Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

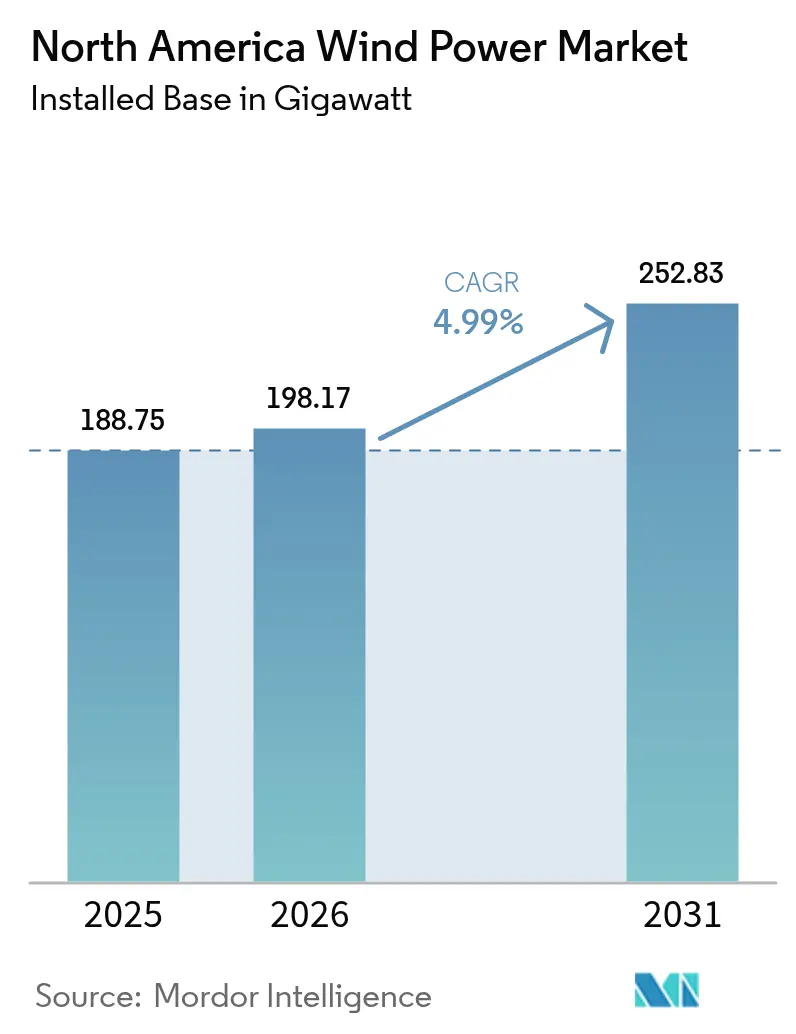

| Base Year Market Size (2025) | 188.75 gigawatt |

| Market Volume (2026) | 198.17 gigawatt |

| Market Volume (2031) | 252.83 gigawatt |

| Growth Rate (2026 - 2031) | 4.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Wind Power Market Analysis by Mordor Intelligence

The North America Wind Power Market size is expected to grow from 188.75 gigawatt in 2025 to 198.17 gigawatt in 2026 and is forecast to reach 252.83 gigawatt by 2031 at 4.99% CAGR over 2026-2031.

The market size growth reflects a decisive regional shift toward renewables, enabled by supportive tax credits, rising corporate demand for clean electricity, and turbine technology gains that now place wind among the lowest-cost generation options.[1]U.S. Department of the Treasury, “IRA Domestic Content Guidance 2024,” treasury.gov Policy tailwinds offset regulatory uncertainty, while large-scale artificial-intelligence data-center buildouts and industrial electrification programs create unprecedented appetite for long-term wind power purchase agreements. Developers continue to navigate interconnection bottlenecks, yet the pipeline remains resilient as investors favor projects that qualify for Inflation Reduction Act (IRA) bonuses and domestic-content incentives. Combined, these forces position the North America wind power market as a core pillar of the region’s decarbonization roadmap.

Key Report Takeaways

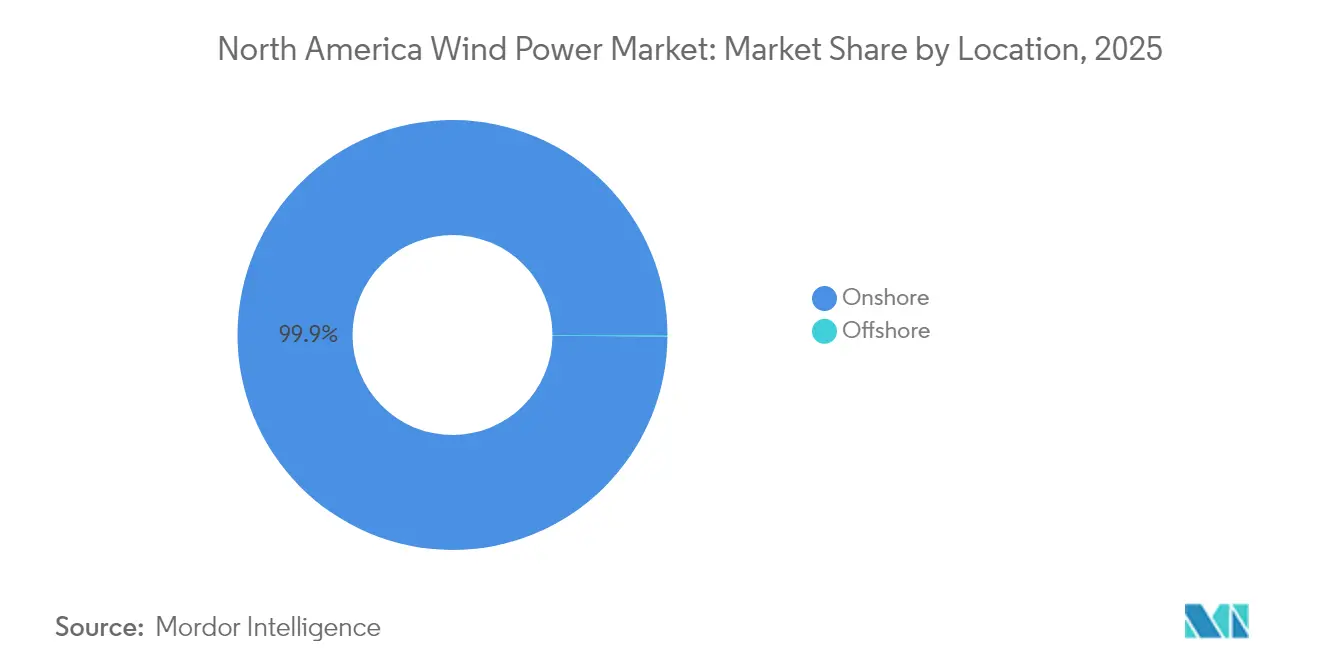

- By location, onshore installations held 99.88% of the North America wind power market share in 2025, whereas offshore capacity is projected to advance at a 47.69% CAGR to 2031.

- By turbine capacity, the 3-6 MW class commanded 53.70% share of the North America wind power market size in 2025, while above-6 MW platforms are set to expand at a 9.98% CAGR through 2031.

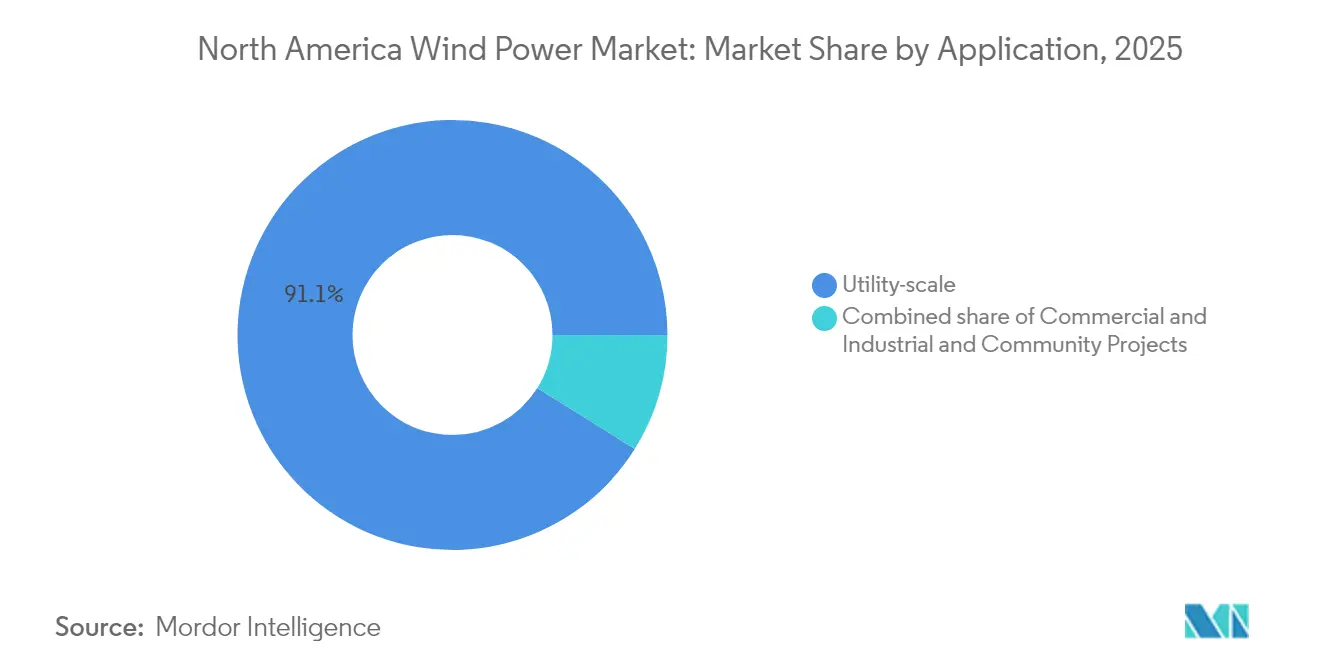

- By application, utility-scale projects accounted for 91.10% of the North America wind power market size in 2025, and commercial-and-industrial sites are growing at a 8.65% CAGR to 2031.

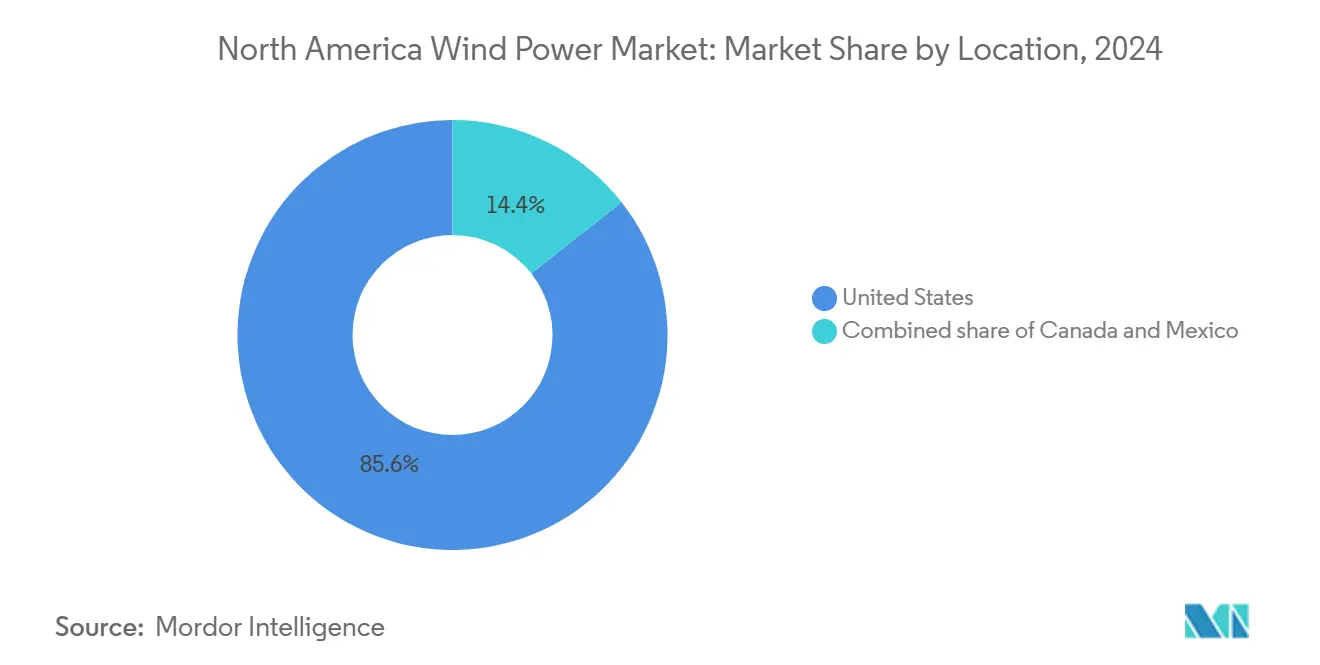

- By geography, the United States led with 85.10% of the North America wind power market share in 2025; Mexico is poised for the fastest growth at 12.95% CAGR through 2031.

- NextEra Energy, Brookfield Renewable, and Ørsted collectively controlled 18% of regional installed capacity in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Wind Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive government incentives & tax credits | +1.7% | North America-wide, strongest in US | Medium term (2-4 years) |

| Declining levelised cost of electricity (LCOE) | +1.1% | Global, with regional variations | Long term (≥ 4 years) |

| Corporate renewable-energy procurement mandates | +0.9% | US & Canada, concentrated in tech hubs | Medium term (2-4 years) |

| IRA domestic-content bonus & manufacturing build-out | +1.0% | United States primarily | Short term (≤ 2 years) |

| Surging AI/data-centre power demand driving long-term PPAs | +0.6% | US tech corridors, expanding to Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IRA Domestic-Content Bonus & Manufacturing Build-Out

Hyperscale cloud providers now procure gigawatt-scale renewables to satisfy 24/7 carbon-free energy commitments. Microsoft’s 10.5 GW global framework with Brookfield Renewable sets a blueprint for virtual PPAs that guarantee revenue visibility for developers. Data-center clusters in Texas, Virginia, and Québec align wind output with consistent load profiles when paired with storage, improving project bankability within the North America wind power market. Willingness to sign 15- to 20-year contracts supports investment-grade financing, and the trend is spreading to semiconductor fabs and green-hydrogen producers.

Surging AI/Data-Center Power Demand Driving Long-Term PPAs

Hyperscale cloud providers now procure gigawatt-scale renewables to satisfy 24/7 carbon-free energy commitments. Microsoft’s 10.5 GW global framework with Brookfield Renewable sets a blueprint for virtual PPAs that guarantee revenue visibility for developers.[2]Brookfield Renewable Partners, “Brookfield Renewable and Microsoft Announce Global Renewable Energy Framework,” brookfieldrenewable.com Data-center clusters in Texas, Virginia, and Québec align wind output with consistent load profiles when paired with storage, improving project bankability within the North America wind power market. Willingness to sign 15- to 20-year contracts supports investment-grade financing, and the trend is spreading to semiconductor fabs and green-hydrogen producers.

Corporate Renewable-Energy Procurement Mandates

Fortune 500 emissions targets have transformed renewable procurement from optional to essential. Renewable-energy-certificate prices jumped to nearly USD 8, prompting companies to pivot toward direct off-take agreements. Virtual PPAs now dominate transactions, allowing corporates to hedge electricity costs while claiming specific wind attributes. Expanded disclosure rules under the U.S. Securities and Exchange Commission intensify pressure to decarbonize scope 2 emissions, cementing wind as a primary solution within the North America wind power industry.

Declining Levelized Cost of Electricity (LCOE)

Advances in blade aerodynamics and taller hub heights have lifted capacity factors above 50% in premier wind corridors, delivering LCOEs that match or beat natural-gas combined-cycle plants.[3]Vestas Wind Systems, “Vestas Receives First US Offshore Wind Order,” vestas.com Offshore fixed-bottom projects now post 40%-plus capacity factors, and floating prototypes confirm access to deeper resource zones. Economies of scale in 6-MW-plus turbines cut balance-of-plant costs, allowing the North America wind power market to compete in merchant power markets without subsidies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transmission queue bottlenecks & curtailment risk | -1.3% | MISO, SPP, ERCOT regions | Medium term (2-4 years) |

| Commodity & rare-earth supply-chain constraints | -0.7% | Global, affecting North America | Short term (≤ 2 years) |

| DoD radar & whale-migration litigation delaying projects | -0.6% | Coastal states, military installations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Transmission Queue Bottlenecks & Curtailment Risk

More than 2,000 GW of renewables await grid studies, with MISO and SPP experiencing curtailment rates above 6% in 2024. FERC Order 1920 mandates 20-year planning horizons, yet reforms will not unblock capacity until the late 2020s. Developers must commit higher deposits earlier in the study process, straining small operators but reducing speculative filings. Cluster studies may expedite approvals, though congestion risks persist for the North America wind power market.[4]Federal Energy Regulatory Commission, “FERC Takes Long-Term Planning Historic Transmission Rule,” ferc.gov

DoD Radar & Whale-Migration Litigation Delaying Projects

Offshore leases face legal challenges linked to radar interference and marine-mammal protection. Seasonal construction pauses lengthen project schedules by 18 months or more, heightening carrying costs. The Department of Defense now collaborates with developers on radar-mitigation technologies, while environmental assessments incorporate adaptive management plans to reduce litigation exposure for the North America wind power market.[5]The White House, “Temporary Withdrawal of All Areas on the Outer Continental Shelf from Offshore Wind Leasing,” whitehouse.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Offshore Acceleration Amid Onshore Maturity

Onshore projects controlled 99.88% of installations in 2025, reflecting decades of streamlined permitting and cost-optimized supply chains across the Great Plains and Texas. Despite this dominance, offshore capacity is scaling rapidly, delivering a 47.69% CAGR to 2031 as Atlantic fixed-bottom farms reach commercial operations. Vineyard Wind and South Fork Wind showcased reliable 40%-plus capacity factors, narrowing cost gaps with onshore assets. State procurement mandates in New York and New Jersey support a 30 GW pipeline, providing visibility for vessel owners and component suppliers. Floating wind pilots in California and Nova Scotia target deeper-water zones, positioning the North America wind power market for another phase of growth beyond 2030.

By Turbine Capacity: Mid-Range Dominance with Large-Scale Migration

Turbines in the 3-6 MW range captured 53.70% of 2025 installations, balancing logistical practicality with competitive LCOE metrics. Over the forecast, developers pivot toward above-6 MW machines, which will record a 9.98% CAGR and supply both large onshore clusters and virtually all offshore plants. GE Vernova’s 2.4 GW SunZia order and Siemens Gamesa’s 21 MW prototype highlight a trajectory toward fewer, more powerful turbines that slash foundation counts and electrical-system costs. Sub-3 MW designs now serve primarily repowering niches.

By Application: Utility-Scale Dominance with C&I Emergence

Utility-scale assets represented 91.10% of capacity in 2025, supported by competitive wholesale markets and capacity-market revenues. Hybrid wind-plus-storage projects are increasingly common, enabling firm dispatch and frequency regulation services valued by system operators. The commercial-and-industrial segment, while only 8.90% today, is expanding at 8.65% CAGR as corporates execute direct PPAs and onsite installations to hedge power costs and meet science-based targets. Community wind remains limited due to zoning hurdles and distributed solar competition, but offers social-license benefits in rural areas, enhancing acceptance of the North America wind power market.

Geography Analysis

The United States accounted for 85.10% of total installations in 2025, led by Texas at more than 40 GW. Domestic-content rules spur new factories in the Midwest, shortening supply chains and qualifying projects for higher tax credits. ERCOT’s merchant market structure supports gigawatt-scale additions, although congestion in West Texas requires transmission upgrades.

Mexico, forecast to grow at a 12.95% CAGR, leverages the Isthmus of Tehuantepec’s robust wind regime and a USD 23 billion infrastructure program that features seven utility-scale wind farms. Near-shoring trends add industrial load in northern states, where developers secure long-term corporate offtake contracts. Canada’s 18 GW fleet spans Ontario, Québec, and Alberta, supported by provincial procurement schemes and Indigenous partnerships. Hydro-Québec’s 10 GW clean-energy plan and British Columbia’s fast-track permitting underline federal ambitions for a net-zero grid by 2050.

Competitive Landscape

North America’s wind sector is moderately concentrated; the five largest owners controlled roughly 48% of operating capacity in 2024. NextEra Energy leads through integrated utility and development arms, announcing plans to repower 1.9 GW of legacy assets with modern turbines. Brookfield Renewable strengthened its presence by purchasing National Grid Renewables for USD 1.7 billion, adding 3 GW operating and 24 GW pipeline assets. Ørsted accelerates U.S. offshore development with supply-chain alliances that localize foundation and cable manufacture, mitigating Jones Act compliance risks.

Turbine makers such as Vestas and GE Vernova pursue service-oriented revenue streams, offering 20-year O&M packages backed by predictive analytics that enhance fleet availability. Market participants increasingly bundle wind, solar, and storage to sell dispatchable clean-energy blocks, differentiating their bids in competitive solicitations. Consolidation is expected to continue as capital-intensive transmission upgrades favor well-capitalized developers within the North America wind power market.

North America Wind Power Industry Leaders

Orsted AS

Duke Energy Corporation

NextEra Energy Inc.

Invenergy LLC

Pattern Energy Group LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Brookfield Renewable completed its USD 1.7 billion acquisition of National Grid Renewables, adding 3,000 MW of operating renewable capacity and 24,000 MW of development pipeline to strengthen its North American platform.

- January 2025: The White House temporarily withdrew all Outer Continental Shelf areas from new offshore-wind leasing pending a review of federal permitting practices.

- December 2024: Canada enacted Clean Electricity Regulations that mandate a net-zero grid by 2050, providing a long-term demand signal for wind projects.

- September 2024: Vestas booked its first U.S. offshore wind order, an 810 MW contract for Empire Wind 1 off New York.

- July 2024: FERC issued Order 1920, instituting 20-year regional-transmission-planning requirements.

North America Wind Power Market Report Scope

Wind power is a renewable energy source that harnesses the energy of wind to generate electricity. It is usually generated using a wind turbine. Wind turbines are mechanical systems that convert kinetic energy into electrical energy. Wind power is sustainable and has a much smaller environmental impact than fossil fuels.

The North American wind power market report includes:

By Location

| Onshore |

| Offshore |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Geography

| United States |

| Canada |

| Mexico |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| By Location | Onshore |

| Offshore | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Geography | United States |

| Canada | |

| Mexico | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System |

Key Questions Answered in the Report

How much installed wind capacity does North America have in 2026?

The region is expected to reach 198.17 GW of cumulative wind capacity by the end of 2026.

What is the forecast CAGR for wind additions through 2031?

The North America wind power market is projected to grow at a 4.99% CAGR between 2026 and 2031.

Which turbine class is growing fastest?

Turbines above 6 MW will expand at about 9.98% per year as developers favor higher output machines.

Why is offshore wind important for future growth?

Offshore projects show a 47.69% CAGR to 2031, unlocking vast coastal and deep-water resources and diversifying regional supply.

How are data centers influencing demand?

Hyperscale data-center operators are signing multi-gigawatt, 15- to 20-year power purchase agreements that underpin new project financing.

Which country will post the fastest growth rate?

Mexico leads with an expected 12.95% CAGR, driven by near-shoring-related industrial electricity demand and supportive infrastructure spending.

Page last updated on: