Learning Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

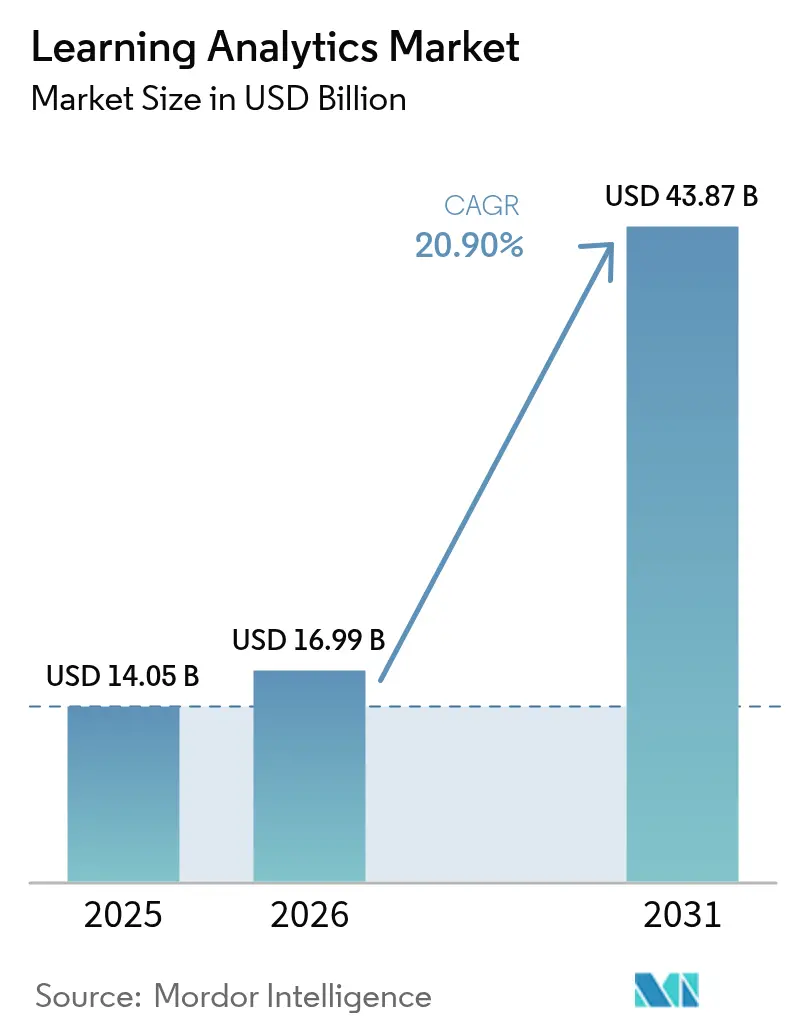

| Market Size (2026) | USD 16.99 Billion |

| Market Size (2031) | USD 43.87 Billion |

| Growth Rate (2026 - 2031) | 20.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Learning Analytics Market Analysis by Mordor Intelligence

The learning analytics market size is expected to grow from USD 14.05 billion in 2025 to USD 16.99 billion in 2026 and is forecast to reach USD 43.87 billion by 2031 at 20.90% CAGR over 2026-2031. Rapid adoption reflects a clear shift toward data-driven decision making across education and corporate training. Institutions deploy predictive dashboards, AI-powered early-warning systems, and cloud platforms to raise student success while streamlining operations. Government funding programs, outcome-based financing, and expanding cloud capacity underpin demand momentum, while privacy compliance and talent shortages temper the pace of implementation. Competitive intensity stays moderate as platform leaders consolidate capabilities, and AI-native entrants introduce niche solutions that deepen market functionality.

Key Report Takeaways

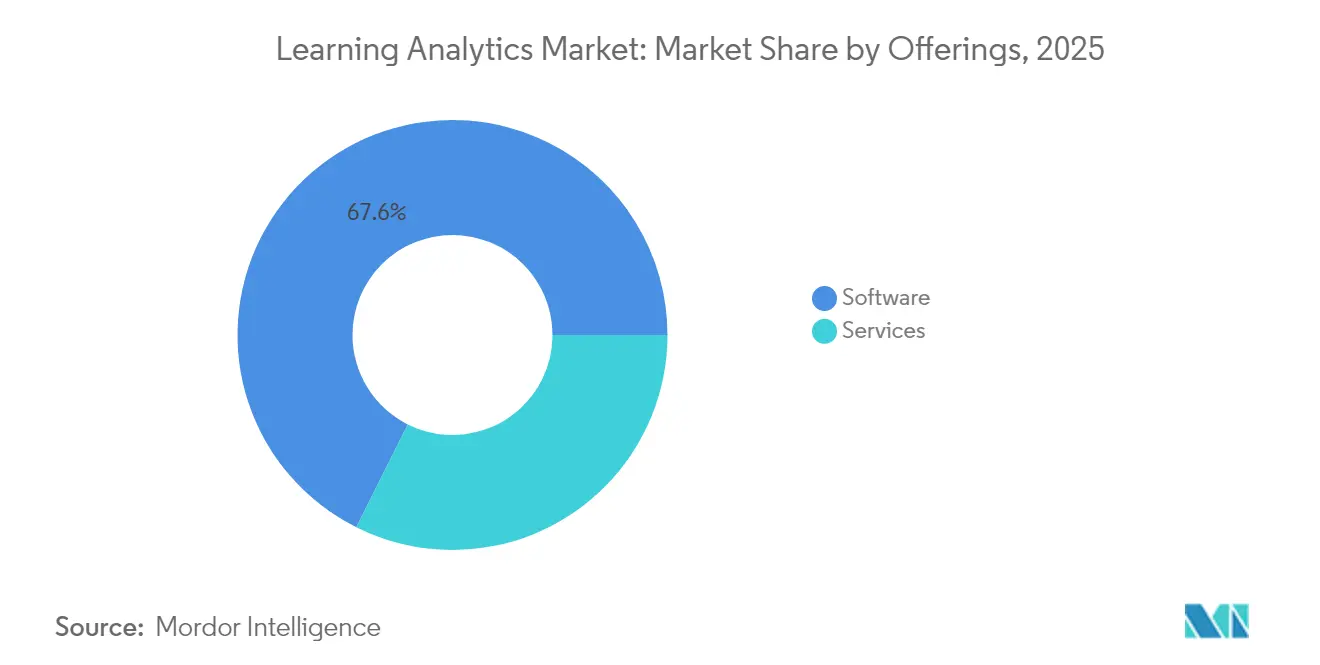

- By offerings, software solutions led with 67.62% of the learning analytics market share in 2025, whereas services are poised for the fastest 22.52% CAGR to 2031.

- By deployment mode, on-premise installations held 70.35% share of the learning analytics market size in 2025, yet cloud deployments are set to post a 22.96% CAGR through 2031.

- By analytics type, predictive tools captured 57.12% of the learning analytics market share in 2025, while prescriptive analytics shows the highest 21.86% CAGR outlook.

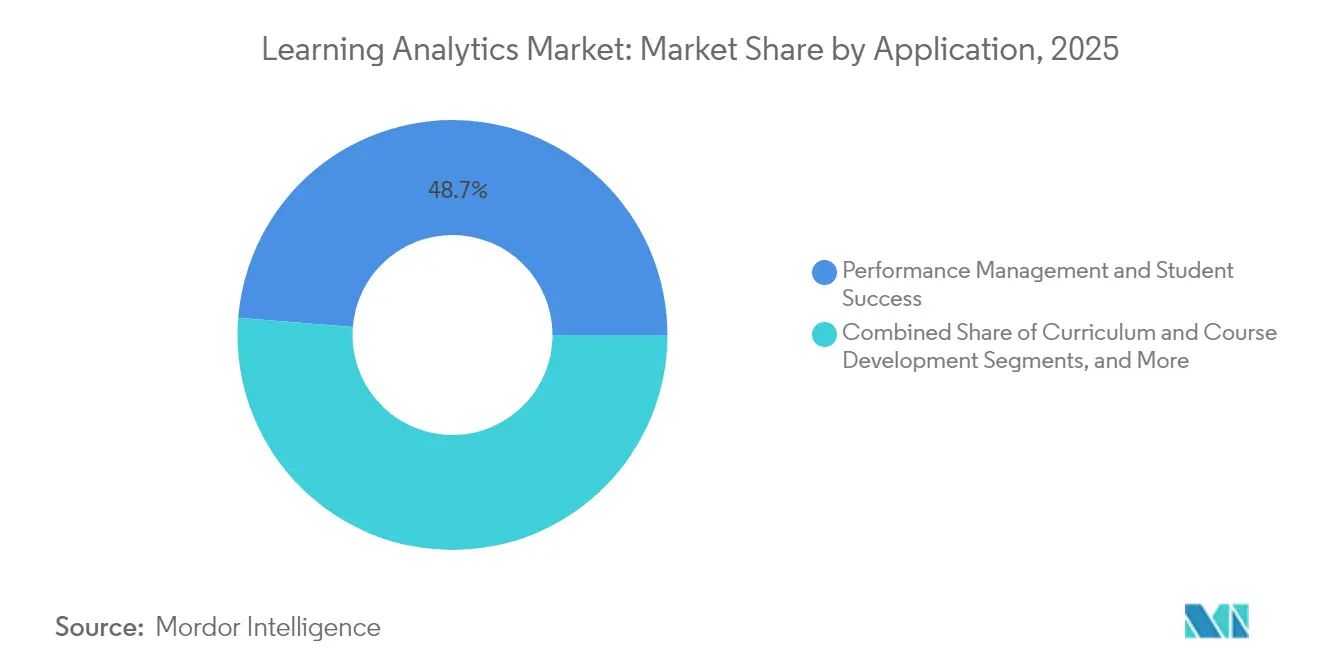

- By application, performance management and student success commanded 48.73% of the learning analytics market size in 2025, whereas curriculum development is projected to expand at 21.23% CAGR.

- By end user, academia accounted for 66.48% share of the learning analytics market in 2025; corporate learning analytics represents the fastest 22.14% CAGR segment.

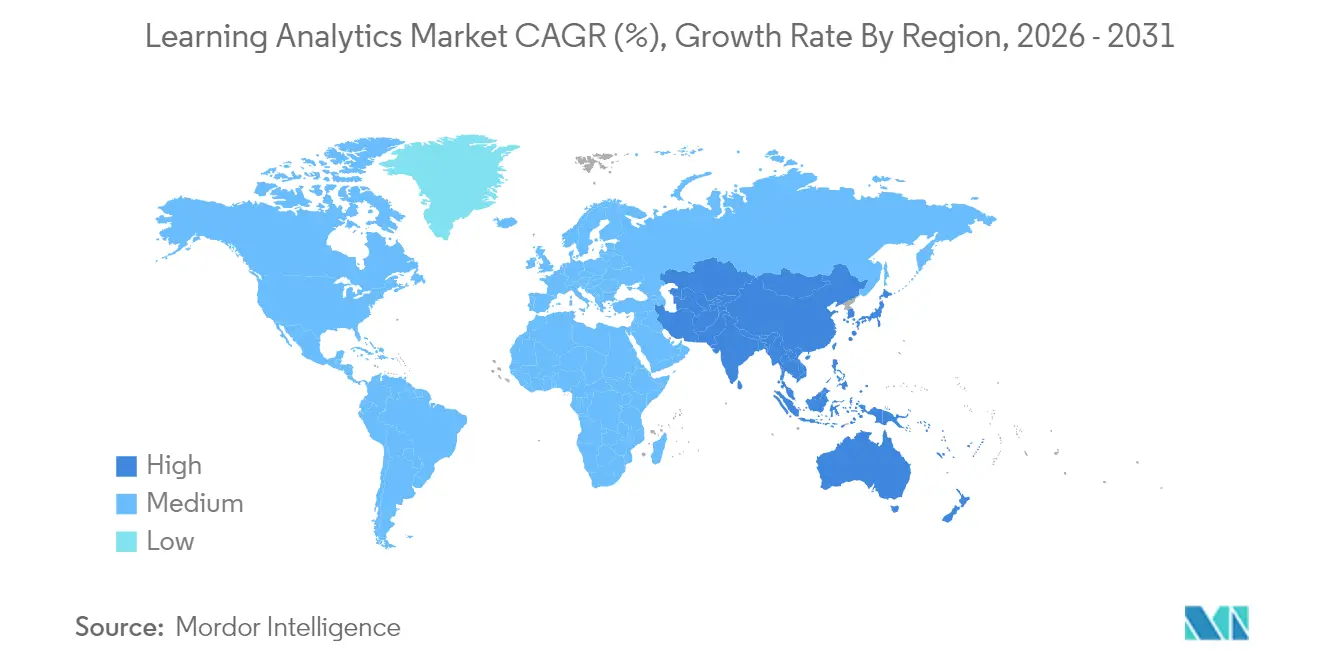

- By geography, North America secured 38.12% of the learning analytics market share in 2025, while Asia-Pacific is forecast to grow at 21.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Learning Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing focus on improving student outcomes and retention | +5.4% | Global, with concentrated adoption in North America and Europe | Medium term (2-4 years) |

| Expansion of cloud-based learning analytics platforms and MOOCs | +4.7% | Global, accelerated in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Government and institutional EdTech funding surge | +3.9% | North America, Europe, India, China | Medium term (2-4 years) |

| Advances in AI/ML enabling deeper analytics insights | +4.3% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Integration of Learning Record Stores with XR content | +2.6% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Outcome-based funding models driving analytics adoption | +3.2% | United States, United Kingdom, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Focus on Improving Student Outcomes and Retention

Institutions now tie financial viability to completion metrics, adopting analytics suites that flag at-risk learners and recommend timely interventions. Post-pandemic enrollment pressures heightened the urgency, and universities using comprehensive platforms have recorded 15-20% gains in first-year retention. Performance-based funding in 28 states links public allocations to student success, turning analytics from optional innovation into operational necessity. The shift also answers accountability demands from accreditors and employers who equate graduate performance with institutional reputation.

Expansion of Cloud-Based Learning Analytics Platforms and MOOCs

Cloud delivery removes infrastructure barriers, letting smaller schools obtain enterprise-grade insights via subscription models. Seamless links with learning management systems shorten deployment cycles, while real-time processing supports personalized feedback loops at scale. Massive Open Online Course providers refine content through continuous cloud analytics, and consortia now share anonymized datasets under stringent encryption standards[1]UK Department for Education, “AI Tools for Teachers Pilot,” gov.uk. The resulting democratization broadens the learning analytics market far beyond early adopters.

Government and Institutional EdTech Funding Surge

Policy makers frame data-driven education as a competitiveness lever. The U.S. Institute of Education Sciences funds generative AI pilots, the UK earmarked GBP 4 million (USD 5.43 million) for AI teacher tools, and India’s Budget 2025 assigned around (USD 57.97 million) to an AI Centre of Excellence. These grants cover technology procurement, professional training, and research, anchoring long-term demand for analytics platforms that document measurable learning gains.

Advances in AI/ML Enabling Deeper Analytics Insights

Machine learning elevates analytics from descriptive dashboards to predictive and prescriptive guidance. Algorithms detect subtle engagement patterns, while natural-language processing evaluates discussion posts to gauge comprehension. Generative tools such as PowerSchool’s PowerBuddy turn complex data into conversational insights for non-technical educators, widening user adoption. As models mature, adaptive systems will continuously fine-tune course pathways to individual learner profiles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy and security compliance burden | -1.7% | Global, particularly Europe (GDPR), United States (FERPA) | Short term (≤ 2 years) |

| Shortage of analytics talent within education sector | -2.6% | Global, acute in developed markets with high demand | Medium term (2-4 years) |

| Vendor lock-in and NGDLE interoperability gaps | -1.3% | Global, particularly affecting multi-platform institutions | Medium term (2-4 years) |

| Algorithmic bias scrutiny slowing procurements | -1.1% | North America, Europe, Australia with strict AI governance | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Security Compliance Burden

GDPR and FERPA impose strict consent and data-handling mandates that raise legal and technical costs. Institutions must modernize governance frameworks, encrypt granular learner records, and justify algorithmic decisions to stakeholders, slowing procurement cycles. Vendors, in turn, localize solutions to meet region-specific rules, adding complexity and cost that can delay global rollouts.

Shortage of Analytics Talent Within Education Sector

Only 23% of educators believe graduates hold required data science skills, yet 69% of employers rank analytics proficiency as critical, creating a structural gap[2]Business-Higher Education Forum, “Analytics Talent Gap Report,” bhef.org. Education faces stiff competition from tech firms for qualified data scientists, which inflates salaries and undermines institutional capacity. Dependence on external consultants raises implementation fees and can limit knowledge transfer, constraining the speed at which the learning analytics market scales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offerings: Services Accelerate While Software Sustains Leadership

Software solutions generated 67.62% of 2025 revenue, forming the backbone of the learning analytics market. Predictive dashboards surface early-warning indicators, while adaptive engines personalize content. Over the forecast horizon, services will outpace software with a 22.52% CAGR, reflecting demand for integration, training, and managed operations. Institutions increasingly rely on partners to bridge technical and pedagogical gaps, underscoring that human expertise remains essential for delivering full value.

Services growth also mirrors rising complexity: multi-source data ingestion, AI model tuning, and evergreen compliance updates require specialized skills. Consulting and managed services firms therefore secure long-term contracts as schools seek outcome guarantees rather than licenses alone. As a result, the learning analytics market size attributable to services is projected to rise steadily through 2031 alongside deepening platform penetration.

By Deployment Mode: Cloud Traction Grows Despite On-Premise Legacy Base

On-premise architectures retained 70.35% share of the learning analytics market size in 2025, supported by data-sovereignty policies and entrenched campus infrastructure. Yet cloud solutions are expanding at 22.96% CAGR, driven by elastic capacity and subscription pricing that lower total cost of ownership. Institutions that moved to the cloud during pandemic disruptions seldom revert, citing seamless remote access and quicker feature updates.

Hybrid frameworks now emerge, letting schools keep sensitive datasets on local servers while harnessing cloud compute for intensive analytics. This layered architecture reconciles privacy mandates with scalability, and it encourages incremental migration paths that further enlarge the learning analytics market. Vendors offering flexible deployment options thus appeal to both risk-averse and forward-leaning customers.

By Analytics Type: Predictive Dominance Transitions Toward Prescriptive Growth

Predictive engines commanded 57.12% share in 2025 as institutions prioritized early identification of at-risk students. These models digest historical grades, engagement logs, and demographic data to forecast success probabilities. Prescriptive analytics, although smaller today, is rising fastest at 21.86% CAGR because it moves beyond alerts to recommend concrete actions, such as tutoring schedules or adaptive assessments.

Descriptive reporting remains foundational, supplying the baseline metrics that fuel more advanced layers. Over time, continuous improvements in model accuracy and explainability will push prescriptive tools into mainstream workflows, reshaping educator expectations and propelling the learning analytics market forward.

By Application: Retention Focus Holds, Curriculum Optimization Climbs

Performance management applications held 48.73% share of the learning analytics market in 2025, underscoring the primacy of retention and graduation outcomes. Real-time dashboards grant advisors actionable visibility into engagement trends, enabling rapid outreach. Meanwhile, curriculum-development analytics should post a 21.23% CAGR, as administrators harness course-level insights to refine pedagogical design, reduce redundancy, and elevate learning efficiency.

Assessment analytics and adaptive testing complement both pillars, tailoring difficulty to individual competence and feeding rich data back into curriculum loops. Collectively, these use cases demonstrate how the learning analytics market evolves from reactive scorekeeping to proactive instructional design.

By End User: Academic Core Persists as Enterprises Accelerate

Academic institutions generated 66.48% of 2025 revenue, benefiting from long-standing student information systems that provide dense data streams. Universities integrate learning analytics to meet accreditation requirements and boost brand standing. K-12 districts deploy similar tools to comply with accountability metrics and to personalize instruction.

Corporate learning analytics is gaining ground at 22.14% CAGR as firms link workforce analytics to productivity and retention. Large enterprises lead adoption through sophisticated talent-management suites, while small and midsize businesses tap cloud subscriptions for affordable insights. This expansion diversifies the learning analytics market and highlights its relevance beyond traditional classrooms.

Geography Analysis

North America kept its leadership with 38.12% share in 2025 owing to mature EdTech ecosystems, clear funding channels, and balanced privacy frameworks that foster trust. Federal initiatives such as the U-GAIN program channel resources into scalable solutions, encouraging institutions to embed analytics in daily operations. Canada’s provincial strategies echo this momentum, reinforcing regional dominance.

Asia-Pacific represents the most dynamic arena with a 21.62% CAGR forecast. India’s ₹500 crore AI Centre of Excellence and China’s modernization policies funnel capital and policy support toward data-driven instruction. Markets such as Japan and South Korea contribute through early 5G adoption and high digital readiness. Despite heterogeneous regulations, the region’s demographic scale and government backing fuel sustained expansion of the learning analytics market.

Europe keeps steady growth, propelled by GDPR-compliant solutions that reconcile analytics value with strict privacy mandates. The UK’s GBP 4 million (USD 5.43 million) AI teacher-support scheme illustrates policy-level confidence, while Germany and France fund institution-level digital transitions. Vendors able to demonstrate airtight compliance enjoy a clear advantage, reinforcing a specialized yet sizeable subsection of the learning analytics market.

Competitive Landscape

Consolidation defines current dynamics. Bain Capital’s USD 5.6 billion privatization of PowerSchool and KKR’s USD 4.8 billion purchase of Instructure inject capital for generative AI roadmaps and international reach. These moves raise entry barriers, but they also validate market potential, attracting fresh investment into specialized niches.

Platform leaders integrate student information systems, learning management, and analytics into unified suites. AI-powered personalization becomes a key differentiator, with conversational interfaces simplifying data interpretation for frontline educators. Mid-tier players contest white spaces such as XR-enhanced analytics and sector-specific compliance modules, ensuring the learning analytics market remains innovative despite moderate concentration.

Financial overreach can expose vulnerabilities; Anthology’s restructuring illustrates the risks of aggressive roll-up strategies without proportional revenue gains. This environment rewards disciplined execution, robust customer success models, and transparent privacy safeguards, shaping competitive contours through 2030.

Learning Analytics Industry Leaders

Domoscio

Unicon Inc

Blackboard Inc.

D2L Corporation

Instructure Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: India’s Budget 2025 set aside around USD 57.9 million for an AI Centre of Excellence dedicated to educational analytics solutions.

- January 2025: The UK government invested USD 1.36 million in AI tools that automate feedback and lighten educator workload.

- January 2025: Anthology began debt restructuring talks after missing interest payments, underscoring financial pressures in the competitive EdTech arena.

- August 2024: UC Irvine released the Student Success Analytics Rubric under its Compass program to benchmark institutional analytics readiness.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the learning analytics market covers commercial software and related services that collect, process, and visualize learner-level data in order to improve decision-making across academic institutions and corporate training environments. Solutions must provide built-in analytical engines, descriptive, predictive, or prescriptive, and be available for purchase or subscription by third-party users rather than used only inside one organization.

Scope exclusion: Stand-alone learning management systems or content repositories with no native analytics modules are not counted.

Segmentation Overview

- By Offerings

- Software

- Predictive Analytics Tools

- Descriptive and Diagnostic Dashboards

- Adaptive Learning Platforms

- Services

- Professional Services

- Managed Services

- Software

- By Deployment Mode

- On-Premise

- Cloud

- By Analytics Type

- Descriptive Analytics

- Predictive Analytics

- Prescriptive Analytics

- By Application

- Performance Management and Student Success

- Curriculum and Course Development

- Assessment and Adaptive Learning

- Recruitment, Marketing and Retention

- By End User

- Academia

- K-12 Schools

- Higher Education Institutions

- Corporate

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- Academia

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed ed-tech product managers, chief information officers at universities, procurement heads in Fortune 1000 learning and development units, and regional channel partners in North America, Europe, and Asia-Pacific. Their inputs refined adoption lags, annual churn, and discount structures, and confirmed which analytics capabilities buyers value most when budgeting.

Desk Research

Our analysts began by mapping the universe of addressable spending through public sources such as UNESCO Institute for Statistics enrollment tables, U.S. National Center for Education Statistics datasets, Eurostat's ICT in Education survey, and patent filings indexed in Questel that signal feature adoption cycles. Trade association white papers from EDUCAUSE, IMS Global, and the International Society for Technology in Education helped size institutional user pools, while company 10-Ks, investor decks, and press releases provided pricing ranges and active-user disclosures. Paid intelligence from D&B Hoovers and Dow Jones Factiva supported revenue splits and vendor expansion timelines.

These materials establish the foundational demand pool, average selling prices, and penetration benchmarks across regions. The sources listed illustrate the breadth consulted; many additional publications were reviewed to validate figures and resolve data discrepancies.

Market-Sizing and Forecasting

Mordor's model starts with a top-down reconstruction of addressable spending, combining student enrollment volumes, average analytics spend per learner, and corporate training outlays. Select bottom-up checks, vendor revenue roll-ups and sampled contract values, are applied to stress-test totals before finalizing. Key variables include: (1) higher-education enrollment trends, (2) corporate L&D expenditure as a share of payroll, (3) cloud migration rates, (4) average price erosion on subscription plans, and (5) regulatory data privacy compliance costs. A multivariate regression with these drivers underpins the 2025-2030 forecast, while scenario analysis captures upside from AI-enhanced adaptive learning and downside from budget freezes. Gaps in bottom-up data are bridged by conservative elasticity assumptions that are revisited once new filings emerge.

Data Validation and Update Cycle

Outputs pass anomaly checks against sector M&A multiples and import-export software codes. Senior analysts review year-over-year swings; inconsistent deltas trigger re-contacts with earlier respondents. Reports refresh annually, and interim updates are issued if material events, funding surges, regulatory shifts, or major platform launches, alter baseline assumptions.

Why Our Learning Analytics Baseline Commands Reliability

Published estimates on this market often diverge because firms vary in solution scope, refresh cadence, and validation depth. Some count only academic spend, others fold generic BI tools into totals, and a few rely on unverified adoption multipliers.

Key gap drivers include: exclusion of service revenues, outdated 2019-2021 price points, limited geographic coverage beyond North America, and one-off survey samples that never reach enterprise buyers. Mordor's approach screens offerings feature by feature, blends academic and corporate demand, and re-benchmarks prices every six months, yielding a balanced view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.05 B (2025) | Mordor Intelligence | - |

| USD 8.20 B (2024) | Global Consultancy A | Narrow academic scope, minimal primary validation, flat ASP assumption |

| USD 8.83 B (2024) | Research Publisher B | Omits service revenues, counts only descriptive analytics modules |

| USD 13.67 B (2025) | Industry Journal C | Partial regional coverage, currency conversion at fixed 2023 rates |

In sum, the disciplined source mix, recurring expert touchpoints, and transparent variable tracking adopted by Mordor Intelligence give decision-makers a dependable, reproducible baseline that sits comfortably between aggressive and conservative external positions.

Key Questions Answered in the Report

What is the current size of the learning analytics market?

The learning analytics market was valued at USD 16.99 billion in 2026 and is projected to reach USD 43.87 billion by 2031.

Which segment dominates the learning analytics market?

Software platforms lead, holding 67.62% share in 2025, although services are expanding faster at a 22.52% CAGR.

How quickly is cloud adoption growing within the learning analytics industry?

Cloud deployments are forecast to advance at a 22.96% CAGR through 2031, outpacing on-premise growth as institutions favor scalable and cost-efficient models.

Which region offers the highest growth opportunity?

Asia-Pacific presents the fastest expansion with a 21.62% CAGR, supported by large-scale government investments in educational technology.

What are the main restraints facing the learning analytics market?

Strict privacy regulations and a global shortage of analytics talent are the two most significant challenges, collectively reducing forecast CAGR by an estimated 4.3 percentage points.

How is artificial intelligence shaping the future of learning analytics?

AI transforms analytics from descriptive reports into predictive and prescriptive tools, enabling proactive interventions, personalized content, and conversational dashboards that broaden educator adoption.

Page last updated on: