Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

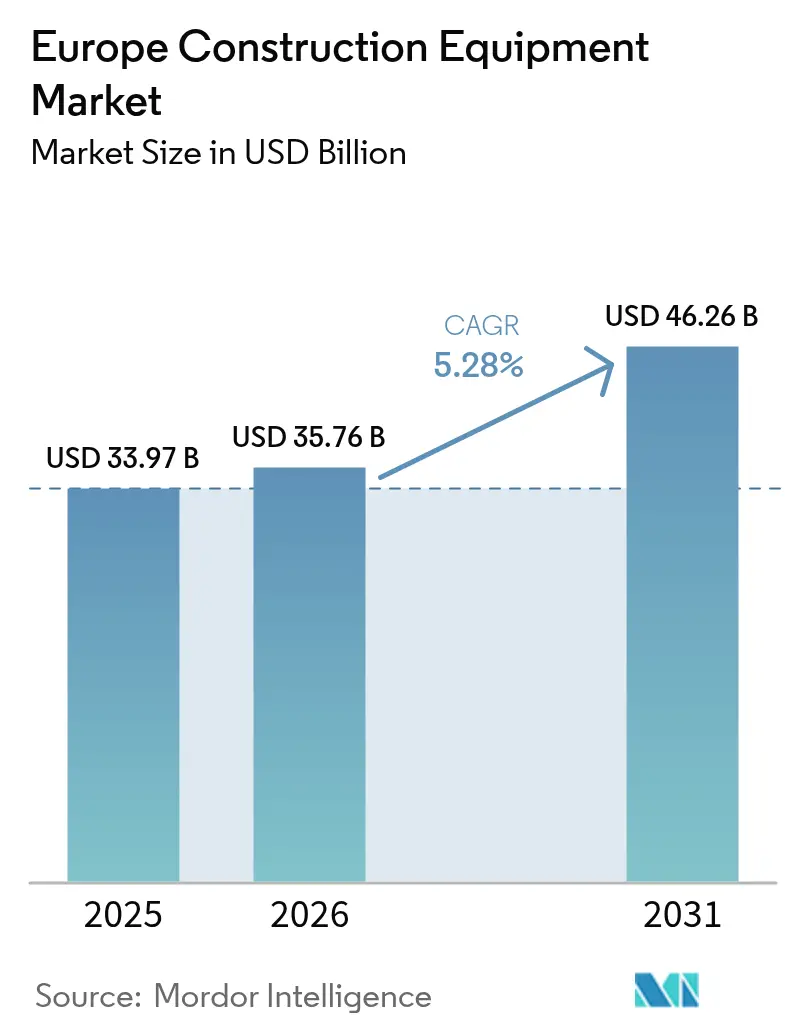

| Base Year Market Size (2025) | USD 33.97 Billion |

| Market Size (2026) | USD 35.76 Billion |

| Market Size (2031) | USD 46.26 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Construction Equipment Market Analysis by Mordor Intelligence

The Europe Construction Equipment Market size was valued at USD 33.97 billion in 2025 and estimated to grow from USD 35.76 billion in 2026 to reach USD 46.26 billion by 2031, at a CAGR of 5.28% during the forecast period (2026-2031). Rising public-works spending linked to the EU Green Deal, the European Central Bank’s 2025 rate-cut cycle, and the ongoing rollout of Stage V emissions rules are the primary forces shaping demand. Equipment buyers are tilting toward battery-electric models for urban projects, while diesel machines remain essential on heavy infrastructure sites. Chinese original-equipment manufacturers (OEMs) are using direct financing and local support centers to narrow competitive gaps with incumbent Western brands. Simultaneously, rental-fleet oversupply is suppressing average selling prices, accelerating the pivot to service-centric revenue streams and subscription telematics bundles.

Key Report Takeaways

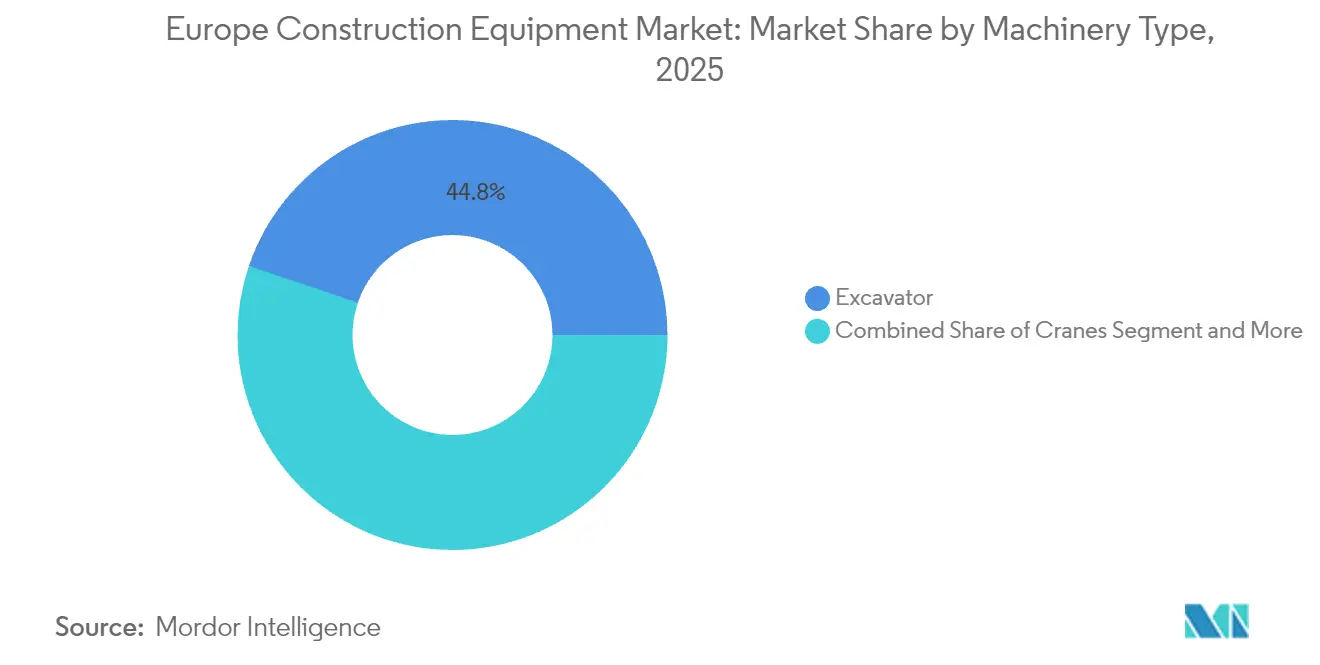

- By machinery type, excavators led with a 44.78% share of the Europe construction equipment market in 2025, whereas telescopic handlers posted the highest 5.36% CAGR to 2031.

- By power source, internal combustion engines held 80.66% of the Europe construction equipment market size in 2025, while battery-electric units are set to expand at a 5.39% CAGR through 2031.

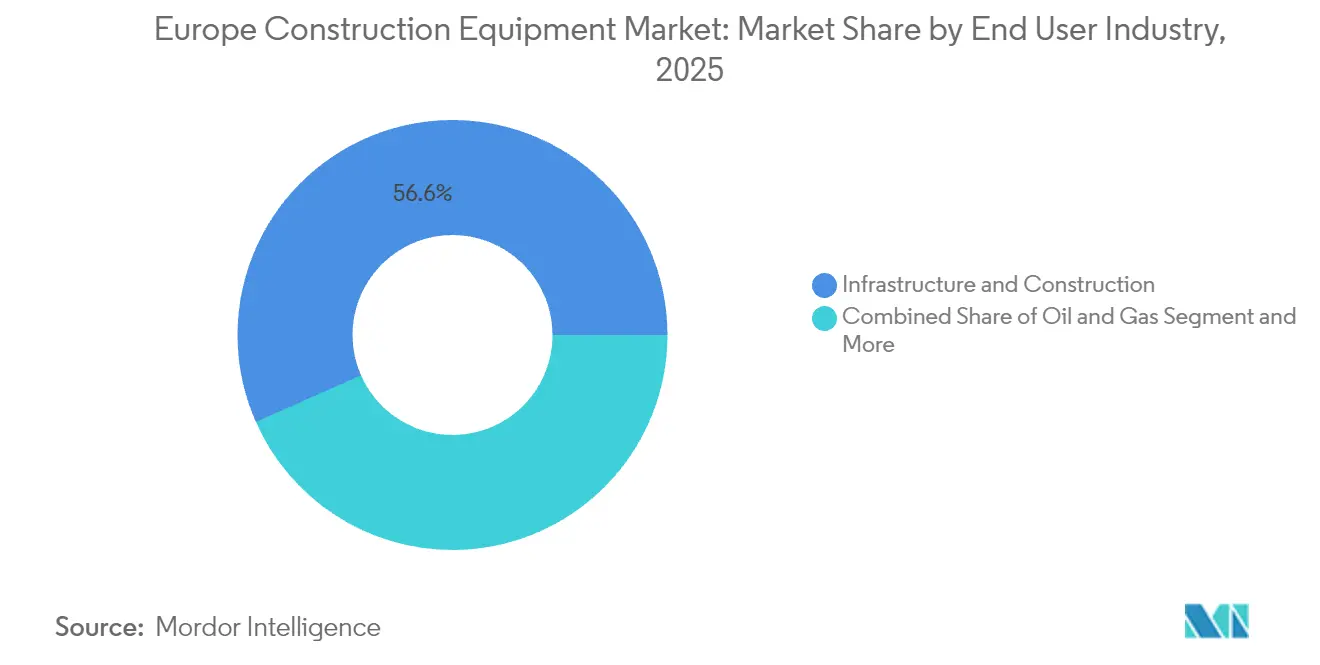

- By end-user industry, infrastructure and construction accounted for 56.62% of the Europe construction equipment market size in 2025; utilities and renewable energy are projected to grow at a 5.31% CAGR by 2031.

- By application, earthmoving secured 43.10% of the Europe construction equipment market share in 2025, whereas excavation and demolition activities are forecast to rise at a 5.41% CAGR to 2031.

- By country, Germany commanded a 24.22% share of the Europe construction equipment market in 2025, while Spain is poised for the fastest 5.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green Deal-Linked Public-Works Pipeline | +1.2% | EU-wide, concentrated in Germany, France, Netherlands | Long term (≥ 4 years) |

| Recovery Of Residential Starts As Ecb Rate-Cut Cycle Begins | +0.9% | Core EU markets, particularly Germany, France, Spain | Short term (≤ 2 years) |

| Accelerated Fleet Electrification | +0.8% | EU-wide, early adoption in Nordic countries | Medium term (2-4 years) |

| Growing Demand For Compact Equipment | +0.6% | Urban centers across EU, concentrated in Western Europe | Medium term (2-4 years) |

| OEM-Led Subscription & Telematics Bundles | +0.4% | Global, with EU as early adopter market | Long term (≥ 4 years) |

| Surge In Battery-Electric Telehandlers | +0.3% | Industrial corridors in Germany, Netherlands, UK | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Green Deal-Linked Public-Works Pipeline

Member states are channeling unprecedented capital into climate-resilient infrastructure, compressing procurement cycles from 18-24 months to as few as 12 months. Germany’s off-budget fund is already lifting real construction outlays by minimal in 2025 after a slight contraction in 2024[1]“Investitionspaket Infrastruktur,” Bundesministerium für Wohnen, Stadtentwicklung und Bauwesen, bmwsb.bund.de . This spending wave boosts demand for excavators, motor graders, and compact machines needed for renewable-energy installations. Contractors increasingly favor Stage V-compliant or electric models, even when premiums exceed more than one-tenth, to secure eligibility for Green Deal tenders. Suppliers therefore face mounting pressure to maintain higher inventory buffers that match accelerated project timelines.

Recovery Of Residential Starts As Ecb Rate-Cut Cycle Begins (2025-26)

Housing investment turned positive slightly in Q1 2025, the first upturn since 2022[2]“Bank Lending Survey Q1 2025,” European Central Bank, ecb.europa.eu. Mortgage approvals and construction loan demand have strengthened, especially in Germany, where pent-up housing needs accumulated during the high-rate period. Compact excavators, mini loaders, and telehandlers benefit the most because urban infill projects dominate new housing activity. Easier credit is also pulling small contractors back into the equipment-financing market, widening the customer base for entry-level electric machines.

Accelerated Fleet Electrification To Meet Stage V/Vi Co₂ & Nox Caps

The regulatory “ratchet effect” is now moving fast enough that buyers defer diesel purchases in anticipation of electric alternatives. Volvo has committed to an all-electric compact lineup by 2030, while SANY displayed six pure-electric units at INTERMAT 2024, equal to one-fifth of its European booth[3]“Roadmap to 2030 Electric Portfolio,” Volvo Construction Equipment, volvoce.com . Cities such as Oslo already require zero-emission equipment on public sites, producing localized demand spikes that exceed current production capacity. Contractors shifting above 1,500 operating-hours per year report total cost of ownership savings above 30%, even after accounting for charging infrastructure investments.

Growing Demand For Compact Equipment On Urban Infill Sites

Urban land scarcity is forcing cities to redevelop existing plots, raising the relevance of zero-tail-swing machines that operate within tight envelopes. Kubota is investing in a new German facility to boost mini-excavator capacity two-fifth by 2028, underlining expectations of sustained demand. Rental penetration for compact units already tops more than three-fifth in major metros, reflecting contractors’ need for flexibility when storage space can cost USD 500 per month per unit. Multi-functional compact models capable of excavation, lifting, and material handling are displacing fleets of single-purpose machines, sharpening the competitive premium on advanced attachment systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rental-Fleet Oversupply | -0.7% | EU-wide, most pronounced in Germany, UK | Short term (≤ 2 years) |

| Scarcity Of Certified Operators | -0.6% | EU-wide, acute in Germany, Netherlands, Nordic countries | Long term (≥ 4 years) |

| Lithium & Rare-Earth Price Volatility | -0.5% | Global supply chains, EU manufacturing centers | Medium term (2-4 years) |

| Persistent Ce-Mark/Homologation Delays | -0.4% | EU borders, affecting all member states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rental-Fleet Oversupply Suppressing New-Unit ASPs

Aggressive fleet expansion during 2021-2022 left rental utilization at only 63.4% in 2024, pushing rental rates down on year over year. Sluggish rental growth has forced companies to cut fleet spending by minimal, creating channel inventory bulges of six to nine months. Manufacturers respond with longer financing terms and service credits, but these steps erode margins and slow innovation budgets.

Scarcity of Certified Operators Inflating Project Timelines

Four out of five European contractors cannot find enough skilled operators, and demographic trends suggest the workforce will lose 1 million people a year until 2050. Projects are now running one-fifth longer, prompting contractors to keep redundant machines on-site to stay on schedule. This labor shortage is also accelerating adoption of semi-autonomous functions that allow less-experienced workers to achieve acceptable productivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Excavator Dominance Drives Electrification

Excavators captured 44.78% of the Europe construction equipment market share in 2025 and are projected to grow at a 5.32% CAGR to 2031, outpacing the overall Europe construction equipment market. Telescopic handlers follow closely in growth, fuelled by warehouse automation projects that demand precision placement at height. Cranes maintain steady volume but see margin pressure from lower-priced imports, while motor graders gain from transport-corridor spending.

Electrification reshapes competitive dynamics within each subcategory. Liebherr’s L 507 E wheel loader delivers 16-hour run-time, showing functional parity with diesel units. Loader and backhoe segments face intense price competition from Chinese OEMs, whereas specialized tunneling equipment retains higher entry barriers thanks to complex safety certifications. Contractors increasingly prefer multi-functional attachments that turn excavators into demolition, recycling, or grading tools, boosting average selling price per unit and locking buyers into proprietary hydraulic interfaces.

By Power Source: ICE Transition Accelerates Electric Adoption

Internal combustion engines still hold 80.66% of the Europe construction equipment market size in 2025, but battery-electric units are climbing fastest at a 5.39% CAGR. Hybrid drive-trains bridge constraints where charging infrastructure is lacking, yet total cost of ownership advantages favor full electrics on high-utilization sites. Provincial mandates in Norway and the Netherlands restrict diesel equipment on public projects, triggering regional spikes in electric orders that outstrip factory lead times.

Capital costs for electric machines are one-fifth higher, but contractors running 1,500 hours annually recoup premiums in under four years through fuel and maintenance savings. Hydrogen fuel cells remain niche, but Liebherr’s pilot hydrogen excavator has sparked interest for use in remote wind farms where grid supply is thin. Manufacturers must now manage dual product platforms—diesel and electric—stretching R&D budgets and supply chains. Battery sourcing is complicated by lithium and rare-earth price swings that raise bills of material, a restraint subtracting 0.5 percentage points from Europe construction equipment market CAGR projections.

By End-user Industry: Infrastructure Leadership Faces Utility Challenge

Infrastructure and construction applications accounted for 56.62% of the Europe construction equipment market size in 2025, but utilities and renewable energy are expected to top the growth league at a 5.31% CAGR through 2031. Wind-farm installations require large lifting capacities yet strict noise caps, pushing demand for hybrid cranes and battery-electric telehandlers. Grid-modernization projects need high-precision excavators and trenchers capable of simultaneous digital mapping to minimize street-closure durations in congested cities.

Manufacturing and warehousing spur demand for compact electric handlers that operate safely indoors. Agriculture and forestry segments wrestle with compliance costs for Stage V engines, accelerating consolidation among smaller operators unable to absorb price hikes. Mining and quarrying stay resilient as aggregates demand grows, but face scrutiny over carbon footprints, steering customers toward machines equipped with idle-reduction software and alternative fuels.

By Application: Earthmoving Stability Contrasts Demolition Growth

Earthmoving retained a 43.10% share of the Europe construction equipment market in 2025, mirroring its ubiquity across project types, yet excavation and demolition are set to record a 5.41% CAGR through 2031 as Europe renews aging building stock. Strict waste-handling rules drive uptake of machines with integrated dust suppression and quick-coupler systems for recycling attachments. Demolition contractors value high-reach excavators such as Caterpillar’s UHD, which debuted at Bauma 2025, capable of 3-story dismantling without repositioning.

Multi-functionality blurs traditional application lines. A single compact excavator fitted with a tilt-rotator and grapple can switch from earthmoving to material sorting in minutes, letting contractors slim fleet sizes and reduce transport costs. Road-building equipment enjoys steady replacement demand due to EU-funded maintenance programs, but margins tighten as rental oversupply tempts municipalities into shorter lease cycles instead of outright purchases.

Geography Analysis

Germany remains the anchor of the Europe construction equipment market, holding 24.22% share in 2025 on the back of its industrial base and the infrastructure outlay that lifts 2025 construction spending by minimal. However, political gridlock and cost inflation temper medium-term optimism, forcing contractors to seek price-competitive imports and rental contracts to hedge demand risk. OEMs with domestic assembly plants benefit from “Buy German” preferences in public tenders but must still match Chinese entrants' flexible financing.

Southern Europe shows divergence. Spain is projected to grow at a 5.35% CAGR through 2031 as tourism-related hotel, resort, and transport projects restart, aided by EU cohesion funds that cut project-loan interest below the bloc’s average. Italy’s recovery is slower; although it receives EUR 200 billion under the EU Recovery and Resilience Facility, permitting delays and seismic retrofitting complexities push work into late-decade schedules. Both markets tilt toward compact and mid-sized equipment suited to urban renewal and hillside construction environments.

Northern and Eastern Europe offer premium and growth-catch-up stories, respectively. The Netherlands and Belgium prioritize port expansion and logistics hubs that need low-emission machinery, and their municipalities pay premiums for electric fleets. Poland remains the largest Eastern European growth engine, adding residential and road capacity as incomes rise. Nordic nations lead in Stage V enforcement and are early adopters of autonomous and electric technologies; Oslo’s zero-emission jobsite mandate effective 2025 accelerates local fleet turnover. Collectively, these regional nuances reinforce the requirement for adaptive product portfolios and underscore why no single manufacturer hold significant regional share in the Europe construction equipment market.

Regulatory Landscape

The EU regulatory baseline for non-road mobile machinery (NRMM) in Europe continues to be anchored by Regulation (EU) 2016/1628, which sets pollutant emission limits and type-approval requirements for internal combustion engines used in construction equipment. In parallel, the Machinery Regulation (EU) 2023/1230 is replacing the prior Machinery Directive framework, tightening requirements around health and safety by shifting compliance emphasis toward updated technical documentation and conformity processes for machinery placed on the EU market.

Standards alignment is also being refreshed at the EU level. In March 2026, the European Commission adopted Implementing Decision (EU) 2026/546 updating harmonised standards relevant to equipment categories including earth-moving machinery and cranes, supporting presumption of conformity under the machinery framework. Separately, Regulation (EU) 2025/14 establishes a harmonized EU regime for NRMM intended to circulate on public roads, with full applicability starting 29 January 2028. This creates an additional compliance track for OEMs and importers beyond emissions and general machinery safety.

Value Chain Analysis

The Europe construction equipment value chain covers component suppliers (powertrains, hydraulics, electronics, and increasingly batteries and sensors), OEM design and assembly, dealer and direct-sales channels, rental companies, and an extensive aftermarket ecosystem across parts, service, attachments, and digital fleet-management subscriptions. The supplier base includes thousands of SMEs integrated with global manufacturers, which ties OEM production to shared industrial inputs and logistics networks across the wider mobility and automotive ecosystems, while rental penetration and telematics bundles shift how value is captured after the initial sale.

Two stress points stand out: compliance complexity and supply risk. On compliance, OEMs and suppliers are managing overlapping obligations linked to the Machinery Regulation (EU) 2023/1230, alongside emerging digital requirements discussed by industry bodies, which increases engineering and documentation workload across the chain. On the supply side, electrification raises exposure to critical materials and electronics, reinforcing the need for more resilient sourcing and localized assembly strategies. In the industry, this comes against a backdrop of return to growth in 2025 (4.6% sales increase reported by CECE) after a sharp 2024 downturn, with infrastructure activity helping stabilize ordering patterns for OEMs, dealers, and rental fleets.

Competitive Landscape

Competition remains moderate yet intensifying. Traditional leaders include Caterpillar, Volvo Construction Equipment, and Liebherr, commanding strong aftermarket networks but saw revenue contraction in 2024 as rental oversupply cut unit demand. They now rely more on subscription telematics and predictive maintenance to stabilize earnings. Caterpillar’s VisionLink™ platform crossed 1 million connected assets in Europe in 2025, generating double-digit growth in data-service revenue while offsetting weaker new-machine margins[4]“VisionLink Connected Assets Milestone,” Caterpillar, cat.com .

Chinese OEMs have moved from export-only plays to full-service operations. XCMG opened its Düsseldorf training center and rolled out captive financing that offers 0% interest for the first year, a direct challenge to Western dealers’ credit terms. SANY elevated international revenue in 2024, with Europe accounting for an increasing share as its electric mini-excavator beat rivals to achieve CE certification. Hybrid distribution models—combining direct sales, digital storefronts, and localized showrooms—allow Chinese brands to undercut traditional dealer margins while maintaining service access.

Consolidation among second-tier Western players is underway. Fayat Group’s acquisition of Mecalac in June 2025 expands its presence from road machinery into compact excavators and loaders, aiming to leverage cross-selling with Bomag and Dynapac. The deal also raises barriers for standalone mid-sized brands that lack the capital to match R&D outlays needed for dual-power-train compliance. Across the board, the Europe construction equipment market’s moderate concentration keeps price competition fierce, but the rising software component offers a pathway to differentiate beyond pure hardware specifications.

Europe Construction Equipment Industry Leaders

Liebherr Group

Komatsu Ltd.

Caterpillar Inc.

J.C. Bamford Excavators Limited

Volvo Construction Equipment

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A practical whitespace sits at the intersection of public-works procurement and low-emission operations. EU Green Deal-linked civil engineering programs and city-level zero-emission site requirements are pulling demand toward Stage V-compliant and battery-electric equipment in dense urban projects. OEM roadmaps and product launches in compact classes, including Volvo Construction Equipment's stated push toward an all-electric compact lineup by 2030 and Liebherr's compact crawler excavator updates, align with contractor total-cost-of-ownership economics already cited in the report context for high-utilization jobsites. This supports an actionable path for electrified compact excavators, wheel loaders, and telehandlers where charging can be organized around depots and predictable duty cycles.

A second opportunity is compliance-led product and service packaging as the EU framework evolves. Regulation (EU) 2025/14 establishes a harmonized rule set for NRMM circulating on public roads, with full applicability from 29 January 2028, while the Machinery Regulation (EU) 2023/1230 drives documentation and conformity upgrades. Those updates are reinforced by the March 2026 harmonised standards revision through Implementing Decision (EU) 2026/546. Together, these changes favor OEMs and dealer networks that can provide turnkey conformity support (technical files, CE processes, software updates) and monetize uptime through connected services. This aligns with the report's evidence on subscription telematics momentum and with the scale of connected-machine deployments, including Caterpillar's VisionLink platform surpassing 1 million connected assets in Europe in 2025.

Recent Industry Developments

- July 2026: Komatsu introduced a factory-fit Human Detection System developed with Safety Shield Global for selected European crawler excavators. The system embeds advanced safety capability at the OEM level rather than as a retrofit, which supports contractors dealing with tighter site-safety expectations and productivity pressure. It also differentiates Komatsu's excavator offering as digital and safety features become part of standard purchasing criteria.

- June 2026: Liebherr made its Generation 8 compact crawler excavators (R 915 Compact G8, R 917 Compact G8, and R 920 Compact G8) available, targeting urban construction and networked jobsite requirements. The launch strengthens Liebherrs position in high-volume compact classes where low-emission procurement and tight-site maneuverability matter. It also signals continued investment in connected-machine functionality as a competitive lever alongside hardware performance.

- December 2024: Kubota Corporation announced a new factory in Germany to raise mini-excavator capacity by 40% by 2028. The investment anchors additional European production close to key demand centers and rental fleets, supporting faster delivery and service responsiveness. It also reflects OEM prioritization of compact equipment supply as urban infill and smaller-project workflows expand across Western Europe.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Europe construction equipment market is treated as the value of equipment sold for use in construction and related earthmoving activity across European countries, counted in current US dollars and tied to end-use demand in the region.

Scope exclusions: We exclude pure parts-only aftermarket revenue, standalone service labor, and financing and insurance, unless they are bundled inside the equipment sale value.

Segmentation Overview

- By Machinery Type

- Cranes

- Telescopic Handler

- Excavator

- Loader and Backhoe

- Motor Graders

- Others

- By Power Source

- Internal-Combustion

- Hybrid

- Battery-Electric

- Hydrogen Fuel-Cell

- By End-user Industry

- Infrastructure & Construction

- Mining & Quarrying

- Oil & Gas

- Manufacturing & Warehousing

- Agriculture & Forestry

- Utilities & Renewable Energy

- By Application

- Earthmoving

- Lifting & Material Handling

- Excavation & Demolition

- Road Building & Paving

- Tunnelling

- Recycling & Waste Management

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Belgium

- Poland

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building the demand backdrop and the equipment cycle signals across Europe, and we do this using public datasets that can be checked by readers. Sources used include, for example, Eurostat construction output series and trade flows, European Commission releases on infrastructure and energy transition programs, and European Environment Agency publications that track emissions policy direction that can impact equipment mix.

We also review manufacturer annual reports, investor presentations, and public price lists where available. This helps us set realistic price bands by equipment class and account for country mix differences. For cross-checking production and shipment movement, an import and export shipment-level database and a company financials and intelligence subscription are used selectively, mainly to validate directional trends and to close obvious gaps in reported unit flows. These sources are then supported by reputable press coverage and association websites covering construction, rental, and equipment utilization. The desk research sources listed above are illustrative and not exhaustive, and many other references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to test pricing, volume momentum, and mix shifts that are not consistently visible in public datasets, and then to confirm what should be treated as in-scope equipment revenue in Europe. We spoke with stakeholders across OEM and dealer channels, rental fleets, contractors, and project-focused buyers across major European markets, so assumptions around utilization, replacement timing, and premium features could be checked and adjusted.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | |

| Mid tier: 50% | Functional/Unit leaders: 38% | |

| Smaller Players: 15% | Managers: 48% |

Market-Sizing & Forecasting

The core model is built with a top-down and bottom-up structure, where the top-down view reconstructs equipment demand from construction activity signals by country and then allocates that demand into equipment revenue pools. In practice, we map construction output trends, infrastructure investment direction, and fleet replacement cycles into unit demand, and then convert units into value using price ladders that reflect the Europe mix.

To keep the model grounded, selective bottom-up approximations are run alongside the top-down view, such as sampled unit volumes by equipment type through channel checks and average selling price (ASP) bands validated with primary respondents. A few inputs that typically move the totals are the country-level construction output trajectory, rental penetration and utilization in core markets, the share of earthmoving versus lifting and handling equipment, Stage V and electrification-driven mix changes, and financing rate direction that affects replacement timing. Where bottom-up inputs are missing for smaller countries or niche categories, we fill gaps using proportional splits based on construction activity shares and then re-check the results with experts.

For forecasting, scenario analysis is used around two or three realistic paths, and the base case is selected after aligning it with respondent expectations for project pipelines and pricing. ASP progression is handled through a simple but repeatable logic that separates list price movement from mix shift, so the model does not overstate growth just because higher-value machines take a bigger share in certain years.

Data Validation & Update Cycle

Validation is done through multiple checks so the numbers stay consistent with real-world signals. We compare model totals with independent indicators like construction output direction, reported order commentary from public filings, and trade and shipment movements, and then outliers are reviewed before the final view is signed off.

If a variance looks material, the assumptions that usually drive it (country weights, unit demand intensity, and ASP bands) are re-tested and respondents can be re-contacted for clarification. Reports are refreshed at least once a year, and interim updates are triggered when there are material events like sharp currency moves, major policy shifts, or sudden swings in construction activity. Before delivery, we check the latest public information again so clients receive a current view.

Mordor Intelligence's Europe Construction Equipment Market Size Versus Other Published Estimates

Published market values for Europe construction equipment often do not match because each publisher makes different calls on timing, currency conversion, and what exactly is counted as equipment revenue. Differences also come from how price changes are applied, since one model may push a single inflation factor while another separates pricing from product mix.

In refresh-led work, the spread typically widens when exchange rates move during the year or when average selling prices shift due to electrification and Stage V compliant equipment taking share, which is why a consistent cut-off date matters. By re-checking country-level price bands near release and aligning currency timing across the full series, Mordor Intelligence reduces drift that can otherwise inflate totals when list prices and mix shift are blended too early.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 33.97 B (2025) | |

| Industry Publisher A | USD 46.15 B (2025) | This figure appears to use a broader equipment basket and a higher value build that can lift totals, especially if crushing and screening and adjacent civil engineering equipment are fully included and ASP inflation is applied more uniformly across types. |

| Regional Publisher B | USD 52.79 B (2025) | This estimate likely assumes a wider geography set and stronger price uplift, and it can also be pushed up when heavy equipment and compact equipment are both expanded with aggressive ASP progression and less frequent currency timing resets. |

The table shows that most of the gap is explained by what gets counted as construction equipment revenue and how quickly pricing is stepped up year to year. By keeping the scope anchored to equipment sales value in Europe and validating unit and price assumptions through repeatable checks, we end up with a market value that is easier to trace back to clear inputs.

Key Questions Answered in the Report

How large is the Europe construction equipment market in 2026?

The market stands at USD 35.76 billion in 2026 and is projected to grow to USD 46.26 billion by 2031 at a 5.28% CAGR.

Which machinery type leads demand?

Excavators hold the largest 44.78% share and are forecast to keep growing as electrified models gain traction.

What drives the shift toward electric equipment?

Stage V regulations, anticipated Stage VI limits, and municipal zero-emission mandates make battery-electric units the preferred choice on urban sites.

Why is rental-fleet oversupply a concern?

Utilization rates hover near 63%, forcing rental companies to trim fleet spending and pushing manufacturers to offer deeper financing incentives.

Which country offers the fastest growth through 2031?

Spain is expected to record a 5.35% CAGR due to tourism infrastructure revival and renewable-energy projects.

How are OEMs responding to competitive pressure?

Incumbents are pivoting to service-centric models, while Chinese entrants leverage captive financing and localized support centers to win share.

Page last updated on: