Insect Repellent Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

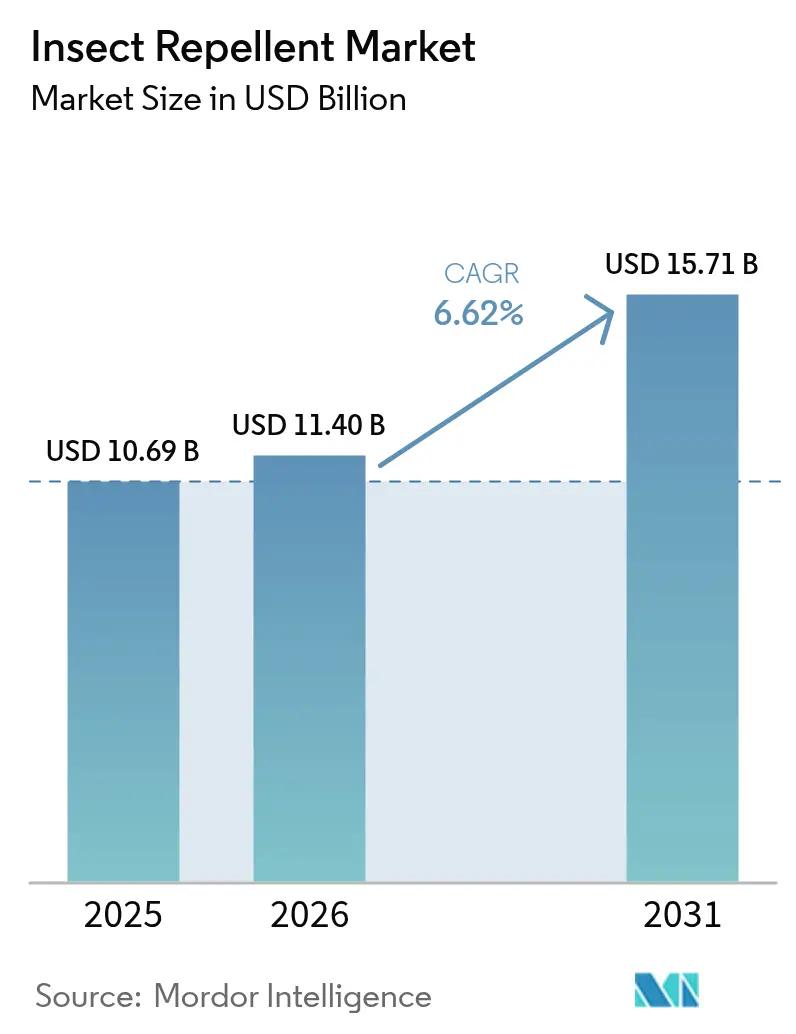

| Market Size (2026) | USD 11.4 Billion |

| Market Size (2031) | USD 15.71 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

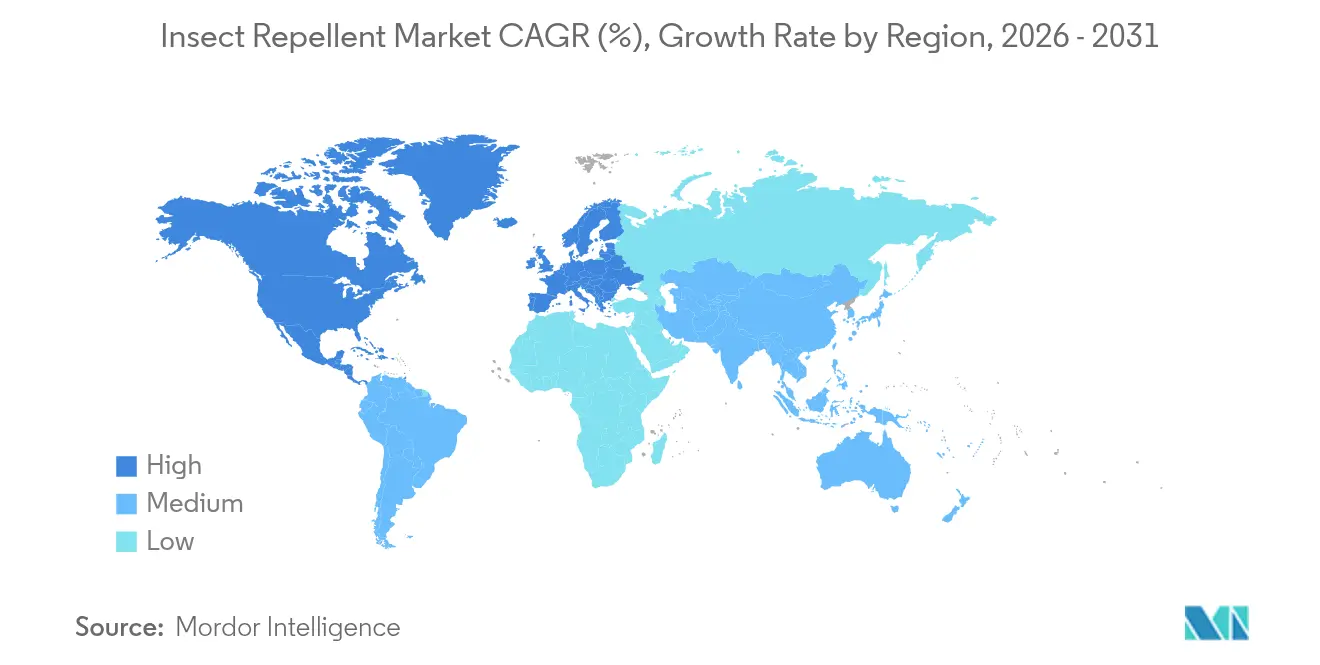

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Insect Repellent Market Analysis by Mordor Intelligence

Insect repellent market size in 2026 is estimated at USD 11.4 billion, growing from 2025 value of USD 10.69 billion with 2031 projections showing USD 15.71 billion, growing at 6.62% CAGR over 2026-2031. This growth trajectory is largely driven by escalating global apprehensions regarding vector-borne diseases, a burgeoning outdoor lifestyle, and ongoing innovations in delivery systems that enhance both protection and user convenience. The European Commission highlights Haiti and Brazil as the foremost nations at risk of vector-borne diseases in Latin America and the Caribbean. In 2025, these countries registered index scores of 8.9 and 8.8, respectively, for diseases like the Zika virus and Dengue fever[1]Source: European Commission, "INFORM Risk Mid Index 2025", www.commission.europa.eu. While Asia-Pacific continues to dominate as the primary regional hub, North America and Europe are witnessing a surge in demand, spurred by climate change's expansion of mosquito habitats. Although natural active ingredients and spatial formats are gaining popularity, traditional offerings like N, N-diethyl-meta-toluamide (DEET) and pyrethroids maintain their edge due to established efficacy and regulatory acceptance. Players in the market are focusing on research and development investments, seasonal promotions, and bolstering e-commerce presence, navigating the delicate balance between price sensitivity and the trend towards premiumization.

Key Report Takeaways

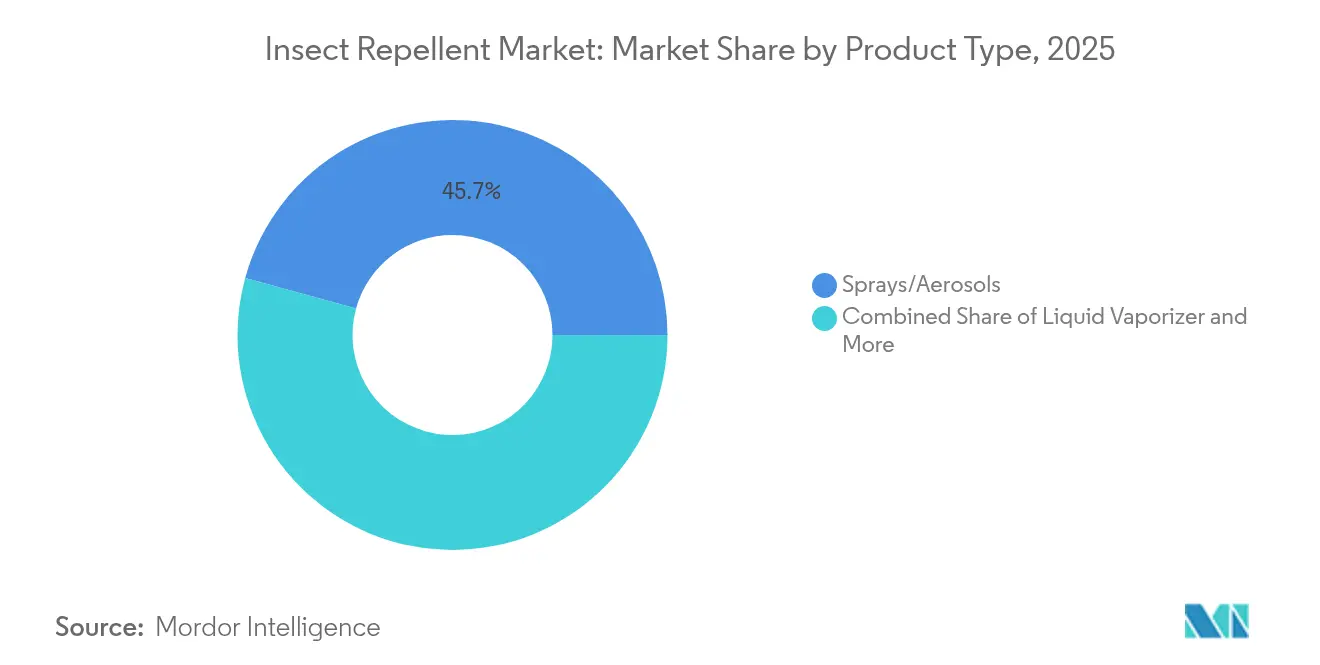

- By product type, sprays and aerosols held 45.72% of the insect repellent market share in 2025, and liquid vaporizers are projected to expand at a 7.32% CAGR through 2031.

- By ingredient, conventional actives captured 82.10% share of the insect repellent market size in 2025, while natural formulations recorded an 8.05% CAGR to 2031.

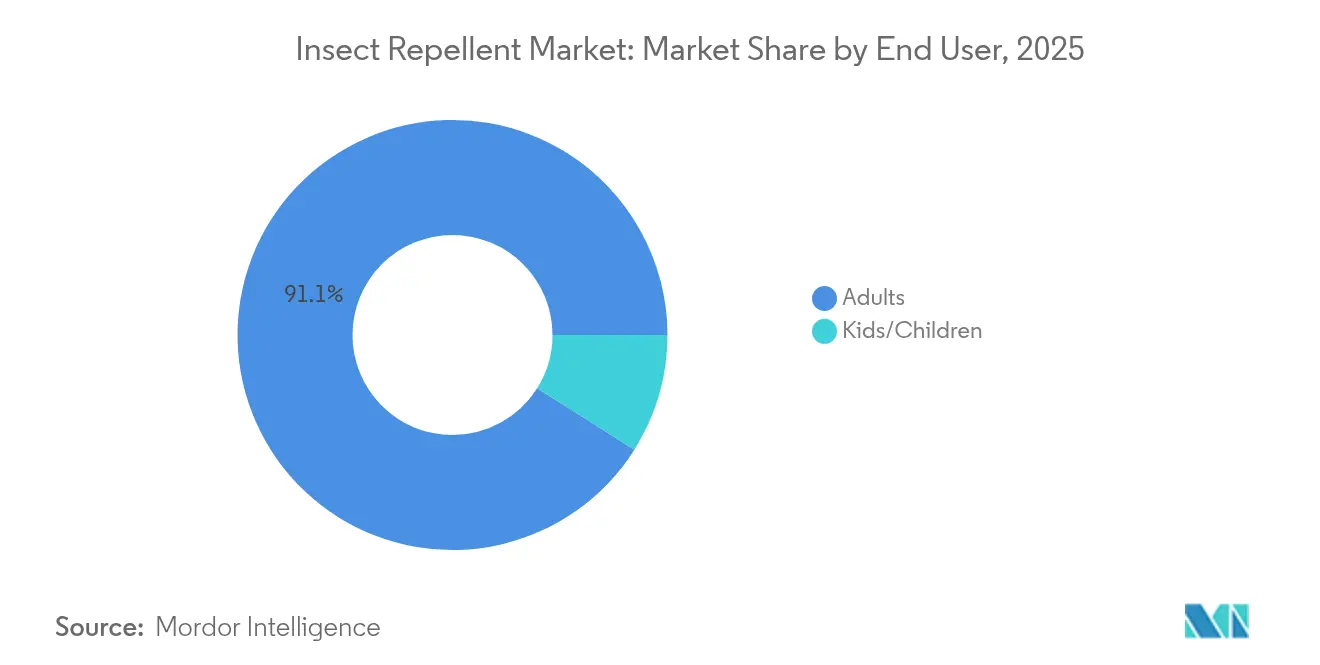

- By end user, adults commanded 91.05% of the insect repellent market share in 2025, and children’s products posted the fastest growth at an 7.95% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets led with 41.20% of the insect repellent market size in 2025, and online retail shows the highest forecast CAGR at 8.55% through 2031.

- Asia-Pacific accounted for 49.10% revenue share in 2025, and the region also registers the strongest regional CAGR at 9.15% during the period to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insect Repellent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Vector-borne Diseases | +1.8% | Global, with the highest impact in Asia-Pacific and Sub-Saharan Africa | Long term (≥ 4 years) |

| Increasing Outdoor Recreational Activities | +1.2% | North America and Europe core, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Growing Pet Ownership | +0.9% | North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Shifting Consumer Preferences Towards Natural Products | +1.4% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Rapid Technological Advancements Driving Innovation | +1.1% | Global, with research and development centers in North America, Europe, and Japan | Medium term (2-4 years) |

| Government and Public Health Campaigns | +0.8% | Global, with concentrated efforts in malaria-endemic regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in Vector-borne Diseases

Vector-borne diseases are on the rise worldwide. The World Health Organization (WHO) highlighted in its September 2024 factsheet that over 700,000 deaths occur annually due to diseases spread by mosquitoes, ticks, and other arthropods. Climate change is pushing vector habitats further north, bringing malaria and dengue threats to temperate regions that were once safe. According to the Centers for Disease Control and Prevention, in 2024, more than 13 million cases of dengue were reported in North, Central, and South America and the Caribbean. Dengue transmission in these areas remains high in 2025[2]Source: Centers for Disease Control and Prevention, "Current Dengue Outbreak", www.cdc.gov. This surge has led to a heightened demand for repellents in these newly at-risk areas. Furthermore, pyrethroid resistance in malaria vectors is now a global concern, affecting over 80% of monitored sites. This resistance is steering consumers towards alternative active ingredients and spurring innovation in new formulations. In response to these challenges, government health agencies are amplifying their recommendations for personal protective measures. Notably, the CDC has highlighted DEET, picaridin, and IR3535 as top choices for effective protection against disease vectors.

Increasing Outdoor Recreational Activities

In the wake of pandemic-induced lifestyle changes, outdoor recreation saw a notable uptick in participation. For example, the Outdoor Foundation reported that in 2024, over 63.4 million individuals in the U.S. engaged in hiking activities at least once[3]Source: Outdoor Foundation, "2025 Sports, Fitness, and Leisure Activities Topline Participation Report", www.sfia.users.membersuite.com. This marks the highest participation rate since 2010, showcasing a growth of approximately 31 percentage points over the past 15 years. As consumers increasingly incorporate pest protection into their recreational gear, sales in adventure tourism and outdoor sports equipment have seen a direct correlation with the growth of the repellent market. This trend isn't limited to traditional activities like camping and hiking; it now encompasses outdoor dining, festivals, and the use of urban green spaces, expanding the market's reach beyond just wilderness enthusiasts. Moreover, professional outdoor workers from sectors like construction, agriculture, and landscaping, often overlooked, are significantly boosting the demand for commercial-grade repellents.

Growing Pet Ownership

In 2024, the American Veterinary Medical Association highlighted a surge in pet ownership, noting that 45.5% of U.S. households now have dogs, while 32.1% own cats. This translates to a staggering 77 million dogs and 58 million cats across the nation. Responding to this trend, a new category of pet-specific repellent products has emerged. These products, often recommended by veterinarians, aim to prevent ticks and fleas, moving beyond the conventional spot-on treatments. Heightened awareness of zoonotic diseases, especially the transmission of Lyme disease via insects carried by pets, has spurred owners to adopt more comprehensive protection measures. This includes using environmental repellents in outdoor areas frequented by their pets. As pets increasingly become integral members of the family, there's a noticeable shift towards premium products. Pet owners are now more inclined to invest in specialized formulations, prioritizing safety and efficacy for their animals. Furthermore, the geographic spread of tick-borne diseases into areas that were once considered safe presents a lucrative opportunity for the market, paving the way for innovative pet-focused repellent solutions.

Shifting Consumer Preferences Towards Natural Products

Natural and botanical repellents are witnessing a surge in demand, projected to grow at a CAGR of 8.47% through 2030. This growth outpaces that of conventional alternatives, driven by consumers' increasing emphasis on ingredient transparency and environmental sustainability. Oil of lemon eucalyptus (OLE), which contains para-menthane-3,8-diol (PMD), has recently garnered regulatory attention. The Environmental Protection Agency (EPA) has granted it approval, recognizing its efficacy claims that rival those of DEET, especially against mosquitoes and ticks. Furthermore, research underscores the potency of essential oils. Peer-reviewed studies highlight the repellent activity of mentha aquatica essential oil against various vector species, bolstering the commercial viability of plant-based alternatives. Growing health concerns regarding synthetic pyrethroid exposure, especially among children and pregnant women, are steering market preferences towards botanical formulations. While these botanical options may offer a shorter protection duration, consumers are increasingly accepting premium pricing for natural products. This trend presents lucrative margin opportunities for manufacturers who are keen on investing in botanical ingredient research and sustainable sourcing practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Alternative Protection Methods | -0.8% | Global, with a higher impact in developed markets | Medium term (2-4 years) |

| Consumer Health Concerns Over Chemicals | -1.2% | North America and Europe primarily | Long term (≥ 4 years) |

| Insecticide Resistance | -0.6% | Global, concentrated in tropical regions | Long term (≥ 4 years) |

| Availability of Counterfeit Products | -0.4% | Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Alternative Protection Methods

Alternative protection technologies are increasingly encroaching on the traditional repellent market. Products like permethrin-treated clothing, bed nets, and electronic devices are drawing consumer interest, even as evidence of their efficacy remains mixed. Systematic reviews indicate that electronic mosquito repellents fail to offer measurable protection against mosquito landings. Yet, consumers continue to adopt them, swayed by their perceived convenience and the allure of being chemical-free. While permethrin-treated clothing boasts a longer protection duration than topical repellents, this advantage poses a substitution risk in the market, especially for outdoor professionals and military users. In residential settings, integrated pest management strategies, merging environmental tweaks, biological controls, and physical barriers, are diminishing the dependence on personal repellent products. Furthermore, the rise of smartphone apps touting ultrasonic repellent features, despite scientific evidence debunking their effectiveness, underscores a consumer trend: a willingness to explore alternative technologies, potentially postponing the shift away from traditional products.

Consumer Health Concerns Over Chemicals

As consumers become more aware of the health risks tied to synthetic repellent ingredients, products like DEET and pyrethroid-based formulations face mounting challenges. Studies from Ghana, China, and other regions have linked mosquito coil smoke exposure to respiratory symptoms and potential neurotoxic effects, shaping how consumers view chemical repellents. Regulatory bodies have intensified scrutiny, taking action against counterfeit and unregistered repellents that hide toxic ingredients, further fueling consumer doubts about product safety and ingredient transparency. Concerns over safety during pregnancy and for children have led to a market shift, with parents leaning towards chemical-free alternatives, even if they come with reduced efficacy. This trend opens doors for botanical products but also limits overall market expansion. Moreover, health concerns, often amplified on social media regardless of their scientific backing, sway purchasing choices and brand image. This dynamic pushes manufacturers to heavily invest in educating consumers and communicating safety measures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Vaporizers Drive Innovation

In 2025, sprays and aerosols command the market with a 45.72% share, capitalizing on their convenience, portability, and instant application appeal to a wide range of consumers. Meanwhile, liquid vaporizers are the fastest-growing segment, boasting a 7.32% CAGR through 2031. This surge is fueled by tech advancements in spatial protection and a consumer shift towards hands-free, continuous coverage. While coils hold their ground in price-sensitive markets, despite concerns over combustion byproducts, mats strike a balance between traditional coils and modern liquid systems. Bait products, tailored for integrated pest management, face growth challenges due to regulatory hurdles and complex applications.

Liquid vaporizers are reaping the rewards of patent innovations, especially in controlled-release mechanisms and volatile pyrethroid formulations. Notably, in July 2024, Godrej Consumer Products unveiled 'Renofluthrin', India's inaugural indigenous mosquito repellent molecule, tailored for liquid vaporizers. These advanced formulations promise 12-hour protection per cartridge, ensuring a steady release of active ingredients. This innovation meets consumer demands for prolonged efficacy, reducing the need for frequent reapplications. Emerging categories like wearable devices and electronic dispensers are weaving repellent delivery into everyday products, but their market presence is still modest, awaiting validation of efficacy and a drop in costs.

By Ingredient Type: Natural Alternatives Gain Momentum

In 2025, conventional insect repellents command an 82.10% market share, bolstered by decades of proven efficacy, regulatory endorsements, and a well-established manufacturing base for DEET, picaridin, and pyrethroid formulations. Meanwhile, natural insect repellents are on a growth trajectory, boasting an 8.05% CAGR through 2031. This surge is fueled by a rising consumer health consciousness and regulatory backing for botanical active ingredients, such as oil of lemon eucalyptus and various essential oil blends. The disparity in growth rates underscores a shift in consumer priorities: many now prefer shorter protection durations if it means enhanced safety and environmental sustainability.

Research underscores the efficacy of natural ingredients. For instance, PMD (para-menthane-3,8-diol) matches DEET's performance against major vector species, provided it's used in the right concentrations. Furthermore, advancements like nano-emulsion technologies bolster the stability and bioavailability of botanical ingredients. This innovation addresses the traditional challenges of plant-based repellents, such as swift degradation and variable efficacy. While there's a growing acceptance of premium pricing for natural products, hinting at potential margin expansions, challenges in sourcing botanical ingredients could temper swift market share growth.

By End User: Children's Segment Drives Safety Innovation

In 2025, adults account for a dominant 91.05% of end-user demand, underscoring their pivotal role in purchasing and utilizing products for personal, family, and professional needs. Meanwhile, the children's segment is poised to expand at a robust 7.95% CAGR through 2031. This growth is largely attributed to increased parental vigilance regarding vector-borne disease threats and a rising demand for formulations tailored for children, emphasizing heightened safety. Products designed for pediatric use come with features like reduced active ingredient concentrations, child-resistant packaging, and formulations that prioritize minimizing skin irritation and the risk of accidental ingestion.

Regulatory bodies are sharpening their focus, distinguishing between adult and pediatric product applications. Notably, the EPA, alongside global agencies, has rolled out specific guidelines for repellent usage, especially concerning children under 2 and pregnant women. Innovations in product development are steering towards delivery mechanisms that limit direct skin contact. This includes treatments for clothing and spatial repellents, which offer protection without the need for topical application. The push towards natural products in the children's segment is evident, with parents leaning towards botanical ingredients. Even if these ingredients offer a shorter duration of protection, it opens avenues for companies delving into research for child-safe formulations and adopting targeted marketing strategies.

By Distribution Channel: E-commerce Transforms Access

In 2025, supermarkets and hypermarkets command a 41.20% share of the distribution landscape, capitalizing on established consumer shopping habits, adept seasonal merchandising, and seizing impulse buying moments during peak mosquito seasons. Online retail stores, riding a wave of pandemic-induced e-commerce adoption, subscription models, and direct-to-consumer strategies that sidestep traditional retail margins, are projected to grow at an 8.55% CAGR through 2031. Convenience stores cater to immediate needs and serve regions with sparse retail options, while pharmacies and specialty outdoor retailers address distinct consumer segments.

The e-commerce boom empowers niche product distribution, enabling specialized natural and premium repellent brands to connect with their audience without the need for broad retail collaborations. Subscription services for repellent refills and seasonal items not only generate consistent revenue but also guarantee ongoing consumer protection. Digital platforms play a pivotal role in educating consumers on application methods, safety protocols, and product choices tailored to specific needs and regional risks. As online shopping gains traction, manufacturers are compelled to bolster their digital marketing and direct-to-consumer logistics, all while preserving ties with traditional retailers for products requiring immediate availability.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 49.10% of global revenue, and the region also registers the strongest regional CAGR at 9.15% during the period to 2031, primarily driven by the ongoing public health focus on dengue and malaria. Government-led awareness initiatives, bolstered by mass media campaigns, have significantly increased the adoption of repellents. A testament to local research and development capabilities, India's Goodknight Flash, featuring Renofluthrin, not only cuts down on import costs but also fortifies supply resilience. With rising disposable incomes, urban households are upgrading from traditional coils to liquid vaporizers, further expanding the regional insect repellent market.

North America, while trailing, boasts substantial figures, largely due to outdoor recreational activities and the spread of insect-borne diseases. In 2024, retail sales in the U.S. reached an impressive USD 376.9 million. The region's strong preference for botanical ingredients allows for premium pricing and higher margins for innovators. Additionally, climate change has lengthened the mosquito season in northern states, leading to a more consistent monthly demand for insect repellents, rather than the previously sharp summer peak.

Europe's growth is tempered by stringent chemical regulations, pushing the industry towards natural formulations that align with eco-toxicology standards. Germany and France are at the forefront, championing sustainability certifications and driving the adoption of recyclable packaging.

In the Middle East and Africa, donor-funded initiatives are bolstering distribution in malaria-prone areas, making repellents more accessible to lower-income communities.

Meanwhile, Latin America's urban sprawl into tropical regions is increasing contact with disease vectors, prompting a surge in diverse product offerings and investments in localized manufacturing.

Competitive Landscape

Top Companies in Insect Repellent Market

The market exhibits a moderate concentration level. Established brands like OFF!, Mortein, and Repel are deployed by incumbents such as S.C. Johnson, Reckitt, and Spectrum Brands. These players utilize omnichannel distribution agreements and heavily invest in advertising during peak mosquito seasons to maintain their shelf dominance.

Innovation sets competitors apart: Godrej Consumer Products introduced Renofluthrin, a locally developed molecule tailored for liquid vaporizers, showcasing regional initiatives to cultivate intellectual property and readiness for export. Meanwhile, U.S. startups are venturing into wearable devices, employing fan-driven diffusion techniques, and successfully drawing in crowdfunding and venture capital. Additionally, there's notable patent activity surrounding controlled-release matrices, indicating a strategy to prolong protection duration without the need for reapplication, appealing to consumers who value convenience over cost.

Digital sales strategies heighten competition. Reckitt partnered with AnyMind Group to oversee its e-commerce operations in Indonesia, customizing content for local languages and capitalizing on live-stream shopping. Subscription services are offering quarterly refills accompanied by educational materials, boosting purchase frequency and reducing churn. Furthermore, corporate social responsibility initiatives, such as donating repellents to disaster-stricken areas, not only enhance brand perception but also cultivate loyalty in the insect repellent sector.

Insect Repellent Industry Leaders

-

Spectrum Brands, Inc.

-

Henkel AG & Co. KGaA

-

Reckitt Benckiser Group PLC

-

Godrej Group

-

S.C. Johnson & Son, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Thermacell Repellents, a major manufacturer of area repellents, released the E65 rechargeable mosquito repeller. The device incorporates a fast-charging dock and a 6.5-hour battery life to provide a 20-foot zone of protection. It was launched to meet the demand for convenient and longer-lasting outdoor repellent solutions.

- November 2024: Nippo, a well-known Indian consumer brand, entered the home care market with the launch of "Swooper." The mosquito repellent product uses a Japanese MFT (Metrofluthrin) formula and features a sandalwood fragrance to appeal to local consumer preferences. It was made available through both retail and online channels.

- July 2024: Godrej Consumer Products (GCPL) introduced its new Goodknight Flash liquid vaporizer in India, featuring the patented molecule Renofluthrin. The company claimed the formulation is twice as effective at driving away mosquitoes and remains active for up to two hours after being switched off. This move solidified GCPL's leadership in India's household insecticide market.

- March 2024: Jeffs' Brands, a technology-driven consumer goods retail company, introduced an innovative pest-repellent product line under its Fort brand. The launch marked the company's entry into the pest-control segment and aimed to capture a share of the growing demand for effective and technologically advanced solutions.

Global Insect Repellent Market Report Scope

Insect repellents are agents used to protect the body from the bites of insects that can cause local or systemic effects. While some bites cause only local skin irritation, some can cause severe illnesses and possibly death as the insects act as carriers or vectors of diseases. Thus, insect repellents protect against all insect bites and prevent diseases from occurring. The insect repellent market is segmented based on product type, distribution channel, category, and geography. By product type, the market is segmented into body work insect repellents (cream/lotion and oil) and other insect repellants. The other insect repellants segment is further sub-segmented into coil, liquid vaporizer, spray/aerosol, bait, and other insect repellants (chalk, powder, etc.). By distribution channel, the market is segmented into offline retail stores and online retail stores. By category, the market is segmented into natural insect repellent and conventional insect repellent. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Bait |

| Coils |

| Sprays/Aerosols |

| Mats |

| Liquid Vaporizer |

| Other Product Types |

| Natural Insect Repellent |

| Conventional Insect Repellent |

| Adults |

| Kids/Children |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Bait | |

| Coils | ||

| Sprays/Aerosols | ||

| Mats | ||

| Liquid Vaporizer | ||

| Other Product Types | ||

| By Ingredient Type | Natural Insect Repellent | |

| Conventional Insect Repellent | ||

| By End User | Adults | |

| Kids/Children | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the insect repellent market in 2031?

The industry is projected to reach USD 15.71 billion by 2031, growing at a 6.62% CAGR.

Which product category is expanding the fastest?

Liquid vaporizers lead with a 7.32% CAGR through 2031, reflecting demand for continuous spatial protection.

How large is Asia-Pacific’s contribution?

Asia-Pacific accounted for 49.10% of 2025 revenue and shows the highest regional growth at a 9.15% CAGR.

Why are natural repellents gaining popularity?

Consumer preference for botanical actives and regulatory support for oil of lemon eucalyptus are driving an 8.05% CAGR in natural formulations.

Which distribution channel is growing most quickly?

Online retail is advancing at an 8.55% CAGR as direct-to-consumer models and subscription services gain traction.

What factors are restraining growth?

Competition from treated clothing and public concern over chemical ingredients are the principal market headwinds.

Page last updated on: