Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

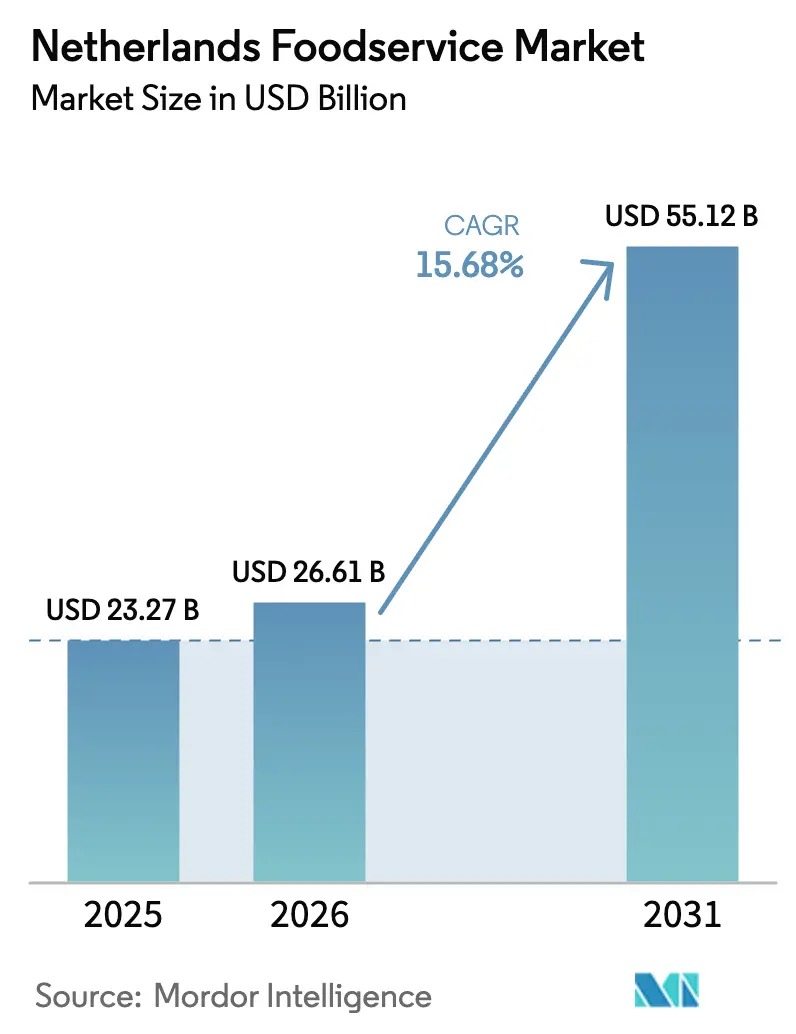

| Base Year Market Size (2025) | USD 23.27 Billion |

| Market Size (2026) | USD 26.61 Billion |

| Market Size (2031) | USD 55.12 Billion |

| Growth Rate (2026 - 2031) | 15.68% CAGR |

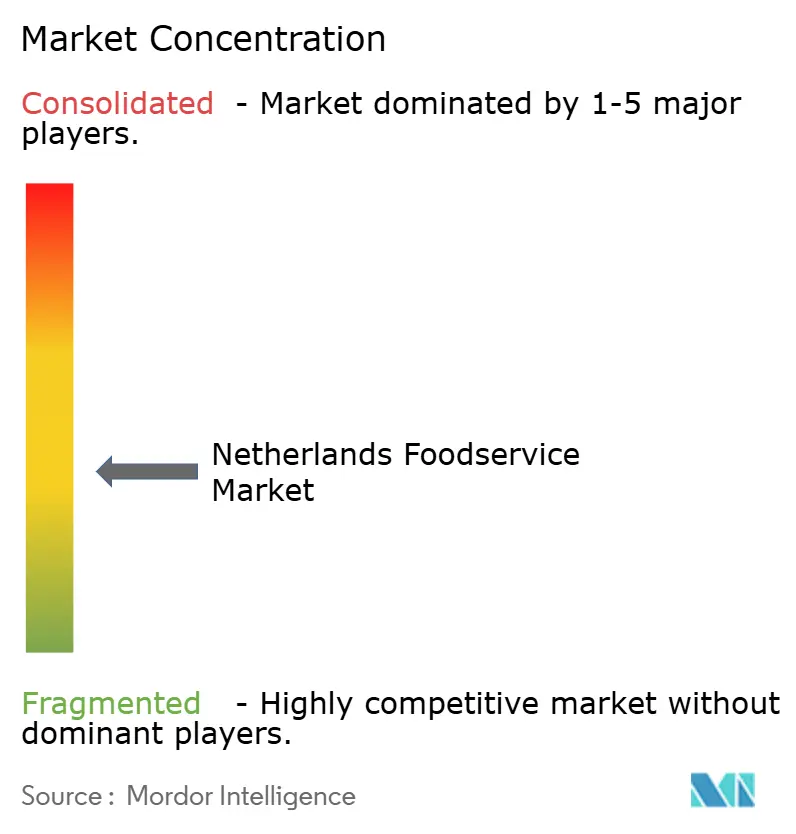

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Foodservice Market Analysis by Mordor Intelligence

The Netherlands foodservice market size is expected to increase from USD 23.27 billion in 2025 to USD 26.61 billion in 2026 and reach USD 55.12 billion by 2031, growing at a CAGR of 15.68% over 2026-2031. The growth in the Netherlands foodservice market is driven by the rapid implementation of digital ordering systems, the cost efficiency of cloud kitchens that avoid high-street rental expenses, and a noticeable consumer shift toward healthier and more experience-focused dining options. Quick service restaurants continue to hold the largest share of revenue; however, delivery-focused cloud kitchens are expanding at a faster rate, supported by venture funding aimed at asset-light business models. Standardized chain outlets are expanding their presence by incorporating self-ordering kiosks, which help mitigate wage pressures. Meanwhile, independent establishments are maintaining their market share by emphasizing menu innovation and localized branding. Challenges such as labor shortages, increased inspection fees, and rising energy-related input costs are driving the adoption of technology, rewarding operators who can increase throughput without a proportional rise in workforce requirements.

Key Report Takeaways

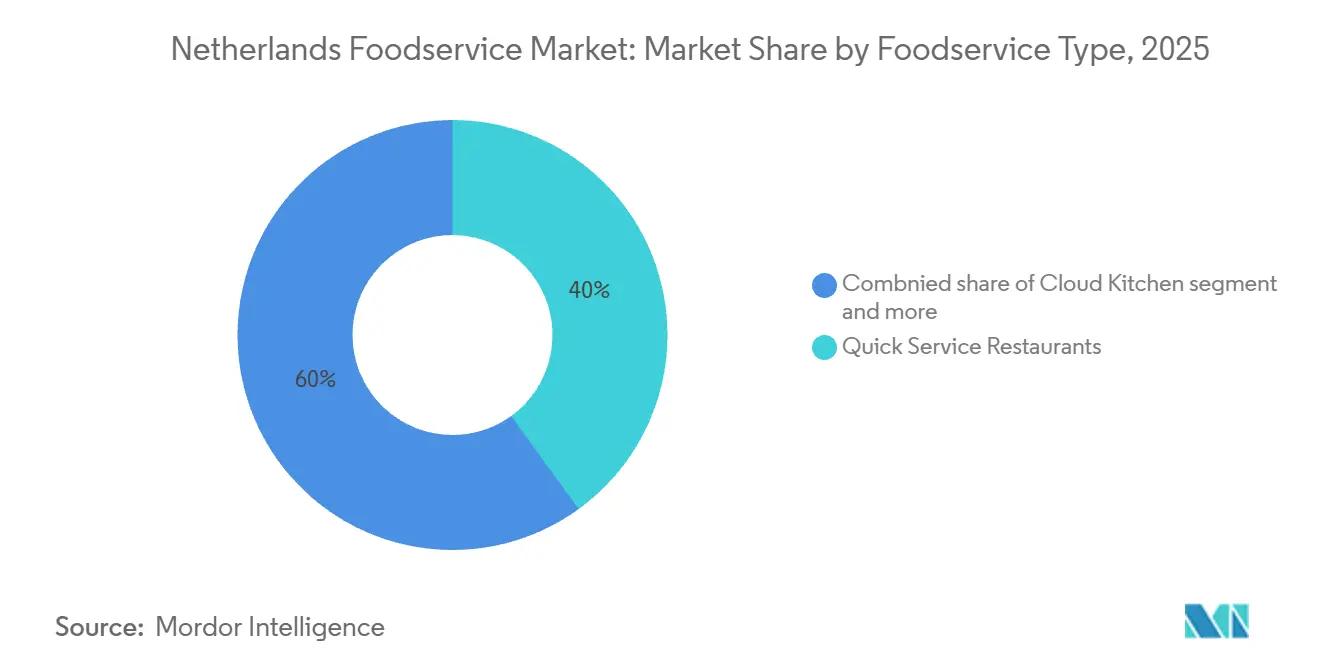

- By foodservice type, quick-service restaurants led with 40.02% of Netherlandsfoodservice market share in 2025; cloud kitchens are advancing at an 26.21% CAGR through 2031, the fastest pace among all formats.

- By outlet, independent players controlled 54.11% of the Netherlands foodservice market size in 2025; chained concepts are forecast to grow at a 16.21% CAGR through 2031.

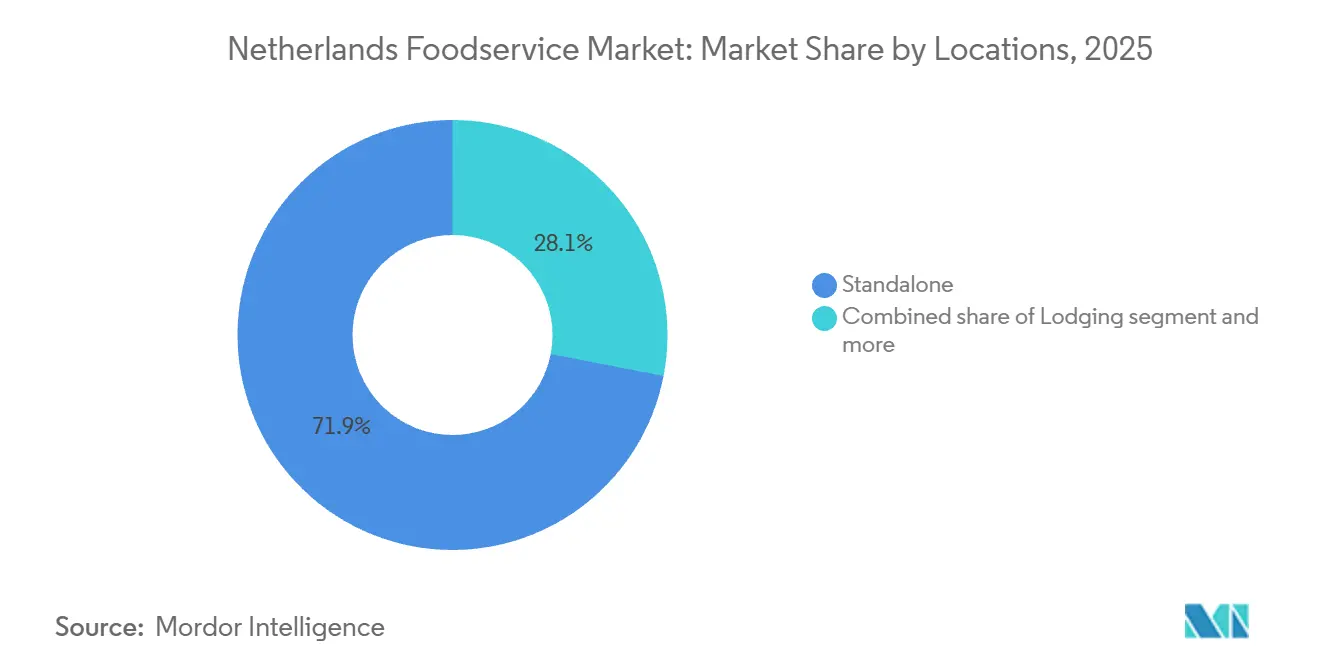

- By location, standalone outlets held 71.23% of Netherlands foodservice market share in 2025; lodging-based locations recorded the highest growth trajectory at a 19.11% CAGR through 2031.

- By service type, dine-in accounted for 55.53% of Netherlands foodservice market; takeaway services are expanding at a 17.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Netherlands contributes to a system defined not by any single country or region but by the interaction of many. The global food service market data by Mordor Intelligence represents that combined structure.

Netherlands Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-conscious trends favoring plant-based and low-calorie options | +1.8% | National, with urban concentration in Amsterdam, Rotterdam, Utrecht | Medium term (2-4 years) |

| Rapid expansion of cloud kitchens reducing real estate costs | +3.2% | National, with early concentration in Amsterdam, Rotterdam, The Hague | Short term (≤ 2 years) |

| Strong multicultural influences boosting ethnic and international cuisines | +2.1% | National, with higher penetration in Amsterdam, Rotterdam, The Hague | Long term (≥ 4 years) |

| Growth in quick service restaurants for convenience | +2.5% | National, with suburban and highway corridor expansion | Medium term (2-4 years) |

| Expansion of delivery platforms enabling wider reach | +2.8% | National, with urban density driving higher order volumes | Short term (≤ 2 years) |

| Rising demand for experiential dining with enhanced ambiance and service | +1.5% | National, with premium segment concentration in Amsterdam, Rotterdam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health-conscious trends favoring plant-based and low-calorie options

Consumer demand for plant-based and reduced-calorie menus is reshaping product development cycles and supplier relationships across Dutch foodservice. McDonald's Netherlands integrated the McPlant burger—developed with Beyond Meat—into its permanent menu in 2024, reflecting sustained demand from vegetarians and flexitarians who prioritize protein alternatives without sacrificing convenience. This shift extends beyond QSR chains; full-service operators are reformulating signature dishes to accommodate dietary preferences, often at higher ingredient costs that compress margins but attract a premium-paying demographic. The trend aligns with broader European Union sustainability directives that encourage reduced livestock consumption, creating regulatory tailwinds for plant-forward concepts. Operators that fail to offer credible plant-based options risk losing share to competitors who can signal alignment with health and environmental values, particularly among urban millennials and Gen Z diners who prioritize transparency in sourcing and preparation.

Rapid expansion of cloud kitchens reducing real estate costs

Cloud kitchens are expanding rapidly due to their ability to eliminate front-of-house labor, reduce space requirements, and enable operators to test new concepts without committing to long-term leases. Keatz, a Netherlands-based cloud kitchen platform, raised funding in March 2024 to grow its network of delivery-only facilities in Amsterdam and Rotterdam. The platform targets restaurant brands aiming to enter new neighborhoods without establishing physical storefronts. This model is particularly appealing in Dutch cities, where rising commercial real estate prices and zoning restrictions limit new restaurant permits. By consolidating multiple virtual brands within a single facility, cloud kitchens achieve kitchen utilization rates exceeding 80%, compared to 50% to 60% for traditional restaurants during off-peak hours. However, this approach relies heavily on third-party delivery platforms, which charge 20% to 30% commissions and control customer data, resulting in thin margins and limited brand equity for operators. Despite these challenges, the projected compound annual growth rate for cloud kitchens through 2031 indicates that cost efficiency and speed to market benefits outweigh these structural drawbacks for an increasing number of delivery-focused brands.

Strong multicultural influences boosting ethnic and international cuisines

The Netherlands' diverse population, influenced by Indonesian, Surinamese, Turkish, and Moroccan communities, has driven consistent demand for ethnic cuisines, transitioning these offerings from niche markets to mainstream dining. Amsterdam has witnessed the opening of numerous new restaurants, featuring Spanish, Indonesian, Korean, Japanese, Italian, Mexican, and West African concepts. This trend highlights both immigrant entrepreneurship and a growing consumer interest in culinary diversity. The multicultural landscape enables independent operators to differentiate themselves without directly competing with quick-service restaurant chains. However, it also fragments the market, limiting opportunities for economies of scale. For example, Indonesian rijsttafel restaurants often command premium pricing in tourist-heavy areas, while Turkish kebab shops typically operate in neighborhood corridors with high-volume, low-margin business models. A key challenge for ethnic restaurant operators lies in adhering to the Netherlands Food and Consumer Product Safety Authority's food safety regulations, which mandate Hazard Analysis and Critical Control Points (HACCP)-compliant documentation and temperature-control systems, requirements that can be costly for small-format kitchens. Operators who successfully combine authentic recipes with efficient operations have the potential to attract both heritage communities and adventurous Dutch diners seeking alternatives to traditional Western European menus.

Growth in quick service restaurants for convenience

Quick service restaurants lead the Netherlands foodservice market, driven by their consistent quality, fast service, and affordability, which resonate with budget-conscious consumers amid inflationary pressures. According to data from Statistics Netherlands (CBS), fast-food turnover grew by 6.4% year-on-year in the second quarter, outpacing the 6.3% growth of full-service restaurants, as consumers increasingly opted for counter-service formats over sit-down dining. McDonald's accounted for a significant share of quick service restaurant visits during this period, leveraging drive-thru lanes, mobile ordering, and delivery partnerships with Just Eat Takeaway to address diverse meal occasions. The resilience of the quick service restaurants segment is supported by operational standardization, which helps address labor challenges. Franchisees utilize self-ordering kiosks and automated beverage dispensers to maintain efficiency even during staffing shortages. However, the segment faces margin pressures due to rising minimum wages, which reached higher hourly rates during the same period, and competition from cloud kitchens that lower costs by eliminating dine-in operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor cost increases and persistent workforce shortages | -2.3% | National, with acute pressure in Amsterdam, Rotterdam, Utrecht | Short term (≤ 2 years) |

| Stringent regulatory compliance for food safety and labor laws | -1.2% | National, with higher burden on independent operators | Medium term (2-4 years) |

| Food safety concerns and hygiene standards | -0.8% | National, with heightened scrutiny in high-traffic urban areas | Medium term (2-4 years) |

| Supply chain disruptions for raw materials | -1.1% | National, with import-dependent categories (cocoa, grains) most exposed | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Labor cost increases and persistent workforce shortages

Labor shortages and wage inflation are impacting profit margins in the Dutch foodservice market. According to Eurostat, the labor cost index increased by 6.9% year on year as of June 2025 [1]Source: Eurostat, “Labour Cost Index,” ec.europa.eu. The 2025 to 2026 Collective Labor Agreement introduced wage increases ranging from 2.5% to 6.9% across various service categories. This has left operators with the difficult choice of raising menu prices, which could potentially lead to a decline in sales volume, or absorbing the higher costs, which reduces profitability. Data from the Central Bureau of Statistics (CBS) revealed thousands of open vacancies in the first quarter of 2025, primarily in kitchen and front-of-house roles. Additionally, student enrollment in hospitality education programs declined over the past two academic years, indicating a shrinking talent pool. ABN AMRO projected hundreds of bankruptcies in 2025, largely due to operators' inability to transfer wage increases to price-sensitive consumers. The workforce in this sector is predominantly young, with half aged between 15 and 24, resulting in high turnover rates and increased training costs, which negatively affect service consistency. To address these challenges, operators are adopting solutions such as self-ordering kiosks, automated beverage systems, and delivery-only formats to reduce staffing needs. However, these technological investments require significant upfront capital, which many independent operators may find difficult to secure.

Stringent regulatory compliance for food safety and labor laws

The Dutch Authority for Food and Consumer Product Safety (NVWA) enforces Hazard Analysis and Critical Control Points (HACCP) principles, requiring foodservice operators to implement temperature controls, cross-contamination prevention measures, traceability systems, and documentation protocols. Non-compliance can result in fines or business closures [2]Source: NVWA, “Inspection Fees 2024,” nvwa.nl. In January 2024, NVWA increased inspection fees, adding fixed costs that disproportionately affect small independent operators, who often lack dedicated compliance staff. Additionally, building requirements for catering establishments mandate durable surfaces, ventilation systems, and drainage infrastructure, with retrofitting older properties potentially incurring significant costs. Labor regulations further complicate operations. The Hospitality Development Platform (HOP), launched in April 2025, introduced an employer contribution and an employee contribution to fund workforce training, adding to payroll expenses. Chained operators are better positioned to manage these costs, as they can distribute compliance investments across multiple locations and utilize centralized legal teams. In contrast, independent operators often operate in regulatory gray areas, risking penalties or exiting the market altogether. This regulatory disparity accelerates market consolidation, with franchisees and multi-unit operators gaining market share at the expense of single-location restaurants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Disrupt Traditional Models

Quick service restaurants accounted for 40.02% of the market share in 2025, highlighting consumer preferences for speed, consistency, and value-oriented pricing, particularly in the context of inflation-constrained budgets. Meanwhile, cloud kitchens are projected to grow at a compound annual growth rate (CAGR) of 26.21% through 2031. This growth is driven by advantages such as lower real estate costs and integration with delivery platforms, enabling operators to experiment with new concepts without committing to long-term leases. For instance, Keatz secured USD 19 million in Series A funding in March 2024 to expand its facilities in Amsterdam and Rotterdam, targeting restaurant brands seeking a neighborhood presence without the need for physical storefronts.

Full service restaurants are experiencing margin pressures due to rising labor costs and regulatory requirements. However, they continue to attract experiential diners who are willing to pay a premium for ambiance and personalized service. Joelia in Rotterdam exemplifies this segment with its Michelin-starred menu and exclusive Chef's Table offerings. The contrast between the stability of quick service restaurants and the rapid growth of cloud kitchens reflects a structural shift toward asset-light, delivery-focused models that minimize reliance on front-of-house labor and commercial real estate. McDonald's Netherlands has implemented self-ordering kiosks and mobile app integration to sustain throughput despite labor shortages. Similarly, cloud kitchen operators are consolidating multiple virtual brands under a single facility, achieving kitchen utilization rates exceeding 80%.

By Outlet: Chained Operators Scale Through Standardization

Independent outlets accounted for 54.11% of the market share in 2025, highlighting the Netherlands' entrepreneurial restaurant culture and consumer preference for unique, locally-rooted concepts. However, chained outlets are projected to grow at a compound annual growth rate (CAGR) of 16.21% through 2031, driven by standardized operations, centralized procurement, and investments in technology that address labor volatility and regulatory challenges [3]Source: CBS Netherlands, “Hospitality Turnover Q3 2025,” cbs.nl. For example, Deliverect's case study at Barak revealed that 92% of orders are now processed through self-service kiosks, with 16% of transactions including paid upsells, contributing 8% of total revenue. This scalability advantage is often difficult for independent operators to achieve without dedicated information technology resources.

In June 2024, Domino's Pizza inaugurated a 3,000-square-meter production facility in Nieuwegein, centralizing dough production and toppings preparation to support its Dutch franchise network. This initiative has reduced per-unit costs and ensured product consistency. While independent operators maintain strengths in menu flexibility, local sourcing, and brand storytelling, which appeal to consumers seeking authenticity, they face significant challenges. These include rising labor costs, compliance requirements from the Netherlands Food and Consumer Product Safety Authority (NVWA), and limited access to capital for technology upgrades. According to ABN AMRO, 450 bankruptcies are forecasted for 2025, with single-location operators being disproportionately affected due to their limited financial capacity to withstand wage inflation or supply chain disruptions.

By Location: Lodging Segment Gains from Tourism Recovery

Standalone locations accounted for 71.23% of the market share in 2025, highlighting the prominence of street-level restaurants, shopping-district eateries, and suburban quick service restaurant outlets that attract foot traffic and drive-thru customers. Lodging-based foodservice is projected to grow at a compound annual growth rate (CAGR) of 19.11% through 2031, driven by hotel portfolio acquisitions and the recovery of tourism, despite challenges such as Amsterdam's capacity freeze and tax increases. For instance, Leonardo Hotels acquired the Zien Group portfolio (1,522 rooms) in the summer of 2024, Extendam purchased Mercure Den Haag Central, and Ramphastos Investments acquired Hotels van Oranje. These acquisitions include integrated restaurant and bar operations that cater to the demand of hotel guests. An example of this integration is the Joelia restaurant in Rotterdam's Hilton Hotel, which offers Michelin-starred dining and attracts both hotel guests and local diners seeking premium experiences.

Retail and travel locations face challenges from e-commerce substitution and changing commuter patterns, as hybrid work reduces foot traffic in office districts and airport passenger volumes remain below pre-pandemic levels. Leisure locations such as theme parks, museums, and event venues benefit from increased experiential spending but are limited by seasonal demand and restricted operating hours. Standalone operators need to invest in digital marketing, delivery partnerships, and loyalty programs to maintain customer traffic. In contrast, lodging operators benefit from built-in demand, as hotel guests often prioritize convenience over exploring external dining options. Amsterdam's "new-for-old" rule, implemented in 2024, restricts net increases in hotel capacity, thereby limiting supply and supporting occupancy rates, which in turn sustain demand for hotel-based restaurants.

By Service Type: Takeaway Surges as Delivery Infrastructure Matures

Dine-in services are projected to retain 55.53% of the market share in 2025, highlighting consumer preferences for social dining experiences, ambiance, and full-service hospitality that cannot be replicated at home. Meanwhile, takeaway services are expected to grow at a compound annual growth rate (CAGR) of 17.14% through 2031. This growth is driven by factors such as Just Eat Takeaway's employed-courier model and its acquisition by Prosus in February 2025 for USD 4.1 billion, which underscored the strategic value of delivery infrastructure.

However, delivery services face structural challenges, including platform commissions of 20% to 30% that reduce restaurant margins and ongoing courier labor disputes. For instance, the Federation of Dutch Trade Unions (FNV) Riders Union has advocated for improved working conditions, which could increase platform costs and further compress restaurant profitability. To remain competitive, dine-in operators must focus on experiential elements such as open kitchens, sommelier pairings, and live entertainment, which justify premium pricing and are difficult for delivery platforms to replicate. Takeaway operators can mitigate platform commission costs by investing in proprietary ordering applications and in-house courier fleets. However, this approach requires significant capital investment and operational expertise, which many independent operators may lack. The market's trajectory indicates a bifurcation: high-volume quick-service restaurant (QSR) chains are likely to integrate delivery as a core channel, while full-service restaurants will treat delivery as a supplementary revenue stream, prioritizing dine-in margins through experiential differentiation.

Geography Analysis

Amsterdam remains the largest city and primary tourism hub in the Netherlands, dominating the country's foodservice landscape. However, regulatory measures are influencing growth patterns. In 2024, the city introduced a "new-for-old" rule, restricting net increases in hotel capacity, which limits lodging-based foodservice expansion. Additionally, tourist taxes rose from 7% to 12.5% plus EUR 3 per night in 2024, potentially reducing visitor numbers and restaurant traffic. Despite these challenges, Amsterdam witnessed over 100 new restaurant openings in 2026, featuring cuisines such as Spanish, Indonesian, Korean, Japanese, Italian, Mexican, and West African. This growth reflects both immigrant entrepreneurship and a strong consumer demand for diverse culinary experiences. The city's high population density and efficient public transport system also benefit delivery platforms. For instance, Just Eat Takeaway records higher order volumes per restaurant in Amsterdam compared to suburban areas, where car dependency limits delivery reach. Cloud kitchen operators like Keatz are expanding in Amsterdam, leveraging high commercial real estate costs, often exceeding EUR 300 per square meter annually in prime districts, to focus on delivery-only formats that eliminate the need for front-of-house spaces.

Rotterdam and The Hague, the second and third largest urban markets in the Netherlands, exhibit unique foodservice dynamics shaped by their demographic and economic profiles. Rotterdam's port-driven economy and multicultural population, influenced by Surinamese, Turkish, Moroccan, and Cape Verdean communities, sustain demand for ethnic cuisines. These offerings extend beyond tourist-focused establishments to neighborhood corridors serving local heritage communities. Joelia, a Michelin-starred restaurant in Rotterdam's Hilton Hotel, exemplifies the city's premium dining segment, attracting both hotel guests and local patrons willing to spend over EUR 100 per person for chef-driven menus and experiential dining. In The Hague, Drippy's launched its smashburger concept before expanding to Rotterdam in April 2025, with plans to open in Amsterdam by June 2025. This illustrates how emerging brands often test their formats in secondary cities before entering Amsterdam's more competitive and expensive market. The Hague's concentration of government offices and international organizations drives weekday lunch demand, favoring quick-service restaurant chains and fast-casual formats over full-service dining. Meanwhile, Rotterdam's younger demographic and vibrant nightlife support café and bar concepts that thrive on evening and weekend traffic.

Utrecht, Eindhoven, and smaller cities in the Netherlands exhibit distinct growth dynamics influenced by factors such as student populations, suburban expansion, and highway connectivity. Utrecht's central location and large student population, primarily from Utrecht University, create demand for budget-friendly quick service restaurant formats and delivery services that cater to price-sensitive consumers. In contrast, Eindhoven's technology sector, anchored by companies like Advanced Semiconductor Materials Lithography and Philips, supports higher-income dining preferences, favoring experiential concepts and international cuisines. Suburban markets outside the Randstad region (Amsterdam-Rotterdam-Utrecht-The Hague corridor) face challenges such as lower population density and car dependency, which limit the viability of delivery-focused models. These areas tend to favor drive-thru quick-service restaurant formats and standalone family restaurants over cloud kitchens or delivery-optimized concepts.

The food service market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for South Africa, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Netherlands foodservice market is fragmented, offering opportunities for niche ethnic cuisines, plant-based concepts, and technology-driven ghost kitchens that can scale without the high fixed costs of traditional restaurants. International quick service restaurant chains such as McDonald's, Domino's, and Subway utilize standardized operations, centralized procurement, and self-ordering kiosks to address labor challenges. In contrast, independent operators focus on chef-driven menus, local sourcing, and cultural authenticity to appeal to consumers seeking alternatives to standardized chain offerings.

Technology adoption is becoming a key competitive factor. For instance, Deliverect reported that 92% of orders at its Dutch client Barak are processed through self-service kiosks, with 16% of transactions including paid upsells, contributing 8% of total revenue. This highlights how digital interfaces can enhance margins without requiring proportional increases in staffing. Strategic trends indicate a bifurcation in the market as capital-intensive chains are investing in automation and delivery infrastructure to maintain market share, while asset-light disruptors are bypassing traditional real estate and labor models entirely.

McDonald's Netherlands demonstrated responsiveness to plant-based demand by permanently adding the McPlant burger to its menu in 2024. Similarly, Domino's opened a 3,000-square-meter production facility in Nieuwegein in June 2024 to centralize dough production and reduce per-unit costs. Emerging disruptors include multicultural operators leveraging Indonesian, Turkish, and Surinamese cuisines to address underserved segments, as well as premium experiential concepts like Joelia, which offers Michelin-starred menus and Chef's Table experiences at EUR 100 or more per person. White-space opportunities exist in health-focused fast-casual formats, delivery-optimized virtual brands, and hotel-integrated restaurants that cater to captive guest demand. Operators that effectively implement digital ordering, optimize delivery logistics, and scale operations without proportional increases in headcount or real estate costs are likely to gain market share. Conversely, those unable to adapt may face margin pressures due to labor cost inflation and regulatory challenges.

Netherlands Foodservice Industry Leaders

Alsea SAB de CV

Autogrill SpA

Bagels & Beans BV

Bidfood Nederland BV

Domino’s Pizza Enterprises Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Avolta inaugurated a notable Starbucks store at Amsterdam Schiphol Airport. The store provides a premium coffeehouse experience, featuring Starbucks’ Mastrena espresso machines and a curated dining menu that includes croissants, focaccias, and warm sandwiches.

- October 2024: Subway has signed master franchise agreements in the past three years, resulting in commitments to open thousands of new restaurants globally. This growth included entering new markets such as Paraguay and Mongolia, as well as significant expansion in European countries including the Netherlands.

- March 2024: Inspire Brands achieved a notable milestone by opening its 10,000th international restaurant in Lelystad, Netherlands, under the Dunkin’ brand in collaboration with Jordan Benelux Holding.

Netherlands Foodservice Market Report Scope

The foodservice market includes businesses that prepare and serve food and beverages for immediate consumption outside the home. This includes restaurants, cafes, fast food outlets, catering services, and delivery services. The market is segmented as follows: segmentation by foodservice type includes café and bars such as bars and pubs, cafés, juice, smoothie, and dessert bars, and specialist coffee and tea shops. It also includes cloud kitchens, full-service restaurants offering Asian cuisine, European cuisine, Latin American cuisine, Middle Eastern cuisine, North American cuisine, and other cuisines, as well as quick service restaurants such as bakeries, burgers, ice cream, meat-based cuisines, pizza, and other cuisines. Segmentation by outlet type includes chained outlets and independent outlets. Segmentation by location includes leisure, lodging, retail, standalone, and travel. Segmentation by service type includes dine-in, takeaway, and delivery. The market sizing has been done in value terms in USD for all the above mentioned segments.

By Foodservice Type

| Café and Bars | By Cuisine | Bars and Pubs |

| Café | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Others | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-Based Cuisines | ||

| Pizza | ||

| Others |

By Outlet

| Chained Outlet |

| Independent Outlets |

By Location

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

By Serivce Type

| Dine-In |

| Takeaway |

| Delivery |

| By Foodservice Type | Café and Bars | By Cuisine | Bars and Pubs |

| Café | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Others | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-Based Cuisines | |||

| Pizza | |||

| Others | |||

| By Outlet | Chained Outlet | ||

| Independent Outlets | |||

| By Location | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| By Serivce Type | Dine-In | ||

| Takeaway | |||

| Delivery | |||

Key Questions Answered in the Report

How large is the Netherlands foodservice market in 2026?

The Netherlands foodservice market size stands at USD 26.61 billion in 2026, on track to reach USD 55.12 billion by 2031.

Which segment is expanding fastest?

Cloud kitchens lead growth, advancing at a 26.21% CAGR as brands favor delivery-only, asset-light models.

What share do independent restaurants hold?

Independents held 54.11% of 2025 revenue but face pressure from chains scaling at 16.21% CAGR.

How are labor costs affecting operators?

Wage inflation of up to 6.9% under the 2025-2026 agreement is squeezing margins, driving adoption of kiosks and automation.

Which geography shows the highest premium-dining density?

Amsterdam tops premium spend, hosting the largest cluster of Michelin-recognized venues in the country.

Page last updated on: