Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 16.39 Billion |

| Market Size (2026) | USD 17.17 Billion |

| Market Size (2031) | USD 21.66 Billion |

| Growth Rate (2026 - 2031) | 4.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Home Appliances Market Analysis by Mordor Intelligence

Mexico home appliances market size in 2026 is estimated at USD 17.17 billion, growing from 2025 value of USD 16.39 billion with 2031 projections showing USD 21.66 billion, growing at 4.76% CAGR over 2026-2031. Rising remittances that exceed 3% of GDP, stricter NOM-015 efficiency labeling, and resilient consumer sentiment create a sturdy demand floor despite periodic peso volatility[1]Diario Oficial de la Federación, “NORMA Oficial Mexicana NOM-015-ENER-2012,” dof.gob.mx. Nearshoring policies motivate global brands to expand Mexican production lines, shortening delivery lead-times and supporting localized component sourcing. Retailers accelerate Buy-Now-Pay-Later rollouts that pull aspirational households into mid-tier price brackets, while e-commerce firms refine last-mile networks to reach semi-urban buyers. Energy-conscious urban dwellers, especially in Mexico City and Monterrey, increasingly favor inverter-grade refrigerators and laundry systems that promote long-term utility-bill savings, reinforcing premiumization inside the Mexico home appliances market.

Key Report Takeaways

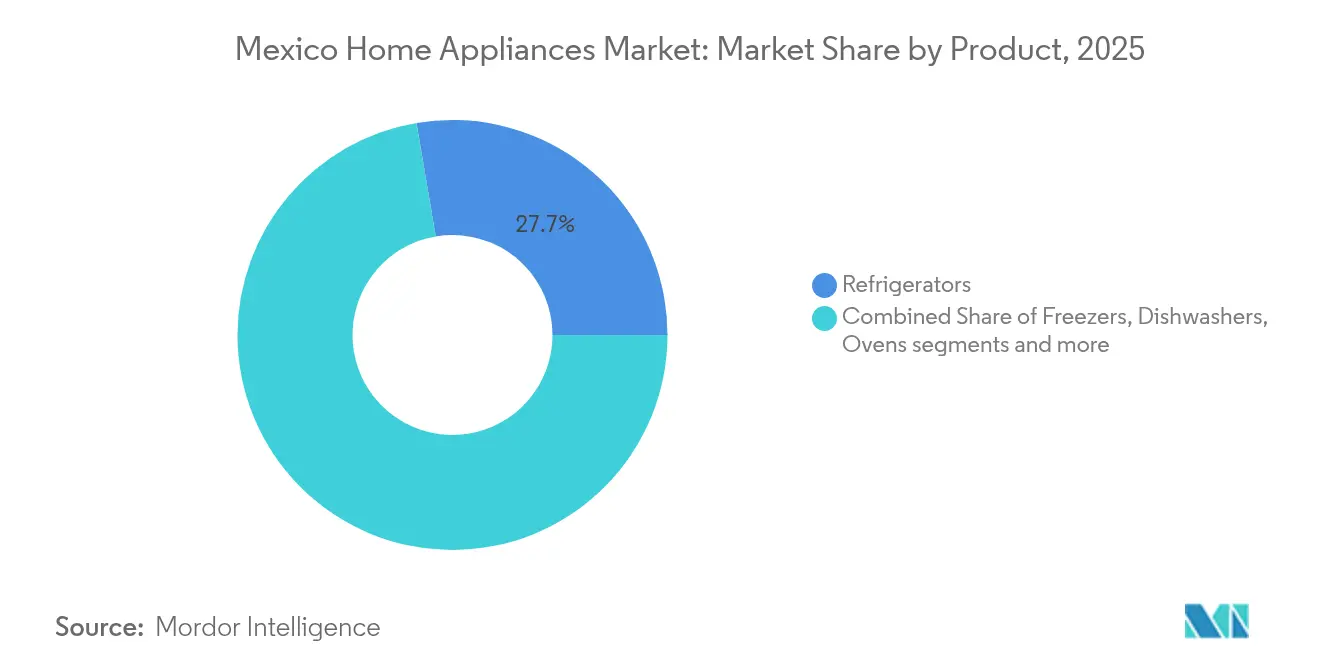

- By product category, refrigerators held 27.68% of the Mexico home appliances market share in 2025, whereas air fryers are projected to post the fastest 4.97% CAGR through 2031.

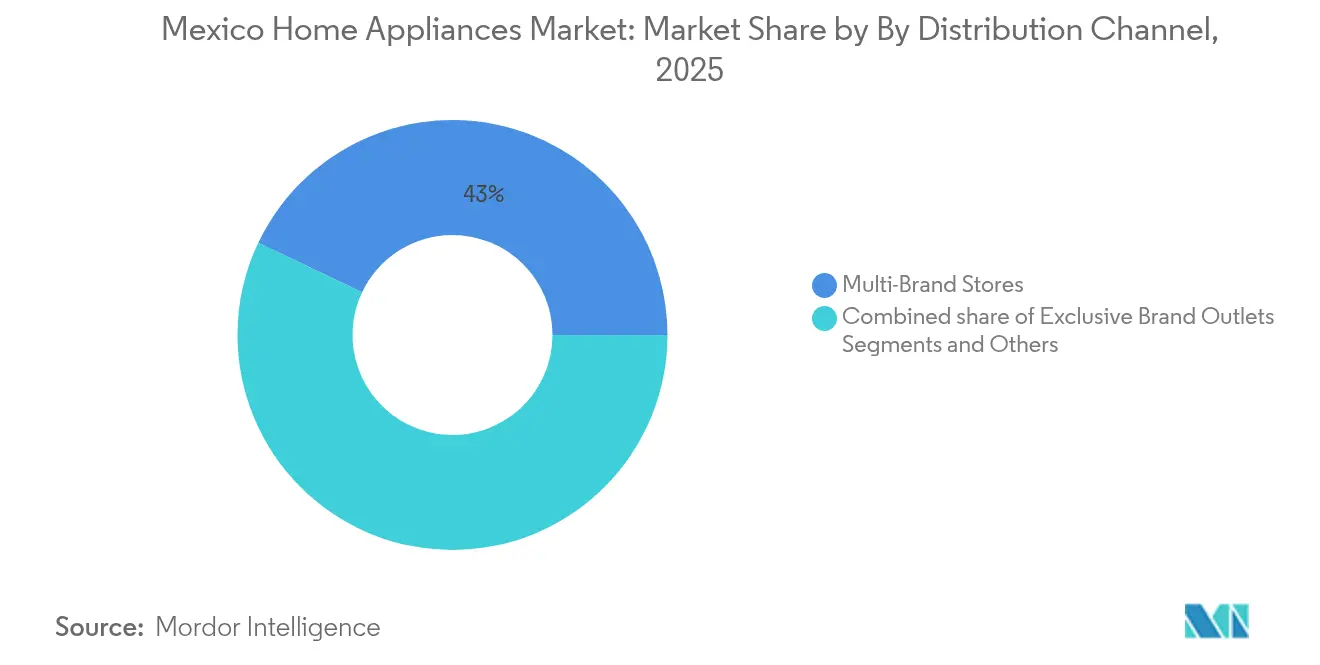

- By distribution channel, multi-brand stores accounted for 42.95% of the Mexico home appliances market size in 2025, while online retail is advancing at a 5.63% CAGR through 2031.

- By geography, Central Mexico captured a 40.82% revenue share in 2025; Southern Mexico is forecast to expand at a 5.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & middle-class expansion | +1.2% | National: strongest in Central Mexico | Medium term (2-4 years) |

| Accelerated urban housing construction | +0.8% | Central and Northern corridors | Short term (≤ 2 years) |

| Mandatory NOM-015 energy-efficiency labeling | +0.6% | National | Long term (≥ 4 years) |

| Remittance-fueled home upgrades | +0.9% | Central and Southern Mexico | Medium term (2-4 years) |

| Buy-Now-Pay-Later retail financing | +0.7% | Urban clusters nationwide | Short term (≤ 2 years) |

| Cross-border e-commerce inflows from the United States | +0.5% | Northern Mexico; spillover to Central | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Middle-Class Expansion

Consumer confidence touched 46.3 points in February 2025, and the likelihood of purchasing household appliances and furniture edged higher by 0.6 points, suggesting selective optimism among newly affluent families. Durable goods imports soared 21.7% in August 2024, while domestic production climbed 11.6%, confirming a healthy appetite even amid mixed macro signals. Consumer credit stood at MXN 2.1 trillion by Q4 2024, enabling access to energy-efficient refrigerators, smart ovens, and split-type air conditioners. Remittances boost liquidity in rural municipalities, bridging purchasing-power gaps and broadening the customer base for premium appliances. Elevated electricity tariffs reinforce the cost-saving narrative around A-rated units, deepening the Mexico home appliances market’s shift toward high-efficiency SKUs.

Accelerated Urban Housing Construction

Urban housing starts in Mexico City, Monterrey, and Guadalajara quicken replacement cycles because new units require full appliance bundles. INFONAVIT and FOVISSSTE mortgages allow first-time owners to allocate residual credit to up-market washers or side-by-side refrigerators. Builders increasingly mandate NOM-compliant appliances to meet municipal green-building codes, embedding higher technical standards into project specifications. Proximity to assembly plants in Guanajuato and Nuevo León lowers freight outlays, allowing manufacturers to guarantee one-week delivery to construction sites. Predictable tranche ordering smooths production scheduling, reducing inventory risk and elevating gross-margin visibility inside the Mexico home appliances market.

Mandatory NOM-015 Energy-Efficiency Labeling

NOM-015-ENER-2012 caps annual energy consumption for refrigerators and freezers and obliges manufacturers to display kWh/year data plus relative savings on a front-of-pack label. Models that beat the ceiling by 10% qualify for an “EFICIENCIA SUPERIOR” seal that retailers highlight in both showrooms and digital catalogs. Accredited labs conduct annual conformity tests unless firms hold certified quality systems that extend validity to three years, forcing continuous R&D investment. Parallel standards such as NOM-021-ENER raise performance thresholds for air conditioners, effectively blocking low-efficiency imports. Over time, mandatory labeling bolsters consumer trust and rewards innovators, anchoring long-run value capture across the Mexico home appliances market.

Remittance-Fueled Home Upgrades

Remittances equal roughly 3% of national GDP and proved counter-cyclical during recent downturns, supplying households with steady cash that cushions disposable income. Guanajuato, Michoacán, and Oaxaca record above-average flows, and retailers serving those states report heightened sales of frost-free refrigerators and multi-program washers. Lenders have introduced remittance-backed instalment plans pegged to expected monthly inflows, letting buyers move into the mid-tier price band without straining liquidity. Premium finishes and advanced cooling features signal socioeconomic progress, making appliances a favored investment among recipients. This income stream stabilizes baseline demand, sheltering the Mexico home appliances market from domestic macro shocks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peso volatility & consumer-credit tightening | -1.4% | National: hardest on import-intensive lines | Short term (≤ 2 years) |

| High domestic logistics & last-mile costs | -0.9% | Nationwide, the steepest in Southern Mexico | Medium term (2-4 years) |

| Informal second-hand appliance market growth | -0.6% | Urban centers | Medium term (2-4 years) |

| Water scarcity concerns for water-intensive units | -0.4% | Northern and Central arid belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Peso Volatility & Consumer-Credit Tightening

Peso swings amplify the landed cost of compressors and electronic boards sourced from Asia, squeezing gross margins or forcing retail mark-ups that deter entry-level shoppers. Commercial banks curbed unsecured lending in late 2024, increasing approval thresholds and limiting credit-card limits, which dampens installment-based purchases. Budget-constrained buyers either delay replacement cycles or migrate to used-goods marketplaces, trimming unit shipments in segments like frost-free freezers. Import-dependent brands remain most vulnerable, as they lack peso-denominated cost buffers inside the Mexico home appliances market.

High Domestic Logistics & Last-Mile Costs

Large appliances traverse mountainous terrain and urban congestion, pushing transport fees to more than half of the delivered unit cost. In low-density states such as Chiapas and Guerrero, average final-mile distance exceeds 120 kilometers, inflating vehicle wear, fuel consumption, and driver labor. E-commerce players wrestle with double-handling needs—warehouse to micro-hub to doorstep—while also absorbing high reverse-logistics rates for returns. Elevated shipping outlays compress margins and discourage free-delivery promotions, slowing digital conversion in the Mexico home appliances market’s hardest-to-reach districts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Major Appliances Anchor Revenue, Small Appliances Accelerate Innovation

Refrigerators maintained a 27.68% share of the Mexico home appliances market in 2025, strengthened by mandatory replacement cycles and energy-label compliance that phase out power-hungry imports. Nominal utility rates have risen, spurring demand for inverter compressors, multi-door formats, and smart-thaw functionality. Washing machines trail closely, aided by dual-tub units popular in semi-urban homes, while room air conditioners gain ground as average summer temperatures climb. Dishwashers face mixed adoption because of water-scarcity worries, whereas microwave-convection hybrids thrive in compact kitchens where space efficiency rules. Collectively, large appliances supply the economies of scale that keep factory utilization high in the Mexico home appliances market.

Air fryers headline the small-appliance story with a projected 4.97% CAGR to 2031, buoyed by fast-cooking convenience and health-oriented meal prep trends. Coffee machines and electric kettles ride Mexico’s expanding specialty-beverage culture, while juicers and blenders suit rising demand for fresh produce diets. Vacuum cleaners, including robotic variants, grow steadily as two-income households seek labor-saving tools. Accelerated design cycles and lower price points let brands introduce Wi-Fi connectivity, voice controls, and modular components without disturbing household budgets. The small-appliance category, therefore, acts as the innovation sandbox within the Mexico home appliances market.

By Distribution Channel: Store Formats Rebalance as E-Commerce Climbs

Multi-brand stores controlled 42.95% of the Mexico home appliances market in 2025 by leveraging broad assortments, same-day pickup, and on-site credit desks that clear loans in minutes. Showrooms allow shoppers to test door hinges, assess noise levels, and gauge real-world capacity—attributes still hard to replicate via online thumbnails. Chains deploy regional warehouses adjacent to highway junctions, shaving transport time and enabling weekend flash sales coordinated across hundreds of outlets.

Online platforms post the sharpest 5.63% CAGR, fueled by smartphone penetration, digital-wallet incentives, and nationwide expansion of fiber networks. Partnerships with Kueski Pay and other Buy-Now-Pay-Later providers deliver zero-interest schemes that rival legacy in-store credit. Exclusive brand stores, both brick-and-mortar and digital, craft curated environments that justify premium pricing on smart-enabled SKUs. Click-and-collect, augmented-reality product demos, and 360-degree video consultations blur channel boundaries, pushing the Mexico home appliances market toward omnichannel parity.

Geography Analysis

Central Mexico dominated the Mexico home appliances market with a 40.82% share in 2025, thanks to the Mexico City megalopolis, denser retail footprints, and higher discretionary income. Same-day delivery services flourish within ring highways, while condo living favors slimline, energy-rated appliances that minimize utility costs and fit compact layouts. Corporate headquarters demand commercial refrigeration and laundry solutions, further raising throughput.

Northern Mexico benefits from maquiladora clusters and cross-border buying behaviors. Consumers in Baja California and Sonora often compare U.S. and domestic prices before purchasing, leading retailers to sharpen promotions to hold local share. Per-capita electricity use in Mexicali runs 3.5 times the national mean, elevating adoption of split-inverter air conditioners and reinforcing the Mexico home appliances market’s focus on climate control. Nearshoring drives component producers to establish hubs in Coahuila and Nuevo León, enhancing supply resilience.

Southern Mexico emerges as the fastest-growing territory, targeting a 5.09% CAGR via remittance-backed spending and public infrastructure upgrades that include road expansions and improved grid stability. Retailers deploy micro-fulfillment centers to overcome rugged terrain and poor road density. Water-efficient washers and eco-wash dishwashers resonate in Chiapas and Oaxaca, where periodic shortages make conservation a top priority. Although freight costs remain steep, localized assembly partnerships help contain end-user pricing, broadening reach inside the Mexico home appliances market.

Competitive Landscape

The competitive field is moderately concentrated. Home-grown Mabe leverages factories in Guanajuato and Nuevo León to remain a category leader in refrigerators and cooking ranges. Whirlpool’s USD 65 million Celaya expansion, finished in December 2024, equips the firm to supply premium French-door units nationally while hedging currency exposure through peso-denominated costs. Samsung and LG tap both domestic plants and cross-border distribution nodes to shorten lead times within Northern Mexico, deploying periodic promotional blitzes whenever the peso weakens.

China-based Jiaxipera opened a USD 60 million compressor facility in Coahuila, boosting regional self-sufficiency for refrigeration systems. Arçelik, operating the Beko brand, integrated Whirlpool’s European assets to acquire procurement heft that extends to its Mexican sourcing operations. Retail financing alliances matter: Kueski Pay’s embedded-checkout APIs help smaller brands compete head-to-head with entrenched giants by smoothing high-ticket transactions. NOM certifications, audited by JJR Laboratory, function as gatekeepers that block low-quality imports, compelling entrants to invest in robust testing and QA processes[3]University of Louisville, “The Dangers Posed by Open-Flame Cooking: The Case of Chiapas, Mexico,” louisville.edu. Technology differentiation, after-sales servicing, and localized production strategies therefore outweigh mere unit-price tactics across the Mexico home appliances market.

Mexico Home Appliances Industry Leaders

Whirlpool Corporation

Mabe

Electrolux AB

LG Electronics

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The U.S. home-improvement giant signed a definitive deal to absorb Mexico’s second-largest DIY chain, adding 20 stores and entering the Mexico City metro area for the first time. Management expects the transaction to expand category assortments—especially large appliances—and unlock procurement synergies by integrating national suppliers into the broader North American network.

- March 2025: Dawoon Refrigeration announces Nuevo León plant. An initial USD 18 million will finance Phase 1 tooling for refrigeration components, with USD 25 million Phase 2 slated for 2027, which will triple capacity. The Korean firm cites customer proximity to Monterrey-area appliance OEMs as a primary locational advantage.

- February 2025: Kueski Pay tops 15 million loan milestone. The fintech confirms that appliance purchases now represent more than 20% of their total loan volume. New integrations with Whirlpool México and other OEM portals let shoppers split payments into 12 interest-free installments, supporting e-commerce penetration in the Mexico home appliances market.

- December 2024: Whirlpool completes Celaya capacity upgrade. The USD 65 million outlay expands annual assembly capacity for premium French-door models and introduces a new plastics recycling loop within the plant. Company officials highlight the upgrade’s role in meeting NOM-015 requirements while cutting logistics costs for central and southern distribution routes.

Mexico Home Appliances Market Report Scope

The Mexican home appliance market is segmented by major appliances, small appliances, and distribution channels. By major appliances, the market is segmented into refrigerators, freezers, dishwashing machines, washing machines, ovens, air conditioners, and other major appliances. By small appliances, the market is segmented into coffee and tea makers, food processors, grills, toasters, vacuum cleaners, and other small appliances. By distribution channels, the market is segmented into mass merchandisers, exclusive stores, online, and other distribution channels. The report offers market size and forecasts in value (USD) for all the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Countertop Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| Northern Mexico |

| Central Mexico (incl. Mexico City) |

| Southern Mexico |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Countertop Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | Northern Mexico | |

| Central Mexico (incl. Mexico City) | ||

| Southern Mexico | ||

Key Questions Answered in the Report

How large is the Mexico home appliances market today?

It is valued at USD 17.17 billion in 2026 and is projected to reach USD 21.66 billion by 2031.

Which channel is expanding fastest for major appliance sales?

Online retail is growing at a 5.63% CAGR as smartphones, digital wallets, and BNPL tools gain traction.

What is driving the popularity of air fryers across Mexico?

Health-focused cooking, compact countertop needs, and quick meal prep underpin a 4.97% CAGR outlook.

Why does Central Mexico hold the biggest regional share?

High urban density, superior logistics, and elevated disposable incomes secure a 40.82% 2025 share.

How do NOM standards influence purchasing decisions?

Mandatory energy labels steer shoppers toward efficient models and force manufacturers to innovate to remain compliant.

What risks could slow near-term appliance demand?

Peso volatility, tighter consumer credit, and rising logistics costs are the chief near-term brakes on growth.

Page last updated on: