Open Gear Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

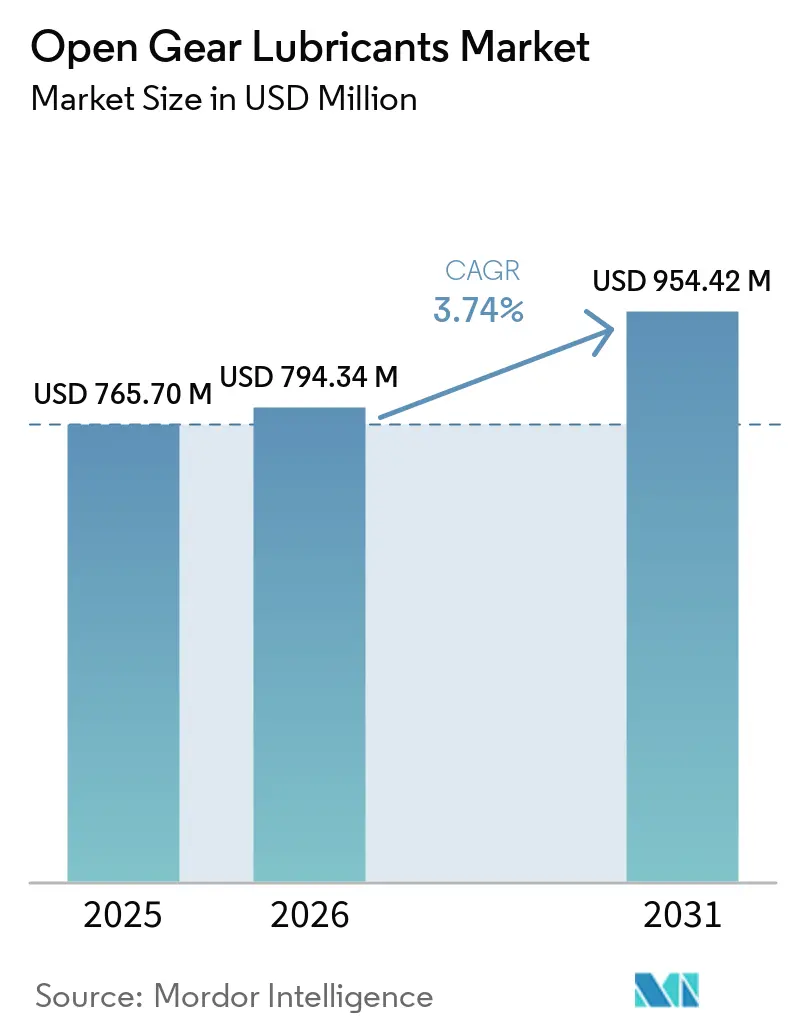

| Market Size (2026) | USD 794.34 Million |

| Market Size (2031) | USD 954.42 Million |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Open Gear Lubricants Market Analysis by Mordor Intelligence

The Open Gear Lubricants Market size is expected to increase from USD 765.70 million in 2025 to USD 794.34 million in 2026 and reach USD 954.42 million by 2031, growing at a CAGR of 3.74% over 2026-2031. As mining ball mills, cement rotary kilns, and offshore wind-turbine pitch systems increasingly demand extreme-pressure lubricants, there's a notable shift in procurement. Operators are moving away from traditional volume-driven mineral oils, opting instead for specialty synthetics. These synthetics not only promise longer service intervals but also offer a lower lifetime cost. Regulatory pushes, like the 2024 United States Environmental Protection Agency's Vessel Incidental Discharge Act, are hastening the shift towards environmentally acceptable lubricants, especially in marine and offshore equipment. Additionally, with the International Electrotechnical Commission technical report set to be released in February 2026, wind turbines with higher power capacities are seeing a redefinition in gearbox lubrication needs. This shift is spurring a heightened demand for synthetics that boast low temperatures and a high viscosity index. The competitive landscape remains fragmented, with no single supplier dominating the market. This environment has allowed niche blenders to flourish, especially by providing original equipment manufacturer-approved nano-additive packages. These packages are proving to be game-changers, significantly extending gear life in kilns operating at elevated temperatures.

Key Report Takeaways

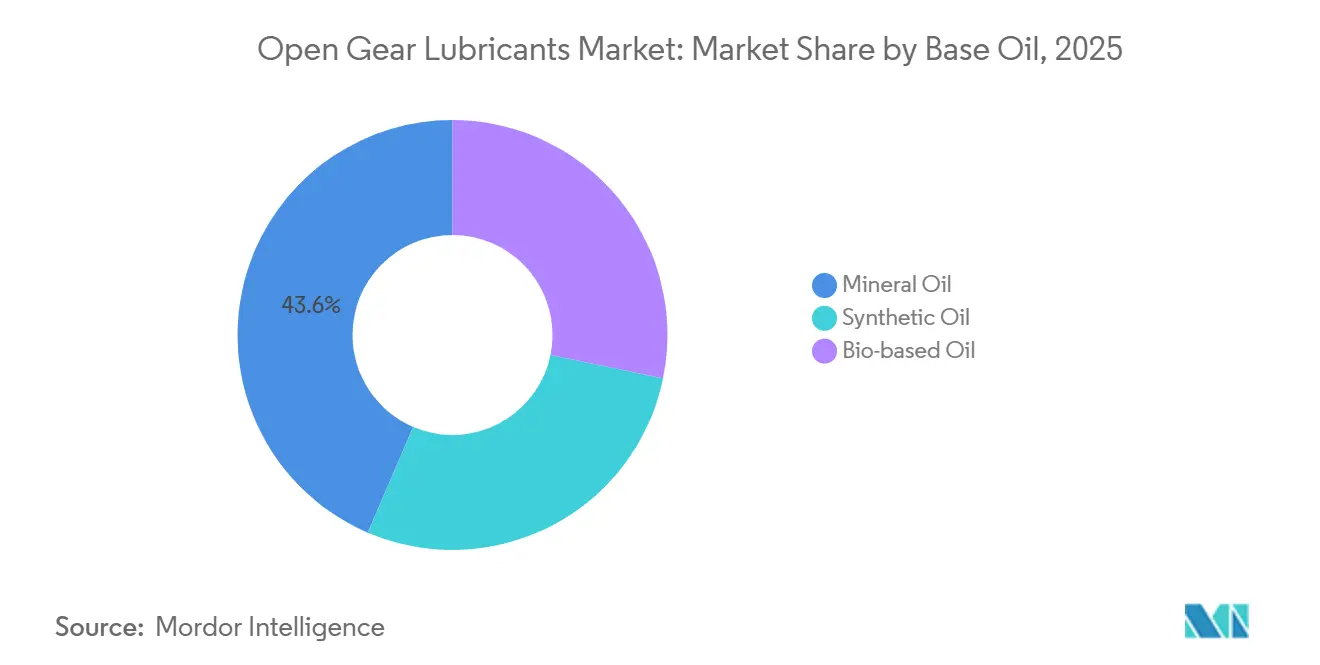

- By base oil, mineral oils led with 43.56% open gear lubricants market share in 2025, while synthetic oils are projected to grow at a 3.68% CAGR during 2026-2031.

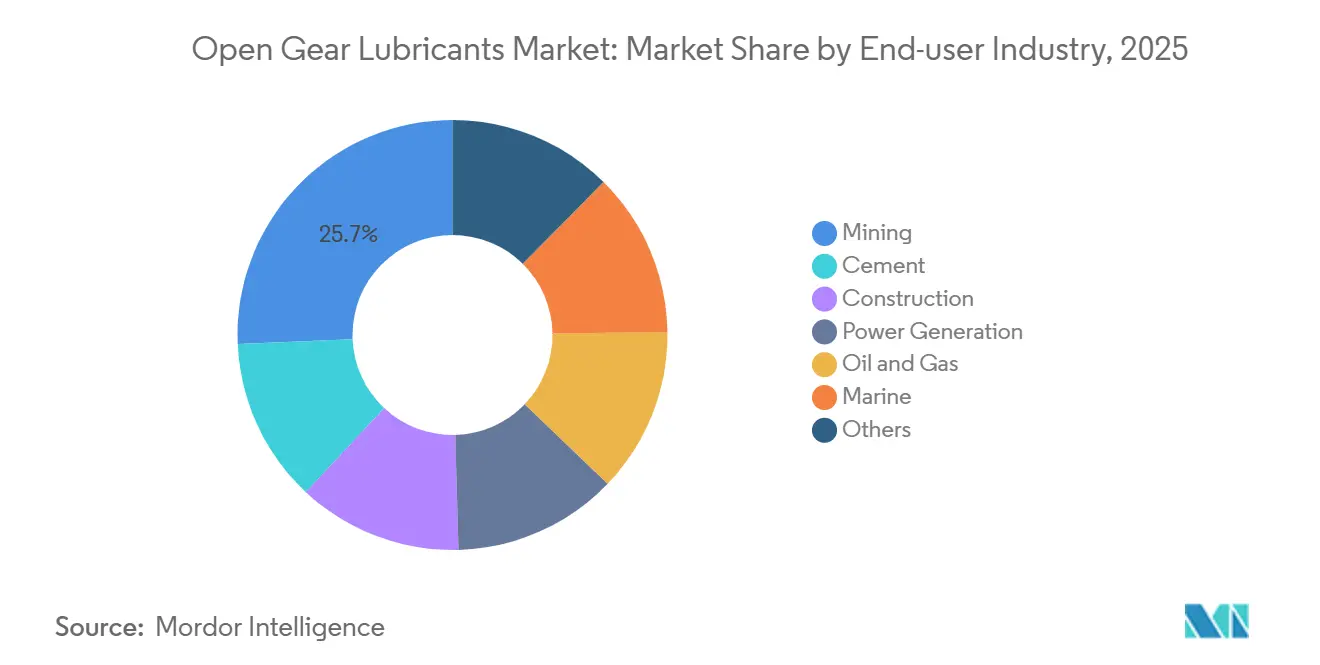

- By end-user industry, mining accounted for 25.66% of the open gear lubricants market size in 2025, and oil & gas is forecast to post the fastest 3.77% CAGR during 2026-2031.

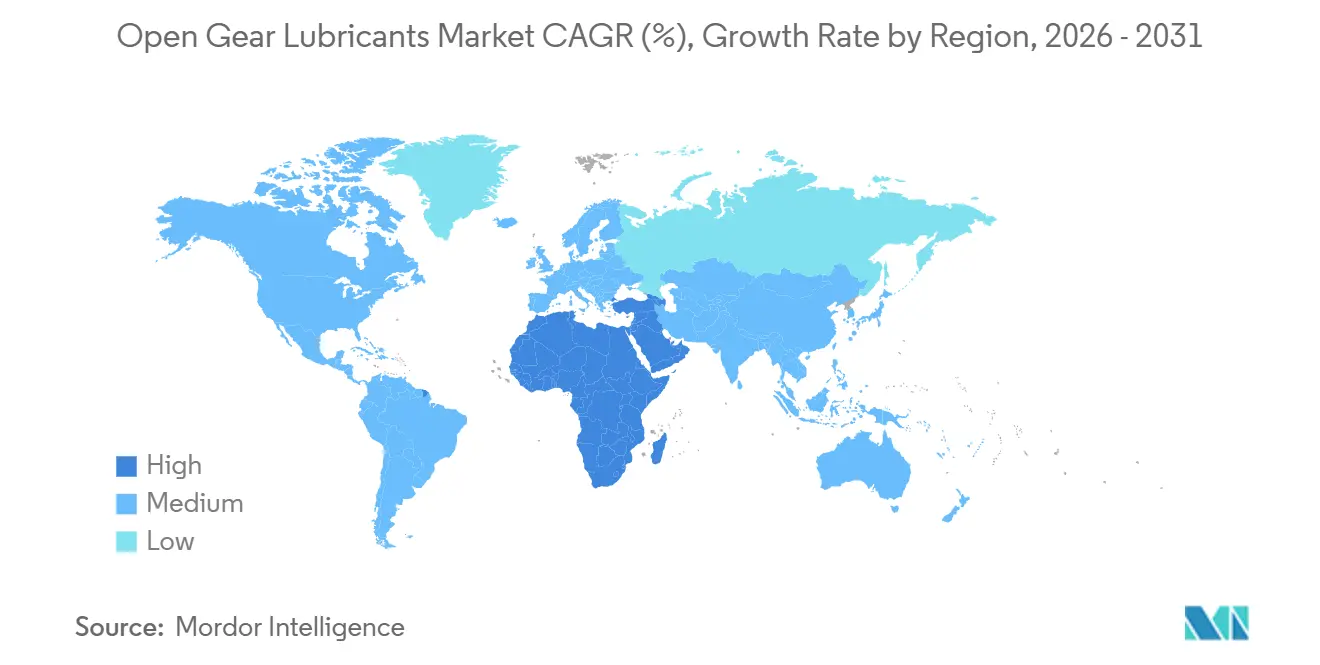

- By geography, Asia-Pacific dominated with 35.40% revenue share in 2025, whereas the Middle-East & Africa region is advancing at a 3.82% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Open Gear Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from mining and cement expansion | +1.20% | Asia-Pacific, South America, Middle-East & Africa | Medium term (2-4 years) |

| Growth in bio-based lubricants adoption | +0.60% | North America, Europe (OSPAR/VGP compliance zones) | Long term (≥ 4 years) |

| Increasing uptake of synthetic base oils | +0.80% | Global, with a concentration in Europe and North America | Medium term (2-4 years) |

| AI-enabled predictive maintenance lowering lubricant wastage | +0.40% | North America, Europe, Asia-Pacific (advanced mining/cement operators) | Long term (≥ 4 years) |

| OEM-approved nano-additive packages extending gear life | +0.50% | Global, early adoption in Europe and Asia-Pacific cement sectors | Medium term (2-4 years) |

| Shift toward centralized spray systems in high-altitude mines | +0.30% | South America (Andes copper/lithium mines), Asia-Pacific (Himalayan region) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Mining and Cement Expansion

Expansions of copper and iron-ore mines in Chile, Peru, and Indonesia, coupled with the introduction of new kilns in Saudi Arabia, are driving up annual lubricant consumption. These lubricants are essential for grinding mills and rotary kilns that operate continuously. Given that failures in kiln gears can halt production and incur substantial costs, procurement teams are now prioritizing high-load Timken ratings over the initial price of lubricants. Synthetic open-gear products from Klüber have reduced lubricant consumption and lowered operating temperatures, leading to noticeable improvements in operational uptime. Additionally, centralized spray systems are minimizing waste by precisely dosing lubricant with each gear rotation. As a result, the focus has shifted from the price per liter to the overall life-cycle cost.

Growth in Bio-Based Lubricants Adoption

The Environmental Protection Agency Vessel Incidental Discharge Act rule mandates that large vessels use environmentally acceptable lubricants at oil-to-sea interfaces. This requirement is expected to drive the demand for biodegradable products that break down within a specified timeframe[1]U.S. Environmental Protection Agency, “Vessel Incidental Discharge National Standards of Performance,” epa.gov. Castrol’s carbon-neutral BioTac OG, certified to PAS 2060, showcases the evolution of bio-based greases, achieving high biodegradability alongside strong Four-Ball Extreme Pressure weld points. To address spill liabilities and meet corporate sustainability goals, offshore wind farms and coastal cement terminals are increasingly turning to bio-esters. This transition is further bolstered by Europe’s OSPAR convention and impending bans on per- and polyfluoroalkyl substances, spurring swift adoption among North Sea marine fleets. Suppliers boasting original equipment manufacturer approvals for bio-based formulations are emerging as preferred vendors in bid assessments. With life-cycle carbon accounting gaining traction in boardrooms, offerings in the bio-based open gear lubricants market are poised to secure long-term contracts, even with a price premium over traditional mineral oils.

Increasing Uptake of Synthetic Base Oils

High-temperature cement kilns and sub-zero wind-turbine gears now utilize polyalphaolefins and Group III hydrocracked stocks, requiring a high viscosity index and extremely low pour points[2]Exxon Mobil, “Mobil SHC Aware Gear Series,” exxonmobil.com . ExxonMobil's Mobil SHC Aware Gear line, endorsed by Nakashima and SKF, achieves high performance in scuffing resistance and meets Vessel General Permit toxicity standards. This underscores the capability of synthetic lubricants to offer both longevity and environmental responsibility. In cement plants, these synthetic lubricants have successfully extended relubrication intervals, significantly reducing technician exposure in high-temperature kiln hoods. While these synthetics come at a higher cost per liter, operators find solace in the fact that they can recover this added cost over time, thanks to diminished consumption and fewer shutdowns. Furthermore, North American wind-farm proprietors appreciate the prolonged drain intervals of synthetics, which in turn, curtail crane rental costs associated with gearbox oil changes. As a result, synthetic lubricants are poised to dominate the open gear lubricants market, marking them as the fastest-growing segment.

AI-Enabled Predictive Maintenance Lowering Lubricant Wastage

Automated spray systems, now equipped with vibration and torque sensors, adjust lubricant flow in real-time, significantly reducing usage compared to fixed schedules. Algorithms compare in-service data against known failure modes, prompting corrective actions before metal-on-metal contact happens. Klüber has teamed up with DALOG and NOVEXA, blending lubricant analytics with gear-profiling services, providing plant managers with a unified dashboard for asset health. In the wind energy sector, concepts endorsed by DNV utilize polyalphaolefin base oils alongside additive top-up cartridges, eliminating the need for routine oil changes over turbine lifetimes. However, developing regions face challenges due to technician shortages, hindering proper configuration. Despite this, early adopters have reported notable savings in operations and maintenance. As training programs expand, predictive maintenance is poised to become the norm, enhancing the open gear lubricants market by linking product sales to digital service revenues.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical supply-chain instability | -0.50% | Global, acute in Europe and Asia-Pacific, dependent on Middle East base oils | Short term (≤ 2 years) |

| Application difficulties with large-diameter open gears | -0.30% | Global, concentrated in mining and cement sectors with girth gears >6 meters | Medium term (2-4 years) |

| Emerging PFAS restrictions affecting legacy chemistries | -0.40% | North America, Europe (EU REACH, U.S. state-level bans) | Long term (≥ 4 years) |

| Skill shortage for advanced lubrication audits in developing regions | -0.20% | Asia-Pacific, Middle East & Africa, South America (excluding major urban centers) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Geopolitical Supply-Chain Instability

Disruptions in the Strait of Hormuz, through which a significant portion of Europe's Group II base stocks transit, can lead to a substantial increase in blending costs within a short period. A diversion to the Red Sea extended lead times considerably, compelling just-in-time cement plants to rely on emergency mineral-oil inventories at a higher cost. While North American blenders have turned to domestic sourcing of polyalphaolefin as a hedge, the transition to synthetic stocks requires an extensive process involving laboratory testing and original equipment manufacturer reapproval. Spot prices for Group II oils have risen significantly, squeezing profit margins for independent blenders.

Emerging PFAS Restrictions Affect Legacy Chemistries

The European Chemicals Agency is poised to implement a phased prohibition on per- and polyfluoroalkyl substances, potentially taking effect soon. This move targets thousands of fluorinated compounds, which have been prized for their water resistance and compatibility with seals. In the United States, states like California and Minnesota have already passed similar laws. As a result, global suppliers are racing against the clock, aiming to reformulate their flagship open-gear greases within the next few years. However, testing new additives for their stability at high temperatures and compatibility with elastomers is no quick task. It can take a significant amount of time, especially when factoring in field trials in active kilns. Moreover, during these transition phases, maintaining dual inventories can strain working capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Base Oil: Mineral Oils Anchor Share Despite Synthetic Momentum

Mineral oils captured 43.56% of the open gear lubricants market share in 2025, thanks to entrenched use in cost-sensitive Asian cement kilns, where buyers still purchase by the drum rather than by equipment life results. The synthetic oils segment is projected to expand at a 3.68% CAGR during 2026-2031. As legacy assets in India and Indonesia come online, synthetics are challenging this dominance. Polyalphaolefin and Group III blends now account for a significant portion of North American sales, driven by the International Electrotechnical Commission mandate for wind-turbine gearboxes. In the cement sector, Klüber's field data reveals that synthetics reduce consumption and operating temperatures, persuading multinationals to adopt premium grades as the standard. While bio-based esters currently hold a small market share, they are witnessing substantial growth, especially where VIDA compliance is essential for deck machinery. Blenders merging bio-esters with polyalphaolefin to expand the temperature range could tap into new revenue streams in Asia's marine sector. Given the technical advantages and regulatory incentives, synthetics are poised to surpass mineral oils in value terms long before the end of the decade, even if their volumes remain subdued due to lower consumption rates.

The market for synthetic oils in open gear lubricants is projected to expand significantly, marking it as the most rapidly advancing segment in the larger market. With original equipment manufacturer-endorsed nano-additives becoming commonplace in kiln and mill gearboxes, mineral oils face the threat of being confined to niche, price-driven applications. In response, suppliers are pairing high-margin synthetics with digital monitoring services, aiming to safeguard their market share and establish enduring service contracts. Concurrently, as Group I mineral capacities dwindle in Europe, supply tightens, and the price gap to Group III narrows. This shift highlights why procurement teams are now prioritizing total cost of ownership over mere invoice price, hastening the industry's pivot towards synthetics.

By End-User Industry: Mining Leads, Oil & Gas Accelerates

Mining retained a dominant 25.66% slice of the open gear lubricants market size in 2025. In South America's copper belts, the demand for rotary-drum and semi-autogenous grinding mill greases remains robust. At high-altitude sites, where elevations are significantly high, temperatures fluctuate dramatically from chilly nights to warm daytime conditions. This wide temperature swing poses challenges for maintaining consistent lubricant films. Sinopec, with its extensive portfolio of products, showcases the diverse formulations tailored to tackle the tropical humidity prevalent in these operations. Cement, taking the second spot, sees new kilns in India, Saudi Arabia, and Vietnam operating around the clock. These kilns rely on translucent synthetics, essential for strobe-light inspections.

Oil and gas is the fastest-expanding segment, clocking a 3.77% CAGR during 2026-2031. Offshore platforms are increasingly turning to environmentally acceptable lubricants, moving away from traditional mineral oils, in a bid to comply with VIDA mandates. In the Gulf of Mexico, deepwater rigs are opting for synthetic blends designed to meet stringent environmental requirements, a crucial step for obtaining permits. While wind-energy pitch systems represent a niche application, their significance is on the rise. The endorsement of Mobil SHC Gear 320 WindPower, branded as 'fill-for-life', underscores the melding of lubricant chemistry with asset management strategies. With predictive maintenance becoming the norm, end-users across sectors - be it mining, cement, oil and gas, or power generation - are demanding more than just products from suppliers. They're seeking data insights, which not only heighten service expectations but also elevate entry barriers for vendors specializing in low-tech greases.

Geography Analysis

Asia-Pacific generated 35.40% of global revenue in 2025. China's robust heavy-industry foundation, coupled with India's cement expansion, is steering the region's industrial narrative. Sinopec's expansion in Tianjin is set to boost the supply of humidity-resistant open-gear products, coinciding with the launch of nickel and copper smelters in Indonesia. The region's technical prowess is evident as Japanese and South Korean inputs shape International Electrotechnical Commission gearbox standards, guiding original equipment manufacturers towards adopting low-temperature polyalphaolefin blends. In a bid to address labor shortages at its remote Pilbara sites, Australian iron-ore miners are turning to automatic spray systems, further emphasizing the industry's shift towards synthetic solutions.

The Middle East and Africa is the fastest-growing territory at 3.82% CAGR during 2026-2031. Saudi Vision 2030's infrastructure projects are fueling continuous cement production. In Riyadh, kilns face extreme ambient temperatures and abrasive sand, increasing the demand for high-viscosity synthetics that resist wash-off. South Africa's platinum revival encounters similar high-dust challenges; however, centralized lubrication systems have proven effective in significantly reducing unplanned downtime in underground shafts. North African marine hubs, with Egypt's new Mediterranean ports leading the charge, are adopting bio-based greases for dockside cranes, aligning with International Maritime Organization pollution protocols. Yet, regional political volatility occasionally inflates freight premiums for imported base oils, steering buyers towards locally packaged synthetics.

While North America and Europe may lag in overall growth, they wield significant influence over chemistry trends, largely due to stringent environmental regulations. Europe's open gear lubricants market is expected to grow modestly, but the prohibition of per- and polyfluoroalkyl substances threatens to overhaul product lineups. In the United States, offshore operators are phasing out mineral oils in stern tubes, a move aimed at securing drilling permits under Vessel Incidental Discharge Act regulations, subsequently boosting demand for polyalphaolefin and ester environmentally acceptable lubricants. The British Gear Association's endorsement of International Electrotechnical Commission standards is further propelling wind-sector demand in the United Kingdom and Nordic regions. Meanwhile, South America, particularly Chile and Peru, is witnessing robust volume growth driven by copper expansion. However, logistical challenges in the Andes mines are inflating prices for centralized lubrication systems, which are often flown in from the United States or Europe.

Competitive Landscape

The open gear lubricants market is moderately concentrated. Digitalization is reshaping the landscape: Artificial intelligence-driven spray-system retrofits, offering significant consumption savings, are luring cement giants into long-term service agreements, moving away from traditional spot purchases. Suppliers who can finance remote-monitoring hardware or seamlessly integrate with plant supervisory control and data acquisition networks are poised to outpace conventional grease manufacturers. Gaining original equipment manufacturer gearbox approvals is becoming increasingly crucial; without a nameplate listing from industry leaders like FLENDER or MAAG, products risk exclusion from global kiln fleets. Consequently, the competitive edge is shifting from mere manufacturing volume to a blend of technical accreditation and digital prowess.

Open Gear Lubricants Industry Leaders

Carl Bechem GmbH

Shell plc

FUCHS SE

Klüber Lubrication (Freudenberg)

Chevron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Kia and TotalEnergies have extended their partnership for five years, ensuring Quartz engine oil supply. This move strengthens after-sales services, supports hybrid/electric technologies, and enhances TotalEnergies' position in the Global Open Gear Lubricants Market by optimizing supply chains.

- November 2024: FUCHS SE acquired STRUB & Co. AG, boosting its presence in the Global Open Gear Lubricants Market. The deal expanded Swiss market access, research, and production capabilities, adding EUR 15 million (USD 16.5 million) in revenue. It strengthened FUCHS’ extreme-pressure grease portfolio for heavy industries and cement kilns globally.

Global Open Gear Lubricants Market Report Scope

Open gear lubricants are specialized greases and oils formulated to protect large, exposed gears operating under extreme loads, slow speeds, and harsh environments. They provide strong adhesion, resist wash-off, reduce wear, and minimize friction in heavy-duty applications such as mining, cement kilns, marine vessels, and wind turbines. Their performance ensures reliability, extended equipment life, and compliance with environmental and safety standards across global industrial sectors.

The Open Gear Lubricants Market is segmented by base oil, end-user industry, and geography. By base oil, the market is divided into mineral oil, synthetic oil, and bio-based oil. By end-user industry, the market is segmented into mining, cement, construction, power generation, oil and gas, marine, and others. The report also covers the market size and forecasts for the Open Gear Lubricants Market in 19 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Mineral Oil |

| Synthetic Oil |

| Bio-based Oil |

| Mining |

| Cement |

| Construction |

| Power Generation |

| Oil and Gas |

| Marine |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Base Oil | Mineral Oil | |

| Synthetic Oil | ||

| Bio-based Oil | ||

| By End-user Industry | Mining | |

| Cement | ||

| Construction | ||

| Power Generation | ||

| Oil and Gas | ||

| Marine | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the open gear lubricants market?

The open gear lubricants market is projected at USD 794.34 million in 2026 and is forecast to reach USD 954.42 million by 2031 at a 3.74% CAGR from 2026 to 2031.

Which base-oil category holds the largest open gear lubricants market share?

Mineral oils led with 43.56% share in 2025, although synthetics are growing faster.

Which end-user industry will expand the quickest over 2026-2031?

Oil and gas is expected to post the fastest 3.77% CAGR as offshore assets switch to environmentally acceptable lubricants.

Why are bio-based lubricants gaining traction in marine applications?

The 2024 U.S. EPA VIDA rule requires environmentally acceptable lubricants at oil-to-sea interfaces, driving adoption of biodegradable esters.

Page last updated on: