontrols.com The U.S. EPA’s hydrofluorocarbon phasedown rule, finalized in 2023, accelerates the move to low-GWP refrigerants such as R-1234ze, which operate at higher pressures and therefore require pumps with upgraded seals. Daikin specifies pump discharge pressures of 8 bar for hyperscale-data-center chillers using low-GWP refrigerants, 30% above legacy R-134a systems.

Oil & Gas Mid-Stream Capacity Expansion

The Middle East is constructing 7,073 kilometers of crude oil pipelines and 8,169 kilometers of gas lines with a combined capital budget above USD 110 billion. Saudi Aramco’s Jafurah program and the Master Gas System expansion specify multistage barrel pumps rated for sour-service hydrogen-sulfide concentrations above 10,000 ppm and temperatures up to 200 °C.[4]Saudi Aramco, “Jafurah Unconventional Gas Program Overview,” aramco.com In North America, booster stations along existing pipe networks deploy two to four pumps in series to reach discharge pressures of 1,200–1,500 psi for heavier crude blends. Flowserve reported a USD 1.2 billion backlog in nuclear and fossil-fuel power projects in 2024, illustrating cross-sector fluid-handling demand. LNG terminals in Asia-Pacific specify cryogenic centrifugal pumps working at −162 °C for loading arms and boil-off reliquefaction.

Power-Generation Build-Outs, Especially CCGT

Combined-cycle gas-turbine plants add 40–50 GW of new capacity every year, each unit needing 12–18 centrifugal pumps for boiler-feed, condensate, and cooling-water circulation. Multi-stage barrel pumps compliant with API 610 generate up to 3,000 psi to meet high-pressure feedwater duties. Asia-Pacific builds most new CCGT facilities and awards long-term service contracts that bundle pumps with condition-monitoring software. The U.S. Nuclear Regulatory Commission approved Vogtle Units 3 and 4, each relying on high-integrity centrifugal pumps for cooling and safety systems. Hydroelectric pumped-storage projects also create opportunities for reversible pump-turbines sized above 100 MW, as seen in South Africa’s Lesotho Highlands Water Project Phase II.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel & alloy price volatility | -0.8% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Shift to positive-displacement pumps in niches | -0.4% | North America, Europe (pharmaceutical, food processing) | Medium term (2-4 years) |

| VFD adoption cutting oversized-pump replacements | -0.6% | Global, led by North America and Europe utilities | Medium term (2-4 years) |

| PFAS regulation limiting fluoropolymer-lined pumps | -0.3% | North America, Europe (chemical transfer, wastewater) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Steel & Alloy Price Volatility

The International Monetary Fund’s metals index rose 7.7% between February and August 2024, with copper up 8.1% and aluminum up 7.8%. A 10% copper jump historically adds a 0.2-point increase to consumer inflation within 12 months, pressuring pump OEMs that use copper in motor windings and bronze impellers. U.S. stainless-steel production fell 11% in October 2024, while ferrochromium prices dropped 29% year on year, reflecting supply-chain concentration in Kazakhstan and South Africa. Nickel-alloy castings gained 15–20% in 2024 after Indonesian export curbs and electric-vehicle battery demand tightened supply, forcing OEMs to substitute duplex stainless steels or lock in fixed-price contracts. European Union anti-dumping duties on Chinese stainless-steel flanges add 8–12% to landed cost and extend lead times by 4–6 weeks.

Shift to Positive-Displacement Pumps in Niches

Pharmaceutical bioprocessing and food-syrup handling increasingly adopt positive-displacement pumps that handle high-viscosity or shear-sensitive fluids more gently than centrifugal designs. While centrifugal models still hold more than 80% penetration in water and wastewater, substitution in sterile-transfer niches erodes incremental growth potential. Biotech plants integrate lobe and diaphragm pumps for culture media and buffer solutions because those designs provide smooth, pulsation-free flow at low Reynolds numbers. Food processors moving toward continuous, aseptic filling lines specify twin-screw pumps to reduce product damage. OEMs respond by bundling centrifugal and PD solutions, though internal competition can prolong sales cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Stage: Multi-Stage Pumps Gain on Desalination Surge

Multi-stage designs are forecast to grow at a 7.3% CAGR through 2031, outpacing the 6.0% market average as seawater reverse osmosis facilities, high-rise plumbing systems, and boiler-feed lines demand compact, high-pressure capability. Single-stage pumps still delivered 62.8% of 2025 revenue because municipal water distribution and HVAC circulation often work below 150 feet of head, favoring lower complexity. The International Energy Agency estimates that 40% of announced electrolyzer projects are located in water-stressed areas, each requiring reverse-osmosis feed pressure of 60–80 bar and thus six to ten multi-stage pumps per train. Boiler-feedwater packages for combined-cycle plants specify barrel configurations compliant with API 610 BB3, handling 3,000 psi discharge. Grundfos’s IE5 motor and VFD package pushes wire-to-water efficiency past 92%, lowering lifecycle energy by one-quarter. Mining companies adopt horizontal split-case multi-stage units that keep 70–75% hydraulic efficiency while resisting abrasion.

Single-stage pumps remain indispensable for cooling-tower makeup, fire-protection loops, and irrigation systems that value low capital cost and simple field repairs. Standard end-suction ANSI/ASME B73.1 footprints allow one-for-one drop-in replacements, and personnel can rebuild seals and bearings on site. Agricultural programs in India supply subsidized single-stage, solar-powered pumps to smallholder farms, boosting irrigation area coverage. In building services, twin-single-stage configurations with duty-standby logic offer redundancy without the cost premium of multi-stage sets. Despite slower growth, the large installed base secures steady aftermarket opportunities for seals, impellers, and wear rings.

By Pump Design (Flow Direction): Mixed-Flow Captures Flood Control

Radial-flow designs held 64.1% of 2025 revenue, anchored by their versatility in chemical processing, HVAC, and water supply, where heads run 50–300 feet and flows cover 100–5,000 gallons per minute. Mixed-flow pumps are expanding at a 6.9% CAGR because flood-control districts and open-pit mines favor higher specific speeds of 1,500–4,000 rpm that deliver greater head per stage without oversizing impeller diameters. The U.S. Army Corps of Engineers is retrofitting Mississippi River and Gulf Coast stations with mixed-flow models that achieve 80–85% efficiency, reducing parasitic power by 10–15% against radial predecessors. Mining tailings lines choose mixed-flow hydraulics for 20–30% solids while maintaining 65–70% efficiency, a clear advantage over radial designs in abrasive service.

Axial-flow propeller pumps, though niche, serve very-high-flow and low-head duties such as cooling-water intakes at coastal power plants and drainage in polders, handling more than 50,000 GPM with heads below 30 feet. Radial machines remain dominant in chemical and refinery services because ANSI dimensional interchangeability and low net-positive-suction-head-required values safeguard process uptime. In aquaculture and wastewater aeration, axial-flow models are gaining share for their ability to move large volumes at minimal energy, improving dissolved-oxygen transfer rates. Across all geometries, computational fluid-dynamic optimization and additive-manufactured flow passages fine-tune efficiency and reduce cavitation risk.

By Impeller Type: Semi-Open Designs Rise on Slurry Tolerance

Enclosed impellers secured 70.4% of 2025 revenue because sanitary food, pharmaceutical, and potable-water standards demand crevice-free surfaces under 0.8 µm roughness per 3-A Sanitary Standard 02-10. Semi-open impellers are projected to grow at a 7.0% CAGR through 2031 by addressing mining, wastewater, and pulp applications where solids exceed 5% by weight and clogging risk outweighs a 2–4% efficiency penalty. Dairy processors specify electropolished enclosed impellers for milk and yogurt lines that must withstand aggressive cleaning agents without harboring bacteria. Mining tailings pumps employ semi-open designs with replaceable wear plates, doubling the mean time between rebuilds to 4,000–5,000 hours.

Open impellers, while smaller in share, handle fibrous material in municipal lift stations and reject brine from membrane systems, allowing vane-to-shroud clearance adjustments to compensate for wear. HVAC and potable-water pumps keep enclosed designs because they deliver 78–85% hydraulic efficiency and maintain low airborne noise of 65–75 dBA at one-meter distance, meeting ASHRAE 90.1 limits. Wastewater plants with ragging issues favor semi-open impellers with passages of three to four inches, reducing blockage events and maintenance over time. OEMs invest in duplex stainless and ceramic composite overlays to delay erosive wear on semi-open vanes.

By Application: Food & Beverage Leads Growth

Water and wastewater contributed 37.9% of 2025 sales, yet the food and beverage segment leads growth at 6.8% CAGR through 2031 as processors automate clean-in-place procedures and deploy stainless-steel 316L pumps that meet FDA contact-surface rules. Chemical and petrochemical demand stays robust with ethylene, polyethylene, and ammonia expansions in the Middle East and North America, where ANSI end-suction pumps move caustic and chlorinated feedstocks. HVAC remains a mature but recurring revenue stream tied to 15–20-year life cycles and refrigerant phasedown retrofits. Oil and gas applications grow with pipeline additions and refinery upgrades; the International Energy Agency projects 103–105 million b/d global crude production by 2030, driving thousands of booster and process-unit pump installs.

Mining calls for abrasion-resistant hard-iron or ceramic composite impellers to serve copper, lithium, and rare-earth slurry lines, with global copper production tracked to rise 3–4% annually through 2031. Power generation purchases span conventional, nuclear, and renewable plants that each require condensate and cooling-water units. Pharmaceutical and biotech facilities specify sanitary pumps compliant with FDA 21 CFR Part 11 electronic records, integrating flow meters and automated cleaning-validation software. Across applications, demand is shifting toward packages that bundle pumps, variable-frequency drives, and predictive-maintenance sensors under a single warranty.

Geography Analysis

Asia-Pacific delivered 50.3% of 2025 revenue and is expected to post a 6.4% CAGR to 2031, supported by municipal wastewater upgrades in China, irrigation modernization in India, and geothermal power additions in Indonesia. China’s CNP Pumps generated RMB 4.795 billion (USD 670 million) in 2023 and holds more than 600 patents that help win domestic and export tenders. India’s Pradhan Mantri Krishi Sinchai Yojana subsidizes solar-powered centrifugal sets for small and marginal farmers, expanding addressable volumes. Southeast Asia’s geothermal capacity reached 2,360 MW in 2022, with brine temperatures above 200 °C requiring corrosion-resistant pumps for reinjection loops.

North America and Europe jointly claimed 35–38% of 2025 sales. Aging infrastructure keeps baseline demand stable while energy-efficiency retrofits and PFAS remediation laws lift replacement rates. The U.S. EPA earmarked USD 11.5 billion in 2024 for pump-station modernization, membrane bioreactors, and nutrient-removal projects. Germany provides rebates covering up to 35% of pump-upgrade costs for industrial and commercial facilities, accelerating VFD adoption. KSB’s 2024 purchase of Hydro Inc. adds wastewater capacity in Maine and a distribution network across the U.S. Northeast, positioning the group closer to municipal customers.

Middle East-Africa and South America are on track for a 6.5–7.0% CAGR, driven by desalination plants, pipeline expansions, and mining projects. Saudi Arabia’s Vision 2030 channels USD 1 trillion into infrastructure, including reverse-osmosis desalination units that each require eight to twelve high-pressure pumps. South Africa’s Lesotho Highlands Water Project Phase II budgets USD 2.3 billion for a 1,270 MW pumped-storage scheme using sixteen to twenty reversible pump-turbines. Brazil’s sanitation law mandates 90% water-supply and wastewater-collection coverage by 2033, implying 50,000–60,000 new pump installs, mainly single-stage end-suction units.

Competitive Landscape

The centrifugal pumps market displays moderate concentration. The five largest suppliers, Grundfos, Flowserve, Xylem, KSB, and Sulzer, collectively hold about 35–40% of global sales, leaving meaningful space for regional players like Kirloskar Brothers, CNP, and Torishima. ITT completed its USD 4.775 billion acquisition of SPX FLOW in January 2026, adding USD 1.3 billion of revenue with a 43% aftermarket mix and new footprints in food, beverage, and pharmaceutical niches. Honeywell bought Sundyne for USD 2.16 billion in March 2025 to gain high-speed pumps and compressors serving refining and LNG markets.

Strategy now revolves around digital integration. Roughly 30–40% of new installations ship with integrated VFDs, reducing energy use by 25–30% in water utilities. Cloud-based condition monitoring trims unplanned downtime 15–20%, and utilities increasingly demand ISO 50001 compliance. Grundfos is buying Newterra to pair treatment skids with pumps in turnkey packages, creating a USD 350 million water-solutions platform. Xylem’s 2024 stake in Idrica added digital-twin expertise for leak detection and asset management. Suppliers that master materials science and regulatory navigation position themselves for growth in PFAS remediation, hydrogen water supply, and data-center cooling.

Centrifugal Pumps Industry Leaders

Grundfos Holding A/S

Flowserve Corporation

Xylem Inc.

KSB SE & Co. KGaA

Sulzer Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Hefei Huasheng Pumps & Valves Co., Ltd. confirmed its participation in the International Industrial Week (IIW) 2026 exhibition in Jakarta. The company plans to showcase its API 610 centrifugal pumps and heavy-duty chemical pump solutions.

- April 2026: Sulzer signed a long-term corporate procurement agreement with Saudi Aramco to enhance supply and service support for industrial pumping systems utilized in oil, gas, and water infrastructure projects.

- January 2026: DXP Enterprises announced the acquisition of PREMIERflow, expanding its portfolio of integrated pump systems for applications in water, wastewater, HVAC, and fire protection. This acquisition underscored ongoing consolidation trends in the centrifugal pump and fluid-handling market.

- January 2026: Hefei Huasheng Pumps & Valves Co., Ltd. reported that its ebullated-bed recycle centrifugal pump for residue oil hydrogenation units achieved a successful one-time startup at a refinery installation, demonstrating advancements in high-temperature refining pump systems.

Global Centrifugal Pumps Market Report Scope

Centrifugal pumps are used to transport fluids by converting rotational kinetic energy into the hydrodynamic energy of the fluid flow. The rotational energy typically comes from an engine or electric motor.

The global centrifugal pumps market is segmented by stage, pump design, impeller type, application, and geography. By stage, the market is segmented into single-stage and multi-stage. By pump design, the market is segmented into radial flow, mixed flow, and axial flow. By impeller type, the market is segmented into open, semi-open, and enclosed. By application, the market is segmented into water and wastewater, chemical and petrochemical, HVAC and building services, oil and gas, food and beverage, mining and metals, power generation, pharmaceuticals and biotech, and others. The report also covers the market size and forecasts for the centrifugal pump market across the regions. For each segment, market sizing and forecasts have been done based on revenue (USD billion).

By Stage

| Single-Stage Pumps |

| Multi-Stage Pumps |

By Pump Design (Flow Direction)

| Radial Flow |

| Mixed Flow |

| Axial Flow |

By Impeller Type

| Open |

| Semi-Open |

| Enclosed |

By Application

| Water and Wastewater |

| Chemical and Petrochemical |

| HVAC and Building Services |

| Oil and Gas (Upstream, Midstream, Downstream) |

| Food and Beverage |

| Mining and Metals |

| Power Generation (Thermal, Nuclear, Renewables) |

| Pharmaceuticals and Biotech |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Turkey | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Qatar | |

| Rest of Middle East and Africa |

| By Stage | Single-Stage Pumps | |

| Multi-Stage Pumps | ||

| By Pump Design (Flow Direction) | Radial Flow | |

| Mixed Flow | ||

| Axial Flow | ||

| By Impeller Type | Open | |

| Semi-Open | ||

| Enclosed | ||

| By Application | Water and Wastewater | |

| Chemical and Petrochemical | ||

| HVAC and Building Services | ||

| Oil and Gas (Upstream, Midstream, Downstream) | ||

| Food and Beverage | ||

| Mining and Metals | ||

| Power Generation (Thermal, Nuclear, Renewables) | ||

| Pharmaceuticals and Biotech | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Turkey | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Qatar | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the centrifugal pumps market in 2026?

The centrifugal pumps market size is estimated at USD 40.46 billion in 2026.

Which region purchases the most centrifugal pumps?

Asia-Pacific accounted for 50.3% of global revenue in 2025 and remains the largest buyer through 2031.

What pump type is growing fastest by stage?

Multi-stage centrifugal pumps are projected to expand at a 7.3% CAGR, driven by desalination and boiler-feed applications.

Why are mixed-flow designs gaining share?

Flood-control and mining projects prefer mixed-flow hydraulics for higher specific speeds and improved efficiency at medium heads.

How are regulations affecting pump materials?

PFAS restrictions are pushing manufacturers to shift from fluoropolymer linings to alternatives like PPS and PEEK, increasing certification timelines and costs.

What digital features are utilities demanding?

Integrated variable-frequency drives and cloud-based condition monitoring that cut energy use up to 30% and reduce downtime by about 20%.

Page last updated on: