Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

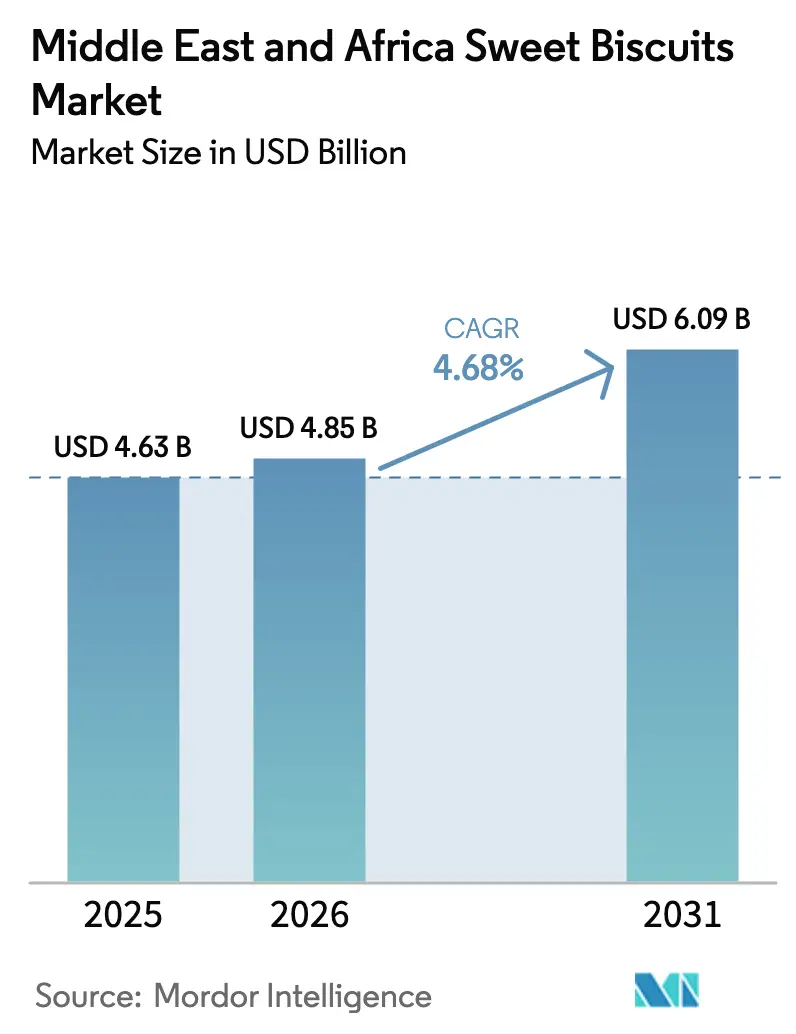

| Base Year Market Size (2025) | USD 4.63 Billion |

| Market Size (2026) | USD 4.85 Billion |

| Market Size (2031) | USD 6.09 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

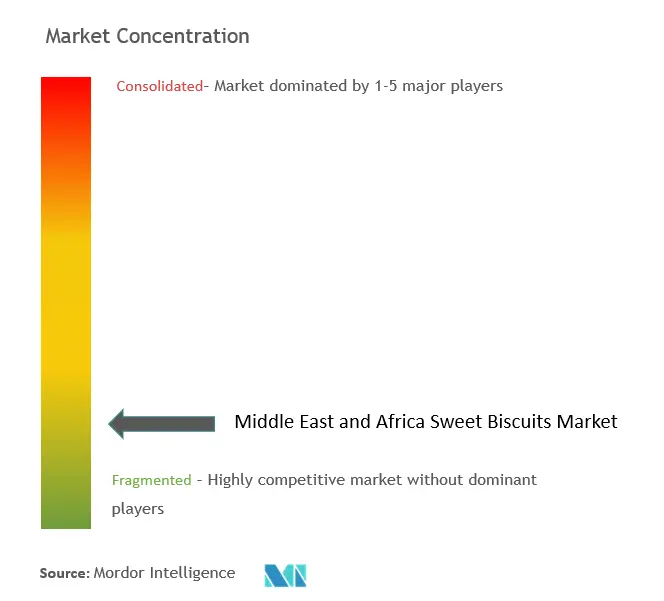

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Sweet Biscuits Market Analysis by Mordor Intelligence

The Middle East Africa sweet biscuits market size was valued at USD 4.63 billion in 2025 and estimated to grow from USD 4.85 billion in 2026 to reach USD 6.09 billion by 2031, at a CAGR of 4.68% during the forecast period (2026-2031). Population growth, rising disposable incomes, and a long-standing habit of snacking are driving demand in the region. While sandwiches are the go-to for daily consumption, cookies are carving out a niche in the premium and artisanal markets. Online grocery shopping is on the rise, with the UAE seeing a 29% uptick and Saudi Arabia a notable 46% in 2024. This surge has made portion-controlled packs more accessible, leading to increased impulse purchases. Initiatives like Saudi Vision 2030, along with duty rebates for local biscuit production, are fueling investments in domestic manufacturing[1]Source: Saudi Food & Drug Authority," SFDA in Vision 2030", www.sfda.gov.sa. These moves not only reduce reliance on imports but also bolster the resilience of the supply chain. Upgrades in retail and logistics further amplify these positive trends. Since 2024, regional hypermarkets have expanded their shelf space by over 500,000 m², enhancing the visibility and promotional opportunities for sweet biscuits. E-commerce platforms, bolstered by last-mile delivery services achieving 90-minute windows in key Gulf Cooperation Council (GCC) cities, are reshaping the shopping landscape. Premium gifts, especially limited-edition tins and date-sugar formulations, see a spike in demand during Ramadan and Eid, pushing up average selling prices. These offerings blend indulgence with a nod to health, making them even more appealing.

Key Report Takeaways

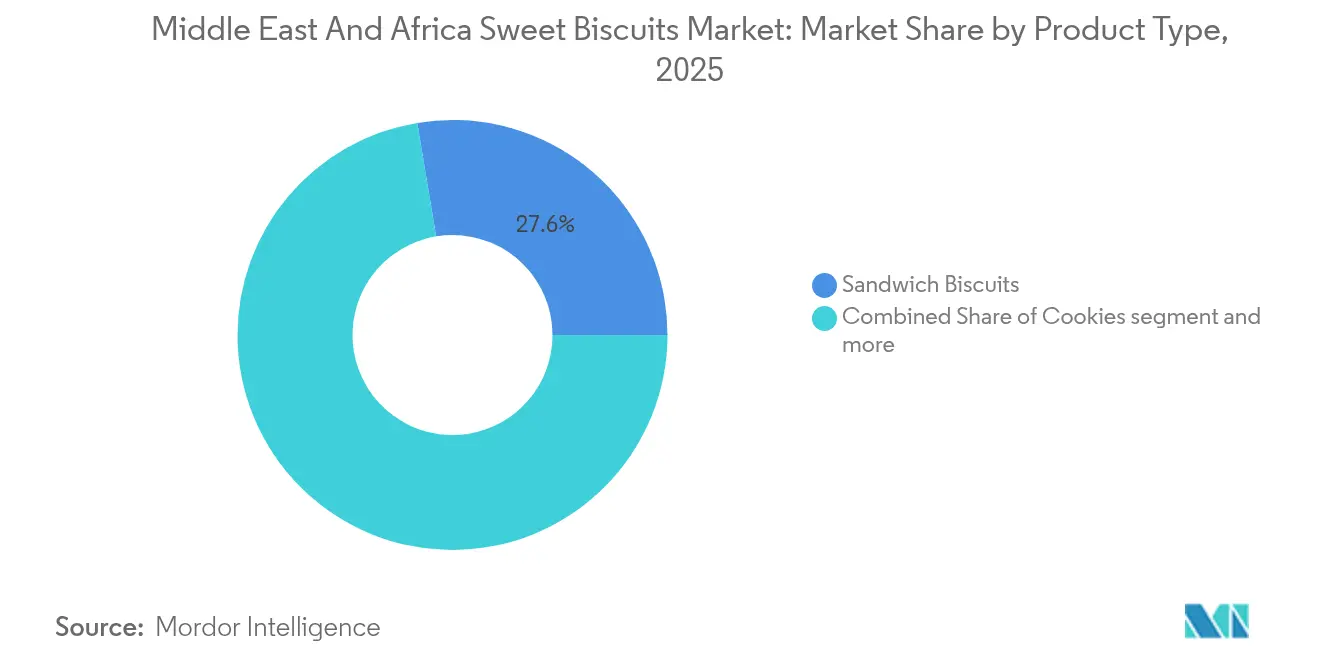

- By product type, Sandwich Biscuits led with 27.62% of 2025 Middle East Africa sweet biscuits market share and are projected to post a steady 4.28% CAGR through 2031.

- By product type, Cookies are set to deliver the fastest 5.62% CAGR between 2026-2031.

- By packaging, Single-Serve Flow-Wraps commanded 51.43% of the 2025 Middle East Africa sweet biscuits market size and should expand at a 4.38% CAGR to 2031.

- By packaging, Gift/Seasonal Tins will register the quickest 6.05% CAGR over the same period.

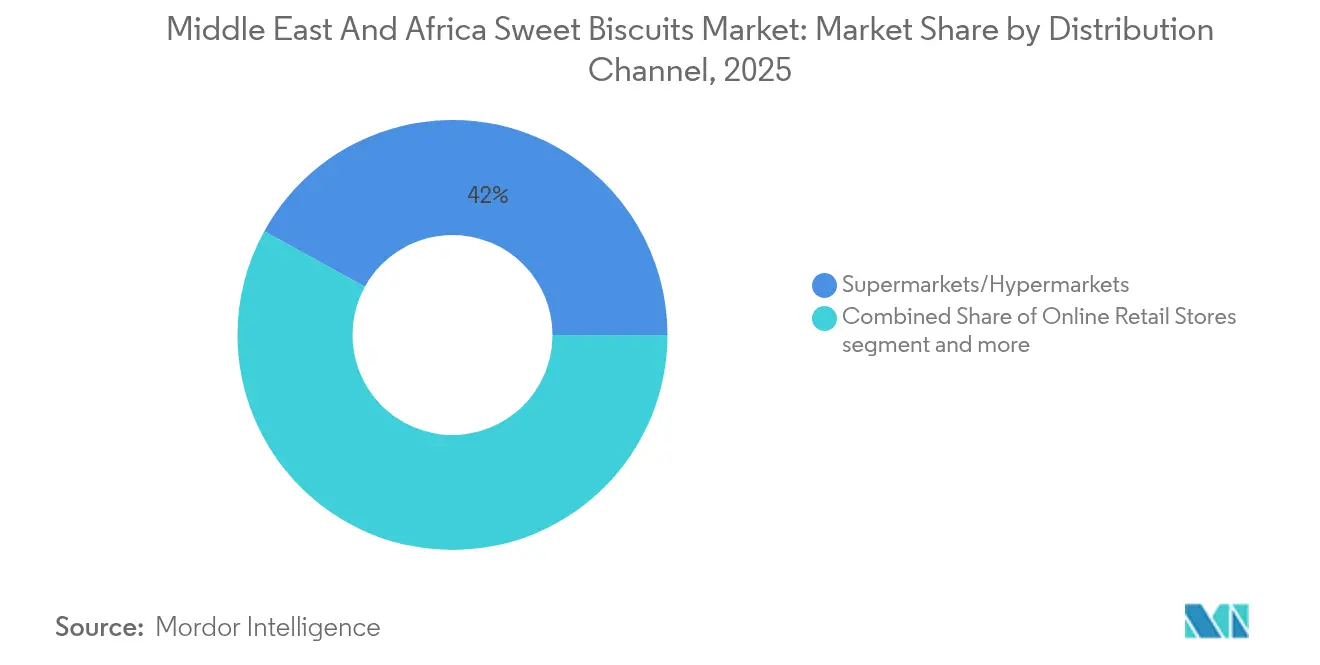

- By distribution, Supermarkets/Hypermarkets held 41.98% share in 2025, while Online Retail Stores will outpace all channels at a 7.08% CAGR through 2031.

- By geography, Saudi Arabia accounted for 18.95% of 2025 sales; South Africa is forecast to grow the fastest at a 6.84% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Sweet Biscuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising penetration of modern retail | +1.2% | GCC core; North Africa expansion | Medium term (2-4 years) |

| Premiumization and gift-pack demand | +0.8% | Middle East; Muslim-majority markets | Short term (≤ 2 years) |

| E-commerce grocery boom | +0.9% | UAE, Saudi Arabia, Kuwait, Qatar | Short term (≤ 2 years) |

| Saudi Vision 2030 duty rebates | +0.6% | Saudi Arabia; regional spillover | Long term (≥ 4 years) |

| Variety and artisanal offerings | +0.5% | UAE, Saudi Arabia premium segments | Medium term (2-4 years) |

| Date-sugar reformulation race | +0.4% | Algeria; potential regional adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Penetration of Modern Retail Drives Channel Transformation

Across GCC capitals, hypermarkets and supermarkets are increasingly adopting eye-level planograms and establishing dedicated Ramadan bays, with a clear emphasis on premium biscuit SKUs. Carrefour, under Majid Al Futtaim, boasts over 465 stores across 13 countries, catering to 770,000 shoppers daily. The brand is also piloting its HyperMax large-format outlets, which are designed to expand grocery ranges and provide a more comprehensive shopping experience. Not to be outdone, Lulu Retail unveiled a sprawling 200,000 sq ft flagship in Mecca, strategically designed to cater to a wide range of consumer needs, and has ambitious plans with 45 new openings across the GCC in the next three years. These strategic rollouts not only boost product visibility and facilitate bundled promotions but also promote the adoption of healthier and artisanal biscuit options among middle-income consumers. This reflects a growing demand for premium, diverse, and health-conscious product offerings in the region, driven by evolving consumer preferences and increasing disposable incomes.

Seasonal Gifting Amplifies Premium Positioning Opportunities

During Ramadan and Eid, biscuit demand sees a notable uptick, with consumers gravitating towards ornate tins and select flavors for gifting. These festive periods are marked by a cultural emphasis on exchanging gifts, driving higher consumption of premium and limited-edition products. In Ramadan 2025, regional e-commerce platforms reported a staggering 203.7% surge in gift GMV, with confectionery and biscuits accounting for 20.4% of the total gift volume. "Dubai Chocolate," a pistachio-based cookie line, commanded prices 1.6-2.0 times higher than regular offerings, reflecting a strong consumer preference for indulgent and unique items. This trend prompted retailers like Noon Minutes and Amazon.ae to broaden their holiday selections to cater to the growing demand. Manufacturers are seizing these opportunities to experiment with indulgent formats, command premium shelf space, and enhance overall category profitability, leveraging the festive season to test consumer preferences and optimize product offerings.

E-commerce Acceleration Reshapes Distribution Economics

In high-connectivity GCC markets, FMCG e-commerce has crossed a pivotal threshold. In 2024, online grocery values surged by 29% in the UAE and by a striking 46% in Saudi Arabia, with biscuits emerging as one of the top five impulse purchases. This growth highlights the increasing consumer preference for the convenience and accessibility of online platforms. Over 40% of orders were made via mobile devices, underscoring a strong demand for single-serve wraps that cater to digital convenience and on-the-go lifestyles. The growing reliance on mobile devices for online shopping reflects a shift in consumer behavior, driven by the need for speed and ease of use. Brands are leveraging algorithm-driven merchandising, subscription bundles, and flash promotions to engage shoppers seamlessly, navigating between physical and online carts, ensuring they remain competitive in this rapidly evolving market. Additionally, these strategies allow brands to personalize offerings, enhance customer retention, and capitalize on the growing e-commerce penetration in the region.

Saudi Vision 2030 Incentivizes Local Manufacturing Scale

Spanning 11 million m², the Jeddah Food Cluster aims to become the world's largest integrated food park, with a target investment of USD 5.3 billion and the creation of 43,000 jobs by 2035[2]Source: Saudi Manufacturing," TRANSFORMING FOOD MANUFACTURING FROM THE HEART OF SAUDI ARABIA", www.saudifoodmanufacturing.com. The cluster will house 76 turnkey factories dedicated to compliant biscuit production, positioning it as a significant contributor to the global food manufacturing industry. Recently, the National Biscuits and Confectionery Company achieved the BRCGS Global Standard Food Safety certification, highlighting the enhanced quality standards and commitment to food safety in the region. This certification is expected to boost consumer confidence and open new market opportunities. Additionally, duty rebate schemes on imported inputs, combined with export incentives, are not only reducing payback periods for new green-field lines but also promoting the regional sourcing of flavors, fats, and packaging materials. These measures are designed to strengthen the supply chain and enhance the competitiveness of local manufacturers in the global market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile wheat and palm-oil pricing | -0.7% | Import-dependent countries | Short term (≤ 2 years) |

| SFDA sodium/sugar front-of-pack rules | -0.3% | Saudi Arabia; possible GCC rollout | Medium term (2-4 years) |

| Red Sea land-bridge port congestion | -0.5% | Egypt, Saudi Arabia, UAE corridors | Short term (≤ 2 years) |

| Stringent food-safety and labeling updates | -0.2% | GCC core; spreading to Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commodity Price Volatility Pressures Input Cost Management

Wheat and palm oil continue to account for over half of the cost of goods sold at most biscuit plants. In 2024, Egypt set a record by importing 14.4 million tons of wheat. This came as global prices dipped by 11%, settling at USD 226.16 per ton FOB Black Sea. However, a weakening local currency tempered the advantage, reducing the potential cost savings for manufacturers and increasing pressure on production costs. In February 2025, Saudi Arabia's tender for 920,000 tons averaged USD 276.37 per ton, underscoring ongoing vulnerabilities in securing affordable wheat supplies amidst fluctuating global prices. Additionally, detours in Red Sea shipping, caused by geopolitical tensions and logistical challenges, are costing an extra USD 1 million for each Europe-Asia round trip. These increased costs are tightening gross margins for manufacturers, forcing them to pass on the burden to consumers through higher shelf prices, which could potentially impact demand and market dynamics.

Regulatory Compliance Complexity Increases Market Entry Barriers

Starting July 2025, the Saudi Food and Drug Authority mandates caffeine disclosures and high-sodium warnings on foodservice menus[3]Source: Saudi Food & Drug Authority," The SFDA Issues Three New Regulations to Promote Healthy Community Nutrition", www.sfda.gov.sa. These measures aim to enhance consumer awareness and promote healthier dietary choices. Additionally, new technical standards have been introduced to ensure accuracy in pre-pack net weights, which will require manufacturers to adhere to stricter compliance protocols. Meanwhile, the UAE Cabinet Resolution 83, effective January 2025, enforces metrological controls on pre-packed containers to standardize measurements and improve consumer trust. These regulations pose significant challenges for smaller players, who now face the burden of financing laboratory analytics, redesigning packaging to meet compliance standards, and upgrading IT traceability systems to ensure regulatory adherence. As a result, these requirements are stretching their capital expenditures and delaying the time-to-market for new SKUs, potentially impacting their competitiveness in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sandwich Dominance Meets Cookie Innovation

In 2025, Sandwich Biscuits dominated the market, clinching a 27.62% share, thanks to their strong consumer appeal. These biscuits, especially in filled formats, are favored for their enhanced taste and perceived value. Their popularity is bolstered by the ability to mix and match diverse flavors, making them adaptable to local preferences. For instance, date-filled variants are especially cherished during Ramadan celebrations. Brands are capitalizing on this versatility, introducing region-specific fillings to broaden their reach and relevance. This segment's dominance stems from its knack for satisfying both traditional and innovative cravings, fueling sustained growth in the biscuit category. Furthermore, manufacturers are emphasizing premium ingredients and indulgent textures to bolster perceived quality. In culturally significant markets, sandwich biscuits often take center stage in promotional campaigns, allowing suppliers to maximize market penetration during peak seasons. Their lasting appeal underscores how filled biscuits have seamlessly integrated into both daily snacking and festive indulgence.

On the other hand, cookies have emerged as the fastest-growing segment, boasting a projected CAGR of 5.62% through 2031. This surge is a testament to shifting consumer attitudes, especially among younger demographics. These consumers are increasingly drawn to artisanal and premium products that not only elevate their snacking experience but also resonate with social media aesthetics. Innovations play a pivotal role in this demand, with ingredients like vegan alternatives, protein fortification, and natural flavor infusions gaining traction, mirroring the broader trend of healthy indulgence. Events like ISM Middle East 2024 have spotlighted these industry shifts, with exhibitors unveiling products that meld functional benefits with traditional taste. Retailers are keenly attuned to these trends, broadening their portfolios with “Instagram-worthy” cookie formats and seasonal delights, aligning with frequent purchase cycles. The cookies segment's agile positioning enables it to siphon market share from both classic plain biscuits and richer chocolate-coated varieties. As the trend of premiumization gains momentum, cookies are increasingly becoming the gateway for consumers in search of novel and functional snacking adventures.

By Packaging Format: Portability and Prestige

In 2025, Single-Serve Flow-Wraps emerged as the dominant packaging format in the sweet biscuits market across the Middle East and Africa, commanding a notable 51.43% market share. This preference underscores urban consumers' desire for freshness, portion control, and hygienic packaging, all essential for their fast-paced lifestyles. The flow-wrap format plays a pivotal role in vending and convenience-store channels, facilitating swift distribution and bolstering biscuit consumption in metropolitan areas. As on-the-go snacking rises, manufacturers are turning to advanced sealing technologies and tamper-evident wrappers, addressing consumer concerns over safety and food quality. While family multipack boxes cater to larger households, particularly in Egypt and Nigeria, and play a vital role in sustaining overall demand, resealable pouches are gaining popularity for their freshness retention, especially among discerning shoppers. Sustainability efforts are gaining momentum, with UAE regulations pushing brands to experiment with compostable flow-wrap films and lightweight packaging, aiming for eco-compliance and a unique market stance.

Gift and Seasonal Tins, despite constituting a mere 6.12% of the 2025 packaging volume, are set to witness a robust CAGR of 6.05% through 2031. This surge is primarily fueled by heightened gifting during Ramadan and Eid, with retailers rolling out premium, limited-edition tins that fetch higher prices and capitalize on lucrative festival sales. By 2031, the market size for these tins is poised to exceed USD 372 million, as producers time their product launches with major holidays to tap into the uptick in consumer spending. Retailers are not just focusing on visually striking packaging but are also investing in collectible tins that double as gifts and keepsakes, solidifying their festive allure. Given the seasonal nature of this market, manufacturers are honing their inventory planning, ensuring they can forecast demand spikes and adjust production cycles accordingly. Advances in material science, like lightweight alloys and superior graphic techniques, are aiding compliance with regional sustainability mandates while catering to shifting consumer tastes. As the gifting culture flourishes, these premium biscuit tins are emerging as cherished symbols of celebration, marking them as the fastest-growing segment in the market.

By Distribution Channel: Store Aisles vs. Smartphone Screens

In 2025, supermarkets and hypermarkets dominated the sweet biscuit sales in the Middle East and Africa, securing an estimated 41.98% share of the overall distribution. Their dominance is bolstered by extensive end-cap promotions, enticing loyalty programs, and a strong cold-chain infrastructure that ensures product quality in warmer climates. These retail giants facilitate bulk purchases, offering families and snack enthusiasts a diverse selection at competitive prices. The trusted reputation of major supermarket chains resonates with consumers who prioritize food safety and freshness. While convenience stores cater to late-night shoppers, they play a secondary role in the retail hierarchy. Specialist bakeries, on the other hand, target a niche audience willing to pay a premium for artisanal experiences. Manufacturers are focusing on omnichannel pack differentiation, refining formats and label designs for high-traffic retail spaces, where strategic product placement amplifies sales.

Online retail is set to eclipse traditional brick-and-mortar stores, boasting a projected CAGR of 7.08% through 2031. This surge is largely attributed to the increasing adoption of mobile technology and digital wallets, which are transforming shopping behaviors in the region. In the UAE, around 56% of consumers engage in both online and offline shopping, a trend echoed by 33% in Saudi Arabia, underscoring the demand for integrated click-and-collect and swift last-mile delivery services. By 2031, the share of online purchases is anticipated to exceed 15%, a notable rise from the 10% recorded in 2024. Retailers are harnessing real-time consumer insights to gauge lifetime value and tailor promotions, effectively blending their physical and digital presences. To streamline last-mile delivery, there's a growing emphasis on e-commerce-friendly packaging, compact corrugated cases, and engaging AR labels. As manufacturers refine their omnichannel approaches, they stand to benefit from increased repeat purchases and enhanced sales through complementary items like beverages and spreads.

Geography Analysis

Saudi Arabia, buoyed by its Vision 2030 industrial policies, claimed the top spot in the 2025 rankings with a commanding 18.95% market share. A notable 46% surge in online grocery turnover has expanded sweet-biscuit access, reaching beyond just tier-one cities. The kingdom's ambitious Jeddah Food Cluster, sprawling over 11 million m² and eyeing investments of USD 5.3 billion, underscores its commitment to self-sufficiency and a robust export stance. Meanwhile, the UAE, serving as a commercial conduit for re-exports into Africa, boasts a multi-free-zone ecosystem. This ecosystem has already lured AED 184 million in agro-commodity processing commitments at JAFZA, highlighting its trade-hub prowess. Despite their smaller sizes, GCC states like Qatar, Kuwait, Oman, and Bahrain leverage high per-capita incomes and a demand for international flavors, leading to premium biscuit consumption that belies their population numbers.

South Africa is set to spearhead growth with a projected 6.84% CAGR through 2031. This growth is largely attributed to the rise of digital wallets, which are making branded SKUs accessible in informal settlements, a market valued at ZAR 178 billion. Egypt, recognized as a milling titan and a regional manufacturing nucleus, saw a boost when Edita Food Industries, leveraging toll-manufacturing alliances, doubled its biscuit capacity under the Oniro brand. Nigeria presents a vast market potential but is hampered by currency fluctuations, which inflate import costs and muddle pricing strategies for global players. Turkey, while adept at melding European flavor trends with Middle Eastern tastes, grapples with inflationary challenges that strain consumer spending. Markets across the region, stretching from Morocco to Kenya, are progressing at diverse rates, influenced by infrastructure developments and regulatory alignments. The GCC's push for unified labeling laws could simplify cross-border product launches. In contrast, Africa's fragmented standards necessitate tailored compliance approaches. The collective growth across these regions bolsters the case for multi-plant operations, which not only mitigate risks but also optimize duty exposures, further enhancing the allure of the Middle East Africa sweet biscuits market.

Competitive Landscape

The Middle East and Africa Sweet Biscuits market is highly competitive owing to the presence of multiple regional and international players offering a wide range of sweet biscuit products. Some of the prominent players in the market are Britannia Industries Limited, Gandour, Deemah United Food Industries Corp Ltd, Tiffany Foods Ltd, and Yildiz Holding Inc., among others. Key companies are adopting strategic approaches such as product launches, partnerships,s and mergers and acquisitions to maintain their position in the market. For instance, in May 2022, the Azcco Global Group acquired the CRAZE biscuit brand which will be re-launched to the market with more than 40 varieties.

Middle East And Africa Sweet Biscuits Industry Leaders

-

Britannia Industries Limited

-

Gandour

-

Deemah United Food Industries Corp Ltd

-

Yildiz Holding Inc.

-

Mondelez International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Blueprint Cookies inaugurated its latest outlet at the Mall of the Emirates in the UAE. This expansion marks the company's entry into one of the region's most prestigious shopping destinations, aiming to attract a diverse customer base.

- June 2025: Ben's Cookies unveiled a Mini version of its cookies, available exclusively on Talabat. This product launch is part of the company's strategy to cater to consumers seeking smaller, convenient snack options while leveraging Talabat's extensive delivery network.

- May 2025: Mondelex International bolstered its foothold in Egypt by launching a new R&D lab dedicated to Biscuit and Baked Snacks. The lab's primary goal is to innovate and develop new baked snacks and biscuits, aligning with the company's vision to meet evolving consumer preferences and enhance its market position.

- April 2022: Flemish biscuit maker Lotus invested US$11m and commenced construction of its third factory in South Africa. Lotus has expanded its production capacity from 1,800 tonnes to about 3,100 tonnes.

Middle East And Africa Sweet Biscuits Market Report Scope

Sweet biscuits are flour-based baked products that are sweet in taste. The Middle East and Africa sweet biscuits market is segmented by type, distribution channel, and geography. By type, the market is segmented into plain biscuits, cookies, sandwich biscuits, filled biscuits, chocolate-coated biscuits, and other sweet biscuits. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. It provides an analysis of emerging and established economies across the region, comprising Saudi Arabia, United Arab Emirates, South Africa, and the Rest of the Middle East and Africa.

By Product Type

| Plain Biscuits |

| Cookies |

| Sandwich Biscuits |

| Filled Biscuits |

| Chocolate-Coated Biscuits |

| Other Sweet Biscuits |

By Packaging Format

| Single-Serve Flow-Wraps |

| Family/Multipack Boxes |

| Gift & Seasonal Tins, Bulk packagings |

Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialist Bakeries |

| Online Retail Retails |

| Others |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| South Africa |

| Nigeria |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Plain Biscuits |

| Cookies | |

| Sandwich Biscuits | |

| Filled Biscuits | |

| Chocolate-Coated Biscuits | |

| Other Sweet Biscuits | |

| By Packaging Format | Single-Serve Flow-Wraps |

| Family/Multipack Boxes | |

| Gift & Seasonal Tins, Bulk packagings | |

| Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialist Bakeries | |

| Online Retail Retails | |

| Others | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| South Africa | |

| Nigeria | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the Middle East Africa sweet biscuits market?

The market is valued at USD 4.85 billion in 2026.

How fast is the market expected to grow?

It will expand at a 4.68% CAGR, reaching USD 6.09 billion by 2031.

Which product segment holds the largest share?

Sandwich Biscuits command 27.62% of 2025 sales.

Which geography is growing the fastest?

South Africa is forecast to post a 6.84% CAGR through 2031.

Page last updated on: