Work Order Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.41 Billion |

| Growth Rate (2026 - 2031) | 7.52% CAGR |

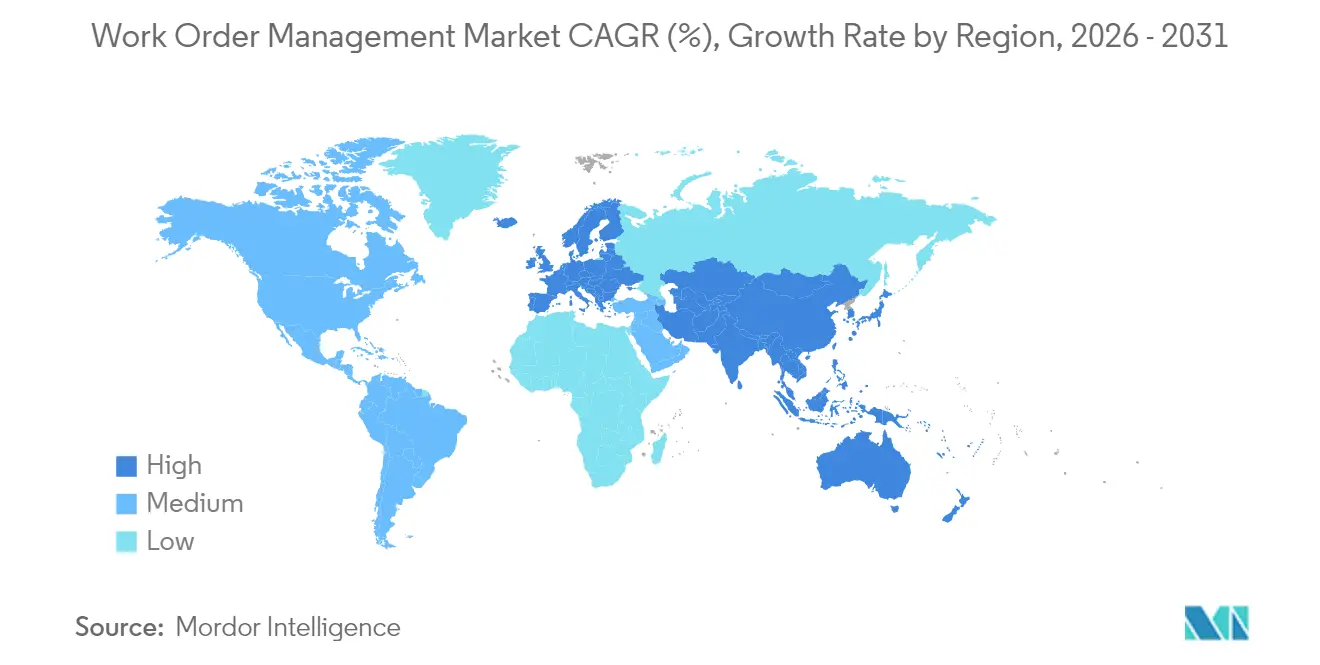

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

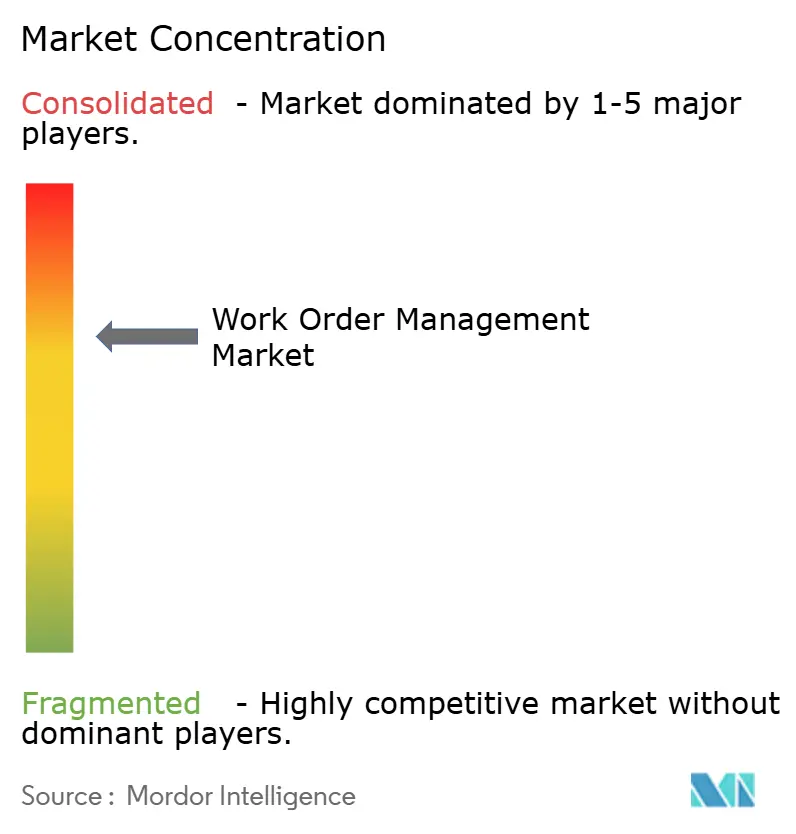

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Work Order Management Market Analysis by Mordor Intelligence

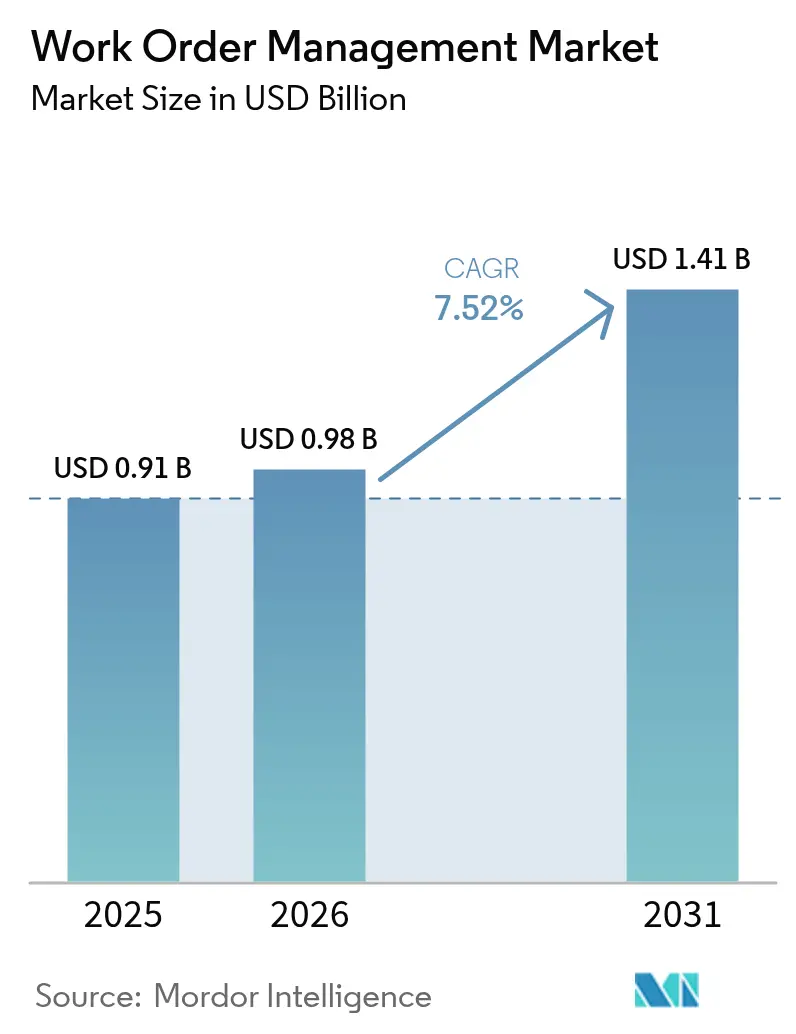

The work order management market size in 2026 is estimated at USD 0.98 billion, growing from 2025 value of USD 0.91 billion with 2031 projections showing USD 1.41 billion, growing at 7.52% CAGR over 2026-2031. Cloud deployment continues to replace on-premises systems as organizations prioritize real-time mobile access, subscription pricing, and rapid scalability. Predictive maintenance programs that tie sensor data to financial outcomes are widening the addressable base beyond traditional manufacturing into highly regulated sectors such as healthcare. A shortage of skilled technicians in mature economies is compelling vendors to embed artificial intelligence that automates scheduling, while low-Earth-orbit satellite services extend coverage to remote assets. Competitive intensity is rising as resource-planning incumbents embed work order modules and mobile-first challengers court small and medium enterprises with freemium tiers.

Key Report Takeaways

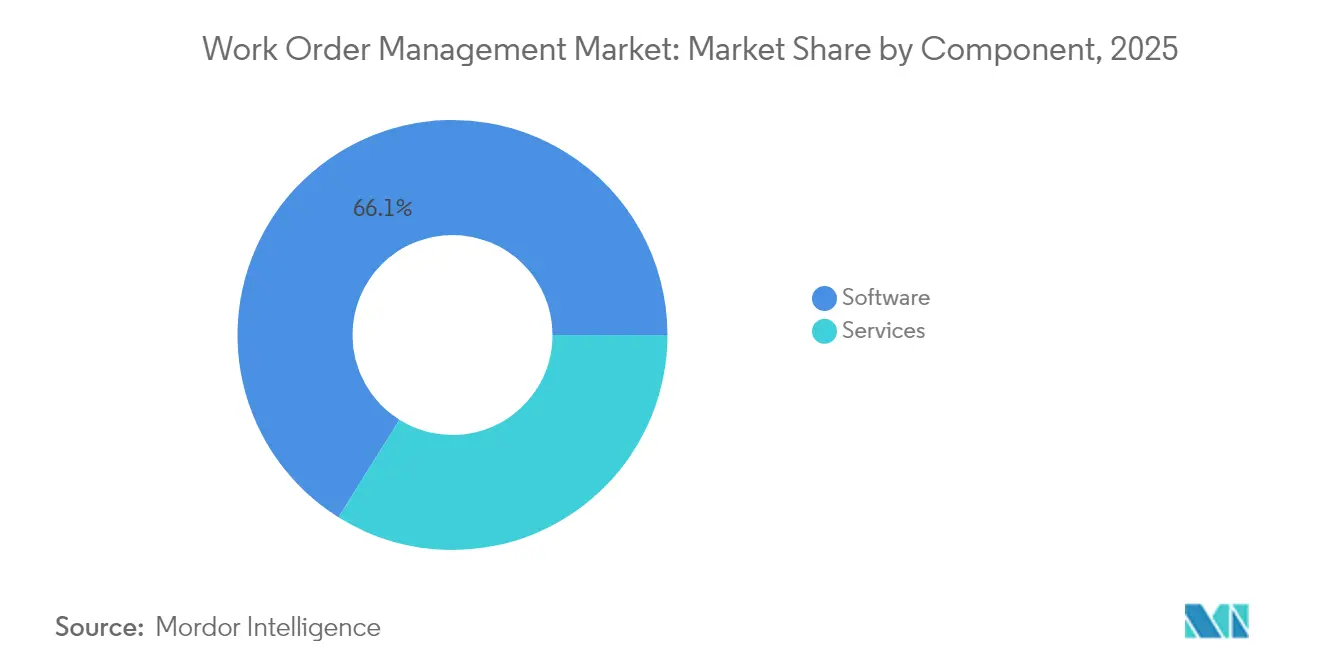

- By component, software led with a 66.10% of the work order management market size in 2025, while services are projected to advance at a 7.88% CAGR through 2031.

- By deployment type, cloud captured 63.05% of the work order management market size in 2025 and is projected to expand at an 8.05% CAGR through 2031.

- By organization size, large enterprises accounted for 65.20% of the work order management market size in 2025, whereas SMEs are expected to grow at an 7.95% CAGR through 2031.

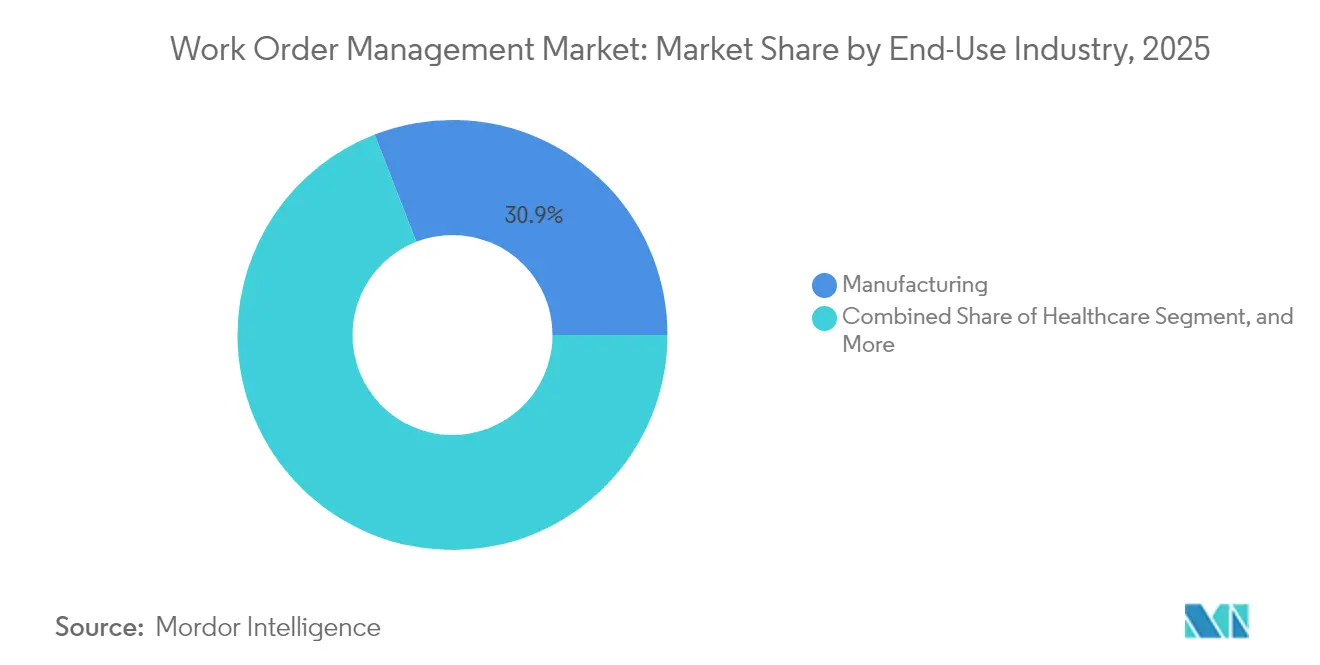

- By end-use industry, manufacturing held a 30.90% of the work order management market size in 2025, and the healthcare sector is forecast to surge at a 9.12% CAGR through 2031.

- By application module, work order management dominated with 34.70% share in 2025, while reporting and analytics is climbing at a 9.01% CAGR through 2031.

- By geography, North America commanded a 38.20% of the work order management market size in 2025, and the Asia Pacific is projected to expand at an 8.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Work Order Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of cloud-based field service platforms | +1.8% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Growing demand for predictive maintenance capabilities | +1.5% | Global, led by manufacturing hubs in Asia Pacific and North America | Medium term (2-4 years) |

| Increasing mobile workforce and BYOD policies | +1.2% | Global, with early adoption in North America and Western Europe | Short term (≤ 2 years) |

| Integration with IoT and asset sensors | +1.4% | Asia Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Shift toward outcome-based service contracts in industrial verticals | +0.9% | North America and Europe, emerging in Asia Pacific | Long term (≥ 4 years) |

| ESG-mandated reporting of maintenance-related carbon footprint | +0.7% | Europe and North America, regulatory influence spreading to Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud-Based Field Service Platforms

Enterprises are migrating to multitenant software that eliminates the need for servers, backups, and annual maintenance fees.[1]Microsoft Corporation, “New AI Capabilities in Dynamics 365 Field Service,” Microsoft.com Subscription contracts scale technician seats on demand, enabling firms to flex capacity for seasonal workloads. Mobile synchronization became mandatory during the COVID-19 pandemic, cementing expectations for real-time visibility across geographically dispersed teams. Regulated utilities and defense agencies adopt hybrid deployment, keeping asset data on-premises while running scheduling logic in the cloud to strike a balance between security and mobility. Leading vendors report that more than three-quarters of new field service contracts specify cloud-only architecture.

Growing Demand for Predictive Maintenance Capabilities

Machine-learning models correlate sensor telemetry with historical work orders to forecast failures and schedule interventions before breakdowns.[2]Siemens AG, “Predictive Maintenance with Industrial Edge Solutions,” Siemens.com Avoiding a single unplanned shutdown can offset the annual cost of an enterprise platform. Vendors acquire IoT specialists to deliver end-to-end asset performance, as illustrated by PTC’s integration of ServiceMax with ThingWorx. Regulatory agencies encourage utilities to deploy predictive maintenance to mitigate wildfire risk, thereby accelerating its adoption in the energy sector. The approach favors organizations with mature reliability teams, widening the gap between digital leaders and laggards.

Increasing Mobile Workforce and BYOD Policies

A growing number of employers are allowing technicians to install field service apps on their personal smartphones, thereby reducing hardware budgets and compressing deployment cycles.[3]International Foundation of Employee Benefit Plans, “BYOD Policy Survey Results,” ifebp.org Zero-trust security frameworks with biometric authentication safeguard sensitive schematics on consumer devices. BYOD accelerates the work order management market by reducing training friction and enabling gig-style staffing for surge events. Compliance with GDPR and HIPAA forces vendors to embed role-based access controls and immutable audit trails. The adoption of encrypted mobile device management is rising as it becomes a standard across both small and large enterprises.

Integration With IoT and Asset Sensors

Industrial assets now ship with embedded connectivity that automatically generates work orders when temperature, vibration, or pressure exceed specified thresholds. The model shortens detection-to-response time for offshore platforms and remote substations where manual inspection is costly. Data standardization challenges persist because sensors emit proprietary formats; however, IEC 62443 guidelines are creating a security baseline that buyers demand. Equipment makers integrate telematics and maintenance software at the factory, providing a services revenue stream throughout the asset's life cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and privacy concerns in cloud deployments | -0.6% | Global, with heightened sensitivity in Europe and North America | Short term (≤ 2 years) |

| High integration complexity with legacy ERP systems | -0.8% | North America and Europe, where legacy systems are prevalent | Medium term (2-4 years) |

| Talent shortage in AI-enabled dispatch algorithm development | -0.5% | Global, most acute in North America and Western Europe | Medium term (2-4 years) |

| Rising satellite internet latency costs in remote asset locations | -0.4% | Global, concentrated in offshore energy, mining, and rural utilities across Middle East, Africa, and remote Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Security and Privacy Concerns in Cloud Deployments

Ransomware incidents targeting field service providers rose sharply in 2024, highlighting vulnerabilities in third-party hosting environments. Healthcare organizations face fines exceeding USD 1 million per breach under HIPAA, prompting cautious migration paths. Vendors respond with SOC 2 Type II audits and end-to-end AES-256 encryption, yet buyer skepticism persists. New European NIS2 rules require essential service operators to report cyber events within 24 hours, adding compliance overhead. Consequently, some firms defer cloud adoption until internal security teams mature.

High Integration Complexity With Legacy ERP Systems

Decades-old resource-planning software relies on bespoke data models that clash with modern APIs, stretching implementation timelines beyond 18 months. Custom middleware and data reconciliation can consume up to 30% of the total project effort, thereby increasing budget risk. Organizations running multiple ERP instances across regions face compounded complexity, often requiring system integrators to build point-to-point connectors. Progress accelerates when vendors ship pre-built adaptors, but cross-vendor environments still demand extensive testing. Integration hurdles slow the pace at which large enterprises can unlock predictive analytics embedded in cloud platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Integration Demands Rise

Services contributed 33.90% of 2025 revenue, yet they are expanding at a 7.88% CAGR, faster than software. Implementation partners migrate legacy data, configure approval workflows, and link field applications to enterprise resource planning systems, activities that can span a full fiscal year for global manufacturers. Managed services appeal to firms that lack in-house IT staff, shifting the responsibility for upgrades and cybersecurity to vendors. Training budgets represent at least 15% of total project spend, which helps lift technician adoption and shorten payback periods. Consequently, services are a strategic lever for vendors to deepen account relationships.

Software remains the backbone of the work order management market, automating dispatch, mobile execution, and asset tracking through a unified interface. The segment benefits from steady subscription renewals and feature expansion, including artificial intelligence dispatch assistants. Vendors bundle adjacent modules, including inventory and customer management, to boost average contract value. Although software growth trails services, it remains the primary entry point for new customers and underpins the broader ecosystem.

By Deployment Type: Cloud Dominance Reshapes Vendor Strategies

Cloud platforms captured a 63.05% share in 2025 and are projected to grow at an 8.05% CAGR through 2031. Operating expenditure pricing eliminates capital budgets for servers, and automatic updates keep installations secure without manual patches. Vendors embed advanced analytics and natural-language interfaces that would be cost-prohibitive on premises. Hybrid models satisfy regulated sectors by keeping asset telemetry onsite while running scheduling algorithms in the cloud.

On-premises installations persist in defense and critical infrastructure, where data sovereignty and air-gapped networks remain non-negotiable. Nevertheless, their relative share will continue to decline as CIOs plan cloud-first roadmaps. The shift drives vendors to prioritize multitenant architectures and to sunset perpetual licenses, moving revenue recognition toward recurring subscription streams.

By Organization Size: SMEs Embrace Affordable Cloud Tiers

Large enterprises accounted for 65.20% of 2025 spending, leveraging existing contracts with SAP, Oracle, and Microsoft to extend resource-planning suites. Complex multi-site operations demand advanced scheduling algorithms and integration with industrial IoT platforms. These organizations negotiate global service-level agreements and often require localization across dozens of languages.

SMEs, however, represent the fastest-growing customer group, with adoption rising at an 7.95% CAGR. Subscription plans starting below USD 50 per user per month remove upfront barriers, while mobile-first apps lower training costs for small crews. Templates for plumbing, HVAC, and electrical trades accelerate go-live within weeks instead of quarters. High churn remains a challenge, pressing vendors to offer freemium tiers and in-product coaching to retain users.

By End-Use Industry: Healthcare Surges on Compliance Mandates

Manufacturing led 2025 revenue with a 30.90% share as predictive maintenance programs shield continuous-flow production from costly downtime. Energy and utilities follow, driven by dispersed assets such as substations and pipelines that require remote scheduling. Healthcare, though smaller today, is expanding at a 9.12% CAGR as hospitals digitize maintenance logs to comply with FDA 21 CFR Part 11 recordkeeping rules.

Adopters in healthcare have reduced medical equipment downtime by one-third, improving patient throughput and asset utilization. Telecommunications, retail, and government agencies also accelerate deployment to manage distributed networks, stores, and civic infrastructure. Each vertical pursues tailored functionality: utilities demand geospatial tracking, while retailers focus on store-appearance work orders.

By Application Module: Analytics Ascends as Buyers Seek Insight

Work order management remained the foundational module with a 34.70% share in 2025, automating task creation, assignment, and closure. Asset and inventory management modules support accurate tracking of spare parts and effective warranty management. Preventive maintenance schedules recurring inspections, while dispatch engines optimize routing to cut travel time.

Reporting and analytics is the fastest-growing module, rising at a 9.01% CAGR as supervisors demand dashboards that surface technician utilization, mean time to repair, and cost per work order. Embedded business intelligence marks the maturation of the work order management market, once core workflows are digitized, data becomes a strategic asset for continuous improvement. Real-time insights enable managers to redeploy resources and quantify the return on investment in predictive maintenance initiatives.

Geography Analysis

North America accounted for 38.20% of 2025 revenue, driven by the early adoption of cloud platforms, an extensive integrator ecosystem, and compliance requirements from OSHA that mandate the use of documented maintenance procedures. The United States drives the region, leveraging large installed resource-planning bases to cross-sell field service modules. Canada follows suit, especially in the energy sector, where operators coordinate maintenance across wide geographic areas. Mexico is emerging as a hub for nearshore manufacturing, requiring modern maintenance infrastructure.

The Asia Pacific is forecast to grow at an 8.65% CAGR through 2031, benefiting from government mandates that encourage industrial IoT deployment in China and smart city initiatives in India. Japan’s aging workforce is accelerating the automation of field service dispatch, while investments in sensors across utilities and transportation are amplifying demand. Vendors localize solutions for language and regulatory compliance, positioning Asia Pacific as the primary growth engine.

Europe’s stringent GDPR and data-sovereignty rules slow cloud migration but raise interest in hybrid deployments. Germany’s automotive and machinery sectors generate strong demand for predictive maintenance, and the United Kingdom’s utilities invest to meet Ofgem reliability targets. France and Russia adopt at a modest pace due to on-premises preferences. The Middle East is seeing momentum from mega-projects in Saudi Arabia and the United Arab Emirates, while South Africa leads African adoption in the mining sector. South America is a mixed region: Brazil invests in manufacturing and energy, whereas currency volatility restrains spending in Argentina and its neighboring markets.

Competitive Landscape

The top five vendors controlled most of the 2024 revenue, indicating moderate market fragmentation. SAP, Oracle, and Microsoft leverage installed resource-planning footprints to embed field service modules, creating switching costs that favor incremental expansion. ServiceNow, IFS, and PTC differentiate themselves with deep functionality, including AI-driven dispatch and augmented-reality support. Mobile-first challengers, including UpKeep, MaintainX, and Limble, target SMEs with freemium pricing and intuitive interfaces, thereby accelerating user growth by reducing adoption friction.

Technology competition centers on predictive analytics, low-connectivity mobile performance, and end-to-end IoT integration. ServiceNow incorporated Element AI to automate incident prioritization, while PTC’s ThingWorx enables manufacturers to embed sensors at the factory. Telecommunications carriers such as Verizon bundle telematics data with maintenance workflows, blurring industry boundaries.

Outcome-based pricing is an emerging model where vendors charge for uptime rather than the number of seats, aligning incentives but requiring robust analytics to verify performance. Generative AI is entering the mainstream, with Microsoft’s Copilot allowing technicians to dictate work orders in natural language. The competitive field remains open for specialists focused on renewable energy assets or compliance-intensive sectors, such as the pharmaceutical industry.

Work Order Management Industry Leaders

ServiceNow Inc.

PTC Inc.

IFS AB

Oracle Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Microsoft integrated Dynamics 365 Field Service with Azure Digital Twins, allowing technicians to visualize real-time sensor data on a 3D model of the asset directly within the mobile app.

- July 2025: Oracle completed the acquisition of Praxedo to expand its cloud work order platform for small and medium enterprises, adding lightweight dispatch and geofencing tools to the Fusion Cloud suite.

- May 2025: SAP released S/4HANA Field Service Edge, an offline-first mobile application that syncs work orders and asset telemetry once connectivity is restored, targeting remote mining and renewable energy sites.

- March 2025: ServiceNow introduced a generative AI module for Field Service Management that automatically drafts corrective action plans based on historical repair data, reducing technician diagnostic time by 25%.

Global Work Order Management Market Report Scope

The Work Order Management Market Report is Segmented by Component (Software, and Services), Deployment Type (Cloud-Based, On-Premises, Hybrid), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-Use Industry (Manufacturing, Energy and Utilities, Healthcare, IT and Telecom, Transportation and Logistics, Government, Retail, Other End-Use Industry), Application Module (Work Order Management, Asset Management, Inventory Management, Preventive Maintenance, Scheduling and Dispatch, Reporting and Analytics, Customer Management), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Manufacturing |

| Energy and Utilities |

| Healthcare |

| IT and Telecom |

| Transportation and Logistics |

| Government |

| Retail |

| Other End-Use Industry |

| Work Order Management |

| Asset Management |

| Inventory Management |

| Preventive Maintenance |

| Scheduling and Dispatch |

| Reporting and Analytics |

| Customer Management |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Software | ||

| Services | |||

| By Deployment Type | Cloud-Based | ||

| On-Premises | |||

| Hybrid | |||

| By Organization Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End-Use Industry | Manufacturing | ||

| Energy and Utilities | |||

| Healthcare | |||

| IT and Telecom | |||

| Transportation and Logistics | |||

| Government | |||

| Retail | |||

| Other End-Use Industry | |||

| By Application Module | Work Order Management | ||

| Asset Management | |||

| Inventory Management | |||

| Preventive Maintenance | |||

| Scheduling and Dispatch | |||

| Reporting and Analytics | |||

| Customer Management | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How fast is the work order management market projected to grow through 2031?

It is expected to expand at a 7.52% CAGR, rising from USD 0.98 billion in 2026 to USD 1.41 billion in 2031.

Which deployment model is gaining the most traction among new buyers?

Cloud deployment leads with 63.05% share in 2025 and continues to grow fastest as firms avoid on-premises infrastructure.

Why is healthcare adoption accelerating?

Hospitals need electronic maintenance logs to meet FDA Part 11 compliance, propelling a 9.12% CAGR for the sector.

What is driving demand for analytics modules?

Supervisors increasingly seek real-time dashboards that highlight technician utilization and mean time to repair, making analytics the fastest-growing module at 9.01% CAGR.

Which region offers the strongest growth outlook?

Asia Pacific shows the highest regional CAGR at 8.65%, supported by manufacturing expansion and government smart-infrastructure programs.

Page last updated on: