Aviation Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 23 Million liters |

| Market Volume (2031) | 30.20 Million liters |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

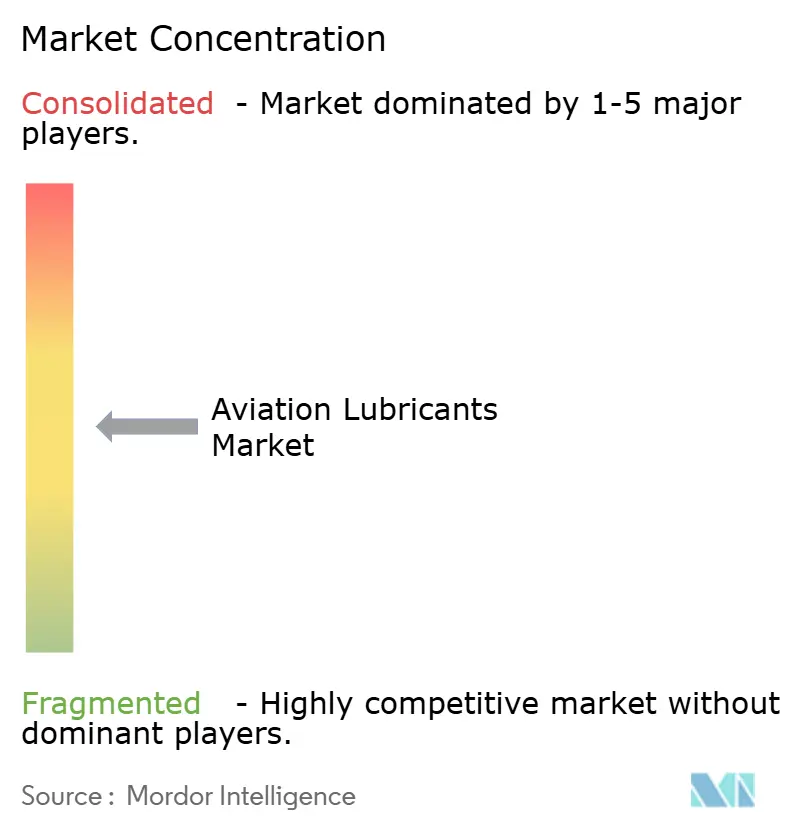

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Lubricants Market Analysis by Mordor Intelligence

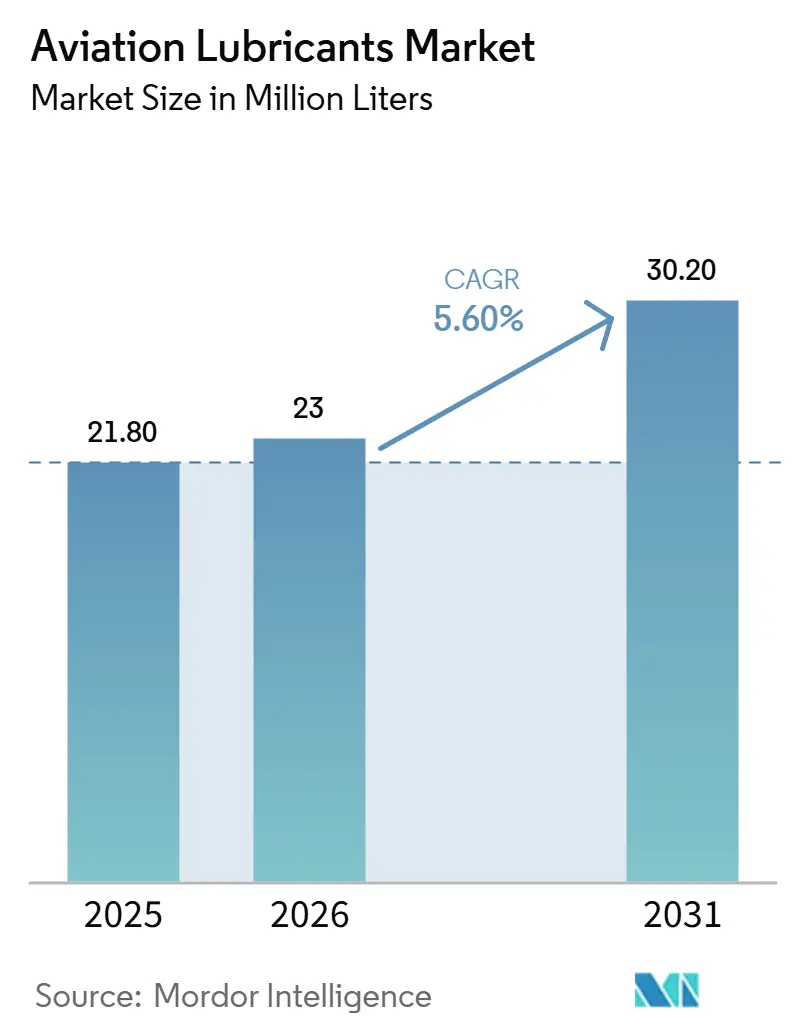

The Aviation Lubricants Market size is expected to grow from 21.80 million liters in 2025 to 23 million liters in 2026 and is forecast to reach 30.20 million liters by 2031 at 5.60% CAGR over 2026-2031. The aviation lubricants market is expanding as airline activity, defense procurement, and maintenance demand continue to drive recurring fluid replacement across engines, hydraulic systems, landing gear, and airframe systems. Long product qualification cycles benefit the market, as once a lubricant is approved for a platform or engine family, switching is limited by safety, compliance, and maintenance considerations. The market is also moving toward higher-performance synthetic formulations, as newer engines and more demanding operating conditions place greater emphasis on thermal stability, deposit control, and compatibility with approved hardware. Sustainable Aviation Fuel (SAF) adoption is creating additional market opportunities, as changes in fuel chemistry are prompting formulators and operators to assess lubricant behavior across adjacent systems and develop long-term sustainability roadmaps. Cost and approval barriers persist, and these same barriers protect incumbent suppliers and keep the competitive field narrower than in many other industrial fluid categories.

Key Report Takeaways

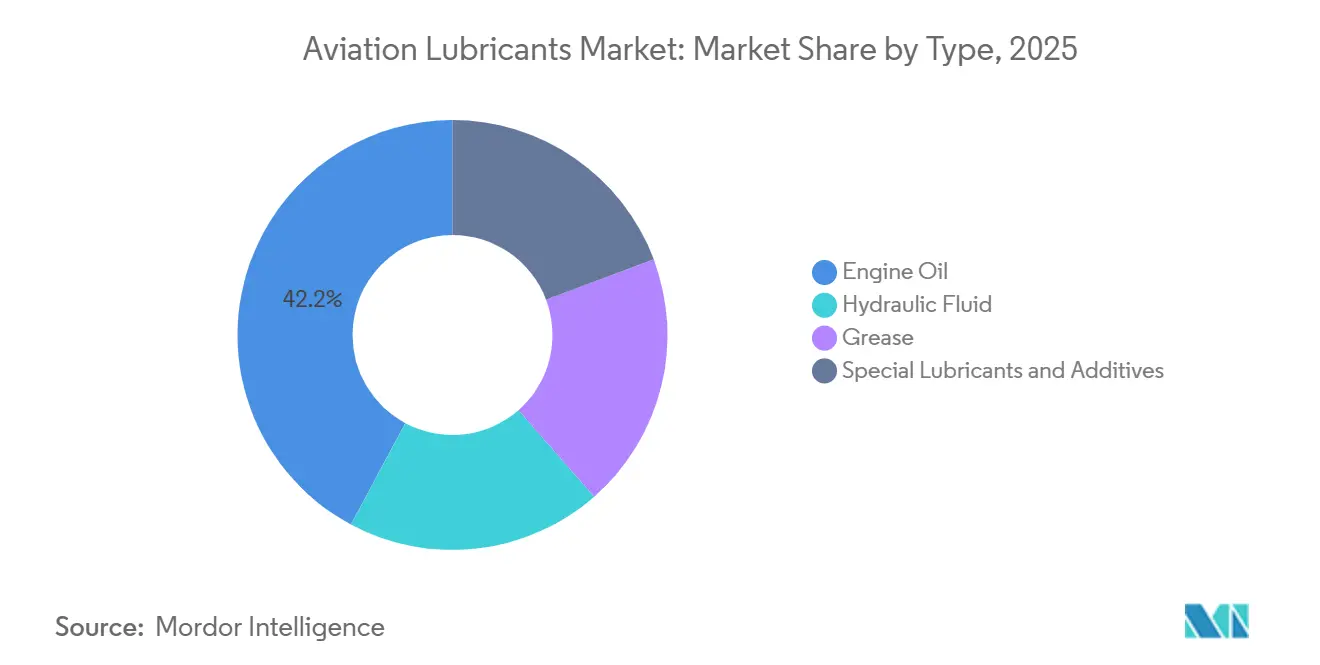

- By type, Engine Oil led with 42.18% share in 2025, while Special Lubricants and Additives are projected to expand at a 6.13% CAGR through 2031.

- By technology, Synthetic Lubricants held 63.25% share in 2025, while Bio-based Lubricants are forecast to grow at a CAGR at 7.05% through 2031.

- By platform, Commercial Aviation accounted for 55.07% share in 2025, while Military Aviation is forecast to grow at a 5.90% CAGR through 2031.

- By application, Engine Systems captured 48.12% share of the aviation lubricants market size in 2025, while Hydraulic Systems is forecast to grow at a 5.84% CAGR through 2031.

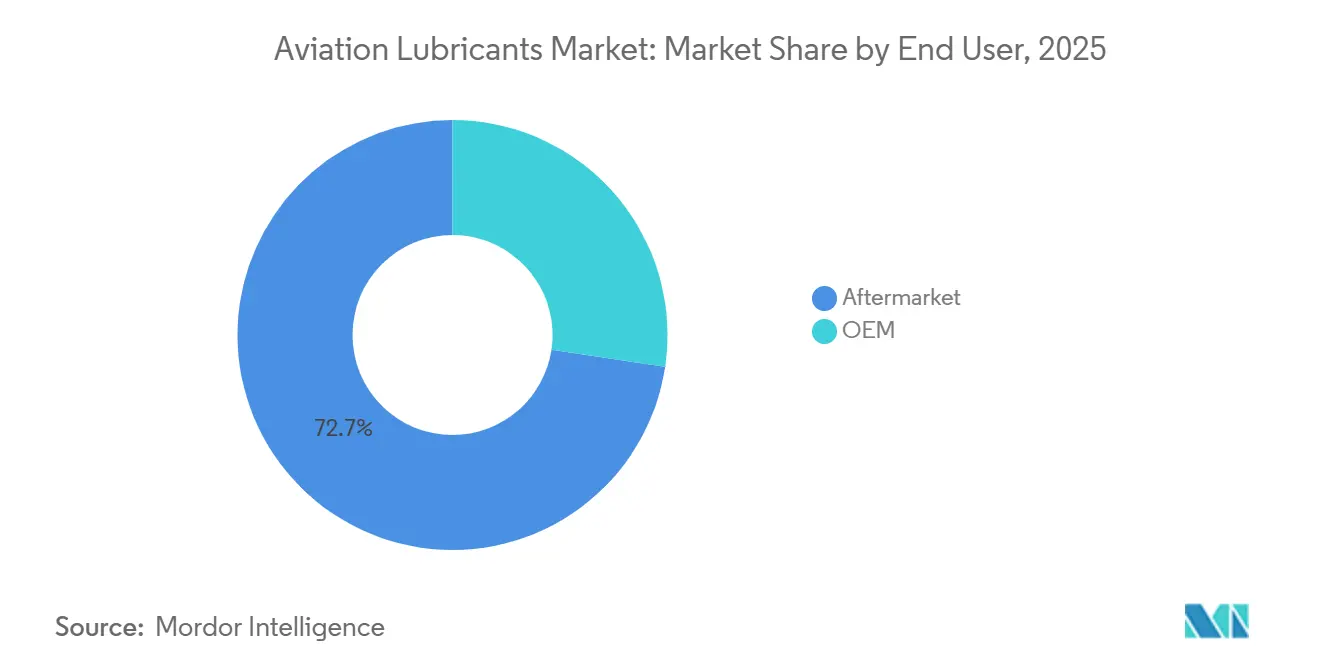

- By end user, the Aftermarket held 72.65% share in 2025, while Original Equipment Manufacturer (OEM) is projected to expand at a 5.71% CAGR through 2031.

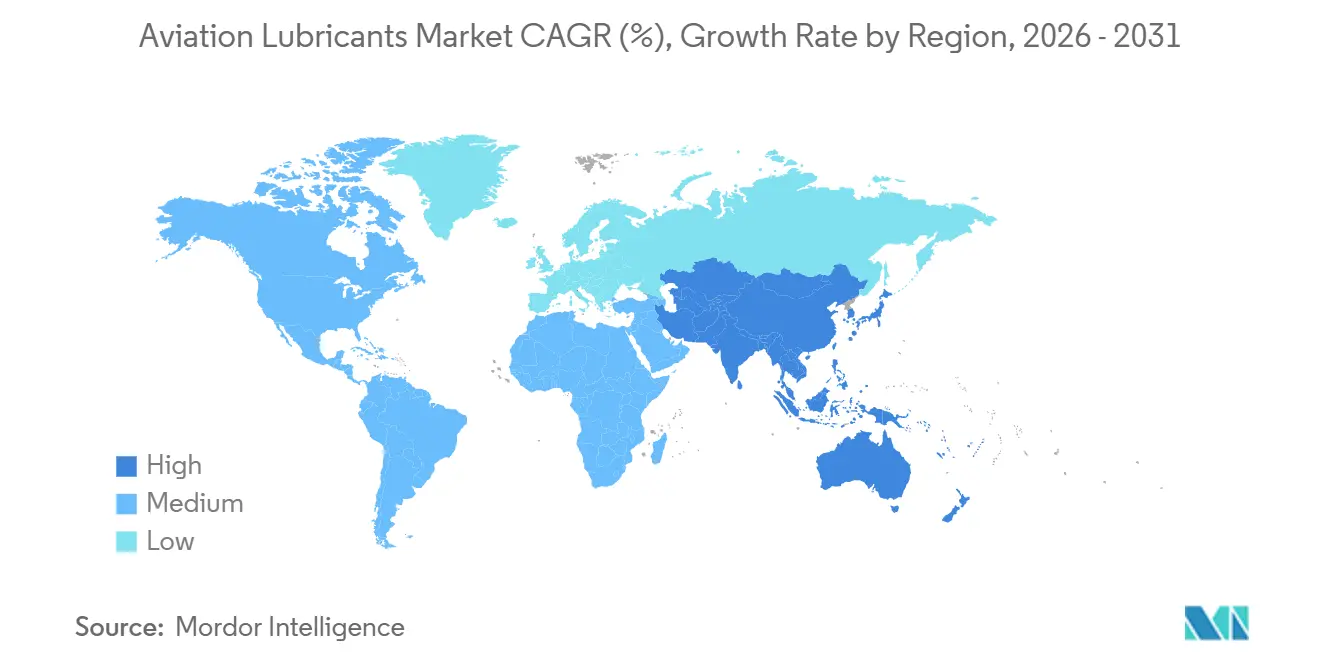

- By geography, North America held 38.02% of the aviation lubricants market share in 2025, while Asia-Pacific is expected to record the fastest CAGR at 6.08% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aviation Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet expansion and hub development | +1.8% | Global, concentrated in the Asia-Pacific and the Middle East | Long term (≥ 4 years) |

| Recurring aftermarket demand from Maintenance, Repair, and Overhaul (MRO) growth | +1.5% | North America and Europe, with spillover to the Asia-Pacific | Medium term (2-4 years) |

| Shift toward synthetic lubricants | +0.9% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| An aging fleet and deferred retirements | +0.8% | North America, Western Europe, and Africa | Short term (≤ 2 years) |

| Sustainable Aviation Fuel (SAF)-compatible lubricant development | +0.5% | European Union core, with early adoption in North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fleet Expansion and Hub Development Sustain Base Demand

Aircraft orders placed in 2026 illustrate how fleet entry feeds directly into the aviation lubricants market through Original Equipment Manufacturer (OEM) fill requirements and subsequent long maintenance cycles. AirAsia placed an order for 150 A220-300 aircraft in May 2026, adding a large block of future lubricant demand tied to new aircraft induction, fleet support, and line maintenance preparation[1]China Eastern Airlines, “Major Transaction in Relation to Aircraft Purchase,” HKEX News, hkexnews.hk. China Eastern Airlines also signed a purchase agreement for 101 A320neo aircraft in March 2026, reinforcing the same demand pattern across another major regional fleet expansion program. These orders support the aviation lubricants market before aircraft age into major shop visits, as each delivery requires approved fluids for the engine, hydraulic, landing gear, and other operating systems. Hub development adds another layer to this demand, as expanding airport ecosystems require on-site storage, handling discipline, and supply assurance for flight operations and ground support activities. Fleet growth therefore supports both the visible aircraft population and the service infrastructure that keeps lubricant consumption active across each aircraft program.

Recurring Aftermarket Demand Anchored by an Aging Global Fleet

The aviation lubricants market is heavily supported by aftermarket demand, as aircraft continue to consume approved fluids through routine use, scheduled checks, and component-specific maintenance events. IATA reported that engine maintenance rose from 41% of total MRO spend in 2019 to 50% in 2024, confirming that maintenance economics are shifting toward engine-intensive work, where lubricant quality and availability matter most[2]International Air Transport Association, “Urgent Action Needed to Ease Engine MRO Bottlenecks,” IATA, iata.org. IATA also stated in June 2026 that annual Leading Edge Aviation Propulsion (LEAP) engine shop visits are expected to rise from 600 in 2025 to more than 5,000 by 2040, indicating a significantly larger maintenance load over time. Delivery delays have kept older aircraft and engines in service longer, which benefits the aviation lubricants market as mature fleets typically require more frequent inspection, replenishment, and approved product continuity. The aftermarket share of 72.7% in 2025 indicates that the aviation lubricants market is driven more by in-service maintenance than by one-time deliveries. This structure also strengthens incumbent brands, as power-by-hour contracts and long-term MRO agreements often lock lubricant specifications into the maintenance framework rather than leaving them open to frequent rebidding.

Shift Toward Synthetic Lubricants Driven by Engine Performance Requirements

The aviation lubricants market has moved decisively toward synthetic chemistry, with synthetic lubricants accounting for 63.3% of volume in 2025. This reflects the operating requirements of modern turbine engines, which function under higher thermal and mechanical stress and therefore require stronger oxidation control, greater film stability, and greater deposit resistance than older fluid systems. These technical requirements reinforce the practical value of products that already carry broad approvals, as operators and MRO providers prefer validated performance over lower-cost alternatives. The same dynamic confines mineral-based products to narrower legacy niches, particularly in older piston-engine applications that do not represent the mainstream growth path of the aviation lubricants market. Product qualification requirements also reinforce the position of synthetic lubricants, as a new entrant must demonstrate not only fluid performance but also repeatability, traceability, and compatibility with platform-specific service expectations. The shift toward synthetics in the aviation lubricants market reflects a structural response to engine evolution and the long approval cycles of aerospace products.

SAF-Compatible Lubricant Formulation Opens Reformulation Opportunities

The aviation lubricants market is entering a reformulation phase as Sustainable Aviation Fuel (SAF) adoption moves from pilot programs to regulated fuel supply in key regions. The U.S. Department of Energy (DOE) and National Renewable Energy Laboratory (NREL) noted that SAF pathways, such as synthetic paraffinic kerosene, have lower aromatic content than conventional jet fuel, which can alter material interactions and raise compatibility concerns for fuel-adjacent systems. From January 2025, EU airports were required to supply aviation fuel with a minimum 2% SAF share under ReFuelEU Aviation, and this requirement will tighten over time. This policy shift is relevant for the aviation lubricants market because airlines, Maintenance, Repair, and Overhaul (MRO) providers, and formulators are evaluating how lubricant systems perform within a broader sustainability and compatibility context. Research published in RSC Sustainability in February 2026 found that commercial-scale biobased polyol ester base oils can match the tribological performance of fossil-derived equivalents while reducing lifecycle carbon intensity. This does not indicate immediate mass conversion in the aviation lubricants market, but product development and qualification spending are moving toward a wider range of future-ready fluid options.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material and specification volatility | -0.5% | Global, most acute in Europe and the Asia-Pacific | Medium term (2-4 years) |

| High cost of premium aviation lubricants | -0.3% | Emerging markets and smaller carriers globally | Medium term (2-4 years) |

| Lengthy Original Equipment Manufacturer (OEM) and airworthiness approval process | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material Volatility and Specification Pressures Compress Margins

The aviation lubricants market remains exposed to raw material price swings because advanced formulations rely on specialized synthetic inputs that cannot be readily substituted when input costs change. This exposure is significant because aviation customers require consistency, documentation, and uninterrupted product performance across long service intervals and safety-critical systems. The specification requirements in the aviation lubricants market are unusually stringent, as approved formulations must comply with industry and military standards, as well as engine- or platform-specific approval lists. As a result, blenders cannot respond to cost pressures as flexibly as in conventional industrial lubricants, since even minor formulation changes may trigger additional review and validation. Premium aviation lubricants therefore carry a persistent cost burden for smaller carriers and emerging operators that have limited purchasing leverage or weaker local supply depth. Consequently, the aviation lubricants market can grow steadily while still facing margin pressure, slower reformulation decisions, and uneven affordability across operator groups.

Lengthy OEM and Airworthiness Approval Timelines Constrain Product Entry

The aviation lubricants market is difficult to enter because product commercialization depends on regulatory compliance, Original Equipment Manufacturer (OEM) testing, and formal approval within platform-specific maintenance documentation. ExxonMobil Aviation states that a new oil technology must satisfy technical standards, pass OEM ground and on-wing testing, and then move through service bulletin approval, a process that typically spans 10 to 15 years across targeted engine families. The aviation lubricants market therefore gives a clear advantage to suppliers that already hold approved products, have deep engineering support, and can manage long, multi-engine qualification programs. China's Civil Aviation Administration (CAAC) illustrates this barrier in practical terms: the first Chinese technical standard for aviation hydraulic oil was issued in December 2020, while the first domestic airworthiness certificate for aviation hydraulic oil was granted only in July 2025. That single milestone took five years for one fluid family in one jurisdiction, demonstrating why expansion in the aviation lubricants market is driven more by qualification depth than by quick product launches. These timelines also slow the pace at which bio-based, reduced-toxicity, or Sustainable Aviation Fuel (SAF)-compatible alternatives can move from promising chemistry to scaled commercial adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Engine Oils and Specialty Additives Define Market Poles

Engine oil held 42.2% of aviation lubricants market share in 2025, confirming that the largest volume segment remains tied to turbine reliability and aircraft dispatch continuity. Engine oil demand remains durable because lubricant consumption is linked to actual operations, routine replenishment, and maintenance checks rather than one-time installation. Operators rarely treat engine oil as a simple consumable, as deviations in product performance carry consequences for maintenance planning and approved operating limits. This keeps replacement behavior conservative and supports established brands already embedded in approved maintenance systems. Hydraulic fluids and greases represent smaller segments but remain critical to the aviation lubricants market, as each supports safety-critical mechanical functions with strict compatibility requirements.

The type mix also indicates that growth in the aviation lubricants market will not come exclusively from the highest-volume category, as higher-specification subsegments are gaining importance alongside increasing equipment complexity. Special lubricants and additives is the fastest-growing type segment at 6.13% CAGR through 2031, reflecting rising demand for targeted formulations in areas where standard turbine oils alone do not address deposit, seal, or thermal management needs. This segment benefits from engine programs requiring tighter control over cleanliness, material interaction, and performance stability across more demanding duty cycles. It also benefits from customer preference for products that combine high performance with lower handling risk and stronger compliance support across maintenance environments. Over time, the aviation lubricants market is likely to see a wider spread between high-volume standard categories and smaller, faster-growing premium formulations with greater technical differentiation.

By Technology: Synthetic Leadership Is Secure, Bio-Based Is the Insurgent

Synthetic lubricants accounted for 63.25% of aviation lubricants volume by technology in 2025, reflecting the alignment between turbine engine requirements and polyol ester-based performance characteristics. In the aviation lubricants market, synthetic products are embedded in operating practice because modern fleets depend on fluids capable of handling higher temperature exposure and tighter performance tolerances. This gives the market a technology structure where the dominant chemistry is supported by both engineering requirements and approval history. Mineral-based products retain a niche in older piston-engine and legacy applications, but that installed base no longer defines the central direction of the aviation lubricants market. As fleet activity increasingly centers on modern turbine platforms, synthetic lubricants maintain their dominant position.

Bio-based lubricants are the fastest-growing technology segment at 7.05% CAGR through 2031, though growth starts from a smaller base within the aviation lubricants market. The primary drivers are sustainability policy and evidence that bio-derived base oils can meet required performance under commercial conditions. A February 2026 RSC Sustainability study reported that bio-based polyol ester base oils can match fossil-derived counterparts on tribological performance while lowering lifecycle carbon intensity. At the same time, a 2025 review in the Journal of Aerospace Sciences and Technologies noted that low-temperature thermooxidative stability remains a central certification barrier for aircraft biolubricants. Mainstream penetration will depend on whether certification pathways and approved application windows expand meaningfully before 2031.

By Platform: Commercial Base Remains Dominant, Military Demand Accelerates

Commercial aviation accounted for 55.07% of aviation lubricants market volume by platform in 2025, driven by the volume of flight cycles, route utilization patterns, and maintenance events generated by airline fleets. The aviation lubricants market draws steady volume from commercial operators because every expansion in aircraft deployment creates follow-on demand across line maintenance, scheduled checks, and long-term overhaul planning. Large airline orders also reinforce future lubricant demand by enlarging the installed base that will subsequently move through aftermarket service. AirAsia's 150-aircraft A220 order and China Eastern's agreement for 101 A320neo aircraft both support that medium-term installed base effect in Asia. Business and general aviation remains smaller by volume but still matters in the aviation lubricants market, as operators often use premium specification products and maintain tighter service discipline across lower-utilization, high-value equipment.

Military aviation is the fastest-growing platform segment at 5.90% CAGR through 2031, increasing its role within the aviation lubricants market even as the commercial base remains larger. Defense procurement is supporting this shift, as new fighter, transport, and rotary-wing programs require approved lubricants tied to military standards and platform-specific maintenance documentation. Military demand is also less exposed to passenger traffic volatility, making this part of the aviation lubricants market more stable during civil aviation disruptions. The segment further benefits from long service lives and structured sustainment programs, as an approved lubricant can remain embedded across operating years and support contracts. This combination of procurement continuity, qualification discipline, and mission-critical performance requirements gives military aviation a stronger growth profile than its current share alone would suggest.

By Application: Engine Systems Dominates, Hydraulics Gains Ground

Engine systems commanded 48.12% of the aviation lubricants market by application in 2025, keeping this application at the center of demand planning, product qualification, and aftermarket brand retention. This share aligns with International Air Transport Association (IATA) FY2024 maintenance data, which showed engine maintenance rising to 50% of total maintenance, repair, and overhaul (MRO) spend from 41% in 2019. Engine-related fluids are especially important in the aviation lubricants market because they are consumed continuously during use and require close monitoring within approved maintenance intervals. The application also carries high documentation sensitivity, which strengthens supplier retention once a product is validated within engine-specific operating environments. Landing gear, airframe, and other applications add secondary demand in the aviation lubricants market, particularly where corrosion control, load-bearing performance, and environmental durability are required.

Hydraulic systems is the fastest-growing application at 5.84% CAGR through 2031, reflecting both technical complexity and regulatory momentum in the aviation lubricants market. Hydraulic circuits remain central to flight control and actuation across large commercial and military platforms, so fluid reliability stays critical even as broader aircraft architecture evolves. The Civil Aviation Administration of China (CAAC) milestone in July 2025, which granted the first domestic airworthiness certificate for an aviation hydraulic oil under China's local framework, demonstrated the institutional focus on this product category. Hydraulic fluids are gaining strategic weight in the aviation lubricants market from both aircraft design requirements and national efforts to build local certification and supply capability. As sustainable aviation fuel (SAF) adoption broadens, system-level compatibility reviews, including hydraulic formulations, could receive additional attention given their relevance to sealing, material, and maintenance performance.

By End User: Aftermarket Maintains Structural Dominance, OEM Grows with Deliveries

The aftermarket held a 72.65% volume share among end users in 2025, making it the primary structural anchor of the aviation lubricants market. This dominance exists because lubricant demand is more closely tied to aircraft use and maintenance than to individual delivery events. Operators cannot defer oil changes or approved fluid replacements beyond maintenance thresholds, so recurring service demand remains strong even when fleet expansion slows. Long-term MRO agreements and power-by-the-hour structures further centralize lubricant decisions, often placing brand selection in the hands of specialized maintenance providers rather than individual airline purchasing teams. This framework keeps the aviation lubricants market closely linked to the installed fleet and the maintenance ecosystem that supports it.

The original equipment manufacturer (OEM) segment is the fastest-growing end-user category, with a 5.71% CAGR through 2031, driven by the release of deferred aircraft deliveries and the requirement for complete initial fluid fills on each new platform. The aviation lubricants market gains volume from every delivery, as engines, hydraulic systems, landing gear, and airframe-related service points all require approved products before aircraft enter service. Large commercial aircraft orders announced in 2026 suggest that this initial-fill channel will remain active as production normalizes and delivery schedules improve. Even so, the aviation lubricants market will continue to rely more heavily on aftermarket turnover, as initial fills represent the first volume event while maintenance drives the longer tail of recurring consumption. Predictive maintenance tools may refine drain interval management at the margin, but they are more likely to adjust usage patterns than to alter the basic end-user structure of the aviation lubricants market.

Geography Analysis

North America retained the largest regional share at 38.02% of the aviation lubricants market in 2025, reflecting the region's dense Maintenance, Repair, and Overhaul (MRO) infrastructure, large installed fleet, and high concentration of widebody and commercial operators. The North American aviation lubricants market also benefits from the region's extensive approval history, broad technical service presence, and established suppliers that support both civil and defense requirements. Mature-fleet conditions continue to sustain lubricant replacement demand, as maintenance intensity remains high even as newer aircraft gradually enter the mix. Canada and Mexico contribute to this regional base through expanding airline activity and fleet support requirements, though the United States remains the principal volume driver in the aviation lubricants market.

Asia-Pacific is the fastest-growing geography, with a 6.08% CAGR through 2031, making it a key regional growth engine in the aviation lubricants market. Major aircraft orders are a central factor, with AirAsia ordering 150 A220-300 aircraft in May 2026 and China Eastern signing for 101 A320neo aircraft in March 2026. These programs expand the future installed fleet and support both Original Equipment Manufacturer (OEM)-fill and aftermarket demand across the aviation lubricants market. The region is also developing greater maintenance depth, which is significant because lubricant consumption scales not only with aircraft numbers but also with local service capacity and inventory management. China's domestic certification progress in aviation hydraulic oil indicates that Asia-Pacific is developing local supply capability in the aviation lubricants market over time.

Europe held a significant position in the aviation lubricants market, though its growth profile is more measured than Asia-Pacific, as the region combines strong MRO demand with stringent certification requirements and sustainability-driven product scrutiny. ReFuelEU Aviation and European Union Aviation Safety Agency (EASA) guidance are shaping procurement discussions in Europe by placing greater emphasis on SAF compatibility and related system performance in the evaluation process. Germany, the United Kingdom, and France remain important demand centers, anchoring major commercial fleets, technical service capability, and large maintenance organizations. South America, the Middle East, and Africa together account for a smaller share of the aviation lubricants market, yet each presents targeted opportunities where hub expansion, recovery in fleet utilization, or older aircraft populations sustain maintenance demand. These regions do not alter the global ranking at present, but remain relevant to suppliers competing through niche approvals, regional distribution, or defense and specialty fluid positions.

Competitive Landscape

The aviation lubricants market is moderately fragmented, with ExxonMobil, Shell, TotalEnergies, BP, through Castrol, and Chevron holding strong positions in core aviation product categories. Approvals embedded in original equipment manufacturer (OEM) service bulletins create a long-lasting advantage because operators prefer continuity, documentation, and approved field performance over frequent supplier changes. ExxonMobil Aviation notes that commercialization for a new oil technology can take 10 to 15 years across targeted engine families, which helps explain why incumbent suppliers maintain a durable position once approved. As a result, competition in the aviation lubricants market depends not only on pricing, but also on approval breadth, technical service support, and the ability to maintain supply consistency over long aircraft life cycles. Scale and qualification history matter more than rapid product turnover in this market.

Specialty suppliers retain room to compete in the aviation lubricants market, particularly in military, specialty grease, and high-performance additive niches where application-specific capability is more decisive than standard portfolio breadth. NYCO, Klüber Lubrication, Anderol, and Nye Lubricants operate in this narrower field, competing through tailored formulations, targeted approvals, and support for demanding applications that larger suppliers may not address with the same focus. The market is also creating space for differentiated product positioning around reduced-toxicity formulations and future sustainable aviation fuel (SAF) compatibility, where qualification remains limited and customer interest is rising. In May 2026, LANXESS AG and Hindustan Petroleum Corporation Ltd signed an MOU to jointly develop and distribute aviation and industrial lubricants across India and South Asian Association for Regional Cooperation (SAARC) countries, illustrating how partnership models are being used to strengthen regional reach. In March 2026, Chevron Lummus Global added Fischer-Tropsch liquid upgrading solutions to its licensing portfolio, widening the raw material pathways available to lubricant formulators pursuing bio-compatible base stocks.

Supply chain resilience is another competitive factor in the aviation lubricants market, as approved products have little room for interruption once linked to active fleets and long-term maintenance programs. Supplier proximity, technical troubleshooting, and after-sales documentation therefore matter alongside formulation quality. The market is also aligning with digital maintenance practices, as real-time oil analysis and predictive maintenance tools influence how operators monitor drain intervals and fluid condition. Despite these changes, the aviation lubricants market continues to favor suppliers that can combine approved formulations, stable access to raw materials, and a strong support network across civil and defense operators.

Aviation Lubricants Industry Leaders

Exxon Mobil Corporation

Shell plc

Eastman Chemical Company

BP p.l.c. (Castrol)

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: LANXESS AG and Hindustan Petroleum Corporation Ltd (HPCL) signed an MoU to jointly develop and distribute aviation and industrial lubricants across India and SAARC countries. The partnership gives LANXESS direct access to the aviation lubricant market through HPCL's established downstream network.

- March 2026: Chevron Lummus Global added Fischer-Tropsch liquid upgrading solutions to its technology licensing portfolio, enabling production of Group III and Group III+ base oils and sustainable aviation fuel (SAF) from renewable feedstocks. This directly expands the raw material options available to aviation lubricant formulators seeking bio-compatible base stocks.

Global Aviation Lubricants Market Report Scope

Aviation lubricants are specialized fluids, oils, and greases used to minimize friction, wear, and corrosion in critical aircraft systems. They are formulated to perform under extreme thermal fluctuations, high altitudes, and heavy loads.

The aviation lubricants market is segmented by type, technology, platform, application, end user, and geography. By type, the market is segmented into hydraulic fluids, engine oils, greases, and special lubricants and additives. By technology, the market is segmented into mineral-based, synthetic, and bio-based. By platform, the market is segmented into commercial aviation, military aviation, and business and general aviation. By application, the market is segmented into engine systems, hydraulic systems, landing gear, airframe, and other applications (auxiliary and other systems). By end user, the market is segmented into OEM and aftermarket. The report also covers the market size and forecasts for aviation lubricants in 18 countries across major regions. The market sizes and forecasts are provided in terms of Volume (Liters).

| Hydraulic Fluid |

| Engine Oil |

| Grease |

| Special Lubricants and Additives |

| Mineral-based |

| Synthetic |

| Bio-based |

| Commercial Aviation |

| Military Aviation |

| Business and General Aviation |

| Engine Systems |

| Hydraulic Systems |

| Landing Gear |

| Airframe |

| Other Applications (Auxiliary and Other Systems) |

| OEM |

| Aftermarket |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Type | Hydraulic Fluid | |

| Engine Oil | ||

| Grease | ||

| Special Lubricants and Additives | ||

| By Technology | Mineral-based | |

| Synthetic | ||

| Bio-based | ||

| By Platform | Commercial Aviation | |

| Military Aviation | ||

| Business and General Aviation | ||

| By Application | Engine Systems | |

| Hydraulic Systems | ||

| Landing Gear | ||

| Airframe | ||

| Other Applications (Auxiliary and Other Systems) | ||

| By End User | OEM | |

| Aftermarket | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Aviation Lubricants Market?

The Aviation Lubricants Market size is expected to grow from 21.80 million liters in 2025 to 23 million liters in 2026 and is forecast to reach 30.20 million liters by 2031 at 5.60% CAGR over 2026-2031.

Which product category leads aviation lubricants consumption?

Engine Oil led the aviation lubricants market with a 42.18% share in 2025 because turbine lubrication remains central to safe aircraft operation and routine maintenance.

Why does the aftermarket dominate aviation lubricant purchases?

The Aftermarket held 72.65% share in 2025 because aircraft require recurring replenishment and approved fluid replacement throughout their service life, not only at delivery.

Which region is growing fastest through 2031?

Asia-Pacific is the fastest-growing regional segment, with a 6.08% CAGR, supported by large aircraft orders, expanding fleets, and growing local maintenance capacity.

Page last updated on: