Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

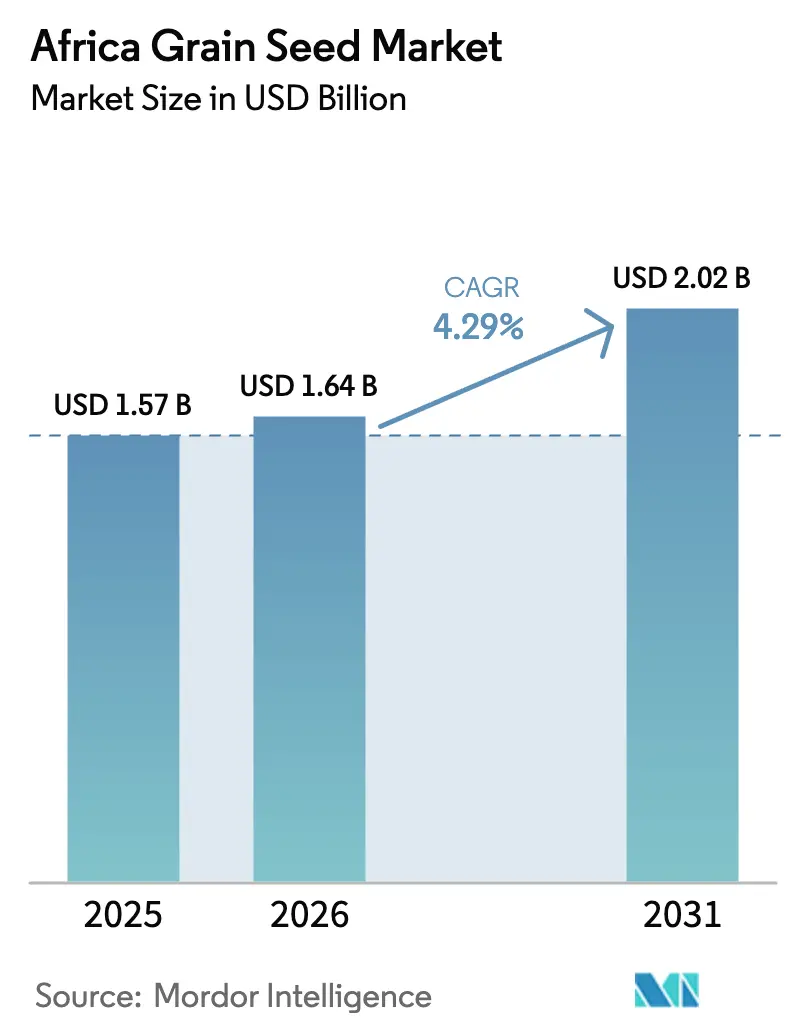

| Base Year Market Size (2025) | USD 1.57 Billion |

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.02 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Grain Seed Market Analysis by Mordor Intelligence

Africa grain seed market size in 2026 is estimated at USD 1.64 billion, growing from 2025 value of USD 1.57 billion with 2031 projections showing USD 2.02 billion, growing at 4.29% CAGR over 2026-2031. Steady government subsidy programs, heightened demand for climate-resilient varieties, and industrial pull from feed and brewing processors form the backbone of this momentum. Kenya’s mobile-based seed ordering platforms and South Africa’s mature commercial farming systems illustrate how digitalization and scale can converge to sustain volume growth. Market participants are also benefiting from regional seed-certification harmonization, which lowers entry costs and allows a wider distribution footprint. However, counterfeiting in informal markets and unfavorable fertilizer-to-grain price ratios remain headwinds that jeopardize realized productivity gains.

Key Report Takeaways

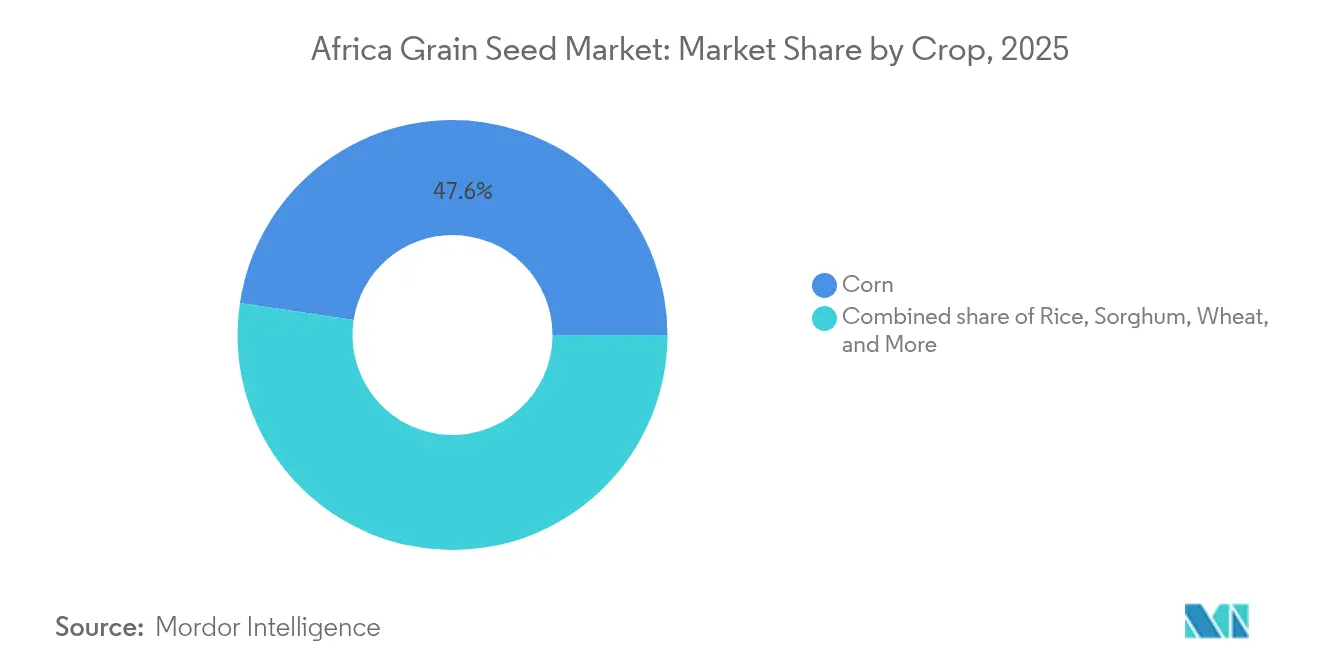

- By crop, corn led with 47.62% of Africa's grain seed market share in 2025, while sorghum is advancing at a 5.88% CAGR through 2031.

- By breeding technology, hybrids accounted for a 58.63% share of the Africa grain seed market size in 2025, and open-pollinated varieties and hybrid derivatives are projected to rise at a 4.67% CAGR through 2031.

- By geography, South Africa commanded 33.45% revenue share in 2025, whereas Kenya is set to register the highest 6.12% CAGR to 2031.

- The top five suppliers controlled 36.20% of Africa's grain seed market share in 2025, underscoring a moderately fragmented marketplace. The major players in the market include Bayer AG, Corteva Agriscience, Groupe Limagrain, Seed Co. Limited, and Syngenta AG.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Grain Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government seed subsidy programs boosting hybrid adoption | +0.8% | Pan-African, strongest in Kenya, Nigeria, Ghana | Medium term (2-4 years) |

| Rising demand for climate-resilient grain varieties | +0.9% | Sub-Saharan Africa core, expanding to North Africa | Long term (≥ 4 years) |

| Expansion of commercial feed and brewing industries needing quality grains | +0.6% | South Africa, Nigeria, Kenya, Egypt | Medium term (2-4 years) |

| Regional harmonization of seed certification easing cross-border trade | +0.4% | Eastern, Southern, and Western Africa | Long term (≥ 4 years) |

| Emergence of mobile-based direct seed marketing platforms | +0.5% | East Africa core, spillover to West Africa | Short term (≤ 2 years) |

| Rapid uptake of male-sterile technology lowering hybrid maize seed costs | +0.7% | South Africa, Kenya, Tanzania, Zimbabwe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Seed Subsidy Programs Boosting Hybrid Adoption

Subsidies remain a critical lever for accelerating hybrid penetration. Kenya has allocated more than USD 50 million annually to its National Agricultural and Rural Inclusive Growth Project, lifting hybrid maize adoption from 35% in 2022 to above 60% by 2024 [1]Source: World Bank, “Kenya National Agricultural and Rural Inclusive Growth Project,” worldbank.org. Nigeria’s Anchor Borrowers Program distributed over 2 million bags of certified seed in 2024, demonstrating the scale at which policy can recast demand [2]Source: Central Bank of Nigeria, “Anchor Borrowers Programme,” cbn.gov.ng. Such programs reduce farmer risk, create habitual demand, and smooth the transition to commercial seed purchasing once subsidies recede. Yet long-term continuity hinges on clear demonstrations of value beyond subsidized seasons.

Rising Demand for Climate-Resilient Grain Varieties

Weather volatility has shifted farmer priorities toward drought tolerance and heat resilience. Drought-tolerant hybrids now occupy more than 40% of total hybrid maize acreage in Eastern and Southern Africa, a sharp rise from 15% in 2020[3]Source: International Crops Research Institute for the Semi-Arid Tropics, “Drought-Tolerant Crops for Africa,” icrisat.org. Bayer’s DroughtGard portfolio and similar traits have found quick acceptance thanks to yield stability under moisture stress. Adoption is spreading beyond maize into sorghum and millet, as improved varieties blend traditional hardiness with better processing quality. Policymakers are streamlining approvals to speed market entry of climate-smart seeds.

Expansion of Commercial Feed and Brewing Industries Needing Quality Grains

The industrial demand for consistent grain quality has created premium market segments that encourage farmers to adopt certified seed varieties with predictable characteristics. In Africa, the feed industry sources grains based on specific nutritional profiles and mycotoxin levels, offering premiums that justify higher seed costs. Brewing companies like South African Breweries Miller, and Heineken N.V. have introduced direct procurement programs specifying grain varieties and quality standards, providing farmers with guaranteed markets. This demand has proven more sustainable than government subsidies, as farmers calculate returns based on market premiums.

Regional Harmonization of Seed Certification Easing Cross-Border Trade

The African Continental Free Trade Area has driven efforts to standardize seed certification processes, reducing regulatory barriers. The Common Market for Eastern and Southern Africa enables regional marketing of approved seed varieties without additional testing, lowering market entry costs and fostering investment in breeding programs. Similarly, the Economic Community of West African States facilitates seed trade by bypassing individual country approvals. However, uneven implementation persists due to additional requirements in some countries. Regulatory convergence is anticipated to grow as countries recognize the benefits of integrated seed markets for food security, addressing challenges that transcend national borders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of counterfeit or low-quality seeds in informal markets | -0.6% | Pan-African, most severe in Nigeria, Ghana, Tanzania | Long term (≥ 4 years) |

| High fertilizer-to-grain price ratios limiting realized seed benefits | -0.5% | Sub-Saharan Africa, particularly landlocked countries | Medium term (2-4 years) |

| Fragmented last-mile distribution increasing seed delivery costs | -0.4% | Rural Africa, most acute in remote farming areas | Medium term (2-4 years) |

| Limited supply of early generation seed for OPV sorghum and millet | -0.3% | Semi-arid regions, Sahel countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Counterfeit or Low-Quality Seeds in Informal Markets

Counterfeit and substandard seed proliferation undermines farmer confidence in improved seed varieties and impacts the formal seed market. The Alliance for a Green Revolution in Africa estimates that 30-40% of seeds sold in informal markets across sub-Saharan Africa fail to meet basic quality standards, leading to yield losses. This issue is significant in Nigeria and Ghana, where weak enforcement allows counterfeit products to circulate freely. Farmers experiencing poor results from counterfeit seeds often revert to saved seeds or reduce input investments in subsequent seasons. Regulatory frameworks exist but lack resources for effective enforcement, particularly in rural areas where most seed transactions occur.

High Fertilizer-to-Grain Price Ratios Limiting Realized Seed Benefits

Volatile fertilizer prices have created economic challenges for farmers, preventing them from affording the complementary inputs needed to maximize the benefits of improved seed varieties. The Russia-Ukraine conflict disrupted global fertilizer supply chains, leading to price increases exceeding 200% in certain African markets between 2022 and 2024, while grain prices remained relatively stable[4]Source: Food and Agriculture Organization, “Fertilizer Price Monitoring,” fao.org. This disparity has made it economically unfeasible for many farmers to invest in premium seeds without the necessary fertilizer applications. Landlocked countries face additional difficulties due to elevated transportation costs, which further increase fertilizer prices. Government fertilizer subsidy programs have offered temporary relief in some regions, but their fiscal constraints limit both their sustainability and reach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Drive Premium Segment Growth

Hybrids secured a commanding 58.63% share of the Africa grain seed market in 2025. Superior yields, uniformity, and processor acceptance make hybrids a staple for commercial producers, especially in South Africa and Egypt. Multinationals deploy extensive R&D pipelines, refreshing varietal catalogs every two to three years. Transgenic hybrids remain limited to jurisdictions with clear biosafety laws, yet male-sterile non-GMO hybrids now bridge cost gaps, expanding reach. The Africa grain seed market size attributable to hybrid maize is projected to increase in line with commercial feed demand through 2031.

Open-pollinated varieties and hybrid derivatives are expanding at a 4.67% CAGR, capturing budget-conscious smallholders. New OPVs promote drought tolerance and biofortification, addressing nutrition as well as resilience. Harmonized COMESA and ECOWAS rules now allow a single variety release to service multiple countries, encouraging seed companies to retain OPV portfolios rather than drop them entirely. This dual-track approach safeguards food security while letting farmers adjust input spending to seasonal cash flow.

By Crop: Corn’s Dominance Meets Climate-Smart Diversification

Corn held 47.62% of Africa's grain seed market share in 2025, underpinned by poultry, swine, and brewing demand. Processors require predictable starch and protein profiles, sustaining premium payment models that justify hybrid seed outlays. Yet fall armyworm outbreaks and erratic rainfall expose mono-crop risk. Sorghum’s 5.88% CAGR indicates farmers are diversifying toward hardier crops. Improved sorghum hybrids and OPVs combine drought resistance with upgraded taste and milling traits, making the switch economically feasible even for subsistence growers. Rice remains buoyant due to import-substitution policies in Nigeria and Ghana, while wheat trails owing to climatic and infrastructural restrictions.

Feed-milling capacity expansion, especially in Nigeria, where installed feed volume surpassed 5 million metric tons in 2024, will keep corn in pole position, but varietal diversification is gaining momentum. The Africa grain seed market size in the sorghum and millet segments is anticipated to widen as consumer preferences tilt toward traditional staples perceived as healthier.

Geography Analysis

South Africa holds a 33.45% market share in the Africa grain seed market, driven by advanced production capabilities, strong biosafety regulations, and an extensive network of agro-dealers ensuring timely seed delivery to commercial farms. A significant portion of hybrid maize under cultivation originates from the latest two breeding cycles, supporting consistently high yields even during periods of drought. Additionally, the country supplies seeds to Zambia, Mozambique, and Botswana through contract multiplication schemes that leverage favorable production microclimates. In 2024, seed exports increased by 7% in value as neighboring countries utilized South Africa's quality control infrastructure.

Kenya is projected to achieve the highest CAGR of 6.12% in the Africa grain seed market by 2031, driven by a smallholder-focused agricultural framework that positions the country as a hub for digital agriculture innovation. In 2024, around 500,000 farmers accessed certified seeds through mobile platforms, significantly reducing ordering lead times from weeks to days. Government e-voucher programs subsidized a portion of seed costs, enhancing early-season liquidity for farmers. This initiative is a key contributor to Kenya's anticipated market growth. Additionally, local processors are strengthening specialty grain supply chains, promoting the adoption of hybrid varieties in crops such as maize, sorghum, and barley. The market share of grain seeds in Kenya is projected to expand further as more counties integrate subsidy portals with distribution telemetry systems.

Nigeria presents both scale and complexity. Counterfeit seed undermines farmer trust, yet ongoing regulatory sweeps and serialization efforts signal gradual progress. Anchor Borrowers participants who received certified seed and agronomic support logged yield gains exceeding 20% in 2024 crops. Ethiopia, Ghana, and Tanzania leverage multi-donor seed sector programs that couple breeder-foundation seed production with private distribution networks. Each country now operates at least one ISTA-accredited seed laboratory, accelerating domestic certification turnaround. In the Sahel, sorghum and millet dominate, and OPV shortages curtail yield gains despite fertile demand conditions. Egypt maintains niche leadership in irrigated wheat and specialty barley suited for malting under controlled water regimes.

Competitive Landscape

The Africa grain seed market competition is moderate, with the top five firms holding around 36.5% combined share. Seed Co Limited maintains its market leadership through an extensive presence in Southern Africa and effective engagement with smallholder farmers. Bayer AG leverages its proprietary trait stacks for drought and pest resistance, supported by localized production facilities in Kenya. Corteva Agriscience enhances its product development by utilizing regional breeding stations, with plans to introduce three hybrids tailored for West Africa in 2024.

Male-sterile production, doubled haploid pipelines, and genomic selection represent critical technological advancements in the seed industry. Seed Co Limited’s acquisition of Victoria Seeds in Tanzania has enhanced its distribution capabilities in East Africa, while Groupe Limagrain’s establishment of an office in Ghana has expanded its presence in Francophone markets. Digital-native companies are partnering with telecom providers to offer bundled solutions that include seed sales, credit, and crop insurance, addressing high-cost last-mile distribution challenges that traditional players find difficult to manage. Adherence to International Seed Testing Association (ISTA) standards and alignment with Common Market for Eastern and Southern Africa (COMESA) labeling requirements have become key differentiators when competing for government subsidy tenders.

Open-pollinated variety (OPV) sorghum and millet segments remain underdeveloped due to low profit margins, deterring larger companies. The specialized regional firms and public-private consortia are stepping in to meet the growing demand for climate-smart crops. Although fragmented informal trade continues to divert market volumes, improved enforcement measures and serialization efforts are projected to enhance brand protection and integrity over time.

Africa Grain Seed Industry Leaders

Bayer AG

Corteva Agriscience

Groupe Limagrain

Seed Co Limited

Syngenta AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The African Agricultural Technology Foundation (AATF) and its partners launched TELA maize hybrids in Ethiopia, Kenya, Mozambique, and Nigeria through the Biotech Maize Seed Systems partnership. These maize varieties combine drought tolerance with insect protection capabilities.

- April 2025: The International Maize and Wheat Improvement Center (CIMMYT) released seven new tropical maize hybrids from its Eastern Africa breeding program. These hybrids are available for licensing and are developed to withstand drought, heat stress, and major diseases. Partners can now pursue national registration and distribution of these varieties.

- March 2025: Bayer opened a EUR 32 million (USD 34.8 million) maize seed facility in Kabwe, Zambia, to supply high-yielding maize seeds to approximately 6.4 million smallholder farmers in 2025, with plans to reach 10 million farmers by 2030. This investment supports Bayer's strategy to double its Crop Science business in Africa by 2030.

Africa Grain Seed Market Report Scope

The Africa Grain Seed Market Report is Segmented by Breeding Technology (Hybrids, Open Pollinated Varieties, and Hybrid Derivatives), Crop (Corn, Rice, Sorghum, Wheat, Other Grains and Cereals), and Geography (Egypt, Ethiopia, Ghana, Kenya, Nigeria, South Africa, Tanzania, Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Insect Resistant Hybrids | ||

| Open Pollinated Varieties and Hybrid Derivatives | ||

Crop

| Corn |

| Rice |

| Sorghum |

| Wheat |

| Other Grains and Cereals |

Geography

| Egypt |

| Ethiopia |

| Ghana |

| Kenya |

| Nigeria |

| South Africa |

| Tanzania |

| Rest of Africa |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Insect Resistant Hybrids | |||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Crop | Corn | ||

| Rice | |||

| Sorghum | |||

| Wheat | |||

| Other Grains and Cereals | |||

| Geography | Egypt | ||

| Ethiopia | |||

| Ghana | |||

| Kenya | |||

| Nigeria | |||

| South Africa | |||

| Tanzania | |||

| Rest of Africa | |||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms