Longevity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

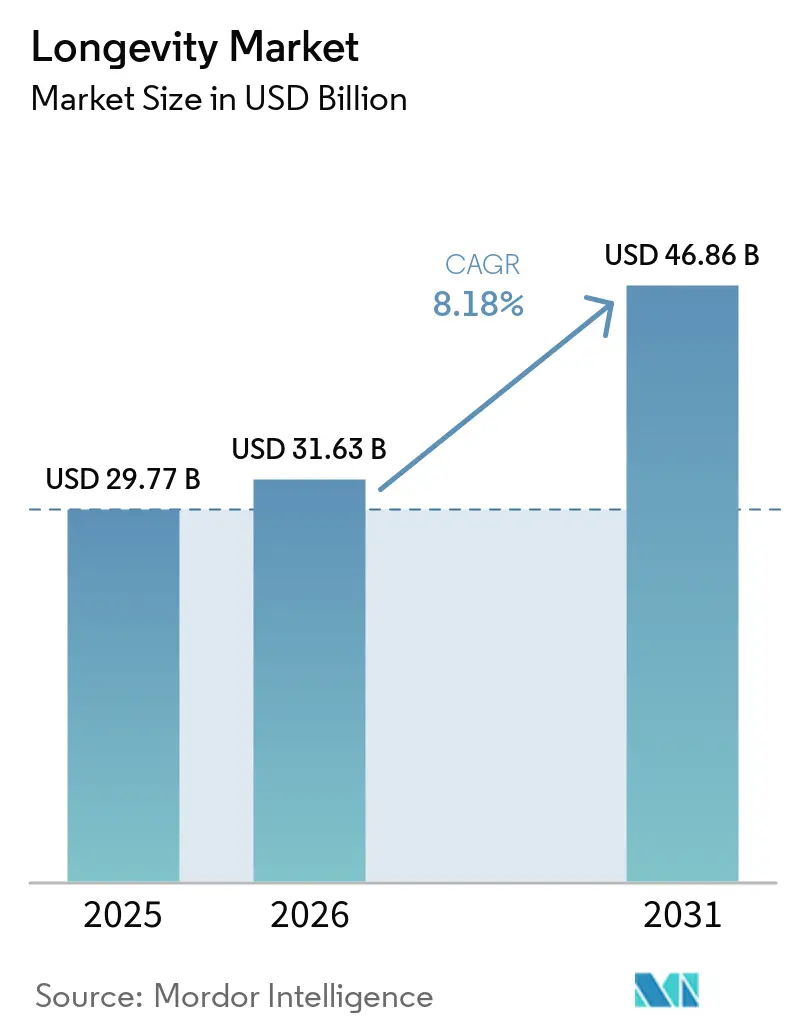

| Market Size (2026) | USD 31.63 Billion |

| Market Size (2031) | USD 46.86 Billion |

| Growth Rate (2026 - 2031) | 8.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Longevity Market Analysis by Mordor Intelligence

The Longevity Market size is expected to grow from USD 29.77 billion in 2025 to USD 31.63 billion in 2026 and is forecast to reach USD 46.86 billion by 2031 at 8.18% CAGR over 2026-2031.

The market's expansion mirrors a strategic pivot in drug discovery, where aging is treated as a modifiable biological pathway rather than an irreversible chronology. Venture funding that tops USD 3 billion for single cellular-reprogramming rounds, rapid advances in CRISPR-based editing, and insurer pilots that reimburse interventions tied to biological age all point to an investment climate primed for scalable rejuvenation pipelines. Pharmaceutical incumbents are broadening risk-buffered alliances with early-stage biotechs, while digital biomarkers and epigenetic clocks translate research insights into consumer-grade feedback loops. Collectively, these forces position the longevity market for sustained high-single-digit expansion as therapeutic, diagnostic, and lifestyle modalities converge within an emerging preventive-care reimbursement framework.

Key Report Takeaways

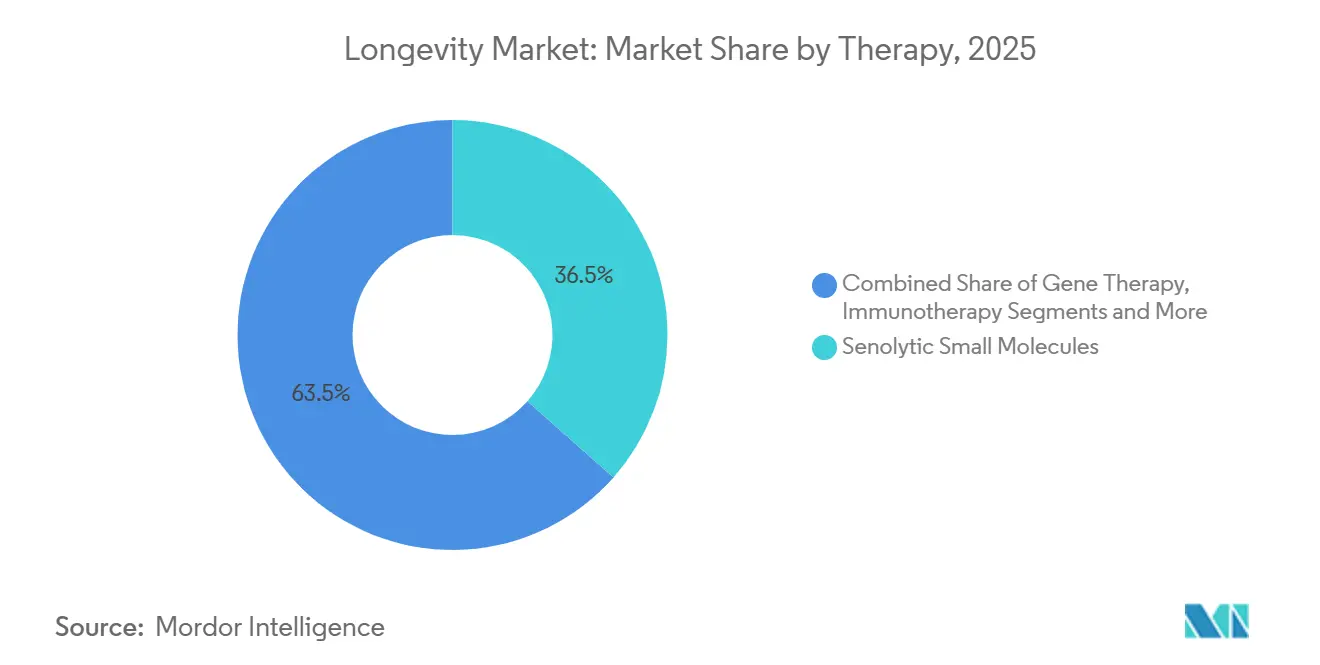

- By therapy, senolytic small molecules led with 36.52% revenue share in 2025, while gene therapy is advancing at an 11.63% CAGR between 2026 and 2031.

- By delivery platform, in-vivo therapeutics accounted for 71.83% of the longevity market share in 2025, whereas digital longevity interventions are projected to post a 12.78% CAGR through 2031.

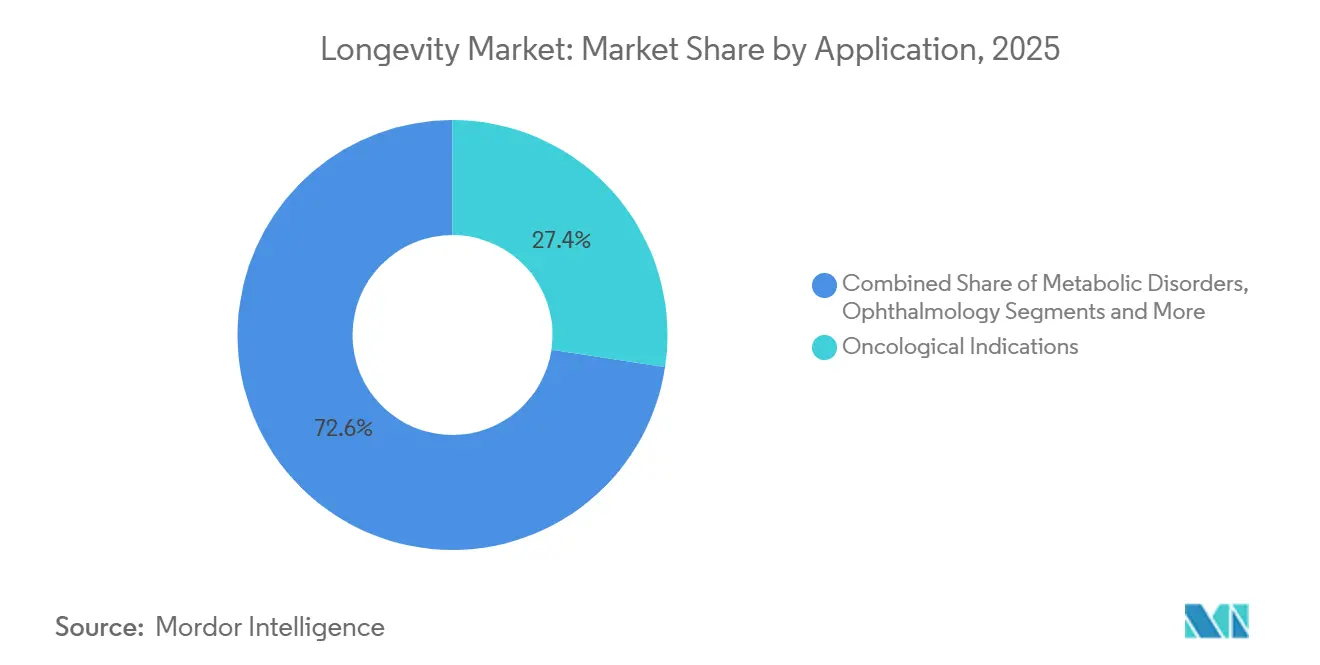

- By application, oncological indications captured 27.37% of 2025 revenue and neurodegenerative disorders are set to expand at a 10.52% CAGR to 2031.

- By end user, pharmaceutical and biotechnology firms held 63.83% of 2025 revenue, with wellness clinics and longevity spas forecast to grow at an 11.22% CAGR through 2031.

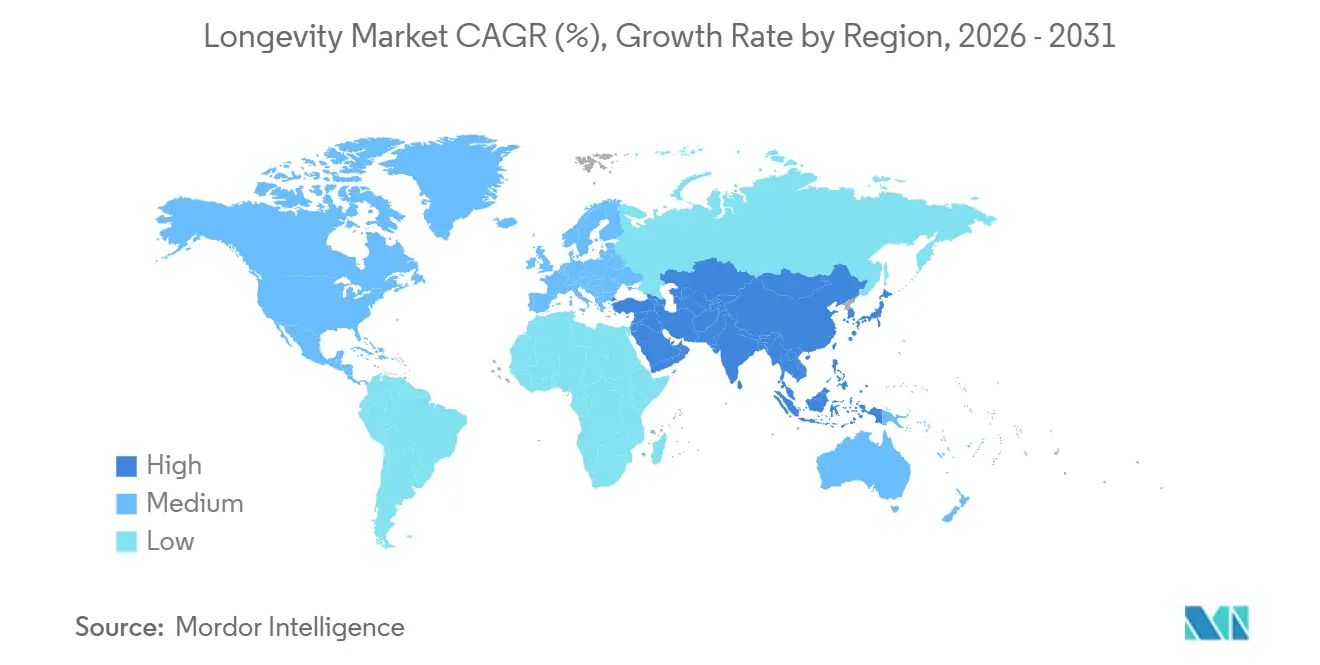

- By geography, North America recorded 41.23% revenue share in 2025, yet Asia-Pacific is on track for a 10.35% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Longevity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise in 65+ population | +1.8% | Japan, Italy, Germany, broader global | Long term (≥ 4 years) |

| Growing burden of age-related chronic diseases | +1.5% | North America, Europe, Asia-Pacific urban hubs | Medium term (2-4 years) |

| Venture capital and SPAC surge in rejuvenation biotech | +1.2% | North America, Europe, Singapore | Short term (≤ 2 years) |

| Breakthroughs in CRISPR and other gene-editing tools | +1.4% | United States, United Kingdom | Medium term (2-4 years) |

| AI-driven in-silico discovery of senotherapeutics | +1.0% | North America, Europe, China | Medium term (2-4 years) |

| Expansion of payor interest in preventive aging care | +0.9% | United States, European national systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in the 65+ Population

The United Nations projects a global cohort of 1.6 billion people aged 65 and older by 2050, more than doubling the 761 million counted in 2021. According to a 2024 United Nations update, by the mid-2030s, the number of individuals aged 80 and older is set to hit 265 million, and by the late 2070s, those aged 65 and older will soar to 2.2 billion globally.[1] United Nations, “Ageing,” United Nations, un.org Japan, where 29% of residents were over 65 in 2024, funds Silver Human Resources Centers that standardize longevity diagnostics in routine geriatric visits, and similar reimbursement pilots are under review in several European Union member states.[2]Ministry of Health, Labour and Welfare, “Annual Report on the Aging Society 2024,” Government of Japan, mhlw.go.jpChina’s 14th Five-Year Plan assigns CNY 3.2 trillion to eldercare infrastructure, opening hospital-based pilot programs that test senolytics for frailty reduction. Medicare, meanwhile, spends USD 23,000 per beneficiary each year managing chronic disease clusters in older adults; actuarial models show that compressing morbidity via senescent-cell clearance could materially lower lifetime outlays. The World Health Organization’s Decade of Healthy Ageing has unlocked multilateral funding streams, giving longevity science formal standing as a public-health priority.

Growing Burden of Age-Related Chronic Diseases

Cardiovascular disease, cancer, neurodegeneration, and metabolic syndrome drive 71% of all deaths worldwide. Alzheimer’s disease alone consumed USD 345 billion in U.S. health expenditures in 2024, and CMS agreed to reimburse lecanemab using an accelerated pathway that links coverage to post-marketing safety surveillance.[3]Alzheimer’s Association, “Fiscal Year 2024 Alzheimer’s Research Funding,” Alzheimer’s Impact Movement, alzimpact.org Preclinical research shows dasatinib-plus-quercetin clears senescent cells in idiopathic pulmonary fibrosis and osteoarthritis, yet translation slows without biomarkers that quantify senescent burden in human tissue. Global diabetes prevalence will top 700 million cases by 2045, with beta-cell senescence becoming a viable pharmacologic target alongside GLP-1 receptor agonists. Draft EMA guidance published in 2024 signals regulatory openness to geroprotectors if functional gain across multiple organ systems is proven.

Venture Capital and SPAC Surge in Rejuvenation Biotech

Altos Labs captured USD 3 billion in Series A financing to pursue partial-reprogramming approaches that reset cellular epigenetic age. Longevity Biomedical accessed public capital through a USD 26.8 million SPAC merger, creating a precedent for aging-focused equity listings. Retro Biosciences committed USD 1 billion to autophagy and reprogramming platforms, underlining investor appetite for 10-year lifespan extension projects. Integrated Biosciences raised USD 17 million to run AI screens on senescence transcriptomes, cutting discovery cycles to 18 months versus the conventional four-year norm. Unity Biotechnology’s UBX1325 completed Phase 2 diabetic macular-edema trials in 2024 and confirmed that senolytic mechanisms can preserve retinal function in humans.

Breakthroughs in CRISPR and Gene-Editing Tools

The FDA cleared Casgevy in December 2023 for hemoglobinopathies, validating ex-vivo CRISPR editing and accelerating in-vivo delivery investment. Base and prime editors correct single-nucleotide errors without double-strand breaks, showing promise in progeria and telomeric-dysfunction models that mirror accelerated aging. Rejuvenate Bio leveraged the FDA’s Animal Rule to test multi-gene interventions in companion dogs, collecting safety data that inform human IND packages. Follistatin AAV constructs reversed sarcopenia in non-human primates but required transient immunosuppression protocols to counter neutralizing antibodies. The ISSCR published guardrails on germline editing aimed at healthy-lifespan enhancement, balancing scientific momentum with ethical oversight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory ambiguity over classifying aging as a disease | −1.3% | United States, European Union | Medium term (2-4 years) |

| High clinical-trial costs and multi-year timelines | −1.1% | North America, Europe, select emerging markets | Long term (≥ 4 years) |

| Bioethical concerns over longevity-access inequality | −0.7% | OECD nations, global dialogue | Long term (≥ 4 years) |

| Public skepticism and “snake-oil” perception of anti-aging products | −0.6% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Ambiguity Over Classifying Aging as a Disease

The FDA treats aging as a risk factor rather than a diagnosable indication, compelling sponsors to pivot toward proxy endpoints such as frailty or metabolic syndrome. The multi-center TAME study seeks precedent for labeling metformin as an age-delaying therapy but remains in progress through 2026. EMA draft guidance in 2024 hinted that functional gains across organ systems could satisfy approval criteria, yet lack of validated surrogate biomarkers slows adoption. Japan’s PMDA takes a looser stance, approving NMN supplements as functional foods, offering a partial workaround that falls short of prescription-drug rigor. ICD-11 now lists an extension code for aging-related decline in intrinsic capacity, but national uptake remains uneven.

High Clinical-Trial Costs and Multi-Year Timelines

Phase 2 aging trials cost USD 7-20 million, while Phase 3 studies often surpass USD 100 million because endpoints require long follow-up for disease incidence or mortality. Without FDA-endorsed biomarkers, sponsors lean on labor-intensive functional endpoints that drive large sample sizes. Unity Biotechnology recruited 200 subjects to confirm synovial-tissue target engagement for UBX2089, illustrating the complexity of dose-finding in heterogeneous aging phenotypes. Accelerated Approval remains underused because regulators have yet to deem epigenetic clocks or inflammatory cytokines reliable surrogates. Emerging-market recruitment remains low at 8% of participants, limiting generalizability and complicating global commercialization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy – Gene Therapy Gains Momentum

Gene therapy will post an 11.63% CAGR through 2031, the fastest rate among modalities, helped by adeno-associated-virus refinements that permit repeat dosing in chronic degenerative conditions. Senolytic small molecules held 36.52% of revenue in 2025, cementing their position as the largest contributor to the longevity market. First-generation agents face off-target toxicity, which catalyzes a shift toward senomorphic compounds that limit SASP emissions without triggering apoptosis. Rapalog trials in metabolic syndrome showed a 30% inflammatory-marker drop, reinforcing the therapeutic logic of pathway modulation rather than cell clearance. Cellular reprogramming remains preclinical but garners high investment, especially with Altos Labs advancing retinal-degeneration protocols toward IND filings. Stem-cell infusions benefit from Japan’s fast-track approvals for frailty, while immunotherapies targeting inflammaging encounter safety trade-offs tied to cytokine suppression. Microbiome manipulation, including Mitopure’s GRAS-cleared urolithin A, rounds out the pipeline with consumer-facing nutraceutical angles.

In aggregate, the longevity market size for gene therapy is poised to expand from a low starting base, while senolytic small molecules retain the highest longevity market share in the short term. Cross-modality combinations such as senolytic preconditioning before gene therapy are under preclinical review and may re-shape competitive hierarchies after 2030.

By Delivery Platform – Digital Interventions Scale Quickly

In-vivo therapeutics captured 71.83% of 2025 revenue, powered by small molecules and systemically administered biologics. Yet digital longevity interventions, which include epigenetic clocks and wearable biomarker platforms, are forecast to grow 12.78% annually, the fastest pace of any platform. Insurer pilots that reimburse biological-age reduction underpin the commercial logic for these data-driven tools. Ex-vivo cell-based approaches, validated by Casgevy’s approval, remain capital intensive but are likely to gain share as manufacturing efficiencies improve.

The longevity market size for digital platforms could outpace expectations if payor pilots convert to full reimbursement policies. Conversely, in-vivo developers protect their dominant longevity market share by layering digital endpoints onto drug trials, forming hybrid models that blend therapeutics with real-time monitoring.

By Application – Neurodegeneration Rises Fastest

Oncological indications represented 27.37% of 2025 revenue, reflecting both anti-tumor senolytic applications and strategies that mitigate chemotherapy-induced senescence. FDA approvals of lecanemab and donanemab validate disease-modifying approaches and lift neurodegeneration to the fastest-growing slot at a 10.52% CAGR. Cardiovascular programs trail slightly but hold strategic interest because vascular senescence underpins multiple high-mortality disorders.

For neurodegeneration, the longevity market size may surpass USD 10 billion by 2031 if senolytic or gene-therapy adjuncts clear clinical hurdles. Cardiovascular and metabolic assets carry broad patient pools that preserve a sizeable longevity market share even if growth rates are modest compared with neurology.

By End User – Wellness Clinics Expand

Pharmaceutical and biotechnology companies generated 63.83% of 2025 revenue by advancing internal pipelines and strategic alliances. Wellness clinics and longevity spas, however, will grow 11.22% annually as affluent consumers demand integrated protocols that blend senolytics, stem-cell infusions, and continuous monitoring. Academic institutes deliver foundational science and partner with contract organizations to scale trials, while CDMOs enlarge dedicated capacity for cell-therapy manufacturing.

High-net-worth demand means the longevity market size for wellness clinics can rise quickly from a small base. Pharmaceutical entities still control the majority longevity market share and will likely consolidate smaller biotechs to secure late-stage assets.

Geography Analysis

North America generated 41.23% of 2025 revenue, buoyed by NIH’s USD 3.7 billion aging-research allocation and steady venture financing in Silicon Valley. The United States lists more than 120 longevity trials, although regulatory ambiguity tempers speed to market. Canada’s CAD 30 million Stem Cell Network grant fosters regenerative-frailty studies, and Mexico’s proximity to the U.S. pulls medical tourists seeking stem-cell therapies.

Asia-Pacific is on course for a 10.35% CAGR through 2031. Japan integrates longevity diagnostics within universal coverage, China funds CNY 16 trillion in preventive infrastructure, and India scales elder-care programs despite uneven access to advanced therapies. South Korea and Australia finalize guidance that clarifies aging-therapy pathways, drawing biotechs that seek faster approvals.

Europe sits mid-pack, but EMA’s permissive stance toward multi-system endpoints could accelerate approvals. Switzerland’s dense cluster of premium clinics attracts global clientele, while the NHS tests whether early pharmacologic and lifestyle interventions reduce multimorbidity by 2034. The Middle East and Africa remain emergent; the UAE licenses stem-cell clinics under compassionate-use rules, and South Africa green-lights MSC therapies for frailty.

Competitive Landscape

More than 50 clinical-stage companies operate in a field where no entity exceeds 5% share, producing a highly fragmented environment ripe for consolidation. AbbVie’s USD 1.5 billion extension with Calico signals big-pharma appetite for aging platforms. Altos Labs leverages a USD 3 billion war chest to chase cellular-reprogramming breakthroughs free from near-term revenue pressure. Unity Biotechnology pivots toward ophthalmology and musculoskeletal uses after earlier setbacks, illustrating iterative strategy shifts common in nascent markets.

AI-native challengers such as Insilico Medicine and Integrated Biosciences accelerate discovery and could shorten time-to-IND filings. Patent issuance for senolytics jumped 40% between 2022 and 2024, suggesting that IP portfolios will drive future licensing and M&A activity. Under-utilized regulatory pathways like Accelerated Approval present upside for sponsors that validate surrogate biomarkers, especially epigenetic clocks, as predictors of functional benefit.

Longevity Industry Leaders

Bristol-Myers Squibb

AbbVie

Eli Lilly and Company

Calico Life Sciences

Unity Biotechnology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Cipla launched Ciplostem, an allogeneic MSC therapy for grade II–III knee osteoarthritis after DCGI approval.

- December 2025: The FDA approved Waskyra, the first cell-based gene therapy for Wiskott-Aldrich syndrome.

- November 2025: Novartis received FDA clearance for Itvisma, extending SMA gene replacement therapy to adults.

- August 2025: Opus Genetics gained FDA authorization to begin Phase 1/2 trials of a gene therapy for Best disease.

Global Longevity Market Report Scope

As per the scope of the report, longevity is about living with a higher quality of life and foreseeing and preventing common chronic diseases that often accompany the aging process.

The longevity market is segmented by therapy, delivery platform, application, end user, and geography. The market is segmented by therapy into Senolytic Small Molecules, Senomorphic Agents, Gene Therapy, Cellular Reprogramming Therapy, stem cell and regenerative therapy, Immunotherapy, Microbiome Manipulation, and Others. By Delivery Platform, the Market is segmented into In-vivo Therapeutics, Ex-vivo/Cell-based Platforms, and Digital Longevity Interventions. By Application, the market is segmented into Cardiovascular Diseases, Neurodegenerative Disorders, Metabolic Disorders, Oncological Indications, musculoskeletal and frailty, dermatology and aesthetics, Ophthalmology, and Others. By End User, the market is subsegmented into Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, CROs & CDMOs, Wellness Clinics & Longevity Spas. The geography region is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the market sizes and forecasts for major countries across different regions. The market size is provided for each segment in terms of value (USD).

| Senolytic Small Molecules |

| Senomorphic Agents |

| Gene Therapy |

| Cellular Reprogramming Therapy |

| Stem Cell & Regenerative Therapy |

| Immunotherapy |

| Microbiome Manipulation |

| Others |

| In-vivo Therapeutics |

| Ex-vivo / Cell-based Platforms |

| Digital Longevity Interventions |

| Cardiovascular Diseases |

| Neurodegenerative Disorders |

| Metabolic Disorders (Diabetes, Obesity) |

| Oncological Indications |

| Musculoskeletal & Frailty |

| Dermatology & Aesthetics |

| Ophthalmology |

| Others |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| CROs & CDMOs |

| Wellness Clinics & Longevity Spas |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy | Senolytic Small Molecules | |

| Senomorphic Agents | ||

| Gene Therapy | ||

| Cellular Reprogramming Therapy | ||

| Stem Cell & Regenerative Therapy | ||

| Immunotherapy | ||

| Microbiome Manipulation | ||

| Others | ||

| By Delivery Platform | In-vivo Therapeutics | |

| Ex-vivo / Cell-based Platforms | ||

| Digital Longevity Interventions | ||

| By Application | Cardiovascular Diseases | |

| Neurodegenerative Disorders | ||

| Metabolic Disorders (Diabetes, Obesity) | ||

| Oncological Indications | ||

| Musculoskeletal & Frailty | ||

| Dermatology & Aesthetics | ||

| Ophthalmology | ||

| Others | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| CROs & CDMOs | ||

| Wellness Clinics & Longevity Spas | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the longevity market in 2031?

It is expected to reach USD 46.86 billion, growing at an 8.18% CAGR from 2026 to 2031.

Which therapy segment is growing fastest?

Gene therapy is forecast to expand at an 11.63% CAGR as vector engineering reduces immunogenicity obstacles.

Why are digital longevity platforms attracting insurers?

Payors pilot reimbursement when epigenetic-age reductions correlate with lower hospitalization costs.

How fragmented is competition among longevity companies?

More than 50 clinical-stage firms exist, with none holding over 5% revenue share, yielding a concentration score of 2.

Which region will grow quickest through 2031?

Asia-Pacific leads with a 10.35% CAGR, driven by policy support in Japan and China.

What restrains faster commercial rollout of geroprotectors?

Regulatory ambiguity on classifying aging as a disease and high multi-year trial costs delay approvals.

Page last updated on: