Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

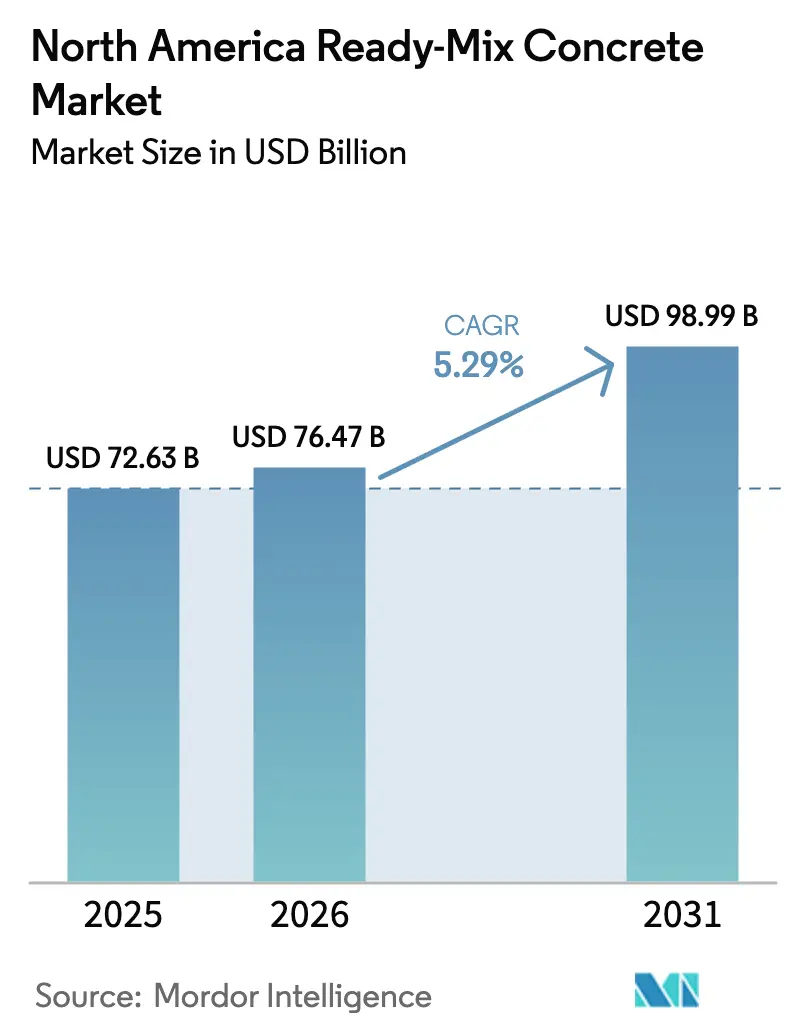

| Base Year Market Size (2025) | USD 72.63 Billion |

| Market Size (2026) | USD 76.47 Billion |

| Market Size (2031) | USD 98.99 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

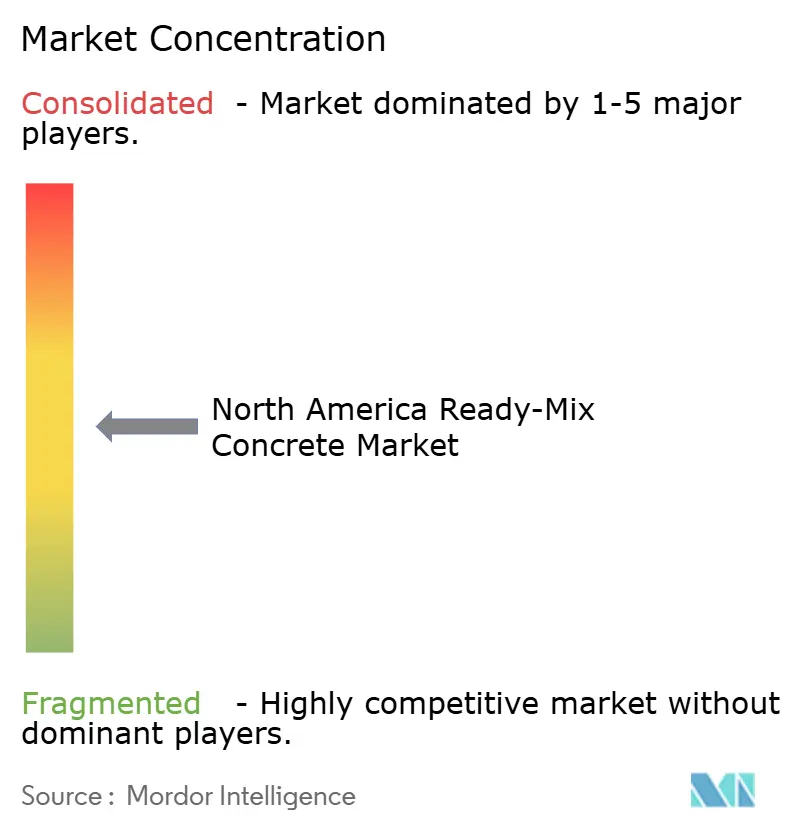

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Ready-Mix Concrete Market Analysis by Mordor Intelligence

The North America Ready-Mix Concrete Market size was valued at USD 72.63 billion in 2025 and estimated to grow from USD 76.47 billion in 2026 to reach USD 98.99 billion by 2031, at a CAGR of 5.29% during the forecast period (2026-2031). The trajectory underscores the sector’s resilience as federal infrastructure outlays, a broad-based housing recovery, and rapid digitalization of dispatch and batching operations converge to expand demand. Funds released under the Infrastructure Investment and Jobs Act (IIJA) have already accelerated concrete consumption along priority highway and bridge corridors, while state decarbonization mandates are nudging producers toward low-carbon mix designs that command premium pricing yet still meet performance specifications. At the same time, AI-enabled quality control systems are trimming material waste and reducing delivery cycle times, giving early adopters a competitive cost advantage. Consolidation continues unabated, with leading vertically integrated suppliers expanding geographic footprints and capturing synergies by controlling cement, aggregate, and downstream mixing assets. Collectively, these forces indicate that the North America Ready-Mix Concrete market will sustain solid mid-single-digit growth through the end of the decade.

Key Report Takeaways

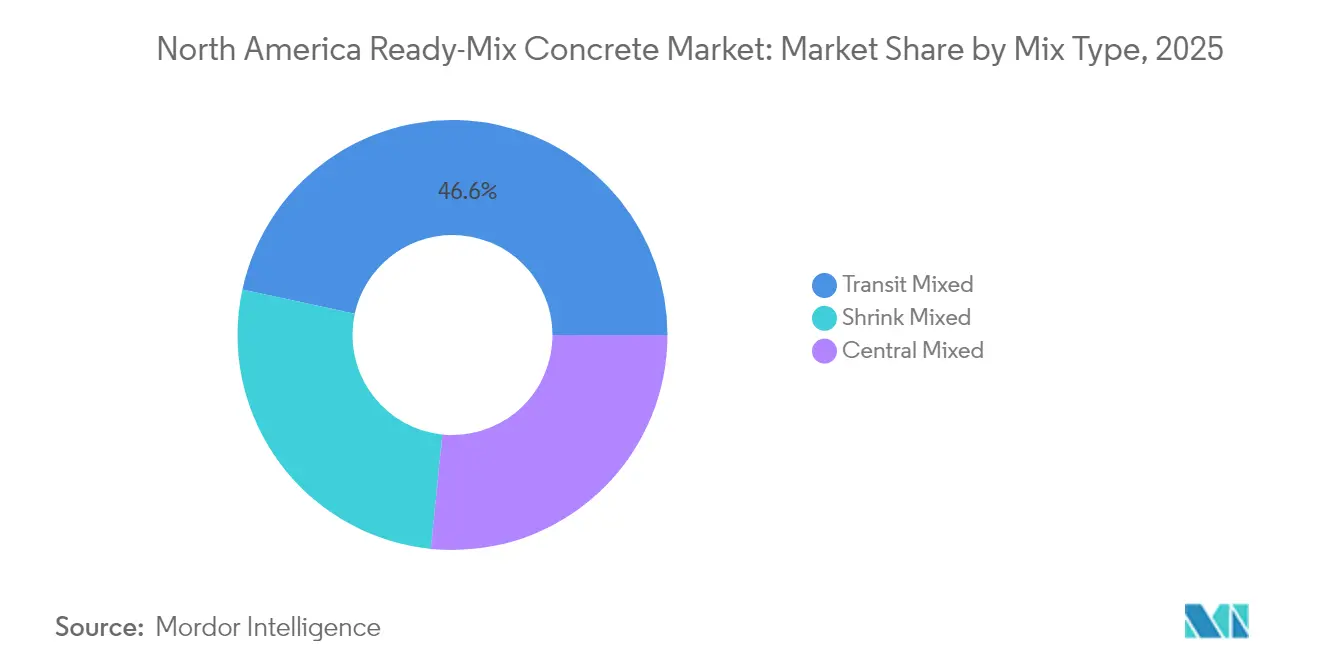

- By mix type, transit-Mixed concrete led with a 46.60% share of 2025 revenue and remains the largest contributor to growth. Shrink-Mixed concrete is advancing at a 5.59% CAGR through 2031, the fastest rate among mix types.

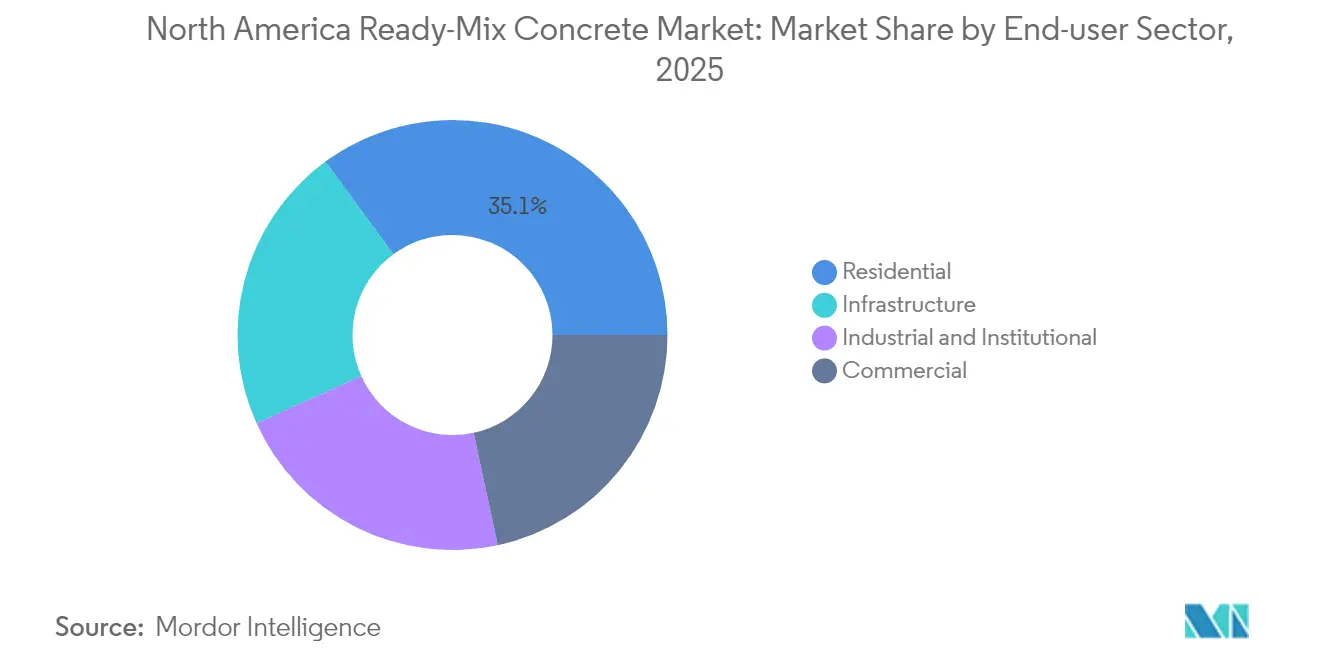

- By end-use sector, the residential segment accounted for 35.07% of 2025 revenue and is expanding at a leading 5.91% CAGR.

- By geography, the United States commanded 84.17% of 2025 value while also posting the highest 5.45% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Ready-Mix Concrete Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal-level infrastructure stimulus packages | +1.8% | Highest concentration in California, Texas, New York, Florida, Pennsylvania | Medium term (2-4 years) |

| Housing starts rebound and residential retrofits | +1.5% | U.S. metropolitan areas | Short term (≤ 2 years) |

| Superior consistency and speed versus site-mixed | +0.9% | Urban markets worldwide | Long term (≥ 4 years) |

| State decarbonization mandates | +1.1% | Early adoption in California and New York, spreading nationally | Medium term (2-4 years) |

| AI-optimized dispatch and batching platforms | +0.6% | Technology-forward producers, especially in dense metro regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal Infrastructure Stimulus Drives Sustained Concrete Demand

Annual IIJA allocations of USD 62 billion for highways and bridges are channeling a reliable order pipeline to producers across the North America Ready-Mix Concrete market[1]Federal Highway Administration, “Budget Estimates Fiscal Year 2025,” fhwa.dot.gov. Contractors on Michigan’s I-69 rebuild, for example, established temporary batch plants to meet accelerated delivery schedules and optimize mix performance[2]Michigan Concrete Association, “I-69 Reconstruction,” miconcrete.org. With disbursements fixed through 2030, producers now operate with unprecedented demand visibility, de-risking capital outlays for new plants and fleets.

Housing Market Recovery Accelerates Residential Concrete Consumption

The residential segment posted the highest 5.98% CAGR as pent-up demand, favorable mortgage support, and migration to Sun Belt metros lifted housing starts. Population inflows into Texas, Florida, and the Carolinas require rapid foundation and slab work—applications where ready-mix’s speed and strength consistency eclipse site-mixed alternatives. Parallel retrofit activity in legacy cities such as Chicago and Philadelphia is boosting demand for specialty decorative and fiber-reinforced mixes.

Technology Integration Transforms Operational Efficiency

Producers deploying cloud-based dispatch platforms report up to 15% improvement in truck utilization and 20% lower material waste through real-time slump monitoring and predictive batching algorithms. Heidelberg Materials uses AI-driven in-drum probes that continuously relay temperature and workability data, reducing rejection rates while shrinking CO₂ intensity. The SlumpGuard vision analytics system adds automated slump prediction and has cut manual testing labor by half at pilot plants

State Decarbonization Mandates Reshape Product Specifications

California’s CALGreen Code caps concrete’s global-warming potential at 260-433 kg CO₂e/m³ depending on strength class, pushing suppliers to integrate higher fly-ash and slag ratios or alternative binders. New York’s Buy Clean law requires Environmental Product Declarations on projects over USD 1 million, favoring producers that can certify low-carbon mixes. These mandates accelerate the scaling of technologies such as Fortera’s ReCarb process, which claims 70% lower embodied carbon versus ordinary Portland cement

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cement and aggregate price volatility | –1.2% | Import-dependent regions across North America | Short term (≤ 2 years) |

| Competition from precast and modular systems | –0.8% | Commercial and industrial segments | Long term (≥ 4 years) |

| Truck-driver capacity and Hours-of-Service limits | –0.7% | Rural and long-distance delivery markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cement and Aggregate Price Volatility Pressures Margins

Energy-linked cement price spikes in 2024 and 2025 strained producer margins as tariffs on imported clinker compounded supply tightness. Aggregate haulage costs also rose amid diesel price volatility, with western Canadian quarries citing freight as 40% of delivered cost. Contract structures often delay pass-through, forcing producers to hedge input costs or absorb margin compression during peak volatility.

Precast and Modular Construction Systems Gain Market Share

In parking structures and warehouse shells, precast panels can shave weeks off schedules, challenging ready-mix volumes. Precasters are harnessing automation and digital-twin design to improve dimensional accuracy, while 3D-printed concrete elements are carving out niche demand for bespoke architectural components. Ready-mix suppliers are countering by offering on-site volumetric trucks and rapid-set mixes that narrow the time-to-erection gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mix Type: Transit-Mixed Dominance Amid Shrink-Mixed Innovation

Transit-Mixed concrete accounted for a 46.60% North America Ready-Mix Concrete market share. As mobile drums enable last-minute water adjustments, contractors value the flexibility to fine-tune slump on arrival, making the format indispensable for bridge decks and mid-rise frames. Over the forecast horizon, the segment continues to leverage established logistics networks and truck telematics that optimize engine idle time and Washington-mandated emissions targets. Central-Mixed concrete holds the second-largest portion of the North America Ready-Mix Concrete market, favored for mega-volume pours such as dam footings, where central batching ensures homogeneous quality. Shrink-Mixed concrete, though currently smaller, is projected to expand at 5.59% CAGR—the highest among mix types—thanks to admixture advancements that prolong workability for small urban deliveries, cutting site congestion and storage footprints.

Demand for Shrink-Mixed products is also being fueled by cities tightening noise and dust ordinances, prompting contractors to avoid on-site mixers. Producers are responding with mini-fleet agitator trucks that feature hydraulic drive systems and carbon-fiber drums, slashing tare weight and boosting payload. Central-Mixed operators, meanwhile, are retrofitting plants with high-shear twin-shaft mixers capable of ultra-high-performance concrete (UHPC) for precast girders on high-speed rail projects.

By End-User Sector: Residential Leadership Drives Market Expansion

The residential sector held a 35.07% slice of the North America Ready-Mix Concrete market. Single-family starts in Texas, Florida, and Arizona surged on domestic inward migration, while multifamily towers in Dallas, Miami, and Toronto drove demand for high-strength pumpable mixes. The segment’s 5.91% CAGR is buoyed by public-private partnerships targeting affordable housing backlogs and by municipal incentives for low-carbon building materials. Commercial construction ranks second, covering retail centers, data halls, and mixed-use downtown redevelopments that rely on ready-mix for accelerated topping-out schedules. Industrial-and-institutional projects deliver stable baseline demand, with semiconductor fabs and school modernization programs specifying shrinkage-compensating mixes for vibration-sensitive flooring.

Infrastructure remains volume-intensive although smaller by revenue, yet it earns premium margins via high-performance formulations used in bridge decks and water-treatment facilities. Across sectors, developers increasingly mandate Environmental Product Declarations, pushing producers to document embodied-carbon reductions. The residential domain is especially sensitive to green-building certification: mixes with 30% fly-ash substitution and warm-mix admixtures help builders secure LEED points.

Geography Analysis

The United States dominated with an 84.17% share of the North America Ready-Mix Concrete market. IIJA funds of USD 62 billion annually guarantee a multiyear pipeline, with California, Texas, and New York receiving the largest allocations. California’s CALGreen Code and executive orders from New York’s Office of General Services compel low-carbon concrete adoption, setting early-mover standards soon to permeate neighboring states. U.S. producers also benefit from dense interstate highway networks that optimize back-haul opportunities for aggregate fleets, trimming logistics costs.

Canada contributes a moderate slice of regional revenue anchored in Ontario and Québec population centers. Federal and provincial infrastructure budgets prioritize rehabilitation of aging overpasses and public-transit expansions, while harsh winter cycles constrain construction windows to roughly eight months, amplifying the appeal of high-early-strength mixes.

Mexico is propelled by industrial nearshoring clusters along the Bajío corridor and northern maquiladora zones. The country’s 38 integrated cement plants supply a domestic clinker capacity of 60.5 million t, allowing ready-mix affiliates of Cemex, GCC, and Holcim-Apasco to leverage captive cement and aggregate while exporting surplus to U.S. border projects when demand peaks.

Competitive Landscape

The market is moderately fragmented. Technology leadership is turning into a key differentiator. Producers using AI-optimized truck queuing and automated batching have boosted on-time delivery above 96%, outclassing peers still reliant on manual dispatch spreadsheets. Sustainability credentials further shape bid competitiveness: CEMEX’s Vertua product line, marketed at 20-70% lower embodied carbon, secured marquee pours on U.S. federal courthouses after surpassing Buy Clean thresholds. Barriers to entry remain high because a single dry-batch plant costs USD 2-3 million, not including aggregate reserves and fleet investment.

North America Ready-Mix Concrete Industry Leaders

CEMEX SAB de CV

CRH

Holcim

Heidelberg Materials

Vulcan Materials Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Holcim completed the spin-off of its North American operations into Amrize, citing the reshoring of manufacturing and infrastructure modernization as catalysts for growth.

- September 2024: SRM Concrete acquired Duluth Ready Mix, Superior-Duluth Ready Mix, and Best Concrete in northeast Minnesota, adding six plants and three quarries in its first foray into Minnesota and Wisconsin.

North America Ready-Mix Concrete Market Report Scope

Ready-mix concrete (RMC) is concrete that is used directly at the job site after being batched at a central plant. RMC finds its applications in foundations, walls, floors and bases, driveways, and other constructional activities, owing to its excellent properties.

The North American ready-mix concrete market is segmented by end-user industry and geography. By end-user industry, the market is segmented into residential, commercial, industrial/institutional, and infrastructure. By geography, the market is segmented into the United States, Canada, and Mexico. The report covers the market size and forecasts for three countries across the region. For each segment, market sizing and forecasts have been provided based on revenue (in USD billion).

By Mix Type

| Transit Mixed |

| Central Mixed |

| Shrink Mixed |

By End-user Sector

| Residential |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

By Geography

| United States |

| Canada |

| Mexico |

| By Mix Type | Transit Mixed |

| Central Mixed | |

| Shrink Mixed | |

| By End-user Sector | Residential |

| Commercial | |

| Industrial and Institutional | |

| Infrastructure | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the 2026 value of the North America Ready-Mix Concrete market?

It totaled USD 76.47 billion in 2026.

How fast is demand forecast to grow through 2031?

Revenue is expected to expand at a 5.29% CAGR to reach USD 98.99 billion.

Which mix type currently holds the largest revenue share?

Transit-Mixed concrete leads with 46.60% of 2025 revenue.

Which end-user sector is growing the fastest?

Residential applications are expanding at a 5.91% CAGR on sustained housing starts.

What share does the United States command?

The U.S. accounts for 84.17% of regional revenue and posts the highest 5.45% CAGR.

How are state regulations shaping product specifications?

CALGreen and New York's Buy Clean rules are driving adoption of low-carbon mixes and requiring Environmental Product Declarations.

Page last updated on: