Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

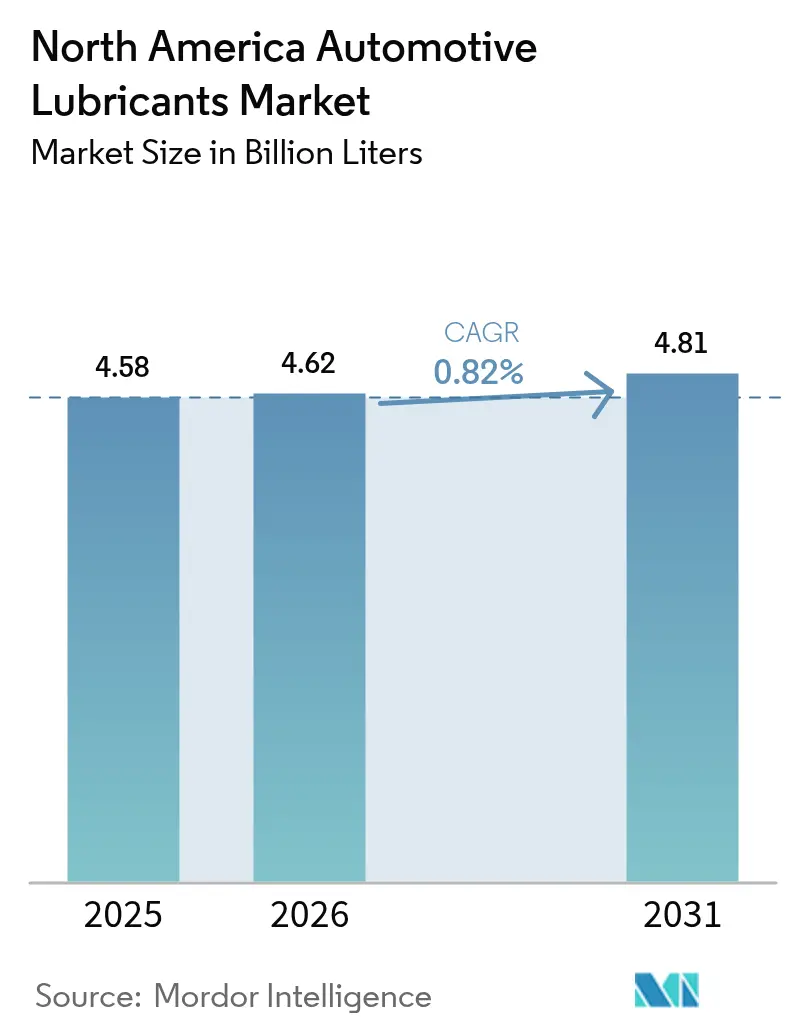

| Base Year Market Size (2025) | 4.58 Billion Liters |

| Market Volume (2026) | 4.62 Billion Liters |

| Market Volume (2031) | 4.81 Billion Liters |

| Growth Rate (2026 - 2031) | 0.82% CAGR |

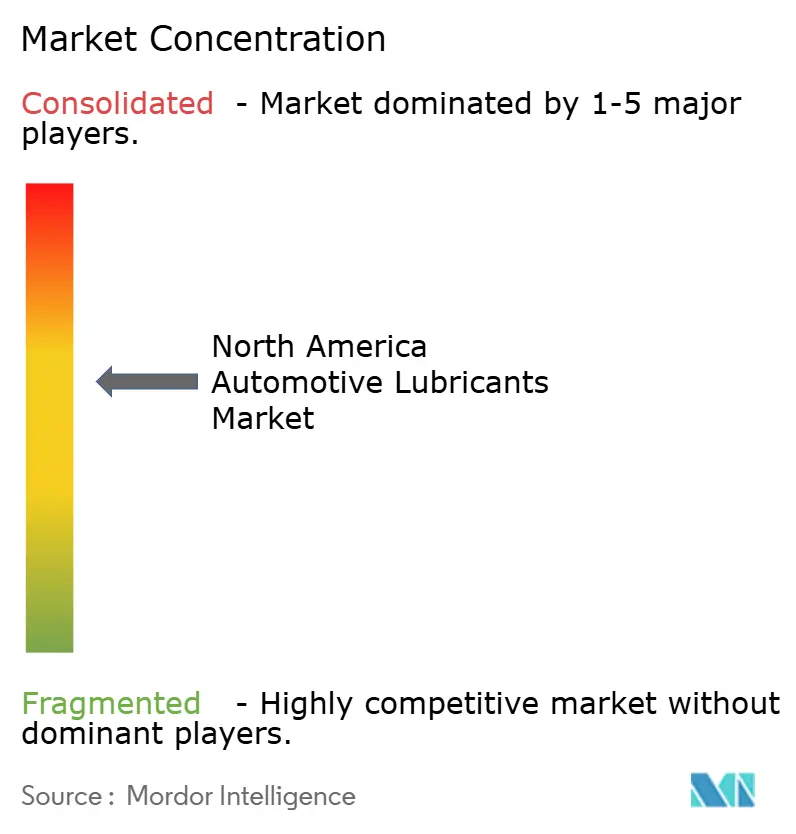

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive Lubricants Market Analysis by Mordor Intelligence

The North America Automotive Lubricants Market size was valued at 4.58 Billion Liters in 2025 and estimated to grow from 4.62 Billion Liters in 2026 to reach 4.81 Billion Liters by 2031, at a CAGR of 0.82% during the forecast period (2026-2031). Mature vehicle ownership levels across the United States, Canada, and Mexico temper volume expansion even as premium e-fluids register pockets of high growth. Extended drain intervals, the rising share of battery-electric vehicles, and intense quick-lube consolidation all place downward pressure on conventional engine oil use. Offsetting forces include a record-old internal combustion engine parc, tougher heavy-duty emissions norms that demand higher-performance formulations, and new factory-fill requirements tied to Mexico’s rapidly scaling vehicle production. Suppliers are therefore pivoting from volume-centric models toward value-added product lines that promise stronger margins and closer OEM collaboration, an approach reinforced by recent consolidation among global lubricant majors.

Key Report Takeaways

- By product type, engine oil led with a 59.65% share of the North America automotive lubricants market in 2025, while automatic transmission fluids are forecast to expand at a 0.98% CAGR through 2031.

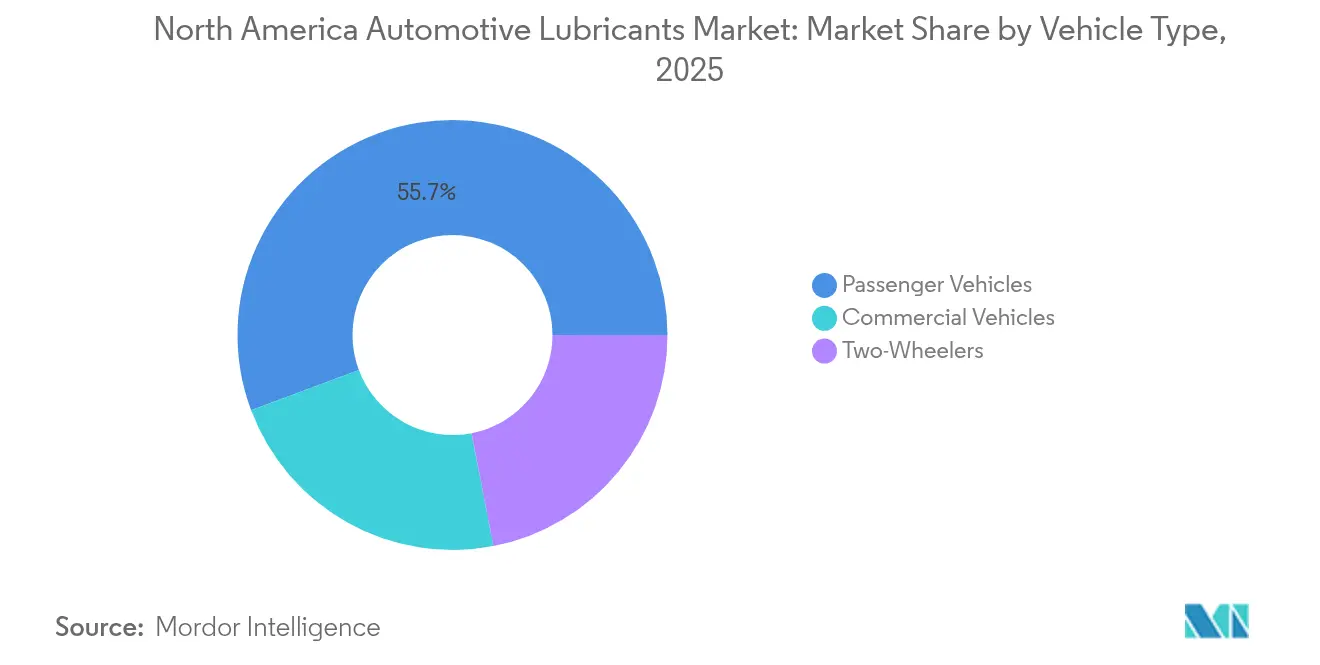

- By vehicle type, passenger vehicles accounted for 55.70% of the North America automotive lubricants market size in 2025, and commercial vehicles are expected to record the highest projected growth at a 0.92% CAGR through 2031.

- By geography, the United States commanded 86.30% of the North America automotive lubricants market share in 2025, whereas Canada represents the fastest-growing country segment at a 0.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ICE parc renewal cycle keeps base-oil demand steady | +0.3% | North America-wide, concentrated in US fleet markets | Long term (≥ 4 years) |

| Electrified light-duty fleet still requires specialty e-fluids | +0.2% | US and Canada, with Mexico emerging | Medium term (2-4 years) |

| Tier-III heavy-duty emissions norms raise lubricant performance requirements | +0.1% | US and Canada regulatory jurisdictions | Short term (≤ 2 years) |

| Mexico's OEM capacity additions (2024-27) spur factory-fill volumes | +0.2% | Mexico manufacturing corridors, spillover to USMCA trade | Medium term (2-4 years) |

| OEM-branded aftersales programs gain share | +0.1% | North America-wide, led by premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ICE Parc Renewal Cycle Keeps Base-Oil Demand Steady

The high average vehicle age continues to underpin a large portion of older internal combustion engine cars and trucks that require more frequent oil changes and higher-viscosity blends. In 2023, motor gasoline sales in Canada reached 12.7 billion litres, with 90.8% distributed through service stations, underscoring the entrenched maintenance needs of conventional powertrains[1]Statistics Canada, “Supply and Disposition of Refined Petroleum Products,” statcan.gc.ca. Vehicles exceeding 12 years of age typically follow 3,000- to 5,000-mile service intervals, counterbalancing the extended drain schedules of newer engines. Demand for conventional and high-mileage oils, therefore, remains resilient as owners of aging vehicles seek formulations that mitigate wear, manage seal swelling, and control deposits beyond 75,000 miles. This trend prolongs baseline engine-oil volumes even as fleet electrification advances.

Electrified Light-Duty Fleet Still Requires Specialty E-Fluids

Electric vehicles eliminate crankcase oil yet introduce fresh opportunities in dielectric coolants and e-axle lubricants. Petro-Canada launched its EVR range in 2024 to serve OEM and Tier-1 battery and gearbox applications. Castrol’s ON series and Valvoline’s hybrid-optimized synthetics follow similar strategies that shift the conversation from liter-based sales to premium chemistry. Mexican EV production increased from 6,717 units in 2020 to 206,870 units in 2024, with 95% of the units exported, thereby tying regional e-vehicle demand to cross-border trade flows. Thermal management for batteries and power electronics requires precise control of conductivity, which favors suppliers with advanced additive expertise and close OEM ties.

Tier-III Heavy-Duty Emissions Norms Raise Lubricant Performance Requirements

New rules covering particulate and nitrogen oxide output in commercial vehicles raise viscosity stability and low-ash thresholds for diesel oils. API CK-4 and FA-4 categories target 2017-plus engines, demanding resistance to oxidation, aeration, and soot-driven shear loss. FA-4 formulations are limited to XW-30 grades and exhibit high-temperature shear of 2.9-3.2 cP[2]American Petroleum Institute, “API Service Categories CK-4 and FA-4,” api.org. Compliance also mandates compatibility with low-sulfur fuels and sensitive aftertreatment hardware such as diesel particulate filters. The technical hurdles reward producers that invest in test rigs, engine benches, and rigorous field validation, shifting sales toward higher-value synthetics.

Mexico OEM Capacity Additions Spur Factory-Fill Volumes

Investments from BMW, Audi, and a growing constellation of Chinese component suppliers broaden Mexico’s role as a production hub. BMW is investing USD 540 million in battery assembly in San Luis Potosí for Neue Klasse models that are scheduled to roll off the lines in 2027. Alongside Audi’s USD 1 billion plant upgrade and more than 30 Chinese supplier projects, this wave is expected to increase demand for stamping press oils, coolant lubricants, and factory-fill transmission fluids. Because 87% of Mexican-built vehicles are shipped to the United States, the ripple effect reaches lubricant distributors across the border.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Longer drain intervals in new engines | -0.2% | North America-wide, concentrated in new vehicle segments | Long term (≥ 4 years) |

| EV penetration in light-duty segment | -0.1% | US and Canada urban markets, Mexico export production | Medium term (2-4 years) |

| Consolidation of quick-lube chains squeezes independent distributors | -0.1% | US and Canada retail markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Longer Drain Intervals in New Engines

ILSAC GF-7 licensing, first issued in March 2025, supports 7,500-10,000-mile oil changes, cutting annual lubricant volume per vehicle by up to 50% compared with legacy schedules. Low-viscosity 0W-16 and 0W-20 grades further extend service windows while boosting fuel economy. Fleet operators are increasingly deploying oil-analysis services to extend intervals even longer, thereby magnifying the impact on consumption. API’s aftermarket audit program now monitors bulk and packaged oils for viscosity retention and oxidative stability, putting pressure on producers that cannot meet extended-service claims.

EV Penetration in Light-Duty Segment

Battery electric cars displace 4-6 quarts of engine oil per vehicle, yet they demand only modest volumes of e-fluid. Mexican sales of electrified vehicles reached 124,310 units in 2024, accounting for 8.3% of the market. However, EV investment announcements declined by 97.4% in the first half of 2025, indicating uncertain near-term scaling. Each BEV uses roughly 1-2 quarts of e-axle lubricant and specialized coolants, producing a net negative swing in liters. The substitution ratio, therefore, erodes baseline demand in the North America automotive lubricants market even as it unlocks high-margin specialty niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oil Dominance Faces E-Fluid Challenge

The engine oil category retained a 59.65% share of the North America automotive lubricants market in 2025, underscoring its role as the largest revenue contributor. Within this space, high-mileage formulations and synthetics command premium price points that help offset the volume drag from longer drain times. Automatic transmission fluids represent the fastest-growing product line, with a 0.98% CAGR, driven by the increasing demand for multi-speed automatics, dual-clutch units, and hybrid gearsets that require tailor-made friction characteristics. The North America automotive lubricants market size for transmission fluids is projected to expand steadily as OEM design complexity increases. Brake fluids maintain a steady demand due to the integration of advanced driver assistance systems, which place higher temperature stress on hydraulics.

EV-specific e-fluids remain a small but growing segment, capturing value through sophisticated chemistry rather than the volume of gallons moved. Castrol, Valvoline, and Petro-Canada have all launched dielectric coolants and e-axle lubes designed to preserve copper windings and power electronics under high voltage. Manual gearbox oils and power steering fluids are trending downward as electric power steering architectures eliminate hydraulic systems. Greases, meanwhile, capture incremental growth from high-speed electric motor bearings requiring tighter shear-stability control. Across each sub-category, OEM approvals increasingly dictate specification, pushing suppliers to secure factory fill endorsements to protect downstream aftermarket pull-through.

By Vehicle Type: Commercial Vehicles Drive Performance Innovation

Passenger cars accounted for 55.70% of the North America automotive lubricants market size in 2025, reflecting the significant weight of the light-duty parc. Even so, heavy-duty trucks and buses deliver the highest innovation pace due to tougher emissions limits and total-cost-of-ownership pressures. Commercial fleets are predicted to achieve a 0.92% CAGR through 2031, aided by API CK-4 and FA-4 oils that enable fuel economy gains and longer drains while safeguarding aftertreatment hardware. The North America automotive lubricants market share for FA-4 grades is rising as OEMs certify more engines for lower viscosity.

Oil analysis programs have become standard in long-haul fleets, replacing time-based schedules with data-driven triggers that safely stretch intervals. This approach boosts demand for premium synthetics with superior oxidation resistance. In the two-wheeler niche, Harley-Davidson and other motorcycle manufacturers specify proprietary primary-drive and wet-clutch lubricants, allowing brand owners to capture elevated margins despite comparatively small volumes. Electric scooters and motorcycles are still in their infancy, yet they demonstrate potential for specialty greases that can handle high-rpm motor bearings and regenerative braking loads.

Geography Analysis

The United States dominated the market with an 86.30% share in 2025, buoyed by an aftermarket that includes roughly 1,500 Valvoline Instant Oil Change outlets, as well as thousands of independent shops. Dense highway mileage and a record average vehicle age of more than 12 years sustain robust demand for engine oils and transmission fluids. API and ILSAC standards shape product formulation, creating technical barriers that favor incumbents with large R&D budgets. Aramco’s acquisition of Valvoline Global Operations in April 2025 provides the Saudi major with a vertically integrated platform to combine its base-oil output with downstream branded retail operations.

Canada, while smaller, is projected to post the fastest CAGR of 0.85% through 2031. Harsh weather and heavy resource extraction activities in the oil sands necessitate premium low-temperature and high-shear oils. In 2023, Canadian secondary distributors moved 23.9 billion litres of refined petroleum products, 94.3% of which were motor gasoline and diesel, indicating a strong pull-through for lubricants. Petro-Canada Lubricants supports domestic demand via its PROTECT&GO quick-lube network and contributed fluids to Project Arrow, the country’s first zero-emissions concept vehicle.

Mexico’s share, while modest, is poised to climb on the back of aggressive OEM investment. BMW will channel USD 855 million into Nuevo León, including USD 540 million for battery assembly, with production slated for 2027. Audi and more than 30 Chinese suppliers add further capacity, pushing factory-fill requirements for engine oils, ATFs, brake fluids, and e-fluids. Although EV-related capital outlays dipped sharply in early 2025, Mexico’s export orientation means volumes produced locally directly influence United States aftermarket patterns. Trade policy uncertainties and potential tariff shifts form a risk backdrop that could alter lubricant demand trajectories.

Competitive Landscape

The North America Automotive Lubricants Market is fairly consolidated, with integrated majors and specialty formulators competing on technology, brand, and channel reach. Innovation pipelines focus on additive packages that balance oxidation control, deposit management, and low-temperature pumpability while meeting stricter greenhouse gas regulations. ILSAC GF-7 and the proposed ILSAC GF-8, alongside API FA-4, demand ongoing formulation tweaks. Companies with dedicated engine test stands and OEM relationships hold an advantage, as validation cycles become longer and more costly.

North America Automotive Lubricants Industry Leaders

Chevron Corporation

ExxonMobil Corporation

BP p.l.c.

Saudi Arabian Oil Co.

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Pennzoil-Quaker State Company, a subsidiary of Shell PLC, and Blue Tide Environmental, LLC, announced the completion of a used re-refining facility in Baytown, Texas, which will produce high-quality, eco-friendly base oils and expand Shell's sustainable lubricant offerings.

- October 2024: Hindustan Petroleum Corporation Limited (HPCL) has achieved a significant milestone by exporting HP LUBRICANTS to the United States for the first time, extending its global presence. This development is expected to increase competition in the US market, diversify lubricant options, and drive innovation with high-quality alternatives for consumers.

North America Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

By Geography

| United States |

| Canada |

| Mexico |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| By Geography | United States | |

| Canada | ||

| Mexico |

Key Questions Answered in the Report

How large is the North America automotive lubricants market in 2026?

The market reached 4.62 billion litres in 2026 and is forecast to grow to 4.81 billion litres by 2031.

What segments are expanding fastest within the region?

Automatic transmission fluids and commercial-vehicle lubricants are pacing ahead, with projected CAGRs of 0.98% and 0.92% respectively.

Which country is the top consumer of automotive lubricants in North America?

The United States accounted for 86.30% of regional demand in 2025, far outpacing Canada and Mexico.

How are electric vehicles affecting lubricant consumption?

Battery electric cars remove engine-oil needs but create high-margin demand for e-axle and dielectric fluids, resulting in lower overall volumes but elevated value potential.

What recent deals have reshaped the competitive landscape?

Aramco bought Valvoline Global Operations for USD 2.65 billion in April 2025, while FUCHS acquired LUBCON for EUR 40 million in July 2024, signaling ongoing consolidation.

Page last updated on: