Warts Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.17 Billion |

| Market Size (2031) | USD 2.55 Billion |

| Growth Rate (2026 - 2031) | 3.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

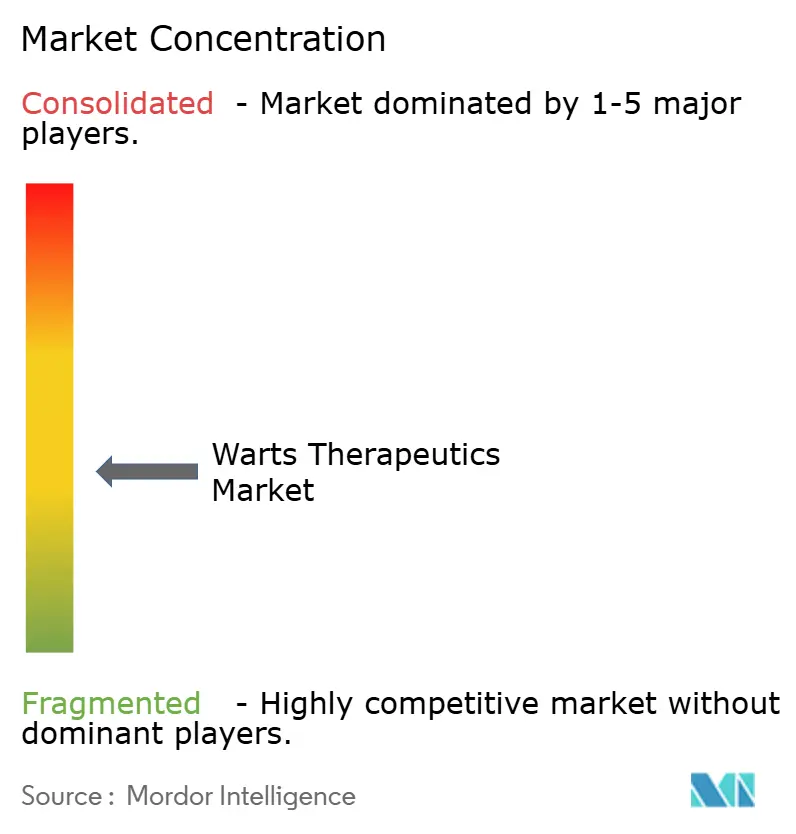

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Warts Therapeutics Market Analysis by Mordor Intelligence

The Warts Therapeutics Market size is expected to increase from USD 2.09 billion in 2025 to USD 2.17 billion in 2026 and reach USD 2.55 billion by 2031, growing at a CAGR of 3.27% over 2026-2031.

Demand rises as HPV infection remains widespread, topical keratolytics stay readily available, and newer heat-based devices demonstrate higher cure rates. Regulatory agencies support precise, minimally destructive options, and direct-to-consumer tele-dermatology platforms shorten wait times for professional care. Supply diversification away from single-country raw-material sources further stabilizes the warts therapeutics market, while continuing recurrence concerns sustain innovation momentum.[1]Hongli Ding et al., “HPV genotype distribution and cervical lesions in Chongqing,” BMC Infectious Diseases, doi.org

Key Report Takeaways

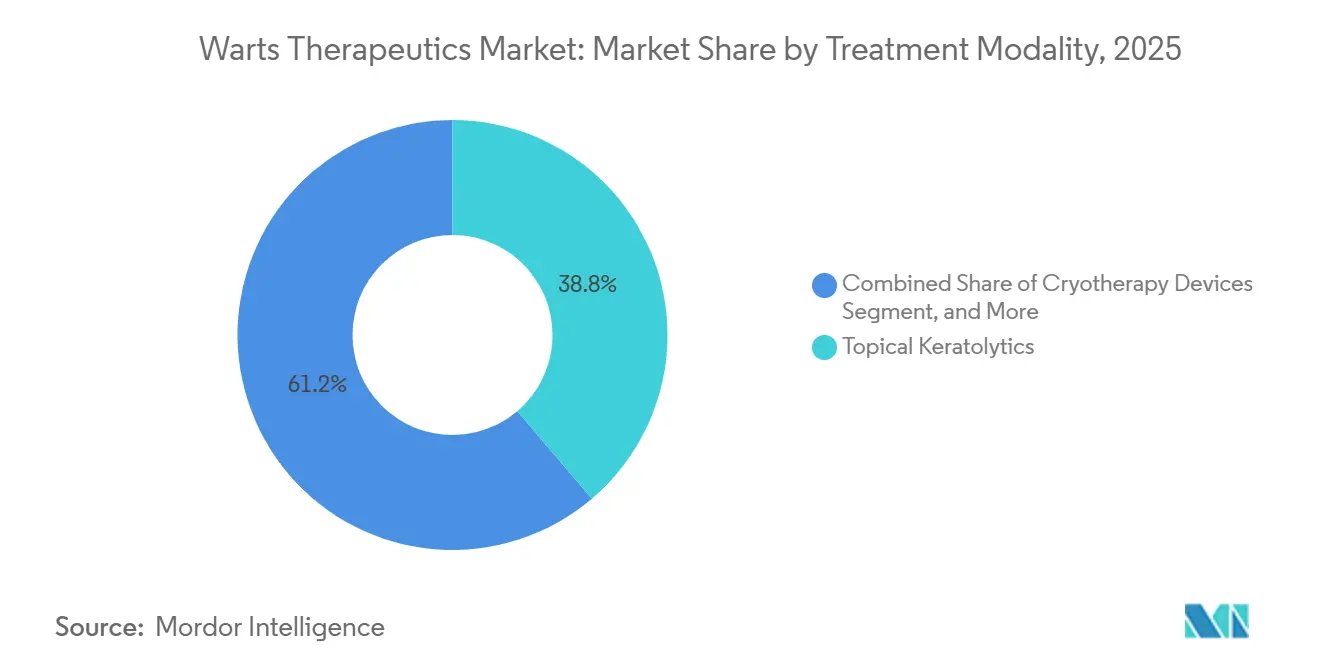

- By treatment modality, topical keratolytics led with 38.81% warts therapeutics market share in 2025. Whereas, hyperthermia and photodynamic therapy are forecast to expand at a 4.98% CAGR through 2031.

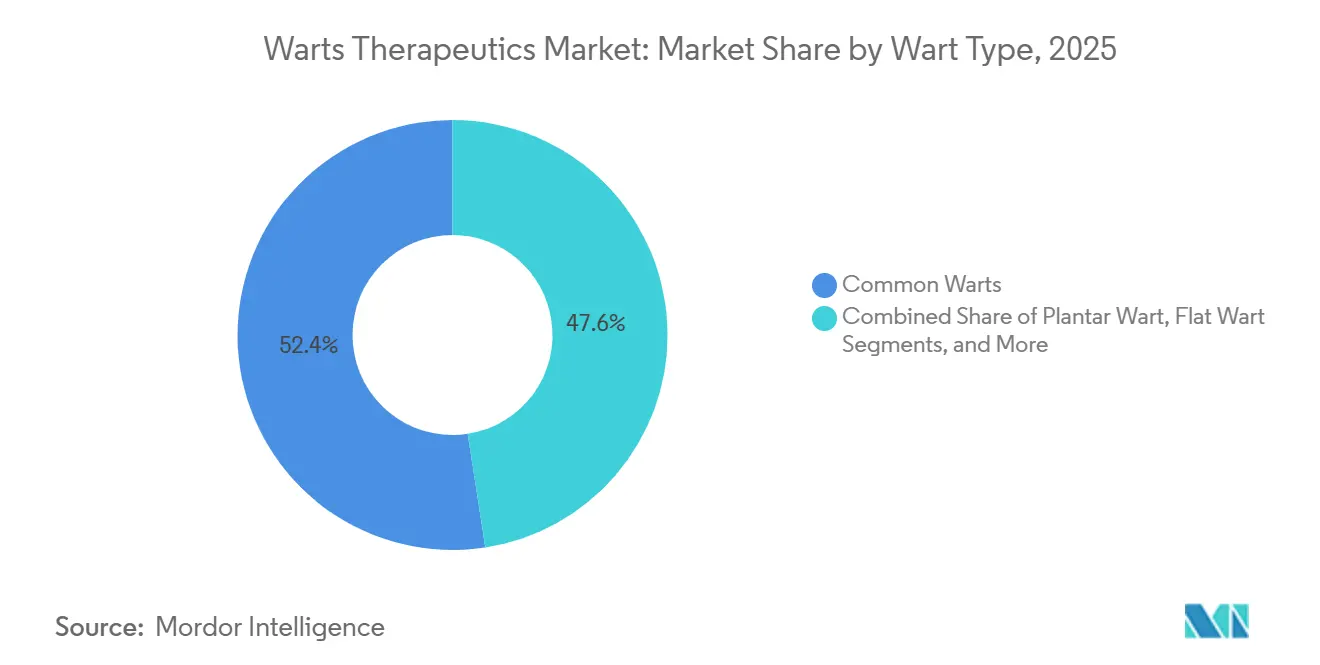

- By wart type, common warts accounted for a 52.43% share of the warts therapeutics market size in 2025. The “others” segment is projected to grow at a 3.56% CAGR to 2031.

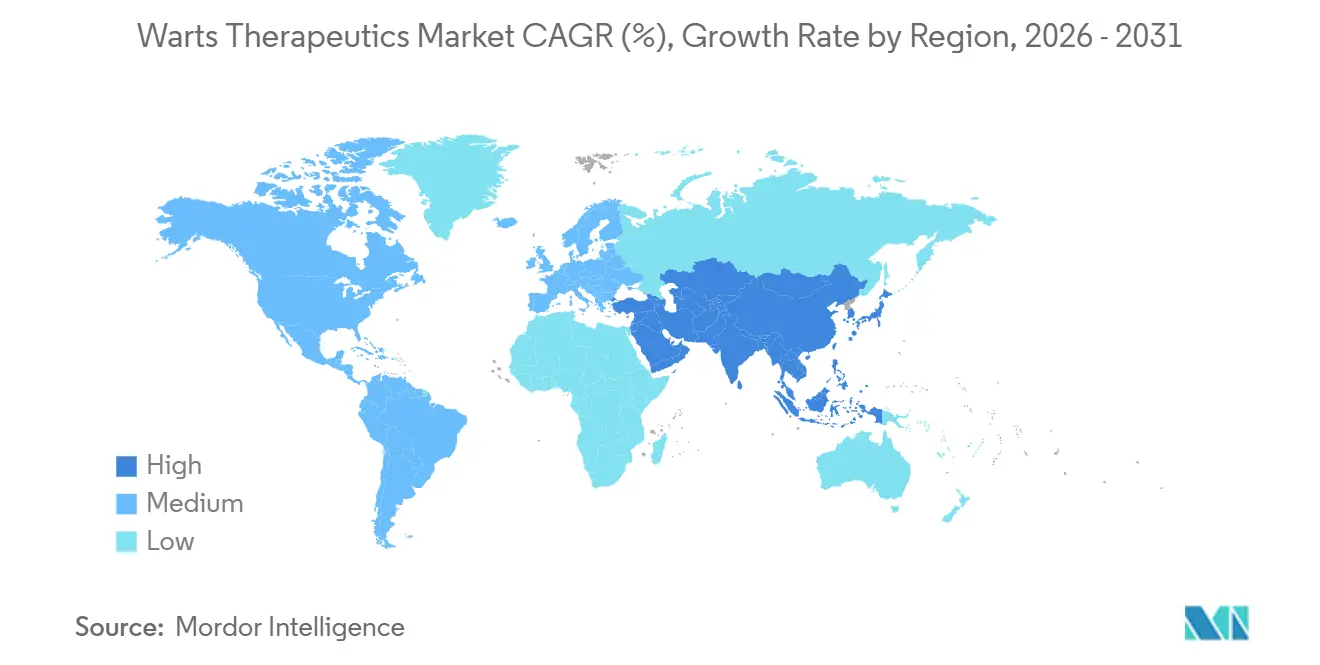

- By geography, North America held 34.65% of the warts therapeutics market in 2025, while Asia Pacific is advancing at a 5.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Warts Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance |

|---|---|---|

| Rising HPV Infection Prevalence | +1.20% | Global, with higher impact in Asia Pacific and developing regions |

| Growing OTC Availability Of Keratolytics | +0.80% | North America & EU, expanding to APAC |

| Dermatology Adoption Of Ambulatory Cryotherapy | +0.60% | North America core, spill-over to EU and APAC |

| Emergence Of Heat-Based Hyper-Thermia Devices | +0.70% | Global, early adoption in developed markets |

| Regulatory Tailwinds For Compounded Immunotherapy | +0.40% | North America, limited EU impact |

| Direct-To-Consumer Tele-Dermatology Expansion | +0.50% | Global, accelerated in APAC and rural markets |

| Source: Mordor Intelligence | ||

Rising HPV Infection Prevalence

HPV persists at 21.41% in large Chinese female cohorts and exceeds 30% in some male populations, keeping therapeutics demand steady. Peaks in people under 21 and over 61 create age-specific treatment needs that broaden the warts therapeutics market. Cutaneous beta types remain outside current vaccine coverage, so therapy rather than prevention meets immediate clinical gaps. The virus’s geographic clustering, notably HPV52 and HPV58 in the Asia Pacific, encourages the development of region-focused regimens. Expanding immunocompromised populations further entrenches recurring demand. Together, these epidemiological patterns underpin long-range market growth.

Growing OTC Availability of Keratolytics

The FDA monograph under 21 CFR Part 358 defines clear labeling for salicylic acid strengths, enabling broad retail access.[2]U.S. Food and Drug Administration, “21 CFR 358.150 — Labeling of wart remover drug products,” ecfr.gov Over-the-counter options appeal to consumers facing dermatologist wait times, and new permeation-enhanced formulations lift adherence rates. Brands balancing prescription-level efficacy with home-use safety solidify leadership in the warts therapeutics market. The self-care trend widens channels and strengthens revenue resilience against procedure-only competitors.

Dermatology Adoption of Ambulatory Cryotherapy

Brymill’s precision liquid-nitrogen applicators receive preference from 85% of US dermatologists, illustrating practitioner loyalty born from safety and consistent freeze delivery. Device miniaturization enables office-based therapeutics for multiple lesions in one visit, cutting repeat appointments. Closed-probe designs reduce collateral tissue trauma, improving patient comfort and clinician workflow. Reimbursement structures favor outpatient procedures, helping the warts therapeutics market sustain cryotherapy volumes even as new modalities appear.

Emergence of Heat-Based Hyperthermia Devices

Controlled 44–45 °C exposure generates 71% clearance, outperforming cryotherapy’s 47% in clinical head-to-heads. Hyperthermia avoids scarring, encourages immune activation, and fits pediatric compliance requirements. Systemic immune up-regulation means clinicians can treat clusters instead of each lesion individually, boosting efficiency. Early adopters differentiate their practices, pulling revenue from patients who previously cycled through less-effective options.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Recurrence & Treatment-Failure Rates | -0.90% | Global, more pronounced in immunocompromised populations | Long term (≥ 4 years) |

| Pain & Scarring From Ablative Therapies | -0.60% | Global, particularly affecting pediatric and cosmetic-conscious segments | Medium term (2-4 years) |

| Supply Bottlenecks Of Pharmaceutical-Grade Cantharidin | -0.40% | North America core, limited global impact | Short term (≤ 2 years) |

| Regulatory Scrutiny On Topical Compounding Pharmacies | -0.30% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Recurrence & Treatment-Failure Rates

Monotherapy failure ranges from 39-49%, driving retreatment cycles that erode patient confidence. Recurrence can approach 38% for cryotherapy, raising healthcare costs and prolonging discomfort.[3]Sirui Han et al., “Prevalence, trends, and geographic distribution of human papillomavirus infection in Chinese women,” BMC Medicine, doi.orgImmunocompromised individuals retain HPV reservoirs that resist conventional modalities, keeping them in perpetual therapy. These realities temper the expansion of the warts therapeutics market despite pipeline advances.

Pain & Scarring from Ablative Therapies

Pain scores above 7 on visual analog scales for bleomycin, plus scarring and post-inflammatory hyperpigmentation after aggressive freezing, deter patients. Facial and hand lesions need cosmetic preservation, so individuals often delay treatment until non-ablative options surface. Diverse skin phototypes face differing pigment outcomes, sparking calls for gentler regimens such as photodynamic therapy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Keratolytics Remain Dominant as Innovation Gains Ground

Topical keratolytics accounted for 38.81% of the warts therapeutics market share in 2025, underscoring consumer reliance on salicylic acid and similar agents. The warts therapeutics market size for keratolytics benefited from FDA-endorsed labeling that simplifies retail stocking, while smart-polymer vehicles enhance skin penetration. Cryotherapy held second position, its usage buoyed by Brymill’s leadership based on freeze-precision engineering. Although cryotherapy satisfaction remains high, tolerance varies across patients, leaving space for alternatives.

Hyperthermia and photodynamic therapy will rise at a 4.98% CAGR to 2031, the fastest among modalities. Superior 71% cure performances attract clinics seeking differentiation. Immunotherapy, such as imiquimod, shows 50% clearance for genital lesions but wrestles with cost restrictions. Energy-based modalities like pulsed dye laser achieve 95% success in select cases yet remain capital-intensive. Emerging solutions—high-intensity focused ultrasound and nitric-oxide platforms—enter the “others” bucket, targeting resistant presentations and sustaining product-launch cadence inside the warts therapeutics market.

By Wart Type: Common Forms Drive Volume While Complex Cases Spur Specialty Demand

Common warts captured 52.43% of the warts therapeutics market in 2025. Adolescents transmit the virus readily through skin-to-skin contact, ensuring steady OTC and clinic visits. Plantar lesions challenge mobility and often require multi-agent protocols; trichloroacetic acid plus silver nitrate reaches 82% resolution with lower relapse than cryotherapy alone.

The “others” group, which includes periungual, subungual, and recalcitrant manifestations, will expand at a 3.56% CAGR. Flat warts resist standard therapy and tend to spread, but local hyperthermia delivers encouraging outcomes in difficult cases. Genital warts remain a smaller portion by incidence, yet command premium professional fees given privacy and complexity. Recognition that subtype and anatomical site influence response steers R&D toward precision selections, fortifying innovation pipelines inside the warts therapeutics market.

Geography Analysis

North America retained 34.65% of the warts therapeutics market size in 2025. The region benefits from high dermatologist availability, established reimbursement for both office procedures and OTC options, and strong supply chains for liquid nitrogen and salicylic acid products. Tele-dermatology bridges rural gaps, with platforms reporting 95% treatment completion rates for image-based consultations. An aging demographic that experiences cumulative sun exposure keeps incidence elevated.

Asia Pacific will post the fastest advance at 5.44% CAGR through 2031. Local studies highlight HPV52 and HPV58 prevalence, especially in China, sustaining the need for adaptable therapeutics. National health systems invest in digital care delivery, enabling broad adoption of smartphone triage and pharmacy integration. Regional manufacturers build production capacity for cryotherapy equipment and topical agents, reducing import reliance and lowering price points.

Europe shows stable demand under harmonized regulatory oversight. Established pharmaceutical bases expedite novel formulation rollouts while strict quality standards foster clinician trust. Latin America, the Middle East, and Africa present emerging prospects: Rising urban middle classes seek cosmetic dermatology, and mobile clinics and telemedicine help overcome specialist shortages. These regions, s therefore, add incremental volume to the warts therapeutics market despite infrastructure lags.

Competitive Landscape

Fragmentation remains high as many dermatology practices operate independently, so no single provider commands a disproportionate warts therapeutics market share. Device makers compete on safety and consistency; Brymill’s flagship cryosurgical units dominate US practices owing to patented spray accuracy. Pharmaceutical companies split focus between expanding OTC penetration and channeling precision products through specialty clinics. Verrica Pharmaceuticals secured FDA approval for cantharidin, reinforcing its lead in chemovigilant therapy and defending its position through litigation that halted unapproved competitors.

Technology adoption differentiates market participants. Clinics that added hyperthermia devices market higher cure rates and reduced scarring, attracting patients dissatisfied with repeated freezing sessions. Direct-to-consumer entrants such as Hims & Hers align diagnosis, prescription, and fulfillment inside a single platform, pressuring brick-and-mortar providers to enhance patient experience. Manufacturers diversify supply chains away from single-country raw-material sources, lowering geopolitical risk and ensuring continuous drug availability.

Strategic alliances accelerate development. Organon’s acquisition of Dermavant adds VTAMA to its dermatology range, while LEO Pharma’s partnership with ICON targets faster trial execution. Financial restructuring at Cutera frees resources for energy-based innovations, and capital raises keep Verrica’s pipeline on schedule. Competitive intensity, therefore, remains lively across modalities, channels, and geographies.

Warts Therapeutics Industry Leaders

Merck & Co., Inc.

Bausch Health Companies Inc.

Verrica Pharmaceuticals Inc.

GlaxoSmithKline plc

Johnson & Johnson Consumer Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Verrica Pharmaceuticals has reached a significant milestone in its clinical pipeline. The company dosed the first patient in its global Phase 3 program evaluating YCANTH (VP-102) for the treatment of common warts.

- March 2025: LEO Pharma signed a strategic partnership with ICON to accelerate clinical trials in dermatology.

- March 2025: Organon completed the acquisition of Dermavant, adding VTAMA cream to its dermatology portfolio.

- February 2025: Verrica Pharmaceuticals raised USD 42 million to advance VP-102 into Phase 3 trials for common warts.

Global Warts Therapeutics Market Report Scope

Warts therapeutics refers to the various medical and over-the-counter (OTC) treatments designed to remove or destroy warts, which are benign skin growths caused by the human papillomavirus (HPV). Treatment goals include killing the virus, removing the wart tissue, or stimulating the body’s immune system to fight the virus.

The warts therapeutics market report is segmented by treatment modality, wart type, and geography. By treatment modality, the market is segmented into topical keratolytics, cryotherapy devices, immunotherapy agents, laser & energy-based therapies, hyperthermia & photodynamic therapies, and others. By wart type, the market is segmented into common wart, plantar wart, flat wart, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Topical Keratolytics |

| Cryotherapy Devices |

| Immunotherapy Agents |

| Laser & Energy-based Therapies |

| Hyperthermia & Photodynamic Therapies |

| Others |

| Common Wart |

| Plantar Wart |

| Flat Wart |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Modality | Topical Keratolytics | |

| Cryotherapy Devices | ||

| Immunotherapy Agents | ||

| Laser & Energy-based Therapies | ||

| Hyperthermia & Photodynamic Therapies | ||

| Others | ||

| By Wart Type | Common Wart | |

| Plantar Wart | ||

| Flat Wart | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the warts therapeutics market in 2026?

The warts therapeutics market size reached USD 2.17 billion in 2026.

What is the expected CAGR for warts therapeutics market between 2026 and 2031?

The market is forecast to expand at a 3.27% CAGR through 2030.

Which treatment modality leads revenue?

Topical keratolytics hold 38.81% warts therapeutics market share, the highest among modalities.

Which technology shows the fastest growth?

Heat-based hyperthermia and photodynamic systems are projected to rise at a 4.98% CAGR.

Which region is expanding most quickly?

Asia Pacific is anticipated to record a 5.44% CAGR, the fastest regional pace.

What factor most limits market expansion?

High recurrence and treatment-failure rates, reaching up to 49%, remain the chief restraint.

Page last updated on: