Organoids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 3.29 Billion |

| Growth Rate (2026 - 2031) | 18.31% CAGR |

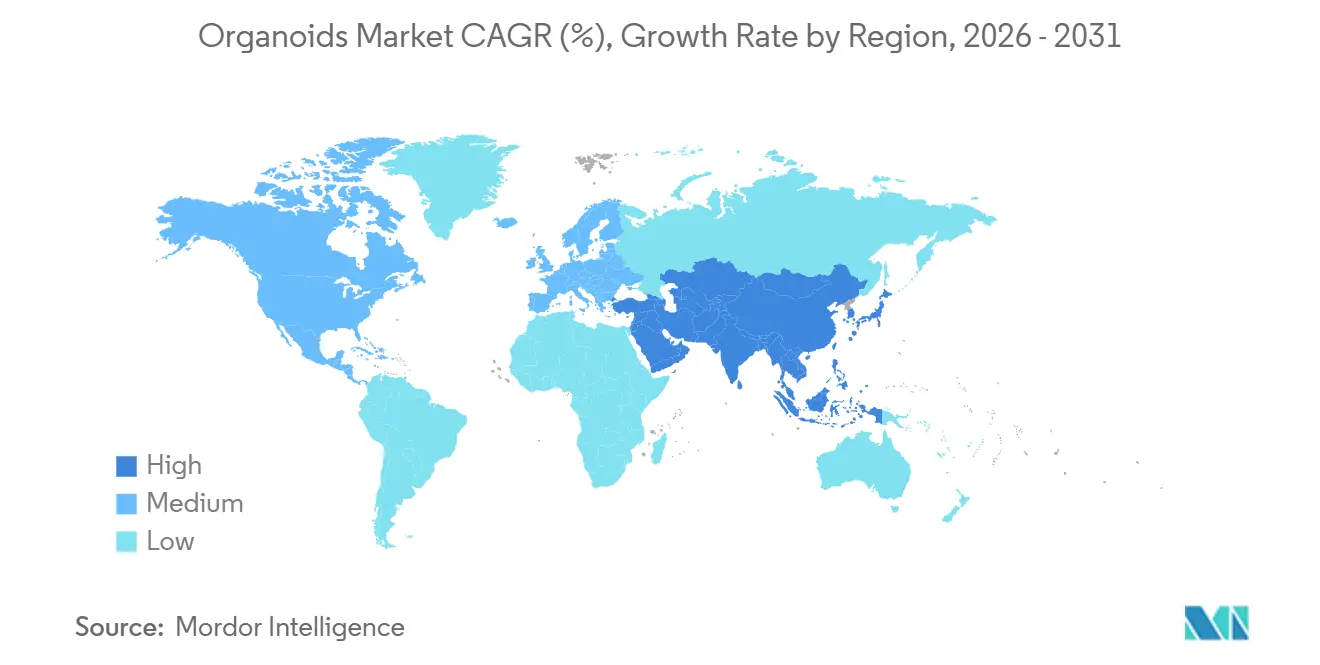

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

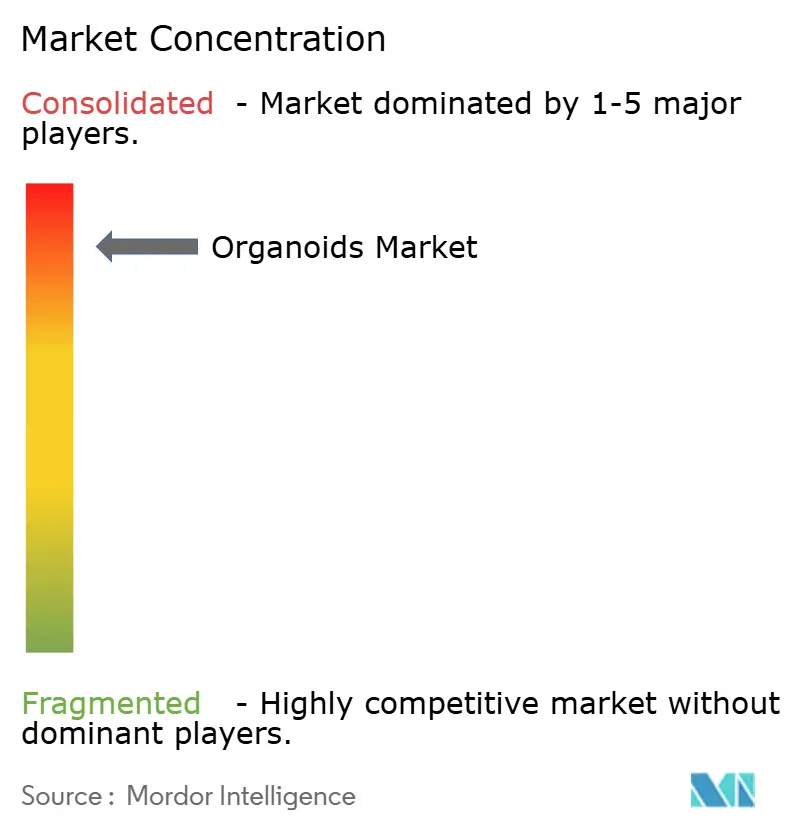

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organoids Market Analysis by Mordor Intelligence

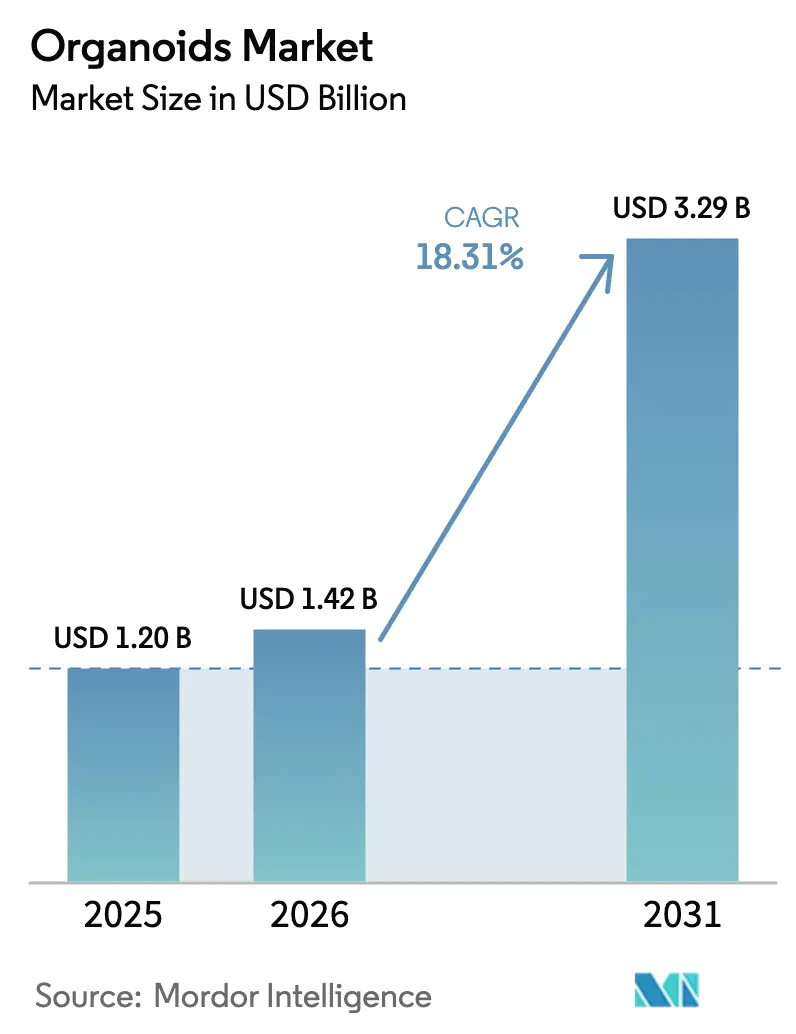

The Organoids Market size is projected to expand from USD 1.20 billion in 2025 and USD 1.42 billion in 2026 to USD 3.29 billion by 2031, registering a CAGR of 18.31% between 2026 to 2031.

Rising investment by pharmaceutical sponsors in three-dimensional patient-derived cultures, the elimination of mandatory animal studies in the United States, and parallel guideline workstreams in Europe are accelerating demand for preclinical organoid packages. Venture funding continues to pour into start-ups that supply bioprinted matrices and microfluidic chips, while established life-science suppliers broaden reagent portfolios to lock in recurring media revenue. Cost pressures linked to animal-derived extracellular matrices persist, yet suppliers are releasing chemically defined substitutes that promise lower batch-to-batch variability. Overall, the organoids market is shifting from an academic niche toward an integrated development platform that compresses timelines, de-risks oncology programs, and unlocks value in precision medicine trials.

Key Report Takeaways

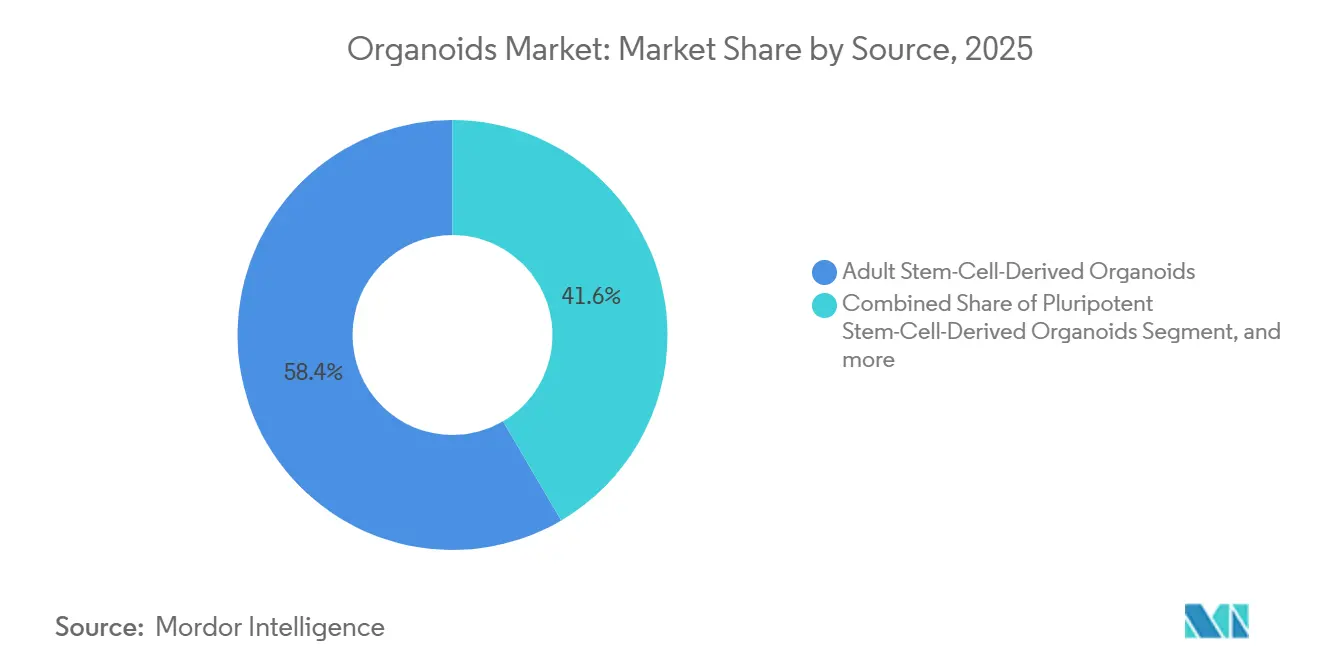

- By source, adult stem-cell-derived models led with 58.43% of the organoids market share in 2025.

- By organ type, intestinal cultures accounted for a 28.65% slice of the organoids market size in 2025, while pancreas models are set to expand at a 20.76% CAGR through 2031.

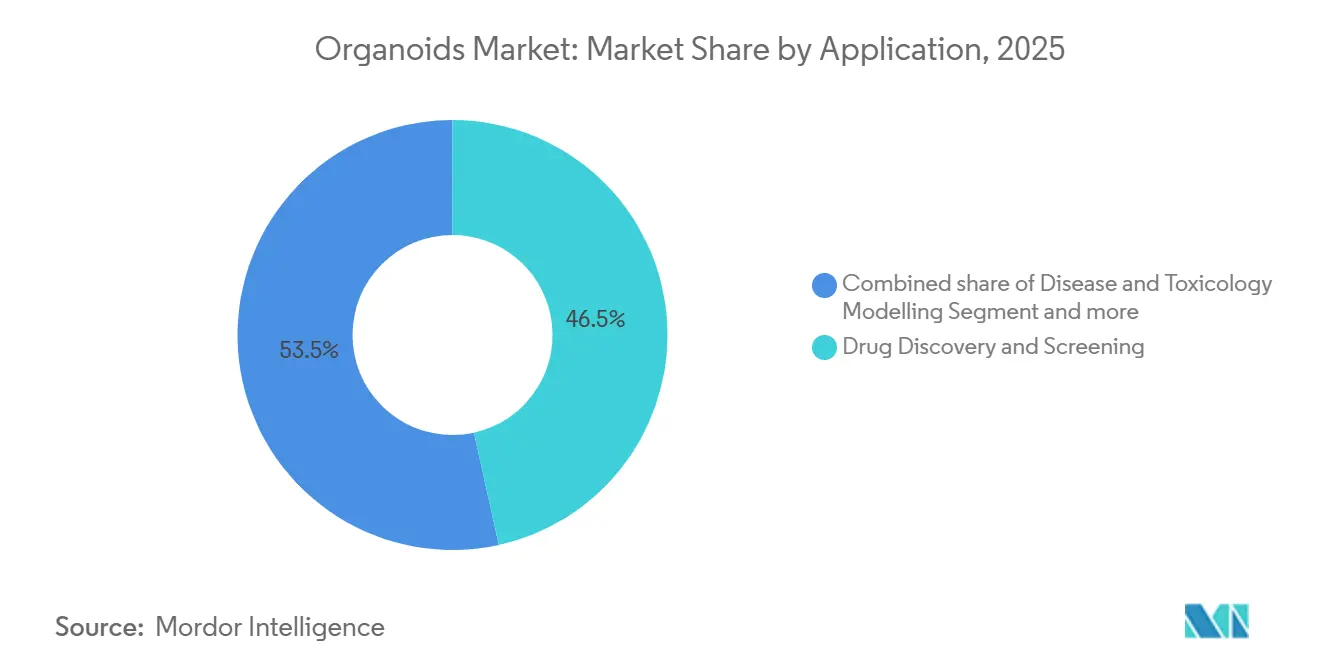

- By application, drug discovery and screening accounted for 46.54% of revenue in 2025; precision and personalized medicine are poised to grow at a 21.55% CAGR through 2031.

- By end user, pharmaceutical and biotech companies accounted for 55.63% of 2025 spending, whereas CROs and CDMOs are forecast to grow at a 21.65% CAGR over 2026-2031.

- By technology, scaffold-based 3-D culture accounted for 32.65% of 2025 revenue; 3-D bioprinting-assisted organoids are projected to post a 21.43% CAGR through 2031.

- By geography, North America dominated with 43.65% 2025 revenue; Asia-Pacific is anticipated to register a 19.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organoids Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of organoids in oncology drug discovery | +4.2% | North America, Europe | Medium term (2-4 years) |

| Expansion of precision medicine trials and personalized therapies | +3.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Government funding for 3-D cell-culture infrastructure | +3.1% | United States, European Union, China | Short term (≤2 years) |

| Shift away from animal testing in preclinical research | +2.9% | Global (led by United States & Europe) | Short term (≤2 years) |

| Commercialization of large-scale organoid biobanks | +2.4% | North America, Europe, early-adopter APAC markets | Long term (≥4 years) |

| Integration of gene-editing and advanced microfluidics platforms | +2.1% | Global innovation hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Organoids in Oncology Drug Discovery

Colorectal tumor organoids predicted chemotherapy response in 84% of cases during a 2025 Nature Medicine study, outperforming traditional cell lines and spurring broader pharmaceutical uptake[1]Nature Medicine Editors, “Organoids Predict Chemotherapy Response,” nature.com . Roche’s 2025 annual report disclosed an internal biobank exceeding 1,000 patient-derived models spanning 12 tumor types, which now underpins lead-optimization screens. The U.S. National Cancer Institute allocated USD 100 million to the Human Tumor Atlas Network, which created spatial transcriptomic maps that integrate with organoid assays to inform combination-therapy design. Sponsors report preclinical timeline compression of 6-12 months and lower late-stage attrition, reinforcing return on R&D capital. These gains strengthen the economic rationale that propels the organoids market toward routine oncology workflows.

Expansion of Precision Medicine Trials and Personalized Therapies

Organoid-guided interventions raised objective response rates by 23 percentage points in relapsed pediatric solid tumors at the Princess Máxima Center, a data point that convinced Dutch insurers to test reimbursement pathways[2]Princess Máxima Center, “Organoid-Guided Therapy Study,” prinsesmaximacentrum.nl. Japan’s Ministry of Health, Labour and Welfare cleared the first companion diagnostic based on patient-derived cultures in March 2025, providing a 14-day functional readout unattainable with histopathology alone. Basket trials now embed organoid assays to enroll patients with shared molecular targets, shrinking screening costs and accelerating recruitment in rare oncology indications. As payers tighten evidence standards, functional response data generated by organoids further underpins reimbursement negotiations, boosting adoption in the organoids market.

Government Funding for 3-D Cell Culture Infrastructure

The U.S. National Institutes of Health directed USD 48 million to Tissue Chip for Drug Screening in fiscal 2025 to couple organoids with perfused microfluidics. Horizon Europe earmarked a slice of its EUR 95 billion research envelope for in-vitro models that reduce animal use, adding momentum on the continent. China’s Ministry of Science and Technology has invested CNY 500 million in regional centers to harmonize protocols and train researchers, lowering the entry barrier for small enterprises[3]Ministry of Science and Technology of China, “Organoid Center Initiative,” most.gov.cn. Public investment spreads fixed costs across academia and industry, creating a pipeline of skilled personnel and standardized reagents that sustains long-term growth in the organoids market.

Shift Away from Animal Testing in Preclinical Research

The U.S. FDA Modernization Act 2.0 removed the statutory animal-testing mandate in December 2022, formally recognizing organoid-based data in new drug applications. The European Chemicals Agency followed with 2024 guidance covering organoid assays for skin sensitization and hepatotoxicity. A Johns Hopkins analysis estimated 30-40% cost savings when sponsors replace animal studies with organoids, coupled with 12-18 month timeline reductions. Industry consortia are now standardizing assay protocols to facilitate multi-site validation, a prerequisite for broader regulatory acceptance, thereby fueling additional organoids market expansion.

Restraint Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of specialized matrices and growth factors | -2.7% | Global, most acute in emerging markets | Short term (≤2 years) |

| Lack of standardized reproducibility protocols | -2.3% | Global, affecting regulatory submissions | Medium term (2-4 years) |

| Ethical and regulatory ambiguity around complex human models | -1.8% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Limited cold-chain logistics for live organoid transport | -1.2% | Global, especially cross-border collaborations | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Cost of Specialized Matrices and Growth Factors

Matrigel ranges from USD 400–600 per milliliter, and large screens often require 5–10 milliliters, pushing reagent bills to USD 6,000 per experiment. Essential recombinant proteins such as R-spondin and Wnt3a cost another USD 300–800 per milligram, with high turnover owing to short half-lives. A 2024 ISSCR survey found 62% of respondents citing reagent expense as a primary barrier, prompting some labs to revert to two-dimensional models. Suppliers are rolling out animal-free hydrogels and bulk-pricing schemes, but cost compression remains incremental, holding back uptake in resource-constrained regions and thereby tempering the organoids market growth rate.

Lack of Standardized Reproducibility Protocols

A Cell Stem Cell multicenter study revealed up to 40% variability in morphology and gene expression across eight labs using ostensibly identical intestinal-organoid protocols. Absent harmonized quality metrics, sponsors struggle to meet evidentiary requirements, delaying filings. The European Medicines Agency convened a 2024 workshop yet does not expect formal guidance until 2027, leaving a multi-year gap. Voluntary initiatives such as the Organoid Standards Initiative seek to create reference materials, but adoption hinges on resources often lacking in smaller labs, constraining scale-up in the organoids market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Tumor-Derived Models Gain Traction

Adult stem-cell-derived organoids anchored 58.43% of 2025 revenue by offering well-validated gastrointestinal and hepatic models that regulators recognize. Pluripotent stem-cell lines supply developmental and rare-disease insights, although longer differentiation timelines limit throughput. Tumor-derived cultures are forecast to log a 20.65% CAGR through 2031, the fastest-growing slice of the organoids market. Novartis now maintains more than 800 patient-derived lines across 15 tumor types, enabling parallel drug screens that shorten lead optimization windows. Nature Biotechnology reported in 2025 that tumor organoids retained genomic fidelity across 10 passages, validating stability for longitudinal studies. As biobanking expands, tumor-derived models are positioned to overtake adult stem-cell lines in absolute revenue within a decade, underscoring the strategic shift toward precision oncology.

The convergence of CRISPR gene editing with tumor organoids supports synthetic-lethal discovery, while AI-enabled imaging accelerates phenotypic readouts. These advances align with pharmaceutical demand for earlier proof-of-concept, reinforcing structural growth in this source segment of the organoids market. Proprietary culture media tailored to tumor lineages promise additional recurring revenue for suppliers, although cost containment remains essential to penetrate mid-tier pharma budgets. Consequently, competitive differentiation is migrating toward service bundles that integrate derivation, screening, bioinformatics, and regulatory support into a single contract.

By Organ Type: Pancreas Organoids Surge

Intestinal models captured 28.65% of organ-type revenue in 2025 through applications spanning inflammatory bowel disease, microbiome studies, and enteric pathogen assays. Liver organoids excel in hepatotoxicity screens, while brain models, despite culture complexity, enable neurodevelopmental research. Pancreas models are projected to book a 20.76% CAGR over 2026-2031, the strongest trajectory inside this segmentation. A 2024 Cell Metabolism study demonstrated faithful recapitulation of beta-cell insulin secretion defects, advancing diabetes drug pipelines. The Cystic Fibrosis Foundation’s USD 15 million outlay in 2025 expanded its pancreatic organoid repository to 500 patient samples, facilitating CFTR modulator testing.

Suspension bioreactors now enable centimeter-scale pancreatic cultures, opening potential for cell-therapy seed stocks. As regulatory agencies evaluate clinical-grade manufacturing protocols, pancreas organoids gain strategic relevance for both drug screening and regenerative approaches. Suppliers that master scale-up technologies will secure early-mover advantage in this high-growth pocket of the organoids market size.

By Application: Precision Medicine Accelerates

Drug discovery and screening generated 46.54% of 2025 revenue, reflecting entrenched pharmaceutical reliance on organoids to truncate target-validation cycles. Disease modeling and toxicology round out legacy demand channels, but the precision-medicine slice is expected to deliver a 21.55% CAGR through 2031. Dutch insurers already reimburse organoid-guided therapy selection in pediatric oncology, a precedent likely to ripple outward as more health systems link payment to functional response data. Japan’s companion-diagnostic approval underscores regulatory alignment, further widening clinical adoption.

Growing clinical demand spurs investments in high-throughput functional assays and fast data-analysis pipelines, creating a feedback loop that enlarges organoids market size within the healthcare delivery value chain. Hybrid business models—combining service fees, licensing, and data monetization—are emerging as clinics integrate organoid readouts into electronic health records, positioning precision medicine as the long-run growth engine.

By End User: CROs and CDMOs Expand Capacity

Pharmaceutical and biotech firms accounted for 55.63% of 2025 spend, yet the 21.65% CAGR forecast for CROs and CDMOs highlights accelerating outsourcing. Charles River injected USD 20 million into organoid infrastructure in January 2025 to broaden screening services. WuXi AppTec rolled out a three-continent service network that spans sample collection through data analytics. Outsourcing appeals to sponsors seeking flexible capacity without heavy capital outlay, especially as assay complexity rises.

Academic centers still drive protocol innovation, but budget constraints push them toward partnerships that tap private capital and industrial process expertise. Hospital-based diagnostics labs increasingly procure turnkey tests from specialty CROs, blurring traditional boundaries and enlarging the overall organoids market.

By Technology: 3-D Bioprinting Gains Momentum

Scaffold-based culture retained 32.65% of 2025 revenue but faces price pressure as synthetic matrices enter the field. 3-D bioprinting, forecast at a 21.43% CAGR, automates layer-by-layer deposition to reduce batch variability. BICO shipped 47 printers in 2025, up 35% year over year, with organoid workflows its fastest-growing use case. Advanced Materials published a 2025 study showing bioprinted liver constructs that maintained albumin production for 28 days, outperforming manually seeded counterparts.

AI-guided process control systems now fine-tune nozzle pressure and extrusion speed in real time, enhancing reproducibility. As microfluidic perfusion integrates with printed constructs, the technology segment positions itself to displace manual scaffold seeding, expanding organoids market share.

Geography Analysis

North America led with 43.65% revenue in 2025, propelled by NIH’s USD 48 million Tissue Chip grants and the FDA’s permissive regulatory stance. Canada injected CAD 12 million into a national biobank while Mexico emerged as a near-shoring destination for contract organoid services catering to U.S. pharma clients. Venture capital concentrations in Boston and the San Francisco Bay Area continue to seed start-ups across matrices, imaging, and bioreactors, underpinning local demand in the organoids market.

Europe benefits from Horizon Europe’s EUR 95 billion framework, with Germany’s Federal Ministry of Education and Research adding EUR 30 million for competence centers that disseminate harmonized protocols. The United Kingdom’s Medical Research Council deployed GBP 18 million to extend its Human Developmental Biology Resource into organoid models, attracting multinational collaborations. France, Italy, and Spain leverage European Structural Funds to support rare-disease applications, expanding regional uptake. Together, these initiatives foster an integrated supply chain that boosts European organoids market competitiveness.

Asia-Pacific is forecast to clock a 19.43% CAGR to 2031. China’s CNY 500 million investment in regional centers seeks to standardize protocols and train personnel. Japan’s approval of an organoid companion diagnostic and South Korea’s KRW 25 billion program expand clinical demand. India lures contract services through lower labor costs, while Australia channels AUD 10 million into biobanks targeting indigenous health. These programs collectively elevate regional capacity, broadening the global organoids market base.

Middle East, Africa, and South America remain nascent but show early signs of infrastructure build-out. Brazil’s São Paulo Research Foundation and South Africa’s Medical Research Council launched pilot initiatives to localize protocols, hinting at future uptake. Export of cryopreserved organoid lines from Europe and North America currently fills supply gaps, indicating early-stage opportunity for logistics providers.

Competitive Landscape

Market concentration is moderate as legacy life-science suppliers extend catalogues while specialized start-ups carve out niches. Thermo Fisher launched animal-free media priced 20% below Matrigel in December 2025, leveraging its global distribution footprint to penetrate cost-sensitive labs. Corning partnered with the Princess Máxima Center to co-develop reference protocols, reinforcing its extracellular-matrix dominance. BICO’s January 2026 acquisition of a German microfluidics firm broadens its platform into organ-on-chip territory, pitting it against Emulate’s perfused systems.

Hubrecht Organoid Technology operates a hybrid licensing-and-service model, while Sartorius doubled bioreactor capacity to meet high-throughput demand. Merck KGaA’s 2025 patent on a synthetic hydrogel underscores an arms race to eliminate animal-derived components, a key cost and reproducibility pain point. Logistics innovators such as Cellesce extend cryopreservation windows to six months, enabling cross-border biobank distribution. Competitive intensity is expected to rise as suppliers converge on turnkey solutions that couple reagents, hardware, and software in seamless workflows, reinforcing platform lock-in across the organoids market.

Organoids Industry Leaders

Merck KGaA

Cellesce Ltd

3Dnamics Inc.

R&D Systems, Inc.

Hubrecht Organoid Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Bio-Techne Corporation, one of the global provider of life science tools, reagents and diagnostic products launched Cultrex Synthetic Hydrogel, a fully defined synthetic extracellular matrix (ECM) designed to support reproducible and scalable 3D stem cell and organoid research.

- December 2025: Pluristyx, Inc. announced the formation of the Organoid COMMONS (Consortium for Organoid Manufacturing, Measurement, Optimization, and Network for Standards), a public-private consortium created to accelerate the adoption of human-relevant organoid models.

- November 2025: ChristianaCare’s Cawley Center for Translational Cancer Research unveiled a first-of-its-kind organoid core in a community cancer center program. The new laboratory facility within the Helen F. Graham Cancer Center & Research Institute grows and tests living, patient-derived tumor models, giving doctors and researchers a faster, more precise way to identify the therapies most likely to work for each patient.

Global Organoids Market Report Scope

As per the scope of this report, organoids are miniature organs resembling the physical and functional properties of the actual organs. These organoids are widely used in clinical research for drug development and drug toxicity evaluation, among other applications.

The Organoids Market is Segmented by Source (Pluripotent Stem-Cell-Derived, Adult Stem-Cell-Derived, and Tumor-Derived Patient), Organ Type (Intestinal, Liver, Brain, Kidney, Lung, Pancreas, Cardiac, and Other), Application (Drug Discovery & Screening, Disease & Toxicology Modelling, Precision & Personalised Medicine, Regenerative Medicine, Organoid Biobanking Services, and Other), End User (Academic & Research Institutes, CROs & CDMOs, Hospitals & Diagnostics Labs, and Pharmaceutical & Biotech Companies), Technology (3-D Bioprinting-Assisted, AI-Guided Automated Platforms, Micro-Fluidic Organ-On-Chip Integrated, Scaffold-Based 3-D Culture, and Suspension / Scaffold-Free Culture), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Pluripotent Stem-Cell-Derived Organoids |

| Adult Stem-Cell-Derived Organoids |

| Tumor-Derived Patient Organoids |

| Intestinal |

| Liver |

| Brain |

| Kidney |

| Lung |

| Pancreas |

| Cardiac |

| Other Organ Types |

| Drug Discovery & Screening |

| Disease & Toxicology Modelling |

| Precision & Personalised Medicine |

| Regenerative Medicine |

| Organoid Biobanking Services |

| Other Applications |

| Academic & Research Institutes |

| CROs & CDMOs |

| Hospitals & Diagnostics Labs |

| Pharmaceutical & Biotech Companies |

| 3-D Bioprinting-Assisted Organoids |

| AI-Guided Automated Platforms |

| Micro-Fluidic Organ-On-Chip Integrated |

| Scaffold-Based 3-D Culture |

| Suspension / Scaffold-Free Culture |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Pluripotent Stem-Cell-Derived Organoids | |

| Adult Stem-Cell-Derived Organoids | ||

| Tumor-Derived Patient Organoids | ||

| By Organ Type | Intestinal | |

| Liver | ||

| Brain | ||

| Kidney | ||

| Lung | ||

| Pancreas | ||

| Cardiac | ||

| Other Organ Types | ||

| By Application | Drug Discovery & Screening | |

| Disease & Toxicology Modelling | ||

| Precision & Personalised Medicine | ||

| Regenerative Medicine | ||

| Organoid Biobanking Services | ||

| Other Applications | ||

| By End User | Academic & Research Institutes | |

| CROs & CDMOs | ||

| Hospitals & Diagnostics Labs | ||

| Pharmaceutical & Biotech Companies | ||

| By Technology | 3-D Bioprinting-Assisted Organoids | |

| AI-Guided Automated Platforms | ||

| Micro-Fluidic Organ-On-Chip Integrated | ||

| Scaffold-Based 3-D Culture | ||

| Suspension / Scaffold-Free Culture | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the organoids market in 2026 and how fast is it growing?

The organoids market size reached USD 1.42 billion in 2026 and is forecast to expand at an 18.31% CAGR through 2031.

Which segment shows the fastest growth inside this field?

Pancreas organoids are projected to post a 20.76% CAGR between 2026 and 2031, outpacing other organ-type segments.

What is driving adoption of organoids in oncology programs?

High predictive accuracy, regulatory acceptance following the FDA Modernization Act 2.0, and pharma initiatives such as RocheÕs 1,000-sample biobank are accelerating oncology use cases.

Why are CROs and CDMOs gaining share?

Sponsors prefer outsourcing complex culture and screening workflows, leading CROs and CDMOs to grow at a 21.65% CAGR through 2031.

How are suppliers addressing the high cost of matrices?

Firms such as Thermo Fisher and Merck KGaA are launching animal-free, chemically defined hydrogels priced below legacy Matrigel to reduce batch variability and reagent expense.

Which regions will expand fastest?

Asia-Pacific is expected to record a 19.43% CAGR as China, Japan, and South Korea invest in standardized organoid centers and companion diagnostics.

Page last updated on: