Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

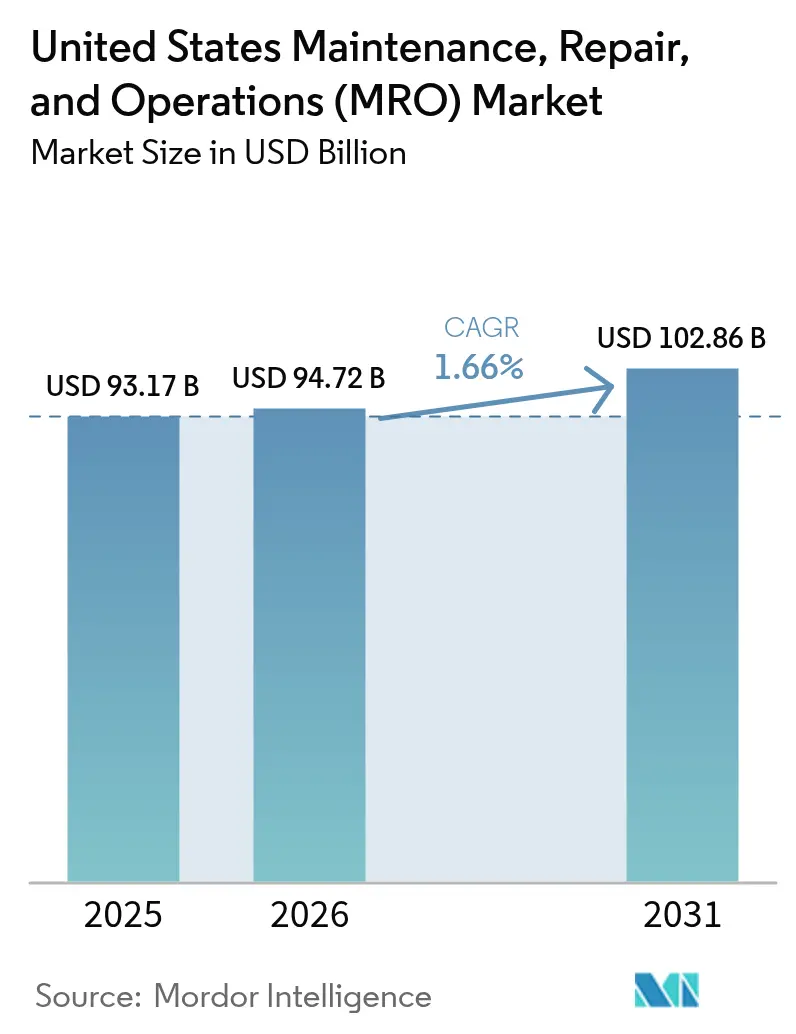

| Base Year Market Size (2025) | USD 93.17 Billion |

| Market Size (2026) | USD 94.72 Billion |

| Market Size (2031) | USD 102.86 Billion |

| Growth Rate (2026 - 2031) | 1.66% CAGR |

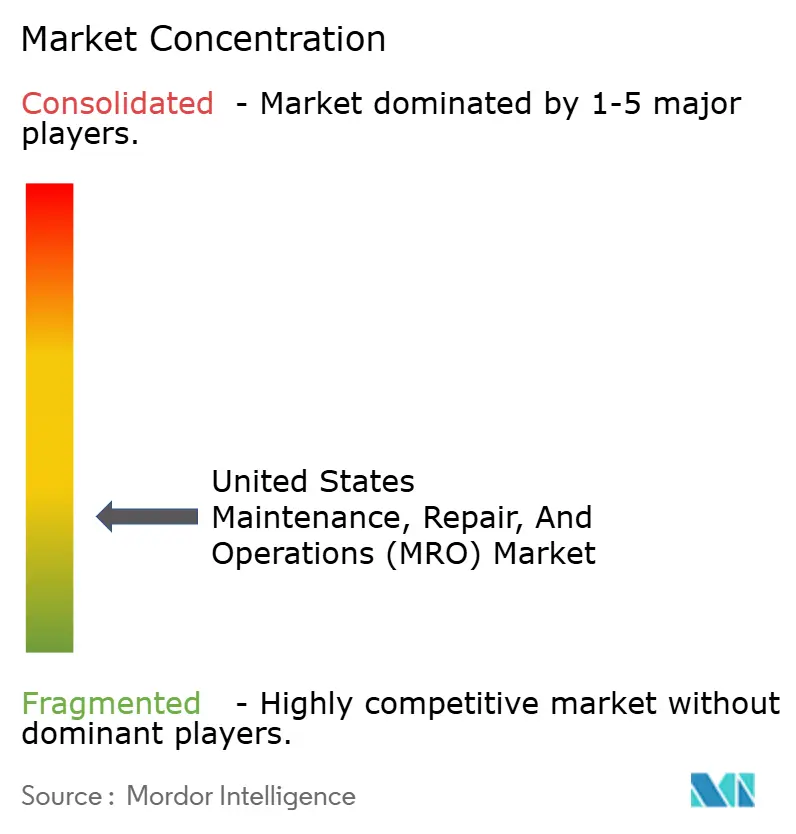

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Maintenance, Repair, And Operations (MRO) Market Analysis by Mordor Intelligence

The United States Maintenance, Repair, And Operations Market size was valued at USD 93.17 billion in 2025 and estimated to grow from USD 94.72 billion in 2026 to reach USD 102.86 billion by 2031, at a CAGR of 1.66% during the forecast period (2026-2031). This outlook reflects the market’s maturity, limited by structural labor shortages yet supported by federal infrastructure spending and rapid digitalization of procurement. Moderate growth is anchored by an expanding installed base of industrial assets, rising demand for energy-efficient retrofits, and wider use of predictive maintenance software. Policy incentives from the Infrastructure Investment and Jobs Act, the CHIPS and Science Act, and the Inflation Reduction Act continue to stimulate capital investment in semiconductor fabs, battery plants, and clean-energy projects, all of which rely on high-value MRO services. At the same time, e-commerce penetration accelerates as buyers migrate to integrated online platforms that streamline sourcing, reduce transaction volume, and improve inventory visibility. Despite these opportunities, the market contends with acute skilled-labor shortages, shrinking distributor gross margins, and ongoing supply-chain volatility that inflates carrying costs and lengthens lead times. Consolidation among rental and distribution companies remains a primary competitive response, with more than USD 15 billion in recent acquisitions aimed at scale efficiencies and expanded geographic coverage.

Key Report Takeaways

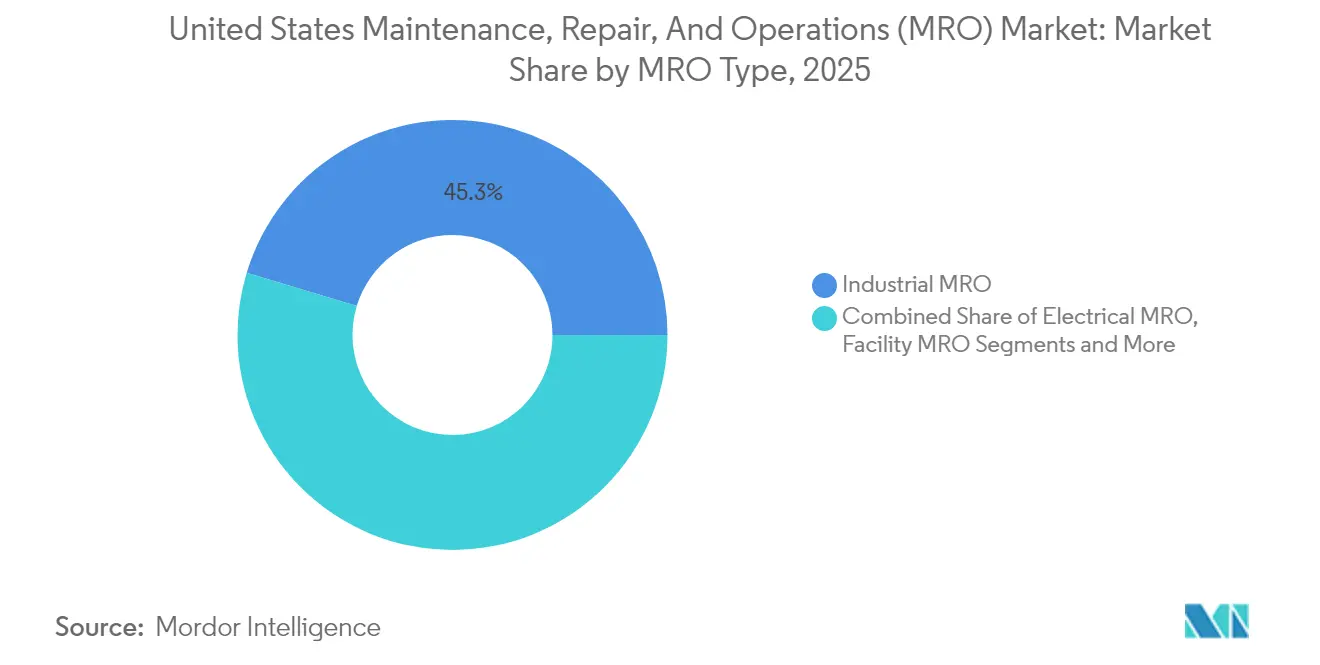

- By MRO type, industrial MRO led with 45.32% revenue share of the United States maintenance, repair, and operations market share in 2025, while electrical MRO recorded the highest projected CAGR at 2.75% through 2031.

- By end-user industry, manufacturing accounted for 37.62% share of the United States maintenance, repair, and operations market size in 2025, and healthcare is expanding at a 2.56% CAGR through 2031.

- By sourcing model, in-house maintenance held 51.36% share of the United States maintenance, repair, and operations market size in 2025; integrated supply is set to grow at a 1.78% CAGR over 2026-2031.

- By maintenance approach, preventive maintenance represented 57.48% share of the United States maintenance, repair, and operations market size in 2025, whereas predictive maintenance is forecast to rise at a 2.06% CAGR to 2031.

- By distribution channel, offline distributors maintained 63.25% share of the United States maintenance, repair, and operations market size in 2025, and online/e-commerce channels are advancing at a 1.88% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Maintenance, Repair, And Operations (MRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Predictive maintenance driven cost savings | +0.4% | National, concentrated in manufacturing hubs | Medium term (2-4 years) |

| Aging industrial assets increasing repair cycles | +0.3% | National, emphasis on Rust Belt and Gulf Coast | Long term (≥ 4 years) |

| E-commerce penetration of MRO supplies | +0.2% | National, accelerated in urban centers | Short term (≤ 2 years) |

| Reshoring investments expanding installed base | +0.3% | Southeast, Southwest, and Great Lakes regions | Long term (≥ 4 years) |

| Federal incentives for energy-efficient retrofits | +0.2% | National, prioritizing industrial corridors | Medium term (2-4 years) |

| Additive manufacturing for on-demand spares | +0.1% | Aerospace clusters and advanced manufacturing zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Predictive Maintenance Driven Cost Savings

Organizations adopting predictive programs report eliminating more than 50% of unplanned downtime and cutting defects by over 70%, shifting MRO from a cost center to a value generator. Aviation operators increasingly embed condition-based monitoring in fleet management contracts, and industrial facilities pair IoT sensors with analytics platforms to secure service-level guarantees. Vendors capable of delivering data-backed uptime commitments command premium rates, while buyers benefit from lower lifecycle costs and higher equipment availability. The growing roster of government-funded Industrial Assessment Centers further diffuses predictive know-how across mid-sized manufacturers. [1]U.S. Department of Energy, “Industrial Assessment Centers (IACs),” energy.gov As predictive solutions scale, software fees and sensor retrofits become recurring revenue streams for service providers, reinforcing the positive CAGR contribution.

Aging Industrial Assets Increasing Repair Cycles

A large share of U.S. industrial machinery installed during the 1950s–1960s is now operating beyond its design life, driving more frequent maintenance events and higher spend per asset. Chemical and petrochemical facilities in the Gulf Coast face heightened regulatory scrutiny, prompting mandated overhauls of pressure vessels and piping systems. Public transit agencies report a USD 50-80 billion backlog for railcar, track, and facility rehabilitation . In aviation, the average certified mechanic age of 54 years underscores the urgency of asset-integrity management programs that minimize safety risks while extending service life. These dynamics collectively increase demand for inspection services, condition assessments, and refurbishment parts, supporting steady revenue growth for the United States MRO market.

E-commerce Penetration of MRO Supplies

Digital procurement platforms now list millions of SKUs, enabling buyers to compare specifications, price, and availability in real time. The shift online compresses purchasing cycles and facilitates vendor-managed inventory that lowers on-hand stock levels by up to 20%. Large distributors report that contractual e-commerce transactions comprise more than 70% of total MRO revenue, indicating a permanent change in buyer behavior. Widespread use of AI chatbots and guided search tools simplifies product selection, particularly for small and medium enterprises that previously lacked dedicated procurement teams. As penetration deepens, digital channels capture incremental share from local branches, adding modest tailwinds to market growth while intensifying price transparency.

Reshoring Investments Expanding Installed Base

Annual outlays for manufacturing construction have doubled to nearly USD 190 billion, fueled by reshoring incentives targeting semiconductors, electric vehicles, and renewable energy equipment. More than 50 chip-fabrication projects and 200 clean-energy facilities are underway or announced, predominantly in the Southeast, Southwest, and Great Lakes regions. Each new plant introduces thousands of assets, HVAC, automation, tooling, requiring ongoing MRO. Spending commitments by firms such as GE Aerospace, which earmarked almost USD 1 billion for U.S. site upgrades in 2025, illustrate how capital projects translate into long-tail service demand. The enlarged installed base bolsters the United States maintenance, repair, and operations market by widening its serviceable universe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin pressure from product commoditization | -0.2% | National, acute in competitive metropolitan markets | Short term (≤ 2 years) |

| Supply-chain volatility and inventory shortages | -0.3% | National, concentrated in import-dependent regions | Medium term (2-4 years) |

| Skilled MRO labor shortage | -0.4% | National, severe in aerospace and manufacturing hubs | Long term (≥ 4 years) |

| Cyber-security risks in connected equipment | -0.1% | National, critical in infrastructure and defense sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Margin Pressure from Product Commoditization

Price transparency on digital platforms reduces distributor mark-ups across standard fasteners, bearings, and consumables. During 2024, leading distributors reported sequential gross-margin declines as customers migrated to lowest-cost suppliers and expanded use of private-label alternatives. [2]Fastenal Company, “Fastenal Company Reports 2025 First Quarter Earnings,” fastenal.com With market leader Grainger holding only 7% share, no participant wields sufficient scale to set industry pricing. Distributors increasingly emphasize value-added services, such as on-site vending, kitting, and technical training, to preserve margins, yet these services entail upfront investment and longer payback periods that strain near-term profitability.

Supply-Chain Volatility and Inventory Shortages

Port congestion, geopolitical disputes, and component scarcity drive extended lead times and higher freight rates, forcing buyers to raise safety-stock levels. Import-dependent regions feel the impact most acutely, particularly for electrical components sourced from Asia. Distributors carry the financial burden of larger inventories, while OEMs confront production delays when critical parts are unavailable. Although federal incentives aim to localize manufacturing, new domestic capacity will take years to materially ease supply-chain pressure, keeping the drag on the United States maintenance, repair, and operations market in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By MRO Type: Industrial Core with Electrical Momentum

Industrial MRO generated 45.32% of 2025 revenue, underpinned by the extensive machinery base in manufacturing, mining, and process industries. The United States maintenance, repair, and operations market size for industrial applications is fueled by reshoring investments in semiconductor fabrication, automotive electrification, and aerospace assembly. High-hour utilization rates create steady replacement cycles for seals, bearings, and hydraulic components. Electrical MRO, projected to grow at 2.75% CAGR to 2031, benefits from grid-modernization grants and plant electrification mandates that boost demand for switchgear, drives, and sensors. As federal incentives accelerate energy-efficiency upgrades, service providers specializing in electrical retrofits capture incremental market share.

The facility MRO segment maintains stable demand from building-system upkeep, including HVAC, roofing, and plumbing, while the “other” category comprises specialized niches such as medical-device calibration and telecom-equipment servicing. Convergence of operational technology and IT blurs traditional boundaries, particularly as interconnected systems require technicians who can manage both mechanical and cyber-security tasks. Providers that integrate multi-disciplinary teams secure longer-term service agreements at favorable margins.

By End-User Industry: Manufacturing Scale Meets Healthcare Upside

Manufacturing commanded 37.62% of the United States maintenance, repair, and operations market share in 2025, supported by USD 57 billion in machinery upkeep and additional fault-related spending. Heavy-industry clusters in the Great Lakes and Gulf Coast create consistent demand for pump, valve, and gearbox overhauls. Yet healthcare leads in growth, advancing at 2.56% CAGR through 2031 as hospitals retrofit aging infrastructure and comply with stringent equipment-maintenance standards. Federal funding under the Infrastructure Investment and Jobs Act earmarks billions for hospital energy upgrades, further expanding the healthcare serviceable market.

Energy and utilities remain steady contributors, driven by pipeline-integrity programs and power-plant life-extension projects. Aerospace and defense demand rebounds alongside higher fleet-utilization rates, with engine-maintenance services surfacing as a high-margin niche. Construction cycles introduce volatility, but the rising prevalence of modular and off-site fabrication increases opportunities for pre-emptive maintenance planning and aftermarket parts supply.

By Sourcing Model: From In-House Control to Integrated Supply

In-house teams continue to manage 51.36% of maintenance expenditure as organizations prioritize direct oversight of mission-critical assets. However, the talent crunch and the need for digital tools propel integrated-supply models to a 1.78% CAGR, funneling spend to vendor-managed-inventory programs. These programs typically lower transaction counts by up to 10% and reduce carrying costs by double-digit percentages, making them attractive amid margin pressure. Outsourcing to third-party maintenance, repair, and operations specialists allows manufacturers to focus on core production while accessing scarce expertise in predictive analytics and cyber-security.

Integrated facility-management providers extend value by combining janitorial, grounds, and MRO services under unified contracts. Faster time-to-repair and reduced stockouts improve equipment availability, enhancing overall plant productivity and reinforcing the migration away from purely internal maintenance teams.

By Maintenance Approach: Preventive Backbone, Predictive Inflection

Preventive schedules account for 57.48% of market revenue, favored for regulatory compliance and ease of planning. Nevertheless, predictive strategies are taking hold, projected at 2.06% CAGR as sensor prices fall and analytics platforms mature. Plants deploying predictive protocols typically cut maintenance spend by 10-15% while raising uptime, strengthening the value proposition despite higher initial investment. Corrective/reactive work persists in cost-sensitive settings but increasingly faces scrutiny from insurers and regulators that penalize unplanned downtime and safety risks.

Scaling predictive maintenance depends on data integration across enterprise resource planning, computerized maintenance management systems, and asset-performance tools. Vendors offering seamless interoperability win contracts, positioning predictive services as a critical differentiator in the United States MRO market.

By Distribution Channel: Offline Stronghold Meets Online Surge

Offline distributors held 63.25% share in 2025 through branch networks that provide immediate inventory and technical advice. Local stock remains vital for breakdown situations where downtime costs eclipse expedited-freight fees. Yet online and e-commerce channels are advancing at 1.88% CAGR as procurement departments digitize workflows and adopt punch-out catalogs within enterprise systems. Major distributors report double-digit growth in endless-assortment websites, signaling sustainable channel migration. Direct-from-OEM sales preserve relevance for proprietary components requiring engineering sign-off or warranty compliance.

Hybrid models emerge, combining local service centers with centralized digital marketplaces to deliver both speed and breadth. Distributors that integrate real-time inventory data, AI-enabled search, and automated order fulfillment position themselves to capture disproportionate share of the United States maintenance, repair, and operations market.

Geography Analysis

Industrial density and asset age create pronounced regional patterns in service demand. The Great Lakes and Midwest retain the largest share due to legacy automotive, steel, and chemicals plants that depend on routine overhaul of high-hour machinery. The Southeast and Southwest register the fastest growth as semiconductor fabs in Arizona and Texas and EV-battery plants in Tennessee and Georgia come online under CHIPS and Inflation Reduction Act incentives. Gulf Coast refineries and petrochemical complexes continue to anchor demand for corrosion-control and turnaround services.

California and Washington dominate aerospace MRO thanks to OEM final-assembly lines and airline hub operations, while Texas hosts a dense cluster of line-maintenance providers at Dallas-Fort Worth and Houston airports. Healthcare-related MRO distributes evenly, yet the Northeast and Midwest face elevated retrofit needs owing to older hospital buildings, increasing demand for HVAC upgrades and life-safety systems.

Regional policy also shapes opportunities: right-to-work states in the South attract greenfield factories that embed predictive maintenance from commissioning, whereas older facilities in unionized northern states prioritize refurbishment under asset-management regulations. Service providers with multi-regional footprints and mobile technician fleets are best positioned to address the varied geographic requirements of the United States MRO market.

Competitive Landscape

The United States maintenance repair and operations market remains fragmented. W.W. Grainger, Fastenal, MSC Industrial, Wesco, and Applied Industrial Technologies anchor the traditional distribution channel, yet each faces margin pressure from e-commerce competition and private-label encroachment. Recent M&A activity centers on fleet rental firms and specialty distributors seeking scale to negotiate supplier terms and invest in technology. For example, United Rentals’ USD 4.8 billion purchase of H and E Equipment Services added 64,000 fleet units and enhances cross-sell potential of maintenance packages to construction customers. [3]International Rental News, “The Biggest Equipment Rental Acquisitions of 2025 So Far,” internationalrentalnews.com

Digital-native entrants leverage low-overhead platforms to offer broader assortments and dynamic pricing, challenging incumbents to accelerate omnichannel strategies. OEMs such as GE Aerospace increasingly bundle parts, software, and field services into performance-based contracts that bypass traditional distribution for high-end components. Compliance with OSHA’s hazardous-waste regulations and ISO 55000 asset-management standards constitutes a barrier to entry, favoring established providers with certified processes and documented safety records.

United States Maintenance, Repair, And Operations (MRO) Industry Leaders

Ferguson PLC

Motion Industries Inc. (Genuine Parts Company)

Airgas Inc. (Air Liquide SA)

DNOW Inc. (DistributionNOW)

HD Supply Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE Aerospace announced nearly USD 1 billion investment across U.S. plants to raise output of commercial and defense components. The strategic commitment secures domestic supply capacity and creates downstream MRO demand for newly installed equipment.

- March 2025: Atlas Copco agreed to buy National Tank and Equipment for USD 218 million, marking its entry into the U.S. specialty dewatering niche and broadening rental-service offerings to energy customers.

- January 2025: United Rentals completed the acquisition of H and E Equipment Services for USD 4.8 billion, aiming to expand fleet depth and realize USD 250 million in cost and revenue synergies within three years. The deal strengthens its presence in high-growth Sunbelt construction markets.

- October 2024: VSE Corporation disclosed a USD 200 million purchase of Kellstrom Aerospace to deepen commercial-aviation aftermarket exposure and diversify its OEM support portfolio.

United States Maintenance, Repair, And Operations (MRO) Market Report Scope

Maintenance, repair, and operations (MRO) items are products and materials purchased by companies that are not directly employed in their manufacturing process. These products are mainly used to keep business operations running. The maintenance, repair, and operations (MRO) include spare parts, equipment, and consumables used by a company to manufacture end products. MRO includes spare parts, equipment, such as pumps and valves, consumables, cleaning supplies, plant upkeep supplies, lubricants, and activities completed to restore or maintain the functioning of the required equipment.

The scope of the study includes the revenues accrued from the said components by service vendors for electrical, industrial, and facility establishments. Further, the study tracks the significant developments, end-user trends, and market forecasts in the United States, which currently occupies around 85% of the total market demand in North America. The study tracks the impact of the COVID-19 outbreak on demand patterns and end-user spending.

The United States maintenance, repair & operations (MRO) market is segmented by industrial MRO (end-user industry [manufacturing, construction, chemicals & petrochemicals, food, beverage & paper processing, others]), electrical MRO (end-user industry [manufacturing (process and non-process), construction, chemicals and petrochemicals, food, beverage and paper processing, other end-user industries]), facility MRO (end-user industry [healthcare and social assistance, manufacturing, construction, other end-user industries]). The report offers market forecasts and size in value (USD) for all the above segments.

By MRO Type

| Industrial MRO |

| Electrical MRO |

| Facility MRO |

| Other MRO Types |

By End-User Industry

| Manufacturing |

| Energy and Utilities |

| Aerospace and Defense |

| Construction |

| Healthcare |

| Other End-user Industries |

By Sourcing Model

| In-house |

| Outsourced (3rd-party/IFM) |

| Integrated Supply (VMI/Integrated-MRO) |

By Maintenance Approach

| Preventive / Scheduled |

| Corrective / Reactive |

| Predictive / Condition-based |

By Distribution Channel

| Offline Distributors |

| Online / E-commerce |

| Direct from OEM |

| By MRO Type | Industrial MRO |

| Electrical MRO | |

| Facility MRO | |

| Other MRO Types | |

| By End-User Industry | Manufacturing |

| Energy and Utilities | |

| Aerospace and Defense | |

| Construction | |

| Healthcare | |

| Other End-user Industries | |

| By Sourcing Model | In-house |

| Outsourced (3rd-party/IFM) | |

| Integrated Supply (VMI/Integrated-MRO) | |

| By Maintenance Approach | Preventive / Scheduled |

| Corrective / Reactive | |

| Predictive / Condition-based | |

| By Distribution Channel | Offline Distributors |

| Online / E-commerce | |

| Direct from OEM |

Key Questions Answered in the Report

How big is the United States Maintenance, Repair, And Operations Market?

The United States Maintenance, Repair, And Operations Market size is expected to reach USD 94.72 billion in 2026 and grow at a CAGR of 1.66% to reach USD 102.86 billion by 2031.

What is the current United States Maintenance, Repair, And Operations Market size?

In 2026, the United States Maintenance, Repair, And Operations Market size is expected to reach USD 94.72 billion.

Who are the key players in United States Maintenance, Repair, And Operations Market?

DNOW Inc. (DistributionNOW), Airgas Inc. (Air Liquide SA), Ferguson PLC, Motion Industries Inc. (Genuine Parts Company) and HD Supply Holdings Inc. are the major companies operating in the United States Maintenance, Repair, And Operations Market.

What years does this United States Maintenance, Repair, And Operations Market cover, and what was the market size in 2025?

In 2025, the United States Maintenance, Repair, And Operations Market size was estimated at USD 93.17 billion. The report covers the United States Maintenance, Repair, And Operations Market historical market size for years: 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the United States Maintenance, Repair, And Operations Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: