Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

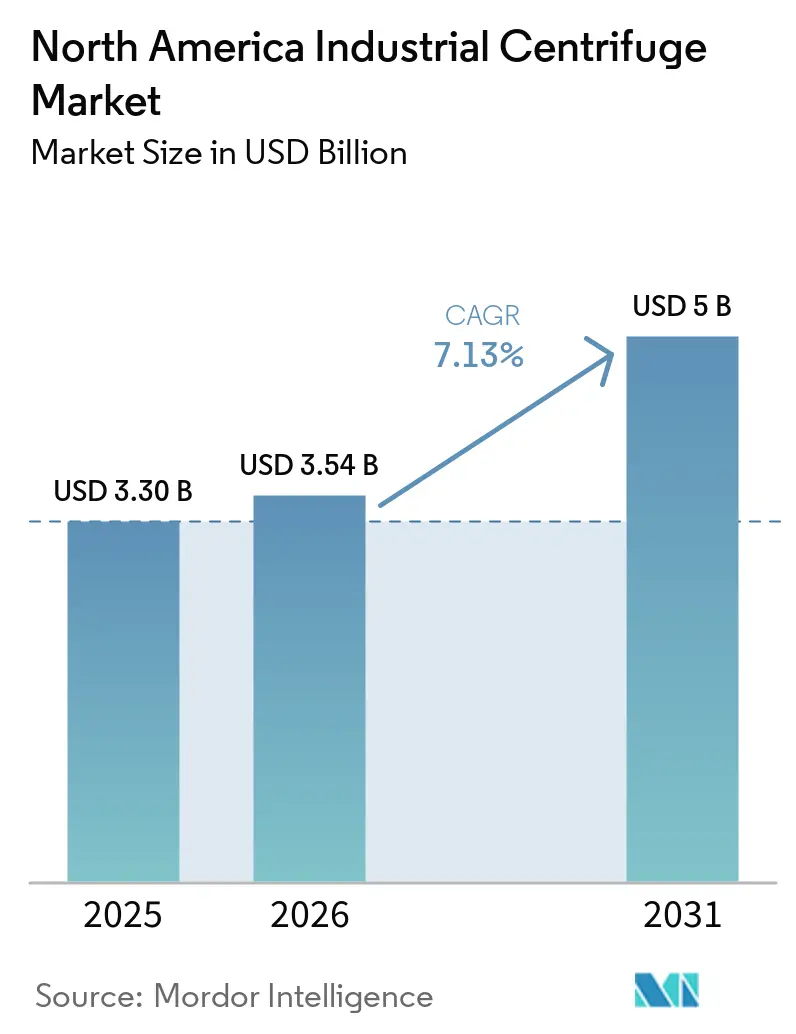

| Base Year Market Size (2025) | USD 3.30 Billion |

| Market Size (2026) | USD 3.54 Billion |

| Market Size (2031) | USD 5 Billion |

| Growth Rate (2026 - 2031) | 7.13% CAGR |

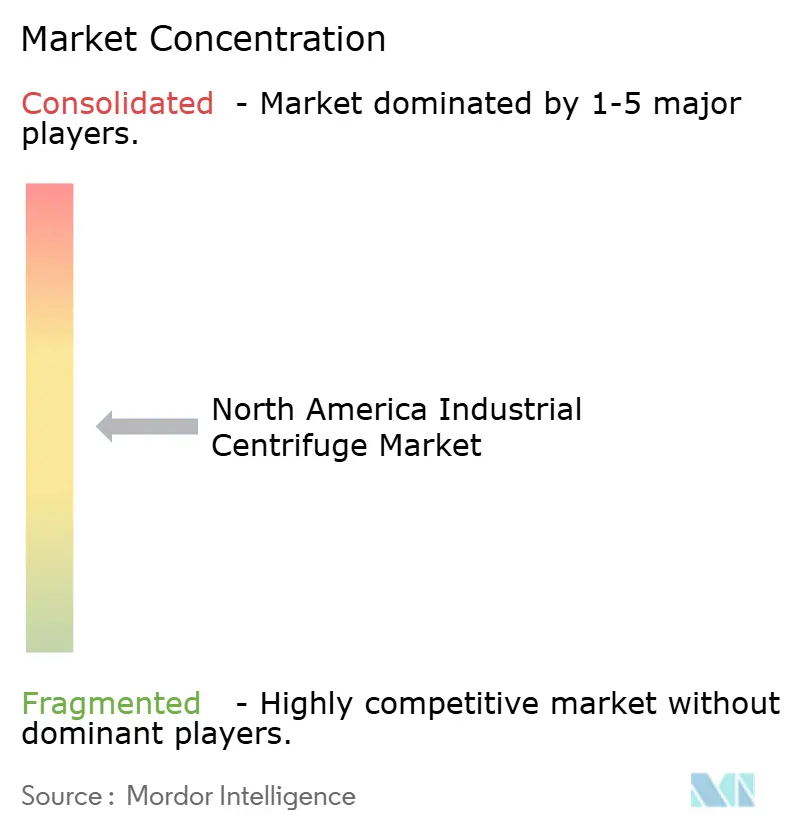

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Industrial Centrifuge Market Analysis by Mordor Intelligence

The North America Industrial Centrifuge Market size was valued at USD 3.30 billion in 2025 and is estimated to grow from USD 3.54 billion in 2026 to reach USD 5 billion by 2031, at a CAGR of 7.13% during the forecast period (2026-2031). Growth is being supported by tighter biosolids regulation, expanding biopharmaceutical manufacturing, wider use of continuous clarification in food and beverage processing, and clean-energy programs tied to hydrogen and battery recycling that require specialized separation equipment. What makes this cycle different is that regulatory demand, pharmaceutical investment, and energy-transition spending are moving through the same procurement period, which is helping major suppliers sustain elevated order backlogs. Buyers are also giving more weight to service coverage, digital controls, and energy use because these factors shape uptime and operating cost over the full equipment life. At the same time, high capital costs, maintenance skill gaps, and membrane-based alternatives are slowing purchasing decisions for part of the customer base. This leaves the North America industrial centrifuge market on a solid growth path, but project financing schedules and labor availability will continue to shape the timing of order conversion.

Key Report Takeaways

- By type, sedimentation centrifuges led the North America industrial centrifuge market with 62.2% share in 2025, while filtering centrifuges are forecast to expand at 8.1% CAGR through 2031.

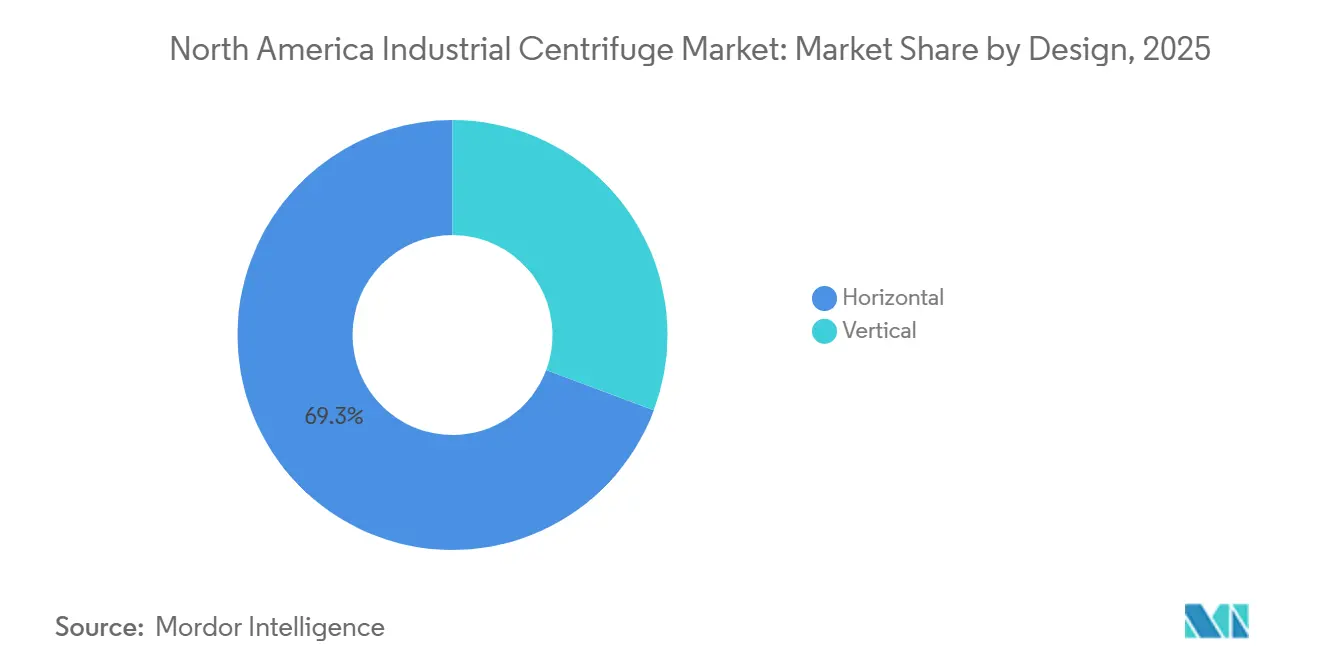

- By design, horizontal centrifuges held 69.3% share in 2025, while vertical centrifuges are projected to grow at 7.5% CAGR over 2026-2031.

- By operation mode, continuous operation units accounted for 73.1% share in 2025, while batch-mode centrifuges are expected to advance at 7.9% CAGR through 2031.

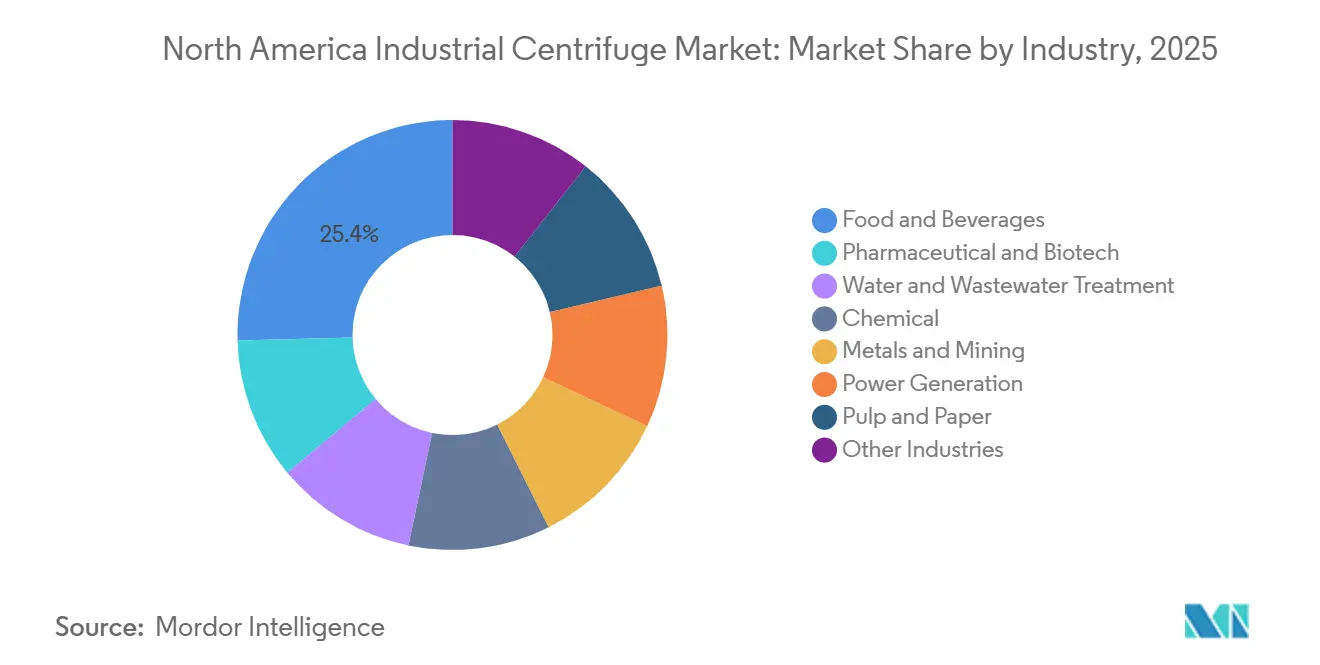

- By industry, food and beverages captured 25.4% share in 2025, while water and wastewater treatment is forecast to grow at 8.3% CAGR through 2031.

- By geography, the United States held 67.5% of the North America industrial centrifuge market share in 2025, while Canada is projected to expand at 8.8% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Industrial Centrifuge Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Push for Wastewater Sludge Reduction | +1.50% | National, with concentrated near-term demand in Great Lakes states, California, and New England | Short term (≤ 2 years) |

| Biopharma Capacity Expansion in the U.S. and Canada | +1.80% | National, with core U.S. demand in Maryland, Georgia, Illinois, Massachusetts, and North Carolina, and spillover into Canada | Medium term (2-4 years) |

| Food and Beverage Processors Shifting to Continuous Clarification | +1.00% | National, with highest density in Midwest and Pacific Northwest processing corridors | Medium term (2-4 years) |

| Energy Efficiency Mandates Under DOE 50001 Driving Retrofits | +0.90% | National, with early gains in Midwest and Southeast industrial clusters | Medium term (2-4 years) |

| IRA Funded Clean Hydrogen Hubs Needing Brine Centrifuges | +0.60% | Gulf Coast, Appalachian, California, and Midwest hub corridors | Long term (≥ 4 years) |

| Battery Recycling Black Mass Separation Demand | +0.50% | Southeast, Midwest, and Southwest near EV battery manufacturing clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Biopharma Capacity Expansion in the U.S. & Canada Is Reshaping Centrifuge Procurement Patterns

North America’s biopharmaceutical sector is going through a large domestic manufacturing build-out, and that is sustaining demand for high-speed disc-stack separators and continuous decanters used in cell harvest, clarification, and protein separation. UCB selected Gwinnett County, Georgia, for a new 460,000-square-foot biologics campus in March 2026, adding another procurement center for pharmaceutical-grade centrifuges in the U.S. Southeast. (1)UCB, “UCB Selects Georgia for New U.S. Biologics Manufacturing Facility,” ucb-usa.com New biologics sites of this kind are being planned for long operating lives and large commercial volumes, which raises the need for reliable separation equipment that can perform at scale. A major shift is that many of these facilities are being designed around continuous biomanufacturing from the outset, and that design choice favors high-speed separators over batch filtration alternatives. Once those layouts are approved, centrifuge demand tends to stay tied to the production line for the life of the plant. This makes biopharma one of the clearest long-cycle demand anchors for the North America industrial centrifuge market.

Regulatory Push for Wastewater-Sludge Reduction Creates Durable Infrastructure Demand

Tighter oversight of biosolids handling is supporting demand for decanter centrifuges across municipal and industrial wastewater systems. The U.S. Environmental Protection Agency finalized Method 1633 in January 2024 for monitoring 40 PFAS analytes in sewage sludge and later moved to incorporate it into 40 CFR Part 136 through a Methods Update Rule signed in December 2024. This process is pushing plant operators to show stronger dewatering performance because cake dryness affects PFAS concentration in sludge that is sent for land application. The compliance burden also sits alongside 40 CFR Part 503, the NPDES program, and related state biosolids rules, which shape permitting and performance verification for centrifuge-based dewatering trains. Better dry solids content also reduces transport and disposal costs, which strengthens the investment case for equipment upgrades even before stricter federal rules are fully implemented. This keeps wastewater infrastructure as a steady demand source for the North America industrial centrifuge market.

Food & Beverage Processors Shifting to Continuous Clarification Drives High-Speed Separator Upgrades

Food and beverage processors across the region are moving toward continuous clarification to improve cost control, product consistency, and compatibility with new fermentation-based production systems. Alfa Laval launched the PureFerm 750 N in April 2026 for high-density cell fermentations used in alternative protein and precision-fermented dairy production. Industrial trials showed a 10-fold reduction in solids carry-over and 30% to 40% more capacity than initially projected, which signals a clear performance gain over smaller pilot systems. (2) Alfa Laval, “New PureFerm Centrifuge Set to Blaze a Trail for Next Generation Food Producers,” alfalaval.us GEA introduced the GSI 260 beverage separator skid in 2025 with a Centrifuge Water Saving Unit that can cut freshwater consumption by up to 99.9%, a feature with strong appeal in water-stressed processing locations. As precision fermentation scales, tighter g-force control and gentler shear management are lifting the baseline specification for new equipment. That is raising the quality threshold for purchases across this end use and supporting higher-value demand within the North America industrial centrifuge market.

Energy-Efficiency Mandates Under DOE 50001 Framework Are Accelerating Centrifuge Retrofits

The DOE 50001 Ready framework is pulling centrifuge retrofits forward as industrial sites place more weight on verified energy savings. Participating facilities in the program have delivered 4% annual energy savings year over year across more than a decade, which has sharpened attention on older separation equipment that cannot keep pace. As manufacturers formalize energy-management systems, centrifuge replacement decisions are being judged more on lifetime operating cost and less on purchase price alone. ANDRITZ states that its DU-series decanter centrifuges can reduce energy use by up to 50% relative to conventional units, while the ecoOne pusher centrifuge can lower power consumption by up to 20% through a single integrated motor design. That makes the payback case stronger for retrofits in plants that run continuously. The same logic is helping support replacement demand in the North America industrial centrifuge market as electricity costs remain a central planning variable.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and Long Payback Periods | -1.80% | National, with strongest pressure in municipal water utilities and mid-size industrial operators | Short term (≤ 2 years) |

| Competition from Membrane Based Separation | -1.20% | National, concentrated in pharmaceutical and food and beverage applications where membrane systems have regulatory acceptance | Medium term (2-4 years) |

| Skilled Centrifuge Maintenance Talent Shortage | -0.80% | National, with the greatest pressure in rural industrial corridors and mid-market operators | Long term (≥ 4 years) |

| Bearings Supply Chain Delays Lengthening Lead Times | -0.50% | National, with added pressure in multi-centrifuge installations where spare parts availability is tight | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Long Pay-Back Periods Constrain Adoption Velocity Across Mid-Market Operators

High installed cost remains the clearest barrier to faster adoption across mid-market operators. Premium pharmaceutical disc-stack separators and large municipal sludge decanters often require payback periods that stretch beyond 5 years, which is difficult for operators with constrained capital budgets. The issue is strongest in municipal wastewater, where rate-case approvals and bond financing can delay procurement by 18 to 36 months even when the operating and compliance need is clear. Interest rate pressure from the earlier part of the decade also raised the cost of capital used in project appraisal, which made replacement programs harder to approve. Because of this, some operators continue to extend the life of older equipment instead of renewing fleets on a faster schedule. This remains a practical brake on growth for the North America industrial centrifuge market.

Competition from Membrane-Based Separation Erodes Centrifuge Addressable Market in Select Applications

Membrane systems are taking a share in selected clarification and cell-harvest applications within pharmaceutical, and food and beverage processing. Cross-flow microfiltration and ultrafiltration now match centrifuge performance in some low-solids settings, which narrows the addressable space for new equipment. The shift is most visible in biologics workflows where single-use tangential-flow filtration reduces cleaning validation demands. Even so, very-high-cell-density fermentation still creates sludge loads that exceed the practical limits of current membrane systems, which protects centrifuge demand in more demanding duty cycles. The outcome is a split market rather than full substitution. Membranes are gaining ground in cleaner downstream steps, while centrifuges keep their role in high-solids and high-throughput processing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Filtering Centrifuges Gain Share in High-Value Separation Applications

Sedimentation centrifuges accounted for 62.2% of the North America industrial centrifuge market share in 2025, supported by the entrenched use of decanter and disc-stack systems in wastewater treatment, dairy processing, and biopharma clarification. Decanters retain the widest footprint within this group because they handle high-solids municipal sludge duty cycles with steady mechanical reliability. Disc-stack units remain the premium choice in pharmaceutical and beverage clarification, where tighter particle separation and in-place cleaning are required. Hydrocyclone and clarifier or thickener systems continue to serve primary dewatering stages in mining and pulp and paper operations, where throughput often matters more than final dryness. Energy audits tied to continuous improvement programs are also bringing older sedimentation systems into replacement discussions at industrial sites.

Filtering centrifuges are projected to grow at 8.1% CAGR through 2031, making them the fastest-expanding type in the North America industrial centrifuge market. Growth is being driven by battery-active-material separation and fine-chemical crystallization, where buyers need cleaner dry solids and tighter process control. Research published in RSC Advances in January 2026 by Oak Ridge National Laboratory and the University of Tennessee showed that heavy liquid centrifugal separation achieved more than 95% efficiency in lithium-ion battery black mass recovery. That result gives technical support to the filtering route in high-purity resource recovery applications. Pusher and peeler centrifuges are therefore receiving more procurement attention in specialty chemicals and API manufacturing, where cake purity and low residual moisture are core process requirements.

Design: Vertical Configurations Gain Traction in Controlled Environments

Horizontal centrifuges held 69.3% of the North America industrial centrifuge market size in 2025, reflecting their strength in continuous high-throughput duties such as sewage sludge dewatering, edible oil processing, and mining tailings management. Their lead is reinforced by a mature service and aftermarket network, which improves parts access and technician familiarity across operator groups. This installed-base advantage keeps ownership costs more predictable for plants that run continuously. It also helps explain why horizontal systems remain the default choice in large-volume and solids-heavy duties across the region. Alfa Laval reported more than 4,200 patents in its separation portfolio in its 2025 annual report, which shows the depth of product development around the designs most used in food and water processing applications.

Vertical centrifuges are forecast to expand at 7.5% CAGR over 2026-2031, outpacing horizontal units in the North America industrial centrifuge market. Demand is centered in pharmaceutical and biotech facilities, where vertical bowl geometries fit cleanroom layouts more easily and support CIP validation in GMP-regulated settings. Their form factor also suits controlled production environments where floor planning and contamination management carry more weight. Another emerging use case is direct lithium extraction, where precise liquid-liquid separation at ambient temperature can support saleable lithium carbonate equivalent without conventional thermal processing. This keeps vertical designs tied to both advanced bioprocessing and selected clean-energy mineral flows.

By Operation Mode: Batch Mode Gains in Pharmaceutical and Specialty Chemicals

Continuous operation centrifuges commanded 73.1% of the market in 2025, reflecting the large weight of food and beverage, wastewater, and commodity-chemical processing in the regional demand mix. These sectors value steady throughput and lower operator intervention more than batch flexibility. Intelligent control is becoming more important in this segment because utilities and processors want self-adjusting systems that can maintain performance with fewer skilled staff. That requirement is becoming stronger as labor availability remains tight across several industrial corridors. These factors keep continuous platforms at the center of the North America industrial centrifuge industry for large-volume duties.

Batch-mode centrifuges are projected to grow at 7.9% CAGR through 2031, the fastest pace among operation modes in the North America industrial centrifuge market. Their appeal is strongest in pharmaceutical API and specialty fine-chemical plants, where variable g-force profiles, programmable wash steps, and precise solids retention matter more than line speed. This flexibility is valuable for multi-product facilities that must move between recipes without compromising quality. ANDRITZ states that its ecoOne pusher centrifuge can be converted on site between two-stage and three-stage operation, which addresses demand for batch versatility without full capital re-specification. That design approach supports batch adoption as smaller commercial facilities scale beyond pilot production in the North America industrial centrifuge industry.

By Industry: Water and Wastewater Treatment Emerges as the Growth Catalyst

Food and beverages held 25.4% of the market in 2025, giving it the largest end-use position in the North America industrial centrifuge market. Demand spans clarification, oil-water separation, starch processing, and beverage stabilization, which gives the segment a broad and resilient equipment base. Many processors are replacing gravity-separation and filter-press systems with continuous disc-stack platforms to improve yield and consistency. At the same time, precision fermentation and plant-based protein extraction are creating new applications that need tighter process control. Trucent states that purpose-built centrifuge systems can raise food and beverage production by 30% to 50% through higher batch throughput and recovery of materials otherwise lost to sediment streams.

Water and wastewater treatment is forecast to grow at 8.3% CAGR over 2026-2031, making it the fastest-expanding end-use segment in the North America industrial centrifuge market. EPA Method 1633 raised the practical importance of dewatering performance because higher dry solids content reduces PFAS mass transferred into land-application streams. The compliance setting also includes 40 CFR Part 503, the NPDES program, and related state biosolids rules, which keep capital planning focused on measurable sludge-handling performance. Centrisys/CNP expanded its Kenosha campus to around 300,000 square feet in July 2025 and added full-scale pilot testing for larger wastewater dewatering systems, which points to expected demand in this vertical. This makes wastewater one of the most visible growth engines for the North America industrial centrifuge market over the forecast period.

Geography Analysis

The United States accounted for 67.5% of the North America industrial centrifuge market size in 2025, supported by its concentration of biopharma manufacturing, municipal water infrastructure, and energy-transition projects. Demand is strongest where those spending streams overlap, especially in states with major biologics investment and large wastewater renewal programs. ANDRITZ reported that North America represented 27% of group revenue in 2025 and described the United States as offering considerable mid-term opportunities through reshoring and onshoring activity. That view aligns with the growing number of U.S. procurement nodes linked to pharmaceutical manufacturing and federally supported industrial expansion. The United States, therefore, remains the central demand base for the North America industrial centrifuge market.

Canada is projected to grow at 8.8% CAGR through 2031, the fastest pace in the region and a clear outlier within the North America industrial centrifuge market. The country benefits from expanding agri-food processing, continued plasma-derived biopharmaceutical activity in the Toronto and Montréal corridors, and municipal wastewater spending tied to federal support. Alfa Laval’s 2025 annual report states that the company had 115 employees in Canada, with operations in Newmarket, Ontario, supporting centrifuge sales and service across local processing sectors. Canada’s lithium and battery-mineral activity in Ontario and Québec is also creating technical reviews for both vertical and horizontal centrifuge configurations. This broader industrial mix helps explain why Canada is expanding faster than the regional average.

Mexico remains the smallest country market in North America, but it continues to expand with new investment in food and beverage processing and chemical production linked to nearshoring. The Bajío agro-industrial corridor is a key outlet for this demand because it combines agricultural processing with manufacturing growth. Alfa Laval maintains service and sales infrastructure in Mexico through Alfa Laval S.A. de C.V. in Tlalnepantla, which helps local buyers access equipment and aftermarket support. Trucent also lists a Mexico office, which supports regional service coverage for processing customers. Over the forecast period, Mexico is expected to trail the United States and Canada in absolute value while still posting healthy percentage gains from a smaller installed base. That keeps Mexico as a smaller but positive contributor within the North America industrial centrifuge market.

Competitive Landscape

The premium tier of the North America industrial centrifuge market is moderately consolidated, with Alfa Laval, ANDRITZ, and GEA Group holding the strongest positions in high-specification equipment and aftermarket service. Their advantage comes from proprietary parts ecosystems, digital controls, and dense service networks, which make vendor switching harder once equipment is installed. This is especially relevant in regulated end uses where process validation, uptime, and service response matter as much as the original equipment price. ANDRITZ said it held a global separation position in the #1 to #3 range and that North America generated 27% of group revenue in 2025, showing the region’s importance to major suppliers. The company also completed 3 U.S.-focused acquisitions in 2025, LDX Solutions, Diamond Power, and Allen-Sherman-Hoff, to widen its service reach around core equipment sales. This installed base and service depth give the top tier strong leverage in replacement and retrofit decisions across the North America industrial centrifuge market.

Competition becomes more fragmented in the mid-market, where regional producers and price-led entrants compete more aggressively on lead time and upfront cost. Centrisys/CNP has used its U.S. manufacturing footprint and BABA compliance positioning to strengthen its fit for federally funded municipal wastewater tenders. That matters because utilities using grant-supported budgets face tighter domestic sourcing requirements than many industrial buyers. Alfa Laval’s April 2026 launch of the PureFerm 750 N also shows how suppliers are tailoring products to precision fermentation and alternative protein processing rather than relying only on legacy food applications. Product positioning is therefore becoming more application-specific, especially in faster-growing niches where performance claims can justify premium pricing. These moves widen the competitive field below the top tier even as the market remains brand-sensitive in regulated applications.

ITT completed its USD 4.775 billion acquisition of SPX FLOW in March 2026, bringing the Seital centrifuge line into its Flow Technologies segment and reshaping ownership in the separation equipment space. GEA’s 2025 launch of the GSI 260 beverage separator skid shows how product differentiation is also shifting toward water efficiency and sensor-linked operating benefits. The main open space in the North America industrial centrifuge market is still intelligent aftermarket services, including predictive maintenance, remote optimization, and energy-performance support. No supplier has yet established a decisive lead in that service layer, which leaves room for incumbent expansion as well as competition from adjacent automation providers.

North America Industrial Centrifuge Industry Leaders

Alfa Laval AB

GEA Group AG

Andritz AG

Flottweg SE

Centrisys Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Alfa Laval launched the PureFerm 750 N high-speed separator, specifically designed for high-density cell fermentation processes in alternative protein and precision fermentation production. Industrial trials demonstrated a 10-fold reduction in solids carry-over and 30 to 40% more processing capacity than initially projected, addressing a capacity gap in North American precision fermentation contract manufacturing.

- March 2026: ITT Inc. completed the USD 4.775 billion acquisition of SPX FLOW, integrating the Seital centrifuge separator line into ITT's newly named Flow Technologies segment. SPX FLOW reported over USD 1.3 billion in revenue in 2025 with 14% organic orders growth, materially reshaping the competitive landscape in the North American industrial separation equipment sector.

- July 2025: Centrisys/CNP opened a new 70,000-square-foot Building 4 at its Kenosha, Wisconsin campus, increasing total footprint to approximately 300,000 square feet. The expansion supports larger centrifuge manufacturing, a growing rental fleet, and an enhanced pilot test lab, with 20 new positions added immediately and plans to double production output within five years.

North America Industrial Centrifuge Market Report Scope

An industrial centrifuge is a device that employs centrifugal force to subject a specimen to a constant force, such as separating different components of a fluid. This is accomplished by rapidly spinning the fluid within a receptacle, separating fluids of varying densities or liquids from solids.

The North America Industrial Centrifuge Market is segmented into type, design, operation mode, industry, and geography. By type, the market is segmented into Sedimentation and Filtering. By design, the market is segmented into Horizontal and Vertical. By operation mode, the market is segmented into Batch and Continuous. By industry, the market is segmented into Food and Beverages, Pharmaceutical and Biotech, Water and Wastewater Treatment, Chemical, Metals and Mining, Power Generation, and Pulp and Paper. The report also covers the market size and forecasts for industrial centrifuges in 3 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Type

| Sedimentation | Clarifier/Thickener |

| Decanter | |

| Disc-stack | |

| Hydrocyclone | |

| Other Sedimentation | |

| Filtering | Basket |

| Scroll-screen | |

| Peeler | |

| Pusher | |

| Other Filtering |

By Design

| Horizontal |

| Vertical |

By Operation Mode

| Batch |

| Continuous |

By Industry

| Food and Beverages |

| Pharmaceutical and Biotech |

| Water and Wastewater Treatment |

| Chemical |

| Metals and Mining |

| Power Generation |

| Pulp and Paper |

| Other Industries |

By Country

| United States |

| Canada |

| Mexico |

| By Type | Sedimentation | Clarifier/Thickener |

| Decanter | ||

| Disc-stack | ||

| Hydrocyclone | ||

| Other Sedimentation | ||

| Filtering | Basket | |

| Scroll-screen | ||

| Peeler | ||

| Pusher | ||

| Other Filtering | ||

| By Design | Horizontal | |

| Vertical | ||

| By Operation Mode | Batch | |

| Continuous | ||

| By Industry | Food and Beverages | |

| Pharmaceutical and Biotech | ||

| Water and Wastewater Treatment | ||

| Chemical | ||

| Metals and Mining | ||

| Power Generation | ||

| Pulp and Paper | ||

| Other Industries | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the projected value of the North America industrial centrifuge market by 2031?

The North America industrial centrifuge market is projected to reach USD 5.00 billion by 2031 from USD 3.54 billion in 2026, growing at a CAGR of 7.13% over 2026-2031.

Which centrifuge type leads in North America?

Sedimentation centrifuges led in 2025 with 62.2% share, supported by strong use in wastewater treatment, dairy processing, and biopharma clarification.

Which centrifuge category is growing the fastest?

Filtering centrifuges are expected to post the fastest growth at 8.1% CAGR through 2031, driven by battery material separation and fine-chemical applications.

Which end-use segment is expanding the quickest?

Water and wastewater treatment is forecast to grow at 8.3% CAGR through 2031 as biosolids handling and PFAS-related compliance needs drive dewatering investment.

Which country dominates regional demand?

The United States held 67.5% share in 2025 because it combines major biopharma investment, municipal water infrastructure needs, and energy-transition project activity.

Why is Canada growing faster than the regional average?

Canada is forecast to grow at 8.8% CAGR through 2031, helped by agri-food processing growth, biopharmaceutical activity, wastewater spending, and battery-mineral processing evaluations.

Page last updated on: