Synthetic Lubricants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

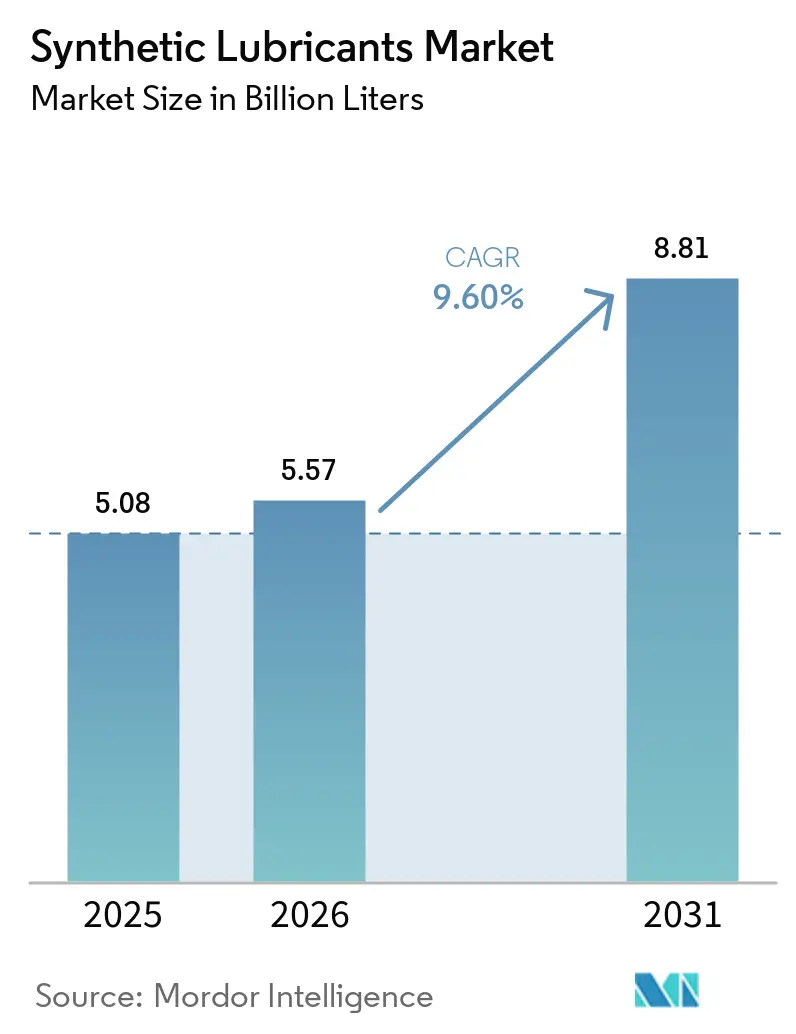

| Market Volume (2026) | 5.57 Billion liters |

| Market Volume (2031) | 8.81 Billion liters |

| Growth Rate (2026 - 2031) | 9.60% CAGR |

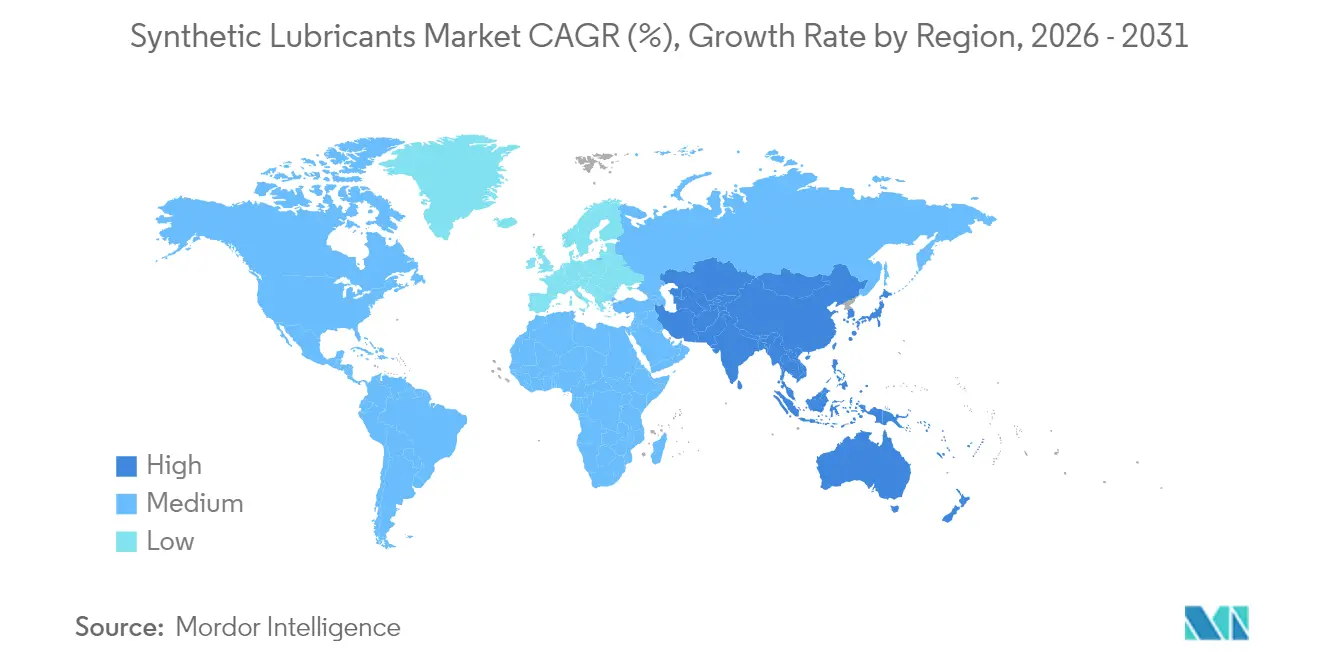

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

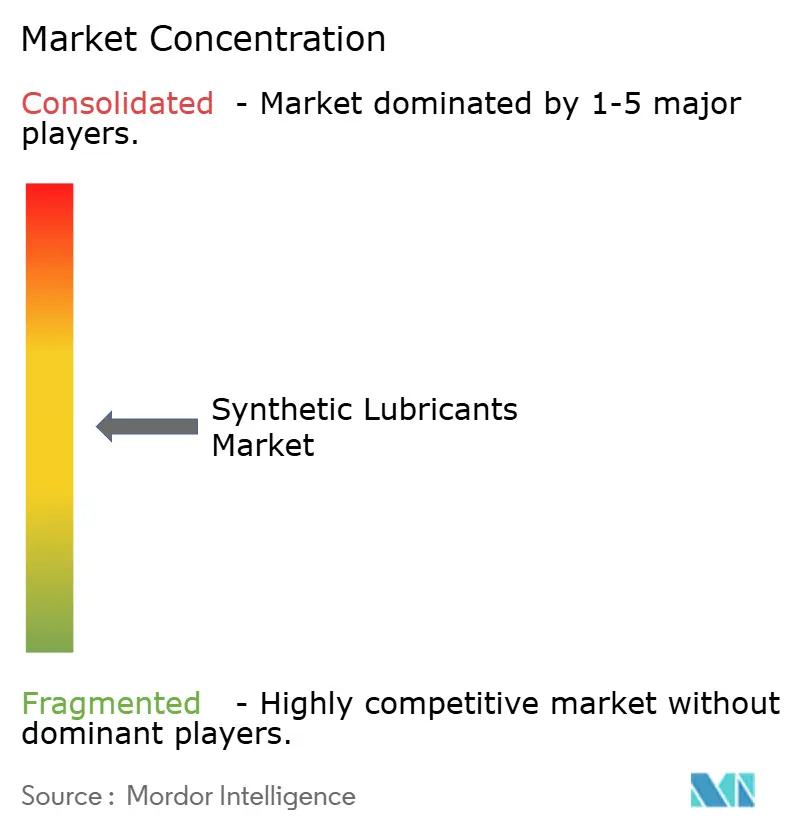

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Synthetic Lubricants Market Analysis by Mordor Intelligence

Synthetic Lubricants market size in 2026 is estimated at 5.57 Billion liters, growing from 2025 value of 5.08 Billion liters with 2031 projections showing 8.81 Billion liters, growing at 9.6% CAGR over 2026-2031. Rising demand for lower-viscosity engine oils, accelerated regulatory pressure on fuel economy, and the rapid adoption of high-performance fluids across automated manufacturing lines are the principal growth engines. The synthetic lubricants market is also benefiting from the introduction of the ILSAC GF-7 specification, effective March 2025, which compels automakers and service networks to shift toward advanced PAO and PAG-based formulations. Continuous investments in metallocene PAO capacity, together with product launches tuned for new API and ACEA categories, reinforce supply security and spur formulation innovation. Against this backdrop, Asia-Pacific maintains leadership on both consumption and growth, aided by China’s large manufacturing base and India’s recovering vehicle parc.

Key Report Takeaways

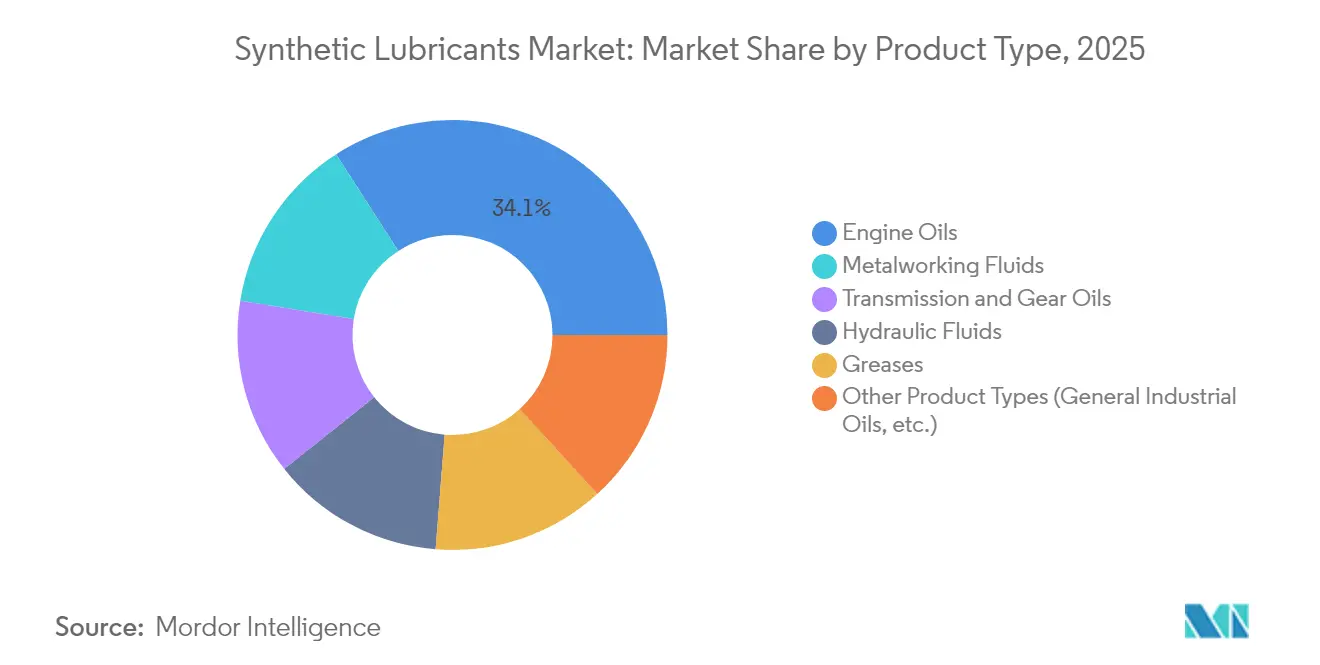

- By product type, engine oils retained 34.10% of the synthetic lubricants market share in 2025, whereas metalworking fluids are projected to grow the fastest at an 10.84% CAGR to 2031.

- By base oil, Polyalpha-Olefin (PAO) held 45.70% of the synthetic lubricants market share in 2025; Polyalkylene Glycol (PAG) is forecast to expand at an 10.95% CAGR through 2031.

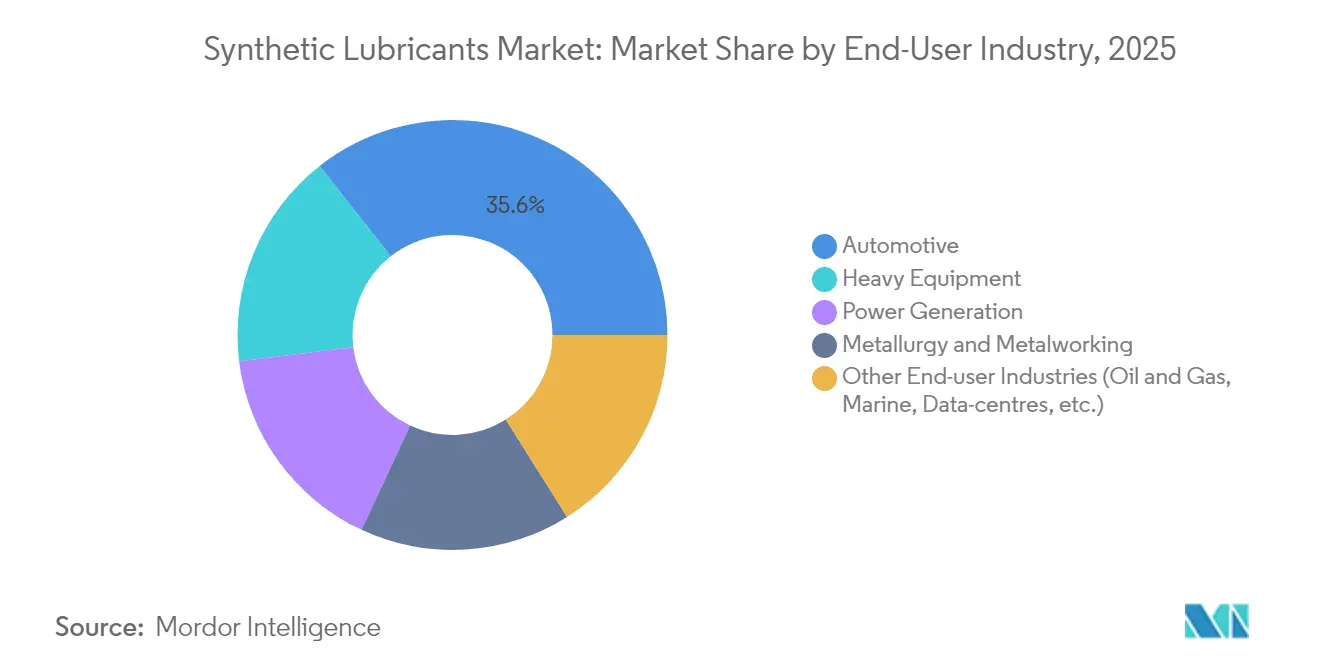

- By end user, automotive applications accounted for 35.60% of the synthetic lubricants market size in 2025, while heavy equipment is poised to post a 10.35% CAGR to 2031.

- By geography, Asia-Pacific commanded 40.00% of the synthetic lubricants market in 2025 and is advancing at an 10.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Synthetic Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Usage of High-Performance Synthetic Engine Oils in the Automotive Aftermarket | + 2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Stringent Emission & Fuel-Economy Regulations | + 2.5% | Global, led by Europe (Euro 7), North America (EPA 2026), Asia-Pacific (China VI) | Long term (≥ 4 years) |

| Growth in Industrial Automation Demanding Advanced Hydraulic & Gear Oils | + 2.2% | APAC core, spill-over to North America & Europe | Medium term (2-4 years) |

| Rapid Expansion in Aerospace & Defence Requiring Synthetic Turbine Oils | + 1.8% | North America & Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Surge in Offshore Wind Installations Boosting Long-Drain Synthetic Gearbox Oils | + 1.5% | Europe & North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Usage of High-Performance Synthetic Engine Oils in the Automotive Aftermarket

The post-2024 aftermarket pivot toward full-synthetic engine oils became pronounced once the API SQ standard entered force in March 2025. Shell’s Helix Ultra line, which satisfies the new category, demonstrates full power retention and better fuel economy, convincing service centers to recommend premium synthetics as default fills [1]Shell Plc, “Introducing Helix Ultra with PurePlus,” shell.com. Market preference is shifting rapidly to 0W-20 and even 0W-8 grades because lower viscosity improves fuel efficiency during cold starts. Valvoline’s premium full-synthetic gear oils, launched late 2024, provide four-fold wear protection over conventional products and command price premiums that customers accept when total cost of ownership is explained. North America and Europe remain at the forefront thanks to higher regulatory stringency and consumer awareness, yet momentum is spreading to urban markets in Asia-Pacific as dealership networks highlight extended drain intervals.

Stringent Emission and Fuel-Economy Regulations

July 2025 marked the planned start of Euro 7, while EPA 2026 tightens heavy-duty requirements in the United States. These rules mandate lower-viscosity grades such as 5W-20 and 0W-20, forcing lubricant formulators to boost oxidation stability to satisfy extended service limits of 650,000 miles for next-generation diesel engines. The ILSAC GF-7 specification adds LSPI protection and timing chain wear control that mineral oils struggle to achieve, making synthetic base stocks indispensable. China’s evolving China VI and India’s Bharat Stage VII frameworks are converging toward similar thresholds, which effectively globalize the most stringent requirements. Harmonized standards benefit multinational suppliers that can deploy one formulation worldwide, cutting validation cycles and strengthening economies of scale.

Growth in Industrial Automation Demanding Advanced Hydraulic & Gear Oils

Accelerated factory automation lifts demand for precision hydraulic fluids capable of stable viscosity under variable load and temperature. The National Fluid Power Association observes renewed growth in fluid-power shipments in 2025 after a cyclical trough, mirroring capital spending on automated equipment. Studies from Mobil show synthetic hydraulics can cut energy use in excavators by 3.6%, saving fuel and reducing emissions. Predictive maintenance programs add impetus as plant managers specify long-life fluids that remain in service beyond 8,000 hours between changes, decreasing downtime. Asia-Pacific is central, given large-scale industrial installations in China, India and Southeast Asia that now integrate Industry 4.0 controls and thus demand high-performance lubrication.

Rapid Expansion in Aerospace, Defense and Offshore Renewables Demanding Synthetic Turbine & Gearbox Oils

The aerospace and defense market recovered quickly, rising from USD 856.3 billion in 2022 to USD 922.2 billion in 2023, and fueled additional lubricant requirements for hotter, higher-pressure turbines. United States defense outlays of USD 886 billion in 2024 sustain military jet and naval build rates, each requiring synthetic fluids that tolerate extreme thermal loads. Parallel to this, offshore wind capacity surpassed 52 GW in the United States pipeline alone, intensifying the need for gearbox oils that last 10 years at sea while resisting white‐etching cracks. Shell’s Omala S5 Wind 320 and ExxonMobil’s Mobil SHC Gear 320 WindPower illustrate the performance leap now possible, pushing the synthetic lubricants market deeper into renewable energy service niches. Combined, aerospace, defense and offshore renewables elevate demand for high-temperature ester, PAO and PAG blends embedded with advanced anti-wear chemistries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Upfront Cost Versus Mineral Oils | -1.8% | Global, most pronounced in price-sensitive emerging markets | Short term (≤ 2 years) |

| Growing Electric-Vehicle Fleet Reducing Demand for Engine Oils | -1.5% | Europe & North America leading, Asia-Pacific following | Medium term (2-4 years) |

| Volatility in Polyalphaolefin (PAO) Feed-Stock Supply | -1.2% | Global, with supply concentration in North America & Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost of Synthetic Lubricants

Full-synthetic products often sell at prices two to three times those of mineral oils, a differential that remains a stumbling block in cost-sensitive segments. In short duty cycles the benefit of extended drains is muted, preventing fleet managers in developing economies from justifying the premium. Caltex data confirm that where service intervals sit below 5,000 km, ROI is difficult to secure. Rising crude prices, however, are lifting the cost base of mineral oils faster than synthetics, narrowing the gap. Meanwhile, predictive maintenance tools underscore lifetime savings, gradually eroding resistance among commercial fleets.

Growing Electric-Vehicle Fleet

Pure battery EVs dispense with engine oils altogether, tightening the outlook for traditional crankcase lubricants in mature markets. The American Chemical Society projects notable reductions in automotive lubricant volumes as EV adoption accelerates. Nonetheless, electrification opens adjacent opportunities in e-transmission fluids, thermal management of coolants, and dedicated grease formulations. Shell’s EV-Plus fluids and TotalEnergies’ water-based e-lubricant, which cuts global warming potential by 30%, highlights the pivot toward purpose-built fluids for electric drivetrains. The synthetic lubricants market therefore pivots rather than contracts, shifting its product mix while maintaining value growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Lead Despite EV Headwinds

Engine oils captured 34.10% of the synthetic lubricants market in 2025 by volume, a position protected by the vast installed base of internal-combustion vehicles and the superior longevity synthetics deliver. Transmission and gear oils follow as the second-largest category because automated manufacturing lines and wind turbines both require high-load, clean-running formulations. Hydraulic fluids benefit from a construction upswing and robotics integration, supplying stable viscosity across wide temperature spreads. Greases remain indispensable in aerospace actuators and heavy machinery joints where drip-free lubrication is vital. Metalworking fluids, though holding a smaller volume share, advance at the fastest 10.84% CAGR as precision machining and additive manufacturing mature.

The segment outlook is shaped by ILSAC GF-7 and API SQ, both of which reduce permissible wear and LSPI occurrence. This shift favors premium synthetics that can sustain longer drains, reducing workshop visits, and oil disposal. Furthermore, metalworking fluids with low mist and high flash points mitigate occupational hazards, leading factories to migrate to synthetic ester-and-PAG systems. Together, these trends ensure that the synthetic lubricants market size for fluids beyond engine oils will expand steadily through 2031.

By Base Oil: PAO Dominance Faces PAG Challenge

Polyalphaolefins occupied 45.70% of the synthetic lubricants market in 2025 because OEMs endorse their balanced cold-flow and high-temperature capability. ExxonMobil’s SpectraSyn MaX shows how metallocene catalysts enable ultra-low volatility, improving fuel economy in 0W-16 and thinner grades. Ester-based stocks retain a foothold in aviation, where flashpoint and elastomer compatibility matter, while Group III and GTL synthetics gain share thanks to lower cost and wider availability.

PAG base oils are scaling quickly at an 10.95% CAGR, propelled by electric-vehicle driveline and compressor requirements. Superior thermal conductivity and sludge-free oxidation products grant PAG fluids an edge in compact e-motors and direct-drive compressors. Chevron Phillips Chemical’s upgraded Kingwood R&D center, opened 2024, underlines incumbent commitment to innovation in conventional PAO even as PAG rises. The interplay between PAO enhancements and PAG penetration will define competitive positioning over the forecast horizon, ensuring the synthetic lubricants industry focuses equally on legacy and emerging chemistries.

By End User: Automotive Leads While Heavy Equipment Accelerates

Automotive applications represented 35.60% of the synthetic lubricants market size in 2025, anchored by OEM factory-fill programs and an aftermarket that increasingly insists on full synthetics for warranty compliance. Heavy equipment, from articulated dump trucks to hydraulic excavators, is the star performer with a 10.35% CAGR. Caterpillar, for instance, treats fluids as engineered components of the drivetrain, driving demand for premium TO-4 and FD-1-compliant synthetics that extend overhaul intervals .

Power generation consumes rising volumes of ester-and-PAO turbine oils as offshore wind buildouts proliferate, while metallurgy and precision machining employ metalworking fluids that stabilize tooling temperatures and reduce scrap. Data centers are an emerging niche, adopting synthetic dielectric fluids for immersion cooling, although current volumes remain modest relative to automotive and heavy machinery. Overall, the heavy-equipment surge offsets engine-oil erosion in electrifying passenger cars, keeping the synthetic lubricants market on a clear upward path.

Geography Analysis

Asia-Pacific held 40.00% of the synthetic lubricants market in 2025, with a 10.62% CAGR outlook. China’s re-acceleration in advanced manufacturing, together with India’s double-digit vehicle sales rebound, underpins regional consumption. New blending plants in coastal China, such as Quaker Houghton’s Zhangjiagang facility scheduled for 2026, illustrate suppliers’ determination to localize supply for high-growth sectors. Japan sustains demand for high-grade factory fills, while Southeast Asian economies ramp up industrial output, widening the customer base. Vietnam lubricants market is growing, driven by automotive manufacturing and rising demand from heavy equipment operators.

North America ranks second in volume and remains a technology bellwether. EPA 2026 rules and API’s category pipeline push formulators into next-generation additive chemistry. The United States also dominates supply of high-viscosity PAO thanks to extensive propylene infrastructure, although propylene tightness predicted for mid-2025 could test margins. Canada’s oil sands and mining fleets, plus Mexico’s automotive export platforms, add stable demand pockets that rely on synthetic lubricants for uptime and warranty assurance.

Europe preserves its premium positioning through stringent environmental legislation and advanced OEM technical standards. Euro 7 compels lower viscosities and stronger aftertreatment compatibility, pushing adoption of ester-enhanced formulations in both light- and heavy-duty fleets. The North Sea offshore wind corridor and the Iberian Peninsula’s emerging renewable clusters require fill-for-life gearbox oils that tolerate brine exposure, widening scope for high-value PAG and PAO blends. Eastern Europe’s industrial base further diversifies demand as automation investments accelerate. The Middle East and Africa, while smaller, show a gradual shift from mineral to synthetic as Gulf petrochemical hubs and South African mines target longer drain intervals in harsh climates.

Competitive Landscape

The synthetic lubricants market is partially consolidated with the presence of major players, such as Exxon Mobil Corporation, Chevron Corporation, Shell plc, TotalEnergies, and BP p.l.c. (Castrol). Shell's 18-year consecutive leadership in global lubricants demonstrates the importance of scale and brand recognition in this industry. ExxonMobil expanded metallocene PAO capacity at Baytown to secure feedstock and shorten development cycles, while Chevron Oronite moves upstream into next-generation dispersant and antiwear chemistries. TotalEnergies pioneers water-based e-fluids with lower carbon footprints. Strategic partnerships between lubricant majors and OEMs, such as Shell’s multi-year alliance with BMW, extended in 2025, lock in factory-fill volumes while guaranteeing joint product development roadmaps.

Synthetic Lubricants Industry Leaders

Chevron Corporation

Shell plc

Exxon Mobil Corporation

TotalEnergies

BP p.l.c. (Castrol)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Shell launched Shell Advance Ultra full-synthetic motorcycle oil meeting the new API SP standard, utilizing PurePlus Technology to enhance engine performance and reduce evaporation while improving fuel economy for two-wheeler applications.

- November 2024: Valvoline launched its first premium full synthetic gear oil, Valvoline Extended Protection, claiming four times the gear wear protection compared to conventional products and featuring anti-foam agents and friction modifiers

Global Synthetic Lubricants Market Report Scope

Synthetic lubricants are chemically engineered lubricants derived from pure chemicals, unlike conventional lubricants refined from crude oil. These lubricants do not contain nitrogen, sulfur, or any other harmful elements that lead to sludge formation and, thereby, damage the engine or machine.

The synthetic lubricants market is segmented by product type and end-user industry. By product type, the market is segmented into engine oils, transmission and gear oils, hydraulic fluids, metalworking fluids, greases, and other product types (general industrial oils, etc.). By end-user industry, the market is segmented into power generation, automotive, heavy equipment, metallurgy and metalworking, and other end-user industries (oil and gas, etc.). The report offers market size and forecasts for 26 countries across major regions. For each segment, market sizing and forecasts are done on the basis of volume (liters) for all the above segments.

| Engine Oils |

| Transmission and Gear Oils |

| Hydraulic Fluids |

| Metalworking Fluids |

| Greases |

| Other Product Types (General Industrial Oils, etc.) |

| Polyalpha-olefin (PAO) |

| Esters |

| Polyalkylene Glycol (PAG) |

| Group III / GTL-derived Synthetic |

| Others (Alkylated Naphthalene, etc.) |

| Automotive |

| Power Generation |

| Heavy Equipment |

| Metallurgy and Metalworking |

| Other End-user Industries (Oil and Gas, Marine, Data-centres, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Engine Oils | |

| Transmission and Gear Oils | ||

| Hydraulic Fluids | ||

| Metalworking Fluids | ||

| Greases | ||

| Other Product Types (General Industrial Oils, etc.) | ||

| By Base Oil | Polyalpha-olefin (PAO) | |

| Esters | ||

| Polyalkylene Glycol (PAG) | ||

| Group III / GTL-derived Synthetic | ||

| Others (Alkylated Naphthalene, etc.) | ||

| By End User | Automotive | |

| Power Generation | ||

| Heavy Equipment | ||

| Metallurgy and Metalworking | ||

| Other End-user Industries (Oil and Gas, Marine, Data-centres, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the synthetic lubricants market?

The synthetic lubricants market size is estimated at 5.57 billion liters in 2026 and is projected to reach 8.81 billion liters by 2031, reflecting a 9.6% CAGR during 2026-2031.

Which product segment leads the synthetic lubricants market?

Engine oils lead with 34.10% market share in 2025, driven by the installed base of internal-combustion vehicles and extended drain intervals.

How fast is the Asia-Pacific region growing?

Asia-Pacific is expanding at an 10.62% CAGR through 2031, the fastest among all regions, underpinned by manufacturing and automotive growth.

What impact will electric vehicles have on lubricant demand?

EV adoption will reduce engine-oil volumes, especially in Europe and North America, yet opens new demand for e-transmission fluids and thermal management lubricants, keeping overall value growth positive.

Why are synthetic lubricants more expensive than mineral oils?

They use chemically engineered base stocks such as PAO, PAG and esters plus advanced additive systems, which cost more to formulate but deliver longer service life and energy savings that offset the higher upfront price over time.

Page last updated on: