Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

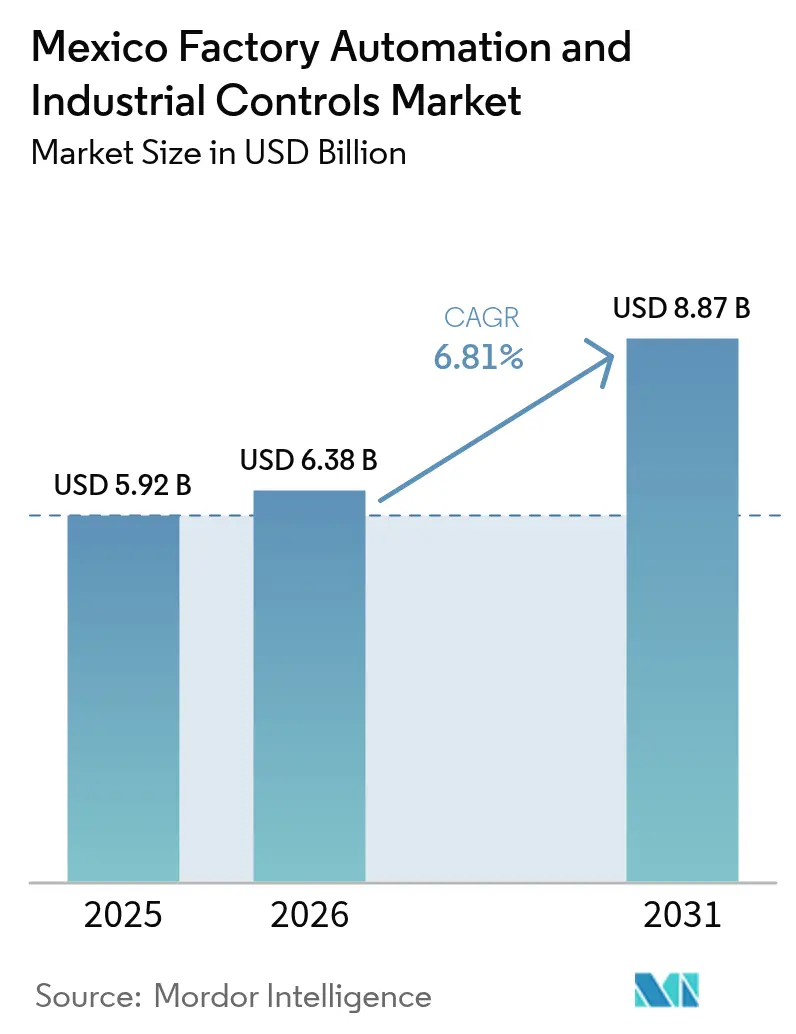

| Base Year Market Size (2025) | USD 5.92 Billion |

| Market Size (2026) | USD 6.38 Billion |

| Market Size (2031) | USD 8.87 Billion |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

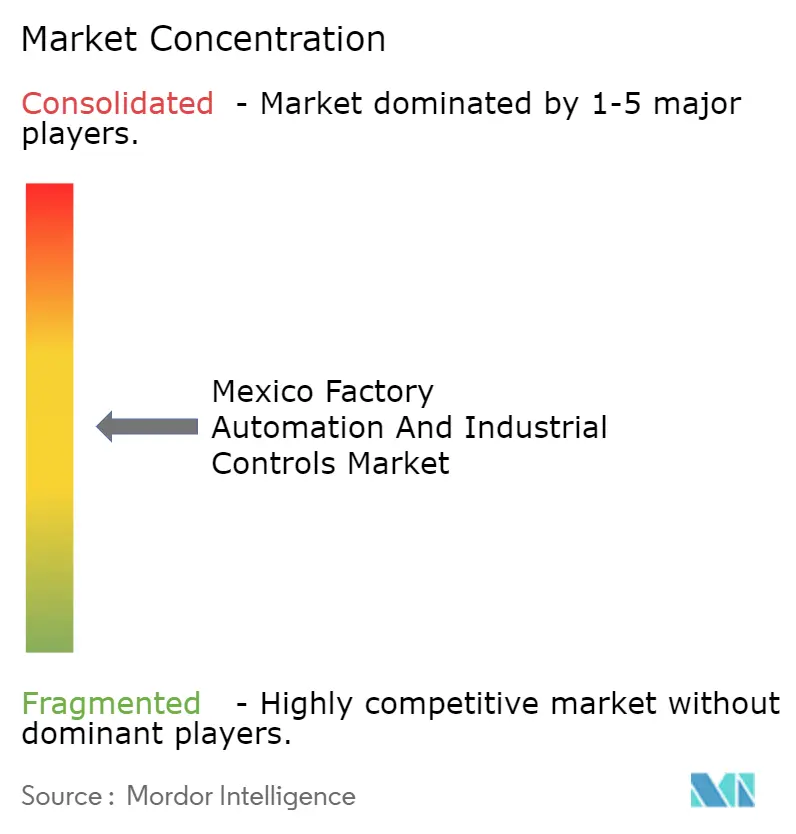

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The Mexico factory automation and industrial controls market size is projected to expand from USD 5.92 billion in 2025 and USD 6.38 billion in 2026 to USD 8.87 billion by 2031, registering a CAGR of 6.81% between 2026 to 2031. Nearshoring by North-American manufacturers, generous fiscal incentives under the Mexico 4.0 decree, and falling robot average selling prices are encouraging continuous capital spending even as peso-dollar swings complicate short-term budgets. Automotive, pharmaceutical, petrochemical, and fast-moving consumer-goods producers are leading the demand for connected machinery that closes information gaps between the shop floor and the enterprise. At the same time, software that enables real-time scheduling, predictive-quality analytics, and digital-twin simulations is moving to the top of management agendas, reflecting a shift from pure hardware replacement to data-driven productivity gains. Competitive intensity is rising as low-cost Chinese robot brands court small and medium enterprises, pushing established suppliers to differentiate through local manufacturing, ecosystem depth, and training partnerships.

Key Report Takeaways

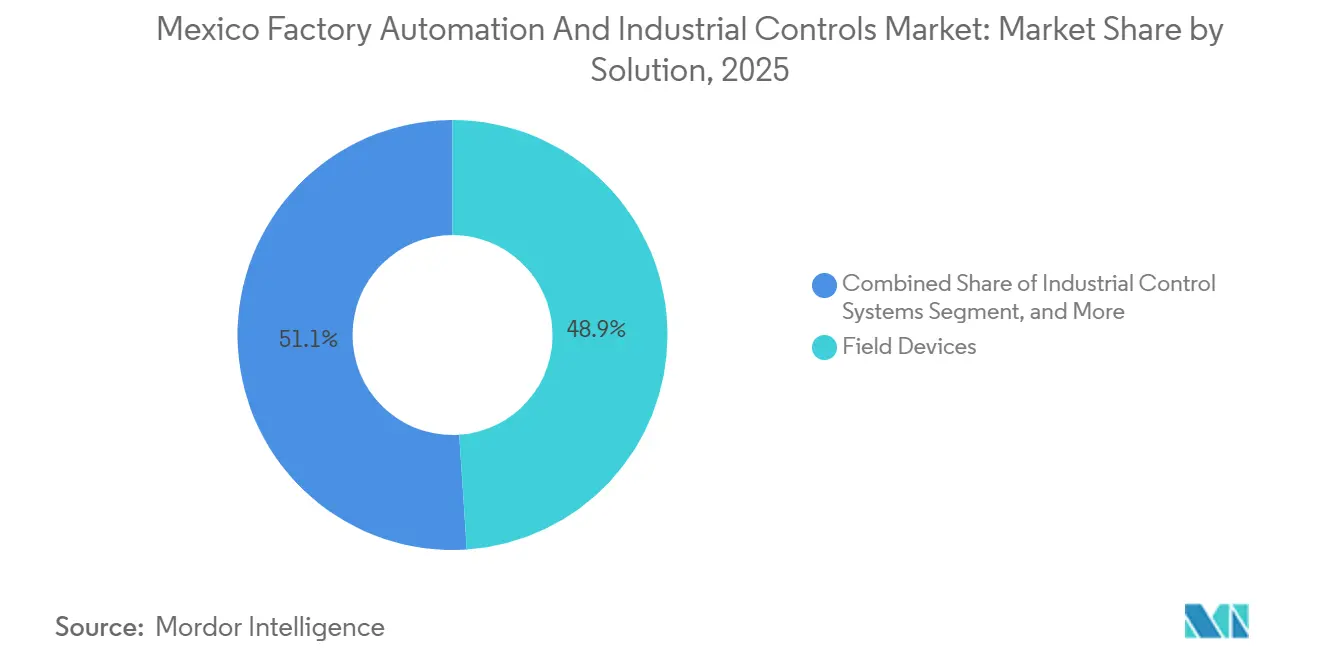

- By solution, field devices held 48.94% of the Mexico factory automation and industrial controls market share in 2025, while software is advancing at a 7.21% CAGR through 2031.

- By automation type, fixed automation led with 45.78% share of the Mexico factory automation and industrial controls market size in 2025, whereas integrated or hyper-automation is projected to expand at a 7.62% CAGR to 2031.

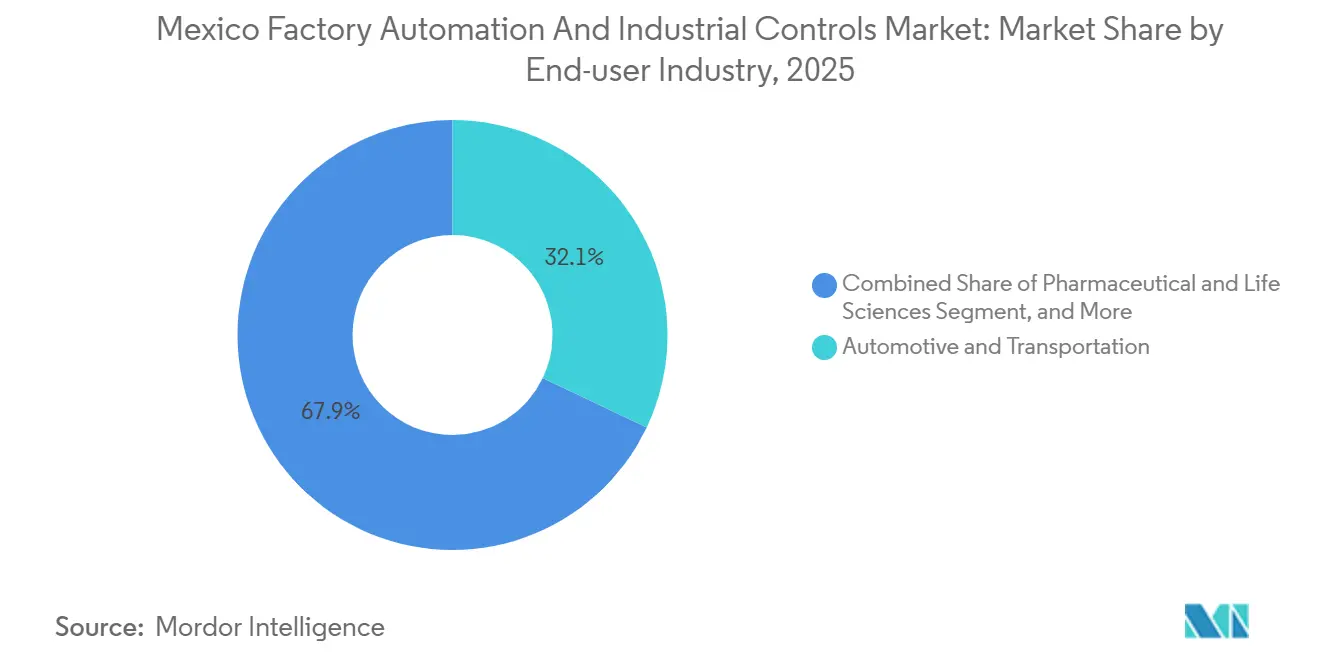

- By end-user industry, automotive and transportation accounted for 32.07% of 2025 demand, but pharmaceutical and life sciences is forecast to post the fastest 8.04% CAGR through 2031.

- By deployment mode, on-premise installations commanded 48.81% of 2025 revenue, yet hybrid architectures are expected to grow at an 8.13% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-Shoring Boost of North-American OEMs | +1.8% | Nuevo León, Querétaro, Guanajuato, Baja California | Medium term (2-4 years) |

| Surge in Industrial-IoT Retrofit Projects | +1.5% | Nuevo León, Jalisco, Aguascalientes | Short term (≤ 2 years) |

| Government “Mexico 4.0” Tax Incentives | +1.3% | National | Short term (≤ 2 years) |

| AI-Based Predictive-Quality Demand | +1.0% | Querétaro, Jalisco, San Luis Potosí | Medium term (2-4 years) |

| Falling Robot Average Selling Price | +0.7% | National | Short term (≤ 2 years) |

| Green-Hydrogen Pilot Lines Automation | +0.5% | Sonora and Pemex facilities | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Near-Shoring Boost of North-American OEMs

Strong relocation flows are propelling the Mexico factory automation and industrial controls market as manufacturers chase supply-chain resilience and lower logistics costs. Nuevo León, Querétaro, and Guanajuato have secured billions in greenfield vehicle, appliance, and HVAC investments that specify programmable logic controllers, supervisory control networks, and robot cells from day one.[1]Pro Mexico Industry Staff, “Nuevo León, Jalisco, and Baja California Lead the Connected Factory Revolution, According to Zebra,” promexicoindustry.com Tier-1 suppliers are following anchor clients with flexible assembly lines that can serve several platforms without disrupting takt time. Although automotive foreign direct investment slumped in late 2025, companies signal that postponed automation budgets will be unlocked once tariff clarity returns, translating to a second wave of orders in 2027-2028.[2]International Federation of Robotics, “IFR Press Release: Americas,” ifr.org Regional governments are reinforcing the trend with industrial-park infrastructure and expedited permitting that shorten commissioning cycles.

Surge in Industrial-IoT Retrofit Projects

Plant owners are connecting legacy presses, mixers, extruders, and packaging lines to inexpensive sensors that stream health, energy, and throughput data into edge gateways. Quick wins include 30% drops in unplanned downtime and 20% lower maintenance bills, achievements that build internal confidence for broader digital programs. Because retrofits preserve sunk capital, payback typically falls under two years, making them attractive when exchange-rate volatility raises the hurdle for large hardware outlays.[3]Design Systems de Mexico, “Industry 4.0 in Mexican Manufacturing: Implementing MES for Digital Transformation,” ds-mfgengineering.mx The main friction is integrator bandwidth; operational-technology and information-technology expertise rarely coexist, so projects stall when partners lack dual skills. Vendors that bundle middleware, training, and cybersecurity support are finding easier adoption paths, especially among food, beverage, and electronics producers.

Government “Mexico 4.0” Tax Incentives

The decree allows immediate deductions on qualifying automation gear and subsidizes workforce upskilling, effectively trimming after-tax project costs by up to one-third. Small and medium enterprises benefit most because they historically faced tight credit and high collateral demands for equipment loans. Several multinational expansions announced in 2024-2026 openly cite the incentive when justifying Mexican capacity adds over Asian alternatives. Yet the program sunsets after 2027, creating a countdown that concentrates procurement decisions in the near term and risks a later demand dip unless permanent productivity gains justify continued spending. Firms that secure skilled technicians through the decree’s training vouchers enjoy faster start-ups and lower commissioning errors, reinforcing the policy’s intent.

AI-Based Predictive-Quality Demand

Real-time machine-vision and inference models embedded in controllers are pushing quality assurance from laboratory sampling to continuous in-line monitoring. Pharmaceutical plants that once tolerated hour-long assay cycles now reject defective tablets within seconds, lifting first-pass yield and regulatory confidence. Automotive suppliers deploy edge-AI weld checkers that flag porosity before a flawed chassis leaves the cell, avoiding scrap and warranty claims. The adoption curve favors operations that already invested in manufacturing execution systems, because clean, contextualized data feeds training algorithms.[4]Rachael Brown, “Five Themes Set to Shape Mexican Manufacturing in 2025,” manufacturingdigital.com Cultural resistance surfaces when operators fear job loss, but pilot lines that highlight human-machine collaboration often convert skeptics into champions, sustaining momentum for wider rollouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Skilled-Labor Shortage | -1.2% | Querétaro, Nuevo León, Jalisco | Medium term (2-4 years) |

| Peso-USD FX Volatility on Capex | -1.0% | National | Short term (≤ 2 years) |

| Mid-Tier Supplier Cyber-Security Gaps | -0.6% | Automotive and electronics corridors | Medium term (2-4 years) |

| Legacy Plant Infrastructure Lock-In | -0.5% | Automotive and petrochemical belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Skilled-Labor Shortage

Demand for engineers fluent in programmable logic controllers, industrial Ethernet, and AI-assisted programming far outstrips supply, forcing vendors to import specialists or delay projects. System-integrator backlogs stretch past six months, raising opportunity costs for manufacturers that need rapid capacity ramps to meet export contracts. Universities produce science and engineering graduates, yet curricula seldom cover industrial controls in depth, causing a mismatch that state-level training centers now attempt to close. Larger companies fund in-house academies, but small and medium enterprises struggle to allocate resources, widening the productivity gap. Unless a pipeline of technicians emerges, automation penetration will lag potential, particularly outside established hubs.

Peso-USD FX Volatility on Capex

A 15% peso slide in 2025 inflated the landed cost of imported robots, drives, and safety PLCs, prompting finance teams to raise internal-rate-of-return thresholds. Automakers and tier-ones deferred multimillion-dollar body-shop upgrades, favoring incremental sensor retrofits that carry smaller dollar exposure. While exporters can hedge naturally through U.S.-dollar revenue, domestically oriented producers lack such buffers, leading to stalled purchase orders. Hedging instruments remain under-used by small and medium enterprises because of cost and complexity, leaving them vulnerable to every currency swing. Should the peso stabilize around 18-19 per USD, the backlog of deferred projects could reopen, but chronic volatility risks redirecting orders to lower-priced Asian suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Software Outpaces Hardware as Digital Twins Gain Traction

Field devices anchored 48.94% of the Mexico factory automation and industrial controls market share in 2025, underscoring the capital already tied up in sensors, motors, drives, and more than 25,000 installed robots. Yet software posted the quickest 7.21% CAGR by enabling digital twins, real-time scheduling, and tight enterprise integration. Manufacturers adopting manufacturing execution systems report faster lot-tracking, quicker deviation handling, and smoother audits, advantages that lift plant utilization while cutting recall risks. Services follow software growth because clients need integration, cybersecurity, and training to extract full value from the new applications. Over time, every major hardware upgrade now triggers a parallel software work stream, weaving analytics into the heart of plant workflows and ensuring recurring spend.

Even so, hardware demand remains resilient. Automotive body-shops still add articulated robots for material handling, whereas oil and gas pipelines order new distributed control system nodes to meet safety standards. Software tempering line-side behavior does not replace the need for rugged components; rather, it magnifies their efficiency. Vendors that package edge gateways, embedded inference models, and low-code dashboards lower entry barriers for small and medium enterprises and unlock new wallet share. Consequently, the Mexico factory automation and industrial controls market continues to pivot toward a life-cycle revenue model in which initial hardware margins give way to multi-year support and license streams.

By Automation Type: Integrated Architectures Displace Fixed Lines

Fixed automation captured 45.78% of the Mexico factory automation and industrial controls market size in 2025 because legacy automotive plants still rely on dedicated welding, painting, and stamping lines. Nonetheless, integrated or hyper-automation is climbing at a 7.62% CAGR as manufacturers stitch together programmable logic controllers, industrial Internet of Things sensors, and AI to create self-optimizing cells. Real-time analytics adjust cycle times, predict maintenance windows, and balance production across multiple SKUs, turning throughput volatility from a liability into a manageable variable. Early adopters in beverage bottling and consumer electronics report 30% gains in overall equipment effectiveness once islands of automation link into plantwide platforms.

Transition costs can be daunting. Legacy lines lack Ethernet cabling, power-over-Ethernet switches, and environmental controls for sensors, so retrofit budgets must fund basic infrastructure before software enters the conversation. Some operators therefore apply a hybrid path: they graft collaborative robots and vision subsystems onto fixed conveyors, slowly building toward true integration. Still, each new greenfield plant tends to skip fixed automation altogether, signaling that its dominance will erode steadily as 2028-2032 replacement cycles arrive.

By End-User Industry: Pharmaceutical Surges as Automotive Plateaus

Automotive and transportation retained 32.07% revenue share in 2025, but its order book softened after an 11% robot-installation dip and an 84% foreign-direct-investment swoon in the third quarter of 2025. Regulatory uncertainty around regional content rules weighs on new-platform launches, moderating line-automation prospects through 2027. Pharmaceutical and life sciences tell a different story, expanding at an 8.04% CAGR thanks to continuous process verification demands and double-digit export growth in medical devices. Digital batch records, validated manufacturing execution systems, and AI vision safeguards are now commonplace as domestic labs chase U.S. Food and Drug Administration approvals. The pattern underscores how compliance pressure often accelerates automation beyond mere cost considerations.

Petrochemicals, utilities, and packaged food processors also allocate rising budgets to modernize safety systems, grid controls, and packaging lines. Each vertical arrives with distinct technical profiles, yet all converge on the need for data continuity from sensor to business-planning layer. Suppliers able to speak the language of both process and discrete industries, while bundling cybersecurity and training, secure cross-vertical reach and higher deal velocity. As a result, the Mexico factory automation and industrial controls market stays diversified, cushioning cyclical shocks in any one sector.

By Deployment Mode: Hybrid Configurations Bridge Cloud Ambitions and Operational Constraints

On-premise deployments held 48.81% share in 2025 because sub-10-millisecond response times, network determinism, and air-gapped security remain non-negotiable in welding, tablet coating, and distillation applications. Yet hybrid architecture exhibits the fastest 8.13% CAGR, satisfying the chief information officer’s appetite for elastic analytics while appeasing plant managers wary of internet latency. Typical designs keep real-time loops inside the firewall and mirror sanitized data to a cloud lake for demand forecasting, carbon tracking, and what-if scenario planning. Companies cite reduced licensing overhead, smoother upgrade paths, and unified multi-site dashboards as decisive benefits.

Cloud-only approaches still win in logistics tracking, fleet telematics, and non-critical reporting where latency tolerance is wide. However, cyber-attack volumes on supervisory control and data acquisition networks have surged, nudging risk officers toward architectures that insulate controllers from direct web exposure. Hybrid therefore strikes a pragmatic middle ground, offering the scalability of cloud with the resilience of local execution, and it will dominate new deployments as reference templates mature.

Geography Analysis

Nuevo León, Querétaro, Jalisco, Guanajuato, and Baja California together commanded about 70% of the Mexico factory automation and industrial controls market in 2025. Nuevo León’s Monterrey corridor hosts more than 200 tier-one suppliers, metal-forming specialists, and aerospace shops, ensuring a steady pipeline of robot welding, vision inspection, and conveyor-control orders. Querétaro leans on multi-sector clusters that span appliances, automotive interiors, and medical glass, each demanding traceable, flexible lines; the region’s industrial park expansions embed redundant fiber backbones and edge-compute nodes as standard fit-out, simplifying later automation upgrades. Jalisco thrives on pharmaceutical and electronics exports, anchoring the largest domestic rollout of AI quality-control algorithms across 14 plants run by a leading generics maker.

Aguascalientes, San Luis Potosí, and the wider Bajío corridor are increasingly attractive because of central logistics and a skilled yet affordable workforce. Bosch Rexroth’s recent hydraulics plant launch demonstrates confidence in local casting and machining supply chains, while HVAC and heavy-equipment brands invest to shorten time-to-U.S. market. Baja California maintains leadership in medical devices and consumer electronics, consuming pick-and-place robots, automated optical inspection stations, and surface-mount technology feeders in high volumes. State governments reinforce the appeal through streamlined permitting, dual-training programs, and partial cash grants tied to job creation.

By contrast, southern states such as Chiapas, Oaxaca, and Yucatán still trail in industrial density, reflecting limited road networks and smaller supplier bases. Nevertheless, large infrastructure projects and near-port logistics improvements may pivot some assembly and packaging capacity southward after 2028. For now, the Mexico factory automation and industrial controls market remains decisively concentrated north and center, where cross-border trucking lanes, robust power grids, and engineering talent co-locate.

Competitive Landscape

The ten largest vendors, led by ABB, Siemens, Schneider Electric, Rockwell Automation, and Honeywell, aggregate roughly 55-60% share, while dozens of midsize and niche players split the balance. Chinese robot makers such as ESTUN, Rokae, and Elite compete aggressively on price, undercutting incumbent average selling prices by up to 30% and pushing hardware toward commoditization. This shift forces established suppliers to lean into software ecosystems, life-cycle services, and local manufacturing to preserve margins and reinforce customer stickiness. System integrators, once brand-loyal, now adopt robot-agnostic platforms that allow mixed fleets, giving end users more leverage and eroding single-vendor lock-in.

Acquisition activity underscores the race for breadth. Applied Industrial Technologies purchased Grupo Kopar to deepen robotics and machine-vision coverage, while Beckhoff prepares a Querétaro technology center to train integrators on PC-based control and AI-assisted programming. Local production plans from Siemens, Schneider Electric, and Balluff emphasize faster lead times and tariff hedging, reflecting how geopolitics shapes sourcing strategies. Collaborative robots and low-code configuration tools lower entry barriers for small and medium enterprises, expanding the addressable base and spawning service opportunities around application engineering, cyber-hardening, and continuous improvement. Altogether, rivalry is migrating from component features to ecosystem completeness, talent enablement, and speed of value realization.

Mexico Factory Automation And Industrial Controls Industry Leaders

ABB Ltd.

Rockwell Automation Inc.

Honeywell International Inc.

Omron Corporation

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Beckhoff Automation Mexico revealed a technology center in Querétaro to strengthen partner support and train system integrators in PC-based control, intralogistics automation, and AI-enabled programming.

- November 2025: FOTON committed MXN 1,200 million (USD 65 million) to open a third assembly plant in Tlajomulco de Zuñiga, Jalisco and expand existing sites, aiming for 60-70% local content.

- November 2025: The Aguascalientes government and OMRON Group agreed to create a demonstration center and joint engineer-training program covering sensors, collaborative robots, and programmable controllers.

Mexico Factory Automation And Industrial Controls Market Report Scope

Factory automation employs control systems, including computers and robots, to oversee and streamline industrial processes within manufacturing settings. This broad field integrates diverse technologies, ranging from machinery and processes to information systems, all designed to boost production efficiency, improve accuracy, and lessen the need for human intervention in repetitive tasks. With the adoption of automated systems, factories can not only elevate their productivity and consistency but also enhance safety and cut down on operational costs. Industrial controls form the cornerstone of factory automation, enabling the monitoring and management of production equipment and processes. These controls encompass a variety of types, including programmable logic controllers (PLCs), distributed control systems (DCS), and supervisory control data acquisition (SCADA) systems, among others. Each type is pivotal in ensuring the smooth and efficient operation of industrial activities.

The market is defined by the revenue generated from the sale of different types of factory automation and industrial control systems products and solutions offered by different market players across Mexico.

The Mexico Factory Automation and Industrial Controls Market Report is Segmented by Solution (Industrial Control Systems [Distributed Control System (DCS), Supervisory Control and Data Acquisition (SCADA), Programmable Logic Controller (PLC), Human Machine Interface (HMI), and Other Industrial Control Systems], Field Devices [Sensors and Transmitters, Valves and Actuators, Motors and Drives, Robotics, and Other Field Devices], Software [Product Lifecycle Management (PLM), Enterprise Resource Planning (ERP), Manufacturing Execution System (MES), and Other Softwares], Services [Integration, and Maintenance and Training]), Automation Type (Fixed Automation, Programmable Automation, Flexible or Modular Automation, and Integrated or Hyper-Automation), End-User Industry (Automotive and Transportation, Oil and Gas, Food and Beverage, Pharmaceuticals and Life Sciences, Power and Utilities, Chemicals and Petrochemicals, Metals and Mining, Fast-Moving Consumer Goods (FMCG), Packaging, and Others End-User Industries), Deployment Mode (On-Premise, Cloud, and Hybrid), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Solution

| Industrial Control Systems | Distributed Control System (DCS) |

| Supervisory Control and Data Acquisition (SCADA) | |

| Programmable Logic Controller (PLC) | |

| Human Machine Interface (HMI) | |

| Other Industrial Control Systems | |

| Field Devices | Sensors and Transmitters |

| Valves and Actuators | |

| Motors and Drives | |

| Robotics | |

| Other Field Devices | |

| Software | Product Lifecycle Management (PLM) |

| Enterprise Resource Planning (ERP) | |

| Manufacturing Execution System (MES) | |

| Other Softwares | |

| Services | Integration |

| Maintenance and Training |

By Automation Type

| Fixed Automation |

| Programmable Automation |

| Flexible or Modular Automation |

| Integrated or Hyper-Automation |

By End-user Industry

| Automotive and Trasnportation |

| Chemicals and Petrochemicals |

| Power and Utilities |

| Pharmaceutical and Life Sciences |

| Food and Beverage |

| Oil and Gas |

| Other End-user Industries |

By Deployment Mode

| On-Premise |

| Cloud |

| Hybrid |

| By Solution | Industrial Control Systems | Distributed Control System (DCS) |

| Supervisory Control and Data Acquisition (SCADA) | ||

| Programmable Logic Controller (PLC) | ||

| Human Machine Interface (HMI) | ||

| Other Industrial Control Systems | ||

| Field Devices | Sensors and Transmitters | |

| Valves and Actuators | ||

| Motors and Drives | ||

| Robotics | ||

| Other Field Devices | ||

| Software | Product Lifecycle Management (PLM) | |

| Enterprise Resource Planning (ERP) | ||

| Manufacturing Execution System (MES) | ||

| Other Softwares | ||

| Services | Integration | |

| Maintenance and Training | ||

| By Automation Type | Fixed Automation | |

| Programmable Automation | ||

| Flexible or Modular Automation | ||

| Integrated or Hyper-Automation | ||

| By End-user Industry | Automotive and Trasnportation | |

| Chemicals and Petrochemicals | ||

| Power and Utilities | ||

| Pharmaceutical and Life Sciences | ||

| Food and Beverage | ||

| Oil and Gas | ||

| Other End-user Industries | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the expected revenue for Mexico’s factory automation and industrial controls market by 2031?

Revenue is projected to reach USD 8.87 billion by 2031, reflecting a 6.81% CAGR from 2026.

Which solution segment is growing the fastest?

Software, driven by manufacturing execution systems and digital-twin applications, is advancing at a 7.21% CAGR through 2031.

Why are hybrid deployment models gaining popularity?

Hybrid architectures blend the low-latency reliability of on-premise control with cloud-based analytics and multi-site visibility, growing at an 8.13% CAGR.

Which industry vertical will outpace automotive in automation spending?

Pharmaceutical and life sciences is projected to grow at an 8.04% CAGR, fueled by stringent traceability and quality-control needs.

How does nearshoring influence automation demand?

Relocation of North-American manufacturers to Mexico concentrates greenfield plants that specify integrated automation from the outset, adding roughly 1.8 percentage points to the forecast CAGR.

What is the chief barrier to faster adoption of advanced controls?

A persistent shortage of engineers skilled in industrial networking and AI-based programming delays projects and inflates commissioning costs.

Page last updated on: