Intracardiac Echocardiography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

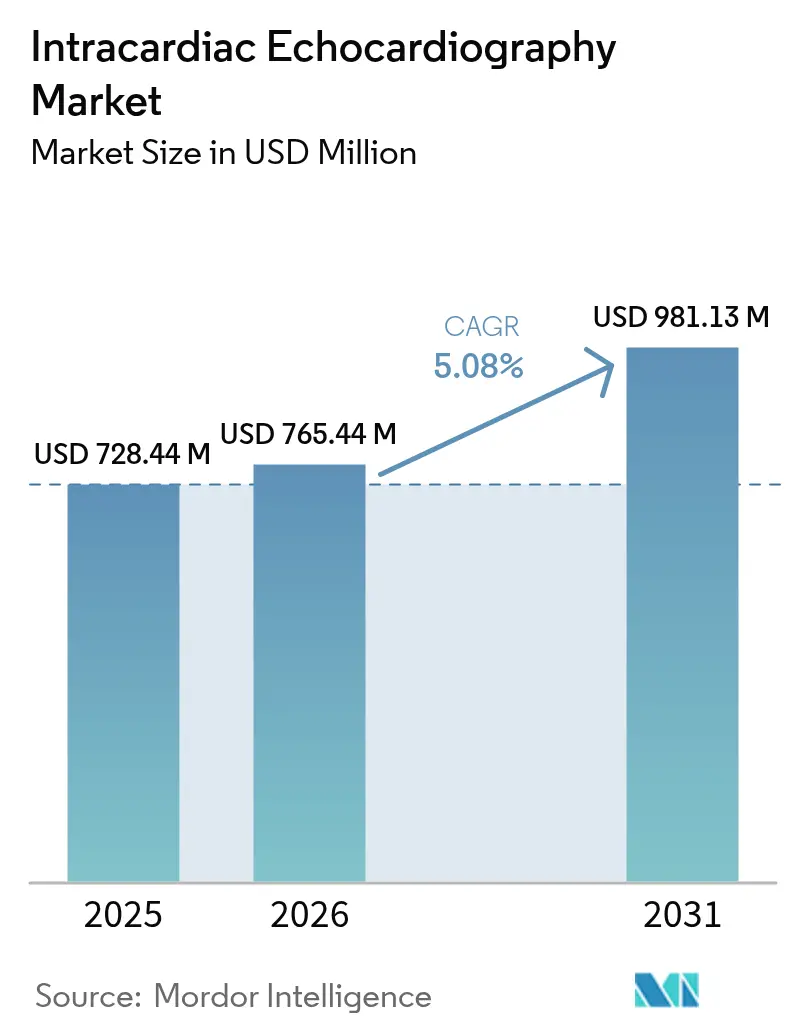

| Market Size (2026) | USD 765.44 Million |

| Market Size (2031) | USD 981.13 Million |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

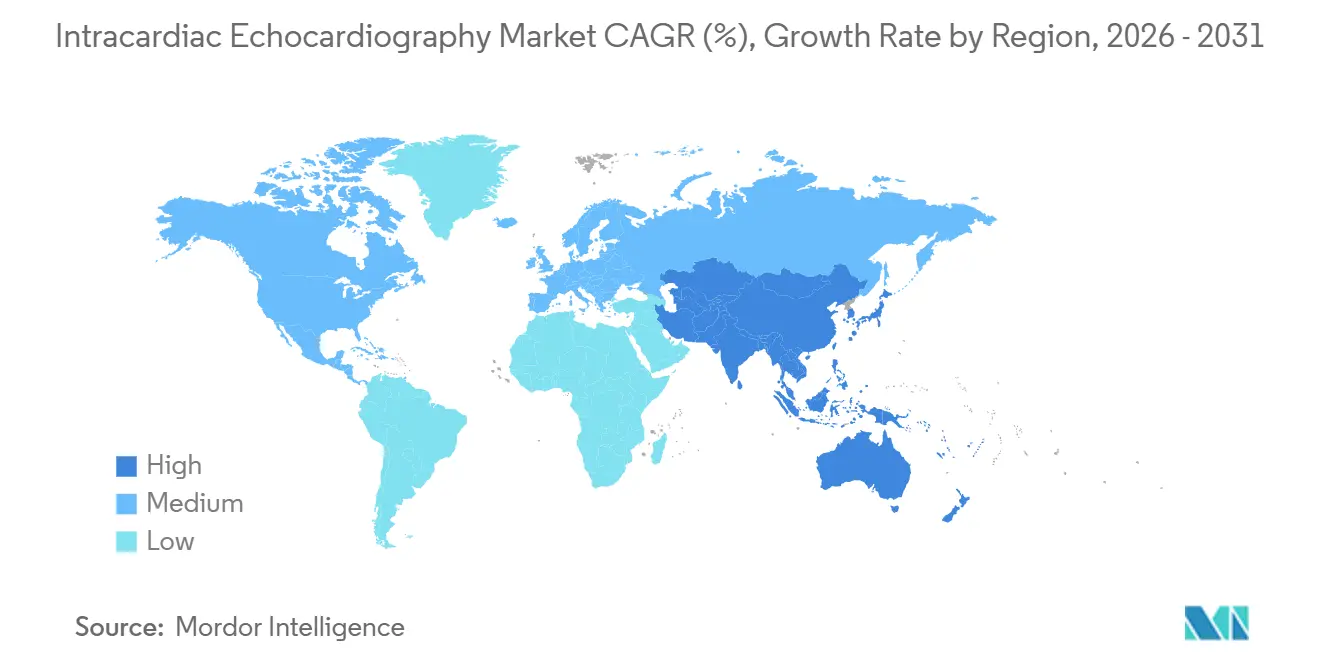

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intracardiac Echocardiography Market Analysis by Mordor Intelligence

The Intracardiac Echocardiography Market size is projected to expand from USD 728.44 million in 2025 and USD 765.44 million in 2026 to USD 981.13 million by 2031, registering a CAGR of 5.08% between 2026 to 2031.

Growth stems from rising demand for minimally invasive cardiac interventions, AI-enabled imaging workflows, and closer integration between pulsed field ablation (PFA) systems and real-time ultrasound guidance. Cost containment efforts in high-volume electrophysiology laboratories, coupled with concern over fluoroscopy radiation exposure, further elevate adoption. In parallel, reimbursement refinements in the United States and widening regulatory clearances in Europe accelerate platform expansion, while emerging Asian programs close capability gaps by leap-frogging straight to 3-D/4-D catheter solutions.

Key Report Takeaways

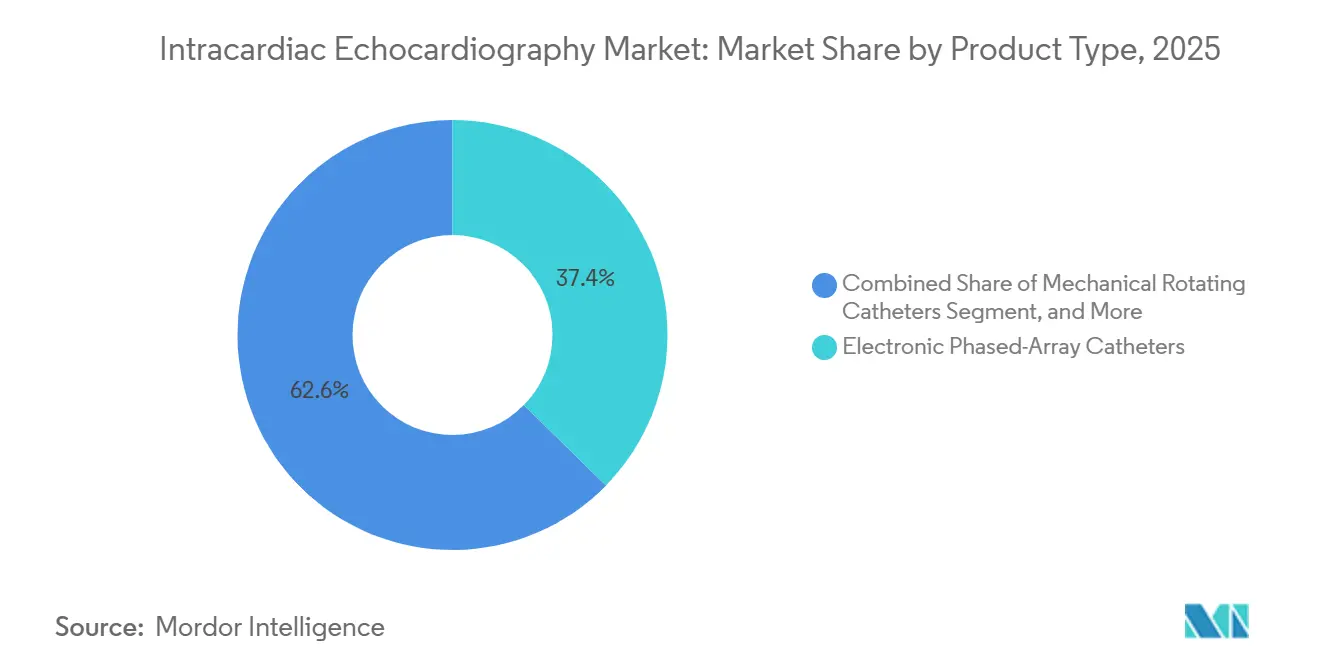

- By product type, electronic phased-array catheters led with 37.35% revenue share in 2025; 4-D volume catheters are forecast to expand at a 7.05% CAGR through 203.

- By technology, 2-D imaging accounted for 47.86% of 2025 revenue, while 4-D imaging is advancing at a 6.90% CAGR to 2031.

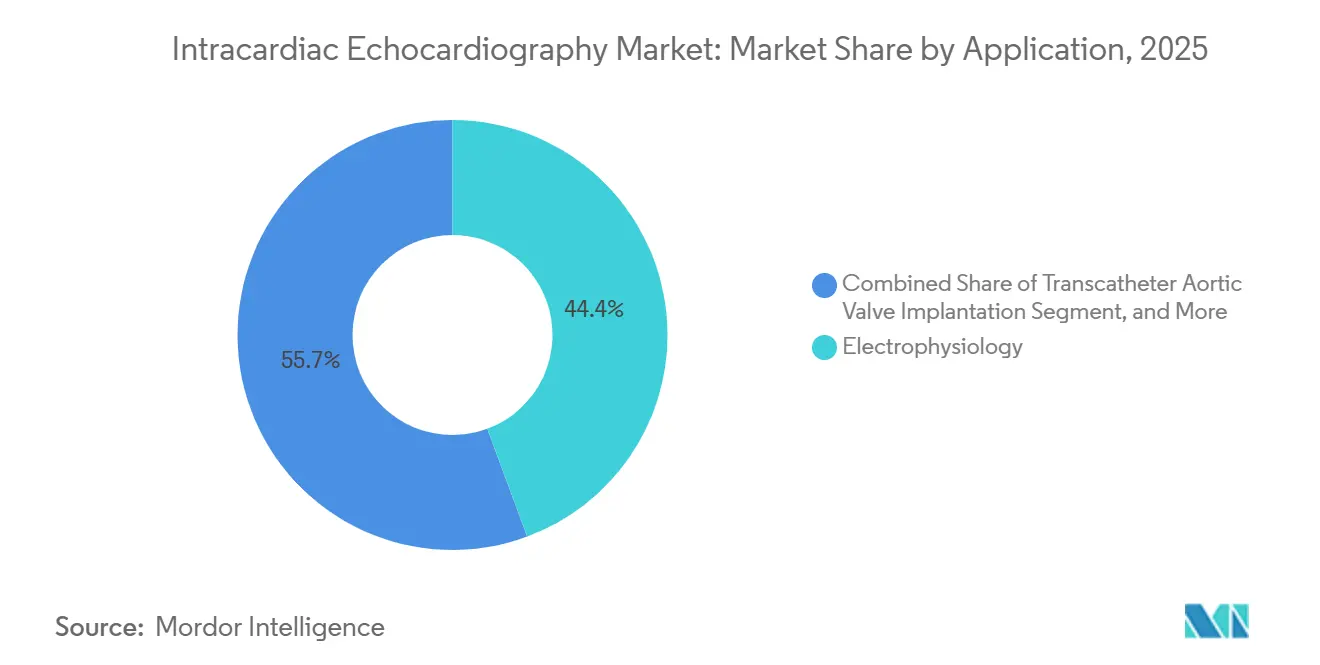

- By application, electrophysiology procedures held 44.35% of the intracardiac echocardiography market share in 2025, and transcatheter aortic valve implantation recorded the fastest growth, advancing at an 8.23% CAGR through 2031.

- By end user, hospitals captured 61.02% of the intracardiac echocardiography market in 2025, and ambulatory surgical centers delivered the highest growth rate, advancing at a 6.86% CAGR through 2031.

- By geography, North America led with a 38.96% revenue share in 2025, and Asia Pacific emerged as the fastest-growing region, posting a 7.78% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intracardiac Echocardiography Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of atrial fibrillation & structural heart disorders | +1.2% | North America, Europe | Long term (≥ 4 years) |

| Technological progress in 3-D /4-D ice catheters | +1.0% | North America, Europe, APAC | Medium term (2-4 years) |

| Shift toward minimally invasive, radiation-sparing workflows | +0.9% | Global | Medium term (2-4 years) |

| Favorable reimbursement in key developed markets | +0.8% | United States, Germany, Japan | Short term (≤ 2 years) |

| Integration with pulsed-field ablation platforms | +0.7% | North America, Europe | Medium term (2-4 years) |

| ASC single-operator cost models accelerating adoption | +0.5% | United States, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Atrial Fibrillation & Structural Heart Disorders

In 2024, 6.7 million adults in the U.S. were diagnosed with atrial fibrillation, a figure expected to exceed 8 million by 2030.[1]Centers for Disease Control and Prevention, “Atrial Fibrillation Prevalence and Projections,” cdc.gov This surge amplifies the demand for ablation procedures, which utilize ICE for transseptal guidance and lesion visualization. Structural heart diseases, like aortic stenosis and mitral regurgitation, currently impact 2.5% of adults over 75. With this age group projected to expand by 30% in Europe and Japan by 2030, the implications are significant. Electrophysiology labs, once content with a single catheter per case, have upgraded to stocking 4-D units for structural work, effectively doubling their annual ICE expenditure per site.[2]Boston Scientific, “Baylis Medical Acquisition Rationale,” bostonscientific.com As reimbursement frameworks evolve and interventional cardiology training extends into tier-2 cities, emerging markets such as India and Brazil offer untapped potential. The result? A steady baseline demand propelling the intracardiac echocardiography market on a consistent growth path, even amidst fluctuating capital budgets.

Technological Progress in 3-D / 4-D ICE Catheters

Siemens Healthineers’ AcuNav Lumos 4-D catheter, cleared by the FDA in August 2024, delivers volumetric views plus AI-based chamber recognition that lighten operator workload.[3]World Health Organization, “Cardiovascular Diseases: Structural Heart Disease Burden,” who.int Multiplanar reconstruction and biplane modalities help operators locate transseptal targets swiftly, limiting fluoroscopy time. Philips followed with the VeriSight Pro launch in Europe during May 2025, underscoring a competitive pivot toward contrast-free workflows. These advances elevate image fidelity, shrink dose exposure, and preserve renal function attributes that appeal to hospital value-analysis committees weighing capital requests. As 4-D catheters enter mainstream procurement schedules, the intracardiac echocardiography market is expected to see a steady upgrade cycle.

Shift Toward Minimally-Invasive, Radiation-Sparing Workflows

FDA approval of Edwards Lifesciences’ EVOQUE tricuspid system in February 2024 exemplifies the trend toward catheter-delivered valve repair that hinges on continuous ultrasound guidance. ICE offers real-time leaflet visualization, enabling immediate confirmation of seal integrity and mitigating paravalvular leak risk. Published registries show procedural success comparable to surgery, yet with shorter stays, prompting health-system CFOs to endorse program expansion. The same visualization benefit extends to left atrial appendage closure and mitral repair, each of which generates incremental console utilization. As case complexity rises, ICE becomes the default imaging backbone rather than an optional adjunct.

Favorable Reimbursement in Key Developed Markets

In the U.S., reimbursement for Intracardiac Echocardiography (ICE) devices is managed by CMS (Centers for Medicare & Medicaid Services) through designated CPT add-on codes. The primary code, CPT +93662, pertains to ICE conducted during therapeutic or diagnostic cardiac interventions, encompassing both imaging supervision and interpretation. This code is billed alongside the main procedure code, such as an ablation, an EP study, or a structural heart intervention. Notably, add-on codes such as +93662 qualify for separate payment and are exempt from the Physician Multiple Payment Reduction Rule. Furthermore, CMS mandates that facilities in certain states adhere to accreditation and credentialing benchmarks, ensuring compliance before claim approvals. With favorable reimbursement rates, hospitals are swiftly transitioning to premium 4-D catheters, thereby diversifying their revenue streams in the intracardiac echocardiography market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High disposable catheter cost & inconsistent reimbursement | –0.8% | Latin America, Middle East, Eastern Europe | Long term (≥ 4 years) |

| Steep learning curve & limited training programs | –0.6% | Asia-Pacific emerging markets, Africa | Medium term (2-4 years) |

| Low clinical awareness in developing nations | –0.4% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Geopolitical-driven supply-chain price volatility | –0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Disposable Catheter Cost & Inconsistent Reimbursement

ICE catheters priced between USD 2,000 and USD 4,000 incur significant overhead, yet Medicare’s CPT 93662 payment varies by region and is under periodic review. In emerging economies, self-pay rates are dominant, making additional disposable income unaffordable for district hospitals. The discrepancy widens in ambulatory surgical centers, which still lack a dedicated ASC code for intracardiac ultrasound-guided ablation. Without aligned payer policies, care teams face budgetary constraints, prompting the use of alternative imaging or transesophageal echocardiography despite sedation drawbacks. These gaps collectively temper the diffusion of the intracardiac echocardiography market in cost-sensitive geographies.

Steep Learning Curve & Limited Training Programs

Studies show operators require 18–20 supervised cases to reach reliable image acquisition benchmarks, a hurdle for centers performing fewer than five ablations weekly. Unlike diagnostic echo, ICE demands simultaneous catheter manipulation and image interpretation. Tailored curricula remain scarce, particularly outside flagship U.S. and European institutions. Low-volume labs therefore postpone procurement or underutilize consoles, curbing the technology’s installed-base productivity. Professional bodies are now drafting competency frameworks, yet widespread adoption hinges on digital simulators and remote-proctoring platforms that can scale instruction efficiently.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: 4-D Volume Catheters Gain Share Despite Phased-Array Dominance

In 2025, electronic phased-array catheters are projected to generate 37.35% of the market's revenue. Priced between USD 800 and 1,200, these catheters seamlessly integrate with legacy CARTO and EnSite consoles, making them an appealing choice for budget-conscious labs. Meanwhile, mechanical rotating catheters, once favored for their 360-degree view, are losing ground due to their slower frame rates. The market for 4-D intracardiac echocardiography catheters is set to expand at a 7.05% CAGR, driven by their ability to provide real-time volumetric views. These views can shorten TAVR procedures by up to 18 minutes and lower the risk of paravalvular leaks. Additionally, AI-enhanced consoles promptly identify pericardial effusion, bolstering the confidence of structural-heart teams.

While phased arrays will continue to dominate high-volume electrophysiology centers, premium 4-D systems, despite being sold at one-third the volume, offer significantly higher profit margins. Consequently, manufacturers are diversifying their portfolios: they offer value-priced phased arrays for standard ablation procedures, while positioning high-spec 4-D catheters as cost-saving alternatives to traditional anesthesia methods like TEE. With the spread of reimbursement uplifts, the intracardiac echocardiography market is poised for a pivotal shift. It's anticipated that 4-D units will soon dominate revenue generation, even as phased arrays maintain their share in the installed base.

By Technology: 2-D Imaging Retains Majority Share as 4-D Adoption Accelerates

In 2025, 2-D imaging accounted for 47.86% of revenue, primarily because cross-sectional views meet the needs of most atrial fibrillation ablations. Additionally, transducer costs for 2-D models are 40% lower than their 4-D counterparts. However, as hospitals increasingly prioritize precision for structural cases, the market share of 2-D in intracardiac echocardiography is set to decline.

Real-time 4-D imaging is transitioning from a luxury to a necessity, especially for valve and appendage procedures, with a projected CAGR of 6.90% through 2031. When fused with mapping systems, 4-D imaging evolves from a mere navigation tool to a critical safety feature, justifying its 2–3× price premium. Furthermore, AI modules in modern consoles enhance efficiency by auto-segmenting chambers and providing proximity alerts, resulting in a 15% reduction in procedure time and fewer complications. In markets with favorable reimbursement policies, there's a trend toward bypassing 3-D upgrades altogether and opting for 4-D. This shift is poised to accelerate the technology refresh cycle in the broader intracardiac echocardiography landscape.

By Application: TAVR Leads Growth as Electrophysiology Anchors Volume

Electrophysiology commanded 44.35% of the intracardiac echocardiography market share in 2025, anchored by atrial-fibrillation ablation workflows where septal puncture accuracy shapes outcomes. Contemporary centers target zero-fluoroscopy protocols, and ICE provides the anatomical roadmap necessary to achieve that benchmark. Left atrial appendage closure programs capitalize on catheter-based ultrasound to avoid general anesthesia and shorten discharge times, appealing to bundled-payment frameworks. Structural heart teams planning transcatheter aortic valve implantation rely on volumetric views to position prostheses, with the segment expanding at 8.23% CAGR through 2031. Device innovators are embedding ultrasound transducers into delivery sheaths, foreshadowing hybrid tools that may further enlarge the intracardiac echocardiography market.

By End User: Hospitals Dominate as ASCs Capture Incremental Growth

Hospitals retained 61.02% of the intracardiac echocardiography market size in 2025 thanks to integrated electrophysiology suites, full-time anesthesia coverage, and direct purchasing power. Academic centers double as training hubs, amplifying procedure counts and validating novel software modules. Yet the ambulatory surgical center channel is ascending, posting a 6.86% CAGR as private-equity sponsors aggregate single-specialty cardiology practices under one-room ASC footprints. Efficiency models prioritize single-operator workflows, and ICE answers that need by removing dependence on transesophageal echo technicians. Early movers have demonstrated same-day discharge for complex ablations without compromising quality metrics, a proof point that emboldens payers to pilot bundled ASC reimbursement.

Geography Analysis

North America led the intracardiac echocardiography market with 38.96% of global revenue in 2025. U.S. academic hubs operate mature ablation programs and produce most peer-reviewed evidence that underpins FDA approvals, while Canada’s provincial health authorities now reimburse ICE-guided left-atrial appendage closure to curb stroke-related costs. Mexico shows rising procedure counts at private hospitals catering to medical tourists seeking fixed-price ablation packages.

Asia Pacific posted the fastest trajectory at an 7.78% CAGR and is on course to rival European volumes by 2031. China’s national volume-based procurement scheme has added ICE catheters to its device catalog, accelerating penetration in tertiary hospitals. Japan’s super-aged demographic fuels structural heart interventions, and local manufacturers partner with global firms to co-develop imaging algorithms tuned to small stature anatomy. Korea and Australia maintain stable replacement demand as installed consoles approach refresh cycles.

Europe remains a methodical adopter, guided by cost-effectiveness appraisals led by agencies such as NICE. Germany is the region’s largest buyer, with sickness funds funding ICE for PFA procedures after publication of real-world registries showing reduced hospital stay. France, Italy, and Spain channel EU recovery funds into cath-lab modernization, including radiation-saving imaging. Post-Brexit, the United Kingdom continues to honor many CE marks but is moving toward its UKCA regimen, potentially adding dual-testing costs that vendors must factor into pricing.

Regulatory Landscape

In the United States, intracardiac echocardiography (ICE) catheters are commonly regulated as Class II cardiovascular diagnostic devices under 21 CFR 870.1200 (product code OBJ), with market access typically achieved via the FDA 510(k) pathway. Clearances for iterative design updates focus on bench and engineering performance and conformance to widely used standards such as ISO 10993 (biocompatibility) and IEC 60601-1/60601-1-2 (electrical safety and EMC), establishing a familiar compliance baseline for global vendors.

In Europe, ICE catheter commercialization is governed by the EU Medical Device Regulation, Regulation (EU) 2017/745 (MDR), which has been in force since May 2021 and continues through transition steps into 2026. This framework reinforces notified-body conformity assessment and post-market requirements. Recent regulatory activity includes Philips receiving FDA 510(k) clearance in May 2025 (K251103) for updated VeriSight/VeriSight Pro ICE catheter models, reflecting the pace of incremental clearances that support product-line refresh cycles in this market.

Competitive Landscape

The intracardiac echocardiography market features a mix of diversified conglomerates and focused imaging specialists. Abbott, Boston Scientific, and Siemens Healthineers anchor the oligopoly, leveraging integrated electrophysiology or cardiovascular portfolios to bundle pricing across echo, mapping, and ablation. Each invests heavily in AI modules that auto-segment cardiac structures, exemplified by Siemens’ AI-powered AcuNav tools that flag optimal viewing windows. Johnson & Johnson pursues horizontal consolidation, illustrated by its USD 13.1 billion Shockwave Medical acquisition that broadens its structural-heart suite.

Disruptors such as iCardio.ai secure FDA clearances for catheter-agnostic echo analytics, aiming to license software across incumbent hardware. Start-ups working on transformer-based catheter pose-tracking promise sensor-less navigation with 9.48 mm precision, compatible with existing consoles. Strategic collaboration remains high; Boston Scientific and Philips signed a co-marketing pact to synchronize FARAPULSE PFA images with VeriSight Pro ultrasound, ensuring seamless workstation ergonomics. Intellectual-property portfolios around catheter tip steering and single-use transducer arrays form key defensive moats, raising entry barriers for new rivals.

Supply-chain resilience is another differentiator. Multinationals shifted catheter molding from China to dual-site facilities in Mexico and Malaysia to hedge geopolitical risk. Component standardization across 2-D and 4-D product lines lowers inventory burden and expedites field replacements. Finally, vendor-supported remote-proctoring platforms accelerate customer onboarding, a critical lever in shrinking the learning curve constraint that restrains intracardiac echocardiography market growth.

Intracardiac Echocardiography Industry Leaders

Boston Scientific Corporation

Stryker Corporation

Conavi Medical

Koninklijke Philips N.V.

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space centers on scaling ICE beyond core electrophysiology into structural heart programs and care settings where avoiding general anesthesia creates operational value. The shift is supported by published clinical comparisons in atrial fibrillation ablation that report ICE as noninferior to transesophageal echocardiography (TEE) for thromboembolic prevention, alongside lower major bleeding (0.2% vs 1.2%) and reduced fluoroscopy time, which aligns with hospital initiatives to cut radiation exposure and anesthesia utilization.

Technology-led opportunities tie to broader deployment of 3-D/4-D catheters and deeper workflow integration with mapping platforms used in complex ablation. The FDA 510(k) clearance for Philips VeriSight and VeriSight Pro in May 2025 (K251103), including an added pediatric indication, expands addressable procedures and patient cohorts for centers that standardize on a single ICE platform. Work described in 2026 literature on integrating 4D ICE with intracardiac mapping and navigation workflows also points to a practical route for consolidating console utilization across electrophysiology and structural heart, supporting demand for AI-assisted navigation and catheter-agnostic analytics software that reduces the learning curve.

Recent Industry Developments

- June 2026: Conavi Medical reported receiving a CAD 1.25 million milestone payment from Ontario's Life Sciences Scale-Up Fund following its FDA 510(k) clearance. The funding is intended to support execution around an approved imaging platform and strengthens the companys ability to invest in commercialization activities relevant to catheter-based imaging workflows used in interventional cardiology.

- November 2025: Boston Scientific and Siemens Healthineers announced a strategic partnership to develop and commercialize Siemens Healthineers next-generation AcuNav 4D intracardiac echocardiography catheter, with Boston Scientific as the exclusive distributor in the U.S. and Japan. The collaboration links ICE catheter innovation to large installed bases in electrophysiology and structural heart, adding competitive pressure on other vendors to match integrated procedural workflows.

- May 2024: Philips expanded access to its 3D intracardiac echocardiography technology to Hong Kong. This extended availability of advanced ICE capability in Asia-Pacific and supported procedure growth in minimally invasive cardiac interventions that rely on real-time intracardiac imaging.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from intracardiac echocardiography used inside the heart during interventional procedures, including ICE catheters and the related imaging console and software needed to run and interpret images across care settings.

Scope exclusions: We exclude external echocardiography systems, general ultrasound consoles not used for ICE, and procedure revenues that are not directly tied to ICE device and software sales.

Segmentation Overview

- By Product Type

- Electronic Phased-Array Catheters

- Mechanical Rotating Catheters

- 4-D Volume Catheters

- AI-Integrated Consoles & Software

- By Technology

- 2-D Imaging

- 3-D Imaging

- 4-D Imaging

- AI-assisted Navigation

- By Application

- Electrophysiology

- Left Atrial Appendage Closure

- Transcatheter Aortic Valve Implantation

- MitraClip & Mitral Valvuloplasty

- Congenital Heart Disease Interventions

- Other structural heart procedures

- By End User

- Hospitals

- Cardiac catheterisation laboratories

- Ambulatory surgical centres

- Diagnostic imaging centres

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where ICE is used and how demand is created, then matching those use cases to what can be observed in public data. We referenced sources such as the US FDA device databases, the US Centers for Medicare and Medicaid Services for procedure and payment signals, OECD health statistics for system capacity context, and clinical literature indexed in PubMed to track adoption patterns in electrophysiology and structural heart procedures.

To anchor pricing and shipment direction, we also reviewed company annual reports, investor presentations, regulatory filings, and reputable medical society and hospital education materials that describe typical use cases. For countries where public data is thinner, we supplemented with paid subscriptions for company financials and intelligence, news and financials, and patent databases to confirm product cycles and commercialization timing. The desk sources listed here are illustrative, and many other public references were also used for data collection, cross checks, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what drives ICE spending in practice, including catheter utilization per procedure, technology mix shifts (2D, 3D, and emerging 4D), and how purchasing happens across hospitals and diagnostic centers. We spoke with a mix of clinicians, cath lab and EP lab leaders, and procurement or service-line managers across major regions, so assumptions from desk research could be challenged and then tightened before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 49% |

| Mid tier: 55% | Functional/Unit leaders: 32% | EMEA: 31% |

| Smaller Players: 18% | Managers: 53% | Americas: 20% |

Market-Sizing & Forecasting

The core model is built using a top-down demand pool, where procedure volumes that commonly use intracardiac echocardiography are reconstructed by region and then converted into ICE catheter demand using penetration rates and average catheters per case. Those volumes are then valued using an ASP ladder that reflects technology mix and purchasing patterns, and the totals are checked against selective bottom-up views like sampled catheter shipments, distributor channel checks, and supplier revenue splits where they are observable.

A few inputs that matter in this market include electrophysiology ablation volumes, structural heart intervention growth (such as left atrial appendage closure and transcatheter valve procedures), imaging modality mix shifts between 2D and 3D, replacement cycles for consoles and software, and hospital budget pressure that can affect purchasing timing. When country-level procedure reporting is missing, we fill gaps using proxy indicators like cath lab capacity, cardiology center counts, and expert-agreed adoption ranges, and then we test sensitivity so outliers do not over-pull the final total.

For forecasting, we used scenario analysis supported by a light multivariate regression view, where procedure growth, adoption curves, and price progression are projected together and then adjusted based on what experts expect for guideline momentum and technology refresh. The final forecast is kept practical, so another analyst can reproduce the steps using the same public procedure signals and clearly stated assumptions.

Data Validation & Update Cycle

Outputs are validated by triangulating the model against independent signals like procedure trends, public reimbursement movements, and observed technology adoption narratives in clinical publications. Large variances are flagged, then the assumptions are rechecked, followed by a second pass where the math and logic are reviewed before sign-off.

The report is refreshed annually, and interim updates are triggered when there is a material event such as a major regulatory approval, a notable pricing shift, or a sudden change in procedure volumes. Before delivery, we run a last validation sweep so the market size reflects the most current inputs available at that time.

Mordor Intelligence's Intracardiac Echocardiography Market Size Measured Against Other Published Estimates

Published market values for intracardiac echocardiography do not always line up, even when the topic label looks the same, because the included product set and the timing of pricing inputs can differ. The year selected for currency conversion, the way ASP is stepped up by technology mix, and how often assumptions get rechecked against procedure reality can each move the final number.

With frequent refreshes of procedure-volume assumptions and consistent currency timing for the base year, the ASP path is revalidated against 2D versus 3D mix changes and hospital purchasing patterns, which limits drift from short-term pricing noise, a discipline applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 728.44 M (2025) | |

| Industry Publisher A | USD 782.30 M (2025) | Often reflects a broader revenue scope that can bundle adjacent ultrasound components, and it may carry forward a different technology-mix uplift in ASPs, which can lift the 2025 value even if procedure volumes are similar. |

| Global Publisher B | USD 780.00 M (2025) | Can differ on what is counted as ICE-related software and console revenue, and it may lean more on forward adoption assumptions with fewer explicit cross checks to procedure mix by region. |

The spread across the three values is mainly explained by scope edges around consoles and software and by how pricing is carried through the base year. By keeping inputs traceable to procedure demand, technology mix, and a repeatable ASP build, the resulting estimate stays balanced and easier to audit when assumptions change.

Key Questions Answered in the Report

How large will the intracardiac echocardiography market be by 2031?

Forecasts place it at USD 981.13 million, underpinned by a 5.08% CAGR over 2026-2031.

Which procedure type currently dominates ICE use?

Electrophysiology ablations hold 44.35% share owing to the need for real-time septal and pulmonary vein visualization.

Why are ambulatory surgical centers gaining relevance?

ASC models post the fastest 6.86% CAGR because single-operator ICE workflows reduce staff costs and enable same-day discharge.

What drives Asia Pacific’s rapid growth?

Expanding healthcare access, supportive government policies, and an aging demographic deliver an 7.78% regional CAGR through 2031.

How do 4-D catheters improve outcomes?

They supply volumetric, contrast-free images that cut fluoroscopy exposure and speed device positioning in structural heart cases.

What is the main barrier to wider ICE adoption?

High disposable catheter costs paired with inconsistent reimbursement remain the most cited limitation, especially in emerging markets.

Page last updated on: