North America Mosquito Repellent Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

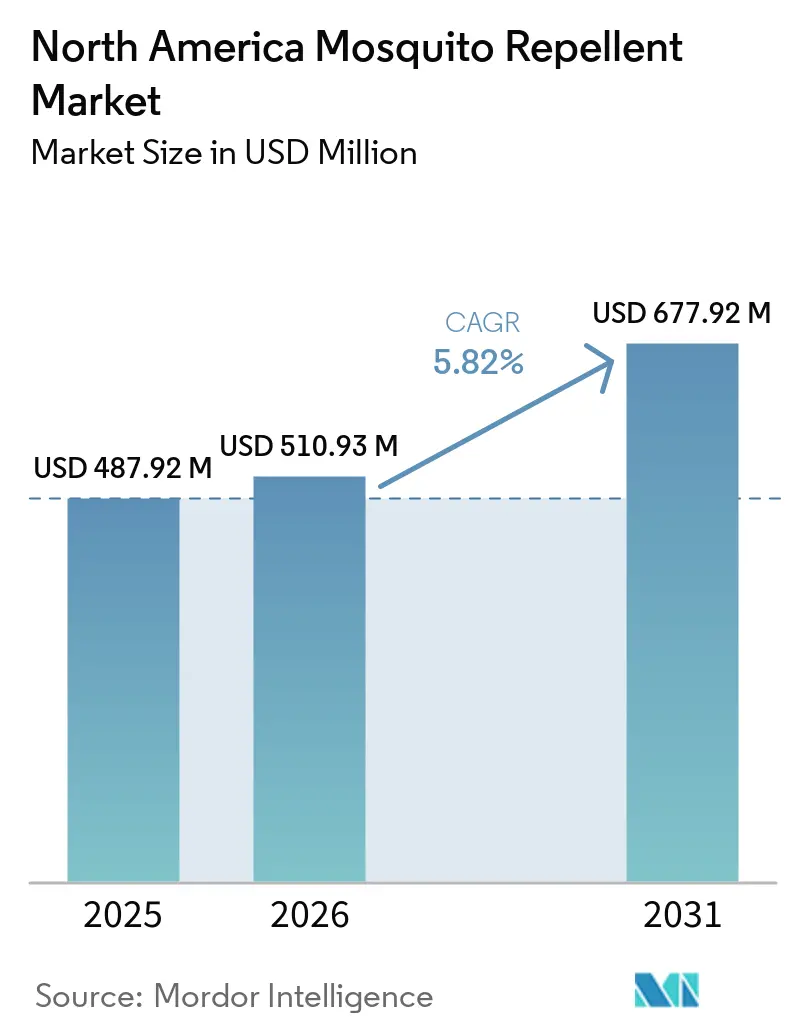

| Base Year Market Size (2025) | USD 487.92 Million |

| Market Size (2026) | USD 510.93 Million |

| Market Size (2031) | USD 677.92 Million |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

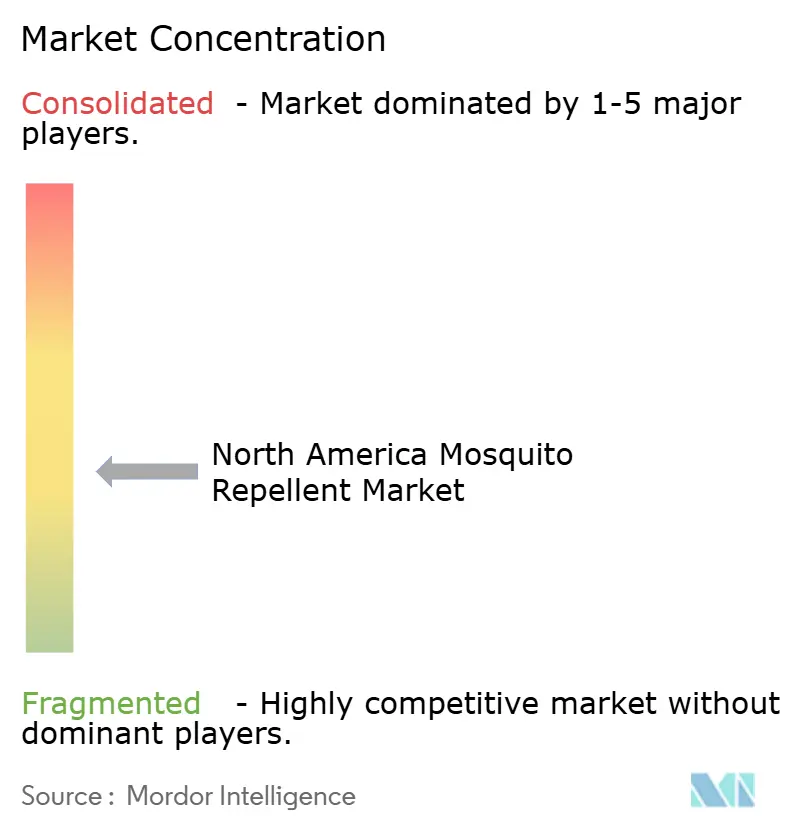

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Mosquito Repellent Market Analysis by Mordor Intelligence

The North America mosquito repellent market size is projected to expand from USD 487.9 million in 2025 and USD 510.9 million in 2026 to USD 677.9 million by 2031, registering a CAGR of 5.8% between 2026 and 2031. Demand in the North America mosquito repellent market is being supported by a sharper public focus on mosquito-borne disease risk, especially after the United States reported 3,798 dengue cases in 2024, far above the long-term annual average reported by the Centers for Disease Control and Prevention[1]Source: Centers for Disease Control and Prevention, “Dengue,” CDC, cdc.gov. The North America mosquito repellent market is also gaining from stronger outdoor participation, as 181.1 million Americans took part in outdoor recreation in 2024, which widened the number of regular use occasions for sprays, vaporizers, and zone protection products, according to the Outdoor Industry Association. Another layer of growth in the North America mosquito repellent market comes from premium product migration, where parents and sensitive-skin users are moving toward picaridin, oil of lemon eucalyptus, and other lower-perception-risk alternatives that sit outside the older DEET-led purchase pattern. The North America mosquito repellent market is further being reshaped by online retail, where direct-to-consumer discovery and reviews are helping newer brands shorten the path from trial to repeat purchase. Competition in the North America mosquito repellent market remains moderately consolidated, with larger players holding the strongest regulatory and retail positions, while tighter review standards in the United States and Canada continue to raise the operating threshold for smaller entrants.

Key Report Takeaways

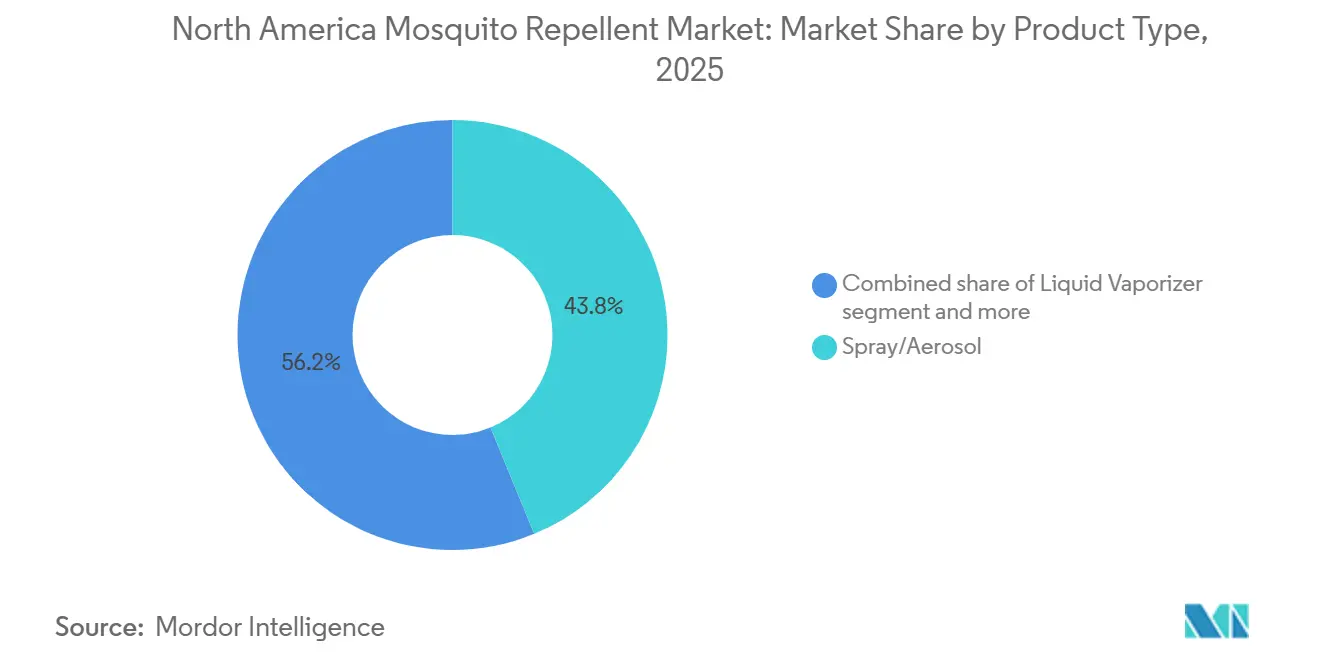

- By product type, Spray/Aerosol led with 43.8% share in 2025, while Liquid Vaporizer is projected to expand at 6.9% CAGR through 2031.

- By ingredient type, Conventional mosquito repellents held 82.7% of the North America mosquito repellent market share in 2025, while Natural mosquito repellents are forecast to grow at 6.8% CAGR through 2031.

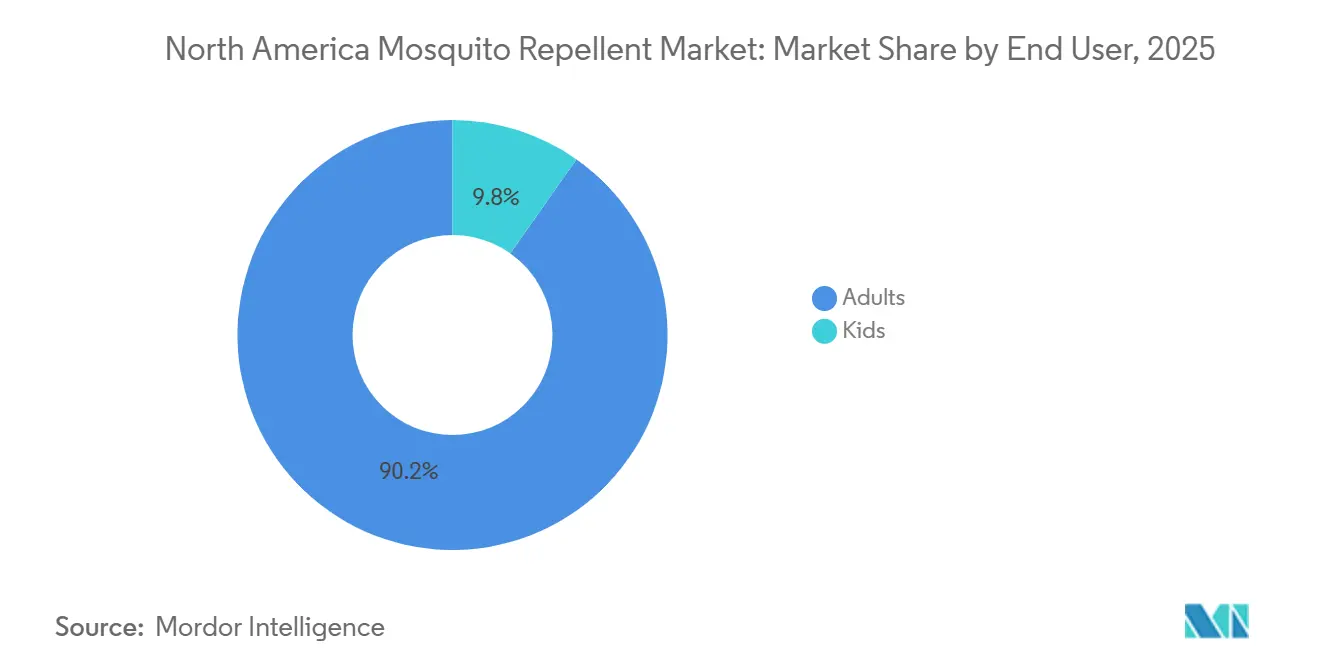

- By end user, Adults accounted for 90.2% of demand in 2025, while kids are expected to record the fastest growth at 7.1% CAGR through 2031.

- By distribution channel, Supermarkets and Hypermarkets held 43.1% of the North America mosquito repellent market size in 2025, while Online Retail Channels are projected to grow at 7.0% CAGR through 2031.

- By geography, the United States held 74.4% share of the regional market in 2025, while Mexico remained the fastest-growing country through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Mosquito Repellent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Mosquito-Borne Disease Awareness and Preventive Spend | +1.8% | The United States and Mexico are primary; spill-over to Canada | Short term (≤ 2 years) |

| Outdoor Recreation and Travel-Led Usage Peaks | +1.3% | North America-wide, led by the United States | Medium term (2–4 years) |

| Retail Premiumization Toward Natural and DEET-Free Formats | +0.9% | The United States and Canada core, expanding to Mexico | Medium term (2–4 years) |

| E-Commerce-Enabled Trial, Subscription, and Replenishment Behavior | +0.8% | North America-wide, strongest in the United States | Medium term (2–4 years) |

| Climate-Driven Season Extension in Southern North America | +0.7% | Northeast United States, Upper Midwest, Canada | Long term (≥ 4 years) |

| Higher Sensitivity to Skin-Compatibility and Family-Safe Claims | +0.5% | The United States, Canada, and primarily urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising mosquito-borne disease awareness and preventive spend

In North America, rising cases of vector-borne diseases are driving demand for insect repellents, keeping public health in the spotlight even during lulls between outbreaks. In 2024, the CDC reported 3,798 dengue cases across U.S. states and D.C., marking a staggering 359% surge from the 2010–2023 annual average. Florida, California, New York, and Texas were the primary hotspots, with ten counties in Florida confirming local transmissions. The U.S. Department of Health and Human Services, through its 2024 National Public Health Strategy, has spotlighted vector-borne diseases as a federal priority. This strategy promotes collaboration between the CDC and EPA, leading to widespread consumer education without the need for individual brand marketing. As the disease threat grows, there's a heightened institutional interest in spatial repellent technology, moving beyond traditional skin-applied formats. SC Johnson's Guardian, in August 2025, became the first spatial repellent to earn a WHO policy nod, hinting at a potential shift of this product category from public health channels to mainstream retail in North America. Moreover, school prevention campaigns and government travel advisories serve as free educational tools, broadening the market for insect repellents without added marketing costs.

Outdoor recreation and travel-led usage peaks

In 2024, outdoor recreation in North America generated a whopping USD 1.2 trillion in economic output, accounting for 2.3% of the GDP and supporting 5 million jobs, as reported by the US Bureau of Economic Analysis. This scale underscores the mainstream economic significance of outdoor recreation, moving it beyond its previously perceived niche status. According to the OIA's 2025 Participation Trends Report, the US outdoor participant base grew by 3% year-on-year, reaching 181.1 million Americans in 2024[2]Source: Outdoor Industry Association, “2025 Outdoor Participation Trends Report,” Outdoor Industry Association, outdoorindustry.org. Notably, hiking and camping each welcomed over 2 million new participants, serving as gateway activities that heighten exposure to mosquitoes and subsequently drive repellent purchases. KOA's 2026 Camping and Outdoor Hospitality Report highlighted that over 52 million North American households went camping in 2025. Outdoor hospitality spending surged to USD 66 billion, marking a USD 5 billion jump from 2024. This data confirms that the post-pandemic enthusiasm for outdoor activities hasn't waned to pre-2020 levels. Reflecting this family-oriented outdoor trend, the Kids end-user segment is projected to grow at a 7.12% CAGR through 2031. As families increasingly incorporate camping, hiking, and waterside recreation into their travel plans, the frequency and diversity of pediatric-specific repellent use occasions are expanding.

Retail premiumization toward natural and DEET-free formats

As consumers increasingly gravitate towards DEET-free and botanically derived formulations, competition at the premium tier intensifies. This shift is creating a clear divide: traditional volume leaders are finding themselves at odds with natural challengers, each catering to distinct customer segments. The EPA's current stance is noteworthy; it holds registrations for around 40 skin-applied repellent products based on picaridin, in addition to those using DEET and Oil of Lemon Eucalyptus (OLE). This regulatory endorsement not only bolsters the credibility of non-DEET ingredients but also expands the range of scientifically validated options for consumers. Advancements in microencapsulation and controlled-release technologies are bridging the efficacy divide. Actives like citronella, lemon eucalyptus, and lemongrass are closing the gap with synthetic DEET, diminishing the historical limitations on protection duration for natural formulations. In a telling move, Spectrum Brands is expanding its Repel Plant-Based line in 2025, introducing sustained-release spray formulations tailored for outdoor enthusiasts. This indicates that major players are starting to embrace the premium-natural segment, potentially shrinking the price premium that independent natural brands have enjoyed.

E-commerce-enabled trial, subscription, and replenishment behavior

Emerging insect repellent brands are finding their footing faster, thanks to the rise of online retail. This shift is particularly beneficial for natural startups and niche players, allowing them to attract customers without the hefty investment in shelf space, a privilege that has long shielded established brands from rapid product changes and direct profit margins. Brands like Murphy's Naturals and The Honest Company are leveraging subscription models, bundled products, and direct pricing strategies. These tactics help them stabilize the historically erratic seasonal demand of their category, leading to more consistent financial outcomes compared to traditional retail promotions. The online channel's projected 7.01% CAGR through 2031 mirrors broader trends in digital personal care commerce. Elements like consumer review platforms, algorithm-based natural product suggestions, and tools for ingredient comparisons are expediting both purchase choices and brand assessments, something traditional retail struggles to match on a large scale. In March 2025, Thermacell made waves by launching its E65 Rechargeable Repeller simultaneously on platforms like Amazon, Walmart, Target, REI, and Bass Pro. This move underscores how tech-savvy outdoor brands are now using online demand insights to clinch physical shelf space, flipping the traditional approach on its head. For established brands, this evolution signifies that online growth isn't just another sales channel; it's a transformative force reshaping how brands are discovered and evaluated by traditional buyers in the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety Perception Risks Around Synthetic Actives | -0.8% | The United States and Canada: urban demographics | Medium term (2–4 years) |

| Regulatory Friction for Novel Actives and Claims Substantiation | -0.5% | North America-wide, Canada is more restrictive | Long term (≥ 4 years) |

| Price Premium of Natural and Plant-Based Alternatives | -0.6% | The United States and Canada primary | Medium term (2–4 years) |

| Product Compliance and Efficacy Gaps in Low-Cost Imports | -0.4% | North America-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Safety perception risks around synthetic actives

Despite decades of endorsement from the EPA and Health Canada, DEET's safety narrative is losing ground, especially among parents of young children. These parents, who frequently apply repellents on their children's sensitive skin, are increasingly swayed by perception over evidence. A 2025 study in PubMed Central highlighted potential risks: it found epidemiological links between DEET exposure and negative impacts on sex hormones and bone mass in children and adolescents[3]Source: National Center for Biotechnology Information, “Study on DEET Exposure in Children and Adolescents,” PMC, ncbi.nlm.nih.gov. If these findings gain traction on a larger scale, they could prompt a push for pediatric reformulations and heighten safety concerns beyond the current evidence. Meanwhile, Health Canada, in its proposed re-evaluation decision PRVD2025-09 (October 2025), is advocating for updated DEET product labels. These include concentration guidelines for children, underscoring the scrutiny reshaping parental choices in repellent formulations. While conventional repellents held an 82.72% share of the ingredient segment in 2025, brand equity is being chipped away by perception risks. Premium retailers are increasingly favoring "clean" alternatives on their shelves, and online parenting communities are amplifying safety concerns, reaching audiences far beyond the study's epidemiological significance. Yet, there's a self-imposed limit: DEET's established effectiveness against Aedes aegypti and Culex pipiens in high-risk areas outshines most natural alternatives. However, this perception gap is poised to stifle growth rates in the conventional segment for the foreseeable future.

Regulatory friction for novel actives and claims substantiation

In North America, the journey for new active ingredients and delivery formats in the repellent market is both lengthy and costly. This regulatory maze is stifling the pace of innovation, even as consumer demand for novel formats surges. The EPA is contemplating a significant shift: potentially stripping personal mosquito and tick repellents of their minimum-risk pesticides exemption (as per 40 CFR 152.25(f)). Such a move would mandate full federal pesticide registration for botanical formulations that were once exempt. This registration process is not only time-consuming, spanning several years, but also demands a hefty compliance investment. Smaller brands, especially those focused on natural products, find it challenging to shoulder this burden. Similarly, Health Canada's Pest Management Regulatory Agency enforces PCPA-based registration for most repellent products. A proposed 2024 amendment to the Pest Control Products Regulations (noted in the Canada Gazette, June 2024) hints at a tightening of regulations, affecting both active ingredient approvals and end-product labeling standards. For major players with established pipelines, these compliance hurdles act as protective barriers. However, for newcomers in the natural market, especially those venturing into novel terpene-based or microencapsulated botanical actives, these regulations pose a significant challenge, hindering their growth beyond minimum-risk exemption thresholds. Consequently, this regulatory landscape is funneling commercially viable innovation towards firms capable of spreading the regulatory costs over larger sales, intensifying consolidation pressures and curtailing the influx of genuinely novel products in the market over the coming years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spray/Aerosol Leads but Vaporizers Reshape Indoor Protection

In 2025, the Spray/Aerosol format held a 43.79% share of North America's mosquito repellent market, driven by consumer familiarity and multi-surface versatility. Active ingredients like DEET, picaridin, and IR3535, validated by EPA and Health Canada, further reinforce its dominance. The format excels in outdoor activities such as camping, hiking, and fishing, where ease of reapplication and high-concentration formulations for Aedes and Culex vectors strengthen its mass-market appeal. The Liquid Vaporizer is the fastest-growing product type, with a 6.96% CAGR through 2031, fueled by demand for contactless, odor-neutral protection in indoor and patio spaces. This shift from skin-applied formats creates distinct retail positioning and higher average selling prices. Coils remain relevant in outdoor and lower-income segments, particularly in Mexico, while Creams, Lotions, and Roll-ons gain traction as precision-application options for children and sensitive-skin users, offering reduced systemic absorption.

Thermacell's June 2026 launch of LIV 2.0, an EPA-registered system protecting up to 3,140 sq. ft. per hub against mosquitoes and no-see-ums, highlights the growing importance of technology-driven zone formats in premium outdoor and institutional markets. Patches and Wearables, though niche, are growing steadily, driven by demand for hands-free convenience among younger North Americans. Another trend to monitor is the rapid adoption of rechargeable zone devices in the US and Canada, which could accelerate the decline of coil demand. As smoke-free formats gain traction among urban-adjacent outdoor users, private-label coil suppliers may lag behind branded vaporizer players who are actively educating the market.

By Ingredient Type: Conventional Dominance Masks Natural Segment's Disruption Trajectory

Natural mosquito repellents are projected to grow at a 6.81% CAGR through 2031. This growth is outpacing the conventional formulations, which until recently enjoyed a stable and largely uncontested position. In 2025, conventional mosquito repellents commanded 82.72% of the ingredient-type segment. This dominance underscores the enduring consumer trust in DEET, picaridin, and IR3535. These ingredients boast multi-decade efficacy validation in high-exposure vector environments and enjoy dual registration status under both EPA and Health Canada frameworks. The divergent growth trajectories of the two segments can be attributed to a generational shift in ingredient transparency expectations. Millennial parents, for instance, are now scrutinizing repellent products through the same clean-label lens they apply to food and personal care. This has led them to favor EPA-approved botanical actives, such as Oil of Lemon Eucalyptus, and picaridin, which serve as a middle ground between fully synthetic and entirely botanical formulations.

In the naturals segment, the key takeaway isn't its current size but its rapid ascent in shelf-space within mass-market retail. This trend often signals mainstream adoption, a precursor to volume surges in consumer goods. A 2025 PMC study hinted at a potential link between DEET exposure and endocrine disruption markers in children. Should larger cohort studies validate this, it might spur a regulatory-driven reformulation mandate, propelling the growth of natural repellents beyond current projections. Moreover, advancements like the microencapsulation of citronella and lemon eucalyptus oil are narrowing the protection-duration gap with synthetic DEET. This progress empowers natural brands to compete in a wider array of outdoor and disease-risk scenarios, effectively addressing a core performance concern that has historically constrained their market reach.

By End User: Adults Anchor Volume While Kids Drive the Premiumization Wave

In 2025, adults dominated the market, accounting for 90.21% of total sales. This trend underscores the strong preference among working-age and senior outdoor enthusiasts, who not only make the majority of purchase decisions but also consume repellents more frequently. Formats tailored for adults, including high-concentration DEET aerosols, picaridin sprays, and zone repellers, are driving the market. These products, sold through established channels like pharmacies, grocery stores, and sporting-goods retailers, come at price points that reflect decades of market maturity. Meanwhile, the kids' segment is poised for growth, expanding at a 7.12% CAGR through 2031, outpacing all other end-user segments. This surge is fueled by parents' increasing demand for dermatologically tested formulations, either low in DEET or entirely DEET-free. Such formulations are specifically designed for children's unique skin barriers and their higher surface-area-to-body-mass ratios. Supporting this trend, the OIA's 2025 Participation Trends Report highlighted a 5.6% uptick in youth outdoor participation in 2024, further amplifying the demand for age-specific repellents.

Brands like Hello Bello and Murphy's Naturals are carving a niche at the intersection of pediatric and natural products. Their minimalist ingredient profiles are commanding significant price premiums over mainstream alternatives. This strategic positioning is beginning to squeeze the gross margins of established brands in the children's segment. Furthermore, the 7.12% CAGR for the kids' segment through 2031 hints at a deeper trend: children who grow accustomed to natural or DEET-free brands are likely to carry those preferences into adulthood. This creates a generational advantage for the naturals segment, a nuance that current market share data might overlook. Brand strategists, both from established and emerging players, might underestimate this cohort effect if they focus solely on present volumes rather than the future consumption trajectory.

By Distribution Channel: Supermarkets Sustain Volume but Online Channels Redefine Brand Trajectories

Online retail channels are projected to grow at a strong 7.01% CAGR through 2031, driven by direct-to-consumer models, subscription bundles, and algorithm-driven product discovery, reshaping brand-building for emerging natural products and tech-enabled repellent formats. In 2025, supermarkets and hypermarkets held 43.13% of the distribution landscape, leveraging high foot traffic, seasonal promotions, and ingrained consumer habits to position repellent products as impulse buys for outdoor preparations and summer supplies. Pharmacies and drug stores cater to specific consumer needs, offering pharmacist recommendations, travel-preparation purchases, and addressing pediatric queries. Convenience stores fulfill immediate needs, especially in regions with limited retail options. Outdoor specialty retailers like REI, Bass Pro, and Cabela's provide credibility to premium and high-performance formats, which mass grocery environments cannot replicate.

Thermacell's March 2025 launch of its E65 product across Amazon, Walmart, Target, REI, and Bass Pro highlights a shift in market dynamics. Tech-savvy outdoor brands now use online demand signals to secure shelf space in brick-and-mortar stores, challenging traditional market entry routes. Digital platforms' consumer review ecosystems have replaced the brand verification role of physical shelf positioning and in-store sampling, lowering the trial barrier for newcomers and sharpening distinctions between commodity and premium repellent products. This trend signals a gradual shift in retailer bargaining power. As direct-to-consumer brands expand subscriber bases and refine order frequency data, their negotiating leverage with traditional buyers strengthens. This could reduce promotional spending and reshape the economic landscape for established players in the latter half of the forecast period.

Geography Analysis

In 2025, the U.S. dominated the North American mosquito repellent market, claiming a substantial 74.4% share. This dominance is attributed to extensive retail coverage, a culture of outdoor activities, and heightened public awareness, bolstered by consistent disease surveillance and health messaging. According to the Outdoor Industry Association, 181.1 million Americans engaged in outdoor recreation in 2024, establishing a vast user base for personal sprays, zone devices, and family-oriented products. The U.S. market's credibility is further enhanced by a well-established EPA registration system, fostering trust in approved active ingredients and enabling major brands to maintain premium pricing. Consequently, product testing and launches, particularly for device-centric and lifestyle-oriented offerings, are predominantly centered in the U.S. within the North American mosquito repellent landscape.

Canada's role diverges; while it boasts a more stringent regulatory pathway for certain formulations, its demand base is comparatively smaller. Brands eyeing cross-border expansion face hurdles due to Health Canada’s PMRA framework, which sets distinct compliance benchmarks, potentially delaying product transfers from the U.S. to Canada. The 2025 proposed re-evaluation of DEET has shifted focus towards alternatives like picaridin and oil of lemon eucalyptus, especially for products aimed at children, where labeling standards are scrutinized. Thus, Canada tends to prefer products that not only demonstrate proven efficacy but also raise fewer concerns regarding repeated use on children.

Mexico is on track to be the fastest-growing market through 2031, with its demand driven more by everyday disease prevention than seasonal trends. In 2024, PAHO reported 558,846 confirmed dengue cases in Mexico, underscoring the household relevance of mosquito protection. While the government's 2025 efforts led to a notable drop in confirmed cases, the lingering disease presence ensures consistent preventive purchasing rather than sporadic spikes. Looking ahead, the World Mosquito Program anticipates a 40% increase in dengue infection rates in Mexico over the next half-century, signaling sustained demand for repellents. With a burgeoning middle class and improved retail access in secondary cities, there's a noticeable shift from traditional coils and home remedies to branded sprays and lotions, offering greater value per purchase in the North American mosquito repellent market.

Competitive Landscape

In North America, the mosquito repellent market is moderately consolidated. SC Johnson & Son, Spectrum Brands Holdings, and Thermacell Repellents dominate, each holding strong positions across mass, premium, and zone-protection formats. SC Johnson’s OFF! franchise, along with Spectrum Brands’ Repel and Cutter lines, enjoy robust placements. Their recognized brand equity, combined with extensive coverage in supermarkets, drug stores, and general merchandise outlets, bolsters their standing. Furthermore, their scale plays a pivotal role in navigating regulations. Larger players like SC Johnson and Spectrum Brands can distribute compliance costs across a broader range of products and markets, a feat more challenging for their smaller counterparts. This scalability grants them a significant edge, especially as the category faces intensified labeling and registration scrutiny in both the U.S. and Canada. Yet, the North American mosquito repellent market remains open. Newer brands are carving out niches, especially where ingredient preferences and novel formats take precedence over sheer volume.

In 2026, SC Johnson fortified its market position by launching OFF! Deep Woods MAX, strategically aligning it with a Major League Fishing sponsorship to emphasize its outdoor utility. Meanwhile, Thermacell charted a device-centric trajectory, debuting the E65 Rechargeable Repeller in March 2025, followed by the LIV 2.0 in June 2026. This approach fosters a refill-based ecosystem, encouraging repeat usage and minimizing shifts driven by promotions. Spectrum Brands, not to be outdone, expanded its premium natural segment with the 2025 launch of its Repel Plant-Based line. These strategic moves underscore a shift: major players are diversifying beyond traditional sprays, venturing into natural formulations, rechargeable systems, and targeting specific usage occasions.

Emerging as a formidable competitive layer are Murphy’s Naturals, Hello Bello, and The Honest Company. These brands are carving a niche in the natural and child-centric segments of North America's mosquito repellent market. While they haven't yet achieved the distribution scale of industry giants, their clear ingredient messaging and appeal to young families bolster their credibility as growth challengers. Thus, the market is evolving: while established leaders maintain the broadest shelf presence, these focused challengers are influencing premium growth and shaping consumer preferences.

North America Mosquito Repellent Industry Leaders

S. C. Johnson & Son, Inc.

Reckitt Benckiser Group plc

Spectrum Brands Holdings, Inc.

3M Company

The Coleman Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Thermacell Repellents launched LIV 2.0, an EPA-registered outdoor mosquito protection system covering up to 3,140 sq. ft. per hub with protection against mosquitoes and no-see-ums. Available through professional installers, LIV 2.0 targets backyards, commercial outdoor venues, resorts, and senior living facilities, extending Thermacell's addressable market substantially beyond personal-use zone devices.

- May 2026: SC Johnson, the U.S. Department of State, and the Global Fund announced a three-year public-private partnership to expand access to SC Johnson Guardian spatial repellent, targeting protection for over 60 million people across approximately 10 priority countries. The collaboration strengthens institutional credibility for spatial repellent technology and expands category awareness with potential implications for North American public health channels.

- March 2025: Thermacell launched the E65 Rechargeable Mosquito Repeller + Fast Charging Dock in the US, featuring 3× faster charging than the predecessor E55 and distributed simultaneously across Amazon, Walmart, Target, Sam's Club, REI, Bass Pro, Cabela's, and Academy Sports. The multi-channel debut positioned the E65 for full mass-market penetration ahead of peak mosquito season.

North America Mosquito Repellent Market Report Scope

A mosquito repellent is a chemical or natural substance applied to skin, clothing, or surfaces to deter mosquitoes from landing, biting, or feeding. The North America mosquito repellent market is segmented by product type, ingredient type, end user, distribution channel, and geography. By product type, the market is segmented into liquid vaporizer, coils, spray/aerosol, creams/lotions, patches, and other types. By Ingredient Type, the market is segmented into natural and conventional. By end user, the market is segmented into adults and kids. by distribution channel, the market is segmented into supermarkets, convenience stores, pharmacies, online retail, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Liquid Vaporizer |

| Coils |

| Spray/Aerosol |

| Creams, Lotions, and Roll-ons |

| Patches and Wearables |

| Other Product Types |

| Natural Mosquito Repellent |

| Conventional Mosquito Repellent |

| Adults |

| Kids |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Pharmacies and Drug Stores |

| Online Retail Channels |

| Other Distribution Channels |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Product Type | Liquid Vaporizer |

| Coils | |

| Spray/Aerosol | |

| Creams, Lotions, and Roll-ons | |

| Patches and Wearables | |

| Other Product Types | |

| Ingredient Type | Natural Mosquito Repellent |

| Conventional Mosquito Repellent | |

| End User | Adults |

| Kids | |

| Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Pharmacies and Drug Stores | |

| Online Retail Channels | |

| Other Distribution Channels | |

| Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North America mosquito repellent market in 2026?

The North America mosquito repellent market stands at USD 510.9 million in 2026 and is forecast to reach USD 677.9 million by 2031 at a 5.8% CAGR.

Which product type leads regional demand?

Spray/Aerosol is the largest product type, holding 43.8% share in 2025 because it fits outdoor, travel, and general household use across price points.

What is driving faster growth in natural formulations?

Natural mosquito repellents are growing at 6.8% CAGR through 2031 due to stronger demand from parents, sensitive-skin users, and shoppers who prefer clearer ingredient positioning.

Why is Mexico growing faster than the United States and Canada?

Mexico has a stronger everyday disease-prevention demand base, supported by high dengue case exposure and broader branded adoption as retail access improves.

Page last updated on: