Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.75 Billion |

| Market Size (2031) | USD 5.82 Billion |

| Growth Rate (2026 - 2031) | 9.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

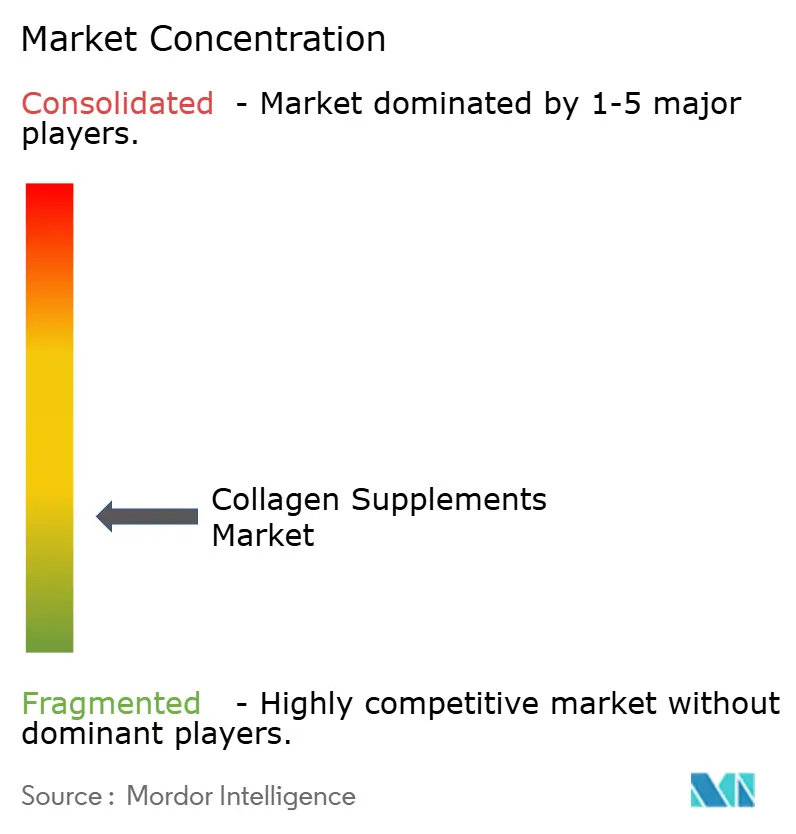

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Collagen Supplements Market Analysis by Mordor Intelligence

The collagen supplements market size was valued at USD 3.43 billion in 2025 and is estimated to grow from USD 3.75 billion in 2026 to USD 5.82 billion by 2031, at a CAGR of 9.20% during the forecast period (2026-2031). The market is primarily driven by increasing demand from older adults seeking solutions for joint health, mobility, and age-related bone density issues, while younger consumers are increasingly drawn to these supplements for skin elasticity, hair strength, and nail health. Advancements in fermentation techniques and tripeptide extraction technologies are revolutionizing product development processes while reducing dependence on traditional animal-derived sources. The expansion of e-commerce platforms has transformed market dynamics, enabling smaller brands to bypass traditional retail barriers and directly reach consumers through digital channels. However, the market faces significant challenges, including the proliferation of counterfeit products, complex regulatory frameworks across different regions, and growing consumer concerns regarding the ethical sourcing and sustainability of animal-derived ingredients.

Key Report Takeaways

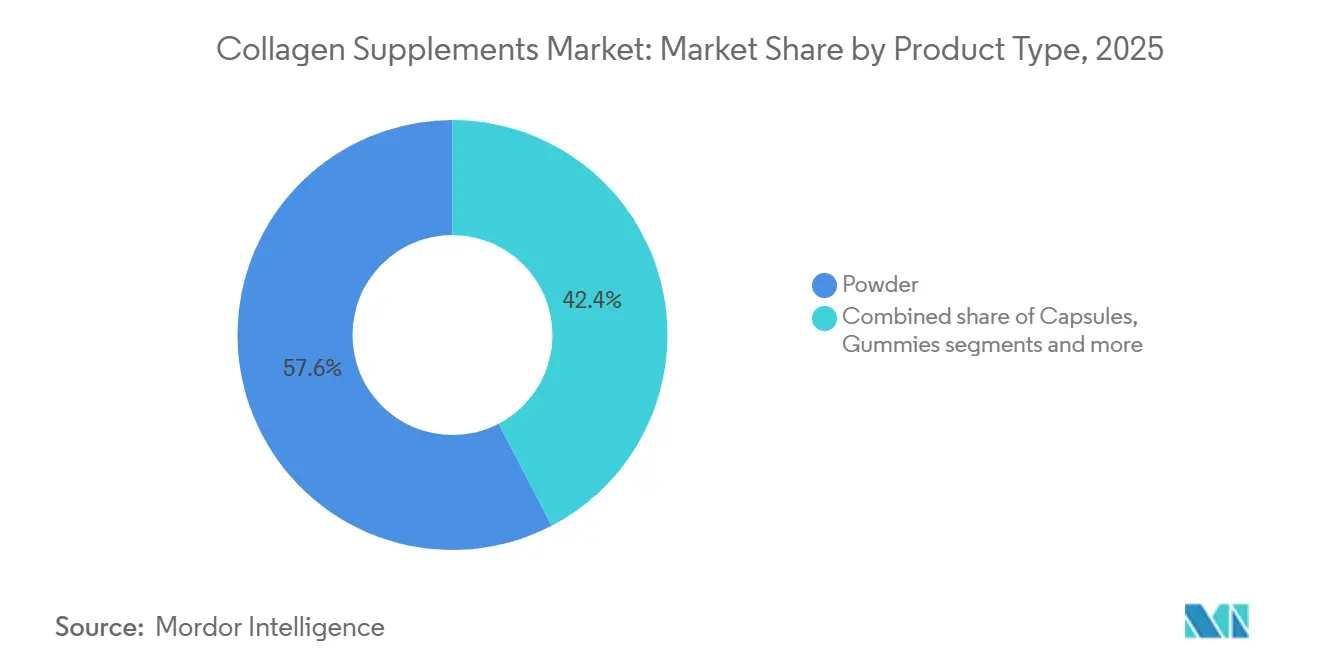

- By product type, powder held 57.64% of the collagen supplements market share in 2025; capsules and gummies are projected to grow at a 10.05% CAGR through 2031.

- By source, animal-based ingredients accounted for 85.52% of the collagen supplements market in 2025, while plant-based and fermentation-based formats are forecast to expand at a 11.47% CAGR to 2031.

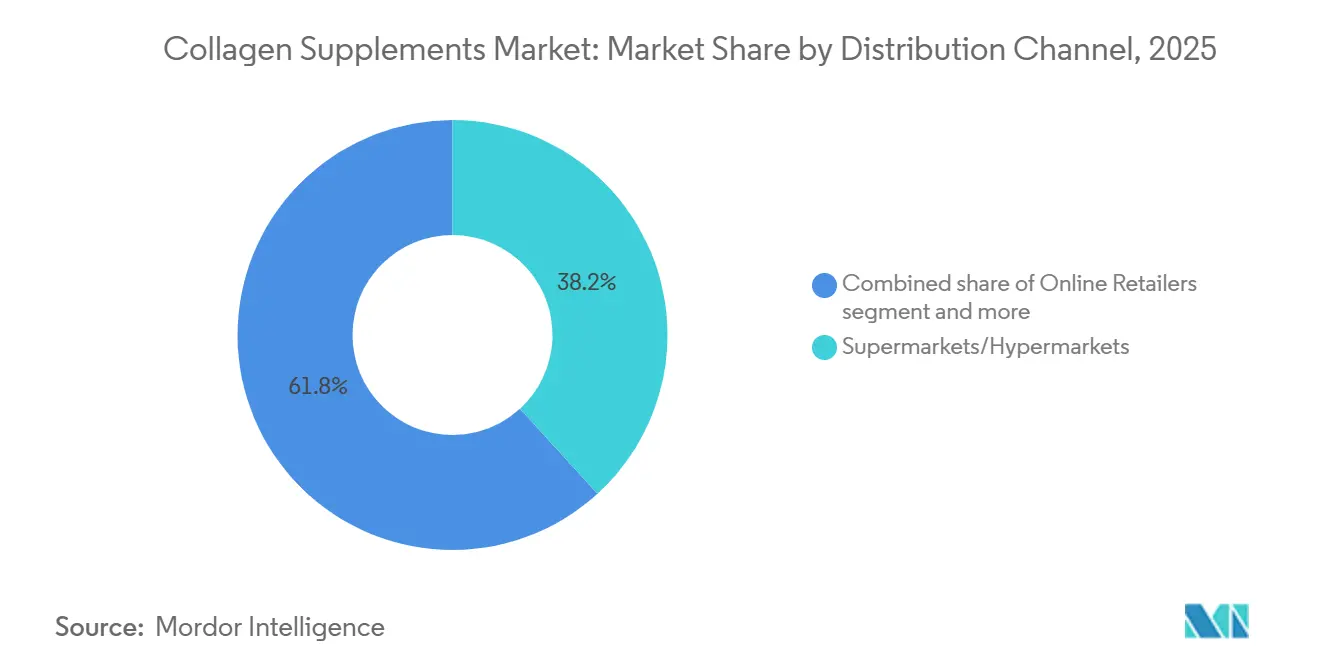

- By distribution channel, specialty and health stores commanded 38.21% revenue in 2025; online retailers will pace fastest at a 10.72% CAGR to 2031.

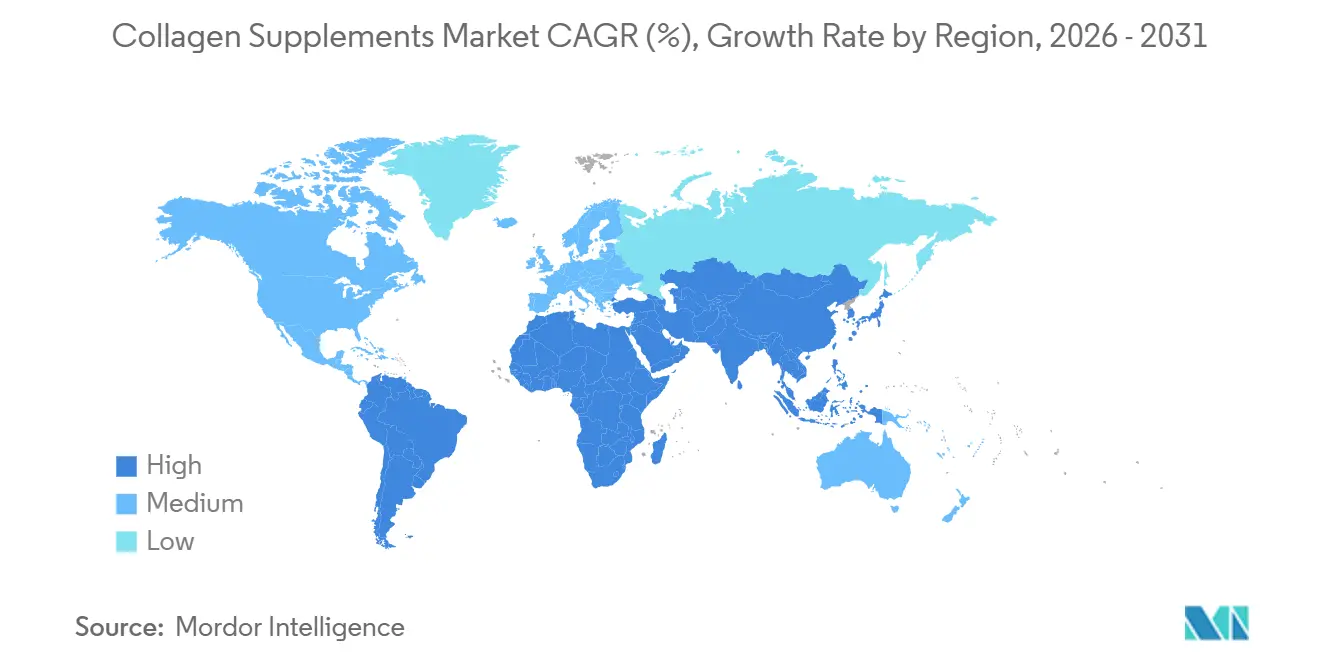

- By geography, North America accounted for 37.95% of revenue in 2025; Asia-Pacific is expected to deliver the highest regional CAGR of 11.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Collagen Supplements Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Elderly population demand for bone and joint support | +1.2% | North America; Europe; other ageing markets | Long term (≥ 4 years) |

| Beauty-from-within appeal to millennials | +0.9% | North America; Asia-Pacific | Medium term (2-4 years) |

| Expansion of health-conscious consumer base | +0.8% | Global | Medium term (2-4 years) |

| Advances in collagen extraction and formulation | +0.7% | North America; Europe | Long term (≥ 4 years) |

| Inclusion of collagen in functional foods and beverages | +0.6% | Asia-Pacific; Global | Medium term (2-4 years) |

| Growth of e-commerce and pharmacy distribution | +0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

The Surge in the Elderly Population Fuels Demand for Bone and Joint Support

The global senior population is driving the collagen supplements market. As of 2024, Eurostat reports Italy has the highest elderly population in Europe at 24.30% [1]Source: Eurostat, "Eurostat Data Browser," European Commission, ec.europa.eu. In Japan, 36.25 million people, or 29.3% of the population, are aged 65 and older, according to the Ministry of Internal Affairs and Communications. Seniors' purchasing power and focus on preventive healthcare have made collagen supplements key to healthy aging. Type I collagen hydrolysate improves joint function in osteoarthritis patients, reducing pain and enhancing mobility. Undenatured type II collagen decreases inflammation and pain with high patient compliance. Research highlights collagen's role in managing joint conditions and supporting cartilage health, boosting consumer trust. Companies offering traceable, clinically validated products with transparent sourcing are building loyalty among older consumers.

The Beauty-from-Within Trend Among Millennials Propels Market Growth

Young adults are shifting from topical skincare to ingestible supplements for holistic skin health. Clinical studies highlight that collagen supplements not only diminish wrinkles but also enhance skin hydration. Notably, marine-derived collagen boasts significantly higher bioavailability than its counterparts. Social media, with its before-and-after photo showcases, has been pivotal in driving this trend, especially for formats like gummies and ready-to-drink products. Millennials, already leading the charge, are bolstered by their growing purchasing power, hinting at a surge in long-term adoption of collagen supplements. This move towards "beauty-from-within" supplements resonates with the younger generation's holistic wellness pursuits, preventive healthcare mindset, and a penchant for innovative supplement formats. As a result, the market has broadened, drawing in health-conscious consumers from diverse age groups and backgrounds, far beyond traditional beauty segments.

The Expansion of the Health-Conscious Consumer Base Drives Market Growth

Collagen supplements, once limited to wellness enthusiasts, now attract mainstream consumers focused on preventive health. This shift aligns with the growing trend of proactive health management, heightened during the pandemic. Rising awareness of collagen's benefits for skin, joints, and muscle recovery has driven demand. Collagen products bridge beauty and health, appealing to diverse age groups and lifestyles. Increasing consumer focus on ingredient quality has boosted demand for premium options like marine collagen and plant-based alternatives, valued for sustainability and enhanced bioavailability. Broader retail distribution, scientific marketing, and innovative formats, such as functional beverages and nutrition bars, further support the market's growth.

Advancements in Collagen Extraction and Formulation Are Contributing to Market Innovation

Biotechnology innovations have transformed collagen production, replacing animal-derived sources with fermentation-based methods that retain bioidentical properties. These advancements address sustainability and regulatory requirements. Evonik's Vecollan, a fermentation-based collagen platform, operates commercially with enhanced performance and simplified regulatory approvals for medical and cosmetic uses. PlantForm Corporation's vivo XPRESS platform uses synthetic biology to produce bioidentical human collagen, meeting the growing demand for vegan alternatives.In October 2024, Glanbia Nutritionals launched Collameta, a collagen tripeptide ingredient within the broader collagen peptides category, with four times faster absorption and ten times higher efficacy than traditional peptides, requiring only 500 mg to 1 g daily. These developments enable manufacturers to create products with improved bioavailability, reduced dosing, and sustainable production methods while maintaining clinical efficacy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeits and mislabeling hinders growth | -0.8% | Global, with concentration in developing markets | Short term (≤ 2 years) |

| Regulatory framework and growing consumer ingredient consciousness | -0.6% | Global, strongest impact in North America and Europe | Medium term (2-4 years) |

| High production costs | -0.5% | Global | Medium term (2-4 years) |

| Sustainability concerns over animal source | -0.4% | Global, strongest in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeits and Mislabeling Hinders Growth

Counterfeit and mislabeled collagen supplements are eroding consumer trust and complicating regulatory enforcement, particularly in online channels where quality control is often lacking. The rise of e-commerce and global trade has made it harder for regulators to verify product authenticity. In 2024, the Philippine Food and Drug Administration (FDA) issued Advisory No.2024-1011, cautioning against unauthorized collagen-glutathione products, such as "Glutathione Collagen Glow" and "BEWORTHS Skin Whitening Capsule" [2]Source: Philippine Food and Drug Administration, “Public Health Warning on Mulittea Multi Collagen Capsule,” fda.gov.ph. These items, devoid of FDA registration, skipped essential safety and quality evaluations. The FDA urges consumers to check product registration on its Verification Portal before buying. Weak regulatory oversight has allowed inferior products into the market, tarnishing the reputations of legitimate manufacturers and stunting market growth due to rising consumer skepticism. In response, industry players are pushing for stricter enforcement and testing protocols to safeguard product integrity and ensure market stability.

Regulatory Framework and Growing Consumer Ingredient Consciousness

The collagen supplement market faces increasing regulatory requirements and consumer demands for transparency in ingredient sourcing and manufacturing processes. The FDA's March 2024 update to New Dietary Ingredient Notification Procedures has established clearer submission requirements for collagen supplements and other nutritional products [3]Source: Federal Register Office, “FDA Guidance on New Dietary Ingredient Notifications,” federalregister.gov. In Asian markets, regulatory frameworks vary significantly - Japan maintains strict documentation requirements for health claims through its functional food regulations, while other markets in the region have less stringent standards. Modern consumers now demand comprehensive information about ingredient sources, processing methods, and third-party testing before purchasing. Manufacturers must comply with Current Good Manufacturing Practices (CGMP) while ensuring supply chain transparency. This complex regulatory landscape benefits established companies with existing compliance systems but creates entry barriers for smaller manufacturers developing new formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Powder Dominance Faces Convenience Challenge

Powder formats accounted for 57.64% of the collagen supplements market size in 2025, primarily due to their cost-effectiveness per gram and flexible dosing capabilities. The high protein content achievable in a single drink particularly appeals to fitness enthusiasts and older adults with chronic joint conditions. However, capsules and gummies are emerging as convenient alternatives, with a projected CAGR of 10.05%. Manufacturers are incorporating sustained-release and low-dose tripeptides to deliver therapeutic quantities in compact capsules, balancing effectiveness with user convenience. While gummies attract new consumers who prefer flavored options over unflavored powder, health-conscious users carefully monitor their sugar content.

The market expansion includes ready-to-drink shots and effervescent sticks, providing portable options unavailable in powder form. To maintain a market presence, companies are developing multi-format product lines. Product innovation extends beyond format diversification into enhanced specifications. Advanced collagen tripeptides demonstrate four-fold faster bioavailability, enabling reduced serving sizes and minimizing product fatigue. Digital-first brands are transforming traditional bulk purchases into customized subscription services through stick-pack kits. The collagen supplements market's development is increasingly determined by the combination of convenience, personalization, and clinical validation.

By Source: Animal Dominance Meets Sustainability Disruption

Animal-based ingredients account for 85.52% of the collagen supplements market revenue in 2025. Bovine and marine peptides remain the primary market foundation, supported by extensive clinical documentation for dermal and joint health benefits. The established supply chains for cattle hide and fish skin continue to provide reliable raw material sources. Marine collagen offers broader religious dietary compliance and enhanced digestibility due to its lower-molecular-weight peptides.

Plant-based and fermentation-derived ingredients are growing at a 11.47% CAGR by 2031, emerging as the fastest-growing source category. This growth responds to increasing environmental and ethical concerns, particularly in European and North American markets, where consumers prioritize carbon footprint reduction and animal welfare. Microbial fermentation produces bioidentical collagen that meets quality standards while eliminating animal-derived ingredients. The market is also seeing development in algae-derived collagen precursors that stimulate natural collagen production, appealing to vegan consumers. However, high production costs present a significant challenge, as fermentation facilities require substantially higher capital investment than traditional processing plants. This results in higher retail prices. The segment is expected to gain increased market presence as production costs decrease and carbon-based regulations strengthen, potentially transforming the collagen supplements market's composition.

By Distribution Channel: Digital Transformation Accelerates

Specialty and health stores account for 38.21% of collagen supplement sales in 2025, maintaining their position as trusted advisors for complex supplement decisions. Store personnel provide guidance on dosage recommendations and complementary joint health products, creating customer loyalty, particularly among older consumers who prefer personal interactions. The online channel is projected to grow at a 10.72% CAGR, transforming the collagen supplements market through direct-to-consumer models that integrate automatic refills, social media partnerships, and educational content. Major e-commerce platforms implement third-party verification systems to address consumer concerns about product authenticity. Subscription models help maintain customer retention and lifetime value despite price competition online.

Supermarkets and hypermarkets serve as convenient access points for new consumers who incorporate collagen supplements into regular shopping routines. Pharmacies offer a clinical environment, particularly for collagen products combined with vitamin C, glucosamine, or hyaluronic acid that target joint health benefits. The market increasingly requires integration across all channels as consumers frequently research products online before making in-store purchases, or reverse this pattern. Success in the collagen supplements market depends on delivering consistent education, convenient purchasing options, and customer engagement across all distribution channels.

Geography Analysis

North America dominates the market with a 37.95% revenue share in 2025, supported by extensive supplement retail networks, including pharmacy chains, health food stores, and supermarkets. Stringent FDA regulations on supplement labeling and quality standards underpin the region's growth. Major retailers like GNC, Vitamin Shoppe, and Whole Foods Market maintain dedicated supplement sections, while e-commerce platforms offer subscription-based supplement delivery services. The region's slower growth rate compared to emerging markets has prompted companies to develop premium products featuring transparent ingredient sourcing and enhanced tripeptide formulations.

Asia-Pacific is experiencing rapid expansion with a 11.65% CAGR, driven by rising disposable incomes among middle-class consumers and widespread e-commerce adoption. Japan's sophisticated regulatory framework for functional foods enables manufacturers to make specific collagen dosage claims based on clinical evidence. China's beauty-focused consumer culture and South Korea's K-wellness product exports significantly contribute to regional market growth. Manufacturing capabilities in the region are expanding, exemplified by the Thai Union's USD 30 million investment in a marine collagen processing facility in Thailand's Samut Sakhon region in June 2025. This state-of-the-art facility, specializing in tuna skin collagen processing, will achieve an annual production capacity of 1,500 tonnes.

European consumers demonstrate a strong preference for sustainable and environmentally conscious collagen products, particularly favoring marine and fermentation-derived options with documented reduced carbon emissions. The region maintains comprehensive labeling requirements through EFSA regulations. The Middle East and Africa markets show promising development, supported by wellness trends among affluent expatriate communities and expanding pharmacy retail networks. South America, while representing a smaller market share, exhibits significant growth potential due to improving economic conditions and the influential role of social media in establishing collagen supplements as an accessible beauty and health solution.

Competitive Landscape

In the fragmented collagen supplements market, global giants and emerging players compete fiercely. Nestlé Health Science, a dominant player, utilizes influencer-led marketing and boasts a vast retail presence. Meanwhile, Shiseido, drawing on its skincare prowess, seamlessly integrates collagen into its holistic beauty offerings. Innovations such as gummies, powders, and functional beverages by regional players like Wellful, Inc., Suntory Holdings Limited, among others, have not only accelerated consumer adoption but also broadened the appeal of collagen.

Additionally, innovation continues to reshape the category. Fermentation-based solutions like Evonik’s Vecollan® offer sustainable, non-animal alternatives with faster regulatory pathways. Thai Union’s entry with ThalaCol marks a strategic diversification by seafood processors into high-value nutraceuticals. Meanwhile, Rousselot’s Nextida GC expands collagen’s functionality into metabolic health, aligning with demand for condition-specific formulations. These advancements are blurring the lines between wellness, medical nutrition, and beauty from within.

Strategic acquisitions and digital disruption are further intensifying competition. Wellful’s 2025 acquisition of Ancient Nutrition strengthens its footprint in the clean-label, functional nutrition space. Vector Consumer’s acquisition of Pura Collagen and the rise of digital-first brands with personalized offerings underscore a shift toward niche targeting. These tech-enabled entrants are gaining traction through AI-based assessments, transparent ingredient sourcing, and lab-tested claims, building trust with modern consumers and forcing legacy players to evolve.

Collagen Supplements Industry Leaders

-

Nestlé SA

-

Amorepacific Corp

-

Meiji Holdings Co.

-

Shiseido Co. Ltd.

-

WM Partners, LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Life Time, a health and wellness brand, has expanded its collagen-based product line. The company's LTH supplement division introduced the Refuel Protein Bar to meet the growing consumer demand for collagen products, which are known to support joint health, skin elasticity, and hair strength.

- February 2025: Revive Collagen, a British company, has expanded its operations to the United Arab Emirates through a partnership with GMG, the owner of Supercare. The liquid collagen brand's ready-to-drink marine collagen supplements are now available in more than 100 Supercare stores across Dubai and through online channels. GMG serves as the exclusive distributor for Revive Collagen products in the United Arab Emirates.

- January 2025: GNC launched its beauty supplement line, featuring Premier Collagen, which includes two supplement formulations designed to promote youthful-looking skin. The products contain marine and bovine collagen peptides engineered for rapid absorption.

- January 2025: Wild Nutrition, a Food-Grown supplement brand, has introduced Collagen 500 Plus, marking its first entry into the collagen product category. The product, available through Wild Nutrition's online platform, features two key ingredients: collagen peptides and Mesoporosil.

Global Collagen Supplements Market Report Scope

Collagen supplements contain amino acids, the building blocks of proteins and other additional nutrients. These supplements are associated with several health benefits, like increasing muscle mass, preventing bone loss, relieving joint pain, and improving skin health by reducing wrinkles and dryness. The collagen supplements market is segmented by form, source, distribution channel, and geography. For each segment, the market sizing and forecast have been done based on value (in USD million).

By Product Type

| Capsules |

| Gummies |

| Powders |

| Drinks and Liquid Shots |

| Other Product Types |

By Source

| Animal Based |

| Plant Based |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty and Health Stores |

| Online Retailers |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Capsules | |

| Gummies | ||

| Powders | ||

| Drinks and Liquid Shots | ||

| Other Product Types | ||

| By Source | Animal Based | |

| Plant Based | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty and Health Stores | ||

| Online Retailers | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the collagen supplements market?

The collagen supplements market stands at USD 6.28 billion in 2026 and is projected to reach USD 8.49 billion by 2031.

Which product form holds the largest share of the market?

Powder formulations lead with 57.64% of 2025 revenue, although capsules and gummies are growing faster at an 8.57% CAGR.

Which region is expanding the fastest?

Asia-Pacific is expected to grow at a 7.28% CAGR as its middle-class population and online retail infrastructure expand.

Why are marine and fermentation sources gaining popularity?

They address sustainability and religious considerations while offering smaller peptide sizes that improve absorption.

Page last updated on: