United States Combine Harvesters Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

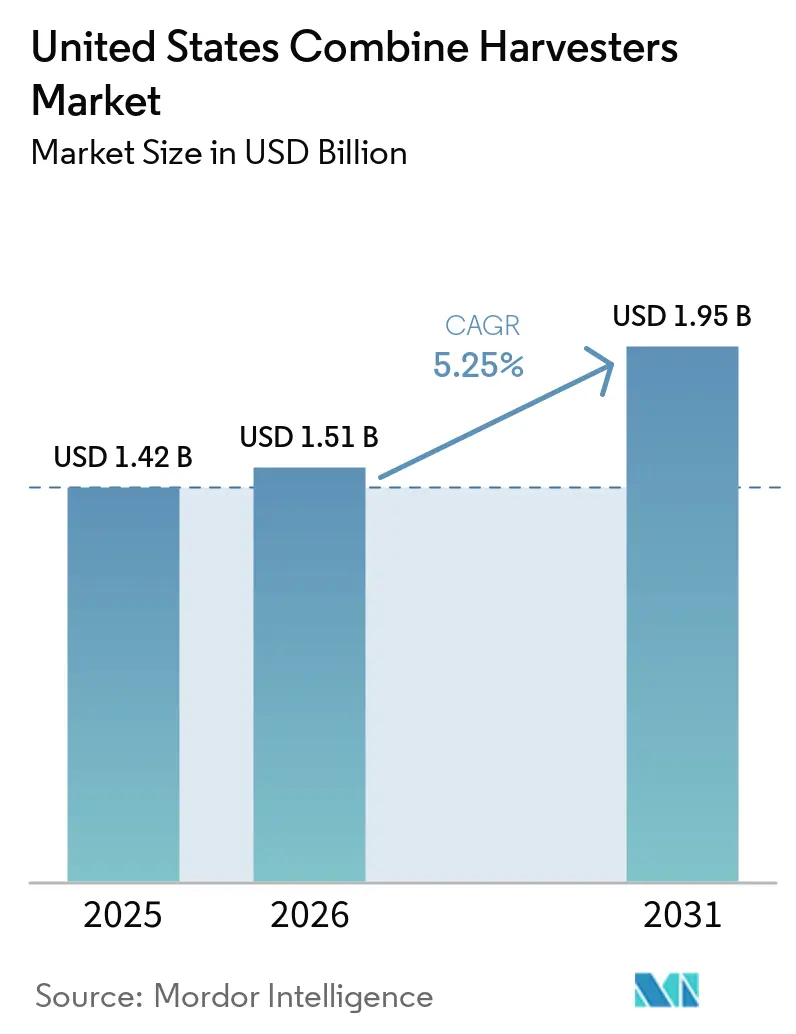

| Base Year Market Size (2025) | USD 1.42 Billion |

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 1.95 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

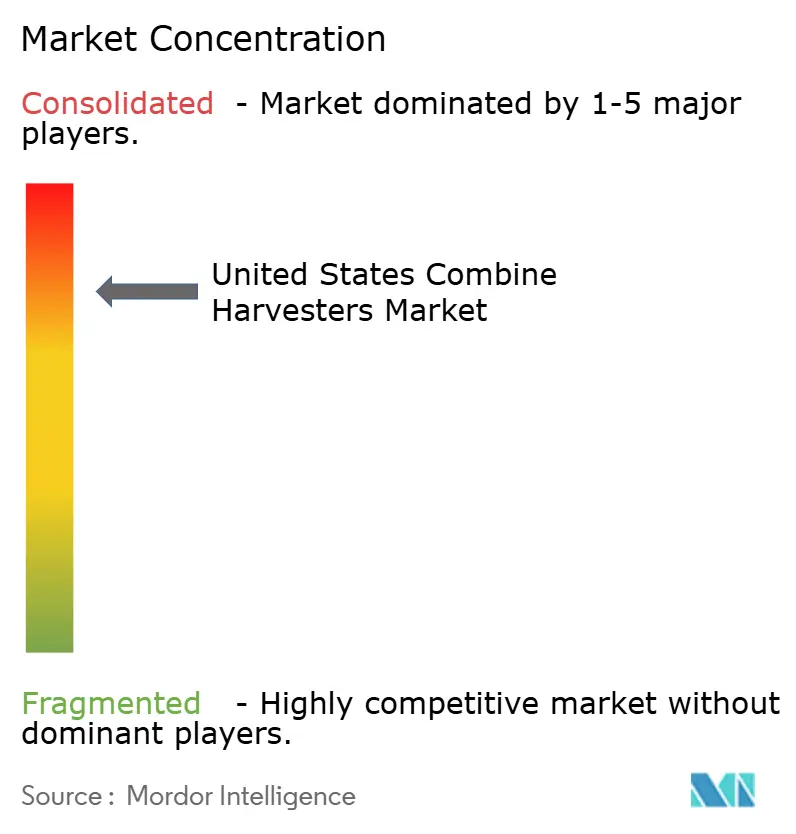

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Combine Harvesters Market Analysis by Mordor Intelligence

The United States combine harvesters market size was valued at USD 1.42 billion in 2025 and is estimated to grow from USD 1.51 billion in 2026 to reach USD 1.95 billion by 2031, at a CAGR of 5.25% during the forecast period (2026-2031). Weaker farm incomes and higher borrowing costs reduced unit sales in 2024 and 2025. However, replacement demand driven by an aging fleet of Class VII to IX harvesters and the growing adoption of autonomous retrofit technologies continues to support market growth. Mid-capacity self-propelled harvesters remain prevalent on medium-sized farms, while large-scale farms are increasingly adopting high-horsepower models compatible with wider headers[1]Source: United States Department of Agriculture, National Agricultural Statistics Service, “Acreage,” USDA, nass.usda.gov. Factors such as industry consolidation, tariff exposure, and right-to-repair regulations are impacting pricing and competition. Additionally, the integration of cloud-based analytics and software-enabled services is shifting competition toward connected farming ecosystems.

Key Report Takeaways

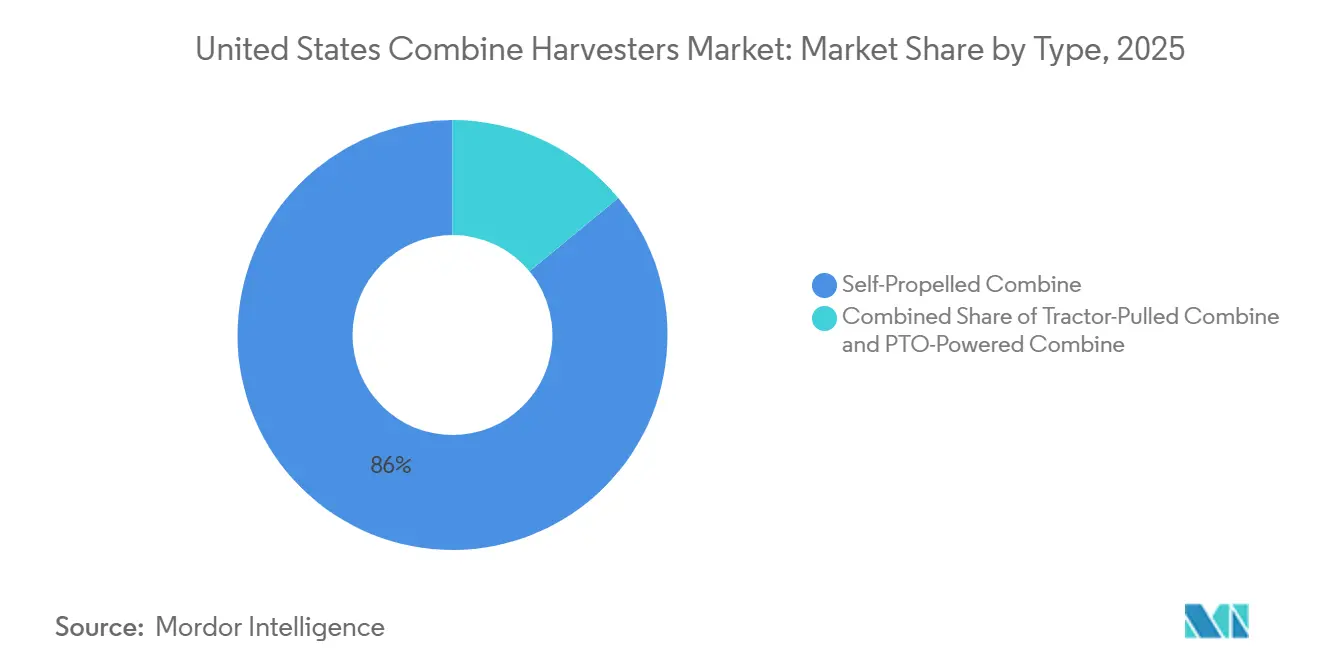

- By type, self-propelled combines held the largest share of the United States combine harvesters market size at 86.0% in 2025, while the PTO-powered combine harvesters segment is projected to record the fastest CAGR of 12.4% during 2026–2031.

- By power output, the 301-450 horsepower segment held the largest market share, 48.6% in the United States combine harvesters market in 2025, whereas the above 450 horsepower segment is projected to grow at the fastest CAGR of 9.6% during 2026 to 2031.

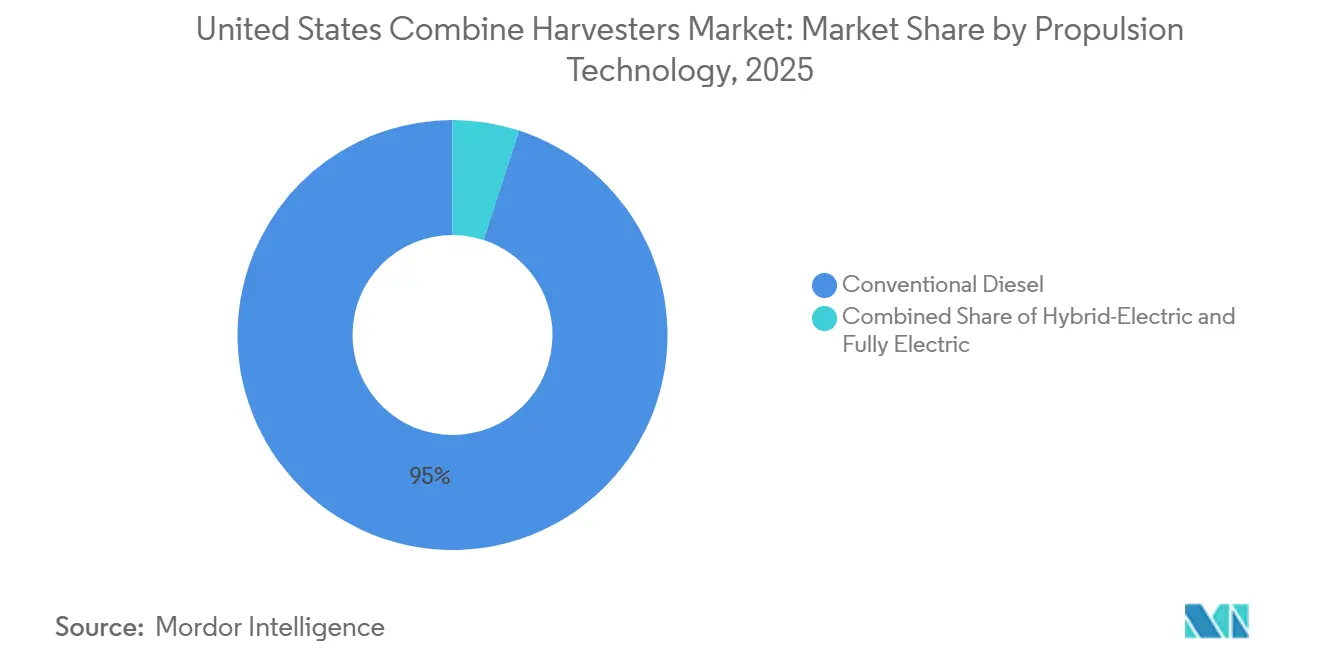

- By propulsion technology, the conventional diesel segment accounted for the largest United States combine harvesters market share of 95.0% in 2025, while the hybrid-electric segment is projected to register the fastest CAGR of 12.3% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Combine Harvesters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased replacement demand for aging Class VII to IX fleets | +2.10% | Midwest and Northern Plains | Medium term (2–4 years) |

| Rising corn and soybean acreage incentivizing mechanization | +1.30% | Nationwide, concentrated in Midwest and Delta South | Short term (≤ 2 years) |

| OEM financing programs lowering up-front cost barriers | +0.90% | Nationwide, highest uptake in Midwest and Plains | Short term (≤ 2 years) |

| Tax incentives under Section 179 for farm equipment | +0.80% | Nationwide, benefits farms with taxable income | Short term (≤ 2 years) |

| Autonomous guidance retrofits on flagship models | +0.70% | Midwest, California specialty crops, and early adopters in Plains | Medium term (2–4 years) |

| Carbon-credit premiums for residue-balancing harvesting | +0.40% | Midwest corn belt and selected conservation programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Replacement Demand for Aging Class VII to IX fleets

The average combine harvester in the United States is aging, with many Class VII to IX units purchased during the previous commodity upcycle now nearing replacement thresholds. As machine usage hours increase, repair and maintenance costs rise significantly, while resale values for older, high-hour equipment decline sharply. This creates pressure for fleet replacement. Additionally, deferred purchases caused by recent supply chain disruptions and higher equipment prices have further extended ownership cycles. The adoption of precision agriculture is also accelerating replacement demand, as upgrading older combines with advanced sensors and connectivity systems is often less cost-effective than investing in newer, technology-enabled machines. These factors collectively contribute to a sustained replacement cycle, supporting long-term market value growth despite a gradual recovery in unit sales[2]Source: Gary Schnitkey, Nick Paulson, Carl Zulauf, and Bradley Zwilling, “The U.S. Farm Machinery and Equipment Market: Sales, Inventories, and Tariff Headwinds,” farmdoc daily, farmdocdaily.illinois.edu.

Rising Corn and Soybean Acreage Incentivizing Mechanization

Growers are anticipated to plant 95.3 million acres of corn and 84.7 million acres of soybeans in 2026, shifting toward soybeans as profitability signals change. States such as Iowa, South Dakota, and Wisconsin are increasing soybean acres while reducing corn, a pattern that drives demand for combines able to switch quickly between crops and handle flexible 40- to 45-foot draper heads. Additionally, about 94% of corn and 96% of soybeans harvested in 2025 used biotech varieties, raising yields and compressing harvest windows. Shorter harvest periods heighten the value of high-capacity machines and autonomous grain-cart systems that cut downtime. The acreage mix, therefore, pulls forward purchases of mid- to high-horsepower models equipped for dual-header packages within the United States combine harvesters market.

OEM Financing Programs Lowering Up-Front Cost Barriers

Captive finance programs have offered significantly lower interest rates on new combines for the 2025 and early 2026 model years compared to prevailing market rates, enhancing equipment affordability for farmers. Over extended financing periods, the resulting savings can help offset the cost of additional attachments or precision agriculture upgrades. Deferred-payment structures further align cash outflows with post-harvest revenues, thereby supporting liquidity for mid-sized farming operations. Additionally, financing packages increasingly include telematics and connectivity subscriptions, which are driving the adoption of digital farming technologies and widening the technological gap between new and aging fleets in the United States combine harvesters market. However, the continuation of these financing incentives is contingent on manufacturers’ financial stability, particularly in the face of tariff-related margin pressures.

Carbon-Credit Premiums for Residue-Balancing Harvesting

Carbon programs are anticipated to pay about USD 6 to USD 10 per acre for documented low-disturbance harvest practices. Combines equipped with radar-based residue spreaders or settings automation help operators meet verification rules without manual intervention. For a 2,000-acre farm, annual carbon payments can equal the incremental cost of residue-control features when amortized over five years. Manufacturers are integrating these tools into flagship models in anticipation of wider carbon markets, adding a modest but growing pull factor on purchasing decisions in the United States combine harvesters market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in commodity crop prices affecting purchase cycles | -1.40% | Nationwide, acute in Midwest corn and soybean belt | Short term (≤ 2 years) |

| High initial capital cost versus custom-harvesting alternatives | -0.90% | Nationwide, most pronounced for farms below 2,000 acres | Medium term (2–4 years) |

| Shortage of skilled operators for advanced machines | -0.60% | Nationwide, concentrated in Midwest and Plains | Medium term (2–4 years) |

| Right-to-repair legislative uncertainty impacting OEM margins | -0.50% | Nationwide, with state-level variation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Commodity Crop Prices Affecting Purchase Cycles

Fluctuations in corn and soybean futures during 2024-2025 significantly compressed farm margins, leading to delays in equipment upgrades within the United States combine harvesters market. The Creighton Rural Mainstreet Index remained below the growth-neutral threshold through early 2026, indicating persistent weakness in the rural economy and restricted financing conditions for machinery investments. Industry data also shows a sharp decline in combine shipments during 2024, with continued weakness in 2025. This underscores the market's sensitivity to commodity price volatility and declining grower confidence. Consequently, many operators are extending equipment ownership cycles until market conditions stabilize, resulting in cyclical demand patterns and inventory management challenges for manufacturers.

High Initial Capital Cost Versus Custom-Harvesting Alternatives

High initial ownership and operating costs associated with self-propelled combines continue to prompt smaller farms to explore custom-harvesting alternatives and cooperative ownership models. Industry analyses suggest that ownership becomes economically viable primarily for farms exceeding approximately 1,900–2,000 acres, while smaller operators may find outsourced harvesting more cost-effective in certain scenarios[3]Source: Oklahoma State University Extension, “Machinery Ownership versus Custom Harvest,” Oklahoma State University Extension, extension.okstate.edu. However, reliance on third-party harvesting contractors can lead to scheduling delays and operational risks during narrow harvest windows. This factor continues to drive replacement demand for owned combines among medium-sized farming operations in the United States combine harvesters market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Self-Propelled Dominance Masks PTO-Powered Resurgence

Self-propelled combines accounted for about 86.0% of the United States combine harvesters market share in 2025. This dominance is attributed to their widespread adoption on large-scale row-crop farms, where they enhance harvesting efficiency and reduce operational time. In contrast, the PTO-powered segment is anticipated to exhibit the fastest CAGR of 12.4% from 2026 to 2031. This growth is driven by increasing demand from organic farms, specialty-crop producers, and cooperative ownership models that prioritize lower capital investment and operating costs.

Manufacturers are enhancing self-propelled combine offerings by incorporating higher-capacity grain handling systems, automation technologies, and productivity-focused upgrades to improve efficiency during narrow crop windows. Meanwhile, PTO-powered combines are gaining traction due to their lower purchase costs and compatibility with existing tractor infrastructure. Additionally, this segment benefits from reduced reliance on subscription-based digital ecosystems and telematics platforms. However, challenges such as lower throughput capacity and limited header compatibility continue to hinder the adoption of PTO-powered combines in large commercial farming operations within the United States combine harvesters market.

By Power Output: Ultra-High Horsepower Gains Traction Among Mega-Farms

Combines rated at 301 - 450 horsepower represented the largest segment of the United States combine harvesters market size, accounting for 48.6% of the total market in 2025. This dominance is attributed to their strong adoption among medium-to-large farms, which require a balance between harvesting capacity, transport flexibility, and operating efficiency. In contrast, combines above 450 horsepower are projected to grow at the fastest CAGR of 9.6% from 2026 to 2031, driven by the increasing consolidation of large-scale farming operations and the rising demand for higher field productivity.

The 301 - 450 horsepower segment remains widely preferred due to its compatibility with large harvesting platforms while maintaining manageable transport requirements and ownership costs. Additionally, strong dealer support networks and higher residual values continue to encourage adoption across commercial farming operations. Meanwhile, combines above 450 horsepower are gaining traction among mega-farms that prioritize greater labor efficiency, reduced harvesting time, and improved fuel productivity per acre. Advancements in automation, satellite connectivity, and machine synchronization technologies are further driving the adoption of ultra-high horsepower combines, despite transportation and regulatory challenges in certain regions.

By Propulsion Technology: Hybrid-Electric Combines Gain Momentum Amid Sustainability Focus

Conventional diesel combines accounted for the largest share of the United States combine harvesters market size in 2025, representing about 95.0% of the total market. This dominance is attributed to their widespread adoption on large commercial farms, driven by proven field reliability, extensive refueling infrastructure, high harvesting endurance, and strong compatibility with existing farm machinery. In contrast, hybrid-electric combines are projected to grow at the fastest CAGR of 12.3% from 2026 to 2031. This growth is fueled by increasing investments by OEMs in fuel-efficient harvesting technologies and a growing emphasis on reducing operating costs and emissions in large-scale farming operations.

The conventional diesel segment remains the preferred propulsion technology due to its established dealer support networks, availability of high horsepower, and suitability for long-duration harvesting operations in key crop-producing regions such as corn, soybean, and wheat. Additionally, lower technology risks and the widespread availability of replacement parts contribute to fleet retention among commercial growers. On the other hand, hybrid-electric combines are gaining traction as manufacturers expand pilot deployments and incorporate advanced power management, automation, and precision farming technologies to enhance fuel efficiency and harvesting productivity. Fully electric combines are projected to remain in the early stages of commercialization during the forecast period, primarily due to limited battery range, challenges with charging infrastructure, and the high power demands of large-scale harvesting applications.

Geography Analysis

The Midwest accounted for the largest share of the United States combine harvesters market in 2025, supported by Iowa, Illinois, Nebraska, Minnesota, and South Dakota contributing a combined corn and soybean acreage of roughly 60 million acres in 2025. The region’s concentration of large commercial farms continues to support the adoption of Class 8 and Class 9 combines equipped with precision agriculture technologies, autosteering, and connected diagnostics. Ongoing automation trials and strong dealer networks are further strengthening the Midwest’s position as a key center for innovation, aftermarket services, and financing activity in the United States combine harvesters market.

The South is projected to grow at the fastest rate during 2026-2031, supported by rising soybean acreage in Arkansas in 2026 and a 4% increase in national cotton plantings, which reached 9.64 million acres in 2025, primarily across Mississippi, Louisiana, and the Delta region. Increasing multi-crop cultivation and residue-management requirements are encouraging the adoption of mid-capacity combines with flexible harvesting platforms. Smaller and fragmented farm structures also continue supporting demand for custom harvesting and lower-cost equipment alternatives across the region.

In the West, Great Plains wheat states continue favoring high-capacity combines for large-scale harvesting operations, while California and Washington show stronger demand for compact machines suited for orchards and vineyards. Labor shortages, drought variability, and rising operational complexity are accelerating interest in remote diagnostics, automation, and connected harvesting technologies. Regional crop patterns, farm sizes, and operational requirements continue shaping diverse demand trends across the United States combine harvesters market.

Competitive Landscape

The United States combine harvesters market is highly consolidated, with a few major manufacturers dominating industry revenue. Deere & Company holds a prominent position, supported by its extensive dealer network, financing capabilities, and a growing portfolio of subscription-based digital farming solutions. However, rising tariff-related costs are creating pricing pressures across the industry, prompting manufacturers to focus on software- and service-based revenue streams that are less affected by raw material price fluctuations.

CNH Industrial N.V. remains competitive by offering higher-capacity harvesting systems and advanced crop-residue management technologies. Meanwhile, Claas KGaA mbH and AGCO Corporation emphasize differentiated technologies, including grain-quality monitoring, automation, and precision harvesting solutions. Additionally, technology-focused companies are creating opportunities for retrofitting and upgrading older fleets with brand-agnostic precision agriculture systems, enabling farmers to modernize equipment without the need for full machine replacements.

Regulatory changes, particularly those related to right-to-repair policies, are projected to impact aftermarket service models. These developments are likely to drive a greater emphasis on open digital platforms and secure diagnostics. Concurrently, leading manufacturers are increasingly competing by offering integrated digital ecosystems that combine fleet analytics, connectivity, and precision farming tools. These strategies aim to enhance long-term customer retention within the United States combine harvesters market.

United States Combine Harvesters Industry Leaders

Deere & Company

CNH Industrial N.V.

AGCO Corporation

Claas KGaA mbH

Kubota Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Deere & Company expanded automation capabilities in Model Year 2027 combines, adding Green Crop Detection, Predictive Ground Speed Automation, and advanced harvesting automation features to improve harvesting efficiency and reduce operator workload in the United States combine harvesters market.

- May 2026: Iowa HF 2763 is a proposed right-to-repair law that would allow farmers and independent repair shops to access the software, tools, and parts needed to repair combine harvesters, which could significantly change the agricultural machinery service market in the United States.

- March 2025: AGCO Corporation and Trimble’s PTx Trimble OutRun autonomous grain-cart retrofit received the Davidson Prize, highlighting increasing adoption of automation and autonomous harvesting technologies across large-scale farming operations.

United States Combine Harvesters Market Report Scope

A combine harvester, commonly known as a combine, is a large agricultural machine used to harvest grain and seed crops. It combines multiple harvesting operations in a single process, including reaping, threshing, and cleaning, thereby improving harvesting efficiency and reducing labor requirements.

The United States Combine Harvesters Market Report is segmented by type, including self-propelled combine, tractor-pulled combine, and PTO-powered combine, by power output including less than 150 HP, 151–300 HP, 301–450 HP, and above 450 HP, and by propulsion technology including conventional diesel, hybrid-electric, and fully electric. The market forecasts are provided in terms of value (USD).

| Self-Propelled Combine |

| Tractor-Pulled Combine |

| PTO-Powered Combine |

| Less Than 150 HP |

| 151 - 300 HP |

| 301 - 450 HP |

| Above 450 HP |

| Conventional Diesel |

| Hybrid-Electric |

| Fully Electric |

| By Type | Self-Propelled Combine |

| Tractor-Pulled Combine | |

| PTO-Powered Combine | |

| By Power Output | Less Than 150 HP |

| 151 - 300 HP | |

| 301 - 450 HP | |

| Above 450 HP | |

| By Propulsion Technology | Conventional Diesel |

| Hybrid-Electric | |

| Fully Electric |

Key Questions Answered in the Report

How large is the United States combine harvesters market today and where is it headed by 2031?

The United States combine harvesters market size is estimated to be USD 1.51 billion in 2026 and is projected to reach USD 1.95 billion by 2031, growing at a 5.25% CAGR over 2026-2031.

Which horsepower class sells the most new combines?

Models rated at 301–450 horsepower captured 48.6% of 2025 sales, making this mid-range class the most popular choice for 2,000- to 3,500-acre grain farms.

What segment of the combine harvester type is forecast to expand at the fastest through 2031?

PTO-powered combines are projected to record a 12.4% CAGR as organic and specialty-crop growers look for lower-cost, tractor-driven solutions.

How concentrated is supplier power among manufacturers?

The United States combine harvesters market remains highly concentrated, with a few major brands holding dominant market positions, strengthening supplier pricing power while increasing antitrust and right-to-repair scrutiny.

Page last updated on: