Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.15 Billion |

| Market Size (2026) | USD 14.67 Billion |

| Market Size (2031) | USD 17.56 Billion |

| Growth Rate (2026 - 2031) | 3.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Surfactants Market Analysis by Mordor Intelligence

The North America surfactants market size in 2026 is estimated at USD 14.67 billion, growing from 2025 value of USD 14.15 billion with 2031 projections showing USD 17.56 billion, growing at 3.67% CAGR over 2026-2031. Growth stems from tightening U.S. and Canadian volatile-organic-compound rules, Mexico’s near-shoring–driven feedstock expansion, and formulators’ shift to bio-based grades that earn EPA Safer Choice and USDA BioPreferred labels. Non-ionic alcohol ethoxylates dominate high-efficacy household formats, while alpha-olefin sulfonates are enjoying renewed investment in concentrated laundry liquids. Enhanced-oil-recovery (EOR) projects in the Permian Basin now specify alkyl-propoxy-sulfate systems, which fetch premium pricing, partially offsetting slower growth in the personal-care sector. Supply security remains volatile because 20–30% quarter-to-quarter ethylene-oxide price swings compress margins for contract manufacturers lacking pass-through clauses.

Key Report Takeaways

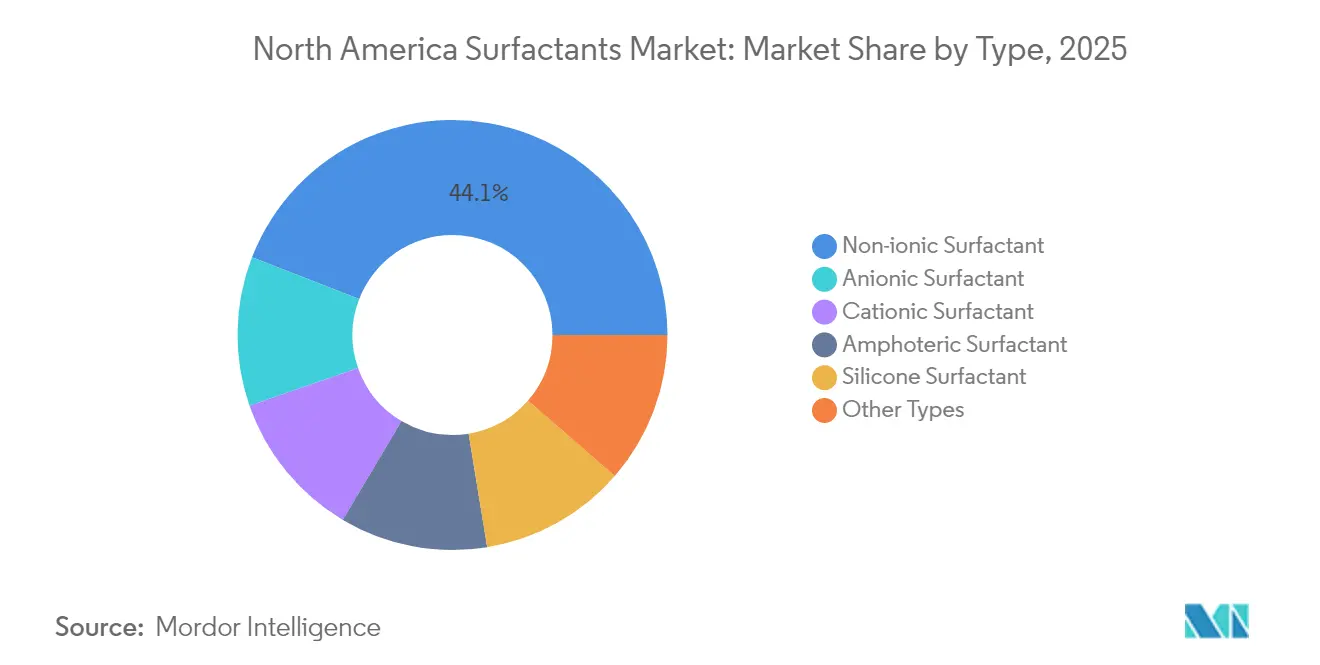

- By type, non-ionic surfactants accounted for 44.12% of the North America surfactants market share in 2025, while anionics led innovation pipelines with alpha-olefin-sulfonate debottlenecking.

- By origin, synthetics accounted for 76.05% of 2025 revenue; bio-based grades recorded the fastest growth rate of 3.92% through 2031.

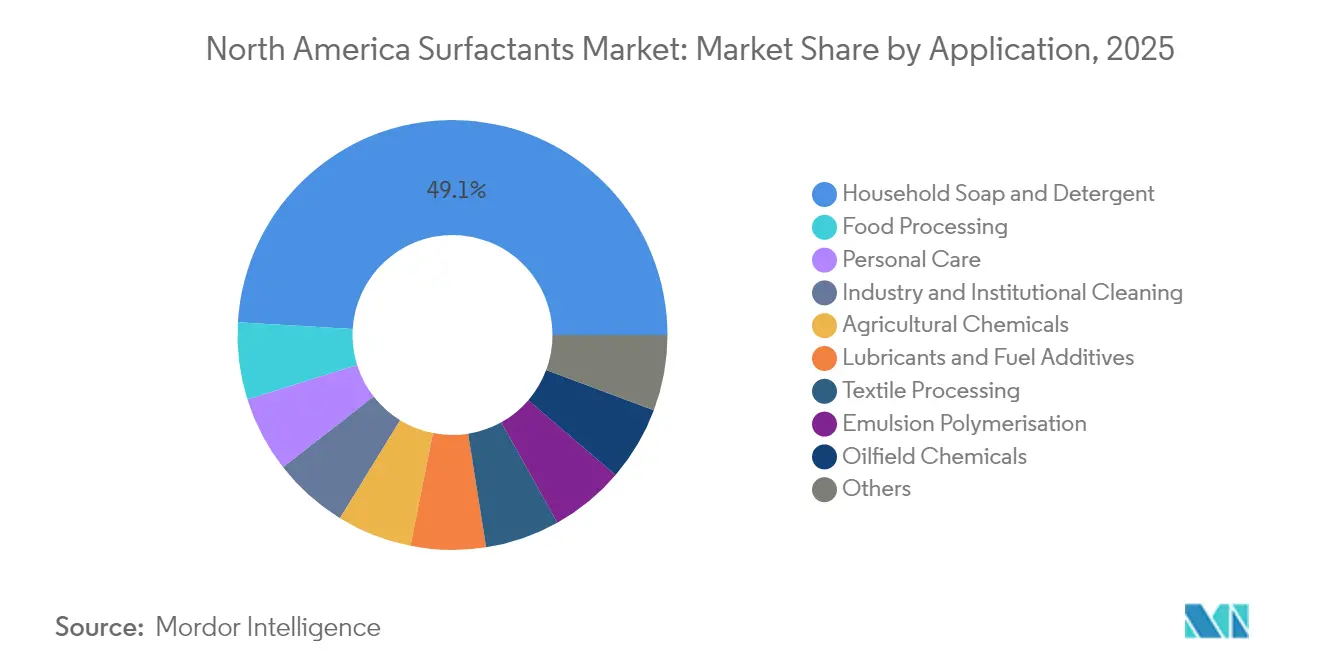

- By application, household soap and detergent accounted for 49.05% of volume in 2025; food processing is projected to register a 5.12% CAGR to 2031.

- By geography, the United States accounted for 78.70% of the 2025 value; Mexico represents the fastest-growing country at a 3.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Surfactants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating shift to bio-surfactants in home and personal-care formulations | + 0.9% | United States, Canada (EPA/CEPA compliance zones) | Medium term (2-4 years) |

| Growth of I&I and institutional cleaning post-COVID | + 0.7% | United States, Canada (commercial facilities, healthcare) | Short term (≤ 2 years) |

| Tightening U.S./Canadian VOC and toxicity regulations | + 0.8% | United States, Canada (federal and state-level enforcement) | Medium term (2-4 years) |

| Rising demand for high-performance surfactants in enhanced oil recovery | + 0.5% | United States (Permian Basin, Eagle Ford, Bakken) | Long term (≥ 4 years) |

| Commercialization of carbon-capture-derived feedstocks | + 0.4% | United States (Gulf Coast industrial corridors) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift to Bio-Surfactants in Home and Personal-Care Formulations

Brand owners embed minimum bio-content thresholds in supplier scorecards, shrinking the historic cost gap between petro-derived and renewable systems. Evonik commissioned a bio-succinic-acid line to service alkyl-polyglucoside demand, while Croda’s Atlas Point site rolled out 100% bio-based alcohol ethoxylates to secure USDA BioPreferred seals. California and New York bans on nonylphenol ethoxylates advance the transition as formulators pre-empt future restrictions. EPA’s August 2024 Safer Choice update allocates extra points for non-food-crop feedstocks such as camelina, guiding purchasing away from palm kernel[1]U.S. Environmental Protection Agency, “Safer Choice Standard,” epa.gov. Collectively, these measures accelerate the North America Surfactants market’s pivot to renewable inputs without compromising detergency targets.

Growth of I&I and Institutional Cleaning Post-COVID

Hospitals, restaurants, and office buildings locked higher cleaning frequencies into standard operating procedures after the pandemic, permanently lifting surfactant demand in sanitizers and floor cleaners. State rules that discourage quaternary ammonium compounds steer buyers toward anionic–nonionic blends that rinse cleanly and pose fewer residue concerns. Pilot Chemical and Innospec win share by offering pre-diluted concentrates that cut shipping weight and satisfy sustainability targets. Office occupancy stabilized in 2024, restoring janitorial budgets to pre-pandemic levels and boosting institutional volumes. Together these shifts lift I&I surfactant growth above household-care averages through 2027.

Tightening U.S. and Canadian VOC and Toxicity Regulations

Canada’s November 2024 CEPA amendments aligned aquatic-toxicity thresholds with EPA benchmarks, effectively banning products that contain more than 0.1% nonylphenol ethoxylates. The May 2025 Canada Biocides Regulations also capped residual 1,4-dioxane in alcohol ethoxysulfates at 10 parts per million, forcing upgrades at plants that lack vacuum stripping. In the United States, California proposes PFAS restrictions that would bar fluorinated surfactants in firefighting foams by 2027, compressing the reformulation window for industrial cleaners. This patchwork means a formula approved in Texas can be illegal in Ontario or California, raising compliance costs and rewarding suppliers with flexible production footprints. The rising bar on toxicity and VOCs keeps regulatory agility at the forefront for every regional producer.

Rising Demand for High-Performance Surfactants in Enhanced Oil Recovery

Chevron’s Permian pilots showed that alkyl-propoxy-sulfate packages unlock 8–12% extra crude from mature wells, proving the commercial value of premium EOR surfactants. These blends must tolerate high salinity and temperature while driving down interfacial tension, requirements that exclude most commodity grades and justify price premiums of 30–50%. The U.S. Energy Information Administration expects national crude production to plateau at around 13 million barrels per day through 2030, making EOR a key lever to extend field life without new drilling. BASF and Stepan tailor sulfonate and ethoxylate ratios to each reservoir, locking in multiyear supply contracts that protect margins from spot volatility. This niche, although small in volume, delivers outsized profitability and offsets slower growth in personal care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petro-feedstock price volatility and supply shocks | -0.6% | United States, Canada, Mexico (petrochemical import-dependent regions) | Short term (≤ 2 years) |

| Aquatic-toxicity scrutiny of legacy LAS/NPE grades | -0.4% | United States, Canada (EPA/CEPA enforcement zones) | Medium term (2-4 years) |

| Limited regional capacity for specialized microbial strains | -0.3% | United States, Canada (biosurfactant fermentation hubs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petro-Feedstock Price Volatility and Supply Shocks

WTI crude oscillated between USD 70 and USD 85 per barrel through 2024, resulting in 20–30% swings in ethylene oxide spot prices that compressed producer margins. Mexican ethane diversification eases some pressure, yet Braskem Idesa’s new import terminal also feeds polymers, limiting relief for surfactants. Import-dependent Canadian formulators face dual freight and currency risk because all ethylene oxide must cross borders. Such volatility discourages long-cycle capital projects, slowing capacity additions despite steady demand growth. The result is a fragile cost base for regional toll manufacturers serving the North America surfactants market.

Aquatic-Toxicity Scrutiny of Legacy LAS and NPE Grades

Peer-reviewed studies in 2024 showed nonylphenol ethoxylates persisting in river sediments and disrupting endocrine systems at just 5 µg L⁻¹, well below many discharge limits. California banned NPEs in consumer products beginning January 2025, prompting reformulation of laundry and dishwashing lines nationwide. Linear-alkylbenzene-sulfonates face softer but growing pressure as EPA aquatic benchmarks set a chronic limit of 35 µg L⁻¹ for freshwater invertebrates. Formulators migrate toward methyl-ester-sulfonates and alcohol-ethoxysulfates, which degrade faster and lack the aromatic ring linked to bioaccumulation. Switching chemistry demands new esterification and sulfonation equipment, raising capital costs and complicating supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Non-Ionics Anchor Volume, Anionics Drive Innovation

Non-ionic surfactants accounted for 44.12% of the 2025 volume, driven by the utility of alcohol-ethoxylates in concentrated pods that require high detergency at low doses. The North American surfactants market size for non-ionics is forecast to rise 3.78% annually as institutional sanitizers continue to shift to low-foam blends that expedite rinse cycles. California’s nonylphenol-ethoxylate ban pushes suppliers toward fatty-acid-ester and alkyl-polyglucoside substitutes, both of which qualify for EPA Safer Choice labels. Anionic surfactants remain the workhorse: Stepan’s 25% alpha-olefin-sulfonate expansion underscores confidence that sulfonate demand in laundry and dishwashing will hold even as biosurfactants scale. Regulatory scrutiny of linear-alkylbenzene sulfonates boosts secondary-alkane and methyl-ester sulfonates, especially for products exported to Europe under the EU Detergents Regulation.

Specialty cationic quats face headwinds because proposed California disinfectant limits reduce QAC inclusion, yet uses in fabric softeners and hair conditioners preserve modest growth. Amphoterics such as betaines gain popularity in sulfate-free shampoos that require mildness and stable foam. Silicone surfactants remain a niche market, primarily focused on agrochemical adjuvants and polyurethane foams, where their unique spreading properties justify premiums. Overall, non-ionics maintain baseline volume while anionics innovate, ensuring that type-level demand within the North America Surfactants market remains broad and defensible.

By Origin: Synthetic Dominance Erodes as Bio-Based Chemistries Scale

The synthetic surfactant segment accounted for 76.05% share of the North America surfactants market in 2025. However, the bio-based cohort expands at a 3.92% CAGR, combining feedstock retrofits at Dow and Croda with fermentation advances by Locus Bio-Energy. Chemically synthesized biosurfactants leverage existing alkoxylation assets, creating drop-in replacements that avoid the need for greenfield capital. True microbial rhamno- and sophorolipids deliver best-in-class biodegradability but remain capacity-constrained. Nonetheless, brand owners award shelf space to high-bio-content labels, incentivizing supply contracts that increase the North American Surfactants market's exposure to renewable pathways over the forecast horizon.

Carbon-capture-derived feedstocks offer a third route. LanzaTech and Twelve each pilot CO₂-to-ethylene flowsheets that could decouple ethylene supply from petrovolatility if tax credits and off-take agreements mature. Hybrid approaches, where 50% of the molecule originates from renewable carbon, dominate near-term launches because they strike a balance between cost and sustainability claims. As fermentation yields improve, the synthetic share will erode gradually, yet synthetics will still occupy the majority of the North America Surfactants market by 2031 because of cost, scale, and performance advantages.

By Application: Household Detergents Hold Share, Food Processing Sprints

Household soap and detergent commanded 49.05% of the 2025 volume. The North American surfactants market size for laundry liquids alone exceeded USD 6 billion, driven by cost-efficient linear alkylbenzene sulfonate systems and rising pod penetration. Unit volumes remain flat as consumers extend wash cycles, but surfactant grams per wash incrementally increase in ultra-concentrated formats. Personal-care demand edges up because sulfate-free claims trigger reformulations toward mild amphoterics. Procter & Gamble’s Tide Evo waterless cartridge system suggests a potential for longer-term volume displacement if solid-dose adoption accelerates.

Food processing is the fastest-growing end use, with a 5.12% CAGR, driven by plant-protein extraction, emulsified beverages, and fruit-washing systems that must comply with FDA food-contact regulations. Only surfactants listed in Title 21 CFR or holding GRAS status can be used in contact with food, funneling demand toward polysorbates and sorbitan esters while constraining the penetration of biosurfactants. Oilfield chemicals benefit from EOR pilots in the Permian, adding a niche but margin-rich outlet. Agricultural, textile, and emulsion-polymer segments round out the mix, each influenced by localized regulatory and performance requirements.

Geography Analysis

The United States generated 78.70% of 2025 revenue, thanks to Gulf Coast alkoxylation hubs, stringent EPA rules that discourage imports, and adjacency to household, institutional, and oilfield users. Dow increased regional alkoxylation capacity 70% since 2019, while BASF’s Geismar site integrated biomass-balance feedstocks to meet brand mandates without new builds. California and New York function as regulatory pacesetters, with bans on nonylphenol ethoxylates and pending quaternary-ammonium limits pushing nationwide reformulation. Though mature, the U.S. market sustains value growth through specialty grades and margin defense.

Canada mirrors U.S. statutes yet lacks indigenous ethylene-oxide capacity, relying on imports from Dow’s Alberta plant or Gulf Coast shipments. In November 2024, CEPA amendments synchronized aquatic-toxicity limits with EPA benchmarks, effectively banning nonylphenol ethoxylates above 0.1% weight and restricting residual 1,4-dioxane. The market size is roughly one-tenth of the U.S. figure, curtailing dedicated capacity spending and encouraging cross-border tolling.

Mexico is the fastest-growing geography, with a 3.88% CAGR, driven by near-shoring of consumer-goods lines, Braskem Idesa’s USD 450 million ethane terminal, and rising detergent penetration. Stepan’s 50,000 tpa Mexican facility supplies a portion of local demand, but approximately 60% of surfactant feedstocks still cross the U.S. border, leaving producers vulnerable to logistics and tariff swings. Infrastructure under-investment limits capacity additions, suggesting continued import reliance even as domestic demand rises.

Competitive Landscape

The North America surfactants market is moderately fragmented. The larger companies, such as Evonik and Stepan, pursue three key levers: renewable feedstock integration, brownfield debottlenecking, and expansion of their Mexico-focused footprint. Biosurfactant specialists race to scale fermentation but remain capital-constrained; neither has locked multi-year offtake contracts to underwrite large plants. Integrated oil majors also push downstream. Meanwhile, large brand owners such as L’Oréal file in-house surfactant patents, signaling partial disintermediation. Success in this evolving landscape hinges on regulatory agility, feedstock flexibility, and the rapid commercialization of novel chemistries before capacity is locked in.

North America Surfactants Industry Leaders

Stepan Company

BASF

Dow

Solvay

Kao Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Stepan lifted alpha-olefin-sulfonate output 25% across Millsdale, Anaheim, and Winder to secure domestic anionic supply.

- January 2025: Croda unveiled 100% bio-based ECO alcohol ethoxylates at Atlas Point to target USDA BioPreferred segments.

North America Surfactants Market Report Scope

Surfactants are a class of chemical substances used to reduce the surface tension between various substances, such as two liquids, a gas and a liquid, or a liquid and a solid. It has both hydrophobic and hydrophilic groups. The North American surfactant market is segmented by type, origin, application, and geography. By type, the market is segmented into anionic surfactant (linear alkylbenzene, sulfolane [LAS or LABS], alcohol ethoxysulfates [AES], alpha olefin sulfonates [AOS], secondary alkane sulfonate [SAS], methyl ester sulfonates [MES], sulfosuccinates, and others), cationic surfactant (quaternary ammonium compound and Others), non-ionic surfactant (alcohol ethoxylate, alkylphenol ethoxylate, fatty acid ester, and others), amphoteric surfactant, silicone surfactant, and other types. By origin, the market is segmented into synthetic and bio-based surfactants (chemically-synthesized bio-based surfactants and biosurfactants). By application, the market is segmented into household soap and detergent, personal care, lubricants and fuel additives, industry and institutional cleaning, food processing, oilfield chemicals, agricultural chemicals, textile processing, emulsion polymerization, and other applications. The report also covers the market size and forecasts for the market in three countries across the region. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD billion).

By Type

| Anionic Surfactant | Linear Alkylbenzene Sulfolane (LAS or LABS) |

| Alcohol Ethoxysulfates (AES) | |

| Alpha Olefin Sulfonates (AOS) | |

| Secondary Alkane Sulfonate (SAS) | |

| Methyl Ester Sulfonates (MES) | |

| Sulfosuccinates | |

| Others | |

| Cationic Surfactant | Quaternary ammonium compound |

| Others | |

| Non-ionic Surfactant | Alcohol ethoxylate |

| Alkylphenol ethoxylate | |

| Fatty acid ester | |

| Others | |

| Amphoteric Surfactant | |

| Silicone Surfactant | |

| Other Types |

By Origin

| Synthetic Surfactant | |

| Bio-based Surfactant | Chemically-Synthesized Bio-Based Surfactants |

| Biosurfactants |

By Application

| Household Soap and Detergent |

| Personal Care |

| Lubricants and Fuel Additives |

| Industry and Institutional Cleaning |

| Food Processing |

| Oilfield Chemicals |

| Agricultural Chemicals |

| Textile Processing |

| Emulsion Polymerisation |

| Others |

By Geography

| United States |

| Canada |

| Mexico |

| By Type | Anionic Surfactant | Linear Alkylbenzene Sulfolane (LAS or LABS) |

| Alcohol Ethoxysulfates (AES) | ||

| Alpha Olefin Sulfonates (AOS) | ||

| Secondary Alkane Sulfonate (SAS) | ||

| Methyl Ester Sulfonates (MES) | ||

| Sulfosuccinates | ||

| Others | ||

| Cationic Surfactant | Quaternary ammonium compound | |

| Others | ||

| Non-ionic Surfactant | Alcohol ethoxylate | |

| Alkylphenol ethoxylate | ||

| Fatty acid ester | ||

| Others | ||

| Amphoteric Surfactant | ||

| Silicone Surfactant | ||

| Other Types | ||

| By Origin | Synthetic Surfactant | |

| Bio-based Surfactant | Chemically-Synthesized Bio-Based Surfactants | |

| Biosurfactants | ||

| By Application | Household Soap and Detergent | |

| Personal Care | ||

| Lubricants and Fuel Additives | ||

| Industry and Institutional Cleaning | ||

| Food Processing | ||

| Oilfield Chemicals | ||

| Agricultural Chemicals | ||

| Textile Processing | ||

| Emulsion Polymerisation | ||

| Others | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How big is the North America Surfactants market in 2026?

The North America Surfactants market is valued at USD 14.67 billion in 2026.

What is the expected CAGR for surfactants across North America through 2031?

The compound annual growth rate is projected at 3.67%.

Which surfactant type holds the largest share region-wide?

Non-ionic alcohol-ethoxylate systems account for 44.12% of the 2025 volume.

Which application segment is growing fastest?

Food processing is expected to lead with a 5.12% CAGR through 2031.

Which country offers the quickest demand upside?

Mexico records the highest 3.88% CAGR, fueled by near-shoring and feedstock investment.

Page last updated on: