Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

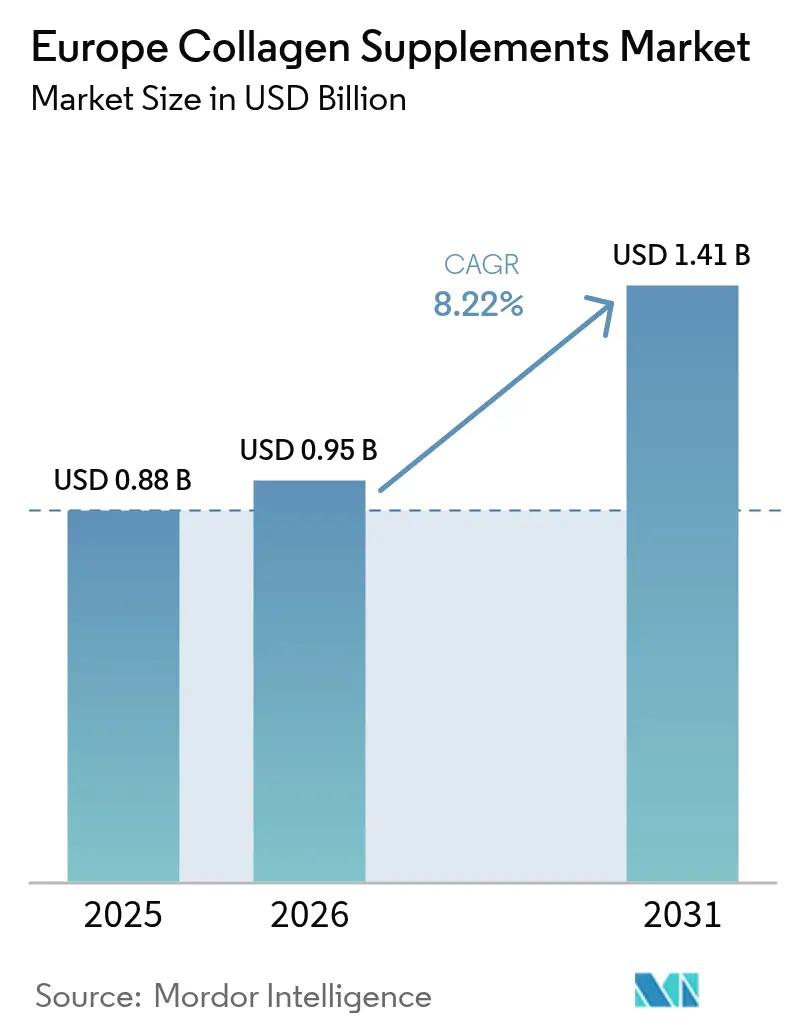

| Base Year Market Size (2025) | USD 0.88 Billion |

| Market Size (2026) | USD 0.95 Billion |

| Market Size (2031) | USD 1.41 Billion |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Collagen Supplements Market Analysis by Mordor Intelligence

The Europe collagen supplements market size is expected to grow from USD 0.88 billion in 2025 and USD 0.95 billion in 2026 to USD 1.41 billion by 2031, registering a CAGR of 8.22% between 2026 and 2031. This growth is driven by an aging population prioritizing preventive nutrition, increasing demand for clean-label products with transparent sourcing, and the expanding reach of e-commerce, which improves accessibility. While powder remains the dominant format, ready-to-drink (RTD) beverages are gaining popularity due to their convenience. Marine collagen is also witnessing increased demand, supported by its sustainability attributes, despite its higher cost. The "beauty-from-within" segment continues to account for more than half of the current demand, but the musculoskeletal health segment is growing at a faster rate, supported by accumulating clinical evidence. Germany's pharmacy-focused model ensures quality assurance, while the United Kingdom's subscription-driven online market fosters product trials and repeat purchases.

Key Report Takeaways

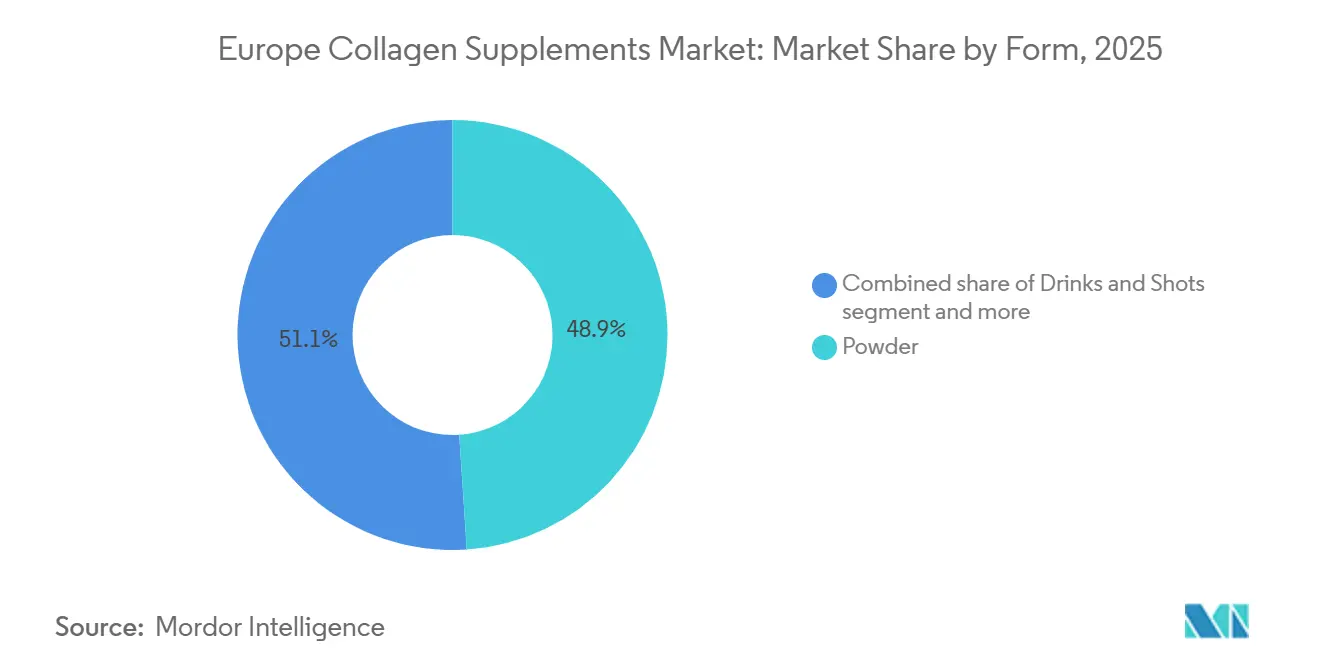

- By form, powders captured 48.94% of 2025 value, while drinks and shots are forecast to post a 9.93% CAGR through 2031.

- By source, animal-based collagen held 64.11% share in 2025, whereas marine-based variants are set to rise at a 9.56% CAGR, the top growth rate among sources in the Europe collagen supplements market.

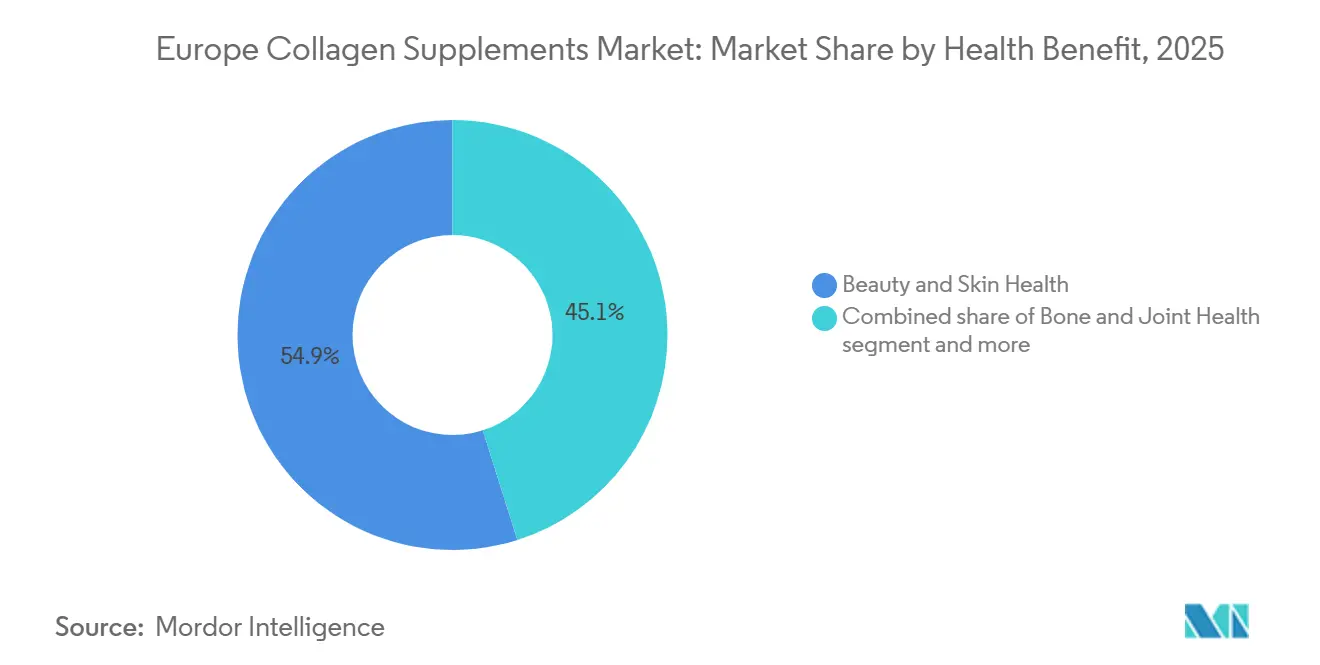

- By health benefit, beauty and skin health commanded 54.89% revenue in 2025; bone and joint health leads future momentum at a 9.23% CAGR, the quickest among health-benefit segments in the Europe collagen supplements market.

- By distribution channel, Pharmacies and drug stores delivered 51.84% of 2025 sales, yet online retail stores are poised for a 9.16% CAGR, the highest among distribution channels in the Europe collagen supplements market.

- By geography, Germany accounted for 19.80% of 2025 spend, while the United Kingdom is projected to advance at a 9.63% CAGR, the strongest pace among major geographies in the Europe collagen supplements market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Collagen Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for natural and clean-label products | +1.8% | Germany, United Kingdom, Netherlands, Sweden; spillover to France and Italy | Medium term (2-4 years) |

| Aging population actively seeking solutions for skin, bone, and joint health | +2.1% | Germany, Italy, France, Spain; moderate impact in United Kingdom and Belgium | Long term (≥ 4 years) |

| Rising focus on holistic wellness and beauty-from-within solutions | +1.5% | United Kingdom, France, Italy, Spain; emerging in Poland and Sweden | Medium term (2-4 years) |

| Strong demand for clinically supported and efficacious ingredients | +1.3% | Germany, United Kingdom, Netherlands; gradual adoption in Southern Europe | Medium term (2-4 years) |

| Expansion of online retail and e-commerce making products more accessible | +1.2% | United Kingdom, Germany, Netherlands, Sweden; accelerating in Poland and Spain | Short term (≤ 2 years) |

| Advancements in technology and innovation enabling diverse supplement formats | +0.9% | Germany, United Kingdom, France; pilot launches in Belgium and Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing consumer preference for natural and clean-label products

Increasing consumer awareness of health, wellness, and ingredient transparency is driving substantial demand for natural and clean-label products in the European collagen supplements market. Consumers are paying closer attention to product labels, prioritizing supplements made with recognizable, high-quality ingredients that align with their health objectives and lifestyle preferences. According to Ingredion’s 2024 report, 73% of European consumers actively seek products with recognizable ingredients, 85% accept functional ingredients offering additional health benefits, and 55% are willing to pay a premium for products with natural claims [1]Source: Vegconomist, "Ingredion Releases Significant Consumer Insights: Clean-Label is King, 73% of EU Consumers Seek Natural Ingredients", vegconomist.com. This change in consumer preferences is prompting collagen supplement manufacturers to focus on clean-label formulations, plant-based or sustainably sourced ingredients, and transparent labeling to build trust and foster brand loyalty. Products marketed as natural, additive-free, or derived from responsibly sourced collagen are gaining popularity, particularly among health-conscious consumers seeking benefits for skin, joint, and overall wellness.

Aging population actively seeking solutions for skin, bone, and joint health

The aging population in Europe is a significant driver of the collagen supplements market, as older adults increasingly seek products to support skin elasticity, bone health, and joint mobility. As of 1 January 2024, the EU population was estimated at 449.3 million, with over one-fifth (21.6%) aged 65 years and older, representing a growing demographic with specific health and wellness requirements [2]Source: Eurostat, "Population structure and ageing", europa.eu. This demographic shows a strong inclination to invest in preventive and functional nutrition, with collagen supplements emerging as a convenient and scientifically validated option to address age-related declines in connective tissue health, joint comfort, and skin appearance. Growing awareness of collagen's role in maintaining musculoskeletal health is further bolstered by healthcare recommendations, marketing efforts, and product innovations targeting age-related concerns. As a result, the aging population's emphasis on preserving mobility, vitality, and aesthetics is driving consistent growth in the European collagen supplements market. This trend is encouraging brands to develop tailored formulations, dosage forms, and delivery systems that align with the preferences and needs of this expanding consumer group.

Rising focus on holistic wellness and beauty‑from‑within solutions

The increasing focus on holistic wellness and preventative healthcare is driving the demand for collagen supplements across Europe. Consumers are prioritizing products that not only promote physical health but also improve beauty-related aspects such as skin elasticity, hair strength, and nail health. This trend aligns with broader healthcare developments, as seen in Germany, where healthcare expenditure rose to 12.3% of GDP in 2024, compared to 11.7% in 2023, indicating heightened investment in health and wellness at both individual and systemic levels[3]Source: OECD, "Health spending and financial sustainability", oecd.org. European consumers are becoming more aware of the importance of nutrition and functional ingredients in maintaining overall wellbeing, which is accelerating the adoption of supplements offering multiple benefits. Collagen, with its scientifically validated effects on skin, joints, and connective tissues, fits well within this "beauty-from-within" approach. In response, brands are introducing clean-label, natural formulations and functional blends to meet the growing demand for integrated wellness solutions.

Strong demand for clinically supported and efficacious ingredients

European consumers are placing greater emphasis on the clinical evidence supporting collagen supplements, favoring brands that invest in peer-reviewed research while penalizing those relying solely on anecdotal claims. This trend is particularly pronounced in Germany, where pharmacy-led distribution channels demand comprehensive dossiers to secure shelf space, and in the UK, where the Advertising Standards Authority has intensified scrutiny of unsubstantiated beauty claims. A 2024 systematic review published in Sports Medicine analyzed data from 19 randomized controlled trials (RCTs) and found that collagen peptide supplementation (15 grams daily for ≥8 weeks), when combined with resistance training, provided moderate-certainty evidence for increased fat-free mass and low-certainty evidence for improvements in tendon morphology and maximal strength. These findings are now being integrated into product labels and marketing strategies, with brands emphasizing specific peptide molecular weights (<2,000 Da) and amino acid profiles (glycine, proline, hydroxyproline) to highlight bioavailability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complexities of halal, kosher, and vegan certifications for supplements | -0.6% | Germany, France, United Kingdom, Belgium; acute in markets with diverse religious demographics | Medium term (2-4 years) |

| Taste, odor, and texture issues with certain collagen formats | -0.7% | United Kingdom, Germany, Netherlands, Sweden; dampens marine collagen adoption | Short term (≤ 2 years) |

| High prices of premium collagen supplements | -0.9% | Poland, Spain, Italy; limits mass-market penetration | Long term (≥ 4 years) |

| Difficulties maintaining consistent product quality and bioavailability | -0.5% | Germany, France, Netherlands; affects brand trust and regulatory scrutiny | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complexities of halal, kosher, and vegan certifications for supplements

Certification requirements for halal, kosher, and vegan collagen supplements create substantial operational and financial challenges, particularly for smaller brands, and hinder geographic expansion efforts. Halal certification, for instance, necessitates audits by organizations such as the Halal Food Council of Europe (HFCE), Halal Food Authority (HFA), or Halal Monitoring Committee (HMC), each enforcing distinct standards related to slaughter methods, cross-contamination prevention, and supply chain traceability. Bovine and porcine collagen are subject to heightened scrutiny: porcine collagen is entirely excluded from halal certification, while bovine collagen must come from animals slaughtered in accordance with Islamic rites. This requirement fragments supply chains and raises raw material costs by an estimated 15-20%. The certification challenges are particularly pronounced in Germany, France, and the UK, where Muslim and Jewish populations constitute significant consumer groups, and in Belgium, where regulatory enforcement of labeling accuracy is stringent. Brands that successfully meet these requirements, such as those sourcing from halal-certified facilities in India or Brazil, can access underserved demographics. However, the initial investment in certification and supply chain adjustments can exceed USD 500,000 for a mid-sized brand, creating a significant barrier to entry and reinforcing the dominance of established players.

Taste, odor, and texture issues with certain collagen formats

Sensory deficits continue to be a significant barrier to repeat purchases and category growth, particularly for marine collagen, which is characterized by a persistent fishy odor despite the use of flavoring and masking technologies. This challenge is especially evident in powder formats, where the large surface area of hydrolyzed peptides intensifies volatile compounds, and in unflavored variants marketed as "pure" or "clean-label," which prioritize ingredient simplicity over palatability. A 2024 study published in *Marine Drugs* identified that marine collagen's unique amino acid profile, with a lower Gly-Pro-Hyp content compared to bovine collagen, is linked to its sensory properties, indicating that the taste issue is inherent to the source rather than a result of processing. In markets like the UK and Sweden, where marine collagen adoption is highest due to sustainability preferences, taste-related churn is particularly pronounced. An estimated 40-50% of first-time marine collagen buyers in these regions either switch to bovine collagen or exit the category entirely after their initial purchase.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Innovation Drives Format Diversification

The Europe collagen supplements market shows a strong consumer preference for powder formulations, which are projected to hold a substantial 48.94% market share in 2025. In key markets such as France, Germany, and the United Kingdom, the adoption of powdered collagen is increasing, driven by beauty and anti-aging trends. Consumers are seeking supplements that support youthful skin, hair, and nails. According to Synadiet - National Union of Food Supplements, the percentage of individuals in France who consumed food supplements in the past 24 months rose from 59% in 2023 to 61% in 2024. Consequently, powdered collagen, particularly marine and bovine collagen, is being incorporated into daily routines for its benefits in enhancing skin elasticity and reducing wrinkles.

The drinks and shots segment has emerged as the most dynamic category, achieving a notable 9.93% CAGR through 2031. The increasing demand for collagen supplements in the form of drinks and shots across European countries is attributed to their convenience, rapid absorption, and the growing appeal of functional beverages. Consumers are favoring ready-to-drink options that fit into their busy lifestyles, driving innovation in this segment. Unlike powders or capsules, collagen drinks and shots offer a pre-mixed, easy-to-consume solution that requires no preparation, making them particularly appealing to professionals and travelers.

By Source: Marine Premiumization Versus Bovine Scale

Animal-based collagen accounted for 64.11% of the European market in 2025, supported by its cost efficiency, well-established supply chains, and superior amino acid profile, particularly for musculoskeletal applications. However, marine-based collagen is projected to grow at a CAGR of 9.56% through 2031, driven by its alignment with sustainability trends, the absence of religious certification challenges, and its perceived purity among health-conscious consumers. Germany and France lead in bovine collagen consumption, reflecting strong consumer familiarity and pharmacy-driven distribution channels that emphasize clinical evidence over sustainability considerations. Despite its dominance, bovine collagen faces two key challenges: the need for halal and kosher certifications, which complicates supply chains and raises costs, and emerging concerns about prion diseases, which, while not linked to collagen supplements, pose a potential reputational risk.

The 9.56% CAGR of marine collagen is fueled by its compatibility with European environmental priorities, particularly in countries like Sweden, the Netherlands, and the UK, where consumers value ocean-friendly sourcing and traceability. Marine collagen's smaller peptide size (lower molecular weight) is believed to enhance absorption, although clinical evidence remains inconclusive. Additionally, its lower Gly-Pro-Hyp content may limit its effectiveness for joint health compared to bovine collagen.

By Health Benefit: Bone and Joint Gains Clinical Traction

In 2025, beauty and skin health applications accounted for 54.89% of the Europe collagen supplements market. This dominance reflects the category's roots in nutricosmetics and the effectiveness of before-and-after imagery in digital marketing. However, the Bone and Joint Health segment is projected to grow at a CAGR of 9.23% through 2031, driven by an aging population, growing clinical evidence, and the increasing medicalization of collagen's positioning. The UK and France lead in beauty-focused consumption, where the "beauty-from-within" narrative is well-established. In contrast, Germany and the Netherlands show more balanced demand across beauty and joint health applications, emphasizing a clinical rather than cosmetic perspective.

The 9.23% CAGR in bone and joint health reflects the growing body of clinical evidence linking collagen peptide supplementation to improved musculoskeletal outcomes, particularly among adults aged 50 and above who aim to maintain functional independence. However, the segment faces challenges related to efficacy timelines. Joint health benefits typically require 8-12 weeks to become noticeable, compared to 4-6 weeks for skin improvements. This longer validation period increases the risk of customer churn. Other health benefits, such as gut health, cardiovascular support, and hair/nail strength, currently hold a marginal share of the market. Among these, gut health is emerging as a promising next-generation positioning, supported by research linking collagen peptides to improved intestinal barrier function.

By Distribution Channel: E-Commerce Erodes Pharmacy Margins

Pharmacies/drug stores accounted for 51.84% of collagen supplement distribution in Europe in 2025. This dominance is supported by consumer trust in pharmacist recommendations and the channel's role in filtering out low-quality products. The pharmacy channel's leadership is particularly evident in Germany, where Apotheke-vetted products command premium pricing, reflecting consumers' preference for quality assurance over convenience.

The 9.16% CAGR of online retail stores is primarily driven by the UK, where an estimated 35-40% of collagen sales occurred online in 2025. Other markets, such as the Netherlands and Sweden, also contribute to this growth due to their advanced e-commerce infrastructure and high levels of consumer digital literacy. The online channel facilitates subscription models that reduce purchase friction and enhance customer lifetime value. For instance, brands like Edible Health and Pura Collagen report that 40-50% of their online customers opt for auto-replenishment, ensuring predictable revenue streams and lowering customer acquisition costs over time.

Geography Analysis

In 2025, Germany accounted for 19.80% of the European collagen supplements market. This dominance was supported by stringent pharmacy-led quality assurance, consumer trust in Apotheke-approved products, and a regulatory framework emphasizing clinical evidence over marketing claims. Germany's position is influenced by its demographic profile, with a median age of 47.8 years in 2025, and a healthcare system that promotes preventive supplementation. However, the market faces limitations due to conservative health claim regulations under EFSA guidelines, which restrict aggressive marketing strategies.

The United Kingdom is projected to grow at a CAGR of 9.63% through 2031, marking the fastest growth among major geographies. This expansion is driven by a wellness culture emphasizing "beauty-from-within" concepts, a well-developed e-commerce infrastructure facilitating subscription-based regimens, and influencer-driven marketing that appeals to younger demographics. Growth is further supported by direct-to-consumer (D2C) brands such as Edible Health and Pura Collagen, which bypass traditional pharmacy channels and focus on digital customer acquisition. Additionally, the increasing presence of nutricosmetics in mainstream retail outlets like Boots and Holland & Barrett has contributed to market normalization.

France, Italy, and Spain collectively present a fragmented yet high-value market opportunity, where nutricosmetics align with Mediterranean beauty traditions. However, regulatory ambiguity surrounding health claims limits aggressive marketing and the clinical positioning that has driven adoption in Germany. In France, the market is characterized by the dominance of pharmacies and a preference for multi-ingredient beauty formulations, such as combinations of collagen, hyaluronic acid, and vitamin C. Italy demonstrates strong demand for marine collagen, despite its sensory drawbacks, reflecting environmental awareness and a cultural association between seafood and health.

Competitive Landscape

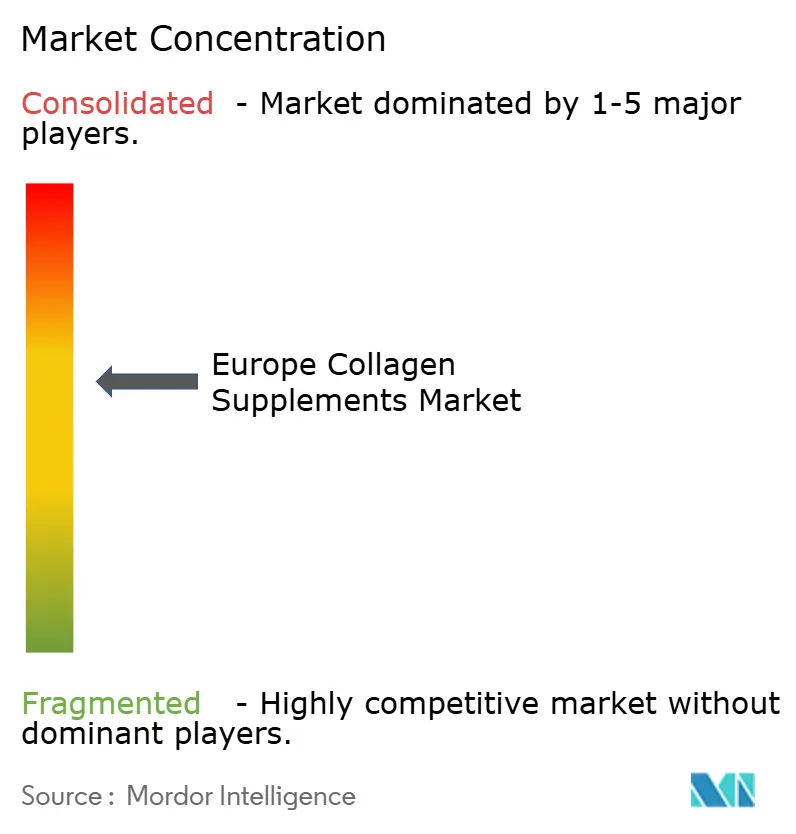

The Europe collagen supplements market is moderately concentrated, with intense competition among consumer health, beauty, and nutraceutical brands. These brands offer a wide range of collagen products in various formats, including powders, capsules, gummies, liquids, and ready-to-drink shots. The market's competitive nature is driven by increasing consumer demand for collagen-based products, which are associated with benefits such as improved skin health, joint support, and overall wellness. Additionally, the growing awareness of collagen's role in promoting healthy aging has further fueled the adoption of these supplements across diverse consumer segments. This has led to a dynamic market environment where companies continuously innovate to capture consumer interest and expand their market share.

Technology adoption plays a key role in the market, particularly through advanced fermentation platforms that facilitate the production of animal-free alternatives without compromising product effectiveness. The market offers significant opportunities in areas such as personalized nutrition solutions, glucose management formulations, and specialized delivery formats tailored to specific demographic groups. Emerging players are differentiating themselves by focusing on innovative product development, including novel extraction methods, sustainable sourcing practices, and direct-to-consumer business models that bypass traditional retail channels.

Innovation remains a priority for the industry, as evidenced by ongoing research and development efforts aimed at addressing consumer acceptance challenges. Patent activities highlight concentrated efforts in developing advanced taste-masking technologies and improving product bioavailability. These advancements reflect the industry's response to shifting consumer preferences and its commitment to enhancing product quality and user experience while maintaining a competitive edge in an increasingly sophisticated market.

Europe Collagen Supplements Industry Leaders

-

Shiseido Co. Ltd

-

Nestlé S.A.

-

Everest NeoCell LLC

-

Revive Naturals LLC

-

Hunter & Gather Foods Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Pura Collagen introduced two new product lines: Pura Digest and GLPure+. Pura Digest integrates hydrolyzed collagen peptides with prebiotic support to promote digestive comfort. GLPure+ combines clinically validated collagen peptides with chromium, vitamin C, and zinc to support metabolism and the natural GLP‑1 hormone response, offering a non-pharmaceutical alternative for glucose management.

- July 2024: Proto-col introduced its Verisol F Marine Collagen range, including the Marine Beauty Collagen product, in August 2025. This supplement contains 10,000 mg of bioavailable marine collagen peptides, hyaluronic acid, and essential vitamins designed to enhance skin elasticity, reduce wrinkles, and strengthen hair and nails.

- April 2024: Nestlé Health Science’s collaboration with ITV’s Lorraine supports the expanding collagen supplement market in Europe by promoting Vital Proteins as a convenient daily collagen option for consumers' morning routines, emphasizing collagen's importance in beauty and wellness.

Europe Collagen Supplements Market Report Scope

Collagen supplements contain amino acids, the building blocks of proteins, and other additional nutrients. These supplements are associated with several health benefits, like increasing muscle mass, preventing bone loss, relieving joint pain, and improving skin health by reducing wrinkles and dryness.

The European collagen supplements market is segmented by form, source, distribution channel, and country. Based on form, the market studied is segmented into powdered supplements, capsules and gummies, and drinks and shots. By source, the market is segmented into animal-based and marine-based collagen supplements. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacies/drug stores, online retail stores, specialty stores, and other distribution channels. By country, the market is segmented into Spain, the United Kingdom, Germany, France, Italy, Russia, and the Rest of Europe. For each segment, the market sizing and forecast are provided based on value (USD).

By Form

| Powder |

| Capsules |

| Gummies |

| Drinks and Shots |

| Others |

By Source

| Animal Based |

| Marine Based |

By Health Benefit

| Beauty and Skin Health |

| Bone and Joint Health |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Pharmacies/Drug Stores |

| Online Retail Stores |

| Specialty Stores |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Form | Powder |

| Capsules | |

| Gummies | |

| Drinks and Shots | |

| Others | |

| By Source | Animal Based |

| Marine Based | |

| By Health Benefit | Beauty and Skin Health |

| Bone and Joint Health | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Pharmacies/Drug Stores | |

| Online Retail Stores | |

| Specialty Stores | |

| Other Distribution Channels | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the Europe collagen supplements market be by 2031?

The market is forecast to reach USD 1.41 billion by 2031, expanding at an 8.22% CAGR from 2026.

Which format is growing fastest across Europe?

Ready-to-drink drinks and shots are projected to log a 9.93% CAGR through 2031 thanks to convenience and flavor improvements.

Why is marine collagen gaining popularity?

Marine variants avoid halal-kosher hurdles and align with sustainability values, driving a 9.56% CAGR even at higher price points.

Which health benefit segment is catching up with beauty?

Bone and joint health leads future momentum, expanding at a 9.23% CAGR as aging consumers seek musculoskeletal support.

Page last updated on: