Objectives And Key Results (OKR) Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

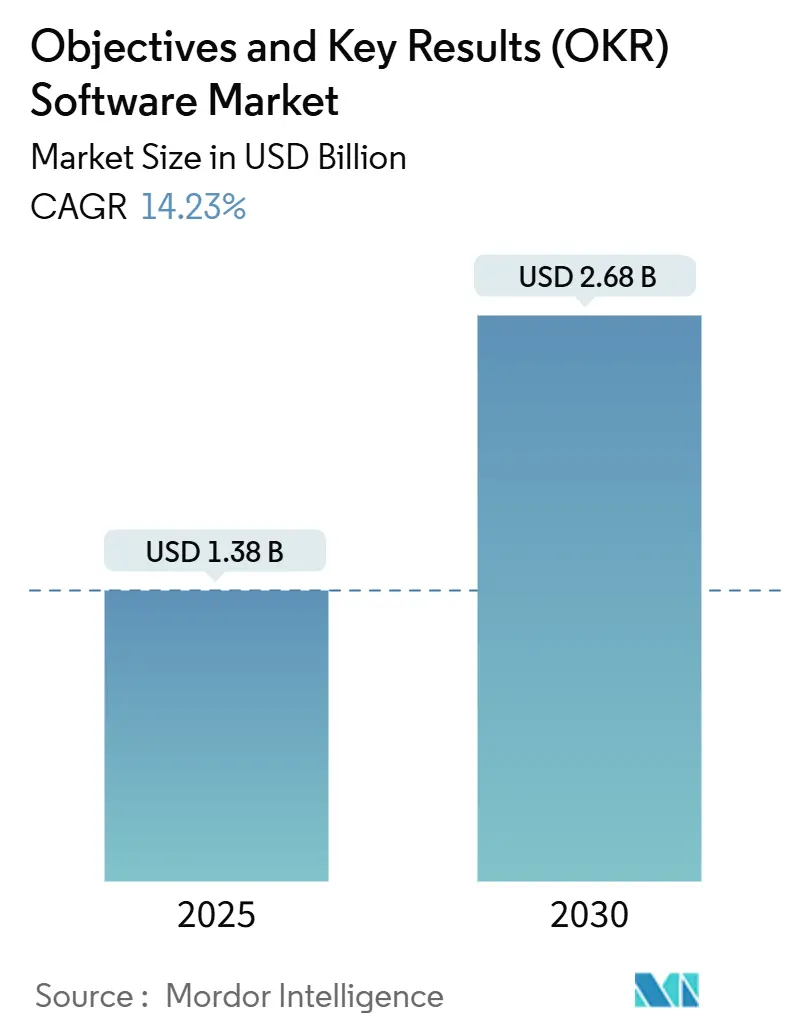

| Market Size (2025) | USD 1.38 Billion |

| Market Size (2030) | USD 2.68 Billion |

| Growth Rate (2025 - 2030) | 14.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Objectives And Key Results (OKR) Software Market Analysis by Mordor Intelligence

The OKR software market size stands at USD 1.38 billion in 2025 and is forecast to reach USD 2.68 billion by 2030, advancing at a 14.23% CAGR. Accelerated cloud adoption, permanent remote work patterns, and AI-driven analytics are reinforcing double-digit expansion. Organizations are replacing annual reviews with always-on goal frameworks that foster real-time alignment at scale. Deep integrations with collaboration suites and HR information systems are turning goal data into a single performance truth. At the same time, venture-capital-funded freemium models are widening access for small and medium enterprises, while enterprise buyers favor platforms that address data governance mandates in regulated sectors. Competitive intensity is climbing as vendors converge toward integrated performance-management ecosystems that bundle OKRs, engagement analytics, and coaching workflows.

Key Report Takeaways

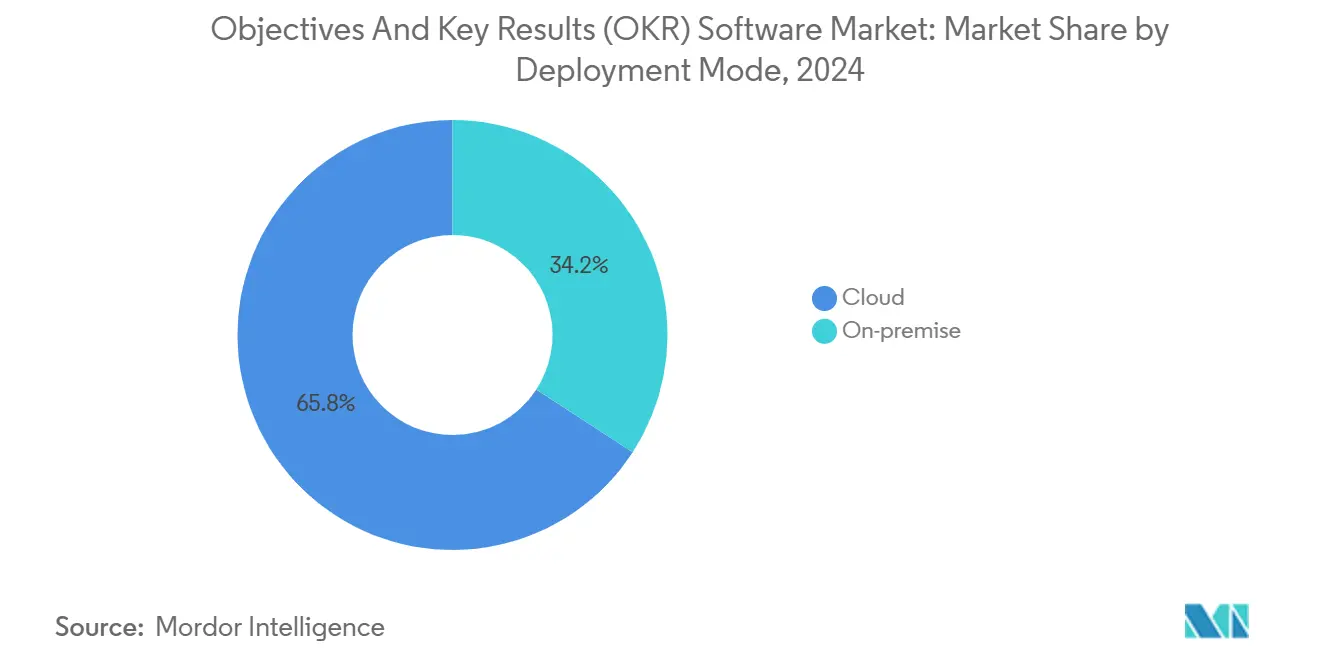

- By deployment mode, cloud-based solutions captured 65.83% of the OKR software market share in 2024; on-premise deployments are projected to expand at a 16.11% CAGR through 2030.

- By component, solutions held 70.83% of the OKR software market size in 2024, while services are forecast to advance at a 16.44% CAGR to 2030.

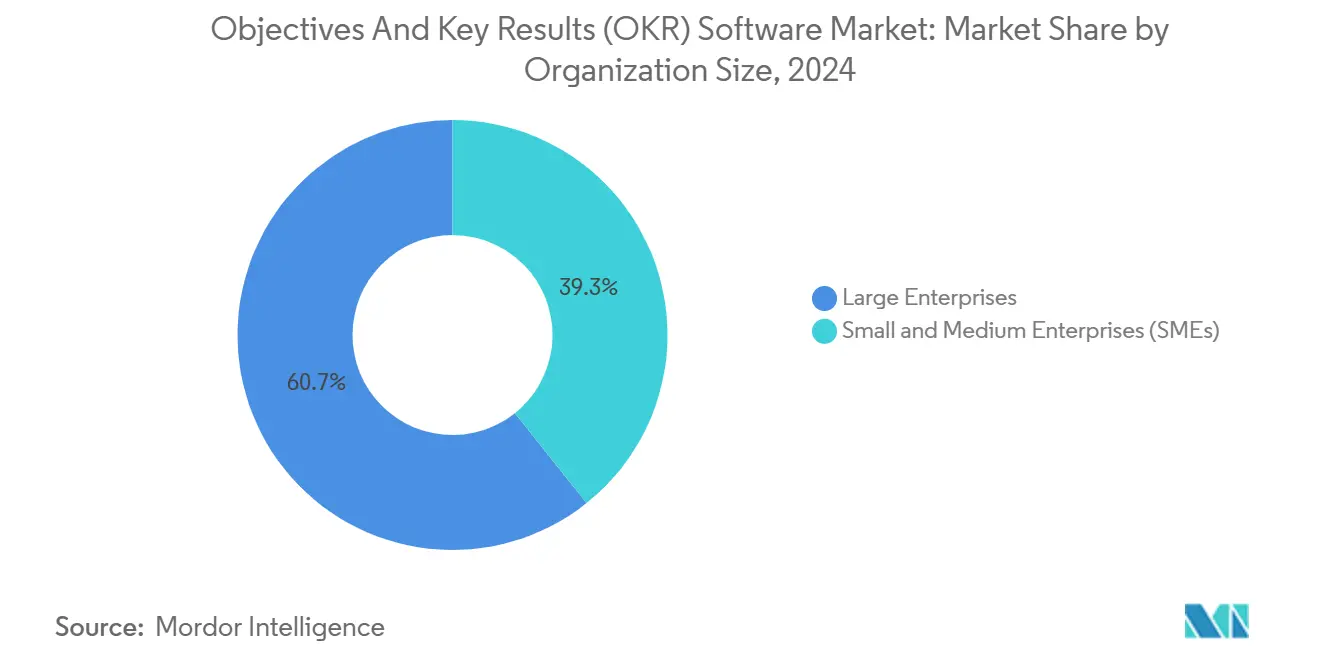

- By organization size, large enterprises accounted for 60.72% share of the OKR software market size in 2024, whereas small and medium enterprises are progressing at a 15.78% CAGR through 2030.

- By industry vertical, IT and telecommunications led with 28.73% revenue share in 2024 in the OKR software market; healthcare is expected to grow at a 14.99% CAGR to the end of the decade.

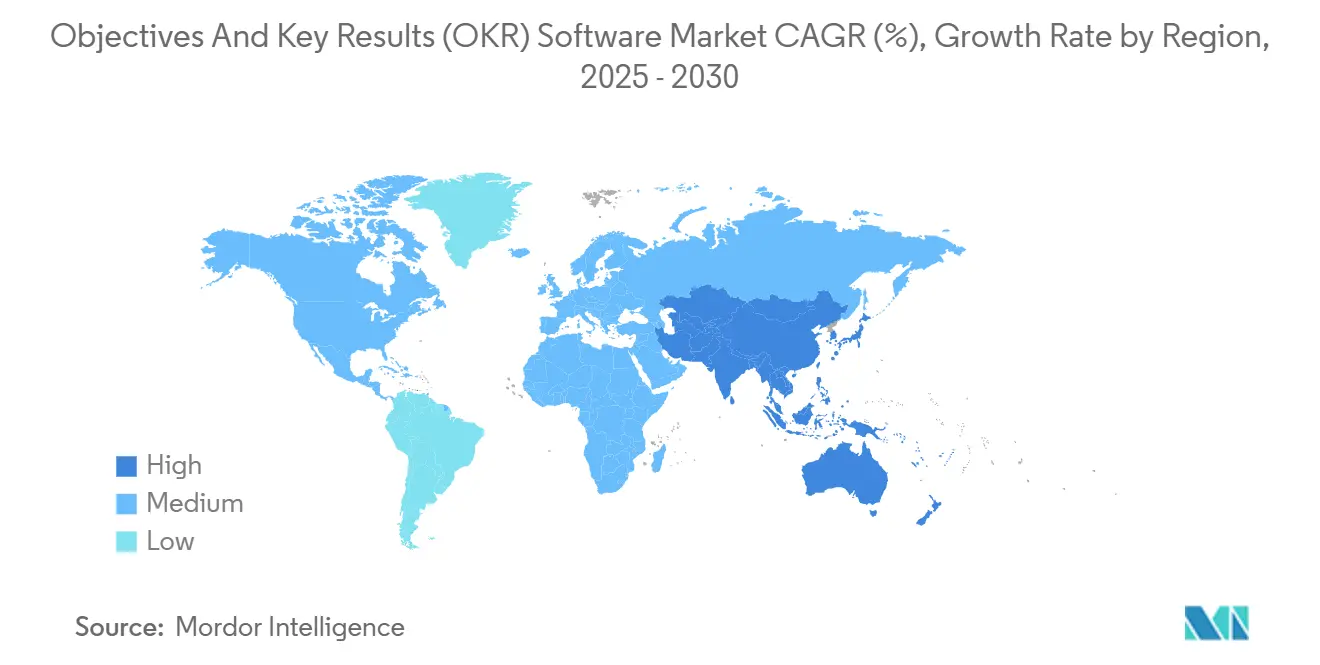

- By geography, North America controlled 39.83% revenue in 2024 in the OKR software market, while Asia-Pacific is set to register the fastest 15.44% CAGR through 2030.

Global Objectives And Key Results (OKR) Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of cloud-based SaaS performance-management suites | +3.6% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Need for goal-alignment and transparency in remote / hybrid workforces | +2.8% | Global, particularly strong in APAC and North America | Short term (≤ 2 years) |

| Deep integrations with HRIS and collaboration stacks | +2.1% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Freemium and VC-funded pricing models accelerating SME uptake | +1.7% | Global, with early gains in India, Southeast Asia, South America | Long term (≥ 4 years) |

| AI-powered OKR recommendation engines for predictive alignment | +1.1% | North America and EU core, spill-over to APAC | Medium term (2-4 years) |

| Vertical-specific OKR templates for regulated industries | +0.9% | Global, with regulatory focus in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Cloud-Based SaaS Performance-Management Suites

Cloud-native platforms are displacing on-premise systems as enterprises seek elasticity, global uptime, and real-time collaboration. Microsoft’s Viva Goals embedded in Teams shows how scalable architectures deliver AI-generated goal recommendations and predictive progress alerts.[1]Microsoft Corporation, “Microsoft Viva Goals,” Microsoft.com Implementation windows have fallen from 9 months to under 6 weeks, and automatic security patching now meets stringent enterprise compliance requirements. Multi-tenant designs also simplify rollout across subsidiaries with localized governance rules. The shift positions cloud as the default foundation for continuous performance optimization, especially in data-intensive industries.

Need for Goal Alignment and Transparency in Remote / Hybrid Workforces

Remote work permanence has elevated OKR platforms from optional to mission-critical. Vietnamese technology group FPT reported 95% employee coverage and 20% revenue uplift after enterprise-wide rollout, underscoring measurable business impact.[2]FPT Corporation, “Digital Transformation Success with OKR Implementation,” Fpt.com Granular visibility into priorities keeps distributed teams engaged and accountable, while built-in sentiment analytics detect friction before output dips. The demand is particularly acute in hierarchical APAC firms modernizing toward collaborative cultures that value psychological safety.

Deep Integrations with HRIS and Collaboration Stacks

OKR suites are evolving into orchestration layers for performance data. WorkBoard’s acquisition of Quantive in May 2025 highlights the race to unify goal management, talent analytics, and engagement metrics under one roof. Yet 35% of enterprises still report inadequate HR tech integration, and 30% view this gap as the largest adoption barrier.[3]Lattice, “HR Technology Integration Challenges Report 2024,” Lattice.com API-first roadmaps, pre-built connectors, and managed-service engagement models are therefore central to vendor differentiation.

Freemium and VC-Funded Pricing Models Accelerating SME Uptake

Gtmhub’s USD 120 million Series C round in 2024 financed expanded freemium tiers that lower entry barriers for cost-conscious SMEs. Zero-license entry points create viral exposure, but sustainable unit economics require conversion to premium analytics within 12-18 months. Vendors are refining onboarding flows and guided best-practice templates to shorten payback periods while delivering enterprise-grade security even at lower tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low awareness and change-management hurdles among SMEs | -1.1% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Complex integration with legacy HR/ERP systems | -0.9% | North America and Europe, with legacy system concentration | Short term (≤ 2 years) |

| Data-security and compliance concerns for strategic data | -0.7% | Global, with heightened focus in regulated industries | Short term (≤ 2 years) |

| Metric-overload fatigue causing user churn | -0.6% | Global, particularly in organizations with multiple performance tools | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Awareness and Change-Management Hurdles Among SMEs

Digital skill gaps remain a headwind: 46% of SMEs lack structured programs that would smooth the transition from spreadsheets to software-driven goal frameworks. Transparency can clash with command-and-control cultures, creating a productivity dip before benefits materialize. Vendors are countering with bite-sized e-learning, pre-configured industry templates, and bundled coaching services that reduce organizational friction.

Complex Integration with Legacy HR/ERP Systems

Enterprises holding on to decade-old HRIS or ERP stacks confront significant technical debt. Integrations must honor SOC 2 and ISO 27001 controls, and heavily regulated verticals must map OKR data flows to HIPAA or SOX rules. Where API coverage is limited, organizations often default to parallel processes, which can undermine ROI. Specialized system integrators and middleware layers are therefore becoming critical success factors in heavily regulated industries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Dominance Accelerates AI Integration

Cloud-based platforms commanded 65.83% share of the OKR software market in 2024 and are projected to grow at a 16.11% CAGR through 2030. The OKR software market size advantage reflects architectural flexibility that sustains rapid AI feature iteration. Enterprise buyers view continuous delivery pipelines as the safest route to compliance and innovation. On-premise deployments linger in government and life-sciences settings with data sovereignty mandates, yet hybrid designs are surfacing that store sensitive datasets locally while pushing analytics to the cloud. Vendor roadmaps heavily weight cloud, signaling declining long-term support for on-premise upgrades.

Cloud deployments also demonstrate higher engagement rates: automated nudges, AI-driven insights, and integrated chatbots amplify user adoption. Meanwhile, scaling across global subsidiaries no longer requires separate infrastructure investments, a decisive cost edge. These dynamics keep the cloud segment firmly ahead on both revenue and unit economics, cementing its leadership inside the broader OKR software market.

By Component: Services Growth Outpaces Solutions

Software licenses still generated 70.83% revenue in 2024, signposting solution primacy. Yet professional and managed services will expand at a 16.44% CAGR to 2030, eclipsing license growth. The shift confirms buyer recognition that technology alone does not institutionalize goal-driven cultures. Advisory engagements covering change management, coaching, and advanced analytics are now bundled with platform contracts, increasing average deal size. System integrators and consulting boutiques specializing in OKRs are emerging as must-have partners for deployments exceeding 5,000 employees.

Services revenue further benefits from multi-year success programs that lock in platform stickiness. As AI functionality deepens, demand grows for data scientists who can translate predictive insights into operational actions. These trends point to a blended commercial model where recurring services account for a growing slice of total addressable opportunity within the OKR software market.

By Organization Size: SME Segment Emerges as Growth Engine

Large enterprises retained a 60.72% share in 2024, driven by complex matrix structures that require sophisticated alignment. However, SMEs will post the highest 15.78% CAGR through 2030, powered by accessible pricing and self-serve configurations. Freemium tiers short-circuit lengthy purchasing cycles, and API-light integrations reduce IT dependence. Mid-market firms (500-5,000 employees) are carving out a hybrid path, demanding enterprise-level security but consumer-grade ease of use. Vendors that tailor packaging, success metrics, and onboarding playbooks to this cohort are capturing outsized growth.

SMEs also illustrate a volume play: churn can be higher, yet cohort growth remains robust as digital transformation accelerates globally. The segment’s multiplier effect on brand visibility and ecosystem expansion is a strategic draw, steering R&D toward intuitive UX and template libraries that lower the learning curve and foster viral adoption across the OKR software market.

By Industry Vertical: Healthcare Leads Growth Despite IT Dominance

IT and telecommunications held 28.73% revenue in 2024, reflecting early adoption of agile methodologies. Healthcare, however, is primed for the fastest 14.99% CAGR. Hospitals deploy OKRs to link clinical objectives to patient outcomes and to streamline compliance reporting. BFSI follows closely as transparency requirements align with risk management mandates. Retail and manufacturing are accelerating adoption to synchronize supply-chain and customer-experience goals that span multiple functions.

Vertical specialization is becoming a differentiator. Vendors are rolling out HIPAA-ready or GDPR-ready modules, pre-mapped to typical metric hierarchies. These features elevate time-to-value in sectors saddled with complex regulations, reinforcing healthcare’s momentum inside the OKR software market.

Geography Analysis

North America continues to anchor the OKR software market with 39.83% share in 2024 owing to entrenched SaaS maturity, management-consulting ecosystems, and enterprise cloud budgets. Local vendors leverage proximity to Fortune 1000 headquarters to pilot AI modules rapidly, reinforcing innovation cycles. Yet high penetration levels signal slower incremental growth compared with emerging territories.

Europe exhibits steady but regulation-driven adoption. Data privacy statutes such as GDPR elevate secure data-handling capabilities to top evaluation criteria. Brexit reorganizations have intensified demand for transparent alignment mechanisms as multi-country operations reassess supply chains. System integrators play a pivotal role in tailoring OKR workflows to heterogeneous linguistic and legal contexts across the continent.

Asia-Pacific represents the highest-velocity expansion at 15.44% CAGR. India’s SaaS boom is democratizing access for SMEs, while China’s state-mandated digital-transformation programs propel enterprise uptake. Japanese conglomerates are customizing objectives to fit intricate seniority systems, creating space for local vendors versed in domestic corporate norms. Southeast Asian startups view OKRs as foundational architecture that scales with their cross-border ambitions, further enlarging regional demand within the OKR software market.

Competitive Landscape

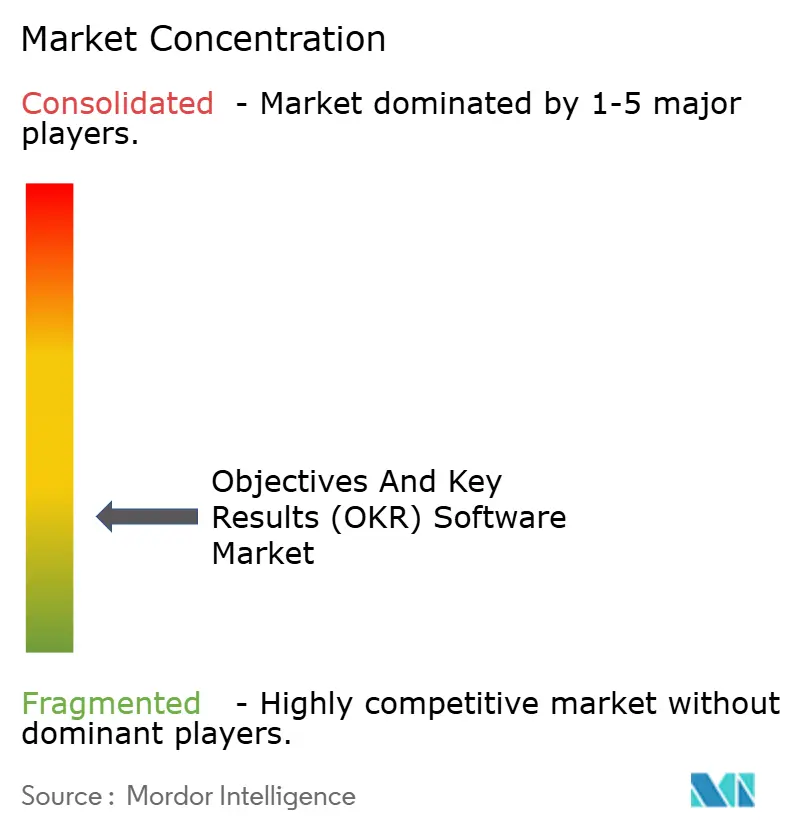

With more active vendors, the OKR software market remains moderately fragmented, yet consolidation signals a pivot toward platform maturity. WorkBoard’s May 2025 acquisition of Quantive merges enterprise-grade analytics with mid-market speed, forming a comprehensive suite that challenges point-solution rivals. Similar tie-ups are expected as buyers prefer integrated workflows over isolated feature sets.

Strategic positioning splits into three archetypes. Enterprise-oriented platforms tout SOC 2, ISO 27001, and zero-trust architectures. SME-focused challengers leverage freemium models and low-touch onboarding to drive viral growth. Vertical specialists embed compliance templates and metric taxonomies targeting healthcare, BFSI, or public-sector pain points. Technical differentiation hinges on proprietary AI that auto-suggests objectives, detects execution risks, and forecasts attainment probabilities. Vendors unable to modernize monolithic codebases face growing replacement risk, especially as AI accelerates release cadences.

Go-to-market motions mirror this segmentation. Enterprise players cultivate channel alliances with global system integrators, while SME vendors master digital marketing funnels that convert trial users into paid subscribers. Competitive barriers now center on ecosystem breadth, pre-integrated HRIS connectors, collaboration plug-ins, and curated advisory networks all elevate switching costs. The emergent narrative frames OKR tools as the nucleus of wider performance-enablement stacks, a positioning that will continue to reshape the OKR software market.

Objectives And Key Results (OKR) Software Industry Leaders

Betterworks Systems Inc.

Quantive Technologies Inc.

Profit.co Inc.

Perdoo GmbH

WorkBoard Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Happy5 acquired SugarOKR to embed goal-setting inside its employee-engagement suite for Asia-Pacific clients.

- March 2025: WorkBoard announced the acquisition of Quantive, forming a combined platform that spans mid-market to large enterprise requirements.

- February 2025: Gtmhub closed a USD 120 million Series C to accelerate international expansion and AI analytics innovation.

- January 2025: Microsoft released deeper Copilot functionality inside Viva Goals, enabling AI-generated objectives based on meeting transcripts and document threads.

Global Objectives And Key Results (OKR) Software Market Report Scope

| Cloud-based |

| On-premise |

| Solutions |

| Services |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Retail and E-Commerce |

| Manufacturing |

| Healthcare |

| Education |

| Government and Public Sector |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud-based | ||

| On-premise | |||

| By Component | Solutions | ||

| Services | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Industry Vertical | IT and Telecommunications | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Retail and E-Commerce | |||

| Manufacturing | |||

| Healthcare | |||

| Education | |||

| Government and Public Sector | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected revenue for the OKR software market by 2030?

The OKR software market is projected to reach USD 2.68 billion by 2030.

Which deployment model leads adoption?

Cloud-based platforms held 65.83% share in 2024 and continue to expand faster than on-premise alternatives.

Which region shows the highest growth potential?

Asia-Pacific is forecast to register a 15.44% CAGR through 2030, outpacing all other regions.

Why are services growing faster than software licenses?

Organizations increasingly recognize that successful OKR rollouts require change-management consulting and integration services, driving services growth at a 16.44% CAGR.

Which industry vertical will grow the fastest?

Healthcare is expected to expand at a 14.99% CAGR as providers link OKRs to patient outcome initiatives and compliance reporting.

Page last updated on: