North America Corrugated And Folding Carton Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

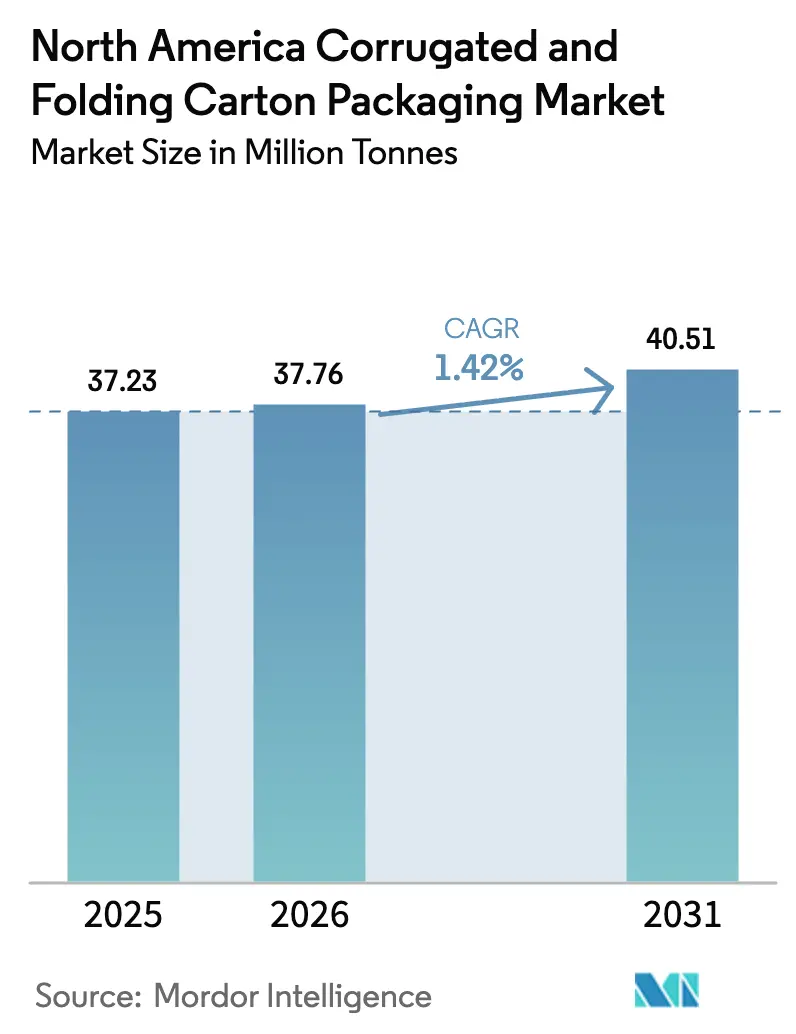

| Base Year Market Size (2025) | 37.23 Million tonnes |

| Market Volume (2026) | 37.76 Million tonnes |

| Market Volume (2031) | 40.51 Million tonnes |

| Growth Rate (2026 - 2031) | 1.42% CAGR |

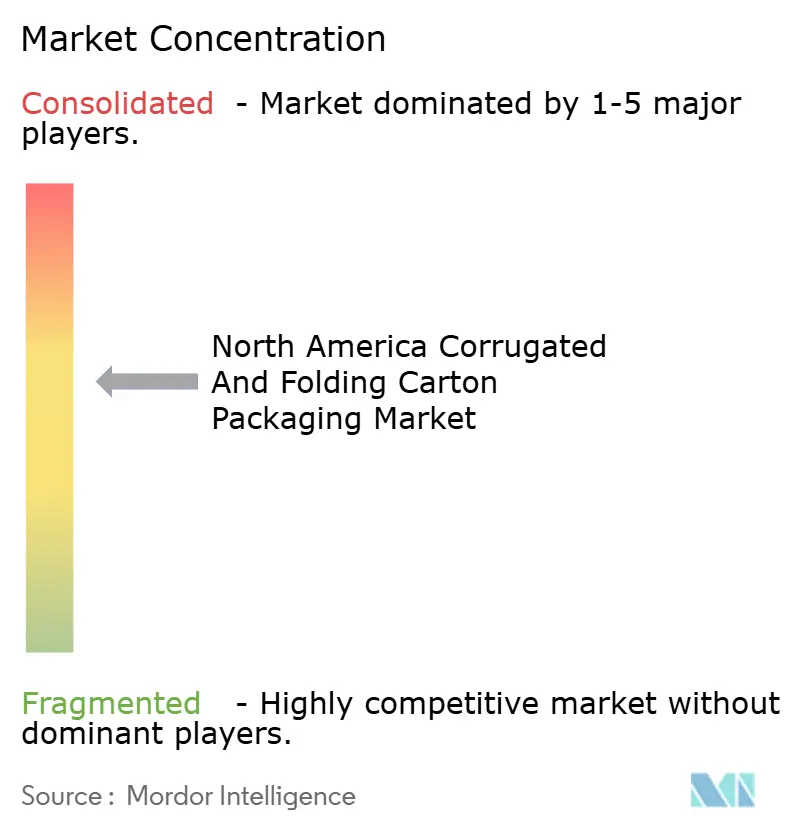

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Corrugated And Folding Carton Packaging Market Analysis by Mordor Intelligence

The North America corrugated and folding carton packaging market size in 2026 is estimated at 37.76 million tonnes, growing from 2025 value of 37.23 million tonnes with 2031 projections showing 40.51 million tonnes, growing at 1.42% CAGR over 2026-2031. Regulatory compliance, near-shoring of manufacturing, and e-commerce fulfillment standards are now the prime drivers of volume rather than pure consumption gains, positioning the North America corrugated and folding carton packaging market for steady yet subdued expansion. Recycled fiber remains the dominant input as brands seek Forest Stewardship Council (FSC) certification, while bamboo and agro-residue blends garner patent attention as credible substitutes for the volatile wood-based supply.[1]Forest Stewardship Council US, “FSC Certification in North America,” us.fsc.org Tight FDA guidance on pharmaceutical cartons and retailers’ shelf-ready mandates propel folding-carton upgrades that carry higher graphics and barrier requirements. Incremental, AI-enabled right-sizing is reshaping board engineering, and capital spending above USD 2.5 billion through 2025 underscores a shift toward automation and digital print that shortens run lengths and personalizes appearance.

Key Report Takeaways

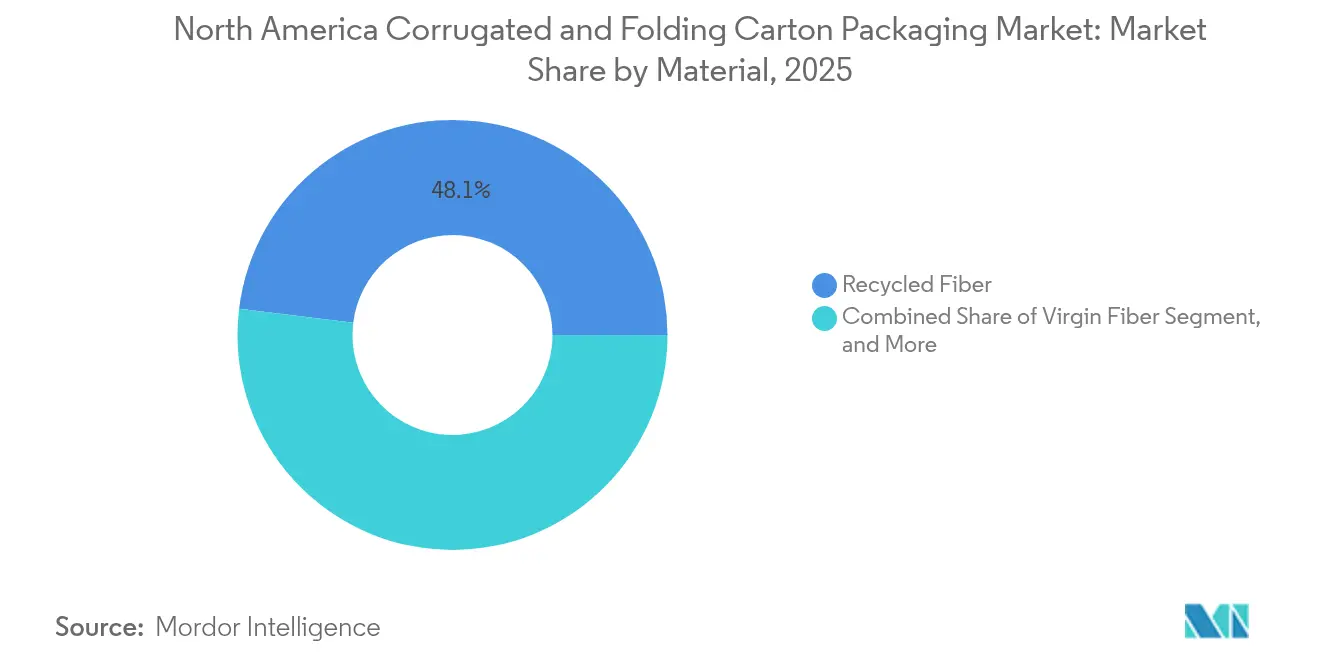

- By material, recycled fiber held 48.05% of the North America corrugated and folding carton packaging market share in 2025, whereas bamboo and agro-residue blends are projected to expand at a 3.16% CAGR through 2031.

- By packaging type, corrugated boxes accounted for 54.55% of the North America corrugated and folding carton packaging market size in 2025, while folding cartons are advancing at a 2.15% CAGR on the back of healthcare demand.

- By board type, single-wall designs led with 38.05% of the North America corrugated and folding carton packaging market share in 2025; triple-wall applications are forecast to grow at a 2.78% CAGR owing to automotive logistics.

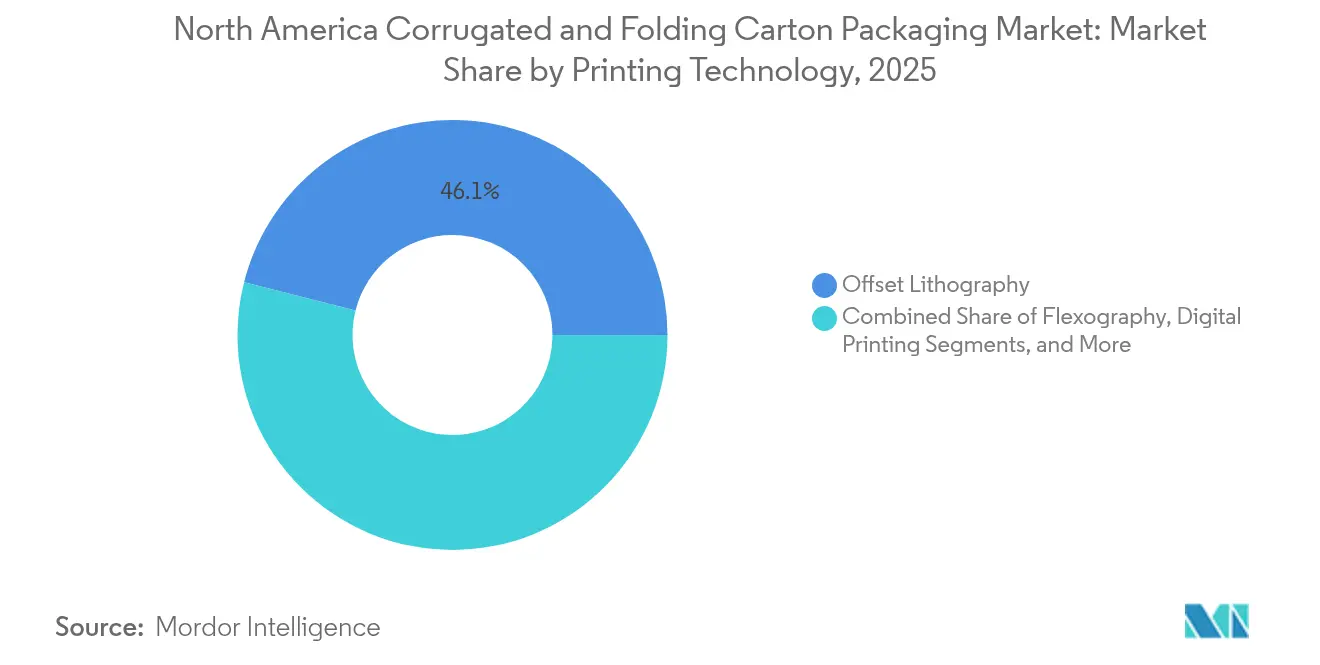

- By printing technology, offset retained 46.05% share of the North America corrugated and folding carton packaging market size in 2025, yet digital printing is climbing at a 3.72% CAGR as converters chase personalization.

- By end-user industry, food and beverage captured 32.10% share of the North America corrugated and folding carton packaging market size in 2025, whereas personal care and cosmetics are predicted to rise at a 2.58% CAGR until 2031.

- By geography, the United States commanded 73.00% of the North America corrugated and folding carton packaging market share in 2025; Mexico is the fastest-growing territory at 3.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Corrugated And Folding Carton Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce packaging volume surge | +0.4% | US hubs extending into Canada and Mexico | Short term (≤2 years) |

| Lightweighting and material efficiency | +0.2% | EPA regions in the US, federal zones in Canada, emerging Mexico | Medium term (2-4 years) |

| Corporate sustainability procurement targets | +0.3% | US retail chains, Canadian operations, Mexican manufacturing | Medium term (2-4 years) |

| Retail shelf-ready packaging adoption | +0.2% | Grocery chains in the US and Canada, expanding Mexican retail | Short term (≤2 years) |

| AI-driven box-size optimization platforms | +0.1% | Fulfillment centers in the US and Canada | Short term (≤2 years) |

| Rise of micro-fulfillment centers | +0.1% | Urban US markets and Canadian cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce packaging volume surge

Automation in fulfillment drives stricter tolerances for cartons, prompting performance upgrades in single-wall boards that must withstand direct-to-consumer shipping stresses. FDA guidance released in 2024 now treats prescription deliveries as e-commerce shipments, compelling folding cartons to integrate tamper-evidence and child-resistant features that align with parcel sortation systems.[2]U.S. Food and Drug Administration, “Packaging-Human Drugs,” FDA.gov AI algorithms embedded in converting lines enable plants to output more than 1,200 discrete box sizes per hour, slashing void-fill usage by 35% and saving corrugating medium. This capability boosts demand for both structural corrugated formats and premium-printed folding cartons that travel as their own shipper. Consequently, the North America corrugated and folding carton packaging market gains diversified volume with higher average revenue per tonne, tempering the mature demand curve.

Lightweighting and material efficiency mandates

EPA waste-reduction targets published in 2024 catalyze investment in lower basis-weight containerboard that maintains compression strength through advanced flute designs, trimming board weight by 18-22% yet meeting automated handling specs. FSC audit data confirms that 89% of corrugated output in North America now carries chain-of-custody certifications, a leap from 76% a year earlier. Such momentum encourages converters to adopt precision corrugators and closed-loop quality control that keep tight tolerances as the paper caliper shrinks. As material weight inches down, unit price edges up because clients pay for documented sustainability progress, contributing incremental value growth in the North America corrugated and folding carton packaging market.

Corporate sustainability procurement targets

Retail and consumer-goods firms embed recyclability thresholds and lifecycle metrics in sourcing contracts, forcing box makers to prove recycled content or carbon scores during tenders. Cascades reported that deals governed by explicit environmental requirements already make up 67% of its folding-carton revenue, commanding 8-12% price premiums when certification is verified. FSC, life-cycle analytics, and carbon disclosure now operate as deal qualifiers across big-box chains and fast-moving consumer goods brands. Smaller converters without auditing capabilities face shrinking addressable demand, sharpening competitive bifurcation, yet enlarging the total certified tonnage flowing through the North America corrugated and folding carton packaging market.

Retail shelf-ready packaging adoption

Grocery and club-store formats want cartons that shift from pallet to shelf with no unpacking, slicing labor minutes, and ensuring planogram consistency. Graphic Packaging’s USD 75 million fine-line die-cut installs target this need, integrating tear-strips and high-fidelity flexo that endure the supply chain’s scuffs while still merchandising on the shelf. Shelf-ready solutions often blend corrugated rigidity with folding-carton graphics, driving cross-vertical synergies inside converter networks. Adoption moves fastest in packaged foods, cosmetics, and small electronics, spurring incremental tonnage of high-spec board grades and widening the functional reach of the North America corrugated and folding carton packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in OCC prices | −0.3% | Recycling-dependent regions across North America | Short term (≤2 years) |

| Converters’ capital-expenditure inflation | −0.2% | US manufacturing centers and Mexican expansion zones | Medium term (2-4 years) |

| Labor shortages in box plants | −0.2% | US and Canadian industrial corridors | Short term (≤2 years) |

| Deforestation concerns and NGO pressure | −0.1% | US and Canadian timber basins | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in OCC prices

BLS producer-price data show containerboard swings of 28-35% through 2024, eroding margins for mills dependent on traded recycled fiber. Georgia-Pacific spent USD 550 million on vertical integration to steady inbound OCC, an option out of reach for smaller independents. During price spikes, converters accelerate tests of tomato-stem and wheat-straw fiber, but the commercial scale remains embryonic and premium priced. State recycling mandates elevate recovered-content quotas, increasing purchasing stress exactly when OCC supplies tighten. The resulting squeeze subtracts volume growth potential from the North America corrugated and folding carton packaging market until fiber alternatives mature.

Converters’ capital-expenditure inflation

Equipment vendors raised list prices amid steel and electronics shortages, inflating turnkey corrugator installs by 15-20% between 2023 and 2025. Borrowing costs climbed, lengthening payback periods on digital printers and servo-driven die-cutters essential for short runs. Firms defer or phase out investments, slowing the replenishment of aging assets that limit productivity. Mexican green-field projects encounter elevated civil works pricing, stretching timelines just as near-shoring demand peaks. Capex inflation, therefore, tempers the modernization pace inside the North America corrugated and folding carton packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Retains Scale amid Alternative Fiber Momentum

Recycled fiber accounted for 48.05% of the North America corrugated and folding carton packaging market share in 2025, validating municipal collection systems and retailer procurement mandates that favor post-consumer content. Market participants exploit its scale economies, yet volatile OCC pricing drove Cascades to incur an extra EUR 45 million (USD 48.6 million) in raw-material spend during early 2024. Consequently, strategic investment flows into agro-residue like tomato stems and wheat straw, a cohort expanding at 3.16% CAGR and supported by 23 patent filings in 2024 alone.

Alternative fiber pilots now move from lab to line as converters search for cost stability and marketing differentiation. While mechanical properties approach those of wood pulp, supply consistency and food-contact compliance still gate large-scale switch-overs. The North America corrugated and folding carton packaging market thus balances two trajectories: recycled fiber’s cost-risk yet comprehensive network, and fast-growing niche fibers still ramping into commercial breadth.

By Packaging Type: Corrugated Volume Dominance Meets Folding-Carton Value Uplift

Corrugated boxes held 54.55% of the North America corrugated and folding carton packaging market share in 2025, thanks to e-commerce logistics that demand durable shippers. Volumes rise in line with parcel counts, yet margin uplift stems from smart-box algorithms and linerboard weight reductions that preserve strength. Folding cartons, though smaller, grow at a 2.15% CAGR because FDA compliance pushes pharma brands into multi-layer barriers and tamper-evident locks that command higher unit pricing.

Converters straddle both forms through hybrid designs that marry corrugated rigidity with carton graphics, satisfying shelf-ready tasks while trimming layers. Investments in digital print blur the line further, allowing corrugators to deliver offset-like imagery on micro-flute and enabling cartons to assume secondary-pack roles. This convergence elevates the total addressable opportunity for the North America corrugated and folding carton packaging market.

By Board Type: Single-Wall Efficiency vs Triple-Wall Strength

Single-wall substrates represented 38.05% of the North America corrugated and folding carton packaging market size in 2025, leveraged for lightweight e-commerce parcels taxed by dimensional-weight tariffs. High-precision corrugators add next-gen flutes that lift edge-crush while shaving basis weight, preserving cost leadership. Triple-wall boards rise at a 2.78% CAGR as Mexico’s automotive exports require dense, vibration-resistant crates, reinforcing Mexico’s outsized influence on heavy-duty demand.

Suppliers develop hybrid flutes that chase single-wall economics yet near double-wall strength, guided by 15 patents filed in 2024. As end users refine SKU-specific cushioning, board selection hinges on predictive analytics rather than rule-of-thumb, expanding consultative service revenue across the North America corrugated and folding carton packaging market.

By Printing Technology: Offset Scale Maintains Share while Digital Rockets Upward

Offset lithography secured 46.05% of the North America corrugated and folding carton packaging market share in 2025, serving long-run food and beverage cartons that require precise brand-color fidelity. Digital print powers a 3.72% CAGR by enabling serialized pharmaceutical packs and personalized cosmetic sleeves, shortening the minimum economic run length to dozens instead of thousands.

Capital migration toward inkjet corrugators and toner-based sheet-fed presses accelerates as converters chase SKU proliferation. Setup-free changeovers cut waste and support micro-fulfillment demands for graphics variation. This technology mix evolves the revenue model from price-per-tonne toward price-per-impression, adding elasticity to the North America corrugated and folding carton packaging market.

By End-User Industry: Food Scale Counter-balances Healthcare Innovation

Food and beverage held 32.10% share of the North America corrugated and folding carton packaging market size in 2025, underpinned by everyday consumption and substitution away from plastic toward recyclable fiber. Personal care and cosmetics climb at 2.58% CAGR, leveraging premium folding cartons with holographic inks and soft-touch varnishes that amplify shelf impact.

Healthcare’s stringent serialization rules make tamper-evident and child-resistant cartons a steady margin driver, while electronics brands adopt anti-static liner stocks to secure microchips amid near-shoring. Industrial segments ride Mexico’s assembly growth, pulling heavier flutes and triple-wall wraps. The heterogeneous end-user base cushions cyclical shocks and sustains multi-segment depth within the North America corrugated and folding carton packaging market.

Geography Analysis

United States volume dominance stems from nationwide e-commerce fulfillment centers that specify lighter single-wall boards yet higher graphics fidelity, sustaining a high-margin mix for converters. Capital outlays in Iowa, Georgia, and Illinois add automated corrugators with AI integration, signaling a commitment to domestic capacity even amid near-shoring flows.

Canada’s packaging demand aligns with grocery and resource exports, but sustainability policy intensifies FSC adoption faster than the continental average. Urban micro-fulfillment growth around Toronto and Vancouver stimulates smaller ship-ready cartons that demand digital print agility. The North America corrugated and folding carton packaging market consequently sees technology migration northward as converters replicate US workflows.

Mexico evolves from import-reliant consumption to self-supplied capacity, anchored by automotive, electronics, and appliance clusters in Bajío and northern states. Rising labor competence, combined with duty advantages under USMCA, attracts both local entrepreneurs and multinationals setting up corrugators and folding-carton lines. Triple-wall board gains traction for cross-border parts shipments, balancing Mexico’s youthful consumer demand for shelf-ready cosmetics and personal-care packs. Local fiber sourcing remains underdeveloped, pushing investments in recycled medium and agro-residue pulping that could diversify the supply mix across the North America corrugated and folding carton packaging market.

Competitive Landscape

The market shows moderate consolidation as the top five converters account for about 65% of regional output, yet dozens of mid-tier independents thrive on niche agility. International Paper allocated USD 260 million to expand digital converting and AI-driven box lines in 2024, targeting e-commerce SKU complexity. Packaging Corporation of America spent USD 45 million on digital cutters that serve pharmaceutical serialization demands, reflecting a pivot toward short runs with track-and-trace features.

Georgia-Pacific’s USD 550 million Green Bay expansion and concurrent Alabama mill projects advance vertical integration amid OCC volatility, locking in linerboard feedstock and throughput. Graphic Packaging’s USD 75 million deployment of precision die-cutting amplifies shelf-ready offering for grocers and club stores, illustrating convergence between carton graphics and ship-ready rigidity. Sonoco’s partnerships with pharma majors embed serialization technology into folding cartons, a sign that regulatory compliance can become a revenue moat.

Smaller independents compete through regional service and custom job speed, yet rising capex costs and labor gaps tighten margins. Alliances form around shared digital print assets and joint FSC accreditation to meet bidding criteria. M&A interest stays active as private-equity investors seek bolt-ons that bring specialty coatings or automation IP. Overall, technology adoption, fiber security, and sustainability credentials set the competitive tempo inside the North America corrugated and folding carton packaging market.

North America Corrugated And Folding Carton Packaging Industry Leaders

International Paper Company

Smurfit WestRock

Packaging Corporation of America

Georgia-Pacific LLC

Cascades Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The FDA published supplemental guidance clarifying package-integrated RF tags for prescription traceability.

- December 2024: Forest Stewardship Council reported certification coverage for 85% of North American corrugated output, up 9% from 2023.

- September 2024: International Paper committed USD 260 million to expand its Iowa plant with AI-enabled converting lines producing 800 box configurations per hour.

- August 2024: Packaging Corporation of America completed a USD 45 million rollout of digital converting equipment in three U.S. plants.

North America Corrugated And Folding Carton Packaging Market Report Scope

The market study factors on the prevalent base scenarios, key themes, and end-use industry vertical-related demand cycles.

The North American corrugated and folding carton packaging market is segmented into (corrugated board packaging (type (single face, single wall, double wall, and triple wall), end-user industry (healthcare, home care, and personal care, beverage, transportation and logistics, food, industrial and hardware-based products, and other end-user industries)) and carton board/boxboard/paperboard packaging (folding carton packaging (end-user industry (food and beverage, tobacco, healthcare and pharmaceutical, personal care and cosmetics, and other end-user industries))) in the United States, Canada, and Mexico. The report offers the volume in tons for the above segments.

| Virgin Fiber |

| Recycled Fiber |

| Bamboo and Agro-residue Fiber Blends |

| Folding Cartons |

| Corrugated Boxes |

| Single Wall |

| Double Wall |

| Triple Wall |

| Folding Boxboard (FBB) |

| Other Board Types |

| Offset Lithography |

| Flexography |

| Digital Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare and Pharmaceutical |

| Personal Care and Cosmetics |

| Electronics and Appliances |

| Other End-user Industries |

| United States |

| Canada |

| Mexico |

| By Material | Virgin Fiber |

| Recycled Fiber | |

| Bamboo and Agro-residue Fiber Blends | |

| By Packaging Type | Folding Cartons |

| Corrugated Boxes | |

| By Board Type | Single Wall |

| Double Wall | |

| Triple Wall | |

| Folding Boxboard (FBB) | |

| Other Board Types | |

| By Printing Technology | Offset Lithography |

| Flexography | |

| Digital Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Electronics and Appliances | |

| Other End-user Industries | |

| BY Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the 2026 volume of North American corrugated and folding cartons?

The region shipped 37.76 million tonnes in 2026.

How fast will volume grow by 2031?

It is forecast to rise at a 1.42% CAGR, reaching 40.51 million tonnes.

Which material leads the mix today?

Recycled fiber commands 48.05% share, underpinned by mature collection systems and FSC mandates.

Where is growth strongest geographically?

Mexico is forecast to post a 3.54% CAGR through 2031 as near-shoring accelerates packaging demand.

Which printing technology is gaining the most traction?

Digital printing is expanding at 3.72% CAGR, driven by personalization and short-run economics.

What restrains faster expansion?

OCC price volatility, labor shortages, and rising capex inflate costs and temper overall market growth.

Page last updated on: