North America Combine Harvesters Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

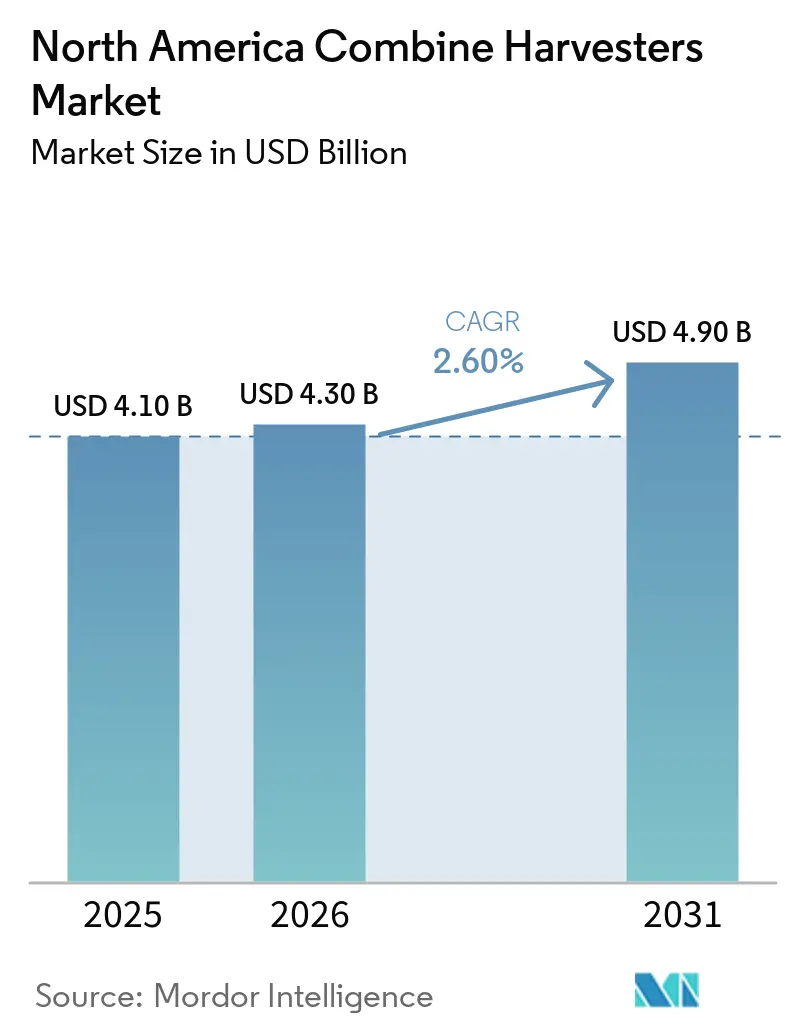

| Base Year Market Size (2025) | USD 4.10 Billion |

| Market Size (2026) | USD 4.30 Billion |

| Market Size (2031) | USD 4.90 Billion |

| Growth Rate (2026 - 2031) | 2.60% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Combine Harvesters Market Analysis by Mordor Intelligence

The North America combine harvesters market size is projected to expand from USD 4.10 billion in 2025 and USD 4.30 billion in 2026 to USD 4.90 billion by 2031, registering a CAGR of 2.60% between 2026 and 2031. Demand is shifting from high-unit-volume machines to high-value machines as large grain operations replace multiple aging harvesters with fewer platforms that bundle satellite guidance, yield mapping, and subscription-based autonomy. Average selling prices climbed in 2025, even as Deere & Company reported a 29% drop in combined unit sales in the United States and Canada, confirming that operators now value technology over fleet size. Canada bucked the volume slide because favorable canola returns and federal financing accelerated fleet renewals. Supply chains for semiconductors improved during 2026, but long hydraulic-component lead times still force manufacturers to carry elevated finished goods inventories, supporting price discipline. Rising protein-crop premiums and double-cropping strategies are widening the addressable customer base, particularly for tracked and high-horsepower variants that protect soil structure and compress harvest windows.

Key Report Takeaways

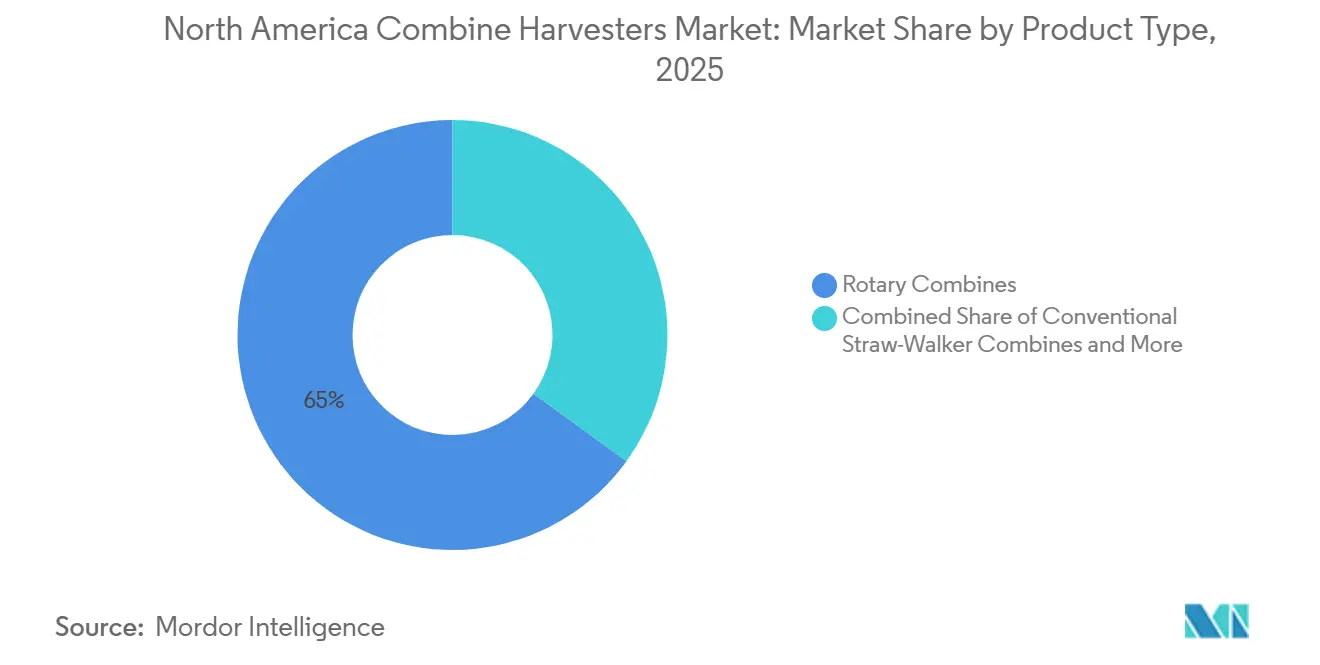

- By product type, rotary combines led the largest segment, with 65% of the North America combine harvesters market share in 2025, while tracked combines are the fastest-growing, forecast to post the fastest 7.8% CAGR through 2026 to 2031.

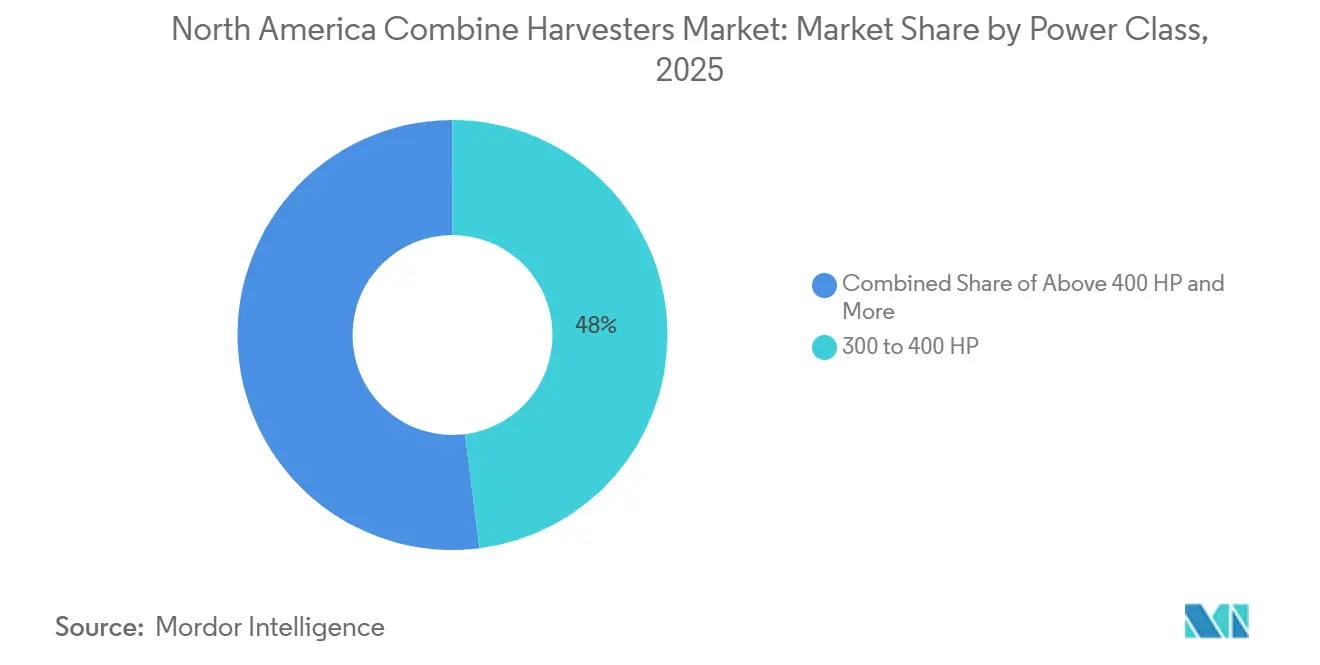

- By power class, the 300 to 400 HP segment accounted for the largest share, 48% of North America combine harvesters market size in 2025, while the above 400 HP segment is the fastest-growing, projected at a 6.9% CAGR from 2026 to 2031.

- By geography, the United States is the largest country, with 68% of the North America combine harvesters market share in 2025, whereas Canada is the fastest-growing country set to post at a 6.3% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Combine Harvesters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising labor costs and labor shortages | +1.2% | United States Midwest and Northern Plains, Canadian Prairies | Medium term (2-4 years) |

| Precision-agriculture adoption and integration | +1.0% | Corn Belt core, Saskatchewan and Alberta | Long term (≥4 years) |

| Government subsidies and preferential financing | +0.9% | Canada nationwide, United States Section 179 zones | Short term (≤2 years) |

| Accelerated fleet-replacement cycles on large farms | +0.7% | Farms above 5,000 acres across United States and Canada | Medium term (2-4 years) |

| Original Equipment Manufacturer (OEM) subscription-based autonomous software upgrades | +0.5% | Early-adopter states and pilot regions in Prairie Provinces | Long term (≥4 years) |

| Interoperability standards for grain cart-combine automation | +0.4% | United States Midwest, Canadian Prairies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Labor Costs and Labor Shortages

A decline in agricultural employment is accelerating the adoption of full mechanization across large grain farms, as indicated by World Bank data. Employment in agriculture decreased to 1.52% in 2025, compared to 1.56% in 2024. In 2024, Deere & Company introduced the S7 Series combines featuring Predictive Ground Speed Automation and automated harvest settings to improve harvesting consistency, productivity, and ease of operation[1]Source: Deere and Company, “S7 Series Combine Launch,” deere.com . Regions such as North Dakota, Montana, Saskatchewan, and Alberta are experiencing significant labor shortages despite high hourly wages. This has led to wage inflation, enhancing the return on investment for autonomous and semi-autonomous harvesters, thereby reducing labor demand. Leasing rates for combines equipped with advanced automation are increasing, reflecting a willingness to invest in features that minimize workforce requirements. Consequently, labor constraints are driving premium pricing and supporting the ongoing shift toward advanced technology in the North America combine harvesters market.

Precision-Agriculture Adoption and Integration

Combines have evolved into rolling data centers that stream location-tagged yield, moisture, and protein metrics to cloud dashboards. Deere’s 2025 SmartPan integration delivers grain-quality analytics before the truck reaches the elevator, locking operators into its ecosystem. Regulatory drivers such as the Environmental Protection Agency (EPA) nutrient-management rules in the Chesapeake Bay and Great Lakes regions heighten demand for traceable agronomic data. Embedded analytics also support variable-rate fertilizer planning, closing the loop between harvest and input application. These synergies intensify equipment stickiness, raise switching costs, and underpin long-run growth for the North America combine harvesters market.

Government Subsidies and Preferential Financing

Government subsidies and preferential financing measures help farmers afford high-cost equipment amidst labor shortages, large-scale farming operations, and the increasing adoption of precision agriculture. Federal climate-smart agriculture programs in the United States continued supporting lower-emission farming practices across major crop regions in 2024, while financing and leasing programs from providers such as AgDirect and CNH Industrial N.V. helped reduce upfront equipment costs for advanced harvesting machinery. These initiatives have contributed to reducing post-harvest losses and aligning with sustainability goals in the region.

Original Equipment Manufacturer (OEM) Subscription-Based Autonomous Software Upgrades

Software upgrade paths enable semi-autonomous functionalities without requiring the purchase of new machinery, separating feature adoption from capital investment cycles. At Commodity Classic 2026 in San Antonio, John Deere unveiled updates to its high-horsepower 8 Series tractors, new technology packages for X9 and S7 combines, and enhancements to its planter lineup. Adoption of these advancements is most prominent in the Corn Belt and well-connected Prairie regions, which benefit from reliable broadband infrastructure. This approach aligns with broader trends in the automotive and heavy equipment industries, where post-sale digital features play a key role in fostering brand loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital costs for advanced combines | -0.8% | United States small and mid-size farms, and Mexico nationwide | Short term (≤2 years) |

| Commodity-price volatility impacting farm cash flow | -0.7% | Corn Belt and Plains in the United States, Canadian Prairies | Medium term (2-4 years) |

| Semiconductor and hydraulic component supply-chain constraints | -0.4% | Manufacturing hubs in the United States, import-dependent Canadian regions | Short term (≤2 years) |

| Rural connectivity gaps limiting real-time telematics | -0.3% | Northern Plains, Appalachia, remote Prairies, and rural Mexico | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Costs for Advanced Combines

High upfront capital costs for advanced combine harvesters significantly constrain the North America combine harvesters market, particularly impacting small and medium-sized farms, which constitute 90% of farming operations in the United States. AGCO Corporation reported approximately USD 2.5 billion in net sales in Q3 2024, reflecting a year-over-year decline amid weaker agricultural equipment demand as growers delayed machinery purchases because of tighter farm margins[2]Source: AGCO Corporation, “Q3 2024 Earnings Release,” agcocorp.com. Smaller operators increasingly favor used units or seasonal rentals, lengthening upgrade cycles. In Mexico, the average farm size is below 500 acres, rendering new machines uneconomical without cooperative models that are still nascent. This trend underscores the growing importance of alternative ownership models, such as equipment sharing and leasing, to address the economic constraints faced by smaller farming operations in the region.

Rural Connectivity Gaps Limiting Real-Time Telematics

Real-time yield mapping and over-the-air updates require robust cellular or satellite links, which large swaths of North Dakota, Montana, and other remote Prairie regions still lack. Deere & Company JDLink Boost combines cellular and satellite connectivity to maintain machine data coverage in remote farming regions, although customers may face additional hardware and service costs depending on configuration and dealer packages. Farmers in coverage gaps must export data by USB drive, undermining the value proposition for premium telematics. National broadband initiatives are underway, but network buildouts extend into the next decade, dampening technology adoption in areas with thin coverage. This limitation is projected to continue until rural broadband infrastructure is expanded. Federal programs in both the United States and Canada are working to accelerate this process, it is anticipated to take several years to complete.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rotary Dominance and Rapid Tracked Adoption

Rotary combines led the largest segment, with 65% of the North America combine harvesters market share in 2025, owing to superior throughput in high-moisture corn. Conventional straw-walker models persist in drier wheat belts, but their share erodes as acreage tilts toward corn and soybeans. Hybrid architectures, championed by AGCO’s Gleaner line, capture a small niche among custom harvesters that need multi-crop flexibility. Rotary dominance will remain intact, but the competitive narrative is shifting toward platform versatility, with Original Equipment Manufacturer (OEM) adding quick-attach axle kits that let growers convert between wheels and tracks in under four hours.

Tracked combines are the fastest-growing, forecast to post the fastest 7.8% CAGR through 2026 to 2031, outpacing all other product types as wetter autumns shorten harvest windows and soil-compaction risk climbs. Rising demand for tracks comes primarily from North Dakota, Minnesota, and eastern Canada, where clay soils saturate quickly. Larger contact patches lower ground pressure, preserving soil tilth for spring planting. Operators also value higher resale prices for tracked units, narrowing total cost-of-ownership gaps with wheeled alternatives.

By Power Class: Mid-Range Workhorses and High-End Speed Demons

The 300 to 400 HP segment accounted for the largest share, 48% of the North America combine harvesters market in 2025. Reflecting their suitability for 2,000 to 5,000-acre farms, balancing fuel efficiency with 12-row corn head capacity. This segment holds a significant position in the North America combine harvesters market, as it corresponds to the standard acreage range within the Corn Belt. The concentration of corn and soybean production in this region underscores the segment's critical role in meeting agricultural needs.

The segment above 400 HP is the fastest-growing, advancing at a 6.9% CAGR from 2026 to 2031, driven by consolidation among mega-farms that value speed over fuel burn. Case IH Axial-Flow 9250 and CLAAS LEXION 8000 series combines represent the premium end of the market, pairing high-capacity grain tanks with advanced harvest automation and residue-management systems. Integrating cutting-edge technologies, such as GPS-guided automation and real-time yield monitoring, enhances this segment's appeal to large-scale farming operations seeking to maximize productivity and profitability.

Geography Analysis

The United States is the largest country, with 68% of the North America combine harvesters market share in 2025, but unit volumes fell sharply as farmers swapped multiple aged combines for fewer high-tech models. Association of Equipment Manufacturers (AEM) reported only 2,275 combines sold year-to-date August 2025, down 42.1% from the prior period[3]Source: Association of Equipment Manufacturers, “Combine Sales Flash August 2025,” aem.org. Despite lower unit volumes, average selling prices climbed, illustrating the technology pivot defining the North America combine harvesters market. Iowa, Illinois, and Nebraska remain core because their contiguous fields exceed 400 acres, enabling high-horsepower models to operate at peak productivity.

Canada is the fastest-growing country set to expand at a 6.3% CAGR from 2026 to 2031, as Saskatchewan, Alberta, and Manitoba leverage interest-free loans under the Advance Payments Program and a temporarily higher AgriStability coverage rate. The combine harvesters market in Canada benefits significantly from the extensive prairie regions in Alberta and Saskatchewan, which are crucial for wheat and barley production. Over 60% of grain farmers in these areas utilize combine harvesters, with increasing demand for advanced models featuring GPS and automation technologies.

In Mexico, the market is expanding due to increased mechanization in maize harvesting. Mexico remains marginal because average farm size sits below 500 acres and few fiscal incentives offset purchase prices exceeding USD 500,000. Import duties on used equipment and limited cooperative ownership structures restrict access to modern combines. Unless land consolidation accelerates or federal subsidies are introduced, Mexico’s contribution to the North America combine harvesters market will hover near low single digits through 2031.

Competitive Landscape

North America combine harvesters market remained highly consolidated in 2025, with the top five original equipment manufacturers (OEMs) accounting for the majority of revenue. Deere & Company leads the market, followed by CNH Industrial N.V., AGCO Corporation, CLAAS KGaA mbH, and Kubota Corporation. These companies dominate the market due to their established brand presence, extensive dealer networks, and consistent investment in research and development. This dynamic presents growth opportunities for precision-agriculture software vendors and aftermarket telematics providers, who can integrate their solutions with existing equipment to offer value-added services that enhance operational efficiency and productivity for end users.

Strategic trends indicate a shift toward subscription-based software revenue models, as manufacturers transition from one-time equipment sales to recurring digital services to foster customer retention within their ecosystems. This reflects a broader industry trend toward digital transformation, where data-driven insights and connectivity are central to improving equipment performance and customer satisfaction. For instance, Deere & Company’s partnership with Bushel Plus in late 2025 expanded real-time harvest analytics and combine optimization capabilities by integrating SmartPan grain-loss measurement technology into Deere’s connected harvesting ecosystem.

Growth opportunities are particularly evident in tracked-combine innovation and high-horsepower platforms exceeding 500 horsepower, where demand is currently outpacing supply. These segments are gaining traction as farmers seek equipment capable of managing larger-scale operations and challenging field conditions. Tracked combines offer improved traction and reduced soil compaction, making them especially suitable for regions with wet or uneven terrain. Similarly, high-horsepower platforms enhance efficiency in covering large acreages, addressing the needs of commercial-scale farming operations. Technology adoption remains a critical competitive advantage, with manufacturers focusing on advancements such as over-the-air software updates, machine-vision weed detection, and autonomous grain-cart coordination. These innovations improve equipment functionality while reducing operational downtime and labor costs.

North America Combine Harvesters Industry Leaders

AGCO Corporation

CLAAS KGaA mbH

Kubota Corporation

Deere & Company

CNH Industrial N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Deere & Company introduced the S7 Series combines, incorporating Predictive Speed Automation and Harvest Settings Automation to enhance harvesting efficiency. Announced at the Commodity Classic in Houston, Texas, this launch is focused on the United States market and targets large-scale producers.

- September 2024: CNH Industrial N.V. (New Holland) revealed its CR10 combine harvester at the Farm Progress Show in Boone, Iowa, United States. The CR10 is powered by a 12.9-litre FPT Cursor 13 engine delivering 635 horsepower. It is equipped with a 455-bushel grain tank and offers a grain unload rate of 4.5 bushels per second, ensuring high efficiency during peak harvest periods.

- May 2024: CLAAS KGaA mbH introduced the Axial-Flow 260 series combine harvester in Wisconsin. This model features integrated technology that does not require a subscription, including Harvest Command automation, Pro 1200 Dual Displays, and the ActiveTrac four-roller hydraulic suspended track system. These features are designed to minimize soil compaction, enhance grain quality, and improve operational efficiency.

North America Combine Harvesters Market Report Scope

Combine harvesters are multifunctional agricultural machines designed to efficiently reap, thresh, winnow, and clean grain crops such as wheat, corn, soybeans, barley, and rice in a single operation. North America Combine Harvesters Market Report is Segmented by Product Type (Conventional Straw-Walker Combines, Rotary Combines, Hybrid Combines, and Tracked Combines), by Power Class (Below 200 HP, 200 To 300 HP, 300 To 400 HP, and Above 400 HP), by Country (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional Straw-Walker Combines |

| Rotary Combines |

| Hybrid Combines |

| Tracked Combines |

| Below 200 HP |

| 200 to 300 HP |

| 300 to 400 HP |

| Above 400 HP |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Conventional Straw-Walker Combines |

| Rotary Combines | |

| Hybrid Combines | |

| Tracked Combines | |

| By Power Class | Below 200 HP |

| 200 to 300 HP | |

| 300 to 400 HP | |

| Above 400 HP | |

| By Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North America combine harvesters’ market in value terms in 2026?

The market is projected to reach USD 4.9 billion by 2031.

What is the projected CAGR for combine harvesters in North America between 2026 and 2031?

The market is projected to grow at a 2.6% CAGR over the period in 2026- to 2031, reflecting steady replacement demand and rising technology content.

Which product type holds the majority revenue share?

Rotary combines led with 65% of regional revenue in 2025 due to their high-throughput performance in corn and soybean operations.

Which geographic market is forecast to grow the fastest?

Canada is projected to post a 6.3% CAGR through 2031, supported by interest-free financing and strong canola economics.

Page last updated on: