North America Potato Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

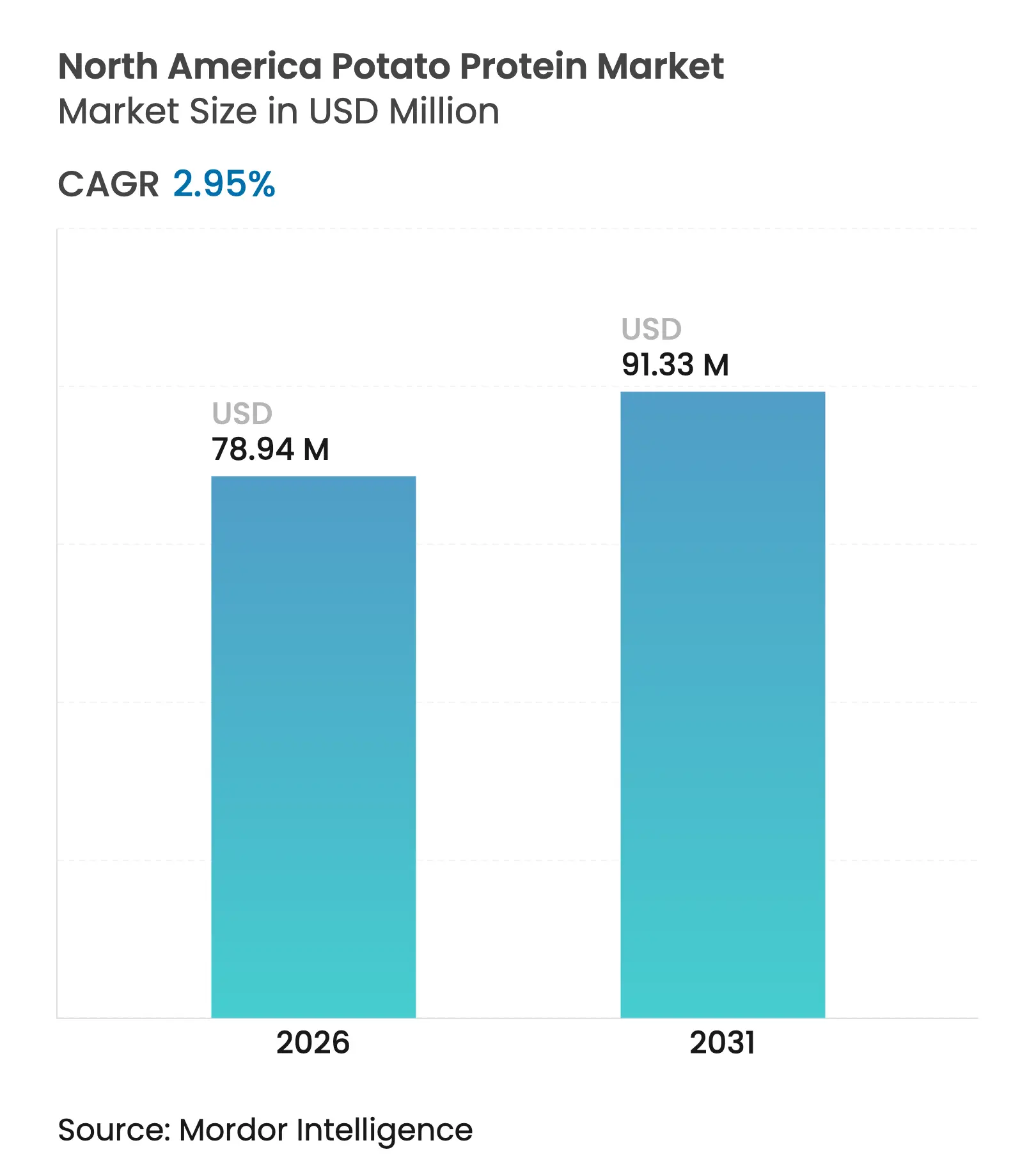

| Market Size (2026) | USD 78.94 Million |

| Market Size (2031) | USD 91.33 Million |

| Growth Rate (2026 - 2031) | 2.95 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Potato Protein Market Analysis by Mordor Intelligence

The North American potato protein market size is expected to grow from USD 76.68 million in 2025 to USD 78.94 million in 2026 and is forecast to reach USD 91.33 million by 2031 at 2.95% CAGR over 2026-2031. The market growth stems from improved extraction efficiency, premium product positioning, and clear regulatory frameworks rather than volume expansion. The market stability is maintained through concentrate formats and established processing partnerships, while technological advancements in cost management and functional improvements enable applications in higher-margin segments. The FDA's Generally Recognized as Safe (GRAS) framework and stricter labeling requirements strengthen potato protein's position as a clean-label substitute for whey, soy, and egg proteins. The market growth is driven by increased demand from premium pet food, aquafeed, gluten-free baking, and meat alternative sectors, where manufacturers optimize taste, texture, and cost-effectiveness. The industry is experiencing a fundamental transformation toward efficient, low-energy production systems through investments in molecular farming, enzyme-assisted extraction, and cell-culture technologies, helping protect profit margins against commodity price fluctuations.

Key Report Takeaways

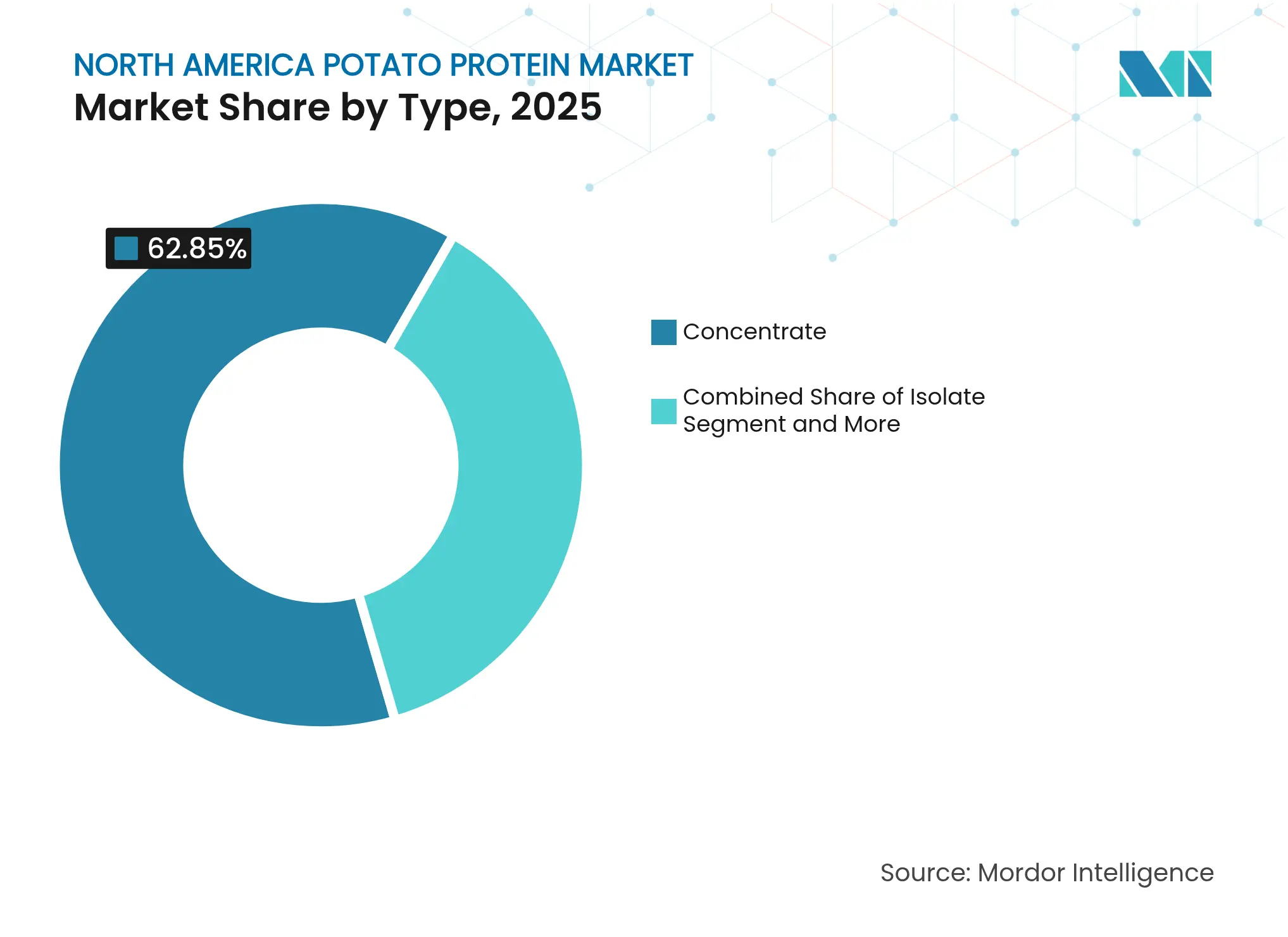

- By type, potato protein concentrates held 62.85% of market share in 2025, and hydrolyzed potato protein records the fastest growth, advancing at a 4.05% CAGR between 2026-2031.

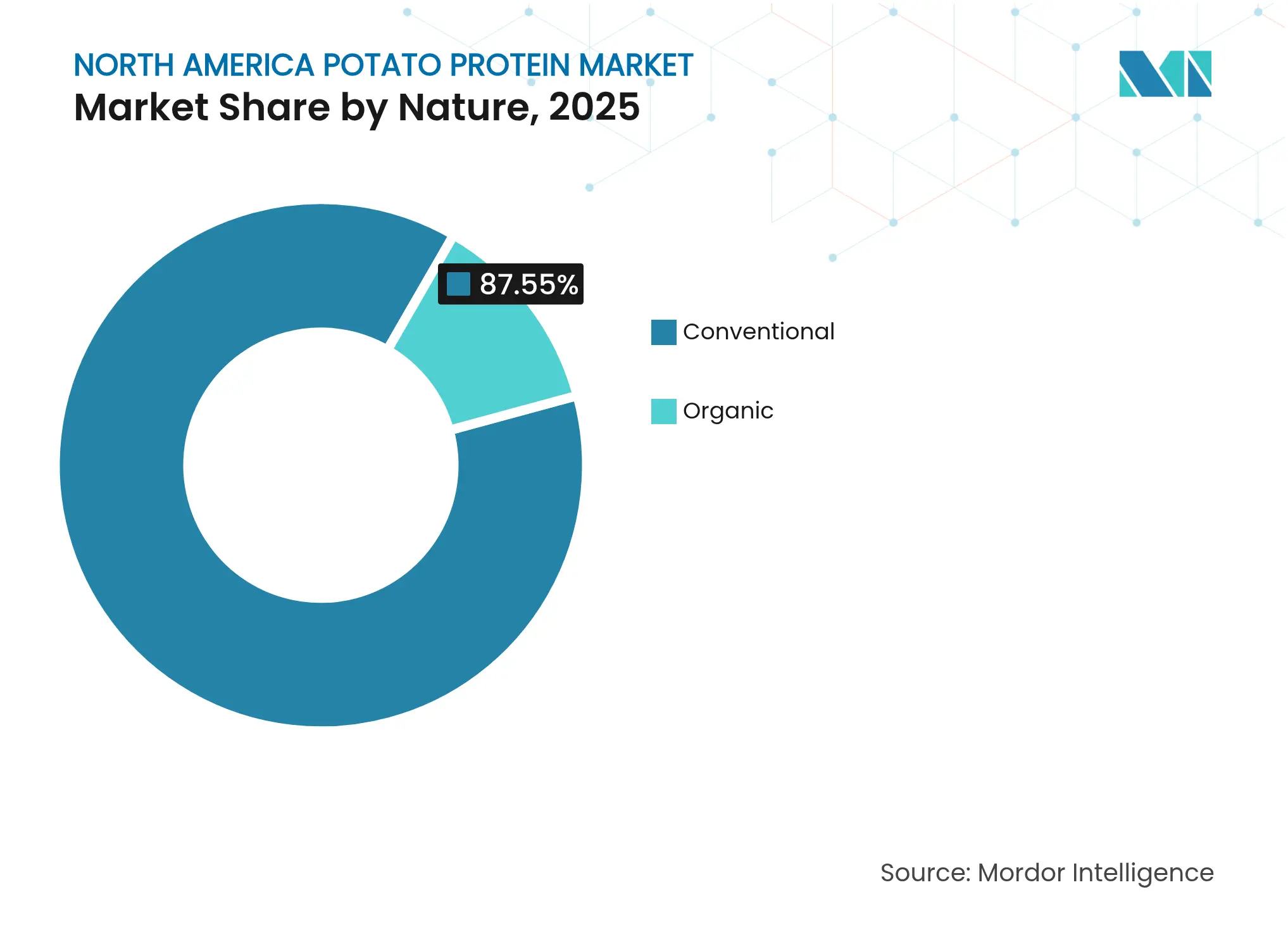

- By nature, the conventional segment captured 87.55% revenue share in 2025; organic formulations led growth at a 4.2% CAGR through 2031.

- By application, meat, poultry, seafood, and meat alternatives accounted for 77.05% of the market in 2025 and is also anticipated to progress at a 3.32% CAGR to 2031.

- By geography, the United States dominated with a 70.85% share in 2025, while Mexico posted the quickest 3.45% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Potato Protein Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Accelerated shift of processors toward clean-label proteins Accelerated shift of processors toward clean-label proteins | +0.8% | United States and Canada | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:United States and Canada | Impact Timeline:Medium term (2-4 years) |

Surging demand for non-allergenic gluten-free ingredients Surging demand for non-allergenic gluten-free ingredients | +0.6% | North America | Short term (≤ 2 years) | |||

Expansion of aquafeed production and animal feed and pet food industries Expansion of aquafeed production and animal feed and pet food industries | +0.5% | United States and Mexico | Long term (≥ 4 years) | |||

Advancements in protein extraction and processing technologies Advancements in protein extraction and processing technologies | +0.4% | United States and Canada | Medium term (2-4 years) | |||

Growing demand for plant-based proteins Growing demand for plant-based proteins | +0.3% | North America | Short term (≤ 2 years) | |||

Rising availability and e-commerce growth Rising availability and e-commerce growth | +0.2% | United States and Canada | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Accelerated Shift of Processors toward Clean-Label Proteins

Food processors are prioritizing ingredient transparency as consumers increasingly scrutinize synthetic additives and processing aids. Potato protein offers advantages in clean-label formulations due to its minimal processing requirements and recognizable source, particularly in meat alternatives and dairy analogues. The FDA's GRAS approvals for plant proteins, including pea protein fermented by shiitake mycelia, indicate regulatory support for protein processing methods that maintain clean-label status. Manufacturers use potato protein's neutral taste profile to replace synthetic emulsifiers and stabilizers. Processing companies report higher demand for potato protein concentrates in premium food applications due to formulation flexibility and consumer acceptance. The clean-label trend drives adoption in organic and natural product categories, where potato protein's non-GMO status and low allergenicity support premium positioning.

Surging Demand for Non-Allergenic Gluten-Free Ingredients

The rising prevalence of celiac disease and increased awareness of gluten sensitivity create consistent demand for alternative protein sources in gluten-free formulations. Potato protein offers a complete amino acid profile and strong binding properties, making it essential in gluten-free baking where wheat proteins are unsuitable. Its emulsification and foaming properties help improve texture in gluten-free products, addressing quality issues in this segment. Patent developments, such as VEG OF LUND AB's potato-based emulsion technology, showcase advancements in texture enhancement for gluten-free applications. Food manufacturers now incorporate potato protein in gluten-free formulations to match the texture of conventional products. This adoption extends beyond traditional gluten-free products as manufacturers reformulate to appeal to flexitarian consumers seeking simpler ingredients.

Expansion of Aquafeed Production and Animal Feed and Pet Food Industries

The aquaculture industry's expansion increases the demand for sustainable protein alternatives to fish meal, with potato protein emerging as a viable option in fish feed. The protein's digestibility and amino acid profile make it suitable for aquafeed formulations, particularly in freshwater species where marine-derived proteins demonstrate lower effectiveness. In the pet food segment, the trend toward premium products has increased the use of potato protein due to its hypoallergenic qualities. This market development is exemplified by Royal Avebe's collaboration with IQI to introduce ProtaSTAR, an ingredient containing 80% protein content, specifically developed for vegan and grain-free pet food formulations[1]Source: Pet Food Industry, “ProtaSTAR Launch,” petfoodindustry.com.

Advancements in Protein Extraction and Processing Technologies

Advances in protein extraction technology improve yield efficiency and functional properties while reducing production costs and expanding applications across food, pharmaceutical, and industrial sectors. The enhanced extraction methods enable better protein isolation, increased purity levels, and optimized processing conditions. PoLoPo, a biotechnology company, has submitted its SuperAA platform potato plant to the U.S. Department of Agriculture for regulatory approval, demonstrating progress in molecular farming techniques for protein production. This development signals a shift toward more sustainable and efficient protein manufacturing methods, potentially addressing growing global protein demands through innovative agricultural solutions [2]Source: Protein Report, “PoLoPo’s SuperAA Potato Platform,” proteinreport.org.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High production costs High production costs | -0.7% | North America | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.7% | Geographic Relevance:North America | Impact Timeline:Short term (≤ 2 years) |

Taste, texture, and sensory challenges Taste, texture, and sensory challenges | -0.5% | United States and Canada | Medium term (2-4 years) | |||

Availability of alternative high proteins Availability of alternative high proteins | -0.4% | North America | Medium term (2-4 years) | |||

Presence of low protein content Presence of low protein content | -0.3% | United States and Canada | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Production Costs

The production costs of potato protein remain high compared to established plant proteins such as soy and pea. The protein extraction process from potato processing streams requires specialized equipment, resulting in high capital investments that restrict new market entrants and limit pricing flexibility. The complex extraction technology and processing methods further add to operational expenses, making economies of scale difficult to achieve. Manufacturers of alternative proteins indicate that their production costs continue to exceed conventional meat prices by 30-50%, making it difficult to achieve price parity. Additionally, the energy-intensive nature of potato protein extraction and the need for continuous equipment maintenance contribute to elevated production costs, impacting overall market competitiveness [3]Source: D. Foth, “Energy Costs and Protein Isolation,” Food Engineering, foodengineeringmag.com.

Taste, Texture, and Sensory Challenges

Taste and texture optimization continues to limit wider adoption of potato protein, especially in consumer products where sensory attributes influence purchasing behavior. Although potato protein demonstrates strong functional characteristics compared to other protein sources, achieving desired taste and texture profiles in final products requires significant formulation development and additional ingredients, leading to higher production costs. Food manufacturers indicate that consumer acceptance depends mainly on taste, with functional benefits being less important than sensory qualities. The challenges in sensory optimization include managing the distinct earthy notes inherent to potato protein, addressing potential astringency issues, and ensuring smooth mouthfeel in various food applications. Additionally, the interaction between potato protein and other ingredients can affect the overall flavor profile, requiring careful consideration during product development. Recent advancements in processing technologies and flavor masking agents have shown promise in improving the sensory attributes, but these solutions often add complexity to the manufacturing process and increase the final product cost [4]Source: Netherlands Enterprise Agency, “Consumer Acceptance of Plant Proteins,” rvo.nl.

Segment Analysis

By Type: Concentrate Dominance Drives Market Stability

Concentrates accounted for 62.85% of the North American potato protein market share in 2025. Their popularity stems from providing a cost-effective balance of functional properties, including emulsification, water binding, and foaming capabilities. These attributes drive their consistent use in plant-based meat alternatives, bakery products, and instant soups. The steady supply of potato raw materials through integrated starch processors ensures reliable concentrate production.

Hydrolyzed potato proteins are projected to grow at a CAGR of 4.05% through 2031. This growth is driven by food manufacturers, nutraceutical companies, and geriatric nutrition providers seeking products with enhanced absorption rates and reduced allergenicity. The enzymatic hydrolysis process improves digestibility, expanding applications in sports beverages and medical nutrition. While isolates maintain a presence in specialized performance products requiring high protein density, their production remains constrained by high capital requirements. The market structure continues to rely on concentrates for volume sales, with hydrolysates capturing premium market segments.

Note: Segment shares of all individual segments available upon report purchase

By Application: Meat Alternatives Lead While Animal Nutrition Diversifies

The meat and poultry alternatives segment accounts for 77.05% of the North American potato protein market in 2025. This dominance stems from the protein's emulsification properties that provide fibrous texture and moisture retention in plant-based burgers, nuggets, and deli slices. The ingredient's neutral flavor profile and allergen-free characteristics appeal to flexitarian consumers, contributing to a steady 3.32% CAGR through 2031.

The animal nutrition segment, particularly premium pet food and freshwater aquafeed, shows the highest growth potential. ProtaSTAR, with its 80% protein content and hypoallergenic properties, meets the requirements for grain-free and limited-ingredient pet food formulations. Aquaculture farmers, specifically in trout and tilapia production, use potato protein to decrease dependence on marine-based feeds. Additional applications in sports nutrition powders, gluten-free baked goods, and ready-to-mix beverages further strengthen the North American potato protein market demand.

By Nature: Conventional Leadership Faces Organic Pressure

Conventional products account for 87.55% of the North American potato protein market in 2025, supported by established infrastructure and lower certification requirements. Conventional grades remain prevalent in industrial food applications where cost considerations take precedence over certification labels. The organic segment is growing at a 4.2% CAGR, driven by increased incorporation into premium snacks, baby foods, and dairy alternatives, alongside expanding retail private label offerings.

The organic potato protein supply remains constrained by limited certified farm acreage in the United States and Canada. However, higher price premiums support investments in dedicated segregation and traceability systems by specialty processors. Conventional manufacturers are developing organic conversion programs to prepare for potential changes in retailer requirements, indicating a gradual shift in market composition.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America maintains its position as the global leader in the potato protein market through its sophisticated food processing infrastructure and well-established supply chains. These supply networks efficiently connect potato production regions with protein extraction facilities, ensuring consistent supply and quality. The United States demonstrates its market dominance with a substantial 70.85% market share in 2025, achieved through its comprehensive integration of agricultural operations and processing systems that maximize protein recovery from potato starch operations.

Canada's strong market presence stems from its strategic location near major potato-growing regions and robust trade relationships that enable smooth cross-border ingredient movement. Meanwhile, Mexico emerges as the region's growth champion with a projected 3.45% CAGR through 2031, as its food processing capabilities expand and consumers increasingly embrace plant-based protein ingredients across both traditional and modern food applications.

The strength of North America's potato protein market is further reinforced by cohesive regulatory frameworks that promote market development through standardized food safety protocols and streamlined ingredient approval processes. The Canadian Food Inspection Agency's Safe Food for Canadians Regulations offers comprehensive guidance for both potato protein imports and domestic production, fostering seamless trade integration throughout North American markets . Mexican regulatory authorities have aligned their food safety standards with broader North American practices, creating an environment conducive to ingredient trade and encouraging investment in domestic processing capabilities. This harmonized approach within the North American food system facilitates the efficient movement of potato protein ingredients across diverse application categories and geographic markets, supporting continued market growth and development.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

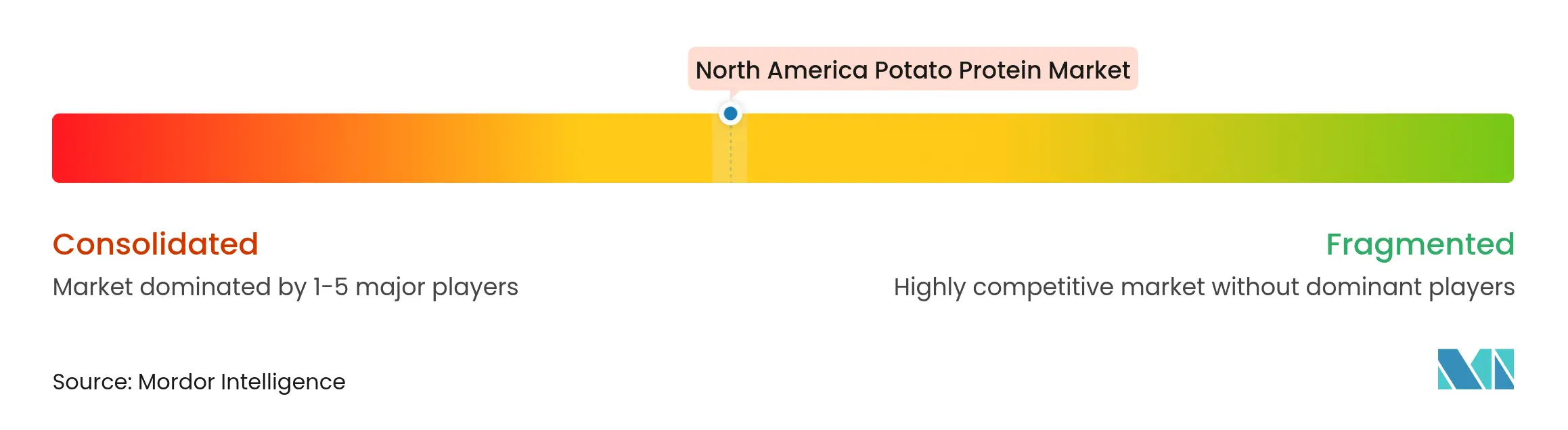

Market Concentration

The market shows moderate consolidation, with established European processors maintaining technological leadership through integrated starch and protein operations. Companies compete primarily through processing efficiency, functional property optimization, and application-specific product development rather than commodity pricing. Major players benefit from vertical integration, controlling potato sourcing, starch production, and protein extraction within unified operations to optimize costs and maintain quality consistency. Companies focus on specialized applications where potato protein's functional properties support premium positioning compared to other plant proteins.

Companies gain competitive advantages through technology deployment, investing in extraction efficiency improvements and new processing methods to enhance protein yield and functional characteristics. Patent activities highlight the industry's innovation focus, as demonstrated by VEG OF LUND AB's potato emulsion technology, which optimizes protein functionality for specific applications.

The market favors companies with diverse protein portfolios that can optimize formulations across multiple plant protein sources, reducing reliance on single ingredients. Emerging biotechnology approaches, including cellular agriculture and molecular farming, present potential disruption opportunities. These new production methods could improve cost efficiency and scalability compared to traditional extraction processes.

North America Potato Protein Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: ROQUETTE FRERES has launched two specialized potato proteins: TUBERMINE FV and TUBERMINE GP. These versatile products cater to a wide array of industries, from animal feed to niche industrial processes

- February 2024: Emsland Group invested in potato processing infrastructure by adding potato washing and grinding stations and expanding capacity for food-grade potato and pea fibers. This expansion increased the company's production capabilities for specialty ingredients.

- February 2024: Avebe launched their next-generation potato proteins, PerfectaSOL S 200 and S 300. The company collaborates with ingredient suppliers and equipment manufacturers to develop high-quality food product concepts.

Table of Contents for North America Potato Protein Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Accelerated Shift of Processors toward Clean-Label Proteins

- 4.2.2Surging Demand for Non-Allergenic Gluten-Free Ingredients

- 4.2.3Expansion of Aquafeed Production and Animal Feed and Pet Food Industries

- 4.2.4Advancements in Protein Extraction and Processing Technologies

- 4.2.5Growing Demand for Plant-Based Proteins

- 4.2.6Rising Availability and E-Commerce Growth

- 4.3Market Restraints

- 4.3.1Presence of Low Protein Content

- 4.3.2High Production Costs

- 4.3.3Availability of Alternative High Proteins

- 4.3.4Taste, Texture, and Sensory Challenges

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Advancements

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers/Consumers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Type

- 5.1.1Concentrate

- 5.1.2Isolate

- 5.1.3Hydrolyzed

- 5.2By Nature

- 5.2.1Conventional

- 5.2.2Organic

- 5.3By Application

- 5.3.1Meat/Poultry/Seafood and Meat Alternative Products

- 5.3.2Animal Nutrition

- 5.3.2.1Animal Feed

- 5.3.2.2Pet Food

- 5.3.2.3Aquafeed

- 5.4By Geography

- 5.4.1United States

- 5.4.2Canada

- 5.4.3Mexico

- 5.4.4Rest of North America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1Royal Avebe

- 6.4.2Kerry Group plc

- 6.4.3Tereos Group

- 6.4.4Agridient B.V.

- 6.4.5Roquette Freres SA

- 6.4.6Meelunie B.V.

- 6.4.7Emsland Group

- 6.4.8KMC Ingredients

- 6.4.9Planture Group

- 6.4.10Sudstarke GmbH

- 6.4.11PPZ Niechlow Sp. z o.o.

- 6.4.12Lyckeby Starch AB

- 6.4.13Bioriginal Food & Science Corp.

- 6.4.14Idaho Pacific Holdings

- 6.4.15Kemin Industries, Inc.

- 6.4.16STDM Food and Beverage Private Limited

- 6.4.17RootExtracts Ltd

- 6.4.18Ingredion Inc.

- 6.4.19American Key Food Products (AKFP

- 6.4.20Solanic B.V.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

North America Potato Protein Market Report Scope

North America potato protein market is segmented by type, application, and geography. Based on type, the market is segmented into potato protein concentrate, potato protein isolate. The market by application, the market is segmented into beverages, snacks & bar, animal nutrition, and others. Further, the market by geography is studied into United States, Canada, Mexico, and Rest of North America.