Organ Preservation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

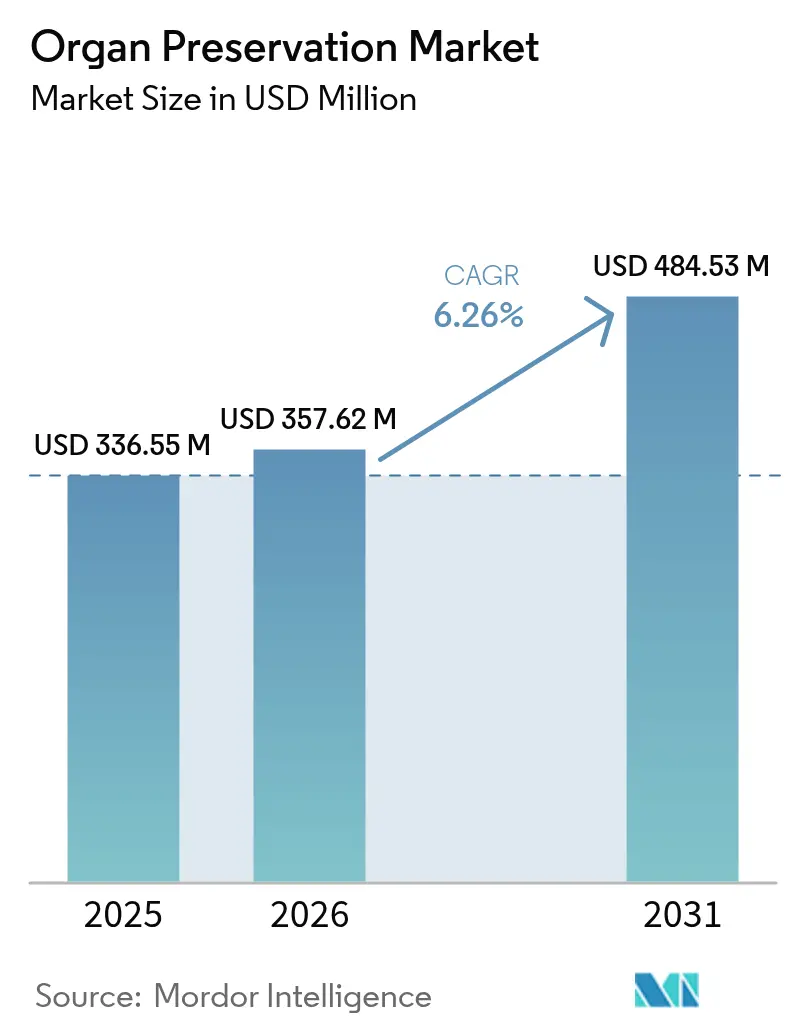

| Market Size (2026) | USD 357.62 Million |

| Market Size (2031) | USD 484.53 Million |

| Growth Rate (2026 - 2031) | 6.26% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organ Preservation Market Analysis by Mordor Intelligence

The organ preservation market size was valued at USD 336.55 million in 2025 and estimated to grow from USD 357.62 million in 2026 to reach USD 484.53 million by 2031, at a CAGR of 6.26% during the forecast period (2026-2031). Demand growth mirrors the widening gap between transplant need and donor supply, with 103,000 people queued for organs in the United States while only 48,000 procedures took place during 2024. Normothermic machine perfusion (NMP) is redefining clinical expectations by giving surgeons extra evaluation time and salvaging organs once deemed unusable, as reflected in the FDA clearance of the Organ Care System Heart. Reimbursement codes for ex-vivo perfusion under Medicare’s Increasing Organ Transplant Access Model add a financial catalyst that broadens hospital adoption. Meanwhile, supply-chain safeguards mandated by the FDA improve device availability yet highlight cost pressures for hospitals that must procure both disposables and capital equipment. Rising rates of diabetes, cardiovascular disease, and chronic kidney disease in older adults further add structural demand, pushing transplant programs to maximize every donated graft.

Key Report Takeaways

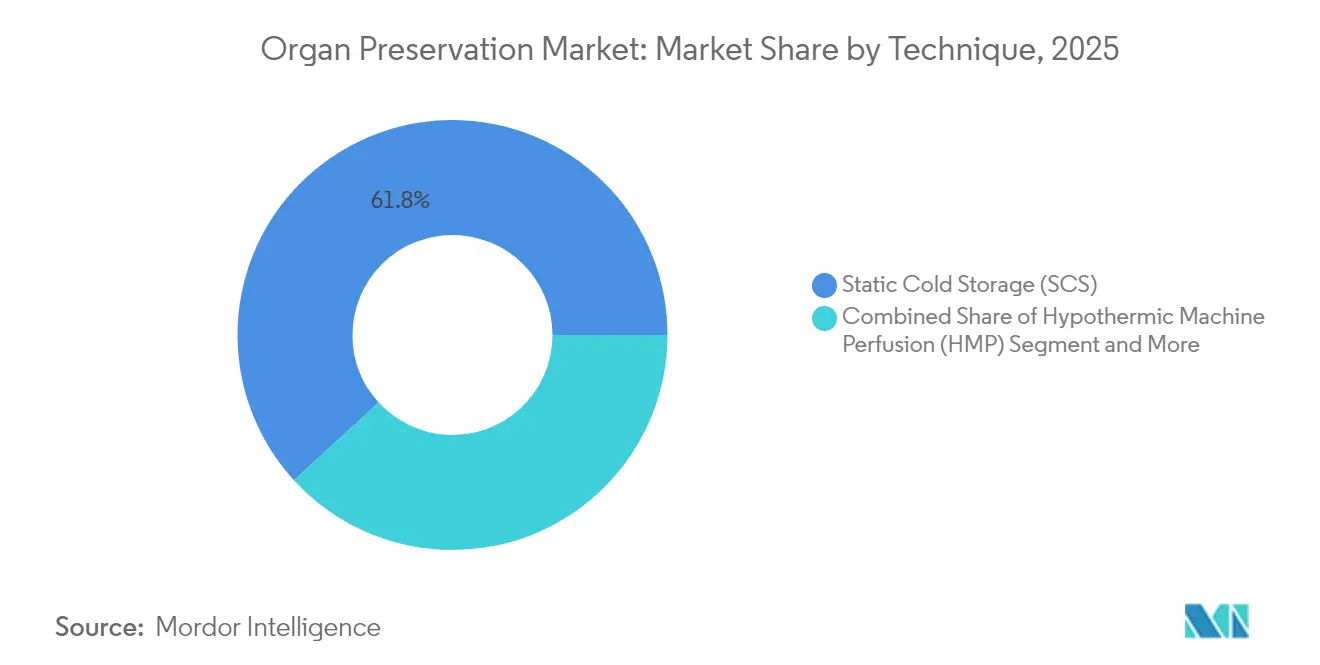

- By technique, Static Cold Storage captured 61.80% of the organ preservation market share in 2025, while Normothermic Machine Perfusion is forecast to expand at a 10.31% CAGR through 2031.

- By preservation solution, University of Wisconsin Solution held 45.10% of the organ preservation market share in 2025; Custodiol HTK is expected to grow at 9.18% CAGR to 2031.

- By product type, Preservation Solutions accounted for 49.30% share of the organ preservation market size in 2025, whereas Transport Systems & Devices are advancing at a 9.12% CAGR.

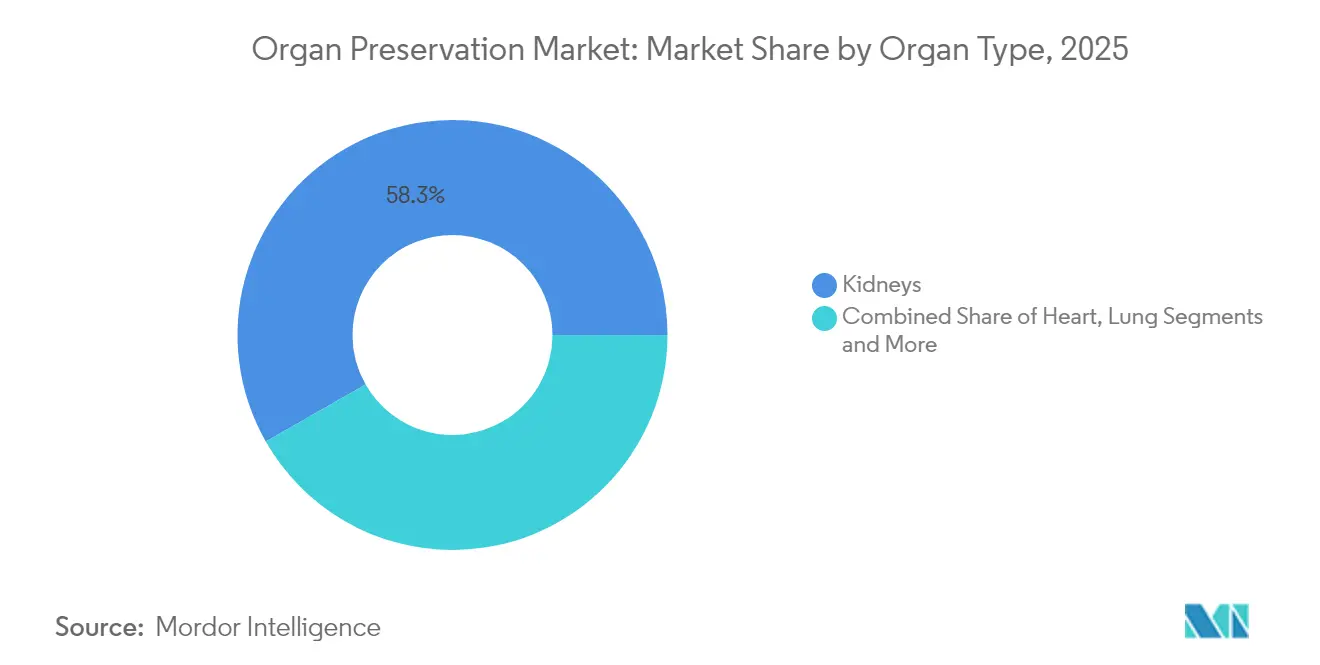

- By organ, kidneys commanded 58.25% share of the organ preservation market size in 2025; lungs represent the fastest-growing organ category at 10.48% CAGR.

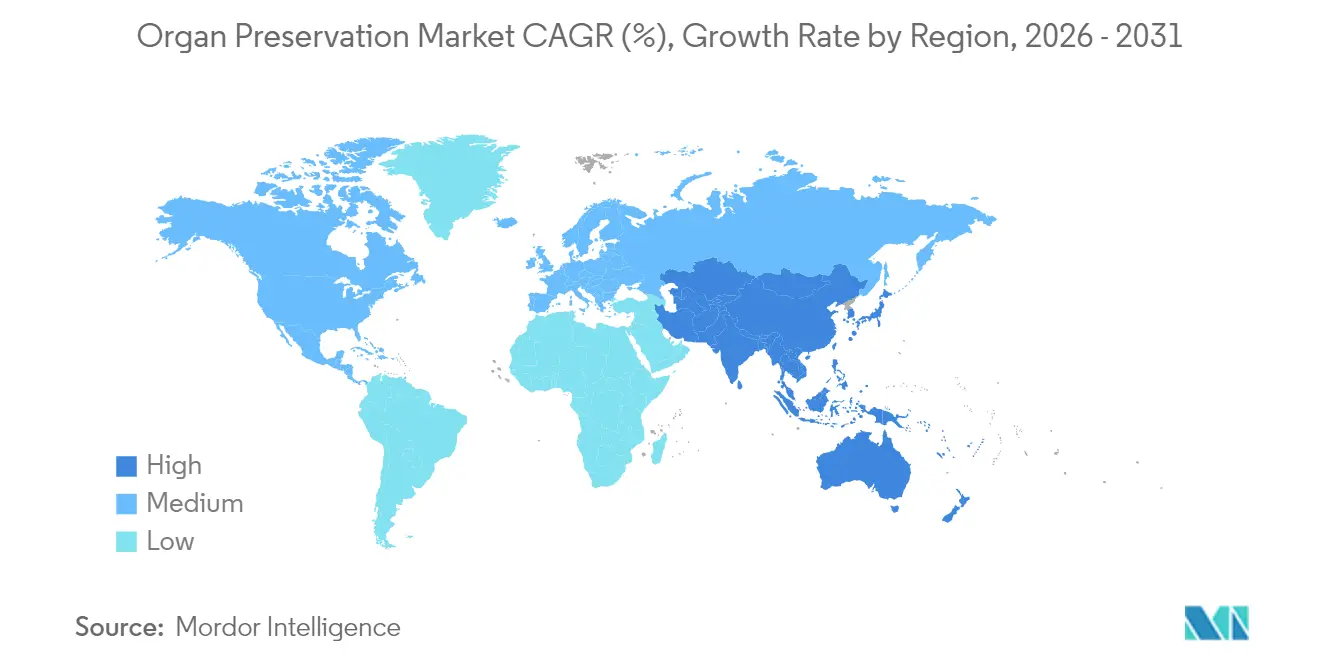

- By geography, North America led with 36.55% revenue share in 2025, but Asia-Pacific is forecast to post a 10.49% CAGR to 2031.

- By end user, Transplant Centers held 42.35% revenue share in 2025, whereas Organ Procurement Organizations are projected to record the highest 11.10% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Organ Preservation Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Multi-Organ Failure In Ageing Population | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Technological Advancements In Preservation Techniques & Devices | +1.5% | Global, led by North America & Europe | Medium term (2-4 years) |

| Increasing Government & NGO Initiatives For Organ Donation | +1.2% | Global, with strongest impact in Asia-Pacific | Medium term (2-4 years) |

| Expansion Of Transplant Program Capacity Worldwide | +1.0% | Global, with rapid growth in Asia-Pacific | Long term (≥ 4 years) |

| Emergence Of Reimbursement Codes For Ex-Vivo Perfusion | +0.8% | North America & Europe | Short term (≤ 2 years) |

| AI-Driven Organ Viability Analytics For Marginal Donors | +0.7% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Multi-Organ Failure in Aging Populations

Life expectancy gains have enlarged the cohort older than 65, a group increasingly eligible for transplantation thanks to evidence showing comparable post-operative outcomes when frailty is managed. Chronic kidney disease, diabetes, and cardiovascular disorders all scale with age, lifting demand for reliable preservation that can cope with longer work-ups typical in geriatric cases. Hospitals therefore prefer solutions that protect organs during extended cold ischemia and offer functional assessment before implantation. Static cold storage remains widespread, yet machine perfusion’s ability to resuscitate marginal grafts is especially valuable when donor age rises. Transplant protocols now include geriatric assessment tools, reinforcing the need for flexible preservation windows that accommodate complex surgical schedules.

Technological Advancements in Preservation Techniques and Devices

Machine perfusion keeps donor organs at physiologic temperature, cutting primary graft dysfunction from 28% to 11% in recent heart studies. Donation-after-circulatory-death (DCD) hearts, once rarely used, are now feasible at scale under normothermic regional perfusion, with 606 U.S. cases recorded across 49 organ-procurement organizations[1]JAMA Network Open, “Normothermic Regional Perfusion Experience of Organ Procurement Organizations in the US,” jamanetwork.com. Device makers integrate GPS tracking, pressure regulation, and temperature telemetry so that teams receive live alerts during transport. Cryopreservation research, such as X-Therma’s protein-mimetic ice blockers, aims to shift preservation from hours to weeks. These innovations collectively shorten allocation times, lower discard rates, and help surgeons expand donor criteria.

Increasing Government and NGO Initiatives for Organ Donation

The World Health Assembly adopted Resolution WHA77.4 that calls for every member state to meet transplant needs by 2035. In the United States, the HRSA OPTN Modernization Initiative modernizes allocation software and sets performance metrics for organ-procurement organizations. Medicare’s Increasing Organ Transplant Access Model mandates 2025 participation and ties hospital payments to higher kidney transplant volumes[2]Centers for Medicare & Medicaid Services, “Increasing Organ Transplant Access Model,” cms.gov. China’s centralized allocation platform (COTRS) now covers every donation, boosting transparency and uptake across 35 transplant hubs. Month-long public campaigns such as National Donate Life Month enlisted 170 million registered U.S. donors in 2025.

Emergence of Reimbursement Codes for Ex-Vivo Perfusion

The CMS rule set published in 2024 establishes unique payment bundles for ex-vivo perfusion disposables and professional services, effective July 2025. Early adopters among U.S. transplant centers report quicker internal approvals for Organ Care System devices because cost recovery is now predictable. European health systems are piloting similar codes within Diagnosis-Related Group updates, spurring purchasing committees to reassess machine perfusion adoption timelines. Insurers increasingly recognize that a USD 30,000 perfusion kit can avert graft loss that would otherwise trigger a USD 400,000 re-transplant. As payer clarity expands, device manufacturers are scaling production lines to meet anticipated demand spikes, which could narrow price differentials with cold-storage supplies.

Restraints Impact Analysis of Organ Preservation Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Organ Transplantation & Preservation Devices | -1.5% | Global, most acute in developing markets | Long term (≥ 4 years) |

| Limited Insurance Reimbursement For Organ Preservation | -1.2% | North America & Europe | Medium term (2-4 years) |

| Supply-Chain Constraints For Proprietary Solutions | -0.8% | Global, with critical impact in remote regions | Short term (≤ 2 years) |

| Regulatory Uncertainty For Novel Normothermic Perfusion | -0.7% | Global, led by regulatory complexity in Europe & Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Transplantation and Preservation Devices

Milliman estimates that total transplant episode expenses grow 5.2% annually for patients under 65, and 9.1% for older cohorts. The Organ Care System Heart requires hospital capital outlays above USD 250,000, and each disposable set adds roughly USD 40,000 per procedure. Preservation solutions also vary widely: University of Wisconsin solution costs USD 120 per liter versus USD 10 for Marshall’s formulation, pressuring cost-conscious hospitals despite equivalent graft survival scores in select cohorts. Developing regions therefore lag in NMP adoption, prolonging reliance on static cold storage. Budget limitations can also delay staff training and certification, which are prerequisite for advanced device use and data reporting.

Regulatory Uncertainty for Normothermic Perfusion

Normothermic devices traverse a patchwork of global frameworks. The FDA review spanned 5,518 days for the Organ Care System Heart, highlighting protracted evidence requirements. In Europe, Advanced Therapy Medicinal Product rules introduce added checkpoints for solutions infused with biologics, slowing multicountry trials. Asia-Pacific regulators still lack harmonized guidance for ex-vivo perfusion, causing device makers to file sequentially instead of concurrently. Without predictable timelines, venture investors price higher risk into funding terms, which can limit R&D budgets for next-generation platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Organ Preservation Market Segment Analysis

By Technique:

Cold Storage Dominance ChallengedStatic Cold Storage retained 61.80% share of the organ preservation market in 2025 because of its simplicity, low cost, and decades-long validation in every transplant program. Even so, delayed graft function remains more frequent with extended criteria donors, prompting centers to trial perfusion add-ons that refresh metabolic substrates during transport. The organ preservation market size attributable to Static Cold Storage will grow modestly but cede share as perfusion adoption outpaces baseline growth.

Normothermic Machine Perfusion is projected to grow 10.31% annually through 2031 as multicenter data show 94% six-month heart graft survival versus 91% for ice storage. Hypothermic variants serve kidneys well by minimizing perfusate cost yet delivering measurable gains in delayed graft function, especially for extended criteria grafts. Regional perfusion in situ is rising too, with 606 U.S. DCD cases reported by 2024. The converging toolkit allows surgeons to sequence cold storage, hypothermic perfusion, and normothermic phases, tailoring methods to donor physiology and travel distance.

By Preservation Solution:

UW Leadership Under PressureUniversity of Wisconsin Solution accounted for 45.10% of the organ preservation market share in 2025. Its hyperosmolar, antioxidant-rich profile minimizes cellular edema and free-radical damage, establishing default use across kidneys, livers, and pancreas grafts. However, high potassium content and viscosity complicate pediatric use, inviting alternatives.

Custodiol HTK is expanding 9.18% CAGR on the appeal of low viscosity and cost parity for multi-organ procurement, with trials confirming similar liver graft survival to UW but simplified flushing protocols. Celsior targets cardiac grafts while Perfadex Plus remains standard for lungs, and new antioxidant-enhanced formulations under clinical review seek to further cut ischemia reperfusion injury. Specialized perfusates for machine perfusion, including proprietary oxygen carriers, represent an incremental revenue tier that supports premium pricing in the organ preservation market.

By Product Type:

Solutions Dominance Faces Device InnovationPreservation Solutions still delivered 49.30% share of the organ preservation market size in 2025 because every transplant, regardless of technology tier, requires a validated solution. That baseline demand keeps volume steady even as device categories accelerate. Manufacturers are reformulating solutions to lower potassium, add antioxidants, and extend shelf life, while digital supply-chain features maintain cold-chain integrity.

Transport Systems & Devices register the fastest 9.12% CAGR, led by Paragonix SherpaPak, LIVERguard, and BAROguard platforms that log GPS coordinates, internal temperature, and pressure in real time. A SherpaPak study covering 569 heart transplants showed a 54% mortality reduction at four years compared with ice storage. Device makers now bundle accessories and cloud analytics that forecast graft viability, turning hardware into recurring-income ecosystems. This software-embedded model attracts capital, as evidenced by Getinge’s USD 477 million buyout of Paragonix in 2024.

By Organ Type:

Kidney Dominance Meets Lung InnovationKidneys made up 58.25% share of the organ preservation market size in 2025 because they constitute the largest transplant volume and enjoy robust reimbursement frameworks. Even so, 20% of deceased-donor kidneys are still discarded due to ischemic injury and logistics bottlenecks. Machine perfusion that permits viability scoring is helping centers accept marginal kidneys and slash discard rates, thereby protecting kidney segment volume in the face of rising comorbidities.

Lungs record the highest 10.48% CAGR thanks to breakthroughs like the HOPE technique that extends safe storage to 20 hours at 12 °C after normothermic perfusion. The continuous distribution allocation policy in the United States raised lung transplant counts 16% within a year, underscoring how preservation innovation amplifies allocation efficiency. Baroguard’s automated pressure control eliminates barotrauma risk during hypothermic transport, and early registry data indicate fewer primary graft dysfunction events relative to ice storage.

By End User:

OPOs Drive Efficiency RevolutionTransplant Centers controlled 42.35% revenue in 2025 because they purchase both solutions and capital equipment, dictate protocol standards, and receive direct reimbursement. Centers now benchmark graft-survival metrics to qualify for performance incentives under emerging value-based payment models.

Organ Procurement Organizations form the fastest-growing end user group at 11.10% CAGR. Normothermic regional perfusion allows OPO teams to recover three organs per DCD donor versus one when using static cold protocols. To scale that benefit, 95% of U.S. OPOs report the need for standardized training and device access. Hospitals and specialty clinics remain cost-sensitive but may accelerate adoption once payer frameworks stabilize and disposables pricing falls.

Geography Analysis

North America Organ Preservation Market

North America retained 36.55% share of the organ preservation market in 2025, underpinned by advanced infrastructure, the OPTN mandate to reach 60,000 annual transplants by 2026, and supportive reimbursement for perfusion. Widespread clinical trials, FDA device clearances, and robust donor-registration campaigns sustain first-mover advantage. Canada’s universal health coverage ensures demand continuity, while Mexico’s device imports rise as public hospitals expand transplant services.

Europe Organ Preservation Market

Europe exhibits steady but slower growth. Germany, France, Italy, Spain, and the United Kingdom lead adoption, yet cost-effectiveness assessments exert downward pressure on device prices. The European Society for Organ Transplantation’s roadmap for Advanced Therapy Medicinal Products spotlights regulatory caution that may defer rollouts for biologic-enhanced perfusates. Nonetheless, cross-border procurement networks in Eurotransplant and Scandiatransplant regions rely on high-performance transport systems to cover long-haul drives between donor and recipient hospitals.

APAC Organ Preservation Market

Asia-Pacific is the fastest-growing region, posting a 10.49% CAGR as transplant program capacity accelerates across China, India, and Japan. China’s COTRS platform legitimized voluntary donation and raised public trust, while new liver units achieve procurement rates comparable to mature Western centers. India’s rising medical tourism, coupled with domestic manufacturing incentives for perfusion devices, adds volume and price competition. Japan’s aging population creates high kidney and heart demand, and public insurers increasingly reimburse NMP in pilot projects.

Mordor Intelligence provides coverage of the organ preservation market across other key regional markets, including Europe and Middle East, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Regulation for organ preservation products spans medical-device rules plus organ quality and safety requirements that govern procurement, transport, and traceability. In the United States, the FDA (CDRH) regulates perfusion and transport devices under risk-based pathways, including PMA for higher-risk systems such as OrganOx metra (PMA P200035) and De Novo classification for novel platforms (for example, DEN250009 in January 2026). FDA guidance addressing investigational device exemptions for hypothermic flushing, transport, and storage, and the use of animal studies to evaluate organ preservation devices, shapes trial design and evidence packages for market entry.

In Europe, market access is framed by EU Medical Device Regulation (EU) 2017/745 (MDR) for device safety and performance, alongside Directive 2010/53/EU on the quality and safety of organs for transplantation. Practice and quality benchmarks are reinforced by the Council of Europe/EDQM “Guide to the quality and safety of organs for transplantation” (9th edition, 2025), which is used as a reference for procurement, preservation, and transport processes, and sets compliance expectations for manufacturers supplying devices and solutions into multi-country transplant networks.

Competitive Landscape

The organ preservation market features moderate fragmentation punctuated by strategic acquisitions. Getinge’s USD 477 million purchase of Paragonix delivers a full suite of organ-specific transport devices and a global sales footprint. TransMedics dominates normothermic perfusion platforms and reported 64% revenue expansion in Q3 2024 with plans to surpass 10,000 annual OCS procedures by 2028.

Investment trends favor organ-specific optimization and data-rich ecosystems. OrganOx secured USD 142 million to commercialize the Metra liver device and support randomized trials across Asia and North America. Vivalyx raised EUR 5.4 million (USD 6.24 million) for organ vitality solutions that interface with AI-driven assessment platforms. Patent-extension rulings for OCS Heart and Liver underscore long regulatory journeys, increasing barriers to entry for smaller contenders.

Competition now hinges on clinical evidence. Paragonix posted a 27% reduction in post-transplant complications with LIVERguard, fueling hospital conversions. Bridge to Life bought Medica’s VitaSmart perfusion system to integrate continuous viability analytics in liver platforms. Large companies leverage service contracts, training modules, and cloud dashboards to lock in customers for disposables and software subscriptions, creating high switching costs for transplant centers.

Organ Preservation Industry Leaders

XVIVO Perfusion AB

Organ Recovery Systems Inc.

TransMedics Inc.

Getinge AB

OrganOx Limited

- *Disclaimer: Major Players sorted in no particular order

Organ Preservation Market Companies Covered in this Report

- Xvivo Perfusion

- Organ Recovery Systems

- Getinge

- Bridge to Life Ltd.

- TransMedics Inc.

- 21st Century Medicine

- Dr. Franz Kohler Chemie GmbH

- Essential Pharmaceuticals LLC

- Waters Medical Systems

- Organox

- CryoLife

- BioLife Solutions

- Preservation Solutions Inc.

- Lifeline Scientific

- Vascular Perfusion Solutions Inc.

- KARA Perfusion

- EBERS Medical Technology SL

Market Opportunities and Future Outlook

The near-term whitespace centers on operationalizing dynamic preservation across more organs and more geographies, moving beyond static cold storage protocols that still dominate daily workflows. In the United Kingdom, NHS Blood and Transplant announced in November 2025 that normothermic regional perfusion (NRP) would be introduced as routine practice, supported by Department of Health and Social Care funding starting April 2026. That rollout pathway draws through demand for perfusion consumables, training, and retrieval-center capability upgrades. At the same time, payer and policy actions such as CMS payment bundles effective July 2025 for ex-vivo perfusion disposables and services continue to reduce internal approval friction at transplant centers by improving the predictability of cost recovery.

Clinical and translational evidence is also expanding room in underpenetrated segments such as pancreas, as well as in longer-distance, longer-duration logistics where viability assessment becomes more relevant. In July 2026, the University of Oxford reported a milestone in its Hypothermic Oxygenated Pancreas Perfusion (HOPP) study, with a study participant receiving a perfused human pancreas, signaling progress toward routine pancreas perfusion workflows that can complement or displace cold storage in selected cases. Alongside these milestones, industry efforts are shifting toward integrated ecosystems (device plus monitoring plus logistics) that support daytime surgery scheduling, “back-to-base” retrieval models, and standardized viability analytics, particularly for marginal donors where discard reduction improves throughput for OPOs and transplant centers.

Recent Industry Developments in Organ Preservation Market

- July 2026: TransMedics Group, Inc. completed its strategic investment in PAD Aviation service GmbH to build a dedicated European organ transplant air logistics network. The investment extends the company’s National OCS Program operating model beyond the United States and strengthens end-to-end control over time-critical transport for perfused organs.

- May 2026: XVIVO Perfusion AB announced that ANSM in France granted reimbursement for machine perfusion of donated hearts, following a regulatory derogation in December 2025. Reimbursement clarity supports hospital budgeting for perfusion disposables and can accelerate routine use of machine perfusion in cardiac transplant pathways.

- June 2024: Paragonix launched PancreasPak, an FDA-cleared pancreas transport device designed to maintain controlled temperature for extended preservation. This broadened organ-specific transport options and reinforced the shift from improvised ice storage toward validated, monitored shipping systems.

Organ Preservation Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers products used to keep donated solid organs viable between procurement and implantation, mainly through preservation solutions, transport systems, and perfusion-based preservation equipment used by transplant programs.

Scope exclusions: Tissue, blood, and cell preservation products, transplant drugs, and long-term biobanking equipment are excluded.

Segments Covered in This Report

- By Technique

- Static Cold Storage (SCS)

- Hypothermic Machine Perfusion (HMP)

- Normothermic Machine Perfusion (NMP)

- By Preservation Solution

- University of Wisconsin (UW) Solution

- Custodiol HTK Solution

- Celsior

- Perfadex Plus

- Others

- By Product Type

- Preservation Solutions

- Transport Systems & Devices

- Accessories & Monitoring Software

- By Organ Type

- Kidneys

- Liver

- Lung

- Heart

- Pancreas

- Others

- By End User

- Transplant Centers

- Hospitals

- Organ Procurement Organizations (OPOs)

- Specialty Clinics & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand pool and the clinical activity context, before the market model was built. Public sources such as national transplant registries, organ donation and procurement authority dashboards, and health statistics portals were reviewed to understand transplant volumes by organ and how they are trending.

We also relied on sources such as peer reviewed transplant journals, medical device regulatory databases (for cleared preservation systems and solutions), and customs or trade statistics where relevant to cross check import patterns of specialized devices and consumables. Along with this, company filings, investor presentations, and reputable press coverage were used to understand product positioning, pricing direction, and recent launches. Where helpful, paid subscriptions for company financials and intelligence, patent databases, and shipment level import/export databases were used to validate select assumptions. These desk research sources are illustrative and not exhaustive, and many other public references were used for data collection, cross checks, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually purchased and used per transplant workflow, since product usage can vary by organ type and by center protocol. We spoke with a mix of transplant surgeons, procurement teams, perfusion specialists, and executives across suppliers and distributors, and then used their input to confirm adoption levels of machine perfusion versus static cold storage, typical replacement cycles, and real world price ranges across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 50% |

| Mid tier: 51% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 18% | Managers: 46% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts from a top-down build that reconstructs demand using transplant procedure volumes and the typical preservation pathway used for each organ, which is then converted into value using observed pricing for solutions, disposables, and system usage. The model is kept practical by anchoring it to measurable indicators such as annual solid organ transplant counts, organ mix shifts (kidney versus liver versus heart and lung), share of machine perfusion adoption, average solution volume used per case, and replacement or service patterns for transport and perfusion equipment.

To ensure the totals do not drift, we corroborate the results with selective bottom-up checks, such as supplier revenue signals where publicly visible, sampled price points from procurement discussions, and channel feedback on shipment cadence for consumables. When a bottom-up data point is missing in a country, proxies are applied using procedure intensity, hospital capability, and adoption stage, and then adjusted through expert feedback. Forecasting is based on scenario analysis supported by transplant waitlist pressure, expected growth in donation programs, improving utilization of extended criteria organs, and the pace of policy and reimbursement support, which are then stress-tested with what respondents expect to change over the next few years.

Data Validation & Update Cycle

Model outputs are checked against independent signals, including transplant registry totals, regional procedure growth, and the expected split between cold storage and machine perfusion use. Outliers are investigated, and assumptions like adoption rates and average selling prices are re-checked with follow-up calls when the variance is material.

Before sign-off, the work goes through multiple analyst reviews that look for arithmetic errors, inconsistent year labels, and country totals that do not match the demand logic. The report is refreshed annually, and interim updates are made when major regulatory actions, product launches, or sharp pricing changes are observed. Right before delivery, a final pass is completed so clients receive the latest updated view available at that time.

Mordor Intelligence's Organ Preservation Market Estimate Compared With Other Published Estimates

Published market sizes for organ preservation do not always line up, even when the topic name looks the same, because the included products and year conventions often differ. Differences also come from how each publisher converts clinical activity into revenue, and how often the inputs are refreshed when transplant volumes or pricing shifts.

Transplant drugs and long-term biobanking equipment sit outside Mordor Intelligence's scope, which can lower the total versus estimates that group adjacent transplant care spending into the same number. Other gaps usually come from whether machine perfusion system value is counted as equipment only or as ongoing disposable usage, how quickly average selling prices are stepped up, and whether currency conversion uses a single-year rate or an average across the period.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 336.55 M (2025) | |

| Global Consultancy A | USD 323.83 M (2025) | Uses a different base year setup and a longer forecast window, and scope language is less clear on whether device disposables and transport components are consistently counted across regions, which can compress the 2025 total. |

| Industry Publisher B | USD 291.20 M (2025) | Anchors the model to a 2024 base and carries forward a narrower revenue pool, and the translation from transplant volumes to per-case spending can undercount higher-value machine perfusion usage in markets where adoption is accelerating. |

Looking across the figures, the spread is mainly explained by what gets bundled into the market and how device plus consumable value is treated over time. When scope is kept tight to organ viability products and the model is tied back to transplant activity and adoption indicators, the resulting number is easier to trace, repeat, and update when new clinical and pricing signals come in.

Key Questions Answered in the Report

What is the current value of the organ preservation market?

The organ preservation market size stands at USD 357.62 million in 2026.

Which preservation technique is growing fastest?

Normothermic Machine Perfusion is expected to advance at a 10.31% CAGR through 2031.

Why is Asia-Pacific the most attractive growth region?

Rapid expansion of transplant programs, regulatory modernization, and growing donor registration drive a 10.49% CAGR in Asia-Pacific.

How do reimbursement models influence technology adoption?

New CMS payment bundles cover ex-vivo perfusion disposables, encouraging hospitals to adopt machine perfusion devices.

Which company leads in transport devices?

Paragonix Technologies, now under Getinge, offers SherpaPak, LIVERguard, and BAROguard systems with documented survival benefits.

Page last updated on: