Construction Machinery Attachment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

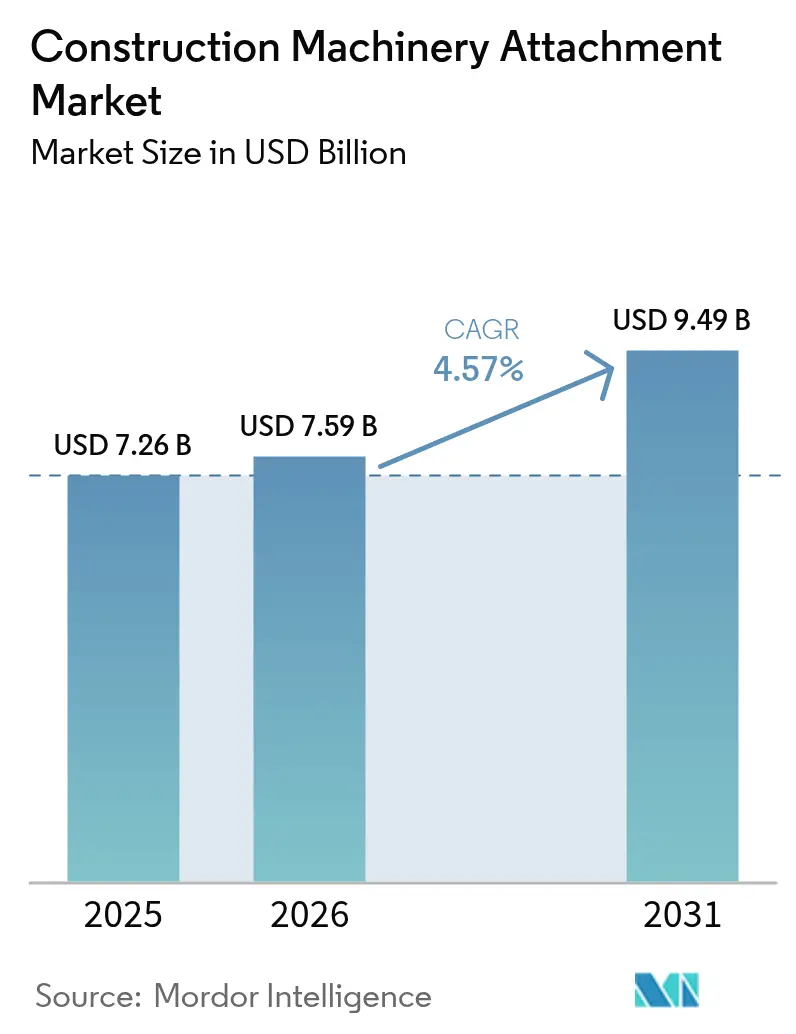

| Market Size (2026) | USD 7.59 Billion |

| Market Size (2031) | USD 9.49 Billion |

| Growth Rate (2026 - 2031) | 4.57% CAGR |

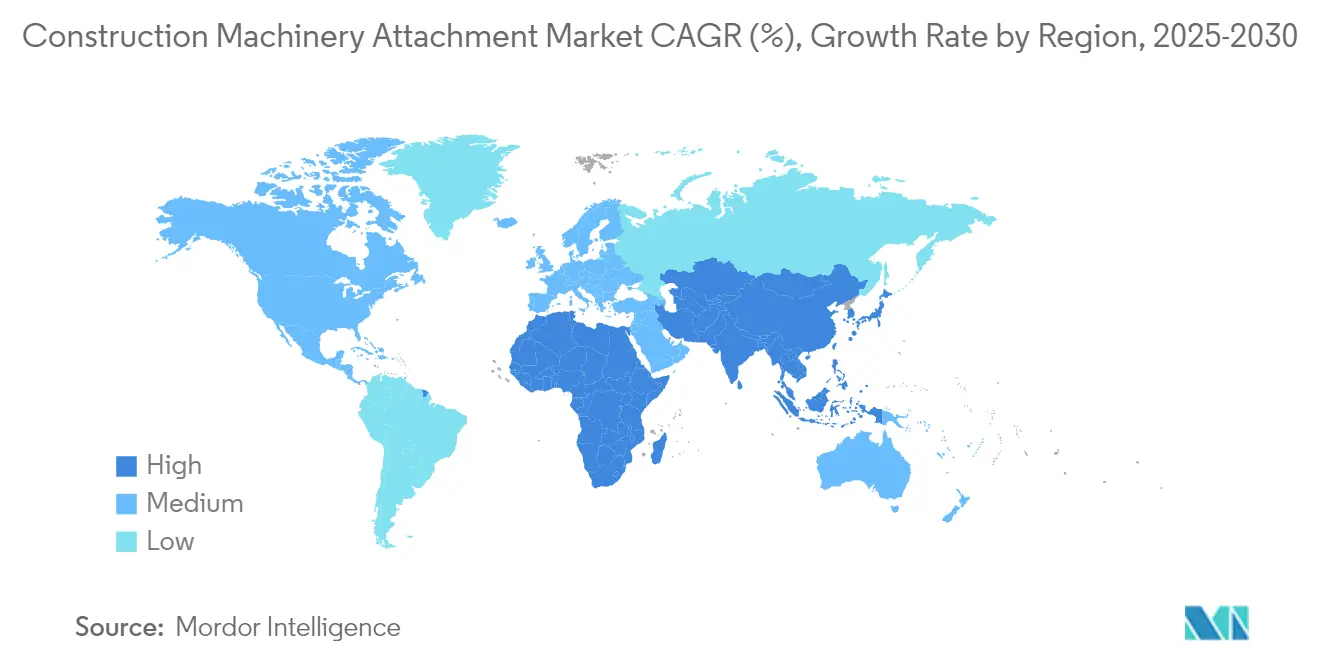

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Construction Machinery Attachment Market Analysis by Mordor Intelligence

The construction machinery attachment market size is expected to grow from USD 7.26 billion in 2025 to USD 7.59 billion in 2026 and is forecast to reach USD 9.49 billion by 2031 at 4.57% CAGR over 2026-2031. Growth is underpinned by accelerated urbanization and government-backed infrastructure upgrades, especially in the Asia-Pacific and North America, which are spurring demand for versatile add-ons that let contractors switch quickly between excavation, demolition, and material-handling tasks. Rental-fleet operators are standardizing high-usage attachments—such as hydraulic breakers, buckets, grapples, and tilt-rotators—to boost utilization rates and reduce total cost of ownership, while stricter safety and emissions regulations are prompting upgrades to newer, more efficient quick-coupler and automated tool-control systems. Upcoming opportunities lie in electrified and hybrid machinery—where lightweight, energy-efficient attachments can extend single-charge runtimes—and in smart, IoT-enabled tools that feed productivity data back to fleet-management platforms, opening aftermarket revenue streams for predictive maintenance and subscription-based software services.

Key Report Takeaways

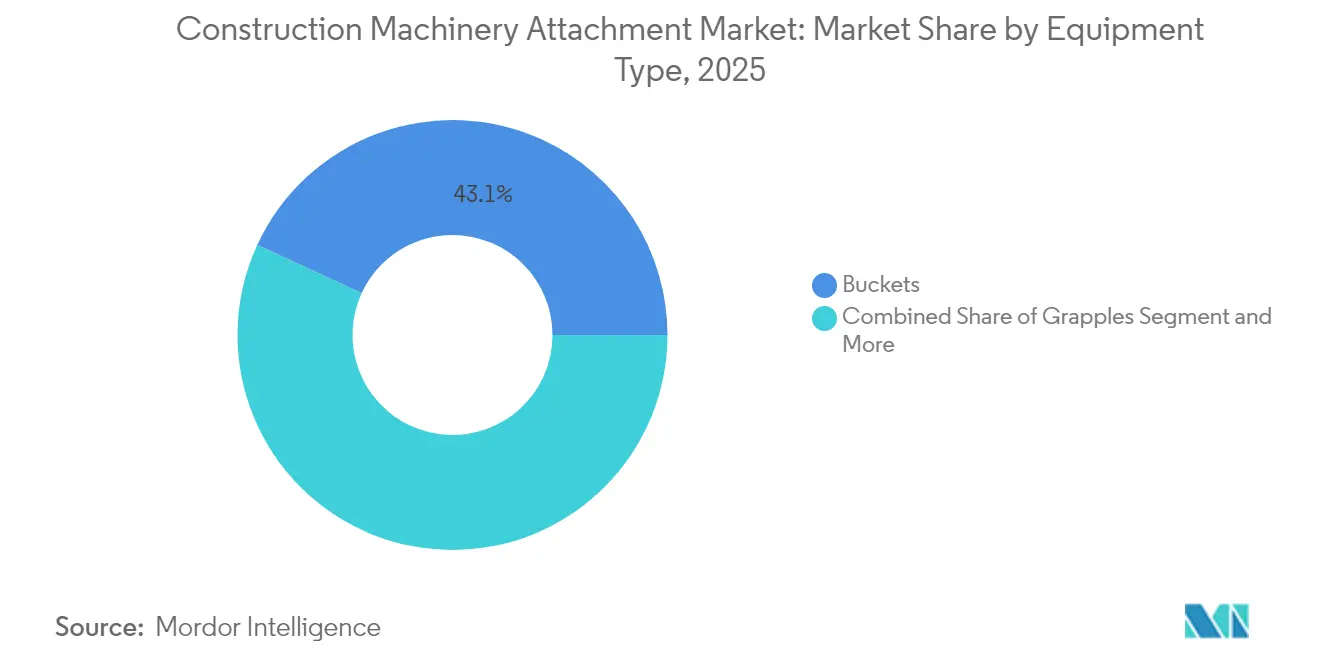

- By equipment type, buckets led with 43.12% revenue share in 2025; quick couplers are projected to advance at a 5.05% CAGR through 2031.

- By equipment class, excavator attachments accounted for 47.20% of the construction machinery attachment market share in 2025, whereas compact track loader tools show the highest 7.01% CAGR to 2031.

- By coupling system, pin-on designs retained 38.70% share in 2025; tiltrotators are poised for a 5.63% CAGR over the same horizon.

- By application, construction activities held a 39.60% share of the construction machinery attachment market size in 2025, while forestry exhibits a 6.43% CAGR outlook.

- By sales channel, the aftermarket posted a 61.75% share in 2025; the rental route expands at a 6.83% CAGR to 2031.

- By geography, Asia-Pacific maintained 46.10% share in 2025 and continues as the fastest-growing regional block at 5.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Construction Machinery Attachment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emerging-Market Infrastructure Boom | +0.9% | Primarily APAC, spill-over to MEA | Long term (≥ 4 years) |

| High-Efficiency Attachment Demand | +0.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rental-Fleet Tool Expansion | +0.7% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Electrification Retrofits | +0.5% | Europe and North America, early China uptake | Medium term (2-4 years) |

| Smart-ID BIM Attachments | +0.4% | Global, early developed-market leadership | Long term (≥ 4 years) |

| Lightweight Composite Designs | +0.3% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Infrastructure Spend in Emerging Markets

Programs such as India’s National Infrastructure Pipeline elevate demand for robust, easy-service attachments suitable for rugged sites and limited workshop access. India’s construction equipment sector targets USD 25 billion by 2030, up from USD 8.5 billion, on the back of rural roads, metro projects, and housing missions. Chinese OEMs respond with value-engineered tools that use simplified hydraulics and local steel grades, backed by regional plants that cut lead times and tariff exposure. These moves recalibrate supply chains and signal deeper localization as OEMs chase proximity to high-growth markets.

Rising Demand for High-Efficiency Attachments

Contractors prioritize throughput and fuel savings as margins tighten, driving widespread adoption of high-flow hydraulics and precision tooling. Tiltrotators illustrate the shift, recording a 5.86% CAGR on the ability to rotate 360°, reduce repositioning, and ease operator fatigue [1]“Tiltrotator market data 2025,” Rototilt Group, rototilt.com. Energy-recapture hammers now cut fuel use by up to 15% over conventional units, while integrated sensors feed job-site analytics platforms that flag maintenance needs early. Ecosystem thinking links quick couplers, automated controls, and telematics into a unified workflow that supports lean scheduling and shorter project cycles.

Expansion of Rental Fleets Requiring Multi-Purpose Tools

Rental companies reengineer fleets around attachments that serve demolition in one shift and finish grading the next, driving utilization and shrinking inventory complexity. In 2025, the United States rental sector is projected to achieve nearly USD 82.6 billion in revenue, representing a 5.7% growth and emphasizing the rising demand for versatile equipment. Universal coupling interfaces help operators move the same hammer, auger, or grapple across carriers, expanding addressable demand without ballooning capital budgets. Modular kits that convert a base unit for material handling, trenching, or precision cutting gain traction as rental firms market turnkey packages that bundle training and telematics support.

Electrification Retrofits Boosting Low-Vibration Tools

Battery-electric carriers are on the rise and are increasingly seeking specialized attachments that conserve energy without compromising productivity. Low-vibration breakers and lightweight augers reduce power draw, extend battery cycles, and comply with city noise codes. Oslo’s 2025 zero-emission job-site mandate anchors early adoption, creating reference deployments for other municipalities. Manufacturers optimize hydraulic circuits, swap steel for composites, and integrate anti-vibration dampers to unlock higher duty cycles per charge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-Operator Shortage | −0.6% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Specialty-Steel Volatility | −0.5% | Global, manufacturing hubs feel largest effect | Short term (≤ 2 years) |

| High Hydraulic Tool Costs | −0.4% | Global, most intense in price-sensitive economies | Medium term (2-4 years) |

| IoT Attachment Data Concerns | −0.2% | Global, regulatory focus in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Skilled Attachment Operators

Industry surveys indicate 73,500 new technicians are needed by 2030 to support advanced tooling, yet training pipelines lag. Complex tiltrotators and smart couplers demand hydraulic, electronic, and diagnostic literacy. Up to 40% of downtime links to operator error, inflating project costs. OEM-sponsored academies, micro-credential programs, and simulator platforms aim to fill gaps, but talent availability remains a chokepoint in near-term deployment plans.

Specialty-Steel Supply-Chain Volatility

Construction consumes 50% of global steel output, so abrupt mill outages or export curbs swiftly lift alloy surcharges and stretch lead times, inflating attachment production costs by 10-25% during peak volatility. Pandemic-era shutdowns followed by rapid project restarts deepened the supply-demand imbalance, making high-wear plates for cutting edges, chisels, and tiltrotator housings difficult to source at stable prices. Inventory strategies of vertically integrated producers such as Cleveland-Cliffs influence benchmark rates, amplifying swings felt by mid-tier OEMs. Smaller manufacturers sometimes delay launches or substitute heavier grades that add weight and raise fuel use, while rental firms keep aging tools in service longer to bridge gaps. Contract clauses that index pricing to steel costs, diversified mill networks, and buffered stock holdings help temper risk, yet persistent uncertainty still pressures margins and clouds delivery schedules. This volatility trims an estimated 0.5 percentage points from the market’s forecast CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Buckets Lead Despite Quick Coupler Innovation

Buckets accounted for 43.12% of the construction machinery attachment market in 2025, owing to their universal applicability across excavation, material handling, and quarrying. The construction machinery attachment market size for buckets is projected to climb steadily as infrastructure renewal sustains baseline demand. Quick couplers, while holding a smaller slice, are set for a 5.05% CAGR as fleet managers value rapid, tool-free swaps that minimize idle time.

Growth patterns underline a pivot to modular design. Manufacturers increasingly embed LIN-bus sensors and RFID tags that track cycle counts and maintenance needs in real time. Hydraulic hammers ride renovation and teardown work in urban cores, whereas grapples gain in forestry and waste transfer. Augers maintain steady orders from telecom trenching and utility pole installation. Specialty shears and pulverizers find traction as recycling mandates tighten. The segment’s future hinges on interoperability standards that let one coupler mate with competing attachment brands without performance loss.

By Equipment Class: Excavators Dominate While Compact Loaders Surge

Excavator attachments represented 47.20% construction machinery attachment market share in 2025, reflecting excavators’ role as the primary earthmoving platform. Compact track loader tools grow fastest at 7.01% CAGR as jurisdictions restrict full-size machines in dense downtown corridors. The construction machinery attachment market size tied to compact loaders is forecast to climb sharply as rental depots expand inventories of trenchers, planers, and cold-milling heads sized for 90 hp carriers.

Skid-steer loader tools remain popular among small contractors for cost-effectiveness, whereas backhoe loader add-ons serve municipal utility jobs. Wheel loader forks and rehandling buckets continue as bulk-material workhorses. Mini-excavator attachments benefit from residential infill construction, with tilting grading buckets gaining share. Telehandler platforms see incremental demand in mezzanine builds and industrial racking installs. Suppliers race to develop cloud-linked control systems that automatically fine-tune hydraulic flows to each attachment’s optimum setting.

By Coupling System: Pin-On Systems Prevail Despite Tiltrotator Innovation

Pin-on systems held a 38.70% share in 2025. Contractors still value simplicity, low cost, and minimal maintenance. At the same time, tiltrotators enjoy a 5.63% CAGR path as productivity gains outweigh their higher price in markets with elevated labor expenses.

Automatic hydraulic couplers, pioneered by Scandinavian suppliers, allow cab-seat tool changes and seal fluid lines on connection, cutting spillage and contamination risk. Universal quick couplers aim to harmonize tooling fleets across multiple OEM carriers, easing logistics for rental houses. Standardization bodies in Europe and North America push for ISO-conformant quick-coupler geometries to bolster cross-brand compatibility, which is expected to accelerate uptake.

By Application: Construction Leads While Forestry Accelerates

Construction absorbed 39.60% of the 2025 demand thanks to foundational earthworks, high-rise builds, and civil works. Conversely, forestry shows the swiftest 6.43% CAGR as climate policies steer funding toward wildfire-fuel reduction and sustainable logging. The construction machinery attachment market size for forestry tools remains smaller, yet investment in purpose-built chainsaw felling heads, brush cutters, and biomass grapples is expanding.

Urban demolition drives the uptake of concrete pulverizers and dust-suppressed breakers. Mining and quarrying call for abrasion-resistant buckets with side-shrouds and wear-liners. Agriculture and landscaping demand multipurpose blades and tillers suited to compact carriers. Waste-handling grapples and shears grow in tandem with circular-economy strategies. Seasonal snow removal attachments see procurement boosts as municipalities fortify winter-maintenance fleets against volatile weather patterns.

By Sales Channel: Aftermarket Dominance Amid Rental Growth

Aftermarket distribution represented 61.75% of global revenue in 2025 because contractors prefer tailoring attachments to each project rather than ordering factory bundles. Independent dealers stock brand-agnostic inventories, offer rebuild services, and provide flexible financing that matches short contract cycles.

Rental sales climb to 6.83% CAGR as general contractors seek asset-light models. Packages now include telematics dashboards, operator training, and on-site maintenance, helping rental firms position themselves as productivity partners rather than equipment lenders. OEM channels continue to bundle proprietary attachments with new carrier sales, leveraging integrated control algorithms and extended warranty marketing. Digital marketplaces also emerge, enabling peer-to-peer attachment sharing, though regulatory and liability issues are still being addressed.

Geography Analysis

Asia-Pacific led the construction machinery attachment market with a 46.10% footing in 2025 and is predicted to log a 5.18% CAGR through 2031. China’s decarbonization roadmap accelerates electric carrier deployment, prompting indigenous OEMs such as Sany and XCMG to roll out purpose-built hammers, grapples, and trenchers that match local emissions targets. In FY2024, bolstered by the government's infrastructure-driven initiatives, India witnessed a 26% surge in construction equipment sales, totaling 135,650 units. Southeast Asian nations channel Belt and Road investments into toll roads and ports, elevating demand for dredging buckets and long-reach demolition attachments.

North America remains the second-largest region, anchored by the USD 550 billion Infrastructure Investment and Jobs Act pipeline that spurs bridge repair, rail upgrades, and water-system overhauls. While carrier sales dipped in 2024, attachment demand shifted to high-value tools that lift job-site utilization. Adoption of tiltrotators rises in Canada, where labor scarcity pushes contractors toward technology that saves operator time. Electric-ready attachments gain early traction in California and New York as state policies tighten emissions caps.

Europe prioritizes low-noise, low-vibration systems, catalyzed by dense urban regulations. Manufacturers refine attachments for all-electric compact excavators as Volvo targets fully electric light equipment portfolios by 2030 . Germany spearheads precision joystick-controlled couplers for historical building renovations. The United Kingdom and France funnel renovation subsidies into energy-efficient building retrofits, boosting demand for hand-arm-vibration-reduced breakers and dust-suppression shears. Eastern European markets emphasize affordability, favoring refurbished attachments and local rebuild shops to stretch budgets while ramping up highway expansions.

Competitive Landscape

The construction machinery attachment market shows moderate concentration, with Caterpillar, Komatsu, and Volvo sharing space with specialized names such as Rototilt, Kinshofer, and Okada. Chinese newcomers leverage cost-competitive pricing and dense dealer grids to win emerging-market orders. Core competition pivots from stand-alone steel to integrated solutions combining hardware, sensor arrays, and cloud portals that deliver predictive maintenance alerts.

Leading OEMs bundle value-added services. Caterpillar’s PL161 tracker embeds Bluetooth tags into attachments, letting fleet managers trace location, hours, and theft events across project sites[3]“PL161 Attachment Tracker product sheet,” Caterpillar Inc., cat.com . Komatsu invests in Smart Construction Dashboard, overlaying 3-D job-site models with real-time attachment metrics to fine-tune cycle efficiency. Volvo partners with Steelwrist on symmetric quick-coupler standards to widen attachment compatibility.

Niche innovators seize gaps in composite-material cutting heads or low-flow hydraulic routers suited to electric mini-excavators. Rental majors vertically integrate refurbishment centers to extend attachment lifecycles and harvest data for pricing algorithms. M&A momentum persists: European specialist Mantovanibenne is scouting strategic tie-ups in North America to tap infrastructure funding, while U.S. private equity firms eye Asian grapple manufacturers for mid-market roll-ups.

Construction Machinery Attachment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Hitachi Construction Machinery

Volvo Construction Equipment

Case Construction Equipment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Remu unveiled in-house Hardox steel crusher buckets equipped with Rock-Zone technology, extending its demolition portfolio.

- January 2025: Ligchine launched the E-Z Grader skid-steer attachment to raise grading speed and accuracy.

- September 2024: Yanmar released a new family of compact track loader attachments aimed at landscaping and light construction tasks.

- July 2024: Mecalac presented MB30–MB80 hydraulic breakers for 5–16 t excavators, featuring no-load protection and automatic greasing.

Global Construction Machinery Attachment Market Report Scope

| Buckets |

| Grapples |

| Hydraulic Hammers |

| Augers |

| Quick Couplers |

| Rippers |

| Pulverizers |

| Shears |

| Mulchers |

| Others |

| Excavator Attachments |

| Skid-Steer Loader Attachments |

| Compact Track Loader Attachments |

| Backhoe Loader Attachments |

| Wheel Loader Attachments |

| Mini-Excavator Attachments |

| Telehandler Attachments |

| Others |

| Pin-On |

| Dedicated Quick Coupler |

| Universal Quick Coupler |

| Tiltrotator |

| Automatic Hydraulic Coupler |

| Construction |

| Demolition and Decommissioning |

| Mining and Quarrying |

| Forestry |

| Agriculture and Landscaping |

| Waste and Recycling |

| Snow Removal and Road Maintenance |

| Others |

| OEM |

| Aftermarket |

| Rental |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Turkey |

| South Africa | |

| Rest of Middle East and Africa |

| By Equipment Type | Buckets | |

| Grapples | ||

| Hydraulic Hammers | ||

| Augers | ||

| Quick Couplers | ||

| Rippers | ||

| Pulverizers | ||

| Shears | ||

| Mulchers | ||

| Others | ||

| By Equipment Class | Excavator Attachments | |

| Skid-Steer Loader Attachments | ||

| Compact Track Loader Attachments | ||

| Backhoe Loader Attachments | ||

| Wheel Loader Attachments | ||

| Mini-Excavator Attachments | ||

| Telehandler Attachments | ||

| Others | ||

| By Coupling System | Pin-On | |

| Dedicated Quick Coupler | ||

| Universal Quick Coupler | ||

| Tiltrotator | ||

| Automatic Hydraulic Coupler | ||

| By Application | Construction | |

| Demolition and Decommissioning | ||

| Mining and Quarrying | ||

| Forestry | ||

| Agriculture and Landscaping | ||

| Waste and Recycling | ||

| Snow Removal and Road Maintenance | ||

| Others | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| Rental | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Turkey | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the construction machinery attachment market?

The market is valued at USD 7.59 billion in 2026 and is projected to reach USD 9.49 billion by 2031.

Which region leads global demand for construction machinery attachments?

Asia-Pacific holds 46.10% of 2025 revenue and is forecast to grow at a 5.18% CAGR through 2031.

Which equipment type commands the largest share?

Buckets account for 43.12% of 2025 revenue, reflecting their universal role in excavation and material handling.

Why are rental channels growing faster than direct purchases?

Contractors favor asset-light strategies, pushing rental revenue to a 6.83% CAGR as fleets adopt multi-purpose, quick-swap tools.

Page last updated on: