Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

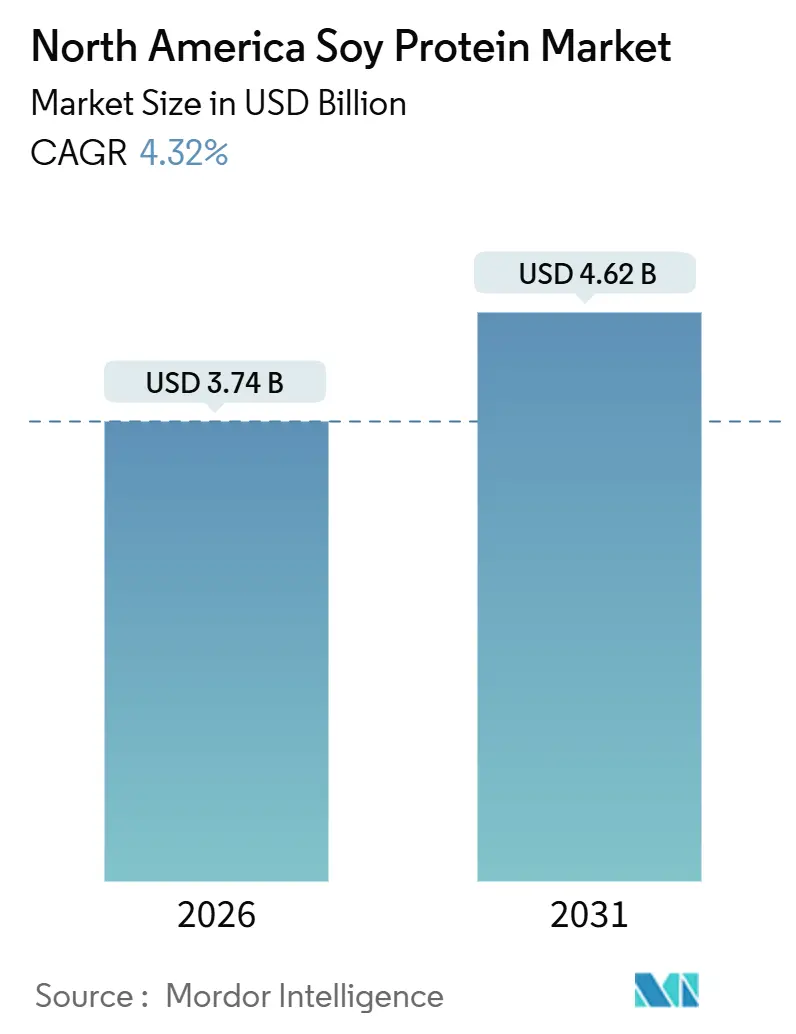

| Market Size (2026) | USD 3.74 Billion |

| Market Size (2031) | USD 4.62 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

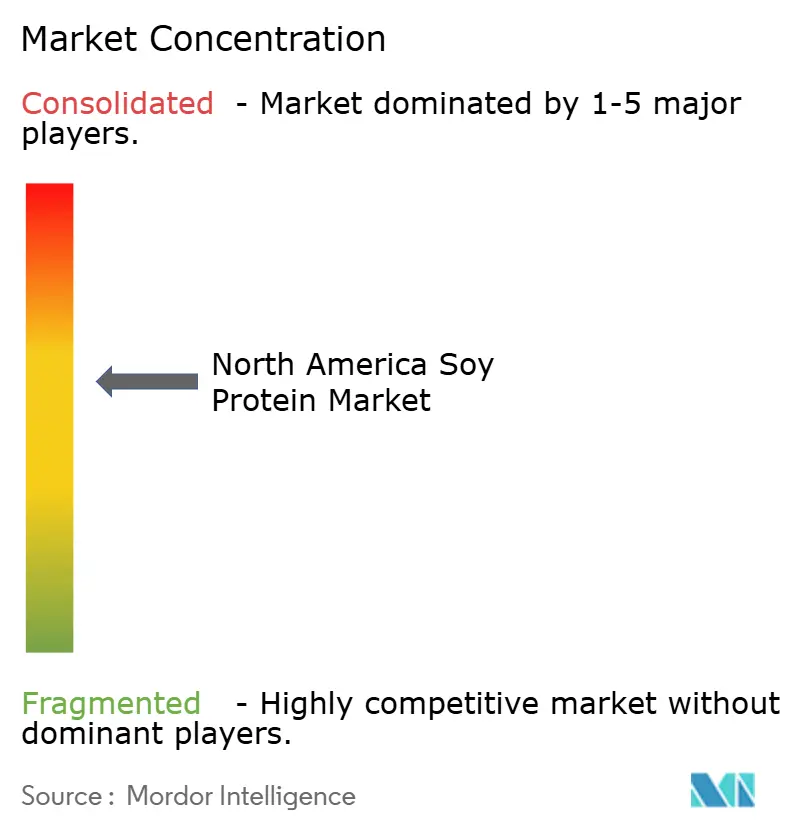

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Soy Protein Market Analysis by Mordor Intelligence

The North American soy protein market is expected to grow from USD 3.74 billion in 2026 to USD 4.62 billion by 2031, at a compound annual growth rate (CAGR) of 4.32% over the forecast period. This growth highlights a steady increase in market size. The rising demand for soy protein is driven by food manufacturers increasingly adopting plant-based formulations to meet sustainability targets, cater to consumers with allergen concerns, and reduce costs compared to animal-based proteins. Major processors are investing in advanced technologies such as high-moisture extrusion, aqueous extraction, and vertically integrated supply chains. These advancements are creating opportunities to produce high-quality, value-added soy protein ingredients that meet clean-label requirements. By form, soy protein isolates dominate the market, while textured soy protein variants are witnessing accelerated growth. By category, conventional soy protein holds the largest share, but organic soy protein is gradually gaining traction as a niche segment. The market is moderately consolidated, with a few key players holding significant shares.

Key Report Takeaways

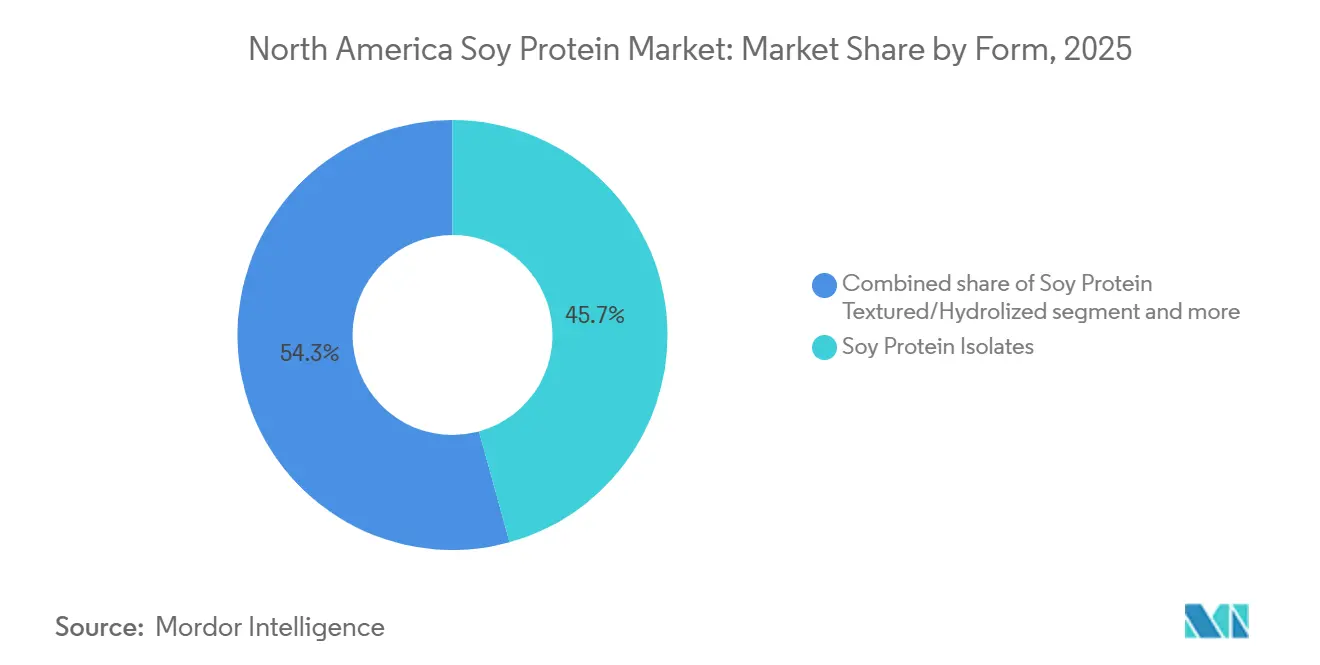

- By form, soy protein isolates led with 45.73% of the North America soy protein market share in 2025, and textured variants are advancing at a 6.36% CAGR through 2031.

- By category, conventional products dominated the North American soy protein market with an 83.77% share in 2025, while organic offerings are expanding at a 5.41% CAGR through 2031.

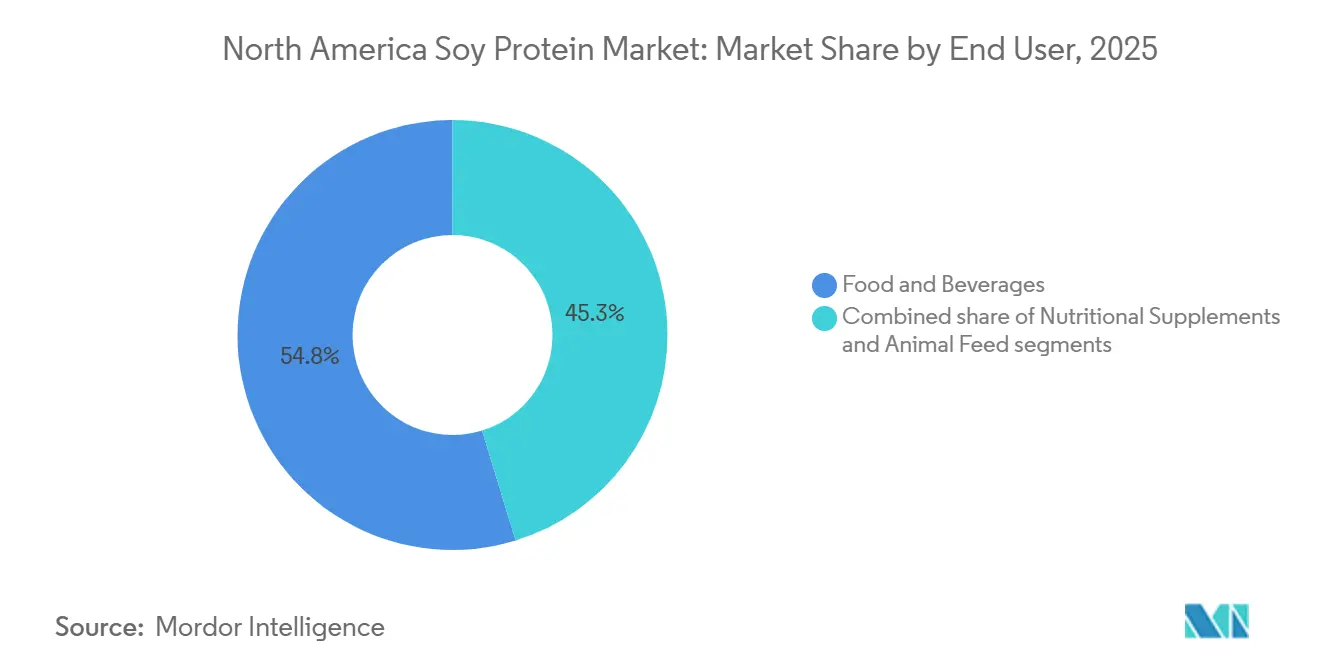

- By end user, food and beverages commanded a 54.75% share of the North America soy protein market size in 2025, and nutritional supplements are growing at a 6.24% CAGR through 2031.

- By country, the United States held 92.48% of the North American soy protein market share in 2025, whereas Canada recorded the highest projected CAGR of 5.18% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Soy Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for vegan and vegetarian diets driving adoption in meat substitutes | +0.8% | United States, Canada, urban centers in Mexico | Medium term (2-4 years) |

| Rising consumer awareness around health, fitness, and protein-rich diets increasing demand | +0.7% | North America-wide, strongest in United States and Canada | Short term (≤ 2 years) |

| Popularity of clean-label and non-GMO ingredients favoring soy over animal proteins | +0.6% | United States, Canada (Ontario, Quebec) | Medium term (2-4 years) |

| Expansion of sports nutrition and high-protein supplements incorporating soy | +0.5% | United States, Canada, premium retail channels | Short term (≤ 2 years) |

| Growing use in infant nutrition and elderly nutrition products | +0.4% | United States, Canada, regulated by Food and Drug Administration and Health Canada | Long term (≥ 4 years) |

| Growth of ready-to-eat and convenience food consumption increasing demand for functional plant proteins | +0.3% | North America-wide, food service and retail | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing consumer preference for vegan and vegetarian diets driving adoption in meat substitutes

In North America, the demand for soy protein is increasingly driven by flexitarian consumers who are looking for affordable and meat-like alternatives, rather than solely by vegan or vegetarian consumers. As of 2024, only 11% of American plant-based meat consumers identify as vegetarian, pescatarian, or vegan, indicating that the growth of this category is largely supported by traditional meat eaters exploring plant-based options, according to the Good Food Institute[1]Source: Good Food Institute, "Plant Based Meat in the United States", gfi.org. Textured soy protein remains a key ingredient due to its ability to mimic the fibrous structure of muscle and provide cost-effective formulations. Recent advancements in twin-screw extrusion technology have further enhanced the production of plant-based products, enabling features like visible marbling in plant-based steaks. Since taste plays a critical role in driving repeat purchases, manufacturers are increasingly combining soy with other plant proteins to improve flavor and texture while maintaining scalability and production efficiency.

Rising consumer awareness around health, fitness, and protein-rich diets increasing demand

In North America, soy protein demand is growing as more consumers focus on incorporating protein into their diets for health and fitness benefits. In 2024, 71% of Americans are actively trying to increase their protein intake, reflecting a broader trend toward healthier eating habits, as per the International Food Information Council[2]Source: International Food Information Council, "2024 IFIC Food and Health Survey", ific.org. Soy protein isolates are gaining popularity due to their complete amino acid profile and affordability compared to whey protein. These isolates are widely used in products like ready-to-drink shakes and high-protein snack bars. The United States' Food and Drug Administration's health claim that consuming 25 grams of soy protein daily can support heart health further boosts their credibility, a benefit not commonly found in newer plant proteins. Soy protein’s high digestibility makes it ideal for senior nutrition products aimed at maintaining muscle health, while its excellent solubility ensures it performs well in single-serve beverages, which are popular in convenience retail formats.

Growing use of soy protein in infant nutrition and elderly nutrition products

The growing demand for soy protein in the United States is driven by its increasing use in nutrition products for both infants and the elderly. In 2024, individuals aged 65 and older made up 18% of the United States' population, while children aged 0–14 accounted for 25%, reflecting the ongoing need for tailored nutrition to support early development and healthy aging, according to the World Bank[3]Source: World Bank, "Population Ages 65 and Above (% of Total Population) - United States", worldbank.org. Soy protein is a key ingredient in infant formulas due to its balanced amino acid profile and suitability for babies with lactose intolerance. For the elderly, it is highly valued for its easy digestibility and ability to support muscle maintenance, which is crucial for aging populations. As healthcare providers and caregivers focus more on age-specific dietary needs, soy protein is being increasingly incorporated into products designed for pediatric and senior nutrition. This trend highlights its versatility and growing importance in addressing the nutritional requirements of these two significant demographic groups.

Expansion of sports nutrition and high-protein supplements incorporates soy

The growing interest in fitness and recreational activities is driving the demand for soy protein in sports nutrition and high-protein supplements across North America. In 2024, approximately 247.1 million Americans engaged in at least one sports, fitness, or outdoor activity, creating a larger market for products such as protein shakes, recovery drinks, and dietary supplements, according to the Sports and Fitness Industry Association[4]Source: Sports and Fitness Industry Association, "SFIA’s Topline Participation Report Shows 247.1 Million Americans Were Active in 2024", sfia.org. Soy protein isolates, which contain up to 90% protein and offer excellent heat stability, are becoming a preferred ingredient in ready-to-drink beverages and retort products, where whey protein often faces formulation limitations. As consumers increasingly prioritize clean-label products and third-party testing becomes a standard in competitive sports, soy protein’s consistent quality and adaptability in blended formulations make it a strong contender in the evolving sports nutrition market. This trend highlights the growing role of soy protein in meeting the nutritional needs of active individuals while aligning with clean-label and sustainability preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict regulatory scrutiny on soy safety slowing new product approvals | -0.4% | United States (Food and Drug Administeation jurisdiction), Canada (Health Canada) | Short term (≤ 2 years) |

| Growing consumer concerns around soy allergies limiting adoption in certain segments | -0.3% | North America-wide, particularly infant formula and bakery | Medium term (2-4 years) |

| Volatility in soybean prices due to climate variability and agricultural supply disruptions | -0.5% | United States (Midwest), Canada (Ontario, Manitoba) | Short term (≤ 2 years) |

| Competition from pea, whey, and other plant proteins fragmenting market share | -0.4% | North America-wide, strongest in plant-based meat and sports nutrition | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict regulatory scrutiny on soy safety slows new product approvals

Regulatory oversight remains a significant challenge for the North American soy protein market, particularly in applications such as infant and medical nutrition. The United States Food and Drug Administration identifies soy as a major allergen, requiring clear labeling on packaging and strict manufacturing controls in facilities that handle multiple products. These requirements increase production costs and limit the flexibility to launch new products. For infant formula, the regulatory process is even more stringent, with mandatory pre-market evaluations that can delay product approvals by up to 18 months, slowing down innovation in this segment. Expanding into Canada presents further challenges, as Health Canada enforces similar allergen labeling rules along with bilingual packaging requirements, which can be particularly burdensome for smaller manufacturers. Although concerns about phytoestrogens in soy have not led to formal restrictions, the category remains under close regulatory scrutiny.

Growing consumer concerns around soy allergies are limiting adoption in certain food and nutrition segments

Increasing consumer awareness of food allergens is limiting the use of soy protein in certain food and nutrition categories, especially in products for children and in convenient, on-the-go snacks. The U.S. Food and Drug Administration classifies soy as a major food allergen, which has made consumers more cautious about it. As a result, many brands are avoiding soy and focusing on “free-from” products that cater to allergy-conscious buyers. This shift has driven the growing use of alternative proteins like pea and rice, even though soy often provides better functionality and cost benefits. In the retail sector, concerns about allergens create additional challenges for established brands. Adding soy to their products often requires reformulating recipes, segregating production processes, and updating product labels, which can be costly and time-consuming. Consequently, soy protein growth is now more concentrated in adult-focused, sports nutrition, and foodservice channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Isolates Lead, Textured Variants Accelerate

Soy protein isolates were the leading segment in the North America soy protein market in 2025, holding 45.73% of the total market share. This dominance is due to their high protein content, neutral flavor, and adaptability across various applications. They are widely used in sports nutrition, medical nutrition, and ready-to-drink beverages, as they provide a clean-label, complete protein option suitable for both liquid and solid products. Their cost-effectiveness compared to animal proteins and consistent quality make them a preferred choice for large-scale manufacturers. With the growing trend of high-protein diets, soy protein isolates are expected to remain a key driver of market growth.

On the other hand, textured and hydrolyzed soy proteins are projected to grow at a faster rate, with a CAGR of 6.36% through 2031. This growth is fueled by their increasing use in meat substitutes, convenience foods, and functional nutrition products, where factors like texture, easy digestion, and quick absorption are essential. Technological advancements in processing methods, such as extrusion and enzymatic treatment, have enhanced their texture and solubility, making them suitable for a wider range of applications. These formats are gaining popularity in innovative product categories, positioning them as significant contributors to market expansion despite their smaller current market share.

By Category: Conventional Dominance, Organic Niche Gaining Ground

Conventional soy protein held the largest share of the North America market in 2025, accounting for 83.77% of the total market. This dominance is attributed to its widespread availability and cost-effectiveness. The extensive cultivation of genetically modified, herbicide-tolerant soybeans, combined with a well-established processing infrastructure in the United States Midwest, ensures consistent production and stable pricing. These factors make conventional soy protein a preferred choice for large-scale applications in food, animal feed, and industrial products, where affordability and reliability are key priorities.

Organic soy protein, although a smaller share of the market, is expected to grow faster, with a projected CAGR of 5.41% through 2031. This growth is driven by rising consumer demand for clean-label, non-GMO, and hexane-free products, particularly in premium segments such as infant nutrition and health-focused foods. The trust associated with the United States Department of Agriculture organic certification further boosts its appeal. While higher production costs limit its adoption in mainstream markets, organic soy protein is steadily gaining popularity in niche and specialty channels that prioritize health and sustainability.

By End User: Food and Beverages Prevail, Supplements Outpace

In 2025, food and beverage manufacturers accounted for the largest share of the North America soy protein market, holding 54.75% of the total market. This dominance is driven by the extensive use of soy protein in products like bakery items, meat alternatives, beverages, and packaged foods. Soy protein is highly valued for its ability to improve texture, act as an emulsifier, and enhance protein content in food products. Its consistent availability and cost-effectiveness make it a preferred choice for large-scale food production. With the growing trend toward plant-based diets, this segment remains the main driver of market growth.

On the other hand, the nutritional supplements segment is expected to grow at the fastest rate, with a projected CAGR of 6.24% through 2031. This growth is fueled by the increasing popularity of soy protein among sports and active-nutrition brands, driven by its complete amino acid profile and affordability compared to whey protein. The rising demand for ready-to-drink protein shakes and blended powders is also boosting this segment. As more consumers, beyond professional athletes, adopt performance nutrition products, soy protein is becoming a key ingredient in supplement formulations, catering to a broader audience.

Geography Analysis

The United States was the largest contributor to the North America soy protein market in 2025, holding a significant 92.48% market share. This dominance is due to its advanced soybean processing facilities and a strong food and nutrition manufacturing industry. The country benefits from a well-connected supply chain that links soybean farming, processing, and ingredient production, ensuring a steady supply of soy protein. Institutions like schools, hospitals, and public food programs also play a major role in driving domestic demand. Leading agribusiness companies are expanding their production capacities, further solidifying the United States' position in the soy protein market.

Canada is projected to grow at a 5.18% CAGR through 2031, making it the fastest-growing market in the region. The growing preference for non-GMO and identity-preserved soy proteins, especially in clean-label and premium nutrition products, is a key driver of this growth. Although regulatory and labeling requirements can be challenging, they also position Canada as a reliable supplier for brands serving both the domestic and the United States markets. Strong trade and manufacturing ties with the United States further support this growth, enabling Canada to expand its presence in the soy protein market steadily. This growth reflects the increasing demand for sustainable and high-quality protein options.

Mexico and other parts of North America are smaller but emerging markets for soy protein. Urbanization, the rising popularity of packaged foods, and the inclusion of soy protein in traditional and convenient meals are driving demand in these regions. Most of the demand is met through imports, creating strong trade relationships with United States' suppliers. As plant-based and cost-effective protein options gain traction among price-sensitive consumers, these markets offer new opportunities for growth. Regional trade agreements also help streamline the supply of raw materials and ingredients, supporting the long-term development of the soy protein market in these areas.

Competitive Landscape

The North American soy protein market is moderately consolidated, with large agribusiness companies such as Archer Daniels Midland Company, Cargill, and Bunge Ltd. controlling it. These companies dominate the market through extensive operations that include soybean crushing, refining, and protein isolation. Their vertical integration allows them to efficiently manage raw material sourcing, streamline production processes, and maintain stable pricing. Their large-scale operations enable them to secure long-term contracts with major food and nutrition manufacturers, creating significant barriers for new large-scale competitors to enter the market.

Smaller and mid-sized suppliers contribute to the market by focusing on specialized products rather than competing on volume. These companies target niche markets by offering organic, non-GMO, and allergen-managed soy proteins tailored for premium and regulated applications. They provide strong support in product formulation, ensure traceability, and comply with strict standards to build trust with their customers. Their agility allows them to quickly adapt to changing consumer demands, such as the growing preference for clean-label and sustainable products. However, their limited production scale makes it challenging for them to compete with larger players on price and capacity.

Innovation and diversification are playing an increasingly important role in shaping the soy protein market. Established companies are investing in advanced processing technologies, developing blended protein solutions, and exploring alternative plant-based proteins to reduce dependence on traditional soy products. These efforts aim to address consumer concerns about taste, allergens, and evolving preferences across various end-use markets. Emerging technologies like fermentation, though still in the early stages, show potential to disrupt the market in the future. Overall, companies with integrated operations, diverse product offerings, and effective cost management are better positioned to thrive in this competitive environment.

North America Soy Protein Industry Leaders

-

Archer Daniels Midland Company

-

Bunge Limited

-

Cargill Incorporated

-

Kerry Group plc

-

CHS Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Alpine Bio, a startup known for engineering soybeans to produce casein proteins, extended its technology to produce lactoferrin with 3.5x more iron than bovine sources and developed an “insanely soluble” soy protein isolate from non-GMO soybeans.

- May 2025: Bunge introduced a new line of soy protein concentrates at IFFA, which was set to launch in the fall. These concentrates were designed to address common challenges in the plant-based protein sector, offering a clean taste, neutral color, and cost-effective solution for food manufacturers.

- May 2025: Bunge announced a USD 550 million investment. This investment included a significant expansion of its production facilities to increase capacity and meet the growing demand for plant-based protein products.

- March 2025: The Ontario-based company, New Protein International, aimed to transform the industry by planning to build Canada’s first large-scale facility to domestically process soybeans into soy protein. This initiative marked a significant step toward reducing reliance on imports and strengthening the local supply chain for soy protein production.

North America Soy Protein Market Report Scope

The North American soy protein market is segmented by form, category, end user, and country. Based on form, the market is classified into soy protein concentrates, soy protein isolates, and soy protein textured/hydrolyzed. Based on category, the market is classified into organic and conventional. Based on end user, the market is classified into animal feed, food and beverages, and nutritional supplements. Based on country, the market covers Canada, Mexico, the United States, and the Rest of North America. The market forecasts are provided in terms of value (USD) and volume (Tons).

By Form

| Soy Protein Concentrates |

| Soy Protein Isolates |

| Soy Protein Textured/Hydrolized |

By Category

| Organic |

| Conventional |

By End User

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternatives Products | |

| Meat/Poultry/Seafood and Meat Alternatives Products | |

| RTE/RTC/ Food Products | |

| Snacks | |

| Nutritional Supplements | Baby and Infant Formula |

| Elderly and Medical Nutrition | |

| Sports/Performance Nutrition |

By Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Form | Soy Protein Concentrates | |

| Soy Protein Isolates | ||

| Soy Protein Textured/Hydrolized | ||

| By Category | Organic | |

| Conventional | ||

| By End User | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternatives Products | ||

| Meat/Poultry/Seafood and Meat Alternatives Products | ||

| RTE/RTC/ Food Products | ||

| Snacks | ||

| Nutritional Supplements | Baby and Infant Formula | |

| Elderly and Medical Nutrition | ||

| Sports/Performance Nutrition | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms