Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Online Acting Education Market is Segmented by Class Type (Live and Pre-Recorded), Time Commitment (Full-Time Programs and Part-Time), Skill Level (Beginner, Intermediate, and Advanced/Professional), Delivery Platform (Web-Browser, Mobile-App, and Hybrid/Connected TV), Acting Domain (Film and Television, Theatre, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

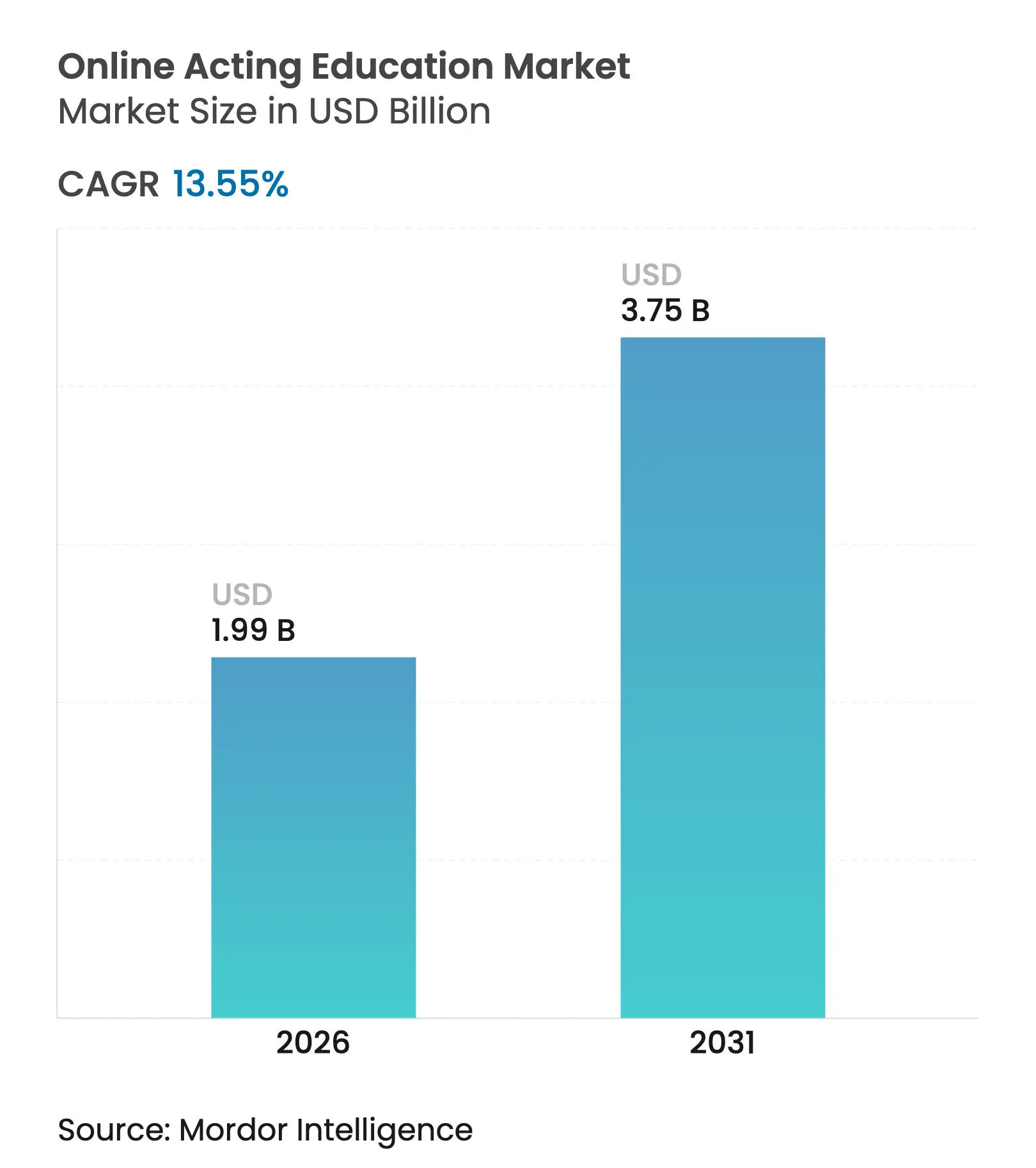

| Market Size (2026) | USD 1.99 Billion |

| Market Size (2031) | USD 3.75 Billion |

| Growth Rate (2026 - 2031) | 13.55 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Online Acting Education Market size in 2026 is estimated at USD 1.99 billion, growing from 2025 value of USD 1.75 billion with 2031 projections showing USD 3.75 billion, growing at 13.55% CAGR over 2026-2031. Robust growth stems from creator-economy platforms that weave acting curricula into influencer toolkits, the mainstreaming of AI-powered performance analytics that provide objective feedback, and sustained government funding for digital arts training. Learners gravitate to flexible formats that let them balance study with gig work, while entertainment studios accelerate demand for voice-over and motion-capture skills. Platform providers respond by blending pre-recorded convenience with live coaching to deliver measurable learning outcomes that justify premium pricing. Market fragmentation persists, yet acquisitions such as Accenture-Udacity flag a consolidation phase where technology scale and content depth decide leadership.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing broadband and smartphone penetration Growing broadband and smartphone penetration | +2.1% | Asia-Pacific, Latin America, Africa | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:Asia-Pacific, Latin America, Africa | Impact Timeline:Medium term (2-4 years) |

Surge in creator-economy platforms integrating actor-centric courses Surge in creator-economy platforms integrating actor-centric courses | +2.8% | North America, Europe | Short term (≤ 2 years) | |||

Cost advantage over brick-and-mortar conservatories Cost advantage over brick-and-mortar conservatories | +1.9% | Global | Long term (≥ 4 years) | |||

AI-driven performance analytics tools improving learning outcomes AI-driven performance analytics tools improving learning outcomes | +2.4% | North America, Europe, Asia-Pacific | Medium term (2-4 years) | |||

Rising demand for remote voice-over and mocap skills in gaming and metaverse Rising demand for remote voice-over and mocap skills in gaming and metaverse | +2.2% | Global gaming hubs | Short term (≤ 2 years) | |||

Government-funded digital skilling grants for performing-arts freelancers Government-funded digital skilling grants for performing-arts freelancers | +1.4% | Europe, Asia-Pacific, selected US states | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

AI-driven performance analytics tools improving learning outcomes

AI-powered motion-capture and speech-analysis engines now track micro-expressions, vocal pitch, and gesture accuracy in real time, reducing feedback latency that once hampered distance training. [1]Remocapp, “Motion Capture Suits: The Technology Behind Digital Performance,” remocapp.com Institutions embed these dashboards to personalise scene study and character development. Research shows that interactive methods that grant learners autonomy and competence lift deep-learning scores, validating the premium placed on data-rich tutoring. Platforms thereby convert subjective critique into quantifiable milestones, shortening mastery cycles and raising retention.

Surge in creator-economy platforms integrating actor-centric courses

Influencer-focused portals have widened their curricula to cover foundational acting, improvisation, and voice craft because performance skills boost on-camera authenticity. India’s USD 1 billion Creator Economy Fund illustrates policymakers' belief that screen-ready talent is a national asset. Revenue models blend subscription learning with content monetisation, as evidenced by Dropout’s ARR surpassing USD 30 million on performance-driven programming that merges entertainment with pedagogy. This dual-income allure differentiates online acting education market offerings from legacy conservatories.

Rising demand for remote voice-over and mocap skills in gaming and metaverse

Gaming studios and metaverse builders commission diverse vocal styles and lifelike avatar movements, spurring enrolment in niche workshops. Surveys show 68% of full-time voice actors invested ≥ USD 500 in coaching during 2024. Course providers package spatial-audio techniques, conversational delivery, and mocap routines into micro-credentials. Although AI voice cloning threatens 5,000 Australian voice jobs, programmes counterbalance by stressing emotional nuance and improvisation that synthetic speech cannot match.

Government-funded digital skilling grants for performing-arts freelancers

Public agencies view the creative sector as an economic lever. The European Commission allocated EUR 55 million to specialist digital-skills courses that include acting. The UK’s GBP 3 million Creative Careers Programme exposed 25,000 students to arts careers, boosting funnel volume. Such grants certify the online acting education market as a legitimate workforce-development pathway.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited hands-on rehearsal and scene-partner interaction Limited hands-on rehearsal and scene-partner interaction | -1.8% | Global | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.8% | Geographic Relevance:Global | Impact Timeline:Long term (≥ 4 years) |

High churn due to binge-consumption learning behaviour High churn due to binge-consumption learning behaviour | -2.1% | Consumer segments worldwide | Short term (≤ 2 years) | |||

Perception gap on credential value versus traditional diplomas Perception gap on credential value versus traditional diplomas | -1.4% | North America, Europe | Medium term (2-4 years) | |||

Bandwidth inequality in emerging markets Bandwidth inequality in emerging markets | -1.7% | Asia-Pacific, Africa, Latin America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High churn due to binge-consumption learning behaviour

Median MOOC completion rates run 12.6%, signalling that excitement fades quickly when skill gains need disciplined repetition. [2]Katy Jordan, “MOOC Completion Rates Revisited,” irrodl.org Acting amplifies the dilemma because muscle memory and emotional dexterity blossom over months, not weekend marathons. Providers deploy gamified milestones and community showcases to foster continuity, yet revenue forecasting remains volatile.

Bandwidth inequality in emerging markets

Uneven broadband limits high-resolution video that underpins performance critique. In the Philippines, fixed-line costs outstrip regional averages, limiting rural uptake. Providers compress streams and issue downloadable packets, but latency still degrades real-time direction. The shortfall inhibits Asia-Pacific’s lower-income cohorts from progressing beyond entry-level modules despite region-wide mobile-first ambitions.

By Class Type: Live Formats Drive Premium Engagement

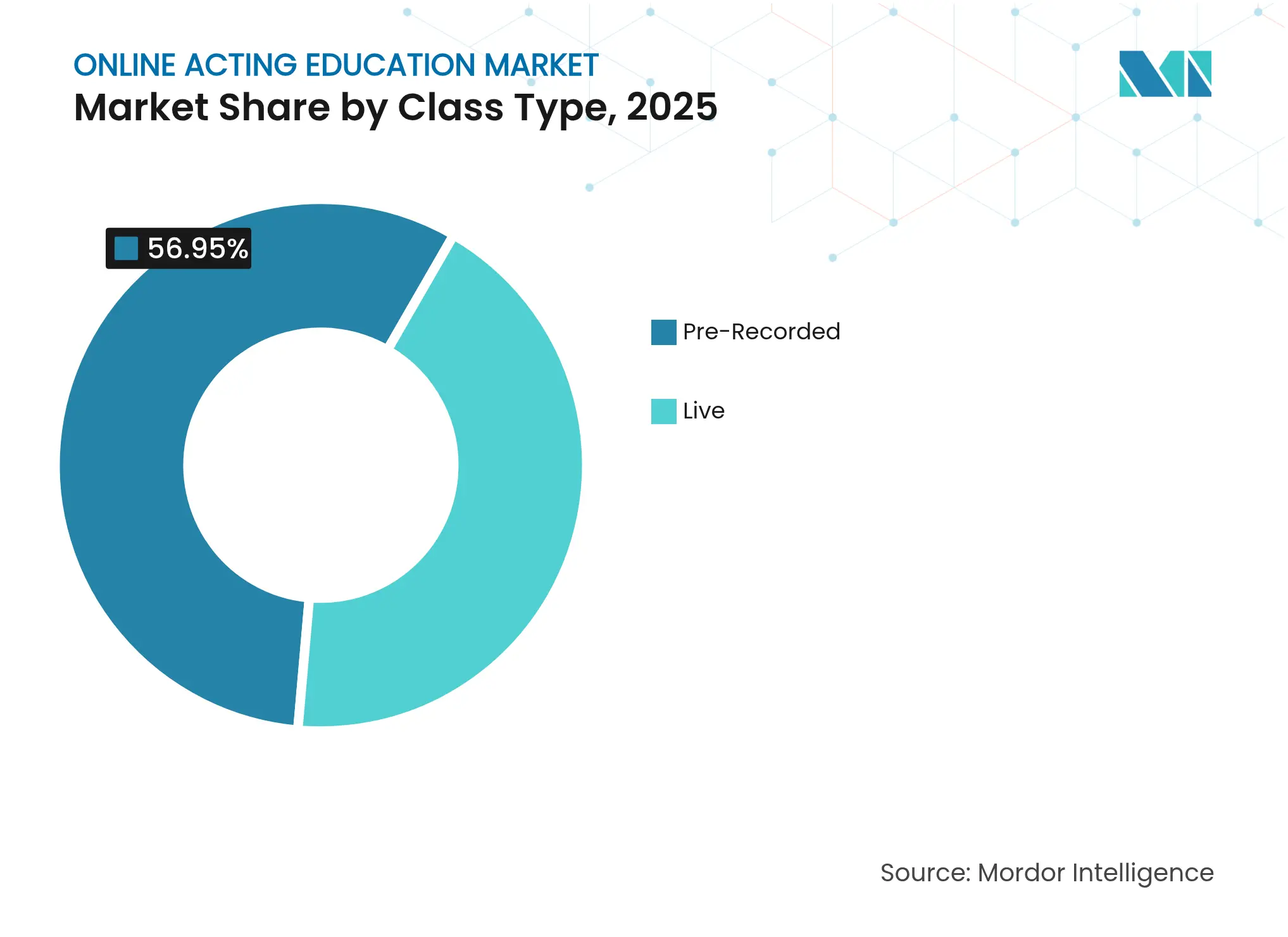

Live streaming enrolments are rising at a 16.25% CAGR even as pre-recorded assets retained 56.95% revenue in 2025, confirming a two-tier model where convenience seekers dominate volume while serious learners fuel the high-margin tier. The online acting education market relies on live formats to mimic conservatory spontaneity, allowing instructors to correct posture, diction, and emotional beats instantly. Research with prospective students reveals 74% will attend at least one synchronous session per course, underscoring blended-learning preference. Providers embed AI role-play to stretch class capacity without sacrificing authenticity. As a result, premium courses price 30% above asynchronous libraries yet enjoy stronger completion, improving lifetime value. The integration of EON Reality’s immersive toolset signals how virtual stages will further elevate live delivery.

Learner preference for predictable scheduling sustains demand for pre-recorded catalogues. However, providers avoid cannibalisation by positioning archives as prerequisite theory that funnels students into live cohorts for scene practice. This pipeline maximises utilisation rates and underpins recurring revenue. As the online acting education market size allocated to live tuition climbs alongside AI-aided facilitation, culture will shift toward continuous studio-style mentorship delivered remotely.

Note: Segment shares of all individual segments available upon report purchase

By Time Commitment: Part-Time Programs Dominate Working-Professional Segment

Part-time tracks commanded 62.55% of 2025 revenue, illustrating how actors juggle auditions, gig economy roles, and supplemental income. Providers package bite-sized modules with rolling intake to minimise opportunity cost. Yet the full-time pathway’s 16.4% CAGR shows appetite for decisive career pivots when platforms bundle industry networking and placement services. The University of Nebraska’s micro-credential partnership typifies how institutions target mid-career professionals seeking stackable qualifications.

Long-form immersive cohorts mirror conservatory intensity by scheduling daily workshops and ensemble rehearsals, relying on AI feedback to maintain instructional bandwidth. Providers report that full-time enrollees exhibit 25% higher average revenue per user, offsetting their longer acquisition cycles. The online acting education market size for full-time enrolments is projected to expand in tandem with enterprise-funded reskilling budgets linked to virtual-production pipelines.

By Skill Level: Advanced Segments Accelerate Despite Beginner Volume

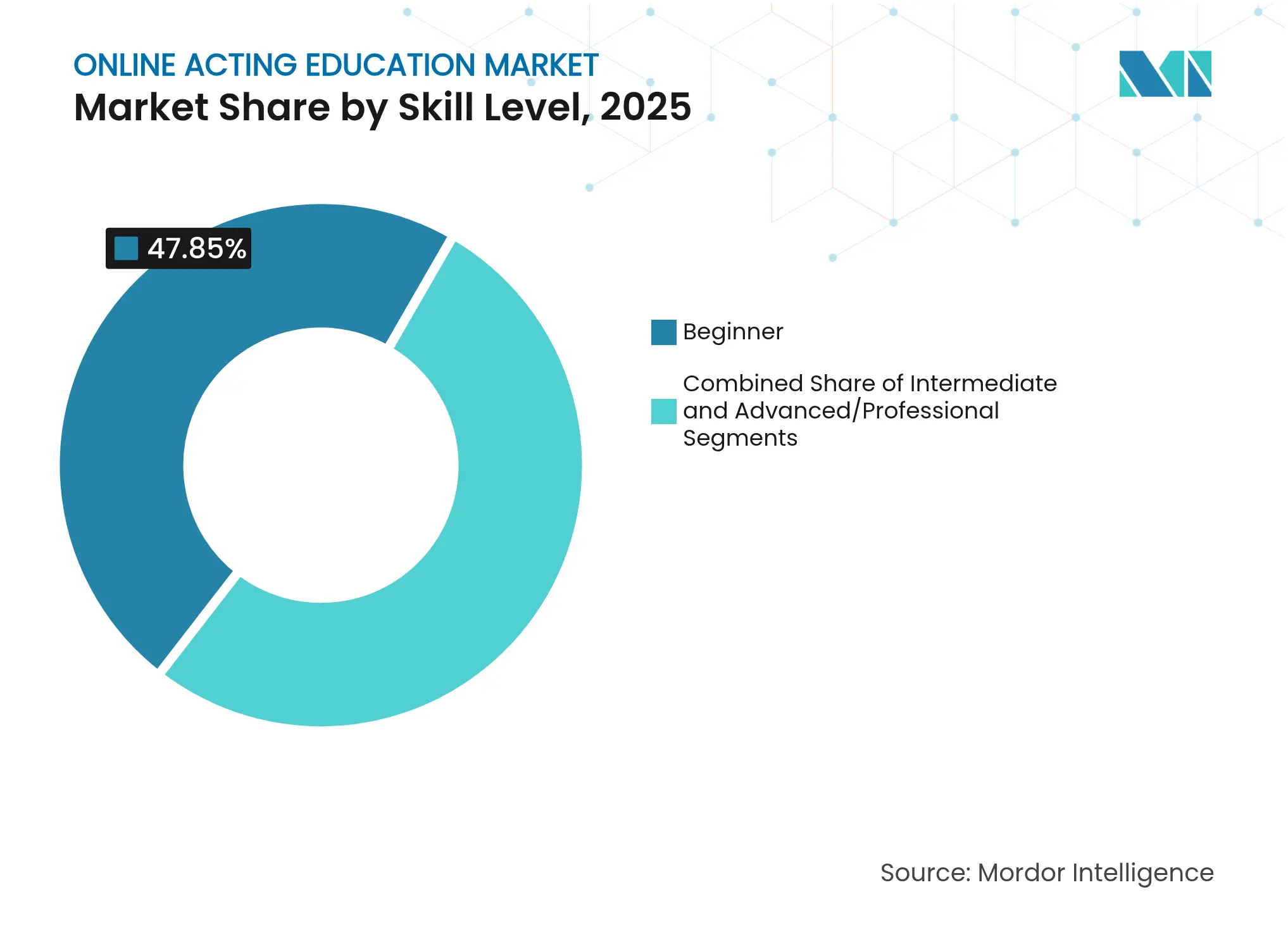

Beginners comprised 47.85% of learners in 2025, functioning as the top-of-funnel for brand exposure. However, advanced cohorts are expanding at 15.95% CAGR, underscoring platform success in nurturing progression. Adaptive AI assessments from Academic Labs map proficiency gaps, producing personalised rehearsal regimens that lift performance metrics. Advanced learners pay premiums for niche domains such as mocap and dialect coaching, generating outsized contribution margins.

The online acting education market size for professional-level content is forecast to approach USD 1.06 billion by 2031, representing significant wallet share migration from physical studios. Synthesia’s equity-for-avatar programme illustrates monetisation avenues that reward seasoned actors’ expertise. Continuous upskilling becomes compulsory as AI expands creative pipelines, cementing demand across the proficiency spectrum.

Note: Segment shares of all individual segments available upon report purchase

By Delivery Platform: Mobile-First Strategy Captures Emerging Markets

Mobile apps delivered 53.90% of 2025 revenues, reflecting smartphone centrality in India, Southeast Asia, and Africa. UX design prioritises low-bandwidth adaptive streaming, social sharing loops, and local-language captions. Nonetheless, hybrid/connected TV adoption is growing at 15.9% CAGR as smart-TV prices fall and living-room viewing repurposes large screens for group rehearsal. The BBC’s GBP 6 million investment in Bitesize improves discovery algorithms and high-resolution playback, reinforcing large-format appeal.

Web portals remain relevant for script annotation and multi-window workflows, especially within North American enterprises that finance employee upskilling. Providers pursue omnichannel parity, ensuring progress synchronises across devices. This approach minimises churn and lifts engagement time, critical for the online acting education market where sustained practice correlates with proficiency gains.

By Acting Domain: Voice-Acting Emerges as Growth Leader

Film and TV retained 45.75% domain revenue in 2025, yet voice-acting’s 15.55% CAGR showcases gaming and audiobook boom dynamics. Learners invest in acoustic-treatment kits and remote-recording technique tutorials to meet studio technical briefs. SM Institute’s adoption of virtual classrooms to train K-pop hopefuls signals crossover demand between music performance and voice acting. Theatre modules leverage digital sets and crowd-sourced ensembles to maintain stagecraft relevance.

Improvisation and comedy micro-courses thrive on social-media virality, fuelling short-form creator output. Cross-training across domains enhances employability; thus, programmes market bundled pathways that weave voice, screen, and stage competencies. The online acting education market share for voice-acting is projected to top 18.25% by 2031, elevating the modality from niche to strategic pillar.

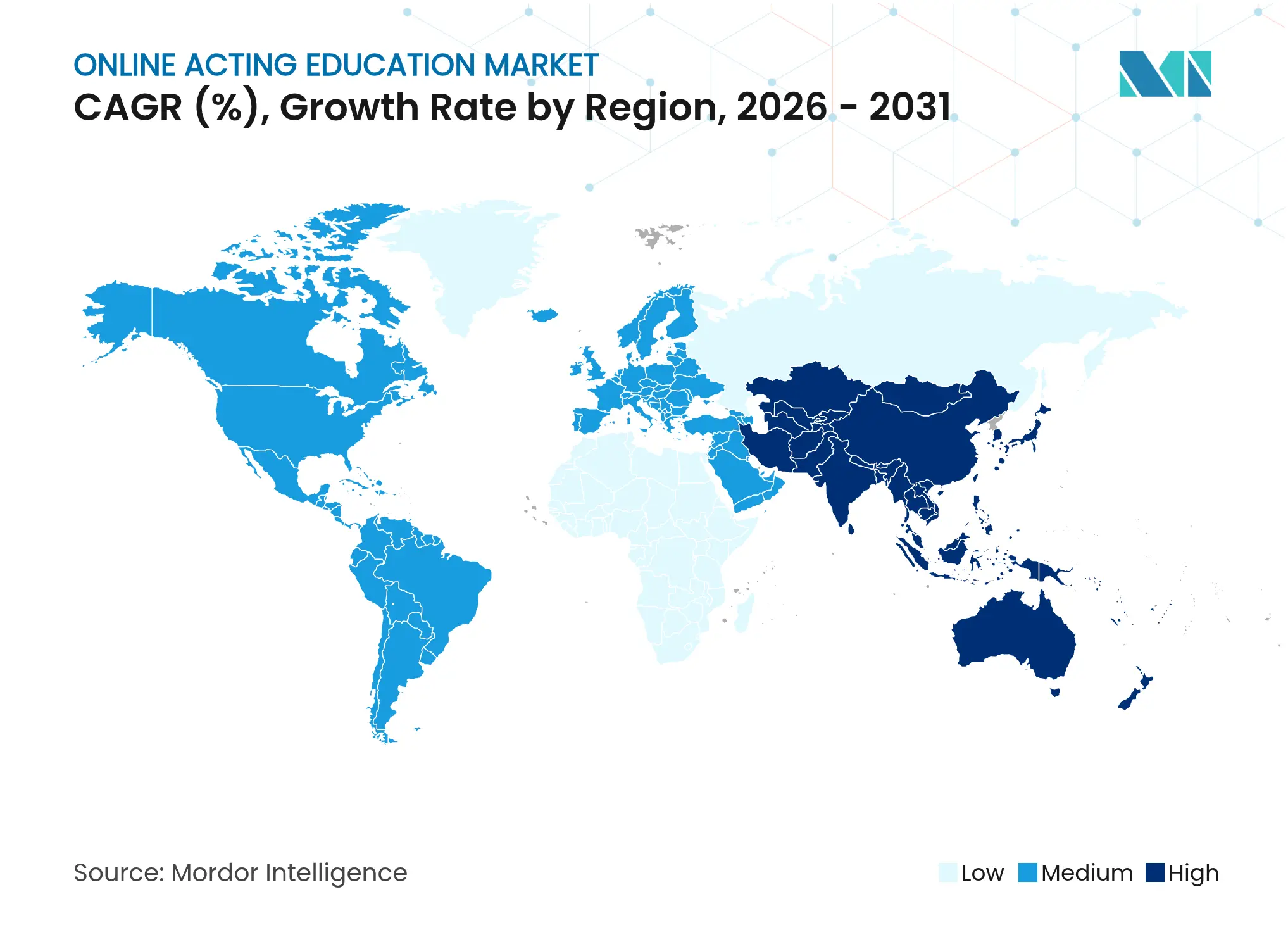

North America posted 38.10% revenue in 2025, anchored by entrenched entertainment infrastructure, strong broadband capacity, and early AI analytics adoption. Celebrity-fronted masterclasses command premium pricing, while universities licence hybrid curricula to scale reach. The online acting education market size in the region grows steadily as professionals pursue specialised voice-over and virtual-production certifications. Yet plateauing population growth and course saturation temper future acceleration.

Asia-Pacific is the fastest-expanding geography at 15.75% CAGR through 2031. Smartphone penetration above 80% in India and China, plus supportive policies such as the USD 1 billion Creator Economy Fund, catalyse mass enrolment. Government digital-arts grants, rising regional OTT content share, and culturally localized syllabi fuel adoption. Nonetheless, bandwidth disparity outside Tier-1 cities obliges providers to offer offline downloads and low-bitrate options.

Europe benefits from EUR 108 million Digital Europe skills outlay, where EUR 55 million fuels arts-oriented digital training. Multilingual content demand and regulatory focus on data privacy build learner trust. The online acting education market size across Europe is predicted to exceed USD 704.6 million by 2031, supported by public subsidies and cross-border co-production of immersive theatre and XR experiences.

Market Concentration

The sector remains moderately fragmented, with MasterClass, StageMilk, and Udemy grouping around celebrity cachet, craft depth, and mass-market breadth, respectively. Traditional conservatories now license short courses, leveraging brand equity online. Accenture’s acquisition of Udacity illustrates how big-tech consulting seeks proprietary learning ecosystems to reskill global workforces. [4]Constellation Research, “Education tech in turmoil amid genAI: Why consolidation is next,” constellationr.com IXL Learning’s purchase of MyTutor shows lateral expansion into one-on-one models that acting coaches can emulate.

Differentiation pivots on technology stack and outcomes. AI-first entrants deliver frame-by-frame feedback, adaptive scripts, and voice emotion graphs, while VR studios craft virtual sets for ensemble rehearsal. Pearson’s XR partnership indicates that publishers see immersive authoring as the next frontier. Creator-economy portals blur lines between education and monetisation, letting learners earn as they study, a model that erodes switching barriers.

Regional specialists surface in voice acting for anime, dialect coaching for Bollywood, and motion-capture for AAA games. Partnerships with talent agencies and streaming platforms yield placement guarantees that justify premium course fees. As the online acting education market consolidates, firms that align celebrity mentoring, adaptive tech, and global distribution will accrue scale advantages.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

The Online Acting Education Market includes various digital platforms, programs, and services designed to teach acting techniques and skills through virtual mediums. These platforms serve a broad audience, from aspiring actors and theater professionals to hobbyists and students looking to improve or master their craft.

The online acting education market is segmented by class type (live, pre-recorded), by time period (full-time, part-time), by geography (North America [United States, Canada], Europe [Germany, United Kingdom, France, Spain, and Rest of Europe], Asia-Pacific [India, China, Japan, New Zealand, Australia and Rest of Asia-Pacific], Latin America [Brazil, Mexico, and Rest of Latin America], Middle East and Africa. The report offers market forecasts and size in value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.