Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

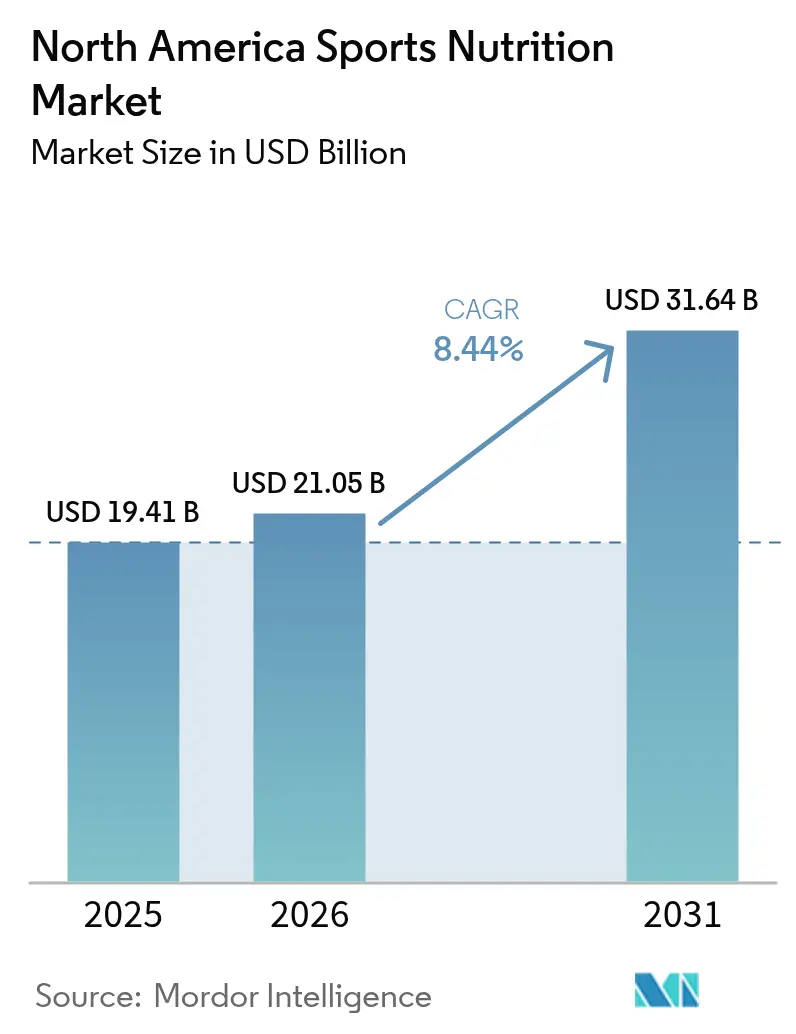

| Base Year Market Size (2025) | USD 19.41 Billion |

| Market Size (2026) | USD 21.05 Billion |

| Market Size (2031) | USD 31.64 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Sports Nutrition Market Analysis by Mordor Intelligence

North America sports nutrition market size in 2026 is estimated at USD 21.05 billion, growing from 2025 value of USD 19.41 billion with 2031 projections showing USD 31.64 billion, growing at 8.44% CAGR over 2026-2031. The increasing demand stems from athletes, weight-management individuals, and everyday consumers who now view protein, creatine, and amino acids as essential wellness staples rather than niche performance products. Additionally, a new consumer segment has emerged, driven by users of GLP-1 weight-loss drugs, who prioritize high-protein formulas with balanced leucine profiles to support lean-mass preservation. Convenience is influencing product preferences, with ready-to-drink shakes, gels, and functional beverages gaining popularity over traditional powder tubs to meet the needs of mobile consumers seeking immediate consumption. Retail consolidation is accelerating, fueled by Amazon's 2024 requirement for third-party testing certificates. This initiative has removed numerous unverified listings and shifted sales toward certified brands. Moreover, major beverage companies are expanding into bars and powders, leveraging their established distribution networks to introduce these new SKUs to mainstream retail shelves.

Key Report Takeaways

- By product type, sports protein products accounted for 83.25% of the sports nutrition market share in 2025, whereas sports non-protein products are advancing at a 9.02% CAGR through 2031.

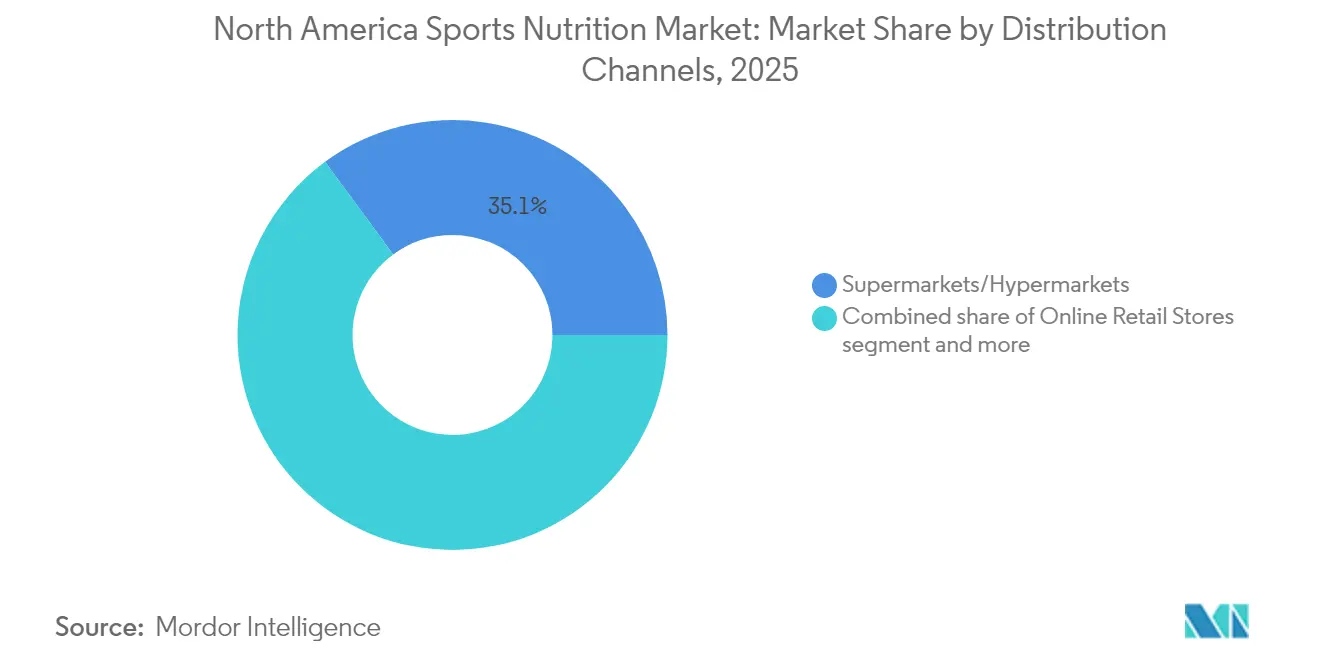

- By distribution channel, supermarkets and hypermarkets held 35.10% of revenue in 2025, while online retail is forecast to grow at a 9.88% CAGR through 2031.

- By geography, the United States captured 84.10% of 2025 revenue, whereas Mexico will post the fastest expansion at a 9.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Sports Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising supplement usage among fitness enthusiasts and athletes | +1.8% | North America, with concentration in US urban metros and Canadian university towns | Medium term (2-4 years) |

| Surge in demand for protein-rich products due to awareness of muscle recovery benefits | +2.1% | United States and spillover to Mexico's youth demographic | Short term (≤ 2 years) |

| Growing health-club and endurance-sport participation | +1.5% | US and Canada, with emerging gains in Mexico's northern states | Medium term (2-4 years) |

| Integration of technology for personalized nutrition recommendations | +1.2% | North America, concentrated among tech-forward consumers in coastal US markets | Long term (≥ 4 years) |

| Female-focused strength training fueling niche SKUs | +0.9% | US and Canada, with urban centers leading adoption | Medium term (2-4 years) |

| Surge in plant-based performance ingredients | +1.3% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising supplement usage among fitness enthusiasts and athletes

Heightened health awareness, the growing popularity of fitness and sports, and the pervasive influence of social media have collectively fueled a surge in supplement usage. This trend, in turn, has become a primary catalyst for the burgeoning sports nutrition market, as consumers increasingly seek products that boost performance and facilitate recovery. In 2024, fitness center and health club memberships in the U.S. totaled 77 million, according to the Health and Fitness Association [1]Source: Health and Fitness Association, "Memberships at U.S. fitness facilities", healthandfitness.org. This growth is primarily driven by budget-friendly club formats such as Planet Fitness, Crunch, and various regional chains, which are attracting first-time exercisers. These newcomers are introduced to supplements through in-club sampling and influencer endorsements. Subscription models significantly contribute to this shift by offering monthly deliveries at a 15% to 20% discount, turning one-time trial purchases into consistent revenue streams. Additionally, the rising popularity of endurance sports, including marathons, triathlons, and cycling events, has increased demand for intra-workout gels and electrolyte formulations, extending beyond the traditional gym demographic. In response, brands are segmenting their products into pre-, intra-, and post-workout categories, each designed with distinct macronutrient profiles and pricing strategies to maximize consumer basket size.

Surge in demand for protein-rich products due to awareness of muscle recovery benefits

Patients using GLP-1 receptor agonists, semaglutide and tirzepatide, are experiencing a 15% to 20% reduction in body weight, with nearly 40% of that loss attributed to lean mass, highlighting the critical role of protein intake. This has driven formulators to develop "muscle-preservation" SKUs featuring elevated leucine content and added collagen peptides. These products are now attracting consumers who previously avoided sports nutrition due to its association with bodybuilding. While whey and casein powders continue to lead the market, plant-based isolates such as pea, rice, and hemp are gaining popularity. This trend is fueled by consumers who perceive dairy proteins as inflammatory or follow vegan diets for ethical reasons. Creatine monohydrate, once primarily used by strength athletes, is now marketed for its cognitive benefits and potential to prevent sarcopenia, thereby broadening its market appeal. Furthermore, the growing adoption of veganism and rising disposable incomes among North American consumers are driving increased spending on plant-based protein products. For instance, in 2024, plant-based protein expenditures in Mexico totaled MXN 10.63 billion, according to the National Institute of Statistics and Geography (INEGI)[2]Source: National Institute of Statistics and Geography (INEGI), "Encuesta Nacional de Ingresos y Gastos de los Hogares", inegi.org.mx.

Growing health-club and endurance-sport participation

Health-club penetration in the U.S. is growing, with budget operators expanding into secondary markets and corporate wellness programs subsidizing memberships. Registrations for endurance sports, such as marathons, triathlons, and obstacle-course races, are increasing, especially among female participants. In 2024, the Bureau of Labor Statistics noted that 19.4% of the female population in the U.S. participated in sports, exercise, and recreation daily [3]Source: Bureau of Labor Statistics, "American Time Use Survey", bls.gov. This trend is noteworthy, as women are more likely to follow structured nutrition protocols and prefer premium-priced products emphasizing clean labels and third-party testing. Boutique fitness studios, including those focused on cycling, rowing, and HIIT, are incorporating supplement sales into their revenue streams. By offering branded protein shakes and energy gels at checkout, they capitalize on the heightened purchase intent immediately after workouts. Additionally, the rise of hybrid training, which combines strength and endurance, has diversified product requirements. Athletes now demand both fast-digesting carbohydrates for glycogen replenishment and slow-release proteins for overnight recovery. This growing complexity in needs gives multi-SKU brands a competitive edge over single-product specialists.

Integration of technology for personalized nutrition recommendations

AI-powered platforms are transforming the supplement industry. These platforms utilize data from continuous glucose monitors, sleep trackers, and training apps to create personalized supplement protocols, turning standard powders into customized nutrition services. For example, Mixfit's algorithm dynamically adjusts protein dosages using real-time muscle-protein synthesis markers from wearable accelerometers. This level of precision allows Mixfit to charge a 40% premium compared to traditional static formulations. By adopting a digital-first approach, brands bypass traditional retail gatekeepers, enabling direct-to-consumer expansion without incurring slotting fees or relying on trade promotions. Additionally, the integration of telehealth consultations with supplement delivery is establishing seamless ecosystems. In these models, dietitians prescribe specific products, and brands fulfill these orders within 48 hours. This strategy enhances customer retention and reduces churn rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening FDA/CFIA claim-substantiation rules | -0.8% | North America, with enforcement concentrated in US and Canada | Short term (≤ 2 years) |

| Consumer skepticism toward supplement efficacy and safety concerns | -1.1% | North America | Medium term (2-4 years) |

| Adulteration and mislabeling issue undermining customer trust | -0.7% | North America, particularly affecting online and discount channels | Medium term (2-4 years) |

| Heavy-metal and stimulant contamination incidents | -0.9% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening FDA/CFIA claim-substantiation rules

In 2024, the FDA sent multiple warning letters to sports nutrition brands for making unapproved structure-function claims. These claims, such as products that "build muscle" or "burn fat," lacked the clinical trials required for drug approval. Consequently, brands had to reformulate products and update labels, causing delays in product launches and higher compliance costs. Similarly, Health Canada's 2024 supplemented foods framework introduced new regulations, including adverse-event reporting and ingredient-limit schedules, which align closely with pharmaceutical oversight. This regulatory shift favors multinational formulators with dedicated regulatory teams, placing regional contract manufacturers at a disadvantage. Furthermore, the FDA revised its New Dietary Ingredient (NDI) notification process, requiring a 75-day pre-market review for novel ingredients. This change creates challenges for first movers while enabling fast followers to launch similar formulations without incurring research and development expenses. Lastly, the CFIA implemented stricter claim-substantiation rules, requiring any health benefit stated on packaging to be supported by peer-reviewed human trials. This standard eliminates the use of vague terms like "supports" and "promotes," which were previously used to imply efficacy without legal accountability.

Consumer skepticism toward supplement efficacy and safety concerns

Third-party testing by NSF International and Informed Choice is now a critical requirement for retail partnerships. However, less than 40% of SKUs hold these certifications, creating a trust deficit that online platforms are addressing through mandatory documentation. In 2024, Amazon introduced a policy requiring sellers to upload certificates of analysis for sports nutrition products. This policy raised the entry barrier for unverified brands, resulting in a 22% decline in active ASINs within the category and increasing the market share of compliant manufacturers. The detection of DMAA, a stimulant banned by the FDA, in pre-workout powders tested in 2024 highlights ongoing supply-chain issues. Contract manufacturers in Asia continue to source ingredients from non-audited suppliers to cut costs. To address consumer skepticism, brands are enhancing transparency by publishing batch-level test results on their websites and adding QR codes on labels that link to real-time certificates of analysis. This approach, while commanding a 15% to 20% price premium, has led to higher repurchase rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Dominates, Non-Protein Accelerates

Sports protein products accounted for 83.25% of the market revenue in 2025, highlighting a well-established consumer perception that links protein supplementation to muscle recovery and improved performance. At the same time, sports non-protein products, such as energy gels, BCAA powders, and creatine, are projected to grow at a strong 9.02% CAGR through 2031. This growth represents the fastest rate among product categories, fueled by athletes increasingly adopting periodized nutrition strategies. These strategies involve incorporating multiple supplements throughout training cycles, moving beyond exclusive reliance on protein powders. Among sports protein products, whey and casein powders continue to dominate as the largest sub-segment. Their leadership is attributed to decades of clinical validation and cost advantages over plant-based alternatives. However, plant-based protein powders are steadily gaining market share as flexitarian diets become more popular, and formulators improve taste profiles using natural flavoring systems. Additionally, ready-to-drink protein beverages are replacing powders in convenience-focused locations, such as gas stations, airports, and vending machines, where consumers prioritize immediate availability over cost per serving. This shift has driven investments in aseptic packaging and shelf-stable formulations.

Protein and energy bars, while part of a mature sub-segment, are experiencing only modest single-digit growth. This limited growth is primarily due to saturation in grocery and mass-merchandise channels, which restricts distribution opportunities, along with increased competition from private labels that compress margins. Conversely, sports non-protein products are benefiting from the growing acceptance of creatine monohydrate. In 2024, creatine monohydrate achieved an impressive 60% year-over-year sales increase on Amazon, driven by influencers promoting its cognitive and strength benefits, which have expanded its appeal beyond the traditional bodybuilding audience. Meanwhile, BCAA powders are losing market share to essential amino acid (EAA) blends. These blends provide all nine essential amino acids, compared to the three found in branched-chain variants. This formulation improvement appeals to consumers, who perceive EAAs as a more complete option, even though clinical differences are minimal. Lastly, energy gels and chews, while primarily used by endurance athletes, represent a smaller segment. However, this segment offers higher lifetime value due to consistent year-round consumption and a willingness to pay premium prices for scientifically validated carbohydrate-to-electrolyte ratios.

By Distribution Channel: Online Retail Outpaces Brick-and-Mortar

Supermarkets and hypermarkets, including Walmart, Kroger, and Costco, accounted for 35.10% of the distribution share in 2025. These retailers effectively use private-label SKUs to attract price-sensitive consumers while cross-selling sports nutrition products alongside grocery essentials. Online retail, led by Amazon's dominance in sports nutrition, is projected to grow at a CAGR of 9.88% through 2031, making it the fastest-growing distribution channel. Pharmacies and health stores, such as GNC, The Vitamin Shoppe, and independent retailers, are recovering from previous declines by focusing on in-store consultations and offering third-party-tested SKUs, which set them apart from generic online products. Other channels, including gyms, direct sales, and corporate wellness programs, form a fragmented but profitable segment. These channels allow brands to bypass retail intermediaries and secure full-price sales through exclusive partnerships.

iHerb is expanding its North American presence through strategic partnerships with The Vitamin Shoppe in July 2024 and Albertsons in January 2025. These collaborations enable same-day delivery in urban areas, positioning iHerb as a competitor to Amazon's dominance in sports nutrition. Direct-to-consumer brands like Transparent Labs, Legion Athletics, and Kaged Muscle are bypassing traditional retail by investing in performance-marketing campaigns that drive traffic to their own websites. In response, brick-and-mortar retailers are adopting augmented-reality tools that let shoppers scan product labels to access information on ingredient sourcing, clinical studies, and user reviews. This digital integration helps bridge the information gap between online and in-store shopping experiences.

Geography Analysis

In 2025, the U.S. leads North America's sports nutrition revenue, contributing 84.10%. This dominance stems from a deep-rooted cultural association between protein supplementation and athletic performance, which originated during the bodybuilding boom of the 1980s. At the same time, the FDA has intensified its regulatory stance, issuing several warning letters in 2024. These letters address unapproved structure-function claims and the inclusion of DMAA in pre-workout products. Such regulatory measures favor established brands with robust compliance teams over regional contract manufacturers. Furthermore, the rise of GLP-1 medications is driving dual demand for protein supplements. Weight-loss patients aim to preserve lean mass, while traditional athletes seek performance improvements. This trend is broadening the market's scope, extending beyond its traditional focus on males aged 18 to 35.

Mexico is projected to achieve the fastest growth in the region, with a CAGR of 9.72% through 2031. This growth is primarily fueled by a population facing high rates of overweight and obesity, which is increasing demand for both weight management and performance supplements. Pharmacies dominate distribution channels, followed by direct sales. This distribution mix underscores the influence of multi-level marketing leaders like Herbalife and Omnilife, which have a strong presence in rural and peri-urban areas where retail infrastructure is limited. Rising participation in football and baseball is boosting demand for sports drinks and energy gels. Additionally, urban gyms in cities such as Mexico City, Monterrey, and Guadalajara are incorporating protein-shake bars into their business models to capture post-workout purchases when consumer intent is at its peak.

Canada's sports nutrition market is stabilizing following a period of regulatory tightening. Health Canada's 2024 supplemented foods framework has introduced requirements such as adverse-event reporting and ingredient-limit schedules, aligning with pharmaceutical-grade oversight. This regulatory shift benefits multinational formulators with established compliance systems over regional contract manufacturers. In Canada, boys and young men are increasingly using whey protein, with half also consuming creatine. These usage rates reflect the normalization of supplementation in youth athletic programs, despite ongoing debates about its long-term safety. Meanwhile, the rest of North America, particularly Central American markets, remains in an early stage of development. These regions face challenges such as limited retail infrastructure and a reliance on cross-border e-commerce, primarily from U.S. and Mexican fulfillment centers.

Regulatory Landscape

Sports nutrition in North America spans both dietary supplement and conventional food regimes, which makes labeling and claim substantiation central compliance priorities. In the United States, sports powders, RTDs, and bars marketed as supplements must align with FDA dietary supplement expectations for labeling and permissible structure-function claims, alongside the FDA Food Labeling Guide and related nutrition labeling guidance. Separately, the FDA set a Uniform Compliance Date window for food labeling regulations through December 31, 2026, reinforcing the need for manufacturers selling food-positioned SKUs (for example, RTD protein beverages and bars) to track labeling rule updates on a common timeline.

Canada adds distinct packaging and labeling requirements that affect cross-border portfolios. As of January 1, 2026, foods sold in Canada must fully comply with Front-of-Package (FOP) nutrition symbol labeling following the end of the transition period on December 31, 2025, with CFIA enforcement carried out through its Standard Inspection Process and without enforcement discretion after the effective date. For brands supplying both the US and Canada, this increases the value of harmonized label architectures, bilingual packaging workflows, and tighter documentation for nutrient thresholds and on-pack benefit statements, which can reduce relabeling cycles and border friction.

Competitive Landscape

The North American sports nutrition market is characterized by fragmentation. Major players command an estimated 35% to 40% of the market's revenue. The remaining share is widely distributed among regional brands, private labels, and direct-to-consumer startups. These entities often compete based on niche positioning rather than scale. Leveraging their extensive beverage distribution networks, PepsiCo and The Coca-Cola Company successfully place their products, Gatorade and BodyArmor, in both convenience and mass-merchandise channels. This structural advantage is one that smaller protein-powder brands find challenging to replicate without incurring significant trade-promotion expenses. Dominating the performance-nutrition segment, Glanbia boasts a manufacturing scale that not only ensures cost leadership but also allows them to absorb regulatory compliance costs. Meanwhile, Abbott leads in the clinical-nutrition segment. Nestlé's recent acquisition of Garden of Life has bolstered its plant-based portfolio, facilitating cross-promotions with mainstream brands. This strategy aims to attract flexitarian consumers who switch between whey and vegan proteins.

There's a burgeoning opportunity in personalized nutrition. Brands are harnessing AI-driven platforms that analyze wearable data, crafting tailored supplement protocols. This shift is elevating standard powders into precision-nutrition services, commanding a notable 40% price premium. Key players in the North American sports nutrition landscape, including PepsiCo Inc., Glanbia PLC, Mondelēz International Inc., The Coca-Cola Company, and Abbott Nutrition Inc., are actively launching new products to cater to diverse consumer demands. Additionally, many are bolstering their offerings through strategic mergers and acquisitions.

Disruptors like Transparent Labs, Legion Athletics, and Kaged Muscle are sidestepping traditional retail. Instead, they're channeling investments into performance-marketing campaigns, driving traffic directly to their websites. Technology's role is expanding, evident in brands embedding QR codes on product labels. These codes link consumers to real-time certificates of analysis and batch-level test results, a transparency move that boosts repurchase rates. The merging of telehealth consultations with supplement fulfillment is birthing integrated ecosystems. In these setups, dietitians not only prescribe specific SKUs but also ensure brands fulfill orders within a swift 48-hour window. This approach not only secures customer loyalty but also minimizes churn.

North America Sports Nutrition Industry Leaders

-

PepsiCo Inc.

-

Mondelēz International, Inc.

-

The Coca-Cola Company

-

Abbott Nutrition Inc

-

Glanbia Plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Format and occasion expansion is creating whitespace beyond traditional tubs and bodybuilding-led positioning, particularly in hydration-plus-protein and coffee-adjacent protein beverages. PepsiCo Beverages North America launched Propel Clear Protein as a ready-to-mix powder positioned around hydration functionality (electrolytes plus protein) and distributed through major online retailers, while Muscle Milk completed a reformulation based on ultra-filtered milk and adopted a clean-label style removal of artificial sweeteners, flavors, and added colors. Danone also extended Oikos Protein Shakes with flavors tied to the protein-coffee "profee" use case, indicating that sports nutrition brands are competing for broader daily consumption moments where taste, convenience, and mainstream retail placement matter as much as gym performance cues.

Regulatory and compliance infrastructure is increasingly used to accelerate innovation and widen listings, especially as scrutiny continues over novel ingredients and claim language. The FDA Office of Dietary Supplement Programs held a March 2026 public meeting on the scope of dietary supplement ingredients, reflecting active regulatory attention on new production methods and the pathway for peptides, proteins, and enzymes. With retailer-led documentation requirements already reshaping online assortments, the environment supports opportunities for certified, transparently tested portfolios (for example, QR-linked batch documentation and third-party testing) and for manufacturers that can run parallel US-Canada label systems, including meeting Canada FOP requirements for food-positioned sports nutrition SKUs sold nationally from January 2026.

Recent Industry Developments

- May 2026: PepsiCo launched Propel Clear Protein, a ready-to-mix powder that combines whey protein with fiber and electrolytes and rolled it out through major online retailers including Walmart.com, Amazon, and Gatorade.com. The update extends sports nutrition into functional hydration and draws on PepsiCo's scale in digital retail to accelerate distribution for a new format.

- May 2026: Muscle Milk completed a full product line reformulation, shifting to ultra-filtered milk-based formulas and removing artificial sweeteners, flavors, and added colors while maintaining high protein per serving. The changes target clean-label preferences in RTD protein beverages and support broader placement in mainstream channels that scrutinize ingredient decks.

- February 2024: The Coca-Cola Company closed its acquisition of the remaining stake in BODYARMOR, bringing full ownership of the sports drink brand under Coca-Cola. Full control strengthens Coca-Cola's ability to align innovation, distribution, and marketing across Powerade and BODYARMOR in performance hydration and sports-adjacent nutrition occasions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as retail and online sales of sports nutrition products across North America that are purchased for performance, recovery, hydration, and workout support, and then consumed as powders, ready-to-drink formats, bars, or functional non-protein products.

Scope exclusions: Excludes ordinary packaged foods and beverages that are not positioned and purchased as sports nutrition, along with any medical nutrition prescribed for clinical use.

Segmentation Overview

-

By Product Type

-

Sports Protein Products

-

Powder

- Whey and Casein Powder

- Plant based Protein Powder

- Other Sports Protein Powder

- Protein Ready to Drink

- Protein/Energy Bars

-

Powder

-

Sports Non Protein Products

- Energy Gels

- BCAA Powder

- Creatine Powder

- Other Sports Non Protein Products

-

Sports Protein Products

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Pharmacy/Health Stores

- Online Retail Stores

- Other Distribution Channels

-

By Country

- United States

- Canada

- Mexico

- Rest of the North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building a fact base on consumption context, labeling rules, and cross-border trade that shapes category availability and pricing. For regulatory and labeling inputs, we refer to sources such as the US FDA labeling and supplement guidance, USDA food category references, Statistics Canada tables, Mexico INEGI statistics, and UN Comtrade trade flows, to understand how products move across borders and how categories are recorded publicly.

Alongside this, company annual reports, investor presentations, press releases, and retailer and association websites are reviewed to map format mix changes and claims-led innovation. To support the model inputs, we also use paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment-level import and export records where available. These sources help us set practical guardrails for volumes, pricing bands, and channel shifts before assumptions are stress-tested through interviews. The desk research source list is not exhaustive, and we used other public references as cross-checks and for clarification.

Primary Interviews and Surveys

Primary work is used to confirm what is really being counted as sports nutrition in-store and online, and how price ladders behave across powders, RTD products, bars, and functional non-protein items. We speak with manufacturers, brand managers, ingredient and packaging partners, distributors, specialty retailers, and gym and wellness channel participants. Interviews and survey inputs include perspectives across APAC, EMEA, and the Americas so the assumptions reflect differences in demand patterns and channel execution.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 18% | |

| Mid tier: 43% | Functional/Unit leaders: 36% | |

| Smaller Players: 22% | Managers: 46% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where category demand pools are reconstructed using North America consumption signals and retail availability, and then filtered by sports nutrition positioning and purchase intent. Once that structure is set, we corroborate totals with selective bottom-up approximations such as sampled average selling price (ASP) by format multiplied by estimated unit volumes, plus channel checks to avoid overcounting overlap between online and physical retail.

Key model inputs include format mix (powder, RTD, bars, and functional non-protein items), channel mix (mass retail, specialty, pharmacy and health stores, and e-commerce), observed ASP bands by pack size, promo intensity and premiumization, and participation indicators tied to gym usage and fitness adoption. When country data is patchy in smaller channels, gaps are handled by applying conservative penetration ranges that are then adjusted after interview feedback confirms what is realistic for that geography.

Forecasts are produced using scenario analysis supported by short time-series smoothing on key variables like ASP progression and e-commerce share, and then reviewed with expert consensus on what is likely to change in the next cycle (new product claims, ingredient trends, and distribution expansion).

Data Validation & Update Cycle

Validation is done through triangulation across independent checks so the final number is not reliant on one data stream. We compare outputs with trade and category signals, price movements, and channel expansion indicators, and then we run variance checks at country and format level to spot unusual jumps that need explanation.

Before sign-off, the model and assumptions go through multi-step analyst review, and experts are re-contacted when the implied pricing or growth rate sits outside the range seen in the market. The report is refreshed annually, and interim updates are added when material events occur such as major regulatory actions, sharp inflation shifts, or channel disruptions. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's North America Sports Nutrition Market Size Compared Against Other Published Estimates

Published market sizes for North America sports nutrition often do not match because firms group products differently, choose different base years, and apply different pricing logic for fast-moving formats. The differences get bigger when one estimate blends in adjacent categories like mainstream sports drinks, or when online pricing is treated as a simple average without promo and pack-size effects.

Some external figures appear to include broader sports beverage or general wellness supplement spend, which can lift totals quickly. In Mordor Intelligence, the count is limited to sports protein products and sports non-protein products sold in North America, and ASP progression is checked by format so powders, RTD items, and bars are not pushed by one blended price trend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.41 B (2025) | |

| Industry Publisher A | USD 20.33 B (2024) | Uses a different base year and appears to use a wider product basket that may fold sports drinks and broader wellness supplement spend into the sports nutrition total, which can raise the 2024 value versus a tighter format-defined count. |

| Industry Analyst B | USD 12.88 B (2023) | Anchors the model to 2023 and may understate e-commerce and specialty channel sales, and it can also apply conservative pricing steps that do not fully reflect premiumization in powders and RTD products. |

The spread across the three values mainly comes from product basket choices, base year timing, and how price and channel mix are treated. By keeping the inputs tied to observable format and channel signals, and then validating assumptions through repeatable checks, our estimate stays easier to trace and update year after year.

Key Questions Answered in the Report

Which product category currently leads in revenue share?

Sports protein products account for 83.25% of 2025 revenue.

What is the projected value of the North America sports nutrition market by 2031?

The market is forecast to reach USD 31.64 billion by 2031, growing at an 8.44% CAGR.

Why are online channels expected to outpace brick-and-mortar?

Mandatory third-party testing on Amazon, influencer discovery, and rapid subscription delivery give online outlets a 9.88% CAGR advantage through 2031.

How are GLP-1 weight-loss drugs influencing supplement demand?

Patients on GLP-1 medications increase protein intake to preserve lean muscle, boosting sales of high-leucine powders and ready-to-drink shakes.

Page last updated on: