Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

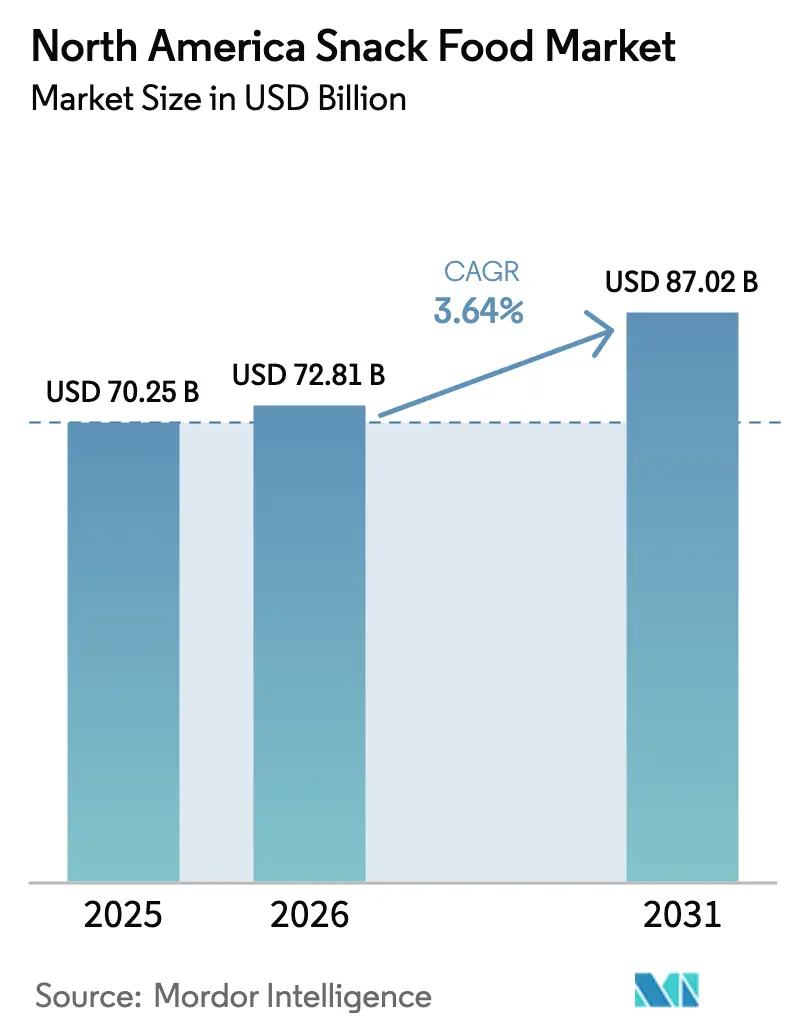

| Base Year Market Size (2025) | USD 70.25 Billion |

| Market Size (2026) | USD 72.81 Billion |

| Market Size (2031) | USD 87.02 Billion |

| Growth Rate (2026 - 2031) | 3.64% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Snack Food Market Analysis by Mordor Intelligence

The North America snack food market size is expected to grow from USD 70.25 billion in 2025 to USD 72.81 billion in 2026 and is forecast to reach USD 87.02 billion by 2031 at 3.64% CAGR over 2026-2031. The market continues to expand as consumers increasingly rely on snacks for various purposes, such as quick breakfasts and meal replacements. This shift in consumer behavior is encouraging manufacturers to improve their product offerings and reformulate them to meet the growing demand for healthier options. There is a rising interest in snacks that provide indulgence without guilt, feature premium and unique flavors, and are made with sustainably sourced ingredients, all of which are driving the market's growth. Retailers are dedicating more shelf space to frozen snacks that are compatible with air fryers, reflecting the influence of air fryer popularity on product innovation. Regulatory changes introduced by the United States Food and Drug Administration (FDA), such as stricter guidelines for "healthy" claims and the removal of synthetic dyes, are pushing companies to innovate and adapt their products. While competition in the market remains moderate, recent mergers and acquisitions indicate that major players are expanding their operations to strengthen their distribution networks and maintain their pricing power in an evolving market landscape.

Key Report Takeaways

- By product type, savory snacks captured 32.12% of the North America snack food market share in 2025; frozen snacks are projected to expand at a 5.44% CAGR through 2031.

- By category, conventional products held 87.92% of the North America snack food market size in 2025, whereas organic/clean-label offerings are poised to grow at a 5.03% CAGR between 2026-2031.

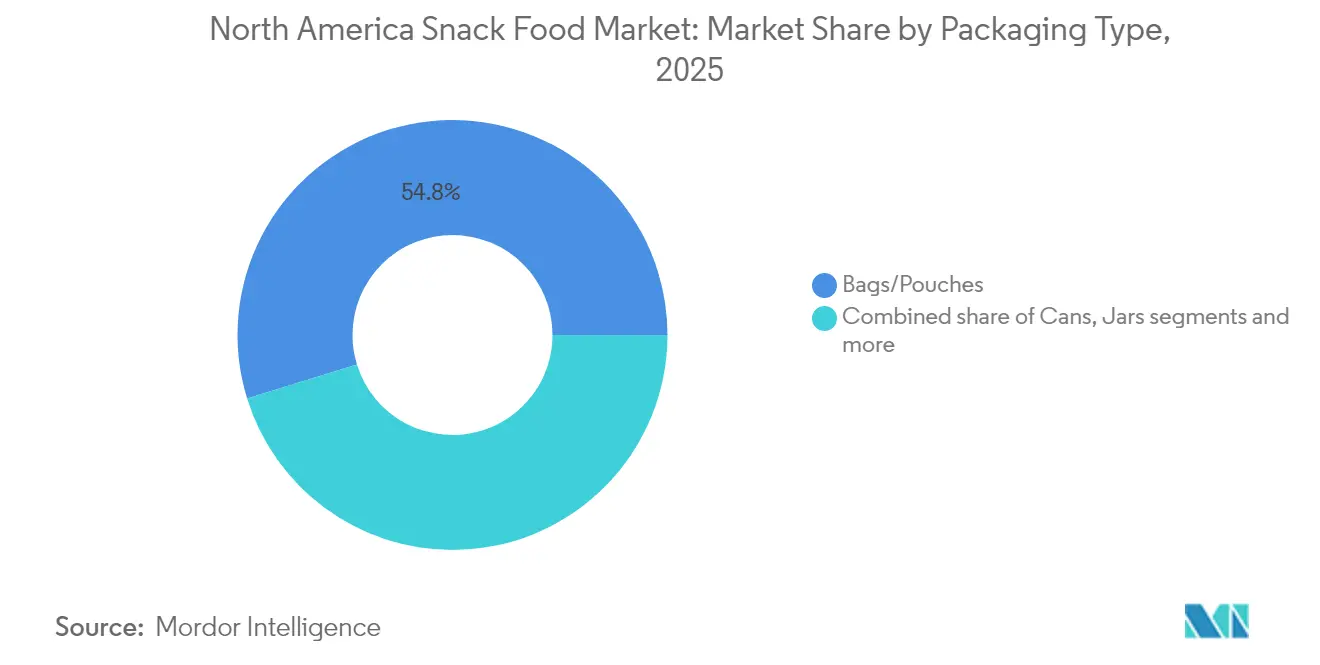

- By packaging, bags/pouches commanded 54.78% revenue share of the North America snack food market size in 2025, while cans recorded the highest forecast CAGR at 4.32% to 2031.

- By distribution channel, supermarkets/hypermarkets accounted for 46.62% of the North America snack food market size in 2025, but online retail is expected to post a 6.38% CAGR through 2031.

- By country, the United States dominated with 81.35% of regional market share in 2025; Mexico is the fastest-growing country, advancing at a 5.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Snack Food Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for convenient and portable formats | +1.2% | North America-wide, strongest in urban centers | Medium term (2-4 years) |

| Increasing consumer preference for healthy snacking options | +0.8% | United States and Canada leading, Mexico following | Long term (≥ 4 years) |

| Innovation in flavors and gourmet premium products | +0.7% | United States premium markets, expanding to Canada | Short term (≤ 2 years) |

| Growing focus on sustainability and ethical sourcing | +0.6% | United States and Canada regulatory-driven, Mexico emerging | Long term (≥ 4 years) |

| Consumption trends among youth and Gen Z | +0.5% | Cross-regional, social media amplified | Medium term (2-4 years) |

| Preference for emotional and functional snacking | +0.3% | Urban North America, premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient and portable formats

Snack foods are becoming increasingly important in North America as consumers look for convenient options to fit their busy and fast-paced lifestyles. With the United States employment rate at 95.8% as of June 2025, as per the Bureau of Labor Statistics, many people face time constraints that influence their eating habits[1]Source: Bureau of Labor Statistics, "The Employment Situation— July 2025," bls.gov. According to the International Food Information Council (IFIC) Spotlight Survey 2024, 56% of Americans now replace traditional meals with snacks or smaller eating occasions, showing a clear shift in how people consume food[2]Source: International Food Information Council (IFIC), "American Consumer Perceptions of Snacking," ific.org . To meet this growing demand, manufacturers are focusing on creating easy-to-carry and ready-to-eat options, such as single-serve pouches, resealable bags, and portion-controlled packs. For instance, Bumble Bee introduced its “Snack On The Run! Tuna Snackers” in early 2024, a protein-packed kit with flavored tuna and crackers that is perfect for eating on the go. These types of products demonstrate how brands are adapting to changing consumer habits by offering solutions, making snacking a more versatile option throughout the day.

Increasing consumer preference for healthy snacking options

Consumers in North America are increasingly choosing healthier snack options, driven by changing regulations and a stronger focus on nutrition. The Food and Drug Administration's updated definition of “healthy,” which will take effect in February 2028, imposes stricter limits on added sugars and sodium while requiring snacks to include key food groups. Manufacturers are modifying their recipes to meet these standards and market their products as healthy. According to the International Food Information Council (IFIC) Food and Health Survey 2024, 66% of Americans are trying to reduce their sugar intake, highlighting a growing awareness of ingredients[3]Source: International Food Information Council (IFIC), "2024 IFIC Food and Health Survey," ific.org. Complementing this, a Pew Research Org report from May 2025 revealed that 52% of United States adults prioritize the healthiness of food when making dietary choices[4]Source: Pew Research Org, "Americans on Healthy Food and Eating," pewresearch.org. Younger consumers are showing a strong preference for snacks that offer functional benefits, such as fiber-enriched chips and immunity-boosting bites. The growing focus on health is expected to encourage companies to develop snacks that offer added health benefits.

Innovation in flavors and gourmet premium products

In North America, brands are focusing on creating unique flavors and premium products to attract more consumers. Social media trends are driving interest in bold and adventurous tastes, such as Korean barbecue-seasoned nuts, yuzu-pepper kettle chips, and matcha-flavored popcorn. For example, in May 2025, Oreo introduced Chocolate-Covered Pretzel Oreos, combining pretzel-flavored wafers, chocolate creme, and a hint of salt to offer a new twist on a classic snack. This product reflects the growing demand for sweet and savory combinations that feel indulgent yet unique. Innovation in healthier options is also gaining momentum. In August 2025, Fruitist launched Blueberry Snack Cups, which are single-serve packs designed for convenience, making them ideal for lunchboxes or on-the-go lifestyles. These products cater to consumers looking for snacks that balance health, convenience, and premium quality. These examples demonstrate how brands are reshaping the market by focusing on creative flavors and engaging storytelling to meet evolving consumer preferences.

Growing focus on sustainability and ethical sourcing

Snack brands in North America are increasingly focusing on sustainability and ethical sourcing to align with consumer expectations and comply with evolving regulations. In 2023, 68% of United States consumers expressed a willingness to pay more for environmentally friendly products, emphasizing the growing importance of these initiatives. Companies like Kellanova have pledged to make all their packaging reusable, recyclable by 2030 as part of their Better Days Promise. Similarly, PepsiCo’s pep+ initiative aims to ensure that 97% of its packaging is recyclable by 2030. Brands are working to build consumer trust by supporting regenerative farming practices, which help improve soil health and reduce carbon emissions. Efforts to tackle food waste are also gaining momentum, with companies like Spudsy using imperfect sweet potatoes to create snacks. These sustainability measures position companies to better handle future regulations, such as extended producer responsibility fees, which could require businesses to take more accountability for the environmental impact of their products.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Concerns regarding the health impact of high salt and sugar levels | -0.4% | United States and Canada regulatory focus, Mexico emerging | Medium term (2-4 years) |

| Fierce price competition among private labels | -0.3% | North America-wide, intensifying during inflation | Short term (≤ 2 years) |

| Strict regulations regarding additives, labeling, and nutritional disclosures | -0.2% | United States Food and Drug Administration-driven, Canada following, Mexico developing | Long term (≥ 4 years) |

| Rising competition from fresh and unprocessed foods | -0.2% | Urban North America, health-conscious segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Concerns regarding the health impact of high salt and sugar levels

In North America, increasing concerns about sodium and sugar levels are creating challenges for the snack food market. The Food and Drug Administration introduced Phase II voluntary sodium-reduction targets in August 2024, aiming for a 20% reduction in sodium across packaged foods within 3 years. The Food and Drug Administration's (FDA) updated definition of “healthy,” which will take effect in February 2028, imposes strict limits on added sugars, sodium, and saturated fats for products making health claims. Salt and sugar play important roles in texture and shelf life, making it difficult and expensive to find natural alternatives. To address this, companies are gradually reducing sodium and sugar levels while introducing reformulated products. For example, in November 2023, PepsiCo announced a 15% sodium reduction in its Lay’s Classic Potato Chips, lowering sodium to about 140 mg per 28 g serving. These efforts show how manufacturers are trying to meet regulatory requirements and consumer expectations.

Strict regulations regarding additives, labeling, and nutritional disclosures

Rules around additives, labeling, and nutritional information are becoming a growing challenge for snack food manufacturers in North America. In April 2025, the FDA announced plans to phase out six synthetic food dyes, including Red No. 3, by the end of 2026. This change is forcing companies to search for natural alternatives that can maintain the same product appearance, flavor, and stability without losing consumer trust. At the same time, Canada’s upcoming front-of-pack labeling rules, set to take effect in January 2026, will require warnings on products with high levels of sodium, sugar, and saturated fat[5]Source: Government of Canada, "Nutrition labelling: Front-of-Package Nutrition Symbol," canada.ca. These regulations are increasing production and compliance costs for manufacturers while also potentially discouraging health-conscious consumers from buying certain products. To adapt, companies are reformulating their products to meet these new standards while trying to preserve the taste and quality that customers expect. This balancing act is making innovation more complex in the market, as brands work to stay competitive and compliant with evolving regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Frozen Snacks Drive Innovation

Savory snacks were the largest segment in the North America snack food market in 2025, making up 32.12% of the total market share. Their popularity comes from strong consumption habits, especially during sports events, movie nights, and social gatherings, where items like chips, popcorn, and pretzels are widely enjoyed. The variety of flavors, convenient packaging, and loyal customer base further strengthen their position in the market. Companies continue to depend on these products for large-scale sales but are under pressure to introduce new flavors and healthier options to keep consumers interested.

Frozen snacks are expected to grow the fastest, with a projected CAGR of 5.44% through 2031, which is more than double the overall market growth rate. This growth is driven by the demand for easy-to-prepare, ready-to-heat options that fit into busy lifestyles and different meal occasions. Meat snacks are also performing well, benefiting from their high-protein appeal and popularity among health-conscious and busy consumers. These trends are reshaping how manufacturers balance their product portfolios. While savory snacks remain a reliable source of revenue, companies are shifting their focus and investments toward faster-growing categories like frozen and protein-rich snacks.

By Category: Clean-Label Acceleration

In 2025, conventional snacks led the North America market, holding 87.92% of the total market share. These snacks are popular because they are affordable, easy to find, and cater to the everyday preferences of consumers. They are widely available through supermarkets, convenience stores, and discount retailers, supported by strong distribution networks. Consumers rely on these familiar products, making them a regular part of their shopping habits. Even during periods of rising costs, people often choose these budget-friendly options, ensuring their consistent demand in the market.

On the other hand, clean-label snacks are growing quickly, with an expected 5.03% CAGR through 2031, nearly double the growth rate of conventional snacks. This growth is driven by consumers wanting transparency, simple ingredients, and products without artificial additives or preservatives. Brands that highlight claims like organic, non-genetically modified organism, or minimally processed are becoming more popular, especially among younger buyers who value trust and quality. This trend also aligns with stricter regulations and calls for better labeling. As a result, clean-label snacks are gaining a premium position in the market, pushing manufacturers to focus more on innovation and marketing in this segment.

By Packaging Type: Digital Commerce Drives Innovation

Bags/pouches were the leading packaging type in the North America snack food market in 2025, accounting for 54.78% of total revenue. Their popularity stems from being cost-effective, lightweight, and easy to carry, making them a practical choice for consumers. Their design allows brands to use attractive graphics, which helps grab attention on store shelves. Features like resealable closures and portion-control sizes add convenience and help reduce food waste, appealing to busy consumers and families. These qualities make bags and pouches a preferred option for both everyday snacks and premium products, ensuring their strong presence across various retail channels.

Meanwhile, cans are expected to grow at the fastest rate, with a projected 4.32% CAGR through 2031. This packaging type is gaining traction, especially in online sales, due to its durability and premium appearance, which appeal to consumers looking for high-quality products. Cans also offer better protection for snacks and extend shelf life, making them ideal for items like seasoned nuts and gourmet popcorn. Their sturdy design reduces the risk of damage during shipping, which is a key advantage in e-commerce. With their combination of practicality and upscale appeal, cans are emerging as a strong alternative to traditional packaging, meeting the evolving preferences of modern consumers.

By Distribution Channel: E-commerce Transformation

Supermarkets/hypermarkets were the leading sales channels in the North America snack food market in 2025, contributing 46.62% of total revenue. These stores attract consumers by offering a wide variety of snacks, ranging from affordable options to premium brands, all in one location. Their strategic placement of snacks at checkout counters and frequent promotional offers encourage impulse buying. The convenience of weekly shopping trips and the trust consumers place in established retail chains make supermarkets and hypermarkets a preferred choice for snack purchases. Their ability to cater to diverse consumer needs ensures their continued dominance in the market.

Online retail is expected to grow at the fastest rate, with a projected 6.38% CAGR from 2026 to 2031. The convenience of home delivery, subscription services, and the ability to explore unique flavors and niche brands online are driving this growth. E-commerce platforms also use personalized recommendations and targeted promotions to engage consumers effectively. This makes online retail particularly appealing for premium and specialty snack brands, as well as direct-to-consumer offerings. While traditional retail remains essential for mass-market reach, the rapid expansion of online channels highlights a significant shift in consumer shopping behavior.

Geography Analysis

The United States leads the North America snack food market, contributing 81.35% of sales in 2025. High disposable incomes, widespread freezer ownership, and a strong snacking culture drive this dominance. The country also sets regulatory benchmarks, such as synthetic dye removal and front-of-pack nutrition labeling, which often influence neighboring markets. Major companies like PepsiCo utilize their scale and innovation capabilities, using insights from their Texas flavor center to develop cost-effective products across various snack categories. These factors make the United States a key player in shaping the region's snack food trends.

Mexico is the fastest-growing market in the region, with a projected CAGR of 5.72%. Urbanization and the adoption of Western eating habits are fueling this growth. Spicy snack flavors, such as chipotle-lime corn sticks, are particularly popular among younger consumers, blending traditional tastes with modern formats. The United States-Mexico-Canada Agreement (USMCA) trade agreement has simplified cross-border e-commerce, enabling United States brands to enter the Mexican market more easily. However, local companies like Monarca Authentic Snacks remain competitive, benefiting from integrated production facilities and a deep understanding of local preferences. Economic growth is also expanding the middle class, increasing demand for premium and clean-label snacks.

Canada's snack food market is more mature, with a focus on premium and eco-friendly products. Retailers are dedicating specific shelf spaces to better-for-you snacks, making it easier for consumers to find healthier options. There is growing interest in sustainable products, such as upcycled snacks made from byproducts like brewery grains. Distribution in Canada relies heavily on brokers who navigate bilingual labeling requirements and provincial regulations. Smaller North American markets serve as testing grounds for new flavors and innovations, contributing incremental growth to the overall regional market.

Competitive Landscape

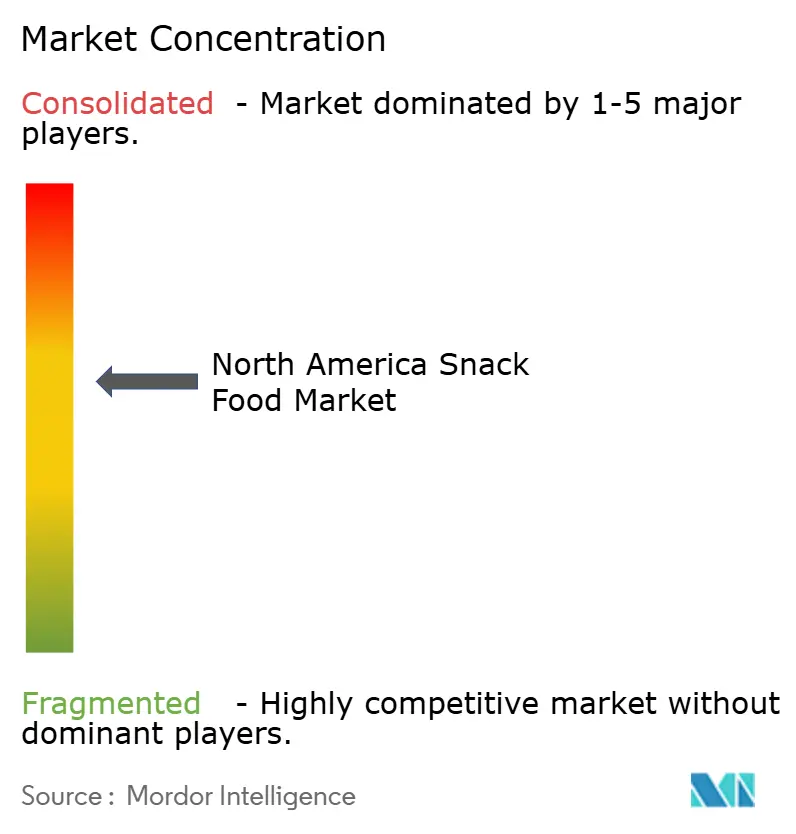

The North America snack food market is moderately consolidated and dominated by a few major players, with Mars, PepsiCo, Mondelez, Conagra Brands, and Hershey collectively accounting for about 60% of total sales in 2024. Mars expanded its portfolio by acquiring Kellanova’s snacking division for USD 35.9 billion, strengthening its presence in granola and plant-based snacks. Similarly, PepsiCo acquired Siete Foods for USD 1.2 billion, adding heritage-inspired tortilla chips to its Frito-Lay lineup to cater to health-conscious Hispanic consumers. These acquisitions highlight a trend where companies prefer to quickly fill gaps in their product offerings through strategic purchases rather than developing new products from scratch.

Smaller, emerging brands are making their mark by focusing on sustainability and health-focused products. For example, LesserEvil’s organic popcorn, made with coconut oil to reduce saturated fat, gained traction and was later acquired by Hershey, which provided the brand with broader distribution while maintaining its core values. Another example is UpSnack Brands, launched in January 2025, which combines heirloom corn-based snacks and sweet potato puffs, using digital marketing to grow its direct-to-consumer subscription model. Private equity investments are also driving growth, as mid-sized companies are being consolidated into larger, vertically integrated operations that share resources like logistics and marketing.

Technology is playing a significant role in shaping the strategies of snack food companies. Artificial intelligence is being used to predict consumer preferences, helping companies develop new flavors more quickly. Blockchain technology is being tested to track the origins of ingredients, such as peanuts, ensuring transparency and addressing concerns about allergies and sustainability. Automated packaging systems are enabling companies to produce limited-edition flavors efficiently, keeping consumers engaged with new offerings. Companies that effectively combine technological innovation with operational efficiency are better positioned to maintain their market share, while smaller players can still find opportunities by focusing on authenticity and unique product stories.

North America Snack Food Industry Leaders

-

PepsiCo Inc.

-

Mondelez International Inc.

-

Conagra Brands Inc.

-

Mars Inc.

-

The Hershey's Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hershey announced a definitive agreement to acquire LesserEvil, which expanded its portfolio with a healthier popcorn line. The acquisition provided Hershey with additional internal production capabilities.

- April 2025: Benestar Brands and Palmex Alimentos rebranded as Monarca Authentic Snacks. The company expanded its operations to include nine manufacturing plants across the United States and Mexico, with its products distributed in 17 countries.

- January 2025: UpSnack Brands acquired Pipcorn and Spudsy, integrating heirloom corn and upcycled sweet-potato technologies into their portfolio. This strategic move aimed to expand their sustainable snack offerings.

- January 2025: Snyder 's-Lance completed the acquisition of Snack Factory LLC for USD 340 million. This strategic move expanded Snyder 's-Lance's presence in the pretzel-based snack segment and strengthened its product portfolio.

North America Snack Food Market Report Scope

A snack is a small portion of food eaten between meals. Snacks come in a variety of forms and shapes, including packaged snack foods and other processed foods. The North American Snack food market is segmented by type, distribution channel, and by country. By type, the market studied is segmented into frozen snacks, savory snacks, fruit snacks, confectionery snacks, bakery snacks, and other types. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels, and by country into the United States, Canada, Mexico, and the Rest of North America. For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Frozen Snacks |

| Savory Snacks |

| Fruit Snacks |

| Confectionery Snacks |

| Bakery Snacks |

| Meat Snacks |

| Other Types |

By Category

| Conventional |

| Organic/Clean-Label |

By Packaging Type

| Bags/Pouches |

| Jars |

| Cans |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Frozen Snacks |

| Savory Snacks | |

| Fruit Snacks | |

| Confectionery Snacks | |

| Bakery Snacks | |

| Meat Snacks | |

| Other Types | |

| By Category | Conventional |

| Organic/Clean-Label | |

| By Packaging Type | Bags/Pouches |

| Jars | |

| Cans | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the current value of the North America snack food market?

The market is valued at USD 72.81 billion in 2026, with expansion expected through 2031.

Which product category is growing fastest?

Frozen snacks lead growth, forecasting a 5.44% CAGR as air-fryer adoption broadens usage occasions.

How large is online retail within North American snack sales?

Online channels hold a smaller share today but are projected to post a 6.38% CAGR, the quickest among all routes to market.

Which country offers the highest growth potential?

Mexico outpaces its neighbors with a forecast 5.72% CAGR, fueled by rising incomes and Western flavor adoption.

Page last updated on: