North America Collagen-Based Supplement Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

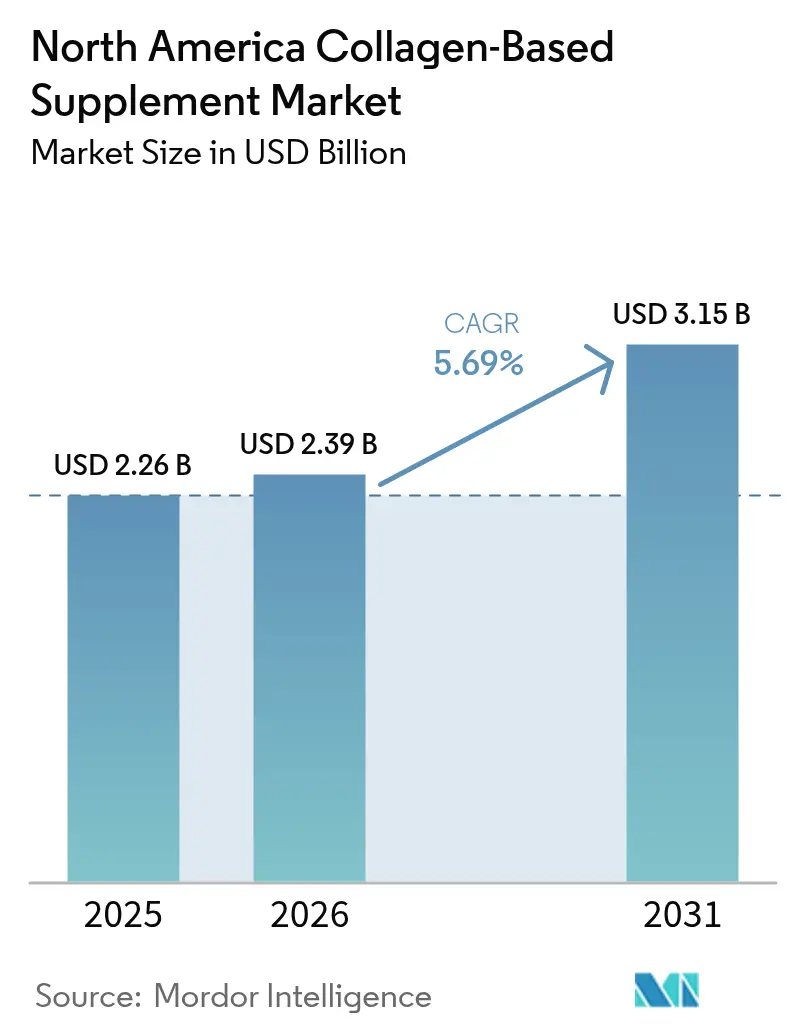

| Base Year Market Size (2025) | USD 2.26 Billion |

| Market Size (2026) | USD 2.39 Billion |

| Market Size (2031) | USD 3.15 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

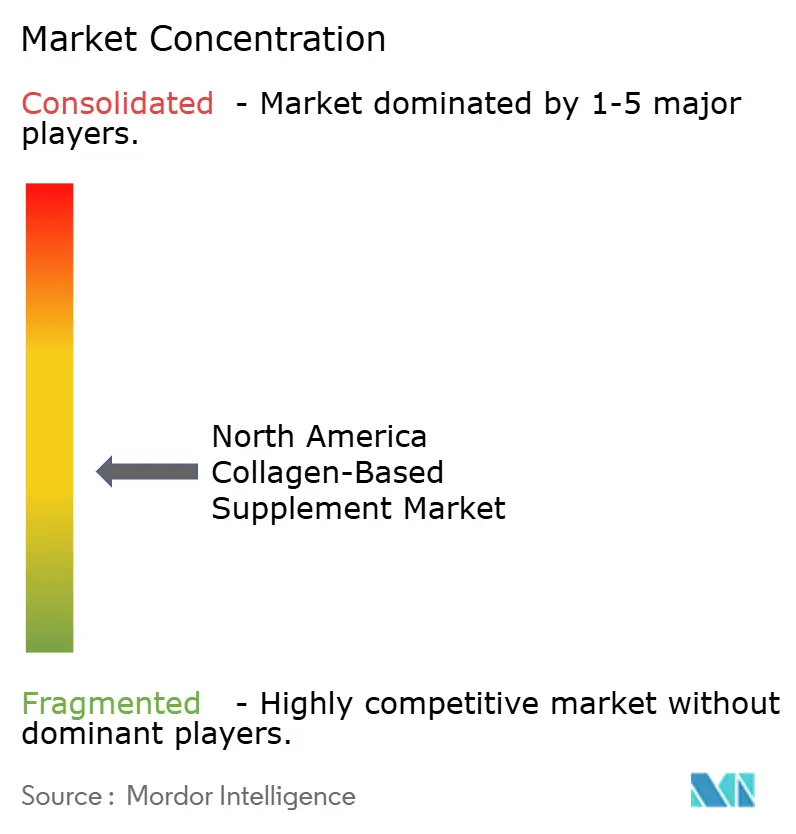

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Collagen-Based Supplement Market Analysis by Mordor Intelligence

North America collagen-based supplement market size in 2026 is estimated at USD 2.39 billion, growing from 2025 value of USD 2.26 billion with 2031 projections showing USD 3.15 billion, growing at 5.69% CAGR over 2026-2031. This growth is driven by increasing consumer awareness about the benefits of collagen in maintaining skin elasticity, improving joint health, and supporting connective tissue. More people are adopting proactive health and wellness routines, which has significantly boosted the demand for collagen supplements. The market is also benefiting from endorsements by dermatologists, widespread promotion on social media platforms, and ongoing clinical research that validates the effectiveness of collagen. Product development in the market is focusing on creating more consumer-friendly options, such as flavored gummies, marine-sourced collagen peptides with eco-friendly credentials, and subscription-based e-commerce models that offer convenience. The North American collagen-based supplement market remains highly fragmented, with numerous players competing to capture market share.

Key Report Takeaways

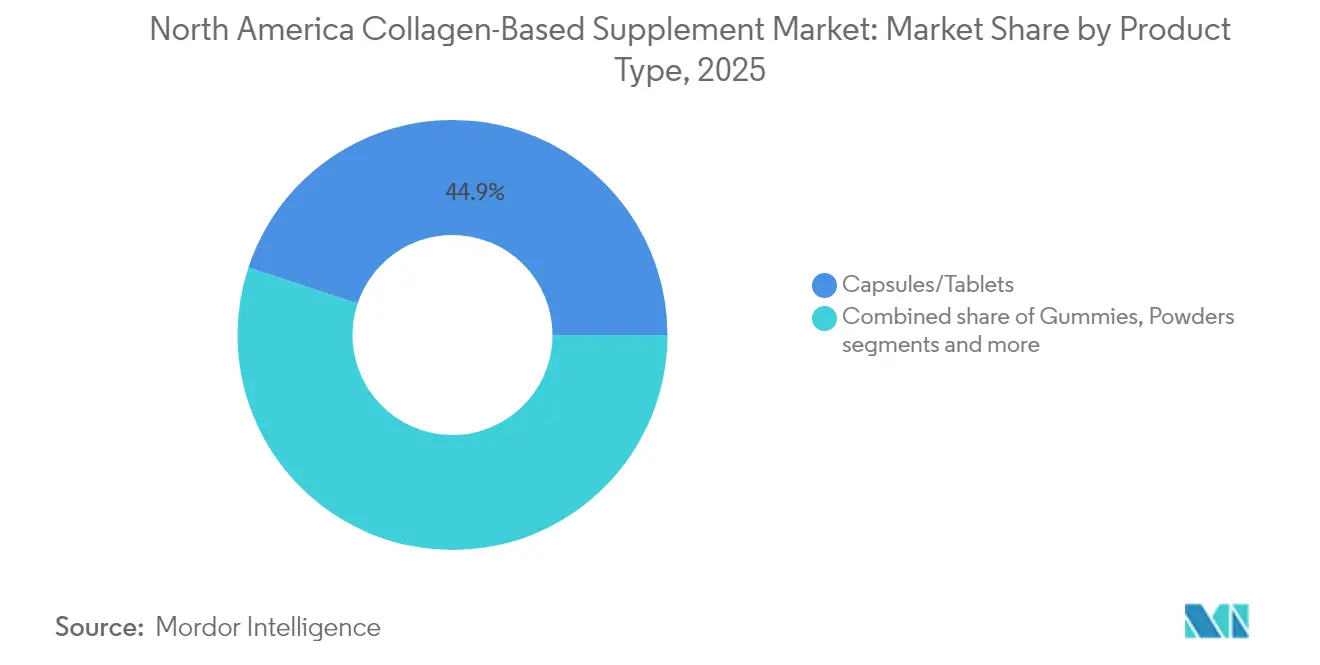

- By product type, capsules/tablets held 44.92% of the North American collagen-based supplement market share in 2025, while gummies are projected to post the fastest growth rate of 8.12% through 2031.

- By source, animal-based collagen accounted for 77.94% of the North American collagen-based supplement market size in 2025; however, marine variants are poised to grow at a 7.25% CAGR from 2026 to 2031.

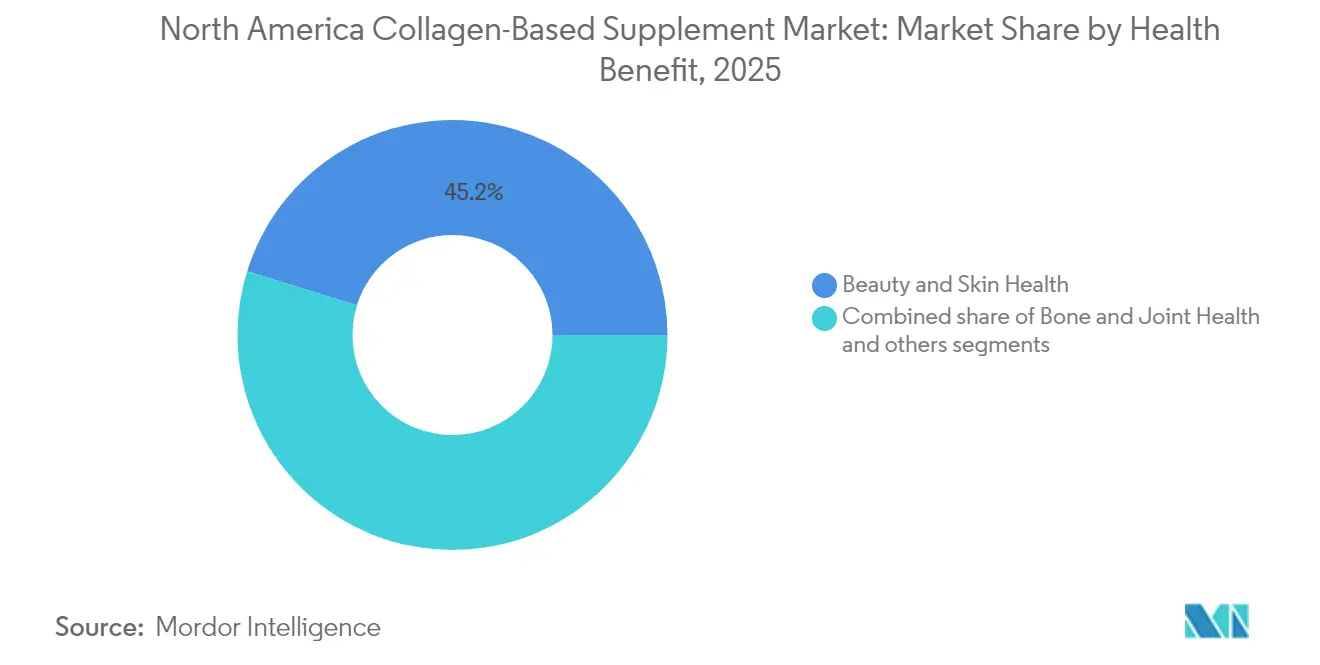

- By health benefit, beauty and skin health led with a 45.21% revenue share in 2025; bone and joint health is expected to expand at an 8.03% CAGR through 2031.

- By distribution channel, drugstores and pharmacies captured a 35.32% share in 2025, while online retail stores recorded the highest 8.31% CAGR through 2031.

- By geography, the United States commanded 84.62% of the North American collagen-based supplement market in 2025; Mexico is the fastest-growing territory, with an 8.33% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Collagen-Based Supplement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of beauty-from-within products | +1.2% | United States, Canada, with spillover to Mexico urban centers | Medium term (2-4 years) |

| Rising prevalence of joint disorders, osteoarthritis, and mobility issues | +1.0% | North America-wide, concentrated in aging United States and Canadian populations | Long term (≥ 4 years) |

| Higher adoption of collagen supplements among millennials and Gen Z | +0.9% | United States and Canada, early gains in Mexico City and Monterrey | Short term (≤ 2 years) |

| Expansion of active lifestyle and sports nutrition trends | +0.8% | United States and Canada, with emerging traction in Mexico | Medium term (2-4 years) |

| Growing demand for clean label and minimally processed ingredients | +0.7% | United States and Canada, regulatory influence from Food and Drug Administration and Health Canada | Medium term (2-4 years) |

| Rising influence of social media, wellness influencers, and dermatologist-led education | +0.6% | United States and Canada, with digital penetration accelerating in Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of joint disorders, osteoarthritis, and mobility issues

The North America collagen-based supplement market is growing significantly due to the rising number of joint-related health issues. According to the Centers for Disease Control and Prevention, approximately 33 million adults in the United States were living with osteoarthritis in 2024[1]Source: Centers for Disease Control and Prevention, "Osteoarthritis", cdc.gov. This growing prevalence is driving older consumers to look for ways to support joint health and reduce reliance on long-term nonsteroidal anti-inflammatory drug (NSAID) use. As a result, there is increasing demand for Type II collagen, which is known for its benefits in protecting cartilage. Products that combine collagen with other ingredients, such as glucosamine, chondroitin, and hyaluronic acid, are gaining popularity. These multi-ingredient formulations address mobility concerns and are particularly appealing to consumers focused on maintaining joint and bone health. This trend is causing collagen products targeting joint health to grow at a faster rate compared to those focused solely on beauty benefits in the region.

Growing adoption of beauty-from-within products

The increasing popularity of "beauty from within" products is driving growth in the collagen supplement market. Dermatologists and aestheticians are now recommending these supplements as a complement to topical skincare routines, shifting the focus from purely cosmetic benefits to scientifically supported skin health. According to PubMed Central, the usage of dietary supplements reached 61.4% in 2023, indicating a growing acceptance of ingestible wellness solutions among consumers[2]Source: PubMed Central, "Trends in dietary supplement use among U.S. Adults", pubmed.ncbi.nlm.nih.gov. Social media plays a significant role, as beauty-related content featuring collagen supplements trends across platforms. Brands that back their products with peer-reviewed studies and collaborate with dermatologists can charge premium prices and avoid the risks of market commoditization. Adoption is particularly strong in urban areas, where wellness-focused lifestyles and higher disposable incomes are more prevalent.

Rising influence of social media and dermatologist-led education

The growing role of social media and dermatologist-led education is significantly boosting the demand for collagen supplements. Online platforms have made it easier for consumers to access expert advice, clinical research, and product recommendations, empowering them to make informed decisions. According to the World Bank, 93% of the United States population uses the internet, and many people now turn to digital platforms to verify the effectiveness of ingredients and compare brands[3]Source: World Bank, "Individuals using the Internet (% of population) - United States", data.worldbank.org. Companies that combine scientific evidence with relatable content from influencers are successfully building trust and encouraging more consumers to try their products. This strategy creates a positive cycle where trusted information leads to increased purchases and brand loyalty. As social media algorithms become more complex and unpredictable, brands are shifting their focus away from relying solely on paid advertisements.

Expansion of active lifestyle and sports nutrition trends

The growing focus on active lifestyles and sports nutrition is driving demand for collagen supplements, as more people incorporate these products into their routines to support joint health, tissue repair, and overall fitness. According to the Sports and Fitness Industry Association, around 80% of Americans, or approximately 247.1 million people, participated in at least one physical activity in 2024[4]Source: Sports and Fitness Industry Association, "SFIA’s Topline Participation Report Shows 247.1 Million Americans Were Active in 2024", sfia.org. This increase in active individuals has expanded the potential market for supplements that enhance performance and recovery. Many recreational athletes now incorporate collagen into their post-workout routines to support the recovery of tendons, ligaments, and muscles. Retailers like GNC and The Vitamin Shoppe play a crucial role in promoting these products by offering knowledgeable staff and product sampling, which helps build consumer trust.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising competition from alternative beauty-from-within ingredients | -0.8% | United States and Canada, with emerging competition in Mexico | Medium term (2-4 years) |

| Concerns about animal-derived sourcing limiting uptake among vegans | -0.5% | United States and Canada, concentrated in urban coastal markets | Short term (≤ 2 years) |

| Potential allergen issues associated with marine and bovine sources | -0.3% | North America-wide, regulatory influence from Food and Drug Administration allergen labeling | Long term (≥ 4 years) |

| Environmental regulations on fishing and livestock byproducts | -0.2% | United States and Canada, with tightening standards from MSC and United States Department of Agriculture | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising competition from alternative beauty-from-within ingredients

Competition from alternative ingredients in the beauty-from-within segment is slowing the growth of collagen supplements. Consumers are increasingly turning to options like ceramides, hyaluronic acid, and biotin, which offer similar benefits for skin and hair health. Ceramides are particularly appealing as they support skin barrier repair without relying on animal-based sources, making them a preferred choice for many. Hyaluronic acid is also gaining traction among formulators due to its ability to provide visible hydration benefits even at low doses. As these alternatives become more popular and close the perceived effectiveness gap with collagen, brands are under pressure to differentiate their products. To stay competitive, collagen companies are combining their products with complementary active ingredients, highlighting clinically proven bioavailability, and emphasizing superior absorption rates.

Concerns about animal-derived sourcing limiting vegan uptake

Concerns about animal-derived sourcing are limiting the adoption of collagen supplements among vegan consumers, as many are unwilling to use products made from bovine or marine peptides. Although some startups are working on developing animal-free collagen using precision fermentation, these solutions are not yet commercially viable due to high production costs and scalability challenges. As a temporary alternative, brands are offering “collagen-boosting” amino acid blends to attract vegan buyers. However, these blends often lack the same level of scientific backing as traditional collagen hydrolysates, which reduces their appeal. This situation presents a dilemma for companies. They must decide whether to invest heavily in research and development for fermentation-based collagen or risk losing access to the growing vegan consumer base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gummies Capture Younger Demographics

Capsules and tablets were the most commonly used format in the North America collagen-based supplement market in 2025, accounting for 44.92% of total sales. Their widespread use is due to their affordability, easy availability, and the trust consumers have in traditional pill forms. These formats are convenient for daily use as they offer stable formulations and precise dosing, making them a practical choice for many. Consumers, particularly those shopping in mass-market and specialty retail stores, continue to rely on capsules and tablets as a dependable way to meet their collagen needs.

Gummies are anticipated to be the fastest-growing format, with a projected CAGR of 8.12% between 2026 and 2031. This growth is driven by improvements in gummy formulations, such as the use of pectin, which enhances texture and taste, making them more appealing to consumers. Marketing efforts through influencers and engaging social media campaigns have significantly boosted awareness and encouraged more people to try gummies. These products are especially popular among younger consumers who value their convenience, enjoyable flavors, and the fun, easy way they offer to incorporate collagen into their daily routines.

By Source: Marine Collagen Gains on Sustainability and Bioavailability

Animal by-products, such as animal-derived peptides, dominated the North America collagen market in 2025, accounting for 77.94% of the market share. This stronghold is largely due to the well-established bovine supply chains, which ensure reliable sourcing, cost efficiency, and scalability for mass production. Animal-based collagen, particularly Types I, II, and III, is highly versatile and widely used in skincare, joint health, and sports nutrition products. These factors make it the preferred choice for manufacturers and consumers, offering consistent quality and affordability.

On the other hand, marine collagen is expected to grow at the fastest rate, with a projected CAGR of 7.25% from 2026 to 2031. This growth is driven by a rising preference for sustainable and eco-friendly products, as marine collagen is derived from fish and aligns with these values. Advances in production methods are also helping to reduce costs, making it a more viable option compared to bovine collagen. With its premium image and appeal to eco-conscious consumers, marine collagen is steadily gaining popularity as a preferred alternative in the market.

By Health Benefit: Bone and Joint Health Accelerates

In 2025, beauty and skin health applications were the top contributors to market revenue, accounting for 45.21% of the total market share. Collagen has become a popular ingredient in cosmetic and anti-aging products because it helps improve skin elasticity, hydration and reduces wrinkles. Consumers trust these products due to strong endorsements from dermatologists and promotions by influencers. The premium branding of collagen-based beauty products, along with their inclusion in daily skincare routines, has further driven their demand in this segment.

The bone and joint health segment is expected to grow at the fastest rate, with a projected CAGR of 8.03% through 2031. This growth is primarily driven by the aging Baby Boomer population and the increasing prevalence of osteoarthritis, creating a need for products that support joint mobility and cartilage health. Many consumers are now opting for collagen-based supplements as a natural alternative to traditional medications like NSAIDs for long-term joint care. This trend underscores the increasing significance of collagen in preventive healthcare and its growing appeal among older adults and health-conscious individuals.

By Distribution Channel: E-Commerce Disrupts Pharmacy Dominance

Traditional drugstores and pharmacies were the leading sales channels for collagen supplements in 2025, contributing 35.32% of the total sales in North America. These stores are popular due to their trusted reputation, convenient locations, and strategic shelf placement, which encourages both planned and impulse purchases. They also offer a wide range of well-known brands and ensure consistent product availability, which builds customer trust. For many consumers, drugstores remain the most reliable and accessible option for purchasing collagen supplements.

Online retail is anticipated to grow at the fastest pace, with a projected CAGR of 8.31% through 2031. E-commerce platforms attract customers by offering personalized product bundles, subscription services, and automatic replenishment options, making it easier for consumers to maintain their purchases. Mobile-friendly checkouts and targeted social media advertising help online retailers reach younger, tech-savvy audiences. This combination of convenience, customization, and effective digital marketing makes online retail the most dynamic and rapidly growing channel in the collagen supplement market.

Geography Analysis

The United States led the North America collagen-based supplement market in 2025, holding an 84.62% market share. This dominance is supported by the Dietary Supplement Health and Education Act regulations, which simplify the process of launching new products. In contrast, Canada follows with a smaller share due to its stricter Natural Health Product requirements. However, these regulations allow brands to position themselves as premium offerings. Within the United States, cities like Los Angeles and New York show the highest adoption rates, while in Canada, regions such as Ontario and British Columbia see growth driven by clean-label products available in pharmacies.

Mexico is expected to experience the fastest growth in the region, with a projected CAGR of 8.33% from 2026 to 2031. This growth is fueled by a rising middle class, increasing awareness of beauty and wellness products, and the growing popularity of e-commerce in cities like Mexico City, Monterrey, and Guadalajara. Meanwhile, the United States market is likely to grow at a slower pace as it becomes more saturated and competition intensifies. Canada is anticipated to maintain steady growth, supported by its focus on high-quality, regulated products. These varying growth patterns highlight the need for brands to adapt their strategies to each country’s unique market conditions.

Smaller markets in the Caribbean and Central America are still in the early stages but show significant potential. As disposable incomes rise and wellness trends spread to these regions, they offer opportunities for companies willing to navigate challenges like fragmented retail channels and evolving regulations. Businesses that invest in creating Spanish-language content, obtaining region-specific certifications, and collaborating with local e-commerce platforms are well-positioned to capitalize on these emerging markets. Over the next decade, these regions could become valuable contributors to the overall market.

Competitive Landscape

The North American collagen-based supplement market is moderately fragmented, with the top five brands holding less than half of the total market share. Established companies, such as Nestlé’s Vital Proteins, Gelita, and Glanbia, utilize their robust distribution networks and diverse raw material sources to maintain their market position. On the other hand, smaller brands like Sports Research and BUBS Naturals focus on direct-to-consumer sales, subscription models, and influencer marketing to gain traction. These brands compete by emphasizing sustainable sourcing, innovative product formats like gummies and drink mixes, and scientific evidence to differentiate themselves from basic commodity products.

On the supply side, key ingredient providers such as Gelita, Rousselot, and Nitta Gelatin play a crucial role by controlling the quality and specifications of collagen peptides. Their vertically integrated operations make it challenging for smaller brands to compete, as they often lack the purchasing power or long-term contracts needed to secure consistent raw material supplies. Meanwhile, biotech startups are exploring the production of animal-free collagen through precision fermentation; however, challenges such as high costs, unclear regulations, and consumer acceptance have delayed large-scale commercialization. Suppliers with certifications like Marine Stewardship Council or grass-fed bovine sourcing are gaining an edge as sustainability becomes a priority in the industry.

For success in this market, brands must focus on omnichannel strategies that connect online discovery with in-store purchases and repeat sales. Companies that invest in customer data, personalized product bundles, and retention strategies can reduce costs and increase customer loyalty. However, rising advertising costs on platforms like Amazon and competition from private-label products are putting pressure on profit margins. To stand out, brands need to offer unique clinical benefits or patented production methods. This creates an environment where smaller, agile companies with transparent supply chains, strong scientific backing, and effective marketing can compete with larger global players.

North America Collagen-Based Supplement Industry Leaders

-

Amway Corp.

-

Gelita AG

-

Perfect Supplements

-

Nestlé SA

-

Great Lakes Wellness

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: QUIRIS Healthcare introduced Elasten, a leading collagen supplement from Germany, to the United States market, which gained significant recognition for its effectiveness in promoting skin health and overall wellness.

- November 2025: AFT Pharmaceuticals introduced its complete range of Lipo-Sachets products to the United States market. This product line included two advanced collagen formulations, the Age Repair Lipo-Sachets formulation combined marine collagen peptides with essential nutrients such as Vitamins C, E, A, and Biotin.

- September 2025: The Australian brand, Chief Nutrition expanded its presence by introducing its best-selling collagen powder to the United States market. This launch marked a significant step in the brand's global growth strategy.

- July 2025: ArcticCollagen introduced a new marine collagen supplement to the market. The product featured 8,000 milligrams of hydrolyzed marine collagen, providing a significant source of lean protein with eight grams per serving.

North America Collagen-Based Supplement Market Report Scope

The North America collagen-based supplement market is segmented by product type, which includes capsules/tablets, powders, gummies, liquid/drink shots, and others. The market also includes sources that include animal-based and marine-based products. The report also provides a detailed analysis of health benefits that include beauty and skin health, bone and joint healt,h and others. The market also encompasses various distribution channels through which it is distributed across the region, including supermarkets/hypermarkets, drugstores and pharmacies, online retail stores, and others. The study also involves a detailed analysis of countries as the United States, Canada, Mexico, and the rest of North America.

| Capsules/Tablets |

| Powders |

| Gummies |

| Liquid/Drink Shots |

| Others |

| Marine-Based |

| Animal-Based |

| Beauty and Skin Health |

| Bone and Joint Health |

| Others |

| Supermarkets/Hypermarkets |

| Drugstores and Pharmacies |

| Online Retail Stores |

| Others |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Capsules/Tablets |

| Powders | |

| Gummies | |

| Liquid/Drink Shots | |

| Others | |

| By Source | Marine-Based |

| Animal-Based | |

| By Health Benefit | Beauty and Skin Health |

| Bone and Joint Health | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Drugstores and Pharmacies | |

| Online Retail Stores | |

| Others | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North America collagen-based supplement market in 2026?

The market stands at USD 2.39 billion in 2026 and is projected to reach USD 3.15 billion by 2031.

Which product format is growing fastest?

Gummies lead with an 8.12% compound growth rate through 2031 owing to taste, convenience, and visual appeal.

Which health benefit segment is expanding most rapidly?

Bone and joint health applications post an 8.03% CAGR, fueled by aging demographics and osteoarthritis prevalence.

What distribution channel shows the highest growth momentum?

Online retail, especially direct-to-consumer websites and marketplaces, is rising at an 8.31% CAGR through 2031.

Page last updated on: