Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

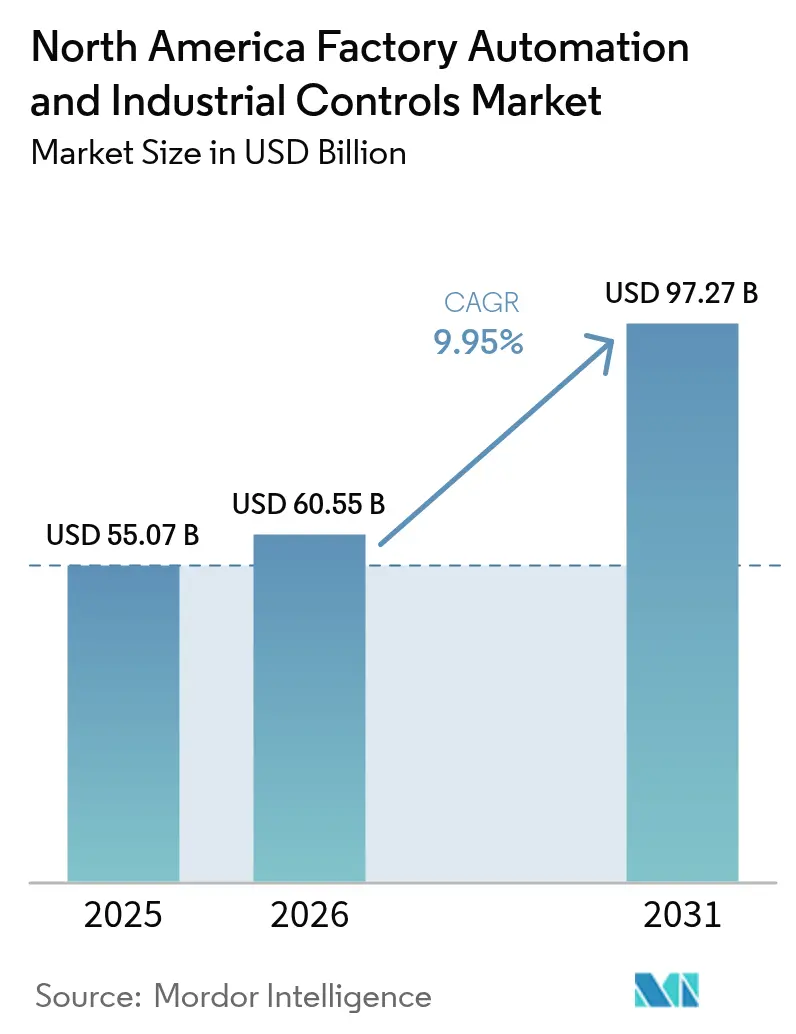

| Base Year Market Size (2025) | USD 55.07 Billion |

| Market Size (2026) | USD 60.55 Billion |

| Market Size (2031) | USD 97.27 Billion |

| Growth Rate (2026 - 2031) | 9.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The North America factory automation and industrial controls market size was valued at USD 55.07 billion in 2025 and estimated to grow from USD 60.55 billion in 2026 to reach USD 97.27 billion by 2031, at a CAGR of 9.95% during the forecast period (2026-2031). This expansion follows sustained investment in intelligent manufacturing ecosystems, ongoing labor shortages, tightening energy-efficiency mandates, and generous federal incentives that reward domestic production upgrades. Manufacturers now treat automation as a strategic necessity that protects output, quality, and supply continuity when skilled talent is limited and global logistics remain unpredictable. Vendors pushing software-centric architectures gain traction because analytics unlock incremental yield, energy savings, and asset longevity without major hardware overhauls. Demand also rises for secure, standards-based platforms that can move data between on-premise, edge, and cloud layers while limiting cyber-exposure. Overall, the North America factory automation and industrial controls market continues to outpace broader capital-equipment spending as factories elevate resilience in every budget cycle.

Key Report Takeaways

- By type, industrial control systems captured 58.15% of the North America factory automation and industrial controls market share in 2025, while field devices advanced at an 10.85% CAGR through 2031.

- By component, hardware commanded 60.05% of the North America factory automation and industrial controls market size in 2025; software is set to expand at an 10.98% CAGR.

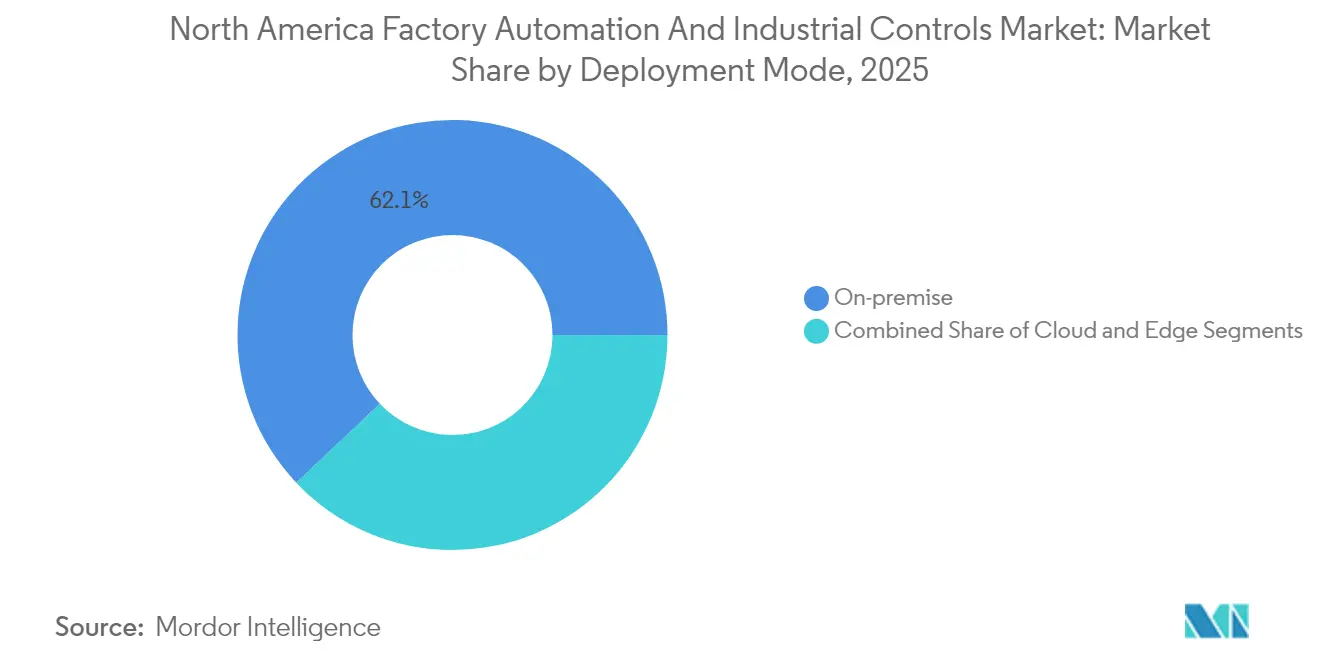

- By deployment, on-premise platforms retained 62.05% share of the North America factory automation and industrial controls market in 2025, with cloud solutions scaling at an 11.1% CAGR to 2031.

- By end-user industry, automotive led with 29.05% revenue share of the North America factory automation and industrial controls market in 2025; pharmaceuticals posts the fastest 11.55% CAGR to 2031.

- By country, the United States held 85.15% of the North America factory automation and industrial controls market share in 2025, while Mexico grew at an 11.05% CAGR on near-shoring momentum.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for energy-efficient manufacturing operations | +1.8% | United States and Canada, with spillover to Mexico | Medium term (2-4 years) |

| Rapid adoption of collaborative robots in SME factories | +1.5% | North America, with concentrated impact in US Midwest and Southern Ontario | Short term (≤ 2 years) |

| Federal incentives accelerating on-shoring of electronics production | +2.1% | United States, with secondary benefits to Mexico and Canada | Long term (≥ 4 years) |

| Integration of 5G-enabled industrial IoT networks | +1.2% | Global, with early deployment in US and Canadian urban manufacturing centers | Medium term (2-4 years) |

| Shortage of skilled labor spurring autonomous material handling | +1.7% | North America, particularly acute in US and Canadian manufacturing regions | Short term (≤ 2 years) |

| AI-driven predictive maintenance reducing unplanned downtime | +1.4% | Global, with advanced adoption in US and Canadian facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in demand for energy-efficient manufacturing operations

Manufacturers across North America implement advanced control loops, load balancing, and real-time energy dashboards to meet strict state and provincial efficiency rules and to cut utility costs. Retrofitting variable-frequency drives and intelligent scheduling modules into legacy lines typically lowers total electricity consumption by 20% to 30%.[1]Assembly Magazine Staff, “North American Robotics Market Holds Steady in 2024,” Assembly Magazine, assemblymag.com Savings arrive faster than productivity-led paybacks, which accelerates board approval for additional automation projects. Facilities integrating on-site renewable power with smart controllers participate in grid-stabilization programs that offer new revenue streams. Vendors that package commissioning services with ISO 50001 advisory win contracts because plant teams need holistic road maps, not just hardware. As carbon pricing discussions resurface in Washington and Ottawa, early movers lock sustainable cost advantages that compound over time.

Rapid adoption of collaborative robots in SME factories

Small and mid-size enterprises adopt collaborative robots priced between USD 110,000 and USD 200,000 because the units require minimal guarding and can be re-tasked by existing technicians.[2]Business Development Bank of Canada Editors, “Robotics and Automation in Metal Fabrication,” BDC, bdc.ca Cobots handle repetitive pick-and-place, machine tending, and light assembly while employees focus on value-added inspection. Payback periods often fall below 18 months when overtime premiums and scrap reductions are considered. The flexibility to shift between SKUs without re-engineering entire lines aligns with the low-volume, high-variety production typical of North American SMEs. As success stories spread through regional manufacturing associations, peer endorsement accelerates wider deployments, further enlarging the North America factory automation and industrial controls market.

Federal incentives accelerating on-shoring of electronics production

The CHIPS and Science Act and the Inflation Reduction Act grant up to 25% tax credits on qualified automation equipment and fund new semiconductor fabs, expanding the North America factory automation and industrial controls market far beyond historical auto-centric spending. Greenfield projects specify high-throughput robotics, wafer-level clean-room handling, and real-time statistical-process-control software because domestic labor costs exceed those in Asia. Contract manufacturers replicate these investments in printed-circuit-board assembly to secure Tier-1 customer contracts. Secondary effects include booming demand for system integrators in Arizona, Texas, and upstate New York, where fabs cluster. Suppliers that embed cybersecurity and traceability by design position themselves as preferred partners for federally funded sites with strict compliance audits.

AI-driven predictive maintenance reducing unplanned downtime

Edge sensors stream vibration, temperature, and current signatures into machine-learning algorithms that flag anomalies weeks before bearing or gearbox failures. Plants report up to 50% reductions in unexpected outages and 10-40% maintenance cost savings after deploying such systems, strengthening the North America factory automation and industrial controls market outlook. Cloud analytics pools multi-plant data, letting corporate reliability teams benchmark assets and standardize spares inventories. When insights route directly to maintenance-work-order software, technicians schedule repairs during planned changeovers, minimizing production loss. Vendors bundling digital twins with service contracts capture recurring revenue and deepen customer lock-in. Boards increasingly view AI-enabled reliability as insurance against margin-crushing stoppages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity vulnerabilities in legacy control systems | -1.3% | North America, with particular concern in critical infrastructure sectors | Short term (≤ 2 years) |

| Capex freeze among mid-tier manufacturers amid high interest rates | -0.9% | United States and Canada, affecting SME automation investments | Short term (≤ 2 years) |

| Supply-chain volatility for critical automation components | -1.1% | Global, with specific impact on North American manufacturing timelines | Medium term (2-4 years) |

| Fragmented North American interoperability standards | -0.7% | North America, creating integration complexity and increased costs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity vulnerabilities in legacy control systems

The Cybersecurity and Infrastructure Security Agency disclosed multiple remote-code-execution flaws in widely deployed PLC and HMI platforms during 2024.[3]Cybersecurity and Infrastructure Security Agency, “ICS Advisory Archive 2024,” CISA, cisa.gov Plants that rushed to connect isolated networks for remote monitoring now face expanded attack surfaces. Patching often requires costly downtime or controller replacement, which stretches maintenance budgets. Insurance premiums climb as underwriters reassess operational-technology risk. Some facilities delay new digitization until zero-trust architectures mature, temporarily slowing the North America factory automation and industrial controls market.

Supply-chain volatility for critical automation components

Persistent semiconductor shortages lengthen lead times for PLC CPUs, industrial PCs, and servo drives to as much as 40 weeks. System integrators redesign cabinets around whatever controllers are available, increasing commissioning hours and documentation complexity. Smaller manufacturers without bulk-purchase leverage must either pay spot premiums or postpone projects, moderating short-term growth. Vendors respond through multi-sourcing strategies and lifecycle-management portals that alert customers before parts reach end-of-life. While disruptions taper by 2026, procurement uncertainty remains a planning headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Control Systems Drive Integration Complexity

Industrial control systems generated the largest revenue in 2025 with a 58.15% share of the North America factory automation and industrial controls market. Field devices displayed stronger momentum, recording an 10.85% CAGR that is lifting sensor and vision-system suppliers. Integration complexity between centralized controllers and proliferating edge devices motivates buyers to favor unified engineering suites. The North America factory automation and industrial controls market size attached to distributed control systems and PLC upgrades continues to rise as plants modernize legacy code and add contextual data layers.

Growth in field devices stems from collaborative robotics, advanced machine vision, and multi-axis motion kits that bolster quality assurance and throughput. Vendors offering out-of-the-box links to major control platforms shorten project cycles, a key factor for tier-one automotive lines targeting shorter model launches. Continuous streaming of device data into analytics hubs also feeds AI models that refine cycle timing and predictive maintenance rules. As a result, software libraries and protocol converters bundled with hardware now command premium margins across the North America factory automation and industrial controls market.

By Component: Software Transforms Operational Intelligence

Hardware still contributed 60.05% of 2025 revenue, reflecting the physical assets installed across thousands of factories. Software, however, advances at an 10.98% CAGR as plants unlock latent data for productivity and sustainability gains. Cloud historians, AI toolkits, and digital twins increasingly ship alongside drives and sensors, proving that value creation has migrated toward code. The North America factory automation and industrial controls market size linked to industrial-software subscriptions is on track to rival discrete hardware outlays by 2031.

Edge-to-cloud architectures let plants collect high-frequency signals locally while pushing summarized insights to central dashboards. Simulation packages help engineers test recipe changes offline, reducing scrap at launch. Augmented-reality work instructions improve technician accuracy and shorten training curves. Integration of cybersecurity modules within standard licenses also answers board and insurer demands for risk mitigation, elevating software from an optional add-on to a strategic requirement.

By Deployment Mode: Hybrid Architectures Balance Performance and Flexibility

On-premise installations accounted for 62.05% of 2025 spending because deterministic response remains essential for safety-critical loops. Yet cloud deployments rise at an 11.1% CAGR as factories accept that centralized analytics offer economies of scale. Edge servers provide the bridge, executing latency-sensitive tasks while synchronizing with cloud AI engines. This hybrid pattern broadens the customer base of the North America factory automation and industrial controls market because even conservative operators can adopt cloud modules without surrendering local autonomy.

Vendors now pre-configure edge gateways with secure containers and automatic patch management. 5G private networks enable mobile robots and augmented-reality devices that demand low latency beyond Wi-Fi limits. As telcos expand coverage inside industrial parks, more workloads shift off-premise, including compute-intensive vision inference. The shift gradually changes revenue recognition from upfront licenses toward recurring platform fees.

By End-user Industry: Automotive Leadership Faces Pharmaceutical Disruption

Automotive retained 29.05% revenue share in 2025 through continuous investment in battery-module assembly, paint-shop robotics, and flexible chassis lines. Electric-vehicle programs in Michigan, Tennessee, and Ontario commission turnkey automation cells that use vision to guide gluing, riveting, and laser welding. At the same time, pharmaceuticals register a 11.55% CAGR, the strongest among end-users, because serialization, clean-room robotics, and real-time release testing demand high-integrity control. The North America factory automation and industrial controls market size allocated to life-science plants, therefore, rises faster than that of traditional discrete sectors.

Food and beverage operators invest in automated inspection and packaging to address worker scarcity and contamination-prevention mandates, while oil and gas firms focus on remote pipeline telemetry that pairs with AI fault detection. Across verticals, the common thread is data-driven decision loops that boost uptime and compliance, reinforcing the relevance of software analytics within every capital request.

Geography Analysis

The United States accounted for 85.15% of 2025 revenue thanks to sizable federal incentives, deep supplier ecosystems, and robust telecom infrastructure. Semiconductor-fab and battery-cell projects in Arizona, Texas, and Ohio specify high levels of process control and robotics, magnifying orders for controllers, vision cameras, and automated material handling. Digital-twin pilots inside Midwestern auto plants demonstrate cycle-time cuts that spread across supplier tiers. As a result, the North America factory automation and industrial controls market experiences technology diffusion at an unprecedented speed in the United States.

Mexico marks the fastest expansion with an 11.05% CAGR to 2031 because near-shoring reduces logistics risk and import tariffs. Automotive, electronics, and aerospace OEMs locate final assembly south of the U.S. border yet demand identical automation standards to ensure warranty consistency. Nuevo León and Querétaro clusters draw system integrators that previously served only U.S. clients. Regional governments fund technical institutes to supply robot programmers, reinforcing the local talent pool. Consequently, cross-border integration projects account for a growing slice of the North America factory automation and industrial controls market.

Canada follows a steady upgrade path focused on resource extraction, food processing, and clean-tech component manufacturing. Harsh climatic conditions and strict safety codes drive the adoption of rugged control hardware and predictive analytics that prevent unplanned outages in remote locations. Provincial grants offset currency-exchange headwinds, enabling mid-size plants to modernize. Collaboration between Canadian universities and OEMs accelerates breakthroughs in machine vision for lumber grading and mining haul-truck automation, broadening the addressable opportunity.

Regulatory Landscape

The regional regulatory environment increasingly links factory automation decisions to cybersecurity, safety, and cross-border conformity. In the United States, the Cybersecurity and Infrastructure Security Agency (CISA) promotes ISA/IEC 62443-aligned practices for industrial control systems and OT products, reinforcing secure-by-design expectations for control platforms that connect to enterprise IT and cloud analytics. For power and utilities end users, the U.S. Federal Energy Regulatory Commission (FERC) approved Reliability Standard CIP-003-11 on March 24, 2026, along with multiple modified CIP standards that address secure application of virtualization and newer technologies in bulk-power system cyber environments. This raises the compliance bar for control-system architectures in critical infrastructure.

Safety and market-access requirements also shape equipment selection and machine-building practices across North America. In Canada, CSA Z434-2026 updates robot and robot-cell safety by incorporating ISO 10218-1:2025 and ISO 10218-2:2025 with Canadian deviations, while CSA C22.2 No. 301:23 defines safety requirements for industrial electrical machinery used in automation-intensive equipment. At the trade-policy level, CUSMA (USMCA) provisions supporting harmonized standards and reduced technical barriers influence how OEMs and integrators document conformity, test procedures, and compliance evidence when deploying multi-vendor automation systems across the United States, Canada, and Mexico.

Value Chain Analysis

The value chain starts with semiconductors, embedded compute, sensors, drives, and motion components feeding controller and robot OEMs, then moves through machine builders, system integrators, distributors, and software suppliers that deliver engineering, commissioning, and lifecycle services. Lead-time and component availability risk remains a choke point for PLC CPUs, industrial PCs, and servo drives, which, in turn, increases the emphasis on authorized distribution, safety-stock strategies, and multi-sourcing programs when end users plan line upgrades or greenfield builds.

Software ecosystems and partner networks account for a larger share of delivered value as plants adopt digital twin workflows, orchestration, and AI-enabled maintenance. For example, Siemens partnering with Xometry (including a USD 50 million minority investment) supports embedding AI-native sourcing and pricing intelligence into Siemens Xcelerator, while Siemens partnering with IFS connects engineering intelligence with operational execution through industrial AI. On delivery, platform-led automation tightens links between robot OEMs and modular cell providers, such as Vention integrating FANUC America robots into its AI-powered design and deployment environment, and Novarc Technologies signing an MoU with Yaskawa America to integrate AI-powered welding intelligence onto Yaskawa robotic platforms. In this setup, interoperable software, application know-how, and service capability shape time-to-production.

Competitive Landscape

The North America factory automation and industrial controls market displays moderate consolidation, with the top five vendors providing integrated hardware, software, and lifecycle services. Rockwell Automation aligns with Microsoft to embed Azure AI into FactoryTalk, while Siemens partners with NVIDIA to accelerate digital-twin rendering.[4]Rockwell Automation Technical Paper, “How Innovation Is Shaping Auto Sector Supply Chains,” Rockwell Automation, rockwellautomation.com ABB expands its Robotics and Discrete Automation campus in Michigan to shorten delivery times for collaborative units.

Mid-tier specialists fill white space in mobile robotics, vision-guided bin picking, and cyber-physical security. KUKA’s KR C5 controller cuts energy draw and cabinet footprint, showcasing incremental innovation that matters in retrofit projects. Cognex and Basler release higher-resolution, AI-ready cameras that integrate via OPC UA, allowing plug-and-play with dominant PLC brands.

Service ecosystems now influence buying decisions as much as product specs. Vendors offering 24/7 remote support, virtual commissioning, and operator-training simulators command price premiums. Cybersecurity qualifications, such as ISO 27001 and alignment with NIST SP 800-82, increasingly appear in request-for-proposal checklists. Market entrants that cannot demonstrate secure development lifecycles struggle despite competitive pricing.

North America Factory Automation And Industrial Controls Industry Leaders

Rockwell Automation Inc.

Siemens AG

Mitsubishi Electric Corporation

ABB Ltd.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity is in software-defined coordination layers that reduce integration friction across mixed fleets of controllers, robots, and autonomous material handling. Public launches at Automate 2026 reflected this shift, including Rockwell Automation unveiling FactoryTalk Orchestration to unify OTTO AMRs with machine-level controls and manufacturing workflows, and Siemens demonstrating Smart Production Orchestration to contextualize shop-floor OT data for enterprise integration using multi-agent AI concepts. These releases create whitespace for plants that already have core PLC, SCADA, and robotics assets but need higher-level orchestration, production logistics coordination, and standardized data context without replacing deterministic control layers.

A second opportunity comes from North American capacity expansion and internal supply-chain automation programs that pull demand for robots, field devices, controls, and integration services. FANUC America announced a USD 90 million investment for an 840,000-square-foot Michigan facility to expand U.S.-based robot manufacturing capacity (targeted for completion in late 2027), and GE Vernova signed a definitive agreement to acquire Robotech Automation, a Canadian systems integrator, to accelerate robotics and automation deployment across its supply chain factories. Alongside federal programs referenced in this report, including CHIPS and Science Act and Inflation Reduction Act incentives for production upgrades, these moves support a sustained pipeline for system integrators, edge and analytics software providers, and retrofit-focused modernization offerings that address labor constraints, energy efficiency, and cyber requirements.

Recent Industry Developments

- June 2026: Schneider Electric signed a definitive agreement to acquire Cognite for USD 3.1 billion, adding an established industrial data and AI software stack to its automation portfolio. The deal strengthens Schneider Electric's ability to deliver context-rich industrial analytics above controllers and field devices, supporting OT/IT convergence and multi-site standardization.

- May 2026: Siemens announced it surpassed USD 1 billion in cumulative U.S. manufacturing investments, spanning expansions across multiple states. The milestone indicates continued localization of industrial capacity and supply chains, supporting shorter lead times and closer technical support for factory automation and industrial controls deployments.

- October 2024: Mitsubishi Electric Power Products Inc. announced an USD 86 million investment to build a new approximately 160,000-square-foot switchgear manufacturing facility in Western Pennsylvania. The project expands regional production of electrification equipment that interfaces with industrial control systems, supporting modernization programs in factories and power-intensive industrial sites.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers spending on factory automation and industrial control technologies used to monitor, control, and automate industrial operations across North America, covering solutions deployed in manufacturing and process environments.

Scope exclusions: We exclude demand and revenues generated outside North America, and we do not count unrelated enterprise IT systems that are not used for industrial control or automation.

Segmentation Overview

- By Type

- Industrial Control Systems

- Distributed Control System (DCS)

- Programmable Logic Controller (PLC)

- Supervisory Control and Data Acquisition (SCADA)

- Product Lifecycle Management (PLM)

- Human Machine Interface (HMI)

- Manufacturing Execution System (MES)

- Field Devices

- Machine Vision Systems

- Robotics (Industrial)

- Sensors and Transmitters

- Motors and Drives

- Other Field Devices

- Industrial Control Systems

- By Component

- Hardware

- Software

- Services

- By Deployment Mode

- On-premise

- Cloud

- Edge

- By End-user Industry

- Oil and Gas

- Chemical and Petrochemical

- Power and Utilities

- Food and Beverages

- Automotive

- Metals and Mining

- Pharmaceuticals

- Other Industries

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand pool and to sanity check the direction of key automation indicators before deeper modeling was done. We referred to public and official sources such as the US Census Bureau (manufacturing and capital spending series), the Federal Reserve (industrial production and capacity utilization), the US Bureau of Labor Statistics (employment and productivity trends), and the US International Trade Commission trade statistics for relevant equipment categories.

To ground the industry narrative, we also reviewed company annual reports and investor presentations, earnings call transcripts, association publications, and reputed press coverage on automation investments and plant expansions. Where required, paid subscriptions were used in a limited way for company financials and news screening, and to locate patent activity patterns that support technology adoption timing. These desk sources are not exhaustive, and many other public documents and datasets were also used to collect, validate, and clarify information during the research.

Primary Interviews and Surveys

Primary work was carried out through expert interviews and structured surveys with a mix of automation suppliers, system integrators, distributors, and end users from major manufacturing hubs across the region. Because not every data series is available at the same level of detail, these discussions were used to confirm adoption timing, typical deal sizes, and the share of spend tied to new projects versus modernization, and then to align assumptions across countries and end-user industries.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | |

| Mid tier: 47% | Functional/Unit leaders: 38% | |

| Smaller Players: 18% | Managers: 48% |

Market-Sizing & Forecasting

The sizing starts from a top-down build where manufacturing output, industrial production, and capital expenditure signals are translated into an automation and controls spending pool by end-user industries, and then allocated across the covered countries. Once that first view is built, we corroborated it using selective bottom-up approximations such as sampled average selling price assumptions for key device groups, supplier revenue cues from public disclosures, and channel checks with integrators, which are then used to adjust totals where gaps showed up.

A few practical inputs were tracked closely because they move this market in visible ways, including industrial production index trends, factory utilization rates, plant expansion announcements, reshoring related investment cycles, and the mix shift between new installations and retrofit upgrades. For forecasting, scenario analysis was applied so that a base case path could be tested against slower and faster investment conditions that interviewees commonly referenced, followed by smoothing of near-term volatility to avoid over-reacting to one-off quarterly spikes. Where bottom-up data was incomplete for smaller categories, gap handling was done using range-based penetration assumptions tied back to the industry demand pool and validated again through follow-up calls.

Data Validation & Update Cycle

Validation is done by checking whether outputs line up with independent signals such as manufacturing capex direction, control hardware shipment trends visible in trade statistics, and the timing of large automation project cycles discussed by practitioners. When a variance stands out, the assumptions are revisited, the math is rechecked, and relevant experts are re-contacted so we do not carry forward an untested jump.

Before sign-off, the model and key assumptions go through multi-step analyst reviews so that coverage, unit logic, and country allocations remain consistent. Reports are refreshed annually, and interim updates are made when material events shift near-term demand, after which a final pre-delivery review is done to ensure the latest public information is reflected.

Mordor Intelligence's North America Factory Automation and Industrial Controls Market Size Compared With Other Published Estimates

Published market sizes for factory automation and industrial controls in North America often do not match because the scope boundaries are not always the same, and the year being reported can differ even when the titles look similar. Differences also come from how firms treat pricing over time, whether they include adjacent automation software and services, and how recently they have refreshed their base-year inputs.

The table below points to a wide spread that can largely be explained by scope and year alignment, followed by how demand indicators are translated into revenue. Some estimates start from a narrower device list, while others fold in broader automation spending without clearly separating industrial control devices from nearby categories, and then the totals move again when currency timing and inflation assumptions are not applied consistently across the period.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 55.07 B (2025) | |

| Regional Consultancy A | USD 16.40 B (2024) | This figure appears to use a narrower combined scope and an earlier base year, which can understate totals if several control and field device buckets and modernization spend are not fully counted. |

| Trade Journal B | USD 68.40 B (2026) | This estimate is presented for a later year, and the scope looks broader across automation hardware and software, which can lift the number if adjacent categories are included without clear cutoffs. |

The table shows that the main spread is driven by year selection and what is counted inside the market, and in Mordor Intelligence's model the North America total is built around factory automation and industrial controls across the covered countries with defined device groupings and end-user linkage checks. With those choices made explicit, the result stays traceable to observable production, utilization, and investment signals, and it can be repeated and stress-tested when assumptions change.

Key Questions Answered in the Report

What is the current value of the North America factory automation and industrial controls market?

It is valued at USD 60.55 billion in 2026.

How fast is the sector expected to grow?

The market is forecast to expand at a 9.95% CAGR to 2031.

Which segment holds the largest share by component?

Hardware leads with 60.05% revenue share in 2025.

Why are collaborative robots gaining attention among SMEs?

Cobots cost between USD 110,000 and USD 200,000 and offer quick paybacks by easing labor shortages.

Which country shows the fastest growth in North America?

Mexico grows at an 11.05% CAGR due to near-shoring into automotive and electronics.

What is a key cybersecurity challenge for factories?

Legacy control systems lack modern protections, exposing plants to remote-code-execution threats.

Page last updated on: