Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 20.02 Billion |

| Market Size (2026) | USD 21.17 Billion |

| Market Size (2031) | USD 27.99 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Cosmeceutical Market Analysis by Mordor Intelligence

Market Overview

The North America cosmeceutical market size was valued at USD 20.02 billion in 2025 and estimated to grow from USD 21.17 billion in 2026 to reach USD 27.99 billion by 2031, at a CAGR of 5.74% during the forecast period (2026-2031). This market segment integrates pharmaceutical efficacy with cosmetic applications through advanced bioactive ingredients and formulation technologies to serve consumer requirements across the United States, Canada, and Mexico. Market expansion is primarily attributed to the increasing consumer preference for clinically validated products targeting age-related concerns while maintaining adherence to regulatory safety protocols. Other key factors driving market expansion include the FDA's Modernization of Cosmetics Regulation Act (MoCRA), which has strengthened industry compliance requirements and benefited companies with established quality management systems.

Key Report Takeaways

- By product type, skin care accounted for 55.92% of the North America cosmeceutical market share in 2025; lip care is projected to log the fastest 8.31% CAGR through 2031.

- By category, conventional products held 71.65% revenue in 2025, whereas natural/organic lines are on track for an 7.78% CAGR to 2031.

- By end-user, women commanded 69.72% of the North America cosmeceutical market size in 2025; the male segment is expanding at a 7.05% CAGR.

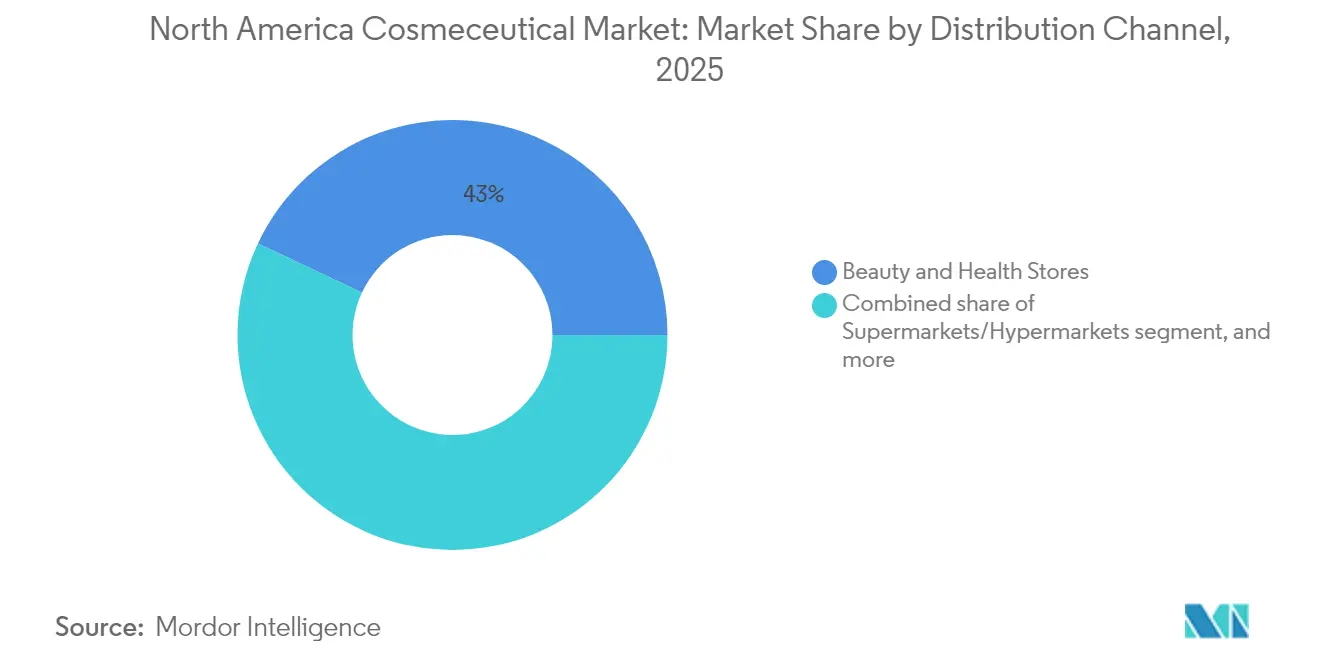

- By distribution channel, beauty and health stores led with 43.01% revenue share in 2025, while online retail is advancing at a 7.08% CAGR.

- By geography, the United States dominated with 82.55% market share in 2025; Mexico is set to post a 7.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Cosmeceutical Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for anti-aging and skin repair solutions in global markets | +1.2% | North America, with strongest growth in the United States metropolitan areas | Medium term (2-4 years) |

| Innovation in bioactive ingredient development and advanced formulation technologies | +0.9% | North America, with research and development concentration in the United States and Canada | Long term (≥ 4 years) |

| Increased focus on preventive skincare through scientific advancements | +0.8% | North America and Europe spillover effects | Medium term (2-4 years) |

| Social media's significant impact on beauty product selection worldwide | +0.7% | North America, with highest penetration in the United States | Short term (≤ 2 years) |

| Consumer preference for clinically validated products and research-based solutions | +0.6% | North America, particularly the United States premium segments | Medium term (2-4 years) |

| Rising adoption of natural and clean-label formulations across markets | +0.5% | North America and Europe, with Mexico showing accelerated adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for anti-aging and skin repair solutions in global markets

The anti-aging cosmeceutical segment is growing rapidly due to demographic changes and advances in peptide and retinoid formulations. The integration of nanotechnology with active ingredients improves peptide stability and bioavailability, overcoming previous formulation limitations. At the 2024 SCALE Conference, Estée Lauder's Clinique and La Mer brands presented marine-derived compounds that provide retinol-like anti-aging benefits without causing inflammation. In April 2025, Promura GmbH invested USD 3 million in Sirona Biochem through unsecured, convertible debentures to advance research, development, and commercialization of anti-aging skincare products, specifically TFC-1326. This development has particular significance in North American markets, where aging populations have higher disposable incomes and demonstrate greater interest in scientifically proven skincare products.

Innovation in bioactive ingredient development and advanced formulation technologies

The integration of biotechnology in cosmeceutical formulations has advanced through enhanced delivery systems and bioactive compounds from sustainable sources. The application of nanotechnology enables better penetration of unstable ingredients, such as vitamin C and retinoids, while nanostructured lipid carriers improve product effectiveness and user experience. Plant-derived metabolites, including flavonoids, phenolic acids, and terpenoids, are increasingly used for their antioxidant and photoprotective properties. The adoption of Natural Deep Eutectic Solvents (NaDES) in extraction methods has improved the stability and bioactivity of these compounds. Pierre Fabre demonstrates this industry transition with its goal to achieve 90% natural-origin ingredients by the end of 2025, supported by over 1,000 annual clinical studies across six research centers [1]Source: Pierre-Fabre, "Dermo-Cosmetics R&D figures", www.pierre-fabre.com. Companies that invest in developing proprietary delivery systems and bioactive compounds gain competitive advantages in the market.

Increased focus on preventive skincare through scientific advancements

The shift from reactive to preventive skincare has increased the adoption of cosmeceuticals that offer proven protection against environmental damage and premature aging. Modern sunscreen formulations provide comprehensive protection against UVA, UVB, and visible light through advanced filters such as methoxypropylamino cyclohexenylidene ethoxyethylcyanoacetate (MCE) and phenylene bis-diphenyltriazine (TriAsorB). Natural photoprotective compounds, including mycosporine-like amino acids (MAAs) and flavonoids, are becoming viable alternatives to synthetic UV filters, meeting both performance requirements and environmental standards. According to the Environmental Working Group's 2024 analysis, only 25% of 1,700 SPF products meet safety and efficacy standards, creating market opportunities for scientifically validated products [2]Environmental Working Group, "Sunscreen Guide - Rated by Scientists", www.ewg.org . Titanium dioxide and zinc oxide remain FDA Generally Recognized as Safe and Effective (GRASE), while advancements in nanoparticle technology address consumer concerns regarding particle size and photocatalytic activity. This prevention-focused approach particularly appeals to younger consumers who emphasize long-term skin health over corrective treatments.

Social media's significant impact on beauty product selection worldwide

Digital platforms have transformed how consumers discover and purchase cosmeceuticals. According to Google data, retinol and retinoids remain the most searched cosmeceutical ingredients, with approximately 49,500 searches in 2024. Social media platforms have increased consumer knowledge about ingredients, leading to greater demand for transparent formulations and evidence-based efficacy claims. Social media content from beauty influencers and dermatologists has influenced ingredient preferences, particularly for hyaluronic acid, niacinamide, and peptide complexes. This digital landscape presents opportunities and challenges for brands, as social media can quickly spread both positive and negative product reviews, making robust quality control and scientific validation essential for market success. The rapid pace of social media trends has also shortened product development cycles, benefiting companies that can quickly formulate new products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs associated with research, testing, and product development processes | -0.8% | Region, with highest impact in smaller companies | Long term (≥ 4 years) |

| Stringent regulatory guidelines for product safety and market approvals | -0.6% | North America, particularly the United States under MoCRA implementation | Medium term (2-4 years) |

| Risk of adverse effects and potential product recalls | -0.4% | Region, with heightened scrutiny in the United States | Short term (≤ 2 years) |

| Intense competition from established conventional cosmetics and personal care brands | -0.5% | North America, particularly in mass market segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High costs associated with research, testing, and product development processes

As investment demands for cosmeceutical development rise, new entrants face daunting barriers, while established firms with robust research and development infrastructures solidify their dominance. Regulatory standards, particularly concerning safety, efficacy, and labeling, especially for products teetering on pharmaceutical claims, intensify these challenges. In the U.S., the FDA oversees cosmetic safety under the Federal Food, Drug, and Cosmetic Act. Recent moves, like the Modernization of Cosmetics Regulation Act (MoCRA), hint at a trend towards heightened scrutiny. Furthermore, the adoption of nanotechnology and sophisticated delivery systems necessitates hefty investments in specialized manufacturing and stringent quality control. These challenges weigh heavily on smaller entities without the cushion of economies of scale, often sparking heightened merger and acquisition interest from private equity. Firms boasting diversified portfolios can more efficiently distribute research and development expenses across various markets and categories, securing a competitive advantage.

Stringent regulatory guidelines for product safety and market approvals

The Modernization of Cosmetics Regulation Act (MoCRA) has reshaped U.S. cosmetics regulations, introducing compliance requirements that impact North American competition. By December 2025, facility registration, product listing, and Good Manufacturing Practices (GMP) compliance will be mandatory, challenging smaller manufacturers without quality systems. Safety substantiation and adverse event reporting add liability risks, potentially hindering ingredient and formulation innovation. State-specific regulations add complexity. California's Safer Consumer Products regulations and Washington State's Toxic-Free Cosmetics Act increase compliance costs. In Canada, the 2024 amendments require fragrance allergen disclosure for concentrations above 0.01% in rinse-off and 0.001% in leave-on products, adding cross-border labeling challenges. These changes benefit established firms with compliance systems while creating barriers for new entrants lacking expertise and resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skin Care Dominance Drives Innovation

In 2025, skin care products hold a 55.92% share of the North American cosmeceutical market, maintaining dominance. Lip care shows the highest growth rate at 8.31% CAGR through 2031. The skin care segment leads due to demand for anti-aging, anti-acne, and sun protection products offering both cosmetic and therapeutic benefits. Anti-aging products utilize peptide technology, with acetyl hexapeptide-8 and palmitoyl pentapeptide-4 reducing wrinkles and boosting collagen. Anti-acne products focus on natural antimicrobials and probiotics to regulate the skin microbiome, while sun protection blends UV filters with antioxidants. Market growth is supported by an aging demographic, with 17.43% of the American population aged 65+ in 2023, according to World Bank data .

Hair care products, including shampoos, conditioners, and colorants, are evolving through bioactive ingredients and sustainable formulations. Natural pigments extracted from neem, fenugreek, and hibiscus flowers provide alternatives to synthetic hair dyes. The lip care segment's 8.31% growth rate reflects increased focus on lip health and advanced formulations with peptides and botanical extracts. Oral care cosmeceuticals show potential growth, particularly in products for enamel strengthening and gum health. The integration of pharmaceutical and cosmetic technologies across segments creates opportunities for companies focused on clinical testing and delivery system development.

By Category: Natural/Organic Acceleration Challenges Conventional Dominance

In 2025, conventional formulations dominate the market with a 71.65% share. Meanwhile, natural and organic alternatives are on the rise, boasting an 7.78% CAGR. This shift underscores a growing consumer preference for clean-label products with transparent ingredients. The conventional segment retains its lead, bolstered by established supply chains, proven efficacy, and cost advantages that resonate with both price-sensitive consumers and mass retailers. These factors make conventional formulations a reliable choice for large-scale production and distribution, ensuring their continued dominance. The robust growth rate of the natural and organic segment signals a market pivot towards sustainable formulations, fueled by heightened environmental and health awareness. This trend reflects a broader consumer demand for products that align with ethical and eco-friendly values.

Advancements in extraction and stabilization techniques have mitigated past challenges of natural formulations, particularly concerning efficacy and shelf life. These improvements have enabled natural products to compete more effectively with conventional options, addressing consumer concerns about performance and durability. Industry giants are setting ambitious sustainability targets: L'Oréal and Unilever aim for 100% sustainable palm oil and 90% natural-origin ingredients by 2025. Such commitments highlight the industry's shift toward integrating sustainability into core business strategies. Leveraging Natural Deep Eutectic Solvents (NaDES) technology, companies are enhancing the stability and effectiveness of natural formulations, all while upholding clean-label standards. While natural and organic products often come with premium price tags, they also promise higher margins for companies that can convincingly showcase their efficacy and sustainability advantages to consumers. This premium pricing reflects the added value perceived by consumers who prioritize health, environmental impact, and product transparency.

By End-User: Male Segment Emergence Reshapes Market Dynamics

Female consumers account for 69.72% of the cosmeceutical market share in 2025, maintaining their position as the primary demographic. The male consumer segment exhibits the highest growth rate at 7.05% CAGR, driven by changing cultural attitudes and increased awareness of personal care. Male consumers are expanding beyond basic hygiene products to adopt comprehensive skincare routines, including facial cleansers, moisturizers, and anti-aging products, particularly in millennial and Gen Z age groups. The most significant growth in male product categories comes from anti-aging formulations and specialized treatments addressing specific concerns like razor burn and ingrown hairs.

Gender-neutral product development presents a market opportunity, with companies formulating products that serve both demographics without gender-specific marketing. Social media influence and celebrity endorsements support the male segment's growth by normalizing men's skincare routines. Subscription grooming services targeting male consumers, such as Bart's Balm, demonstrate demand for accessible, curated product experiences. In the female segment, consumers continue to drive premium market growth through their investment in clinically validated, multi-step skincare routines featuring advanced active ingredients and personalized formulations.

By Distribution Channel: E-commerce Disruption Accelerates Omnichannel Evolution

Beauty and health stores hold a 43.01% market share in 2025, capitalizing on their product education capabilities and personalized consultation services. Online retail channels are growing at a 7.08% CAGR, influenced by changes in post-pandemic shopping behavior and direct-to-consumer brand strategies. The traditional retail model remains effective through experiential shopping and professional guidance, helping consumers make informed decisions about cosmeceutical products, especially for premium items that require detailed explanations of active ingredients and usage instructions.

Supermarkets/hypermarkets provide mass-market access to conventional formulations, while specialty retailers and branded stores focus on premium, professional-grade products. The integration of online and offline channels creates comprehensive shopping experiences that combine digital convenience with physical product interaction. Ulta's loyalty program demonstrates this effectiveness, generating over 95% of sales through integrated customer engagement. Digital innovations, including augmented reality and virtual try-on technologies, enhance online shopping experiences by reducing return rates and building consumer confidence.

Geography Analysis

The United States holds an 82.55% share of the North American cosmeceutical market in 2025. This dominance stems from its sophisticated consumer base, robust regulatory framework, and presence of major beauty companies. The market benefits from high disposable incomes, advanced healthcare infrastructure, and consumers who prioritize clinically validated skincare solutions. The Modernization of Cosmetics Regulation Act (MoCRA) has enhanced safety standards while providing competitive advantages to companies with established quality systems, reinforcing the United States' position as a global cosmeceuticals hub.

Mexico is set to lead the pack with an impressive projected CAGR of 7.36% through 2031. This surge is fueled by a burgeoning middle class with heightened purchasing power, an increasing awareness of beauty, and a regulatory landscape that's becoming more harmonized, paving the way for international brands. Enhancements in the COFEPRIS regulatory framework, which streamline product approvals and ensure compliance with international standards, coupled with a growing consumer savvy about ingredient efficacy, further bolster this market's expansion. Additionally, the increasing availability of premium and innovative products tailored to local preferences is expected to drive further growth.

Canada's growth trajectory remains steady, largely due to its alignment with US regulatory standards and a consumer tilt towards natural and organic products. Notably, Canada's 2024 regulations, which mandate the disclosure of fragrance allergens, underscore the market's commitment to transparency and prioritizing consumer safety. This regulatory shift is anticipated to encourage brands to reformulate products and adopt cleaner labeling practices, aligning with evolving consumer expectations. Meanwhile, the broader North American landscape, encompassing the Caribbean and Central America, is witnessing growth, spurred by economic advancements and urbanization, especially in the realm of premium personal care products. The rising disposable income in these regions, coupled with increasing access to global brands, is expected to further fuel market expansion.

Competitive Landscape

The North American cosmeceutical market demonstrates moderate consolidation. Major multinational corporations compete with emerging biotech companies and direct-to-consumer brands in developing innovative ingredients and delivery systems. Companies like L'Oréal S.A., The Estée Lauder Companies Inc., Kenvue Inc., and Procter & Gamble Company maintain their market positions through research and development capabilities, global distribution networks, and regulatory expertise, particularly in addressing new standards such as MoCRA implementation.

Smaller biotech brands and direct-to-consumer (DTC) players are ramping up competition. They're rolling out clinically validated actives, quick-absorbing formats, and solutions tailored for sensitive or acne-prone skin. These innovations cater to the growing consumer demand for effective and science-backed skincare products. In a saturated market, themes like microdosing routines, dermocosmetic hybrids, and a science-driven minimalist approach are gaining traction as key differentiators, helping brands carve out a niche and appeal to informed, ingredient-conscious consumers.

Companies are differentiating themselves through technological advancement, focusing on nanotechnology, AI-driven personalization, and sustainable ingredient sourcing to gain market share. Market opportunities exist in underserved segments, including male grooming formulations, natural sun protection products, and oral care cosmeceuticals. New market entrants utilize direct-to-consumer models, social media marketing, and subscription services to establish direct customer relationships outside traditional retail channels. The complex regulatory environment creates entry barriers while benefiting established companies with existing compliance systems, indicating potential market consolidation among companies that lack regulatory expertise or adequate financial resources.

North America Cosmeceutical Industry Leaders

-

L'Oréal S.A.

-

The Estée Lauder Companies Inc.

-

Shiseido Company, Limited

-

Procter & Gamble Company

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Natural Skin Care, LLC launched Vita CE with Ferulic Acid, an antioxidant serum that addresses aging signs and improves skin health. The formulation includes a Trans-Epidermal Carrier to enhance ingredient absorption and efficacy.

- February 2025: Colgate-Palmolive introduced the Colgate Total Active Prevention System, a three-product oral care system that helps consumers maintain their oral health. The system combines toothpaste, toothbrush, and mouthwash to reduce bacteria and prevent oral health issues.

- November 2024: CeraVe expanded into the haircare market with its Anti-Dandruff Shampoo and Conditioner system. The products eliminate up to 100% of visible flakes while protecting the scalp barrier and treating mild to moderate dandruff symptoms. The formulation maintains hair health and softness.

- July 2024: Viome has developed personalized AM/PM toothpaste and gel formulations using artificial intelligence and oral microbiome data analysis to enhance overall health outcomes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North America cosmeceutical market as finished topical or ingestible beauty products that incorporate biologically active ingredients and are sold through retail and professional channels across the United States, Canada, and Mexico. Products include anti-aging creams, antioxidant serums, dermo-cosmetic hair care, lip care, oral care, and ingestible nutricosmetics that make clinically testable claims.

Scope exclusion: devices such as home-use facial rollers, LED masks, and professional energy-based systems remain outside this value pool.

Segmentation Overview

-

By Product Type

-

Skin Care

- Anti-ageing

- Anti-acne

- Sun Protection

- Other Skin-care Types

-

Hair Care

- Shampoos and Conditioners

- Hair Colorants and Dyes

- Other Hair-care Types

- Lip Care

- Oral Care

-

Skin Care

-

By Category

- Conventional

- Natural/Organic

-

By End-User

- Male

- Female

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Beauty and Health Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

- United States

- Canada

- Mexico

- Rest of North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview dermatologists, retail buyers, contract manufacturers, and marketing heads across the United States, Canada, and Mexico. These discussions clarify ingredient cost inflation, clinic sell-through rates, and upcoming regulatory impacts, which are then used to challenge or confirm secondary findings before the model is frozen.

Desk Research

We start with publicly available cornerstones such as the US FDA Voluntary Cosmetic Registration Program database, Health Canada's Cosmetic Notification System, the Mexican COFEPRIS import registry, and trade flows from UN Comtrade. Consumer spend indicators are drawn from Bureau of Labor Statistics Consumer Expenditure Surveys, while shipment volumes come from Harmonized System codes that isolate cosmeceutical formulations. Additional context is gathered from dermatology and pharmacology journals, industry association briefs from the Personal Care Products Council, and news archives on Dow Jones Factiva. A few paid assets, D&B Hoovers for company financials and Questel for patent trends, help us gauge competitive intensity. The sources listed illustrate our desk inputs and are not exhaustive.

Market-Sizing & Forecasting

A top-down demand pool is built from dermatology clinic patient volumes, per-capita premium skin-care spend, online channel share, ingredient cost curves, and MoCRA compliance milestones, which are then benchmarked with selective bottom-up checks such as sampled average selling price times unit shipments from leading contract manufacturers. Gaps in bottom-up coverage, especially within small private labels, are corrected through interpolation using retail scanner data averages. A multivariate regression incorporating disposable income, 40+ population growth, search interest in "retinol," and e-commerce penetration produces the 2025-2030 outlook.

Data Validation & Update Cycle

Model outputs go through variance scans against historical import values and quarterly earnings signals. Senior reviewers sign off after anomalies are resolved, and reports refresh every twelve months, with interim updates triggered by material events such as MoCRA implementation deadlines or a major ingredient price shock.

Why Mordor's North America Cosmeceutical Products Baseline Commands Everyday Trust

Published estimates often diverge because each firm chooses its own product cut, distribution mix, and refresh rhythm. When definitions shift, so do headline dollars.

Key gap drivers here include whether ingestibles are counted, how off-price online channels are treated, the year of currency conversion, and if forecast models adjust for MoCRA-linked reformulation costs that we have embedded from December 2025 onward.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 20.02 B (2025) | Mordor Intelligence | |

| USD 20.04 B (2024) | Global Consultancy A | excludes nutricosmetics and applies flat average selling prices |

| USD 17.80 B (2024) | Industry Publisher B | uses retail revenue only and projects growth from historic CAGR without regulatory cost overlay |

These comparisons show that while figures sit in a similar band, Mordor's disciplined scope choices, explicit MoCRA cost adjustments, and annual refresh give decision-makers a transparent baseline that can be traced to clear variables and repeated with confidence. The alternative numbers stem from narrower baskets or static assumptions, which makes our estimate the steadier reference point.

Key Questions Answered in the Report

What is the current size and projected growth of the North America cosmeceuticals market?

The market stands at USD 21.17 billion in 2026 and is forecast to reach USD 27.99 billion by 2031, reflecting a 5.74% CAGR.

Which product segment drives the most revenue?

Skin care products command 55.92% of total revenue and remain the primary growth engine, especially in anti-aging, acne, and sun-protection lines.

Where is the fastest geographic growth expected?

Mexico leads with a 7.36% CAGR through 2031, buoyed by rising middle-class incomes and streamlined COFEPRIS regulations.

How is regulation influencing competitive dynamics?

The U.S. MoCRA law introduces mandatory facility registration, product listing, and GMP compliance by December 2025, favoring companies with established quality systems.

Page last updated on: