East Asia Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

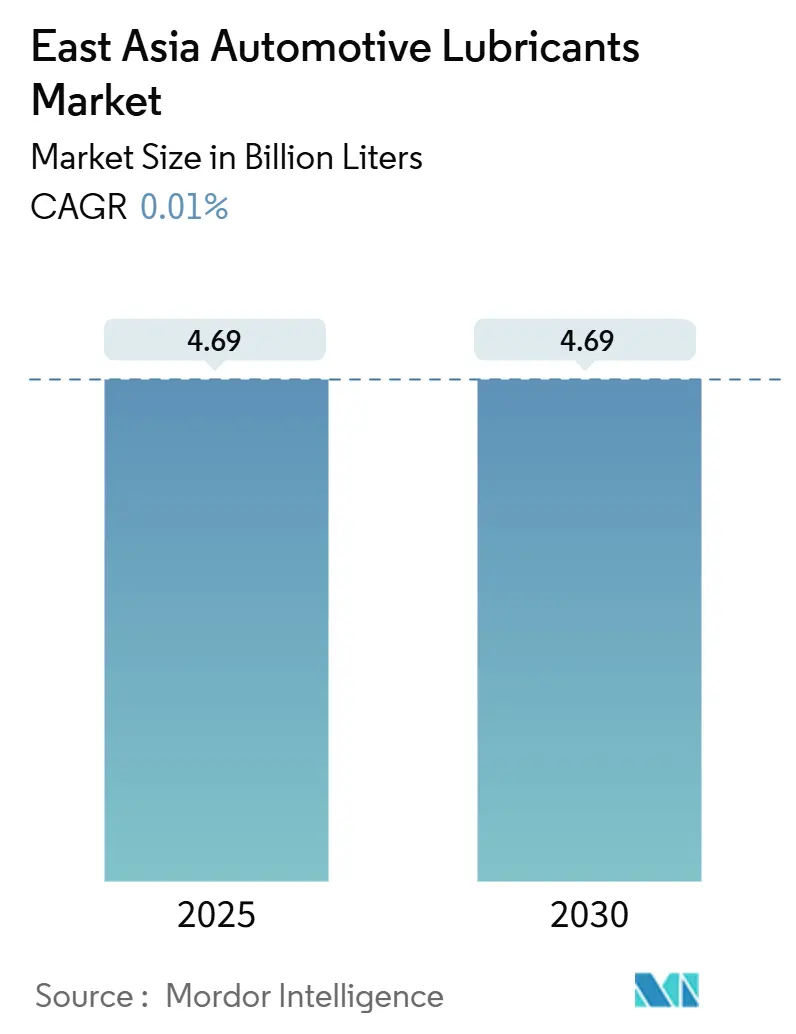

| Market Volume (2025) | 4.69 Billion liters |

| Market Volume (2030) | 4.69 Billion liters |

| Growth Rate (2025 - 2030) | 0.01% CAGR |

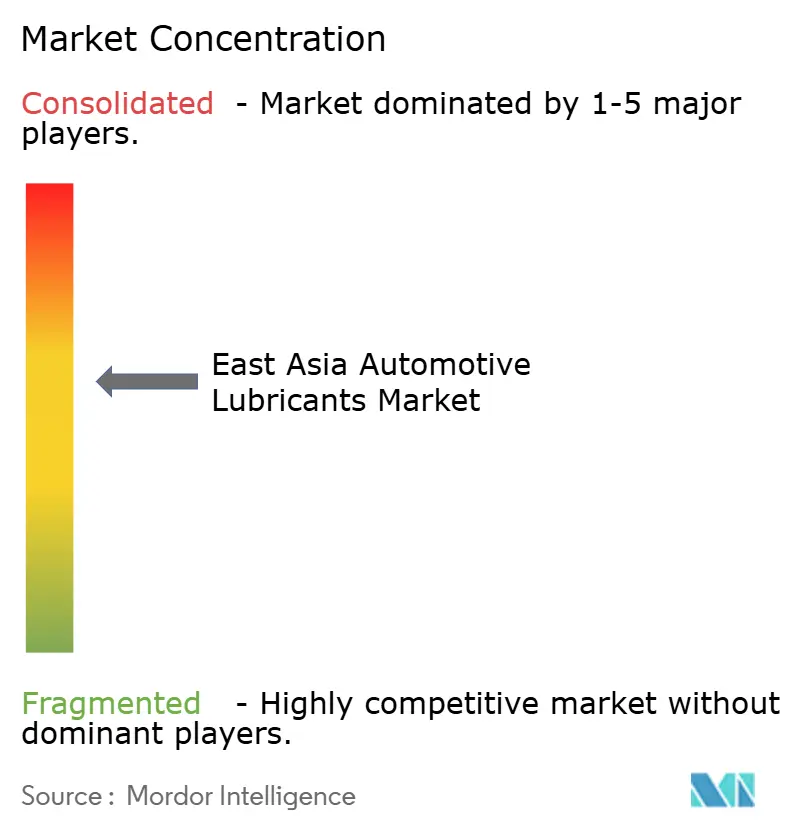

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

East Asia Automotive Lubricants Market Analysis by Mordor Intelligence

The East Asia Automotive Lubricants Market size is estimated at 4.69 billion liters in 2025, and is expected to reach 4.69 billion liters by 2030, at a CAGR of 0.01% during the forecast period (2025-2030). A mature vehicle parc, longer oil-drain intervals, and the gradual shift toward electric and alternative-fuel drivetrains continue to constrain the expansion of volumes. China’s dominant automotive production base, the region’s scale advantages in heavy-duty transport, and pragmatic fiscal stimulus for infrastructure projects still provide a large replacement pool; yet, overall demand barely offsets the loss of diesel-focused lubricants. Competitive intensity has shifted toward value-added synthetics, OEM-approved service bundles, and lower-viscosity engine oils that meet increasingly stringent fuel efficiency norms. Base-oil price volatility has further compressed blender margins, accelerating the adoption of digital distribution and vertical integration among leading suppliers.

Key Report Takeaways

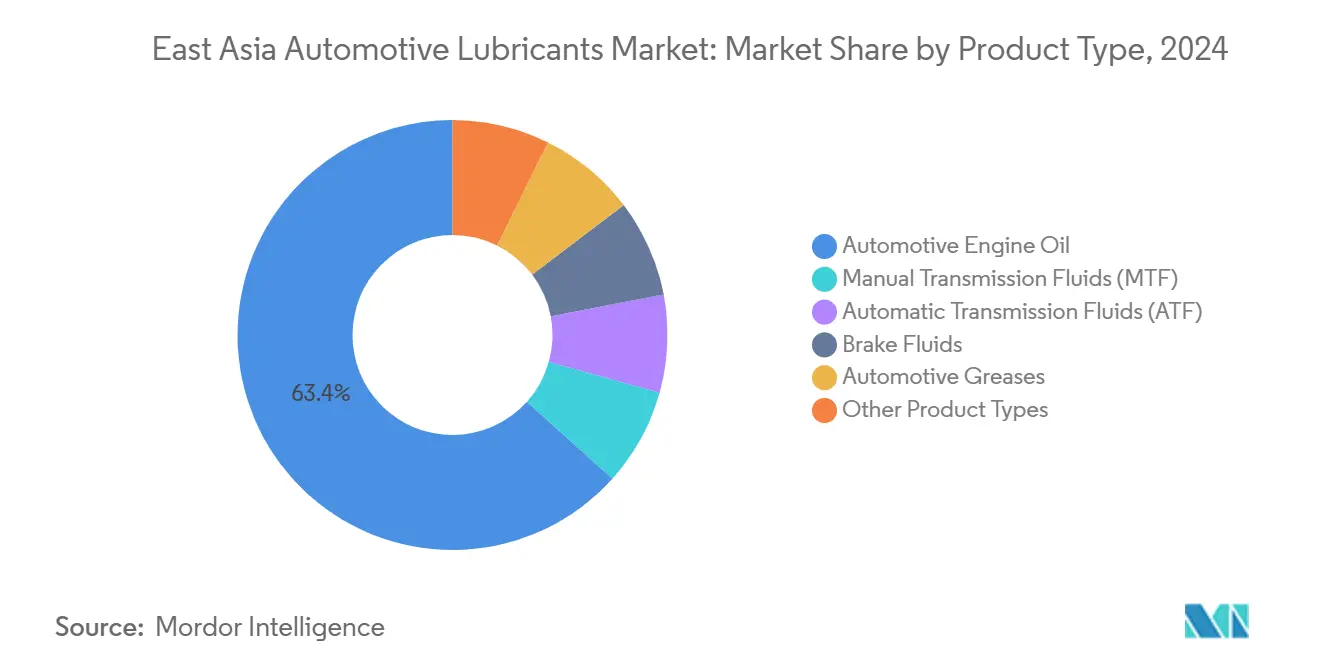

- By product type, automotive engine oil led with a 63.35% share of the East Asia automotive lubricants market in 2024; automatic transmission fluids are projected to expand at a 0.37% CAGR through 2030.

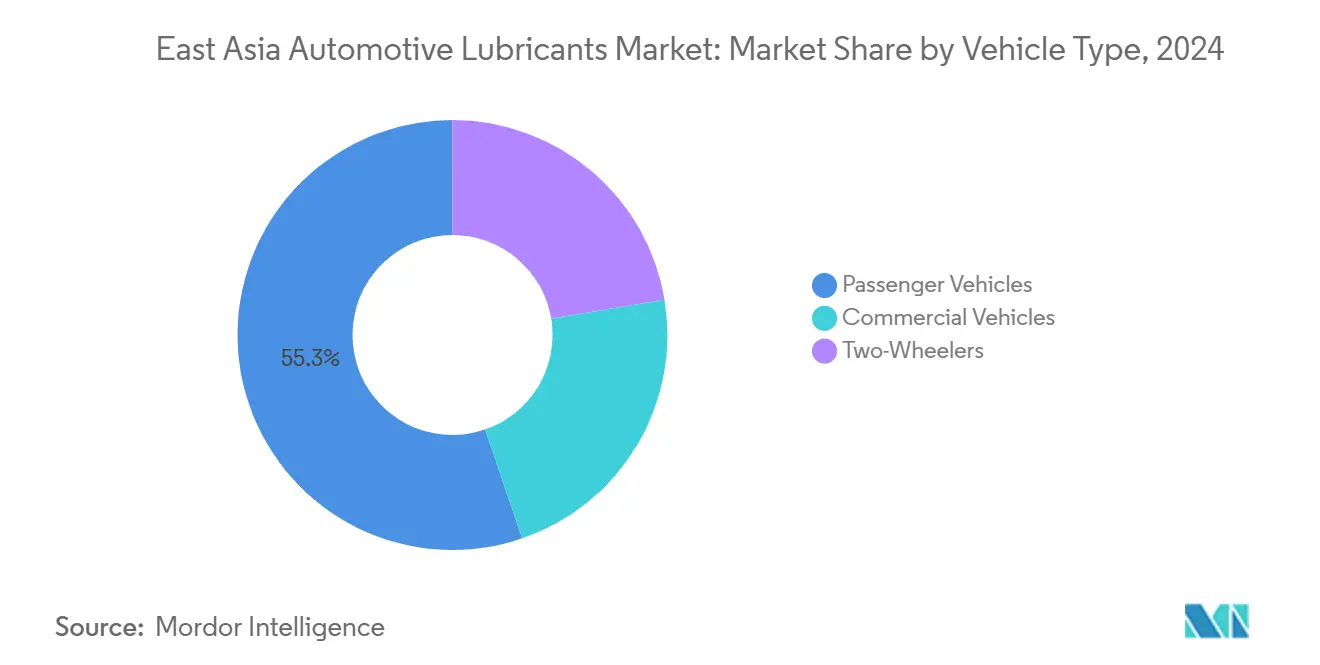

- By vehicle type, passenger vehicles accounted for 55.26% of the East Asia automotive lubricants market size in 2024, while commercial vehicles recorded the fastest forecast CAGR at 0.48% through 2030.

- By geography, China accounted for 74.28% of the regional volume in 2024; Taiwan represented the fastest-growing geography, with a 0.76% CAGR over 2025-2030.

East Asia Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China's expanding commercial-vehicle parc | +0.2% | China core, spillover to supply chains in Korea, Taiwan | Medium term (2-4 years) |

| Japan and Korea leadership in synthetic-research and development | +0.1% | Japan and Korea core, technology transfer to China | Long term (≥ 4 years) |

| OEM–service integration sustaining premium SKUs | +0.1% | Global, with early gains in Japan, Korea, urban China | Medium term (2-4 years) |

| Government fuel-efficiency mandates (CAFE, WLTP) | +0.2% | China, Japan, Korea with regulatory harmonization | Short term (≤ 2 years) |

| E-commerce parts platforms unlocking rural last-mile demand | +0.1% | China rural, expanding to Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

China’s Expanding Commercial-Vehicle Parc

Steady public-works spending and e-commerce logistics keep China’s heavy-duty truck market on an expansion path even as passenger-car demand plateaus. Commercial-vehicle output increased, reinforcing the lubricant replacement pool despite rising LNG and battery-electric truck penetration. State-owned CNPC increased its finished-lube capacity, aligning supply with the intensified cross-border transport along Belt and Road corridors. Nevertheless, the erosion of diesel demand from LNG truck adoption adds complexity to near-term product mix planning. Blenders are therefore tailoring dual-purpose CK-4 oils and low-Ash EV axle fluids to serve a bifurcated fleet that now requires both legacy and next-generation formulations.

Synthetic Technology Leadership in Japan and Korea

ENEOS, Idemitsu, and SK Enmove continue to leverage advanced base-stock chemistry to extend drain intervals while meeting lower viscosity grades (0W-16 and 0W-12) required by OEMs. ENEOS launched a low-carbon PAO blend in 2024, while Idemitsu introduced a bio-based racing oil platform targeting high-performance hybrids. These innovations pre-empt China’s GB 19578-2024 fuel consumption rules, which tighten fleet-average limits[1]Ministry of Ecology and Environment, “Notice on the GB 19578-2024 Fuel Consumption Limits,” mee.gov.cn. Cross-licensing agreements already enable Chinese blenders to co-produce GLV-2-ready synthetics using Japanese additive packages, thereby accelerating the adoption of premium-grade lubricants across the East Asia automotive market.

OEM–Service Integration

Automakers now bundle factory-approved lubricants into paid maintenance contracts, locking in brand preference and premium pricing despite flat volume growth. Shell’s multi-year supply deal with XCMG heavy equipment in 2024 exemplifies the trend, guaranteeing factory-fill and aftermarket replenishment volumes. Digital-native platforms, such as Tuhu, integrate ExxonMobil’s Mobil 1 and Idemitsu’s APOLLOIL ranges into AI-driven service scheduling, capturing rural and tier-3 demand pockets that were previously served by non-branded bulk oil. The strategy shields premium SKUs from price wars and sustains margin resilience in the East Asia automotive lubricants market.

Government Fuel-Efficiency Mandates

Fuel-economy regulations are the principal catalyst for product reformulation. China’s Stage 4 light-commercial rules and GB 19578-2024 standard, Japan’s Top Runner targets, and Korea’s K-CAFE collectively cover the majority of regional lubricant demand. All three regimes reward low-viscosity synthetics, driving the adoption of 0W-20 and 5W-20. WLTP certification requires stringent cold-start and transient-load testing, which favors Group IV/V base oils due to their superior shear stability[2]European Commission, “WLTP Laboratory Test Procedure Factsheet,” ec.europa.eu. API’s GF-7 protocol, effective 2025, raises test-bench costs, disadvantaging smaller regional blenders. Harmonizing China’s modified WLTP with Japan and Korea could unlock scale economies for multinational suppliers operating across the East Asia automotive lubricants market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM long-drain technologies shrinking lubricant change frequency | -0.3% | Global, with advanced adoption in Japan, Korea | Long term (≥ 4 years) |

| High pricing of Group IV/V synthetics in Tier-3 cities | -0.1% | China Tier-3 cities, rural markets | Medium term (2-4 years) |

| Stringent waste-oil take-back rules raising collection costs | -0.2% | China core, expanding to Korea, Taiwan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Long-Drain Technologies

OEM-approved oils that enable 15,000-20,000 km intervals directly cut annual lithic lubricant demand per vehicle. Sinopec’s 2024 long-drain diesel series targets fleet operators keen on lower downtime, and Japan’s kei-car makers now specify 10,000 km intervals from the factory warranty period. While value per litre rises, aggregate volume falls, compelling blenders to upsell premium synthetics and ancillary services to offset the contraction in the East Asia automotive lubricants market.

Waste-Oil Take-Back Rules

China’s circular-economy regulations require licensed collectors to process used engine oil at certified facilities, inflating compliance costs for distributors. Similar legislation is under consideration in Korea and Taiwan. Large refiners like SK Enmove can absorb the expense through in-house rerefining, but independent blenders face higher logistics fees and potential write-downs, which may dampen capacity expansions over the next two years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine-Oil Dominance Confronts Specialized-Fluid Growth

Automotive engine oil accounted for 63.35% of the East Asia automotive lubricants market share in 2024. Within this core segment, 0W-XX and 5W-XX synthetics are gaining momentum as OEMs target stricter fuel standards. The East Asia automotive lubricants market size for automatic transmission fluids is expected to expand at a 0.37% CAGR, supported by higher automatic-gearbox penetration in urban passenger cars. Demand for manual transmission fluids and hydraulic power-steering oils continues to erode as electric power-steering systems and CVTs become standard in new models. Brake-fluid consumption remains closely tied to vehicle production trends, while thermal-management fluids for BEV battery packs represent a nascent but strategic growth frontier.

Product-portfolio diversification is now imperative. Greases, though a modest volume slice, benefit from the electrification wave as low-noise formulations lubricate electric motor bearings. Leading suppliers, such as Lopal Dragon, are reallocating their research and development budgets toward hydrogen fuel thermal-management fluids, pre-positioning for emerging zero-emission heavy-duty platforms. Together, these specialized fluids offset the structural softness in mainstream engine oil demand, ensuring that the East Asia automotive lubricants market continues to pivot toward higher-value, niche applications.

By Vehicle Type: Commercial Vehicles Provide the Incremental Upside

Passenger cars accounted for 55.26% of the total volume in 2024; however, their replacement cycle stability leaves limited headroom for growth. Conversely, commercial vehicles log longer annual mileage and show a 0.48% CAGR through 2030. Growth stems from sustained infrastructure investment, cross-border e-commerce logistics, and governmental incentives for fleet modernization. Heavy-duty diesel demand nevertheless faces gradual compression as LNG and battery-electric trucks proliferate, accelerating the shift toward low-SAPs, high-TBN oils compatible with aftertreatment systems.

Two-wheelers remain important in Southeast Asia-focused submarkets but exhibit mature dynamics in Japan and Korea. While electrified scooters reduce demand for petrol-engine oil, they open new categories for specialty greases and coolant-dielectric blends used in battery thermal management. OEM-dictated drain intervals also rise in the motorcycle segment, further aligning lubrication cycles with broader efficiency-driven trends across the East Asia automotive lubricants market.

Geography Analysis

China retains unrivaled scale, capturing 74.28% of regional lubricant volumes in 2024. Commercial-vehicle expansion along Belt-and-Road corridors, combined with high-mileage ride-hailing fleets, underpins the baseline replacement pool. Regulatory tightening under GB 19578-2024 and Stage 4 LCV standards pulls demand toward 0W-20 synthetics and emission-system-compatible diesel oils. At the same time, e-commerce platforms extend branded oil availability to rural counties, widening the premium-serviceable market for majors like Shell and ExxonMobil.

Japan and South Korea wield outsized influence through technology exports and specification leadership. Both countries maintain a high level of vehicle ownership maturity yet rely on performance-oriented consumer preferences to support the penetration of premium-grade vehicles. Domestic refiners, including ENEOS and SK Enmove, consistently invest in research and development to create ultra-low-viscosity formulations and friction-modifier chemistries. Their innovations cascade into China and Taiwan under cross-licensing agreements, standardizing high-performance benchmarks across the East Asia automotive lubricants market.

Taiwan is the fastest-growing submarket at a 0.76% CAGR, driven by semiconductor-sector fleet expansion and rising luxury-vehicle registrations. The Ministry of Economic Affairs’ industrial upgrading incentives amplify demand for clean-room-ready specialty greases and high-temperature compressor oils.

Competitive Landscape

The East Asia automotive lubricants market is moderately consolidated. Global majors leverage brand capital, OEM endorsements, and proprietary additive chemistries, while national oil companies exploit captive base-oil streams and domestic distribution scale. Chinese champions are deepening vertical integration, investing in rerefining and hydroisomerization units that hedge against Group II/III price volatility. White-space competition intensifies in EV thermal-management fluids, hydrogen transport greases, and long-drain HDDEO meeting China VI-b norms. With volumes flat, strategic storytelling emphasizes life-cycle carbon intensity, closed-loop waste-oil collection, and AI-enabled condition monitoring—hallmarks of a mature yet innovation-hungry East Asia automotive lubricants market.

East Asia Automotive Lubricants Industry Leaders

China Petrochemical Corporation

ENEOS Corporation

PetroChina Kunlun

Shell plc

Idemitsu Kosan Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP p.l.c initiated a process to sell its Castrol lubricants division, valued at up to USD 10 billion, as part of a broader USD 20 billion asset-rotation plan aimed for completion by 2027.

- November 2024: PTT Lubricants introduced its EVOTEC Technology platform in Taiwan, offering engine oil ranges engineered for enhanced endurance and fuel efficiency in motorcycles and passenger cars.

East Asia Automotive Lubricants Market Report Scope

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| China |

| South Korea |

| Japan |

| Taiwan |

| Others (Mangolia, Hongkong) |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| By Geography | China | |

| South Korea | ||

| Japan | ||

| Taiwan | ||

| Others (Mangolia, Hongkong) |

Key Questions Answered in the Report

What is the size of the East Asia automotive lubricants market in 2025?

The market stands at 4.69 billion litres in 2025, making it the largest lubricants region globally by volume.

What CAGR is expected for East Asian automotive lubricants through 2030?

Volume is projected to remain almost flat, with a 0.01% CAGR, as efficiency gains and electrification offset new demand.

Which product category is growing fastest in East Asia?

Automatic transmission fluids are expected to show the highest growth, advancing at a 0.37% CAGR through 2030, driven by wider adoption of AT and CVT.

Why is Taiwan the fastest-growing submarket?

Semiconductor industry expansion and rising premium-vehicle registrations lift lubricant demand, supporting a 0.76% CAGR.

How are fuel-efficiency rules influencing lubrication trends?

0W-20 and 5W-20 synthetics are gaining market share as OEMs need lower viscosity to comply with CAFE and WLTP standards.

Page last updated on: