Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.19 Billion |

| Market Size (2031) | USD 12.59 Billion |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Centrifuges Market Analysis by Mordor Intelligence

The Industrial Centrifuges Market size is estimated at USD 9.19 billion in 2026, and is expected to reach USD 12.59 billion by 2031, at a CAGR of 6.49% during the forecast period (2026-2031).

Solid growth stems from stricter wastewater-discharge rules, pharmaceutical and biotech capacity additions, and a rapid build-out of lithium-ion battery-recycling lines, all of which are pushing operators toward higher-throughput, higher-purity separations.[1]U.S. Environmental Protection Agency, “Effluent Guidelines 40 CFR Part 437,” epa.gov Sedimentation units maintained leadership, yet filtering variants are scaling quickly as drug-makers and specialty-chemical producers tighten purity targets. Vertical designs are gaining share in cleanrooms where every square meter of floor area carries a premium. Continuous-mode machines dominate high-volume commodities, but batch equipment is steadily rising in regulated multiproduct suites. Regionally, North America benefits from federal infrastructure and reshoring programs, while Asia-Pacific accelerates on the back of Zero Liquid Discharge mandates and pharmaceutical export growth.[2]U.S. Department of Energy, “Bipartisan Infrastructure Law Clean Water Funding,” energy.gov

Key Report Takeaways

- By type, sedimentation centrifuges captured 56.6% of the industrial centrifuge market share in 2025. Filtering centrifuges are forecast to expand at a 7.2% CAGR from 2026 to 2031.

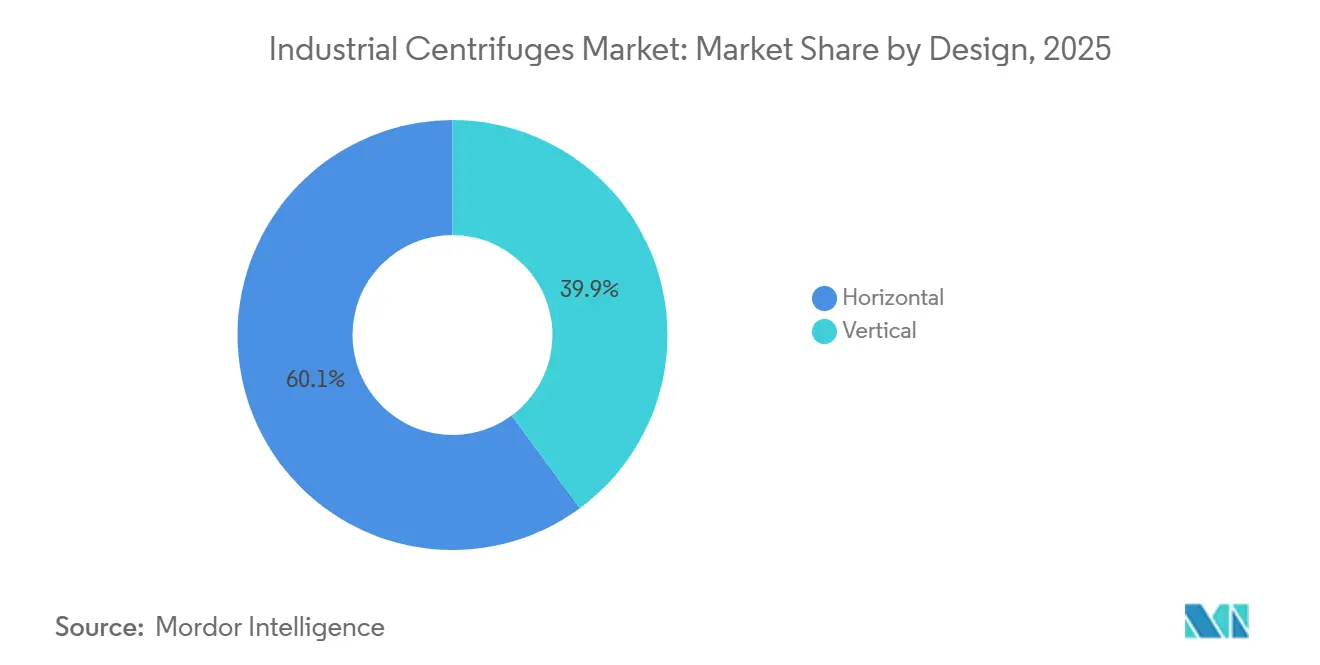

- By design, horizontal machines led with 60.1% revenue share in 2025. Vertical configurations are projected to grow at a 7.6% CAGR through 2031.

- By operation mode, continuous centrifuges held a 66.3% share in 2025. Batch units are advancing at a 7.8% CAGR between 2026 and 2031.

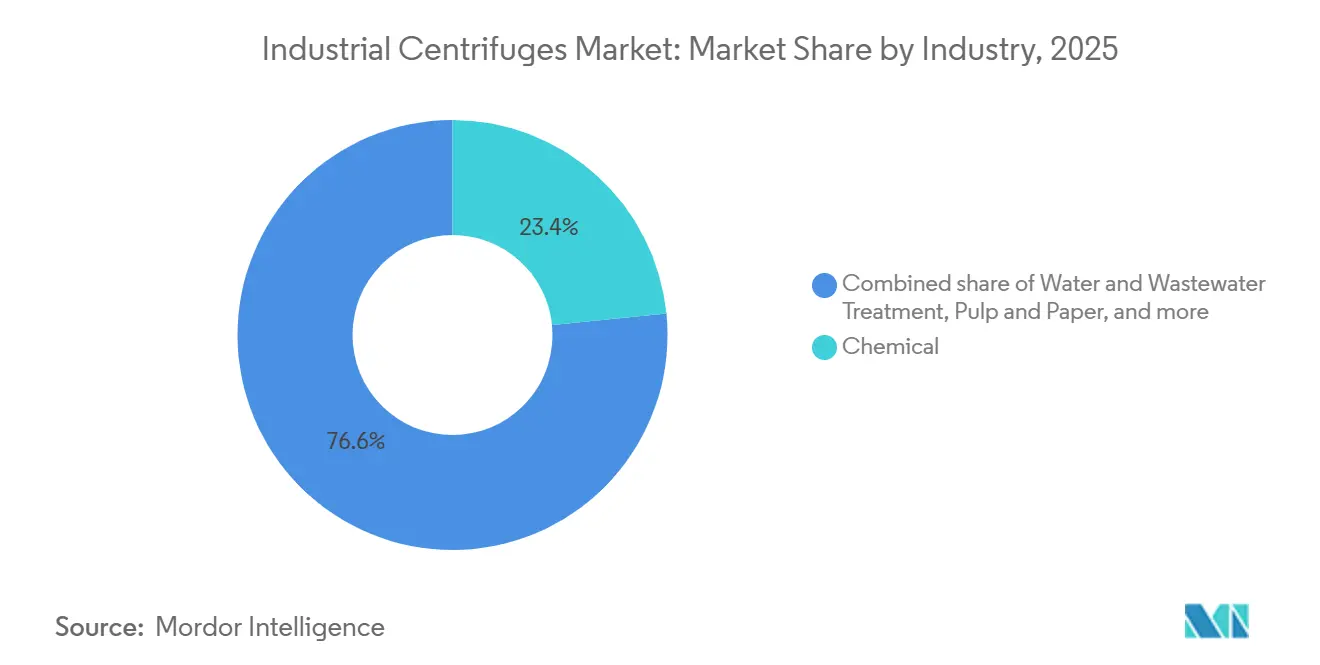

- By industry, chemical processing commanded a 23.4% share of the industrial centrifuge market size in 2025. Water and wastewater treatment is expected to post the fastest 8.3% CAGR to 2031.

- By geography, North America led with 36.7% revenue share in 2025. Asia-Pacific is anticipated to grow at a 7.5% CAGR through the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Centrifuges Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent wastewater regulations | +1.2% | Global (North America, EU, China) | Medium term (2-4 years) |

| Capacity expansion in pharma & biotech | +1.4% | North America, Europe, India, Singapore | Short term (≤2 years) |

| Demand from food & beverage clarification | +0.8% | Europe, North America | Long term (≥4 years) |

| Industrial wastewater-reuse mandates | +1.1% | APAC core, Middle East, South America | Medium term (2-4 years) |

| Surge in Li-ion battery-recycling lines | +1.3% | North America, Europe, China, South Korea | Short term (≤2 years) |

| Scale-up of algae-based biofuel plants | +0.6% | North America, select APAC markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent Wastewater Regulations

EPA’s 40 CFR Part 437 limits are forcing centralized waste-treatment operators to adopt decanter centrifuges that yield drier cake and lower disposal volumes. China’s updated Water Pollution Prevention and Control Law drives Zero Liquid Discharge installations in chemical parks, favoring compact vertical designs able to handle saline brines. In the EU, Industrial Emissions Directive updates require pulp-and-paper mills to cut suspended solids, spurring retrofits with disc-stack separators that achieve turbidity below 10 NTU. Brownfield space constraints give vertical machines an edge, while compliance deadlines stretching to 2028 anchor multi-year aftermarket demand.

Capacity Expansion in Pharma & Biotech

AGC Biologics doubled its Copenhagen capacity in 2025 and installed automated disc-stack separators that trim harvest cycle time by 40%.[3]AGC Biologics, “Copenhagen Expansion Press Release,” agcbio.com Grifols’ FDA-approved plasma line in North Carolina employs tubular-bowl centrifuges to reach 98% immunoglobulin purity.[4]Food and Drug Administration, “Biologics License Approvals,” fda.gov Modular cleanrooms and single-use bioreactors fuel demand for skid-mounted vertical centrifuges, allowing contract manufacturers to switch campaigns within 72 hours. Biosimilar ramp-ups in India and South Korea extend growth, as filtering centrifuges deliver tighter particle-size control critical for bioavailability.

Demand from F&B Clarification

Juice and beverage processors are trading settling tanks for hermetic disc-stack separators that support cold-pressed, extended-shelf-life SKUs. European dairy cooperatives installed more than 150 clarifiers in 2024-2025 to hit bacterial-count rules under Regulation (EC) No 853/2004. Craft breweries recover yeast with compact horizontal decanters, cutting wastewater costs by 60% and creating resale biomass streams. Plant-based drink makers deploy three-phase decanters to separate oil, proteins, and water in one step, although membranes are gaining share where gentle handling outweighs throughput.

Industrial Wastewater-Reuse Mandates

China targets 30% industrial water reuse by 2025, prompting Jiangsu and Shandong chemical parks to install decanters ahead of reverse-osmosis polishing. The UAE’s law on industrial recycling pushes petrochemical complexes toward disc-stack separators for oil-water splits. India’s revised textile standards cap total dissolved solids at 2,100 mg/L, driving dye houses to adopt pusher centrifuges for salt recovery. Continuous-mode systems suit 24/7 plants, yet batch machines gain ground in smaller facilities that process by campaign.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure | −0.9% | Global, acute in South America and MEA | Short term (≤2 years) |

| Elevated operating & energy cost | −0.7% | Europe, North America, select APAC markets | Medium term (2-4 years) |

| Competition from membrane technology | −0.5% | Global, focused in F&B and pharma | Long term (≥4 years) |

| Shortage of skilled centrifuge operators | −0.4% | North America, Europe, spill-over to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure

A mining-tailings decanter can cost more than USD 2 million, and installation adds up to 40% on top, pressuring operators in South America and Southeast Asia to delay purchases. European suppliers now offer pay-per-tonne contracts that shift capex onto the OEM, but uptake remains low outside pharma. Custom bowl materials push lead times past 12 months, stretching project-finance windows.

Elevated Operating & Energy Cost

Disc-stack separators in European dairy plants run 15-20 kW nonstop, yielding annual electricity outlays of USD 15,000-25,000 per unit at 2026 tariffs. Variable-frequency drives can trim load 20-30%, yet retrofits cost up to USD 80,000. In abrasive mining duties, bearing swaps and bowl resurfacing lift opex by USD 30,000-50,000 a year, nudging some users toward membranes where solids content is modest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Filtering Variants Gain on Purity Demands

Sedimentation equipment retained 56.6% of the industrial centrifuge market share in 2025, thanks to entrenched use in mining, municipal sludge, and edible oil refining. Continuous decanters in copper-tailings ponds treat 100 m³/h and yield cake at 22% solids, while clarifiers in dairy achieve turbidity under 1 NTU. Filtering machines are forecast to grow 7.2% annually, capturing API crystallization, lithium-carbonate refining, and specialty-chemical purification. Basket units suit small-batch drug intermediates, whereas pusher designs run continuous adipic-acid crystals. Peeler centrifuges in battery-grade lithium facilities automate cake discharge and shield operators from caustic spray. As ISO 14644 cleanroom rules tighten, vertical filtering models that integrate clean-in-place features are becoming the standard in Grade C and D suites.

Both categories will coexist: sedimentation variants dominate where throughput, robustness, and low opex rule; filtering types win where purity, wash efficiency, and cake dryness directly influence product value. These divergent requirements underpin a balanced demand outlook and ensure no single technology displaces the other over the forecast window.

By Design: Vertical Configurations Capture Cleanroom Share

Horizontal layouts held 60.1% of the industrial centrifuge market in 2025, driven by mining, wastewater, and shipboard installations where floor space is abundant and low center-of-gravity designs curb vibration. Decanters process 24/7 with minimal oversight, and horizontal disc-stack models in marine fuel-oil purification prevent sludge accumulation. Vertical machines, however, are set to compound 7.6% a year, propelled by cleanroom economics that price space at USD 5,000-10,000 per square meter. AGC Biologics’ Copenhagen site realized a 40% footprint saving by selecting vertical disc stacks, enabling two extra bioreactor trains within the same envelope. Vertical peeler centrifuges boost solvent containment, mitigating explosion hazards in flammable-solvent API plants. Battery-recycling lines favor vertical decanters because overhead conveyors feed slurry directly into top-mounted inlets.

The industrial centrifuge market will likely see convergence as suppliers refine hybrid geometries, tilted bowls, or modular frames that blend the space and maintenance advantages of both forms, smoothing adoption barriers across end-use sectors.

By Operation Mode: Batch Flexibility Offsets Continuous Efficiency

Continuous centrifuges owned a 66.3% share in 2025, leveraging nonstop operation in bulk foods, base chemicals, and mining. Decanters in municipal biosolids log 8,000-10,000 hours yearly, with automated sludge discharge keeping uptime above 95%. Batch machines, projected to climb 7.8% CAGR, cater to multiproduct drug plants and specialty-chemical campaigns. Basket and peeler units permit rapid switchover and cleaning validation within six hours, crucial under FDA 21 CFR Part 211 and EU GMP Annex 1. Grifols processes donor pools individually via batch tubular-bowl designs that sustain lot traceability. In battery-recycling pilots, batch filtering centrifuges handle assorted chemistries, enabling parameter tweaks between campaigns to maximize yield.

With personalized medicine, cell-therapy, and bespoke specialty-chemical streams gaining share, the industrial centrifuge market will continue to balance continuous throughput gains with batch-driven flexibility, each commanding loyalty in its respective niche.

By Industry: Water Treatment Outpaces Chemical Incumbency

Chemical processing remained top at 23.4% revenue share in 2025, underpinning solvent recovery, polymer dewatering, and catalyst recycling. Decanters in polyvinyl-chloride resin streams reduce downstream drying energy by 40%, while disc stacks reclaim palladium catalysts in fine-chem plants. Water and wastewater treatment is expected to record the highest 8.3% CAGR, thanks to 40 CFR Part 437 and China’s Zero Liquid Discharge mandates that force mechanical dewatering before disposal or reuse. Municipal utilities in North America are swapping belt presses for decanters, cutting polymer use by 30% and producing dryer cake for land application. Textile mills in India retrofit disc stacks to hit solids limits below 30 mg/L, avoiding hefty discharge penalties.

Pharma and biotech strides mirror capacity expansions; F&B applications widen with craft-brew yeast recovery and plant-based protein clarification. Mining, pulp-and-paper, and power generation represent steady albeit cyclical demand based on commodity pricing and environmental upgrades.

Geography Analysis

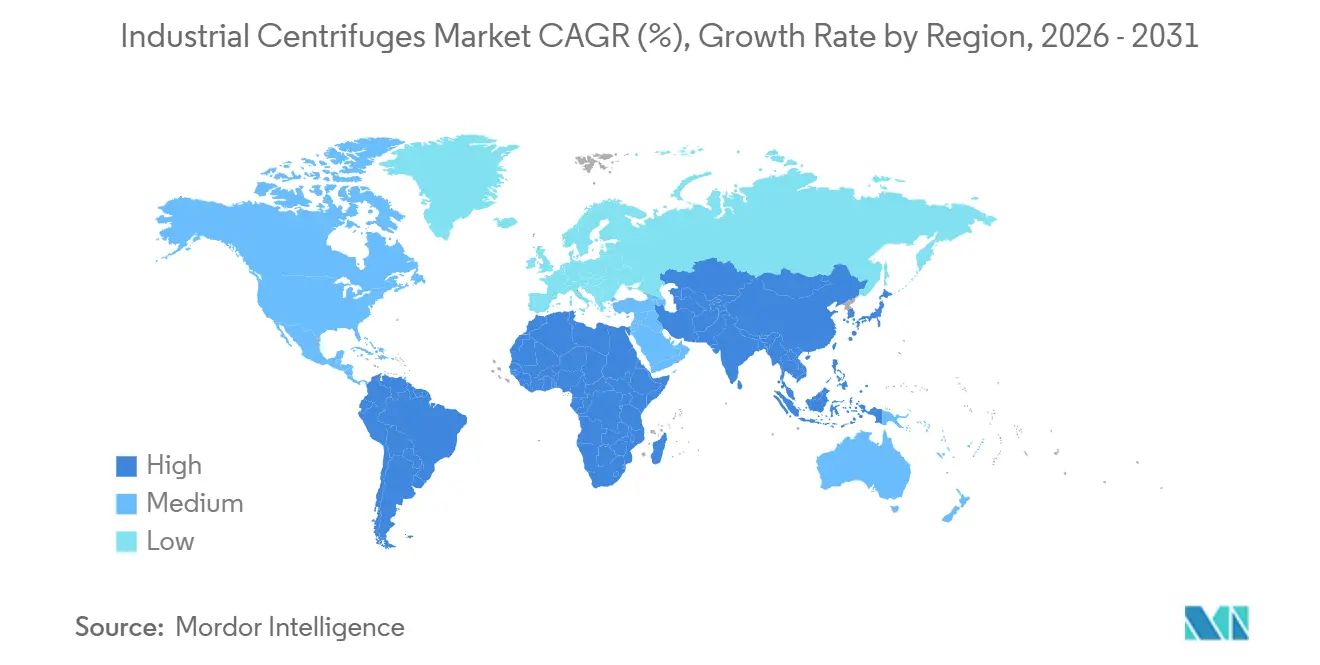

North America secured 36.7% of 2025 revenue, buoyed by federal infrastructure funds, battery gigafactory buildouts, and near-shoring of critical pharma actives. Li-Cycle’s Rochester and BASF’s planned South Carolina sites alone will need roughly 20 industrial centrifuges for black-mass and precursor processing. Alberta’s oil-sands producers invest USD 500 million annually in tailings decanters to satisfy reclamation rules, while Mexico’s API hubs add hermetic disc stacks to comply with FDA and EMA standards.

Asia-Pacific is projected to log a 7.5% CAGR, the fastest global clip. China’s chemical parks deployed more than 300 new decanters across 2024-2025 to meet Zero Liquid Discharge obligations. India’s Hyderabad-Ahmedabad pharma corridor adopts vertical disc stacks for biosimilar lines targeting Western export markets. Japan and South Korea retrofit municipal and industrial wastewater plants with energy-saving vertical separators, and ASEAN nations scale palm-oil and rubber centrifuge capacity amid sustainability incentives.

Europe retains a sizeable share as the Industrial Emissions Directive tightens limits and the revised Urban Wastewater Treatment Directive imposes nutrient caps, compelling clarifier upgrades in municipal facilities. Energy-intensive regions like Germany favor bowl designs with regenerative braking to offset high electricity tariffs. South America sees sporadic yet high-value orders in Chilean copper and Brazilian lithium mines, while MEA water-reuse projects in the UAE and Saudi Arabia rely on disc-stack separators for desalination brine. Africa’s mining belts prefer refurbished units due to foreign-exchange hurdles, keeping sales volumes low but aftermarket services active.

Competitive Landscape

The top five suppliers, Alfa Laval, GEA, Andritz, Flottweg, and Mitsubishi Kakoki, control an estimated 45-50% of global revenue, indicating moderate concentration. European incumbents differentiate through integrated automation, predictive maintenance, and global service footprints that cut unplanned downtime up to 30%. Chinese and Indian challengers offer 15-25% lower capital costs and shorter lead times, winning orders in price-sensitive municipal projects and emerging markets. Alfa Laval’s latest disc-stack line lowers energy use by 20% and embeds IoT sensors for vibration, bearing temperature, and solids load monitoring, enabling service interventions before failure. GEA’s retrofit program with a European dairy cooperative adds variable-frequency drives to 50 clarifiers, guaranteeing 25% power savings. Andritz niches into mining with tungsten-carbide-coated bowls that survive abrasive slurries for 5,000 hours, while Mitsubishi Kakoki positions peeler centrifuges for solvent-rich API crystallization, complete with ATEX Zone 1 compliance.

Competitive intensity will sharpen around battery recycling, algae biofuels, and pharmaceutical single-use suites, where domain know-how rather than price dictates vendor selection. Patent activity focuses on hermetic sealing, ceramic-composite bowls, and AI-driven separation algorithms, suggesting that software and materials will define the next wave of differentiation.

Industrial Centrifuges Industry Leaders

Alfa Laval AB

GEA Group AG

Andritz AG

Flottweg SE

Mitsubishi Kakoki Kaisha, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Alfa Laval's launch of the Culturefuge 200 B separator is revolutionizing high-density fermentations, offering a significant advantage to medium-sized biopharma producers. With this new separator, pharmaceutical companies, regardless of their size, can now harness medium-scale processes.

- September 2025: GEA has unveiled the GSI 260 skid, marking a new era of separators tailored for the beverage industry. The exterior boasts the Kinetic Edge Design, while the interior is equipped with a direct drive, resource-efficient features, and modular adaptability.

- April 2025: Thermo Fisher Scientific Inc. has rolled out new floor-model centrifuges, emphasizing sustainability while ensuring top-notch performance and sample security. The newly launched Thermo Scientific Cryofuge, BIOS, and LYNX centrifuges stand out as pioneers, being the first in their category to incorporate natural refrigerant cooling systems.

- March 2025: GEA has introduced the kytero 10, the world's smallest single-use disk stack centrifuge. Designed for the biopharmaceutical, food, and emerging food sectors, it supports product development with smaller bioreactor sizes. It separates bacteria, cell cultures, and yeasts and is used in cell and gene therapy.

Global Industrial Centrifuges Market Report Scope

An industrial centrifuge is a machine used for fluid or particle separation. Centrifuges rely on centrifugal force, generating several hundred or thousands of times Earth’s gravity. Industrial centrifuges can be classified into two main types: sedimentation and filtering centrifuges. Industrial centrifuges are used in various processes, including wastewater processing, chemical processing, pharmaceutical and biotechnology, food processing, mining, and mineral processing.

The global industrial centrifuge market is segmented by type, design, operation mode, industry, and geography. By type, the market is segmented into sedimentation and filtering. By design, the market is segmented into horizontal and vertical. By operation mode, the market is segmented into batch and continuous. By industry, the market is segmented into food and beverages, pharmaceutical and biotech, water and wastewater treatment, chemical, metals and mining, power generation, pulp and paper, and other industries. The report also covers the market size and forecasts for the industrial centrifuges market across major regions, such as Asia-Pacific, North America, Europe, South America, and the Middle East and Africa. Market sizing and forecasts are made for each segment based on revenue (USD).

By Type

| Sedimentation | Clarifier/Thickener |

| Decanter | |

| Disc-stack | |

| Hydrocyclone | |

| Other Sedimentation | |

| Filtering | Basket |

| Scroll-screen | |

| Peeler | |

| Pusher | |

| Other Filtering |

By Design

| Horizontal |

| Vertical |

By Operation Mode

| Batch |

| Continuous |

By Industry

| Food and Beverages |

| Pharmaceutical and Biotech |

| Water and Wastewater Treatment |

| Chemical |

| Metals and Mining |

| Power Generation |

| Pulp and Paper |

| Other Industries |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | Sedimentation | Clarifier/Thickener |

| Decanter | ||

| Disc-stack | ||

| Hydrocyclone | ||

| Other Sedimentation | ||

| Filtering | Basket | |

| Scroll-screen | ||

| Peeler | ||

| Pusher | ||

| Other Filtering | ||

| By Design | Horizontal | |

| Vertical | ||

| By Operation Mode | Batch | |

| Continuous | ||

| By Industry | Food and Beverages | |

| Pharmaceutical and Biotech | ||

| Water and Wastewater Treatment | ||

| Chemical | ||

| Metals and Mining | ||

| Power Generation | ||

| Pulp and Paper | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value for the industrial centrifuges market through 2031?

The market is expected to reach USD 12.59 billion from USD 9.19 billion in 2026, expanding at a 6.49% CAGR between 2026 and 2031.

Which centrifuge type is growing fastest?

Filtering centrifuges are forecast to grow 7.2% annually, propelled by pharmaceutical API crystallization and battery-material purification.

Why are vertical centrifuges gaining traction?

Vertical designs save up to 40% floor space, a key benefit in cleanrooms where space costs USD 5,000-10,000 per m² per year.

Which end-use segment should see the highest growth?

Water and wastewater treatment is projected to post an 8.3% CAGR, driven by stricter discharge regulations in major economies.

What is the main competitive advantage of leading suppliers?

Market leaders differentiate through integrated automation and predictive-maintenance platforms that cut unplanned downtime by as much as 30%.

How do energy costs affect centrifuge adoption?

High electricity tariffs, especially in Europe, make operating disc-stack units expensive; variable-frequency drives can lower energy draw by up to 30%.

Page last updated on: