Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

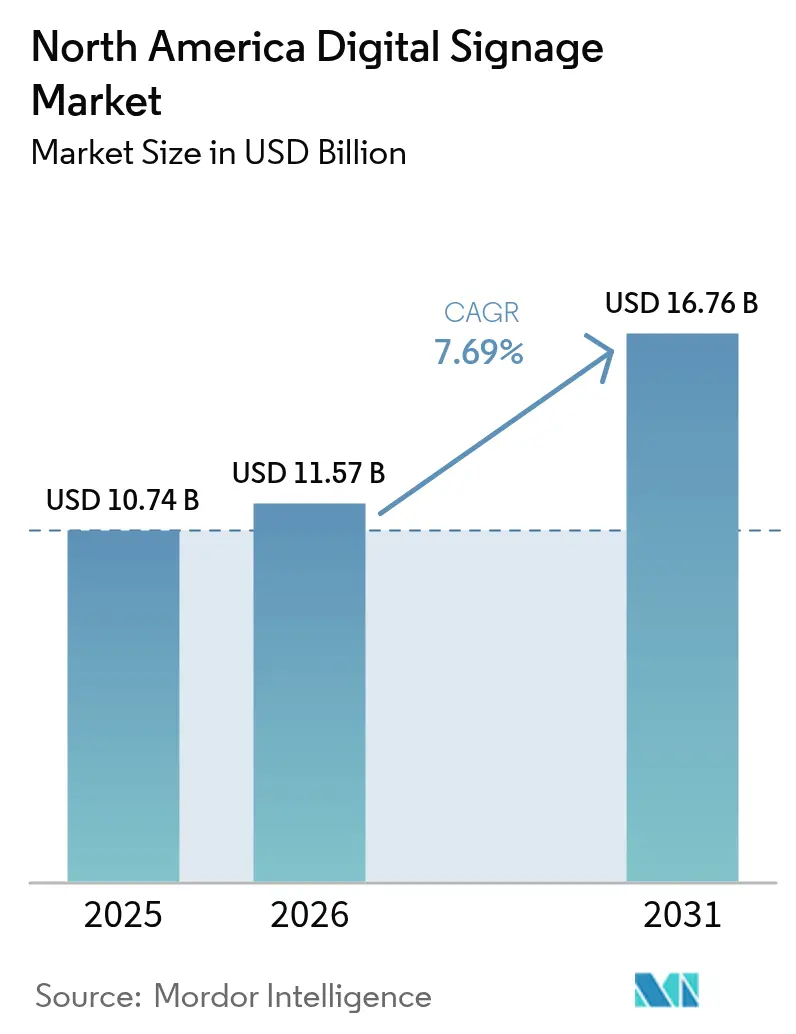

| Base Year Market Size (2025) | USD 10.74 Billion |

| Market Size (2026) | USD 11.57 Billion |

| Market Size (2031) | USD 16.76 Billion |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Digital Signage Market Analysis by Mordor Intelligence

The North America digital signage market size was valued at USD 10.74 billion in 2025 and estimated to grow from USD 11.57 billion in 2026 to reach USD 16.76 billion by 2031, at a CAGR of 7.69% during the forecast period (2026-2031). Growth comes from retailers, transportation hubs, and corporate campuses that now treat screens as data-rich tools for customer engagement rather than passive billboards. Hardware still anchors most projects, yet cloud software and analytics subscriptions are expanding margins for vendors and easing roll-outs for end-users.[1]Hughes, “Frost Radar: Digital Signage Solutions 2025,” hughes.comInteractive formats, transparent LED façades, and programmatic buying are reshaping return-on-investment calculations, while declining LCD panel costs and bundled “hardware-plus-software” offers are pulling small businesses into the upgrade cycle. Tariff shifts, energy-efficiency rules, and localized manufacturing are redrawing supplier maps, but sustained capital spending by multi-site brands keeps the demand curve intact.[2]Natural Resources Canada, “Digital Signage,” nrcan.gc.ca

Key Report Takeaways

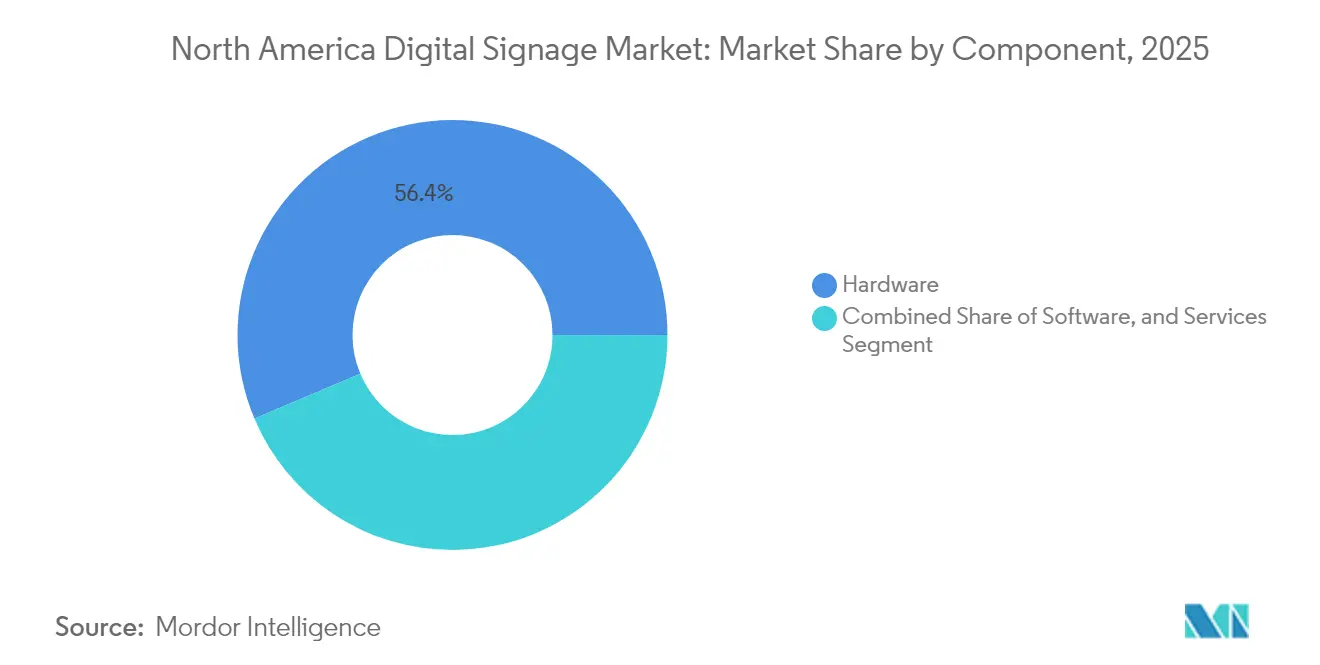

- By component, hardware commanded 56.35% of the North America digital signage market size in 2025, while software is projected to grow at an 8.73% CAGR between 2026-2031.

- By location, indoor screens led with a 67.65% revenue share in 2025; the outdoor segment is projected to advance at a 9.08% CAGR through 2031.

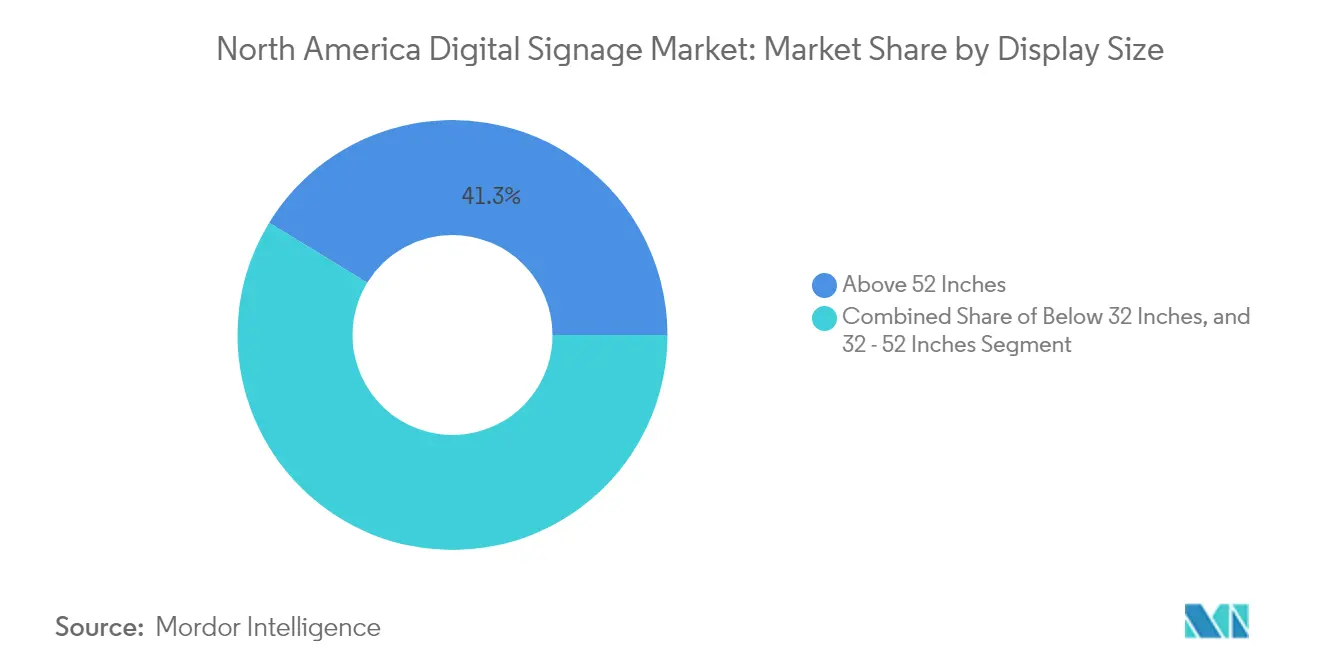

- By display size, above-52-inch formats captured 41.25% of the 2025 North America digital signage market share and are expected to expand at an 8.31% CAGR during the outlook period.

- By installation location, in-store deployments accounted for 68.80% of revenues in 2025; roadside networks are expected to grow at 8.09% CAGR.

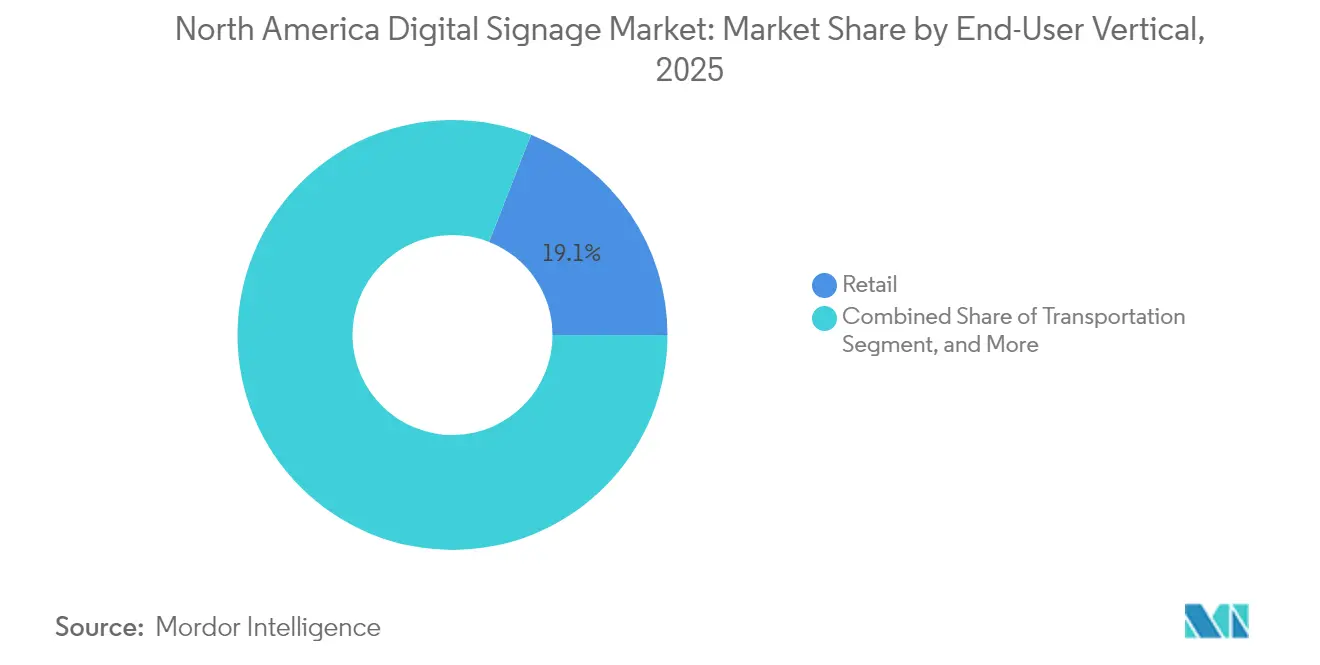

- By end-user, retail held 19.05% of the North America digital signage market size in 2025, whereas transportation records the highest forecast CAGR at 10.48% through 2031.

- By hardware type, LCD and conventional LED kept 46.25% share in the 2025 North America digital signage market share, however,transparent LED are expected to expand at an 11.05% CAGR during the outlook period.

- By country, the United States held 80.25% revenue share in 2025, while Mexico is on track for a 7.82% CAGR thanks to smart-city projects and retail chain expansion.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Digital Signage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolution of turnkey solutions across U.S. retail chains | +1.2% | United States, Canada spillover | Medium term (2-4 years) |

| Context-aware advertising using mobile data | +0.9% | Canada, major U.S. metros | Medium term (2-4 years) |

| 4K/8K video walls in U.S. airports | +0.8% | United States hubs | Short term (≤ 2 years) |

| Smart-city outdoor roll-outs in Mexico | +0.7% | Mexico’s largest cities | Long term (≥ 4 years) |

| LCD price decline benefiting SMBs | +1.1% | Secondary markets across region | Short term (≤ 2 years) |

| Programmatic DOOH platforms | +1.3% | Urban North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Evolution of Turnkey Solutions Accelerating Deployment Across U.S. Retail Chains

Bundled offerings that combine screens, media players, software, content templates, and remote monitoring have reduced national rollouts by 37% since 2023. Retail groups now standardize experiences across hundreds of stores while tailoring promotions to local inventory levels and conditions. Subscription pricing, rather than capital outlay, encourages the adoption of digital signage among 60% of enterprises that intend to subscribe within two years. Chains adopting this model report 22% higher engagement and an 18% increase in average basket value, confirming the pivot from a cost center to a revenue driver.

Context-Aware Advertising Leveraging Mobile Data Enhances ROI for Canadian Advertisers

Anonymized cellphone signals now feed real-time audience estimates into content schedulers. Canadian pilots show ROI gains of 41% over traditional out-of-home buying, plus 27% higher engagement and 19% conversion lifts in retail settings. Geofencing lets brands retarget exposed passers-by on their phones, knitting together physical impressions and digital follow-ups without storing personal identifiers.

Integration of 4K/8K Video Walls Powers Experiential Venues in Major U.S. Airports

Airports have installed ultra-high-definition canvases that double as art, way-finding, emergency alerts and premium ad slots that fetch 3.8× standard rates. A 10,000-square-foot installation in Dallas Fort Worth incorporates gesture tracking, lifting audience dwell time by 72%. Such dual-use systems justify higher capex through both operational utility and advertising yield.

Smart-City Initiatives Driving Outdoor Digital Signage Roll-outs in Mexican Urban Centers

Mexico City, Monterrey and Guadalajara are wiring weather-proof LED kiosks with environmental sensors, SOS alerts and municipal news feeds. Solar power and battery storage offset grid constraints, trimming operating costs by 31% while attracting private ad partners. A 2025 smart-city accord in Sonora is expected to accelerate similar networks nationwide.[3]FESPA, “Sustainable Solutions in Digital Signage,” fespa.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy Concerns Regarding Location-Based Targeting and Facial Analytics | -0.7% | Canada and United States, particularly in urban centers | Medium term (2-4 years) |

| Rising Energy-Efficiency Regulations for Large-Format Displays | -0.5% | North America, with strongest impact in California and Canada | Long term (≥ 4 years) |

| Supply-Chain Volatility for High-Brightness LED Components | -0.8% | Global, with significant impact on North American pricing | Short term (≤ 2 years) |

| Capex Barriers for Independent QSRs in Rural Areas | -0.4% | Rural regions across North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Privacy Concerns Regarding Location-Based Targeting and Facial Analytics

State-level U.S. bills and Canada’s Digital Charter are tightening consent rules, forcing vendors to shift from face recognition to anonymous demographic counts. Surveys indicate 68% of Canadian youth oppose facial analysis in commerce, prompting retailers to weigh reputational risk against personalization benefits.

Rising Energy-Efficiency Regulations for Large-Format Displays

ENERGY STAR rules require displays to improve power performance by 4%, adding component costs yet accelerating innovation such as ambient-light sensors and scheduled dimming. Manufacturers answer with e-paper menu boards and zero-power standby modes while balancing brightness demands for sunlit venues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Driving Recurring Revenue Models

Hardware captured 56.35% of the North America digital signage market share in 2025, anchored by capital-intensive screens and media players. Despite this lead, the software slice is advancing at an 8.73% CAGR as cloud dashboards, AI scheduling engines, and audience analytics shift buyer focus from one-time installs to lifetime value. Subscription bundles now comprise 43% of platform revenue, aligning vendor incentives with continuous content optimisation. Hardware makers are increasingly pre-loading licenses and managed services, creating a seamless procurement process and freeing retailers from the need to juggle multiple suppliers.

The services tier-covering planning, cabling, calibration, on-site maintenance, and creative design-expands steadily because end-users lack in-house bandwidth to refresh campaigns across sprawling estates. Integrators that manage networks end-to-end win multi-year contracts, locking in predictable annuities while keeping failure rates below service-level thresholds. Edge-AI features embedded in modern media players reduce bandwidth costs and enable localised decisions-such as muting audio during quiet hours or flagging malfunctioning LEDs for proactive repairs.

By Location: Outdoor Innovations Driving Above-Average Growth

Indoor venues held 67.65% of North America digital signage market size in 2025, buoyed by climate-controlled conditions and existing power/data infrastructure. Corporate headquarters, colleges and mall walkways rely on indoor screens for visitor orientation, promotional upsells and employee notices. In response to content fatigue, operators layer touch, gesture or QR interactions, merging in-person and mobile experiences into a single engagement funnel.

Outdoor networks, representing 32.35% of revenue but outpacing overall growth at 9.08% CAGR, benefit from durable casings, auto-dimming and self-cleaning glass treatments. Smart-city pilots add public Wi-Fi, environmental sensors and emergency alerts to justify municipal budgets, while solar-powered totems bring dynamic information to energy-constrained locales. The evolution of remote-diagnostic software slashes truck-roll expenses and lengthens uptime SLAs.

By Display Size: Above 52 Inches Capturing Premium Advertising Inventory

Screens above 52 inches held 41.25% share of the North America digital signage market size in 2025 and keep expanding because high-resolution panels now support near-field viewing. Airport concourses and entertainment arenas rely on tiled video walls to anchor experiential zones. Below-32-inch displays dominate shipment volume thanks to menu boards, shelf-edge tags and elevator screens where distance and physical constraints limit size. Templates emphasise concise copy and bold pricing, reinforcing impulse decisions. The 32-52-inch band balances footprint and readability, becoming the default in QSR order points, office reception areas and healthcare triage stations.

Panels exceeding 52 inches command the lion’s share of high-impact media spend despite lower unit counts. Brands convert complete walls into immersive canvases at stadiums, museums and airport concourses, pairing 4K or 8K resolution with dynamic soundscapes. As pixel density rises, these giants can be viewed at close quarters without grain, unlocking installations in boutiques and corporate atriums previously reserved for printed banners.

By Installation Location: In-Store Deployments Driving Measurable Sales Lift

Retailers report up to 33% sales uplift for items showcased on end-cap displays that rotate creative based on daypart or inventory levels. Centralised control ensures brand consistency across hundreds of branches while preserving flexibility to push local deals. Integrating stock APIs avoids consumer frustration by hiding out-of-stock SKUs and spotlighting overstocked lines.

Roadside and out-of-store units are expected to grow at 8.09% CAGR as programmatic targeting maximizes dwell-time relevance. Roadside billboards, transit shelters and fuel-station canopies are migrating to LED formats that host multiple advertisers through programmatic scheduling. Brightness sensors, redundant power supplies and rugged ratings trim downtime and safeguard safety codes. Linking mobile retargeting to exposure data provides marketers proof of incremental store visits, a metric previously elusive in out-of-home media.

By End-User Vertical: Transportation Sector Leads Growth Through Passenger Experience Enhancement

Retail retained 19.05% of North America digital signage market share in 2025, with loyalty integrations and hyper-local promotions sharpening competitive edges against e-commerce rivals. AI engines match offers to demographic heat-maps, while computer-vision modules verify planogram compliance and dwell time.

Transportation, with a forecast 10.48% CAGR, enhances journey flow through live gate updates, baggage carousel cues and entertainment loops that monetise layover time. Inside taxis and ride-share vehicles, tablets deliver surge-priced offers tied to passenger demography and trip length. Airports retrofit ageing flight-information displays with modular LED ribbons that flex between operational alerts and ad-supported lifestyle content.

By Hardware Type: Transparent LED Displays Redefining Installation Possibilities

LCD and conventional LED kept a 46.25% share in 2025, anchoring mainstream projects thanks to cost efficiency and mature supply chains. Transparent LED displays provide over 80% light transmission, enabling retailers to animate storefront windows without obstructing sightlines and driving double-digit increases in foot traffic. Their dominance secures bulk-procurement economies and simplified spares inventory. Transparent LED sheets, however, are rewriting architectural norms with over 80% light transmission, allowing retailers to animate shop windows without blocking sight-lines. Forecasting a 11.05% CAGR positions the format as the fastest-growing segment of the North America digital signage market, particularly in luxury retail, automotive showrooms, and experiential pop-ups.

OLED enters premium arenas where near-infinite contrast ratios and off-axis clarity justify higher ticket prices. Narrow pixel-pitch LEDs fill control rooms and broadcast sets that view screens at arm’s length, while ruggedised projectors still serve irregular façades and temporary events. Media players graduate from passive playback boxes to miniature edge servers capable of on-device analytics, buffering against connectivity outages, and preserving playback integrity.

Geography Analysis

The United States generated 80.25% of 2025 spending in the North America digital signage market. Robust retail footprints, major transit hubs, and enterprise campuses underpin sustained demand. Recent tariffs encourage local assembly, giving U.S. manufacturers price leverage while prompting foreign vendors to localize production. Energy-compliant hardware and cloud-managed software are penetrating corporate communication workflows, enlarging non-advertising opportunities.

Canada held roughly 12.55% of regional revenue. Advertisers there lead in context-aware campaigns that analyze anonymous mobile signals, achieving ROI lifts that outpace traditional OOH formats. National privacy and energy mandates shape both data usage and hardware specifications, with ENERGY STAR displays posting 4% efficiency gains over baseline models. Market consolidation is under way as domestic operators exit or merge, and ePaper pilots signal a push toward sustainable indoor signage.

Mexico, at 7.20%, is the fastest-growing slice of the North America digital signage market. Urban smart-city frameworks blend public information, emergency alerts, and ad funding in unified kiosks. Foxconn’s Sonora smart-city memorandum illustrates rising foreign investment in civic-tech infrastructure. Knowledge gaps among small merchants persist, yet falling hardware prices and mobile-payment tie-ins continue to expand addressable demand across retail, hospitality, and entertainment venues.

Regulatory Landscape

North American digital signage deployments sit at the intersection of electrical-safety, radio-interference, accessibility, and energy-efficiency requirements, which affect product certification, installation design, and content governance. In the United States, commercial displays and media players used in signage must meet FCC Part 15 electromagnetic-interference requirements, and federal deployments also face accessibility obligations under Section 508. This typically pushes buyers toward WCAG-aligned content and user-interface practices for interactive signage and wayfinding.

Standards and compliance timelines are also tightening for manufacturers and integrators. UL Solutions published UL 48 (Edition 15) for Electric Signs in May 2025, with an effective date of May 14, 2027, requiring product lifecycle planning for re-testing and documentation. In Canada, Accessibility Standards Canada adopted EN 301 549 as a National Standard of Canada (CAN/ASC-EN 301 549:2024) in December 2024, which raises the bar for accessible digital technologies across public-sector and regulated environments. These requirements add pressure alongside energy programs such as ENERGY STAR display specifications that encourage power-performance improvements for large-format signage.

Value Chain Analysis

The North America digital signage value chain typically starts with core components (LCD/LED/OLED panels, LED modules, controllers, power supplies, housings, and compute such as media players/SoCs), then moves through display OEMs, CMS and analytics software providers, and finally to Pro AV integrators. Integrators handle site surveys, network design, mounting, cabling, commissioning, and ongoing managed services. Distributors remain pivotal in bridging OEM supply to integrators and end users, particularly for LED video walls and specialty form factors used in retail, transportation, and venue deployments.

Recent channel moves show the chain being optimized for availability and support. Exertis Almo became the exclusive North American distributor for select Planar Leyard LED video wall series in November 2024, and Electro-Matic Visual partnered with Unilumin USA as a master distributor in October 2025. These changes strengthen localized warehousing, technical support, and partner enablement for integrators. Up the stack, platforms are converging around full-service workflows, including Exertis Almo introducing its Autora Digital Signage Management platform for integration partners (March 2025). Software consolidation is also continuing, with vendors acquiring customers and unifying CMS ecosystems to reduce fragmentation across mixed hardware fleets.

Competitive Landscape

North America digital signage market competition features a blend of diversified electronics giants, cloud-native software houses and specialty integrators. Samsung Electronics, LG Display and SHARP NEC share roughly 43% of revenue, leveraging in-house panels, media players and CMS suites that streamline procurement. Their roadmaps emphasize transparent LED, sub-1-millimeter pixel pitch and energy-optimized power rails.

Independent software vendors such as BrightSign, Poppulo and SignageOS differentiate through hardware-agnostic orchestration, advanced analytics and AI content policing that flags off-brand or outdated messaging automatically. Telecom equipment stalwarts incorporate digital signage modules into broader unified-communications portfolios, blurring lines between boardroom screens and marketing displays.

Tariffs on imported LED sub-components, energy-use caps in California and Ontario, and semiconductor supply disruptions are driving near-shoring and multi-sourcing strategies. Hardware margins compress, so vendors bundle managed services, predictive maintenance and data analytics dashboards to preserve profitability. Partnerships with cloud hyperscalers shorten time-to-market for enterprise buyers seeking elastic capacity and global uptime guarantees.

North America Digital Signage Industry Leaders

Sharp NEC Display Solutions, Ltd.

Samsung Electronics Co. Ltd

LG Display Co. Ltd

Panasonic Corporation

Sony Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Retail media networks and programmatic DOOH are creating whitespace for vendors that can deliver full-stack capabilities (inventory management, measurement, and automated operations) rather than standalone screens. A clear indicator of this shift is Perion Network Ltd. being selected as an end-to-end technology partner for Best Buy Canada’s 308-store in-store retail media network (June 2026). The selection increases the emphasis on software, ad decisioning, and analytics in what were historically hardware-led projects. It also expands opportunities for integrators and OEMs that can package repeatable, multi-site deployments with remote monitoring and SLA-backed services for chains rolling out standardized in-store formats.

Compliance-driven upgrades also support near-term replacement and retrofit demand, particularly where accessibility and energy rules intersect with interactive wayfinding and high-brightness outdoor signage. Canada’s adoption of CAN/ASC-EN 301 549:2024 and federal Section 508 obligations in the United States encourage buyers to refresh user interfaces, content templates, and interactive workflows to meet WCAG-aligned requirements. At the same time, ENERGY STAR display specifications and state energy codes (including California Title 24 requirements tied to automated dimming in applicable permanent installations) increase the value of sensors, scheduling, and power-optimized display designs. On the vendor side, platform convergence and embedded compute reduce deployment friction, reflected in hardware-software integration initiatives such as BrightSignOS-class SoC approaches built directly into large-format displays, which helps multi-site operators simplify procurement and operations across mixed estates.

Recent Industry Developments

- June 2026: LG Electronics USA introduced five new Direct View LED (DVLED) display solutions at InfoComm 2026, including additions to the LG MAGNIT lineup. The update broadened its premium LED portfolio for large-format, mission-critical signage and supported integrators looking for standardized DVLED families across multiple site types.

- September 2025: Samsung Electronics expanded its digital signage partnership with Toyota Motor, supporting the deployment of 23,000 smart signage displays in dealerships across Europe, the Middle East, and the CIS. The rollout size reinforced dealership networks as a repeatable, multi-site use case for centrally managed commercial displays and content operations.

- June 2024: Samsung Electronics announced a partnership with Vu Technologies focused on AI-powered digital signage solutions for retail advertising. The collaboration highlighted data-driven content delivery and automation, aligning signage deployments more closely with performance marketing and retail media workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues generated from digital signage deployments across North America, where commercial grade displays and related equipment are used to show dynamic content in public or business settings.

Scope exclusions: We exclude consumer TVs used at home and software-only content platforms that are not tied to a digital signage display deployment.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Location

- Indoor

- Outdoor

- By Display Size

- Below 32 Inches

- 32 - 52 Inches

- Above 52 Inches

- By Installation Location

- In-Store

- Out-of-Store/Roadside

- By End-user Vertical

- Retail

- Transportation

- Hospitality

- Corporate

- Education

- Healthcare

- Government

- Sports and Entertainment Venues

- Other End-user Verticals

- By Hardware Type

- LCD/LED Display

- OLED Display

- Media Players

- Projectors/Projection Screens

- Transparent LED Displays

- Other Hardware Types

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand and supply picture for digital signage across the United States, Canada, and Mexico, and then to cross-check adoption patterns by end location. We mainly reviewed public materials such as US Census construction and business activity series, US Bureau of Labor Statistics employment and wage data that informs installation capacity, and USITC and Statistics Canada trade data for display-related imports.

To keep the model grounded, we also referred to sources such as FCC device authorization databases for shipment direction checks, peer-reviewed journals and conference proceedings on display technology and lifecycles, and association and venue operator websites that indicate rollout intensity by retail, transit, and hospitality locations. Company filings, investor presentations, and reputable press were used to sanity-check pricing movement, replacement cycles, and the pace of network expansion, and we supplemented this with our own paid subscriptions for company financials, patent lookups, and shipment-level trade intelligence where available. These examples are not exhaustive, and many other public and paid sources were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what was learned from desk research and to fill gaps that are not visible in public data, especially around project size, refresh cycles, and pricing practices for indoor versus outdoor deployments. We spoke with a mix of display OEM ecosystem participants, integration and installation channels, and buyer-side teams across retail, transportation, corporate, education, healthcare, and hospitality in North America, and then used these inputs to triangulate adoption rates and average revenue per deployment.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 17% | |

| Mid tier: 51% | Functional/Unit leaders: 27% | |

| Smaller Players: 20% | Managers: 56% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool build that reconstructs where screens are installed and refreshed, and then links that footprint to average deployment value by use location. To keep the math repeatable, we relied on practical inputs such as estimated screen counts by venue type, typical replacement cycles for commercial displays, the mix of indoor versus outdoor high-brightness units, and observed pricing spreads by format (video walls, kiosks, menu boards, and single screens).

Once the initial total was formed, it was corroborated with selective bottom-up checks, such as sampled average selling price times expected unit volumes, channel feedback on annual project flow, and supplier roll-ups from public financial disclosures where available. If a bottom-up proxy was incomplete for a country or vertical, the gap was handled by applying validated penetration and refresh assumptions from similar venue types, and then re-tested in follow-up calls.

For forecasting, we used scenario analysis supported by expert inputs, since spending is sensitive to macro conditions and to the timing of retail remodels, transportation upgrades, and large venue expansions. Variables tracked include new store openings and refurbishments, transit and airport modernization activity, digital out-of-home ad spend direction, component price trends for LED and LCD, and the share shift toward larger-format and higher-brightness installations.

Data Validation & Update Cycle

Outputs are checked against multiple independent signals, and then reviewed for unusual jumps that do not align with expected deployment and replacement behavior. When variances show up, the underlying drivers are re-checked, assumptions are stress-tested, and targeted re-contact is triggered with respondents who can explain what changed in pricing, project timing, or mix.

Before sign-off, the model and key assumptions go through a multi-step internal review so calculation logic, units, and currency handling are consistent across the North America scope. The report is refreshed annually, and interim updates are made when material events occur, after which a final pre-delivery pass is completed so the numbers reflect the latest available view.

Mordor Intelligence's North America Digital Signage Market Size Compared Against Other Published Estimates

Published market values for North America digital signage can differ even when the topic name looks identical, because the boundary of what is counted is not always the same. Differences usually come from how hardware versus software is treated, whether Mexico is included, how kiosks and outdoor units are classified, and how pricing is converted and updated across years.

Trade and shipment direction checks, plus venue-level rollout signals from retail and transit expansion activity, are used as evidence points to keep Mordor Intelligence aligned to the installed base and refresh-driven demand, rather than only to a narrow advertising spend view.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.74 B (2025) | |

| Industry Research House A | USD 11.07 B (2025) | Uses a type-based scope where kiosks and certain screen formats can be counted more broadly, which can lift totals when multi-function units are treated as full digital signage deployments. |

| Regional Consultancy B | USD 8.61 B (2024) | Uses an earlier base year and can understate value if replacement-cycle revenues and higher-brightness outdoor mixes are not fully captured in the year's pricing and deployment assumptions. |

Across the three figures, most of the spread is explained by scope boundaries and timing, not by math errors. When the counted unit types and the base year are made consistent, the remaining difference usually comes from pricing progression and how refresh demand is modeled for existing networks.

Key Questions Answered in the Report

What is the current value of the North America digital signage market?

The market stands at USD 11.57 billion in 2026 and is expected to grow at a 7.69% CAGR to reach USD 16.76 billion by 2031.

Which component category is growing fastest?

Software platforms are expanding the quickest, supported by an 8.73% CAGR as enterprises prefer cloud subscriptions and AI-driven content optimisation

Why are transparent LED displays gaining attention?

They provide over 80% transparency, allowing retailers and architects to turn windows into dynamic media surfaces without blocking light or views.

How do programmatic DOOH platforms improve screen utilisation?

Real-time bidding allocates ad slots based on live audience and environmental data, boosting average screen fill-rates by 32% compared with fixed-schedule selling.

What are the main regulatory challenges?

Tighter privacy laws restrict facial analytics, while ENERGY STAR and state energy codes compel manufacturers to raise power efficiency and manage brightness outdoors.

Which country is projected to grow the fastest in the region?

Mexico leads with a 7.82% CAGR through 2031, driven by smart-city projects and expanding retail footprints.

Page last updated on: