Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

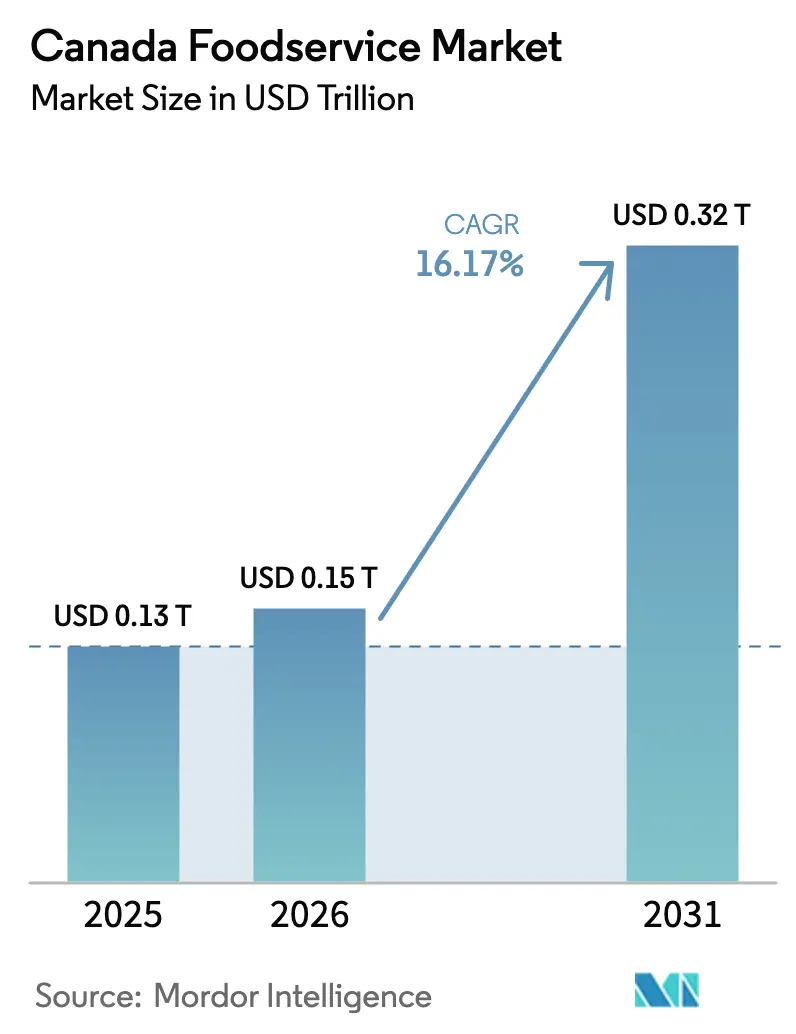

| Base Year Market Size (2025) | USD 0.13 Trillion |

| Market Size (2026) | USD 0.15 Trillion |

| Market Size (2031) | USD 0.32 Trillion |

| Growth Rate (2026 - 2031) | 16.17% CAGR |

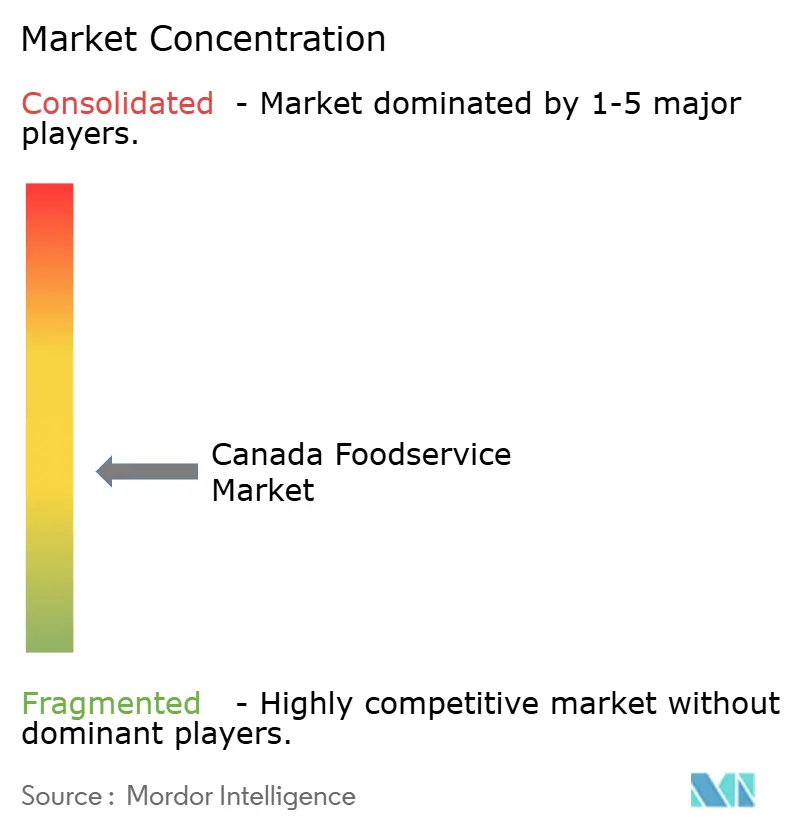

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Foodservice Market Analysis by Mordor Intelligence

The Canada foodservice market size was valued at USD 0.13 trillion in 2025 and estimated to grow from USD 0.15 trillion in 2026 to reach USD 0.32 trillion by 2031, at a CAGR of 16.17% during the forecast period (2026-2031). This acceleration reflects a structural shift in how Canadians consume meals outside the home, driven by the convergence of digital ordering infrastructure, delivery-only operating models, and a resurgence in socializing-driven dining after pandemic-era restrictions lifted. The sector recorded huge sales during 2024, supporting 1.2 million employees across chains and independent, according to Restaurants Canada[1]Source: Restaurants Canada, "We are the voice of foodservice in Canada", restaurantscanada.org. Quick Service Restaurants (QSRs) retained price-led traffic, yet the fastest momentum now sits with cloud kitchens, chained outlets, and takeaway channels, all of which leverage technology and unit-level economics to scale.

Key Report Takeaways

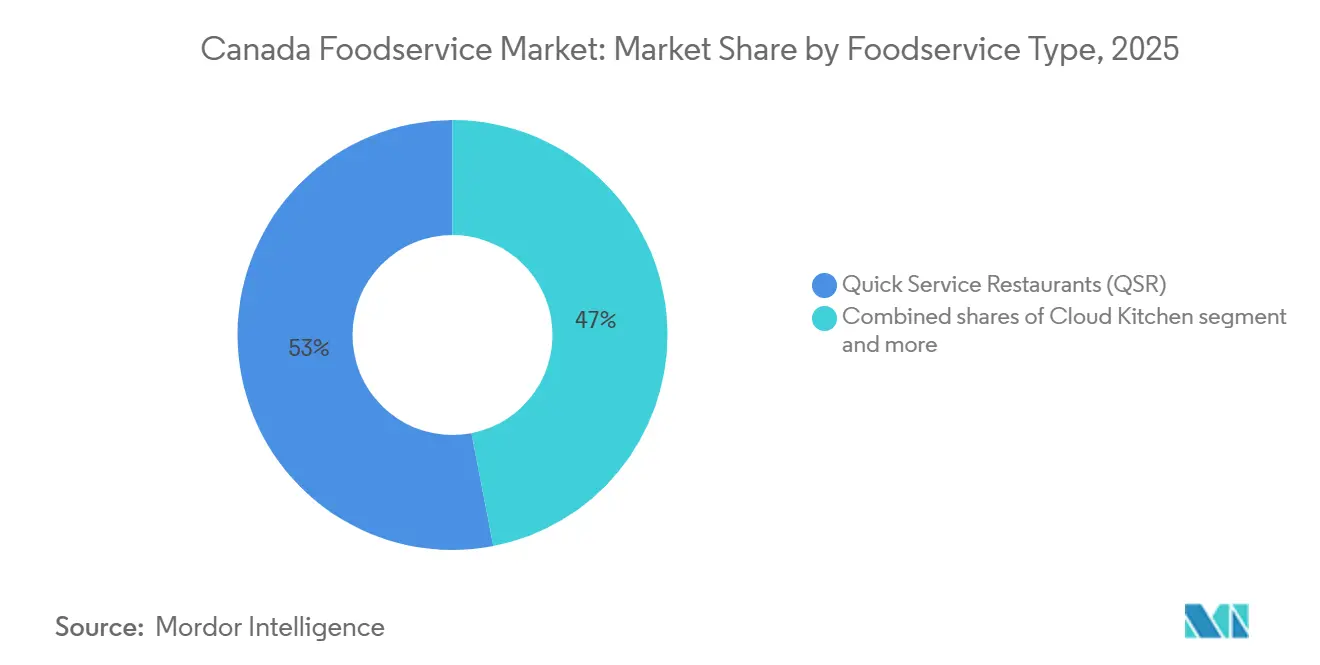

- By foodservice type, quick service restaurants held 53.04% of the foodservice market share in 2025; cloud kitchens are on track to post a 16.78% CAGR to 2031.

- By outlet, independents controlled 63.55% of the foodservice market size in 2025, while chained outlets are forecast to expand at a 16.82% CAGR through 2031.

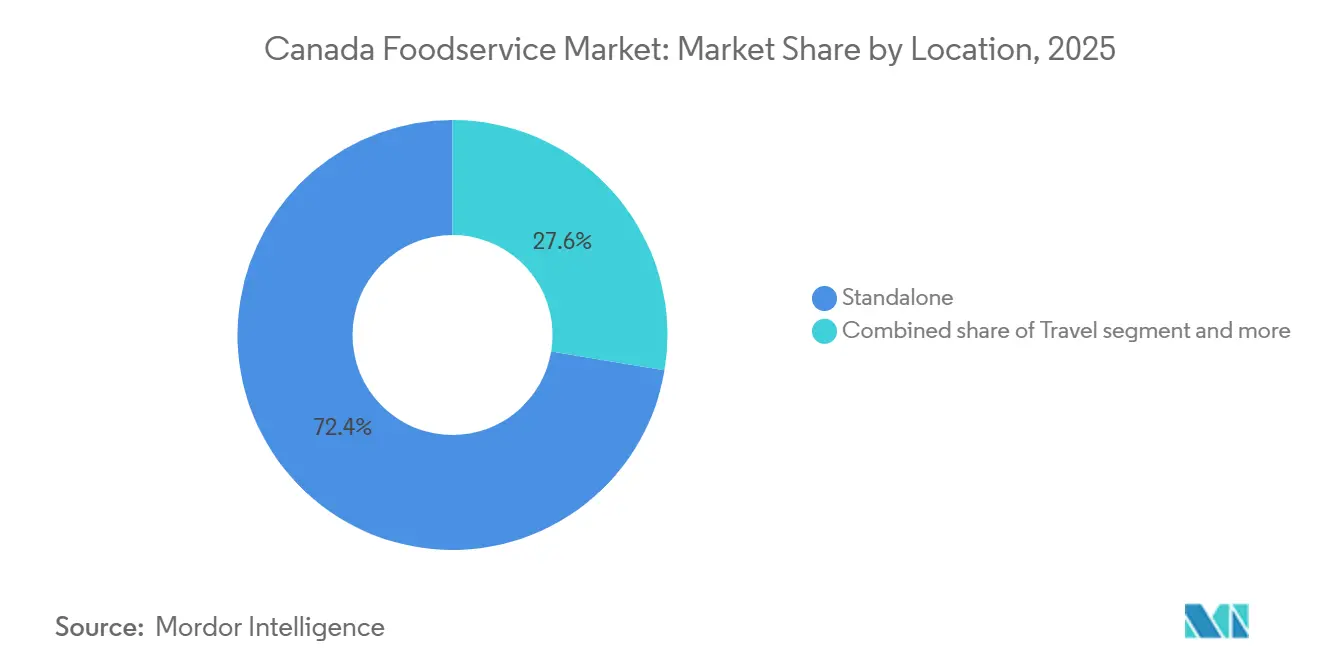

- By location, standalone sites captured 72.38% of the foodservice market size in 2025 and will maintain an 18.06% CAGR to 2031.

- By service type, dine-in claimed 55.84% of the foodservice market share in 2025; takeaway will accelerate at an 18.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acceleration of branded café formats and specialty coffee-chain rollout | +2.8% | National, concentrated in Ontario, British Columbia, Quebec | Medium term (2-4 years) |

| Progressive localization of menus by international operators | +2.3% | National, with stronger adoption in Quebec and multicultural urban centers | Medium term (2-4 years) |

| Entrenched dine-out habits supported by socializing-driven consumption | +3.1% | National, urban-centric in Toronto, Vancouver, Montreal | Short term (≤ 2 years) |

| Rapid scale-up of dark-kitchen and delivery-only operating models | +3.5% | National, early concentration in Toronto, Vancouver, Calgary | Short term (≤ 2 years) |

| Growing prominence of halal-compliant positioning in brand architecture | +1.9% | National, highest penetration in Greater Toronto Area, Greater Vancouver Area | Long term (≥ 4 years) |

| High penetration and fluency of mobile-app-based ordering behavior | +3.2% | National, led by Ontario and British Columbia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acceleration of Branded Café Formats and Specialty Coffee-Chain Rollout

Branded café operators are deploying capital into high-traffic corridors and suburban nodes, leveraging real-estate arbitrage as pandemic-era vacancies persist. Starbucks maintained over 1,400 stores across Canada, while Second Cup operated 190-plus locations, both investing in drive-through retrofits and mobile-order pickup lanes to compress transaction times. Tim Hortons, with approximately 4,000 domestic restaurants, expanded its beverage portfolio and introduced pizza in April 2024 to capture afternoon and evening occasions traditionally dominated by QSR pizza chains. This daypart extension signals a strategic pivot from breakfast-centric revenue toward all-day traffic, a move that compresses competitive moats for single-occasion specialists. Specialty-coffee consumption correlates with discretionary-income resilience, insulating café chains from cyclical downturns that pressure full-service formats. The rollout of loyalty apps and personalized promotions further entrenches repeat visits, creating switching costs that independent cafés struggle to replicate.

Progressive Localization of Menus by International Operators

International chains are embedding Canadian ingredients and regional flavor profiles into core menus to mitigate the perception of homogenization. McDonald's Canada sourced Canadian beef and introduced poutine and the seasonal McLobster in Maritime provinces, while A&W Canada partnered with Beyond Meat and emphasized Canadian beef provenance in marketing campaigns. Tim Hortons built brand equity around double-double coffee and Timbits, products that resonate with national identity and differentiate the chain from U.S.-based competitors. Localization extends beyond ingredients to packaging, portion sizes, and promotional calendars aligned with Canadian holidays and sporting events. This strategy reduces the risk of consumer backlash against perceived cultural insensitivity and allows chains to command premium pricing by framing offerings as locally relevant. Quebec operators face heightened expectations for French-language menus and culturally attuned service, creating compliance complexity that smaller entrants find difficult to navigate.

Entrenched Dine-Out Habits Supported by Socializing-Driven Consumption

Despite economic headwinds, socializing remains a primary motivator for restaurant visits, with 72% of DoorDash users in 2024 citing delivery as a form of self-care and 96% ordering to satisfy immediate cravings. Full-service restaurants are driven by group dining occasions and celebrations that independents and casual chains capture through experiential differentiation. The return of corporate gatherings, family milestones, and date-night routines post-pandemic reinforced dine-in demand, even as takeaway and delivery channels expanded. Operators invested in ambiance upgrades, live entertainment, and chef-driven menus to justify higher check averages and offset labor-cost inflation. This bifurcation, value-seeking QSR visits versus experience-seeking FSR occasions, shapes segmentation strategies and capital allocation, with chains targeting distinct consumer cohorts rather than competing across all dayparts.

Rapid Scale-Up of Dark-Kitchen and Delivery-Only Operating Models

Cloud kitchens eliminate front-of-house overhead, enabling operators to concentrate capital on kitchen throughput, delivery logistics, and digital marketing. DoorDash reported over 20 million active users in Canada by the third quarter of 2024, while Uber Eats contributed significantly to Uber's global gross bookings in the second quarter of 2024, underscoring the scale of third-party delivery infrastructure. Breakfast orders surged 45% year-over-year in 2024, and late-night transactions climbed 36%, evidence that delivery platforms are expanding addressable occasions beyond traditional lunch and dinner windows. Dark kitchens also permit rapid concept testing and menu iteration without the capital lock-in of physical storefronts, reducing time-to-market for new brands. However, reliance on aggregator platforms exposes operators to commission compression and algorithm changes that can abruptly alter order flow, creating strategic vulnerability for delivery-dependent models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened competitive pressure from independents and street-food operators | -1.8% | National, concentrated in Toronto, Vancouver, Montreal | Short term (≤ 2 years) |

| Variability in food-safety practices and hygiene compliance | -1.3% | National, provincial inspection disparities in Ontario, British Columbia, Alberta | Medium term (2-4 years) |

| Rapid imitation of concepts leading to differentiation fatigue | -1.1% | National, urban markets with high operator density | Medium term (2-4 years) |

| Reliability constraints in cold-chain and perishable logistics | -1.5% | National, acute in remote and northern regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Competitive Pressure from Independents and Street-Food Operators

Independent restaurants and street-food vendors captured consumer attention through hyper-local sourcing, chef-driven menus, and experiential storytelling that chains struggle to replicate at scale. Toronto, Vancouver, and Montreal witnessed the proliferation of food trucks, pop-ups, and market stalls offering ethnic cuisines and artisanal products, often at price points competitive with QSR value meals [2]Source: City of Toronto, "Ethnic Cuisines", toronto.ca. Independents leveraged social-media marketing and influencer partnerships to build brand equity without traditional advertising budgets, eroding the awareness advantages historically enjoyed by chains. Farm-to-table positioning and craft-beverage pairings resonated with consumers seeking authenticity, forcing chains to invest in menu premiumization and ingredient transparency to defend market share. The flexibility of independents, rapid menu pivots, localized promotions, and nimble cost structures contrasts with the bureaucratic inertia of franchised systems, creating asymmetric competitive dynamics.

Variability in Food-Safety Practices and Hygiene Compliance

The Canadian Food Inspection Agency enforces the Safe Food for Canadians Regulations, mandating licensing, preventive controls, and traceability for foodservice operators [3]Source: Government of Canada, "Canadian Food Inspection Agency", inspection.canada.ca/en. Provincial health authorities in Ontario, British Columbia, and Alberta administer inspection programs with differing frequencies, penalty structures, and public-disclosure requirements, introducing compliance complexity for multi-jurisdiction chains. Recalls for Listeria, Salmonella, and E. coli contamination periodically disrupt supply chains and erode consumer confidence, particularly when media coverage amplifies food-safety lapses. Smaller operators and independents often lack the resources to implement robust hazard-analysis protocols, creating public-health risks that regulatory bodies struggle to monitor comprehensively. Chains with centralized quality-assurance functions and third-party audits maintain compliance more consistently, yet reputational damage from a single incident can cascade across franchise networks, underscoring systemic vulnerability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Redefine Expansion Economics

Quick service restaurants held 53.04% of the market in 2025, underpinned by burger, pizza, and bakery formats that deliver speed and perceived value. McDonald's launched the Big Arch burger in August 2024, commercializing menu hacks that originated on social media, while Tim Hortons introduced pizza nationally in April 2024 to extend daypart coverage. Cloud kitchens, however, will expand at 16.78% CAGR through 2031, the fastest rate among all foodservice types, as operators eliminate front-of-house costs and concentrate capital on delivery radius and kitchen throughput. Full-service restaurants as well as cafes and bars grow more slowly, constrained by higher labor intensity and real-estate commitments that limit unit-level returns.

DoorDash recorded year-over-year growth in breakfast orders and 36% in late-night transactions during 2024, evidence that delivery platforms are unlocking demand outside traditional meal windows. Cloud kitchens capitalize on this shift by operating extended hours without incurring front-of-house staffing costs, compressing payback periods, and enabling rapid concept testing. Full-service chains are driven by ethnic-cuisine differentiation and experiential dining, while independents and casual formats captured demand. Café and bars benefited from specialty-coffee proliferation, with Starbucks maintaining over 1,400 stores and Second Cup operating 190-plus locations, both investing in drive-through retrofits and mobile-order pickup lanes.

By Outlet: Franchise Scalability Drives Chain Growth

Independent outlets commanded 63.55% of the market in 2025, reflecting the fragmented nature of Canada's foodservice landscape and the appeal of hyper-local concepts. Chained outlets, however, will grow at 16.82% CAGR through 2031, outpacing independents due to franchise scalability, brand recognition, and access to capital for technology investments. Tim Hortons operated approximately 4,000 restaurants in Canada, while Starbucks maintained over 1,400 stores, both leveraging centralized supply chains and marketing budgets that independents cannot match.

Franchise models reduce capital intensity for parent companies while transferring operational risk to franchisees, enabling rapid geographic expansion. Chick-fil-A entered British Columbia, Ontario, and Alberta, targeting suburban corridors with drive-through-heavy formats that align with post-pandemic consumer preferences. Independent operators retain the flexibility to pivot menus and pricing in response to local demand, yet lack the purchasing power and technology infrastructure that chains deploy to compress costs and enhance customer experience. The bifurcation between chains and independents will intensify as digital ordering, loyalty programs, and data analytics become table stakes, favoring operators with scale and technical sophistication.

By Locations: Standalone Sites Capture Convenience Premium

Standalone locations accounted for 72.38% of the market in 2025 and will sustain an 18.06% CAGR through 2031, the fastest growth rate among all location types. Standalone sites offer drive-through access, ample parking, and visibility from arterial roads, attributes that align with suburban migration and car-dependent consumption patterns. Retail, lodging, and travel-linked locations grow more slowly, constrained by foot-traffic volatility and lease structures that limit operational flexibility.

Operators prioritize standalone sites for new builds, particularly in suburban and exurban markets where land costs remain manageable, and zoning permits drive-through configurations. Tim Hortons and McDonald's concentrated expansion in standalone formats, leveraging drive-through lanes to capture morning commuter traffic and evening takeaway orders. Retail locations within shopping malls faced headwinds as foot traffic declined, prompting chains to renegotiate leases or exit underperforming sites. Lodging and travel locations, airports, hotels, and highway rest stops recovered from pandemic lows but remain vulnerable to tourism fluctuations and business-travel reductions. The shift toward standalone sites reflects a broader preference for convenience and speed over experiential or impulse-driven dining.

By Service Type: Takeaway Gains from Convenience Prioritization

Dine-in service captured 55.84% of the market in 2025, sustained by socializing-driven consumption and experiential dining occasions that delivery cannot replicate. Takeaway, however, will grow at 18.75% CAGR through 2031, the fastest rate among service types, as consumers prioritize convenience and time savings over in-restaurant experiences. Delivery grew in tandem, supported by DoorDash's 20 million-plus active users in Canada and Uber Eats contributing a major share of Uber's global gross bookings.

Takeaway orders generate higher margins than delivery due to the absence of third-party commissions, prompting operators to invest in dedicated pickup lanes and mobile-order lockers. McDonald's and Starbucks prioritized drive-through and curbside pickup infrastructure, reducing transaction times and capturing incremental volume from time-pressed consumers. Dine-in service remains critical for full-service restaurants, where ambiance, table service, and beverage pairings justify premium pricing. Yet labor shortages and wage inflation compress dine-in margins, incentivizing operators to shift mix toward takeaway and delivery channels that require fewer front-of-house staff. The service-type bifurcation reflects a structural shift in consumer behavior, with convenience increasingly valued over experiential dining.

Competitive Landscape

Canada's foodservice sector exhibits moderate concentration, reflecting a fragmented landscape where regional specialists and independent operators coexist with multinational chains. Franchise models dominate expansion strategies, enabling parent companies to scale without capital intensity while transferring operational risk to franchisees. Tim Hortons, McDonald's, and Starbucks leverage centralized supply chains, national marketing budgets, and technology platforms that independents cannot replicate, yet hyper-local concepts and street-food vendors capture consumer attention through chef-driven menus and experiential storytelling.

Chains respond by accelerating product-development cycles, launching limited-time offers, and embedding loyalty programs into mobile apps to create switching costs. Technology adoption intensified: 77% of operators increased investments in 2024, prioritizing point-of-sale upgrades, kitchen automation, and data analytics. White-space opportunities persist in suburban corridors, underserved ethnic cuisines, and delivery-optimized formats that eliminate front-of-house overhead.

Restaurant Brands International invested up to USD 45 million in Tim Hortons China and Popeyes China, signaling confidence in international expansion even as domestic competition intensifies. Starbucks partnered with Too Good To Go across more than 2,600 Canadian locations, reducing food waste and appealing to sustainability-conscious consumers. Emerging disruptors include ghost-kitchen aggregators and virtual brands that test concepts rapidly without physical storefronts, compressing time-to-market and capital requirements. The competitive landscape will bifurcate further, with scale-advantaged chains consolidating share in high-traffic corridors while independents defend niche positions through differentiation and community engagement.

Canada Foodservice Industry Leaders

-

Doctor's Associates, Inc.

-

Inspire Brands Inc.

-

McDonald's Corporation

-

RECIPE Unlimited Corporation

-

Yum! Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Heal Wellness also signed a new franchise agreement for Bradford, Ontario, reinforcing its asset-light, franchise-driven expansion strategy across Canada.

- October 2025: Happy Belly Food Group’s healthy QSR brand Heal Wellness signed its first real estate location in Montreal, Quebec, planning a Q1 2026 opening, extending its footprint into a key provincial market.

- April 2024: U.S. Italian QSR Fazoli’s entered the Canadian market with a franchise development agreement to open 25 restaurants across Canada over the next decade, targeting Alberta first with openings expected in 2025 as part of its first international expansion.

Canada Foodservice Market Report Scope

Foodservice refers to the business of preparing, serving, and selling ready-to-eat food and drinks for immediate consumption, encompassing diverse establishments like restaurants, cafes, catering, and institutions, focusing on providing meals outside the home for profit or service. The Canada foodservice market is segmented by foodservice type, outlet, service type, and location. By foodservice type, the market is segmented into cafes and bars, cloud kitchen, full-service restaurants, quick service restaurants and more. By outlet, the market is segmented into chained outlets and independent outlets. By location, the market is segmented into leisure, lodging, retail, standalone, and more. By service type, the market is segmented into takeaway, delivery and more. The market forecasts are provided in terms of value (USD).

By Foodservice Type

| Café and Bars | By Cuisine | Bars and Pubs |

| Café | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

By Outlet

| Chained Outlets |

| Independent Outlets |

By Locations

| Leisure |

| Lodging |

| Retail |

| Sandalone |

| Travel |

By Service Type

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Café and Bars | By Cuisine | Bars and Pubs |

| Café | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Sandalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms