Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

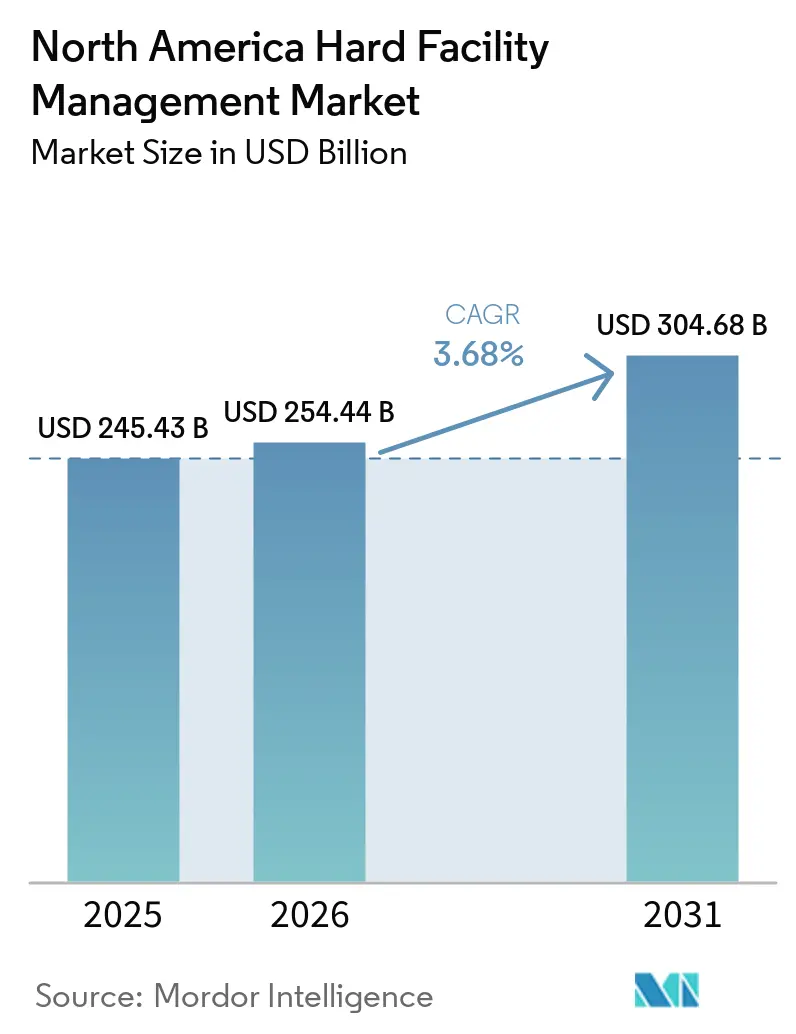

| Base Year Market Size (2025) | USD 245.43 Billion |

| Market Size (2026) | USD 254.44 Billion |

| Market Size (2031) | USD 304.68 Billion |

| Growth Rate (2026 - 2031) | 3.68% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Hard Facility Management Market Analysis by Mordor Intelligence

The North America hard facility management market size is projected to expand from USD 245.43 billion in 2025 and USD 254.44 billion in 2026 to USD 304.68 billion by 2031, registering a CAGR of 3.68% between 2026 and 2031. The North American hard facility management market continues to benefit from long-term output-based contracts tied to mechanical, electrical, and life-safety performance in occupied buildings. These services remain difficult for owners to defer because compliance rules, occupancy requirements, and equipment warranty conditions make uninterrupted upkeep a core operating need. The North American hard facility management market also draws support from building decarbonization programs, expanding data center construction, and the wider use of digital asset management platforms, which lift contract scope and average contract value. Competitive positioning is increasingly shaped by providers that can self-perform technical work, manage multi-site portfolios, and support higher-availability environments with resident engineering teams. The main pressure points remain skilled labor shortages, electrical equipment bottlenecks, and the higher capital needs tied to retrofit and digitalization programs, especially for smaller operators and mid-market clients.

Key Report Takeaways

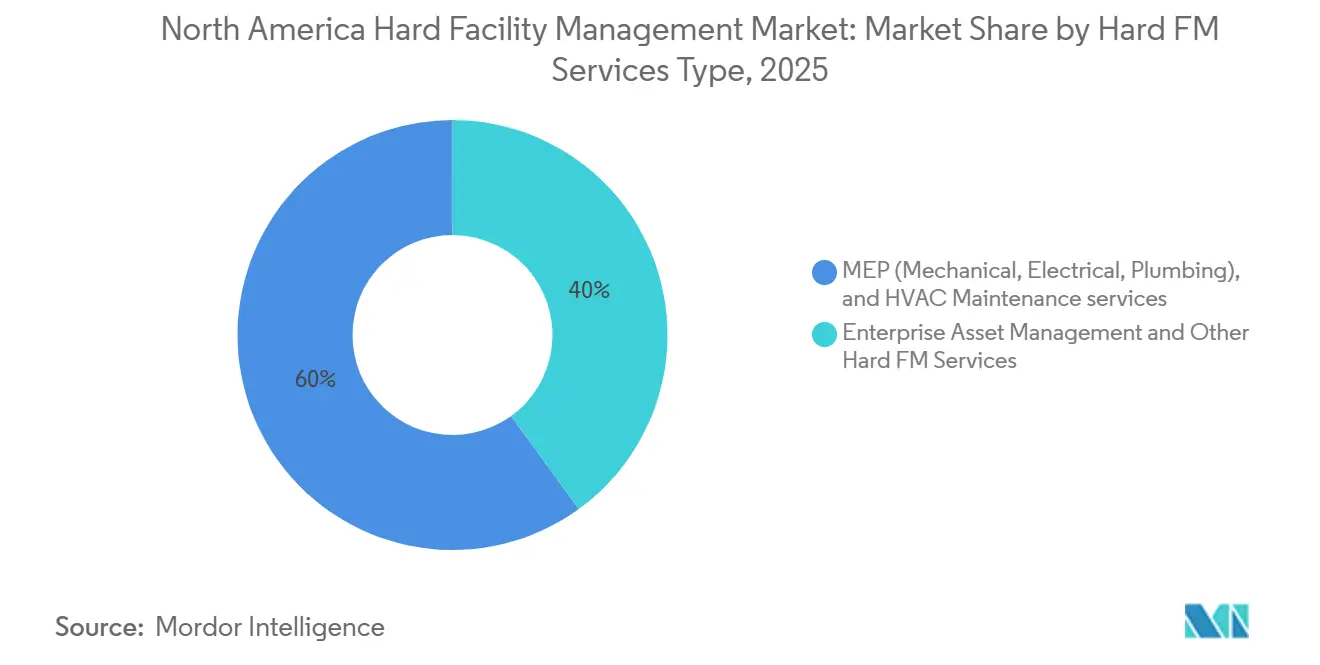

- By hard FM services type, MEP and HVAC maintenance services represented 60.00% of the North America hard facility management market in 2025, while Enterprise Asset Management is projected to expand at a 5.80% CAGR through 2031.

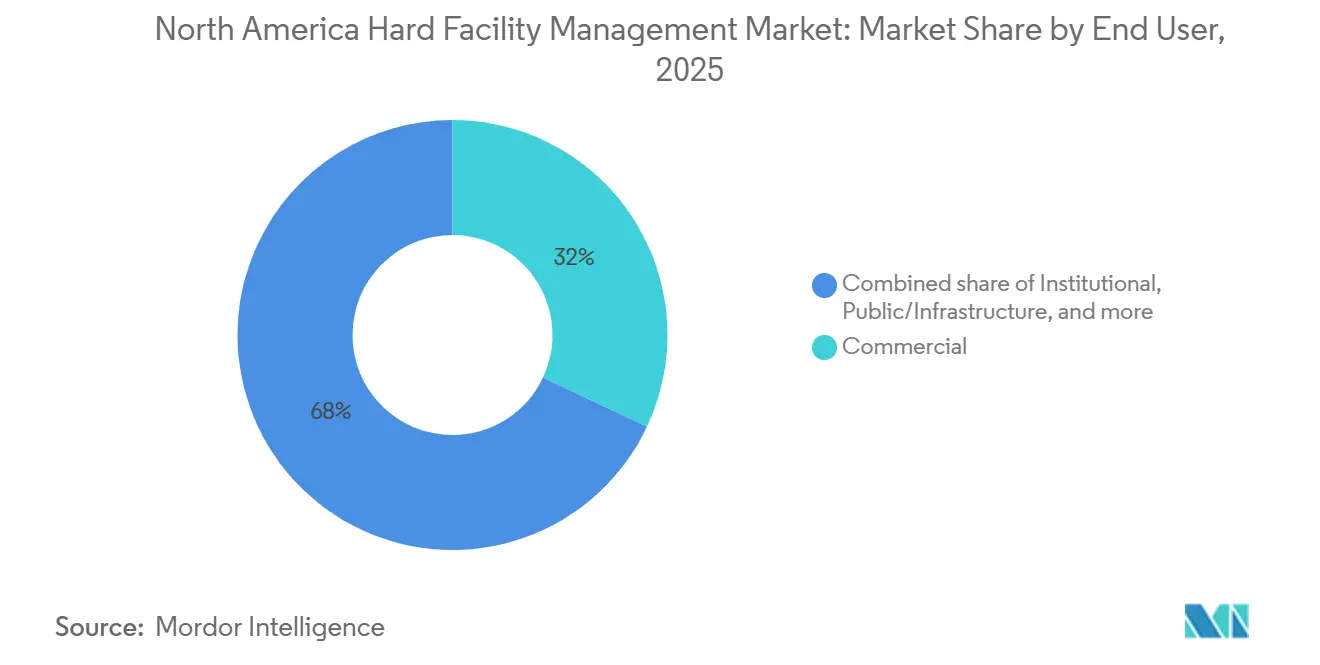

- By end user, commercial clients accounted for 32.00% of the North America hard facility management market in 2025, while public and infrastructure clients are projected to expand at a 5.00% CAGR through 2031.

- By geography, the United States in the North America hard facility management market accounted for 87.00% of regional value in 2025, while Canada is projected to grow at a 5.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Hard Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High HVAC Services Demand In The United States | +1.1% | United States, spill-over to Canada | Short term (≤ 2 years) |

| Building Decarbonization And Performance Standards Accelerating Retrofits | +0.8% | United States and Canada, led by New York, Oregon, and British Columbia | Medium term (2-4 years) |

| AI Data Center Buildout Raising Mission-Critical Mechanical And Electrical Demand | +0.6% | United States data center hubs, including Northern Virginia, Dallas, Phoenix, and Chicago | Short term (≤ 2 years) |

| Smart Building And Predictive Maintenance Adoption | +0.4% | United States and Canada, enterprise and institutional portfolios | Medium term (2-4 years) |

| Rise In Infrastructure And Institutional Asset Renewal Across The Region | +0.3% | North America, with early gains in U.S. federal and Canadian provincial portfolios | Medium term (2-4 years) |

| Return-To-Office Concentration In Premium Buildings Raising Uptime Requirements | +0.2% | United States core office markets, including New York, Chicago, and San Francisco | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High HVAC Services Demand In The United States

In North America, HVAC maintenance stands out as the predominant recurring task in the hard facility management market. This is largely due to the diverse climate across the United States, which consistently tests the resilience of mechanical systems. The imperative to uphold standards in ventilation, filtration, and indoor air quality fuels a steady demand for services. This demand is further amplified by the aging commercial building stock, where older systems necessitate more frequent testing, repairs, and proactive replacement planning. Research highlighted a significant gap, identifying HVAC technicians as critically understaffed. The findings pointed to a staggering 139,000 annual job openings in the United States, coupled with a dwindling talent pipeline. This scenario accentuates the value of service providers boasting self-performing labor capabilities.[1]Jones Lang LaSalle Incorporated, “Building Tomorrow's Workforce Today,” JLL, jll.com Consequently, firms in the North American hard facility management market that can ensure technician availability across expansive portfolios are enjoying enhanced pricing power and improved client retention.

Building Decarbonization And Performance Standards Accelerating Retrofits

Building performance regulations are mandating retrofit work as a necessary expenditure for many large facilities. This trend not only bolsters the North American hard facility management market but also extends both the duration and technical scope of contracts. New York City’s Local Law 97 has heightened the urgency for heating system replacements, electrical upgrades, and consistent compliance support in large buildings. Meanwhile, Oregon’s Building Performance Standard, effective January 1, 2025, introduces statewide operating and maintenance mandates. These new requirements particularly benefit providers skilled in commissioning and energy performance. On a federal level, the Federal Building Performance Standard is steering agencies towards eliminating on-site fossil fuel emissions in government-owned buildings. This federal directive not only underscores the importance of retrofitting but also signals a prolonged demand for such services in government facilities.[2]State of Oregon Department of Energy, “Oregon Building Performance Standard (BPS),” State of Oregon, oregon.gov As a result of these regulatory shifts, the North American hard facility management market is gravitating towards outcome-based agreements. These agreements seamlessly integrate mechanical maintenance, electrification assistance, and energy performance oversight.

AI Data Center Buildout Raising Mission-Critical Mechanical And Electrical Demand

In North America, the hard facility management market is witnessing a surge in demand, particularly in high-availability segments tied to AI-driven data center constructions. These centers impose stricter uptime requirements and heightened service expectations compared to conventional commercial buildings. The US IT load capacity is projected to jump from 80 GW in 2025 to 150 GW by 2028, underscoring a robust demand for cooling systems, power distribution tools, and backup generation support. Global capacity is forecasted to increase by 97 GW from 2025 to 2030, with North America capturing a significant portion of the hyperscale activity. The nature of this work demands more labor, as providers are required to deploy resident engineering teams, ensure quicker response times, and navigate tighter electrical and thermal tolerances. Highlighting the rapid growth of this specialized demand, CBRE noted a 65% year-over-year surge in its critical infrastructure services revenue for Q1 2026, outpacing the broader North American hard facility management market.

Smart Building and Predictive Maintenance Adoption

North America's hard facility management market is transitioning from rigid service schedules to a more dynamic, condition-based maintenance approach. This evolution is reshaping pricing strategies, staffing decisions, and performance metrics for service providers. In a move underscoring this trend, Johnson Controls, in April 2026, bolstered its OpenBlue platform by acquiring Nantum AI, infusing it with AI-driven HVAC optimization and energy control features. CBRE highlighted the mainstreaming of digital oversight, noting its AI-enhanced Smart Facilities Management was active across 20,000 client sites, covering a vast 1 billion square feet. A May 2026 study validated the efficacy of BIM and IIoT in enhancing energy predictions and curbing HVAC energy consumption, further driving client interest in connected maintenance models. As these advanced tools gain traction, the North American hard facility management market is poised to favor providers adept at merging hands-on service delivery with software-driven diagnostics and compliance oversight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Trades Shortages And Wage Inflation | -0.6% | United States, with sharp pressure in Sun Belt markets, and Canada | Long term (≥ 4 years) |

| High Upfront Retrofit And Digitalization Costs | -0.4% | North America, with heavier pressure on mid-market and municipal clients | Medium term (2-4 years) |

| Fragmented Regulations And Compliance Burden | -0.3% | United States multi-state portfolios and Canada multi-province portfolios | Long term (≥ 4 years) |

| Grid Equipment And Transformer Bottlenecks Delaying Electrical Upgrades | -0.3% | United States, especially data center and grid-intensive markets | Short term (≤ 2 years), Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Trades Shortages And Wage Inflation

North America's hard facility management market grapples with a significant constraint: a shortage of licensed HVAC technicians, electricians, and plumbers. Research projected that by 2030, the United States could see 2.1 million unfilled skilled trades positions, leading to potential annual economic losses of USD 1 trillion. This underscores the structural nature of the labor gap, rather than it being a fleeting issue. Hard FM providers find themselves in competition with construction, manufacturing, and energy sectors for these skilled workers. Often, these sectors entice talent with higher starting salaries or more appealing project-based pay. Consequently, labor costs surge at a pace that outstrips the reset rate of many fixed-fee service contracts, squeezing profit margins even amidst steady demand. As a result, the North American hard facility management market is leaning towards firms that prioritize apprenticeship pipelines, in-house training, and direct labor models, rather than over-relying on spot subcontracting.

High Upfront Retrofit And Digitalization Costs

Parts of the client base in North America's hard facility management market are still hesitant to fully embrace the trend. This reluctance stems from the multi-year capital commitments required for retrofit and digitalization programs. Upgrades like IoT sensors, building automation, and predictive maintenance software often necessitate integration with older mechanical systems. This not only escalates upfront costs but also obscures the timeline for payback. Smaller operators find themselves at a disadvantage, facing challenges in accessing enterprise-grade analytics tools, which are costly to develop, license, and maintain. Public and institutional clients, despite recognizing the clear long-term savings, often experience delays. This is due to procurement regulations and budget approvals, which can extend the implementation process across several cycles. A testament to the industry's direction, the acquisition of Alloy Enterprises in May 2026 highlights a growing trend: firms are increasingly opting to purchase technological capabilities rather than develop them in-house. This trend amplifies the competitive challenges for companies with limited capital flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hard FM Services Type, MEP And HVAC Services Anchor Revenue While Enterprise Asset Management Scales

Enterprise Asset Management (EAM) is emerging as the fastest-growing segment in North America's hard facility management market, with projections indicating a robust CAGR of 5.80% from 2026 to 2031. This trend underscores a pivotal shift: moving from reactive maintenance and fragmented work orders to integrated platforms. These platforms seamlessly merge asset records, sensor data, compliance tasks, and lifecycle planning. Major occupiers are leveraging these systems to minimize downtime, ensuring maintenance, documentation, and reporting are streamlined within a cohesive framework. Highlighting the trend, CBRE reported a facilities management revenue of USD 20,645 million in 2025, showcasing the trend of large enterprises merging physical maintenance with data-driven oversight. Further emphasizing this direction, ABM's platform, ABM Connect, garnered recognition on Fast Company’s 2026 list, underscoring the rising commercial significance of software-driven facility intelligence.

In 2025, MEP and HVAC maintenance services commanded a dominant 60.00% share of North America's hard facility management market, underscoring their pivotal role in the region's revenue landscape. This prominence is a testament to the extensive installed base of HVAC systems, electrical assets, and associated controls spanning commercial, institutional, and industrial properties. The demand for these services remains robust, directly influencing occupant comfort, indoor air quality, equipment reliability, and adherence to regulatory standards. Furthermore, as decarbonization initiatives gain traction, contracts that once centered on routine maintenance are increasingly encompassing retrofit and monitoring tasks. While other hard FM services, such as fire safety and technical systems, may be smaller in scale, their consistent demand is anchored in safety obligations and replacement cycles, rather than being seen as discretionary expenses.

By End User, Commercial Demand Remains Broad While Public Sector Renewal Drives Faster Growth

Public and infrastructure clients are emerging as the fastest-growing segment in North America's hard facility management market, with projections indicating a CAGR of 5.00% from 2026 to 2031. In the United States, the GSA's fiscal year 2026 Congressional Justification highlighted a request of USD 10.46 billion, targeting life-safety systems and mechanical infrastructure across federal buildings. Meanwhile, in Canada, the Build Communities Strong Fund has earmarked CAD 51 billion (USD 37.3 billion) over a decade starting 2026-2027, focusing on health, transit, and education assets. Additionally, the Québec Infrastructure Plan has allocated CAD 167 billion (USD 122.1 billion) for public asset maintenance and upgrades. This blend of federal and provincial investments solidifies a more robust public-sector foundation for North America's hard facility management market than in previous cycles.

Commercial clients held a 32.00% share of North America's hard facility management market in 2025, solidifying their status as the dominant end-user segment. High-density occupancy in office, retail, and mixed-use portfolios amplifies the demand for maintenance, particularly for HVAC, electrical, and life-safety systems. JLL’s 2026 report noted a rise in average office utilization from 54% in 2025 to 56% in 2026, indicating more consistent service workloads. As premium buildings spearhead the recovery, their heightened demands for uptime, certification, and data-driven maintenance become evident. Furthermore, institutional and industrial facilities, vital to sectors like healthcare and advanced manufacturing, underscore the industry's reliance on specialized systems that demand minimal downtime.

Geography Analysis

North America Hard Facility Management Market in Other Markets

In 2025, the United States commanded a dominant 87.00% share of North America's hard facility management market, solidifying its status as the region's primary revenue hub. The vast array of properties in the United States, spanning office, industrial, retail, healthcare, education, and mixed-use sectors, ensures a consistent demand for mechanical and electrical services. Highlighting this concentration, EMCOR reported a staggering USD 16.52 billion in revenue from its United States operations for fiscal year 2025, accounting for 97% of the group's total revenue.[3]EMCOR Group, Inc., “Fourth Quarter and Full Year 2025 Earnings Release,” EMCOR Group, emcorgroup.com Furthermore, bolstered by federal decarbonization policies, there is an uptick in retrofit and compliance work, especially with mandates steering federally owned buildings away from on-site fossil fuel use. Adding to this demand is the burgeoning United States data center wave, with projections indicating the national IT load capacity will surge from 80 GW in 2025 to 150 GW by 2028.

Canada is emerging as the fastest-growing player in North America's hard facility management arena, with projections indicating a robust CAGR of 5.20% from 2026 to 2031. Central to this growth is the Québec Infrastructure Plan 2026-2036, unveiled on March 18, 2026, which earmarked a substantial CAD 167 billion (USD 122.1 billion) over a decade, emphasizing the maintenance of public assets. Complementing this, the federal Build Communities Strong Fund injected an additional CAD 51 billion (USD 37.3 billion) over ten years, targeting infrastructure enhancements across provinces and territories. Capitalizing on this momentum, Canadian firms are strategically expanding. A testament to this is Dexterra's bold move in July 2025, acquiring a 40% stake in United States-based PVC for a notable CAD 84.0 million (USD 61.5 million). Further underscoring this trend, JLL inked a significant contract in September 2025 with WestJet, spanning 1.9 million square feet across Calgary's headquarters and 17 airport locales, highlighting the burgeoning integrated FM mandates in Canada's transport sector.

As the North American hard facility management market evolves, a clear polarization is emerging: a divide between expansive maintenance portfolios and the more lucrative mission-critical services. Both the United States and Canada are witnessing heightened expectations from service providers, driven by public decarbonization mandates, institutional renewals, and the rise of AI-linked digital infrastructure. This shift is prompting larger firms to bolster investments in direct labor, data platforms, and specialized engineering. In contrast, smaller operators find themselves grappling with labor shortages and capital limitations. Consequently, while the United States stands firm as the market's anchor, Canada is carving out a niche with its accelerated growth, fueled by public asset renewals and institutional expansions.

Competitive Landscape

Innovation and Integration Drive Future Success

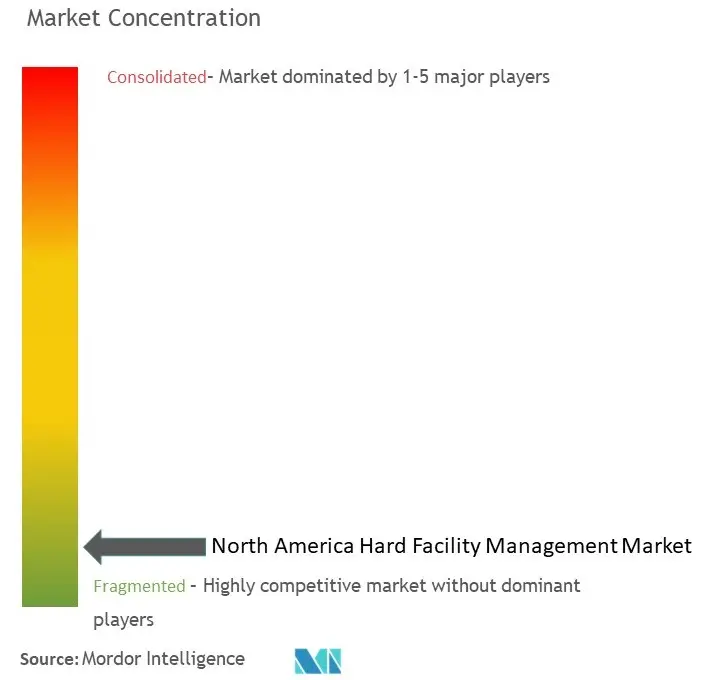

In North America, the hard facility management market exhibits a moderate concentration at the enterprise level, while remaining highly fragmented at lower tiers. Major players like CBRE Group, Jones Lang LaSalle, ABM Industries, EMCOR Group, Cushman and Wakefield, and Johnson Controls vie for substantial multi-site contracts. They leverage proprietary technology tools, maintain self-performing technical workforces, and adeptly navigate complex compliance across expansive portfolios. Highlighting the industry's shift towards digitalization, CBRE's 2025 annual filing spotlighted Nexus AI as a pivotal platform bolstering its Smart Facilities Management offerings. Meanwhile, EMCOR's impressive USD 13.25 billion in remaining performance obligations at 2025's close underscored robust demand from sectors like network communications, institutional clients, and high-tech manufacturing.[4]CBRE Group, Inc., “Annual Report 2025 (Form 10-K / Annual Report Filing),” CBRE Investor Relations, ir.cbre.com In this landscape, North America's hard facility management market underscores the importance of scale, especially when complemented by technical labor expertise and software-driven service visibility.

In North America's hard facility management arena, mission-critical infrastructure has emerged as the prime growth frontier. In a strategic move, CBRE finalized its USD 1.2 billion acquisition of Pearce Services in November 2025. This acquisition birthed a Critical Infrastructure Services division, raking in a commendable USD 1.7 billion in revenue for 2025. Following suit, Johnson Controls made waves in 2026 with its acquisitions of Nantum AI and Alloy Enterprises, bolstering its prowess in building intelligence and liquid cooling for dense environments. Not to be outdone, EMCOR expanded its electrical domain with the January 2025 purchase of Miller Electric Company for USD 865 million, enhancing its foothold in the rapidly growing Southeastern markets. These strategic maneuvers highlight a clear trend: North America's hard facility management market is gravitating towards providers adept at merging field execution with advanced capabilities in power, cooling, controls, and data management.

The forthcoming competitive divide in North America's hard facility management market is poised to revolve around the ability to bundle energy performance, compliance assistance, and mechanical services into a unified contract. Digital platform-equipped providers stand to benefit from heightened switching costs, as elements like performance data, work-order histories, and asset intelligence become integral to the service relationship. ABM's persistent focus on ABM Connect underscores a pivotal shift in mid-market competition, moving from mere labor scale to technology-enhanced visibility. Concurrently, OEM-backed services from giants like Johnson Controls and Siemens intensify the competition, especially in technically intricate buildings, challenging traditional aggregators even amidst a backdrop of consolidation in the North American hard facility management market.

North America Hard Facility Management Industry Leaders

CBRE Group, Inc.

Jones Lang LaSalle Incorporated

ABM Industries Incorporated

EMCOR Group, Inc.

Sodexo, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Johnson Controls, bolstered its thermal management portfolio by acquiring Alloy Enterprises, a Boston-based innovator in liquid cooling technology tailored for high-density data centers. This move, first announced on February 18, 2026, positions Johnson Controls to meet the surging demand for cooling infrastructure, especially from AI-centric hyperscale deployments across North America.

- April 2026: Vanderbilt University entrusted ABM Industries with comprehensive facility operations at its New York City campus. Operating under the ABM Performance Solutions model, ABM's responsibilities span MEP systems integration, critical operations, vendor contract oversight, and maintenance for a historically significant Manhattan property, guiding it through renovation, startup, and long-term operations.

- April 2026: Johnson Controls, furthering its AI ambitions, acquired Nantum AI, a New York firm renowned for its AI-driven energy optimization and HVAC control algorithms. By integrating Nantum's proprietary algorithms into its OpenBlue digital ecosystem, Johnson Controls is poised to lead in autonomous building energy management and solidify its edge in AI-driven hard FM service delivery.

- March 2026: AECOM secured a spot on the U.S. Missile Defense Agency's SHIELD contract, a lucrative indefinite-delivery/indefinite-quantity deal capped at USD 151 billion. The contract mandates a diverse array of engineering and facility infrastructure services, underscoring AECOM's pivotal role in defense-sector hard FM.

- November 2025: CBRE finalized its USD 1.2 billion acquisition of Pearce Services, a top provider of technical maintenance and asset management for critical electromechanical infrastructure in the United States. This deal brought on board over 4,000 employees and 28 locations, pushing CBRE's Critical Infrastructure Services revenue to an estimated USD 1.7 billion in 2025.

- September 2025: WestJet, Canada's second-largest airline, tapped JLL for integrated facilities management. JLL will oversee a 1.9 million-square-foot portfolio, including WestJet's Calgary headquarters and 17 airport locations, bolstering JLL's footprint in Canada's aviation sector.

- August 2025: Dexterra Group sealed the deal on Right Choice, a workforce accommodation provider active in Canada's Montney and Duvernay gas regions, for CAD 69.0 million (approximately USD 50.5 million based on the Bank of Canada's 2025 average rate).

- July 2025: Dexterra Group took a 40% stake in PVC, a facilities management provider from the United States, for CAD 84.0 million (approximately USD 61.5 million at the Bank of Canada's 2025 average rate). They hold an option to acquire the remaining 60% by Q3 2027. This move marks Dexterra's entry into the fragmented United States mid-market FM sector, underscoring its ambition for cross-border expansion.

North America Hard Facility Management Market Report Scope

The North America Hard Facility Management Market Report is Segmented by Hard FM Services Type (MEP and HVAC Maintenance Services, Enterprise Asset Management, and More Hard FM Services), End User (Commercial, Institutional, Public/Infrastructure, Industrial, and More End Users), and Geography (United States, Canada). The Market Forecasts are Provided in Terms of Value (USD).

By Hard FM Services Type

| MEP (Mechanical, Electrical, Plumbing), and HVAC Maintenance services |

| Enterprise Asset Management |

| Other Hard FM Services |

By End User

| Commercial |

| Institutional |

| Public/Infrastructure |

| Industrial |

| Other End Users |

By Country

| United States |

| Canada |

| By Hard FM Services Type | MEP (Mechanical, Electrical, Plumbing), and HVAC Maintenance services |

| Enterprise Asset Management | |

| Other Hard FM Services | |

| By End User | Commercial |

| Institutional | |

| Public/Infrastructure | |

| Industrial | |

| Other End Users | |

| By Country | United States |

| Canada |

Key Questions Answered in the Report

What is the current and forecast size of the North America hard facility management market?

The North America hard facility management market was valued at USD 245.43 billion in 2025, is projected at USD 254.44 billion in 2026, and is forecast to reach USD 304.68 billion by 2031 at a CAGR of 3.68%.

Which service category leads hard facility management demand in North America?

MEP and HVAC maintenance services led the region with 60.00% of value in 2025 because building owners cannot defer critical mechanical and electrical upkeep.

Which end-user group is expanding the fastest across the region?

Public and infrastructure clients are projected to grow at a 5.00% CAGR through 2031, supported by federal and provincial asset renewal programs in the United States and Canada.

Why are data centers becoming more important for facility management providers in North America?

AI-driven data center expansion is raising demand for mission-critical cooling, electrical distribution, backup power, and resident engineering support, especially in major U.S. hyperscale hubs.

Which country drives the most revenue and which one grows the fastest in this region?

The United States accounted for 87.00% of regional value in 2025, while Canada is forecast to post the fastest growth at a 5.20% CAGR through 2031.

What are the main challenges facing providers in this space?

The main challenges are skilled trades shortages, wage inflation, high retrofit and digitalization costs, and delays tied to electrical equipment availability for large upgrade projects.

Page last updated on: