Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

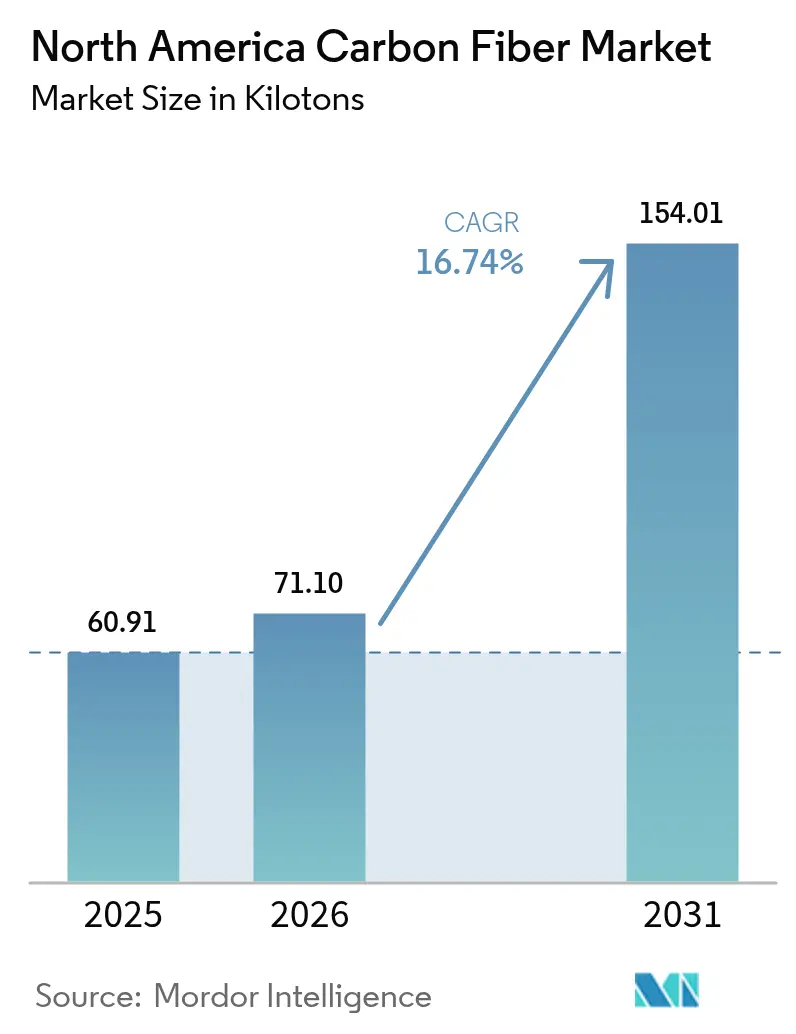

| Base Year Market Size (2025) | 60.91 kilotons |

| Market Volume (2026) | 71.1 kilotons |

| Market Volume (2031) | 154.01 kilotons |

| Growth Rate (2026 - 2031) | 16.74% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Carbon Fiber Market Analysis by Mordor Intelligence

The North America Carbon Fiber Market size is expected to grow from 60.91 kilotons in 2025 to 71.1 kilotons in 2026 and is forecast to reach 154.01 kilotons by 2031 at 16.74% CAGR over 2026-2031. Demand rises as aerospace production recovers, electric-vehicle makers cut curb weight and renewable-energy firms build longer wind blades. Polyacrylonitrile (PAN) continues to lead raw-material supply, yet fast-growing petroleum-pitch alternatives signal price-driven substitution. Recycled fibers gain traction because automakers and wind-turbine OEMs seek lower life-cycle emissions. United States output expansions by Hexcel and Toray improve local availability, but precursor sourcing and capital intensity still pose risk. Competitive success now depends on diversified end-use portfolios, agile production lines and close customer integration, rather than reliance on legacy aerospace volumes.

Key Report Takeaways

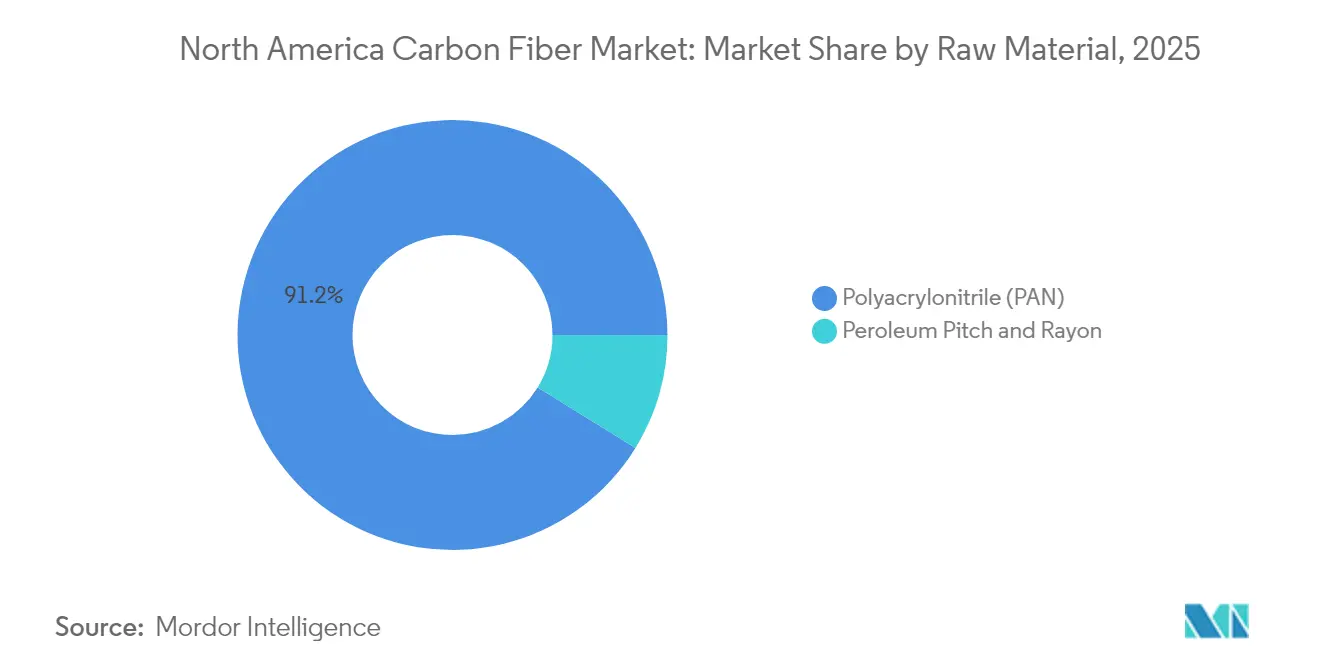

- By raw material, Polyacrylonitrile (PAN) retained 91.20% share of the North America carbon fiber market in 2025; petroleum pitch and rayon are projected to grow at an 18.25% CAGR to 2031.

- By type, virgin fiber commanded 75.40% share of the North America carbon fiber market size in 2025, while recycled fiber is advancing at a 18.48% CAGR through 2031.

- By application, composite materials accounted for 66.70% share of the North America carbon fiber market size in 2025 and are expected to rise at an 18.10% CAGR during the outlook period.

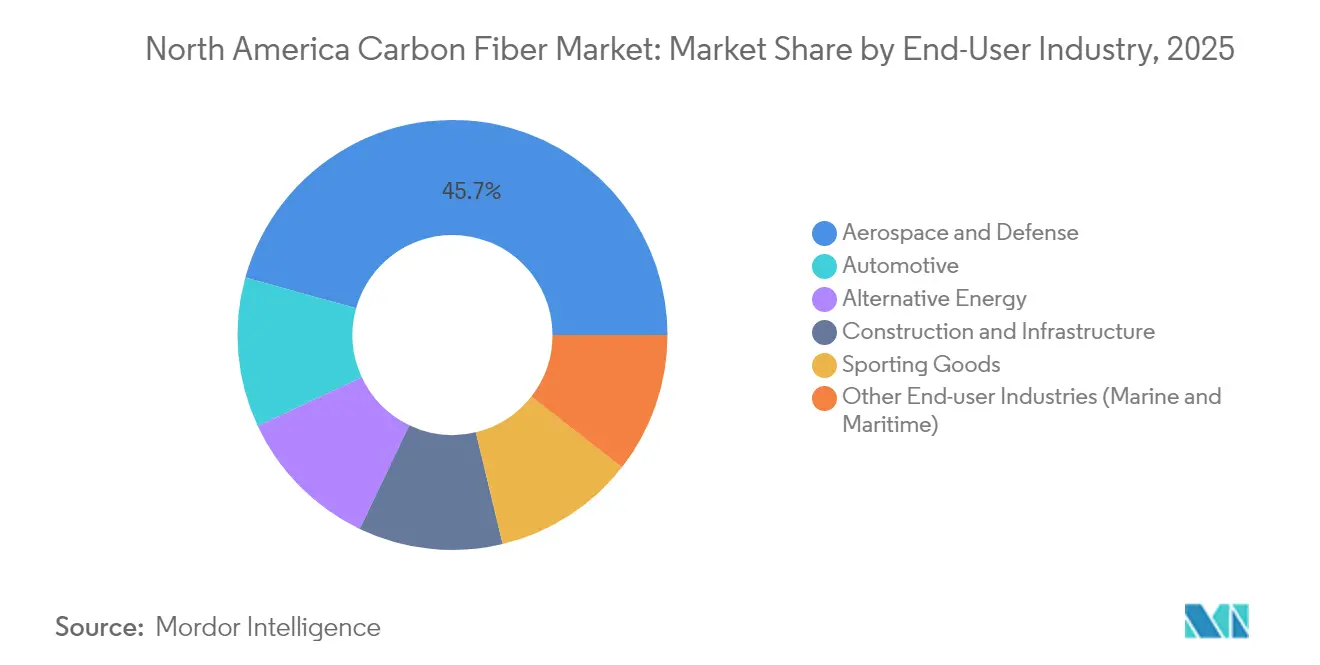

- By end-user industry, aerospace and defense held 45.70% of the North America carbon fiber market share in 2025, whereas automotive is forecast to expand at an 18.05% CAGR through 2031.

- By geography, the United States led with 62.90% share and is also set to post the fastest 17.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Carbon Fiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand from Lightweight Vehicles | +4.20% | United States & Canada, with spillover to Mexico | Medium term (2-4 years) |

| Accelerating Usage in Aerospace and Defense | +3.80% | United States primarily, with Canada defense applications | Long term (≥ 4 years) |

| Growing Utilization from Wind Energy Sector | +3.10% | United States & Canada, concentrated in wind corridor states | Medium term (2-4 years) |

| Expansion of High-Performance Sporting Goods | +1.70% | North America-wide, with premium market concentration | Short term (≤ 2 years) |

| Adoption in Hydrogen Storage Tanks for Heavy-Duty Mobility | +2.90% | United States & Canada, focused on transportation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Lightweight Vehicles

Automotive electrification positions the North America carbon fiber market at the center of new lightweight strategies. Automakers use automated-fiber-placement lines to integrate structural parts in mainstream models, as shown by General Motors’ pilot trials. Federal R&D funding from the U.S. Department of Energy accelerates ductile carbon-fiber composite development for battery-pack housings[1]U.S. Department of Energy, “Vehicle Technologies Office FY 2025 Program Plan,” energy.gov . Regulations on fuel economy and consumer range expectations underpin sustained multi-year demand across volume platforms.

Accelerating Usage in Aerospace and Defense

Aerospace keeps its lead within the North America carbon fiber market because next-generation aircraft and hypersonic defense systems require high-modulus fiber. Toray supplies thermoset and thermoplastic prepregs for NASA’s HiCAM program to improve fast-build composite wings. Collins Aerospace invested USD 200 million to enlarge Spokane carbon-carbon brake capacity, while GE Aerospace earmarked almost USD 1 billion for U.S. composite part production, reinforcing long-cycle demand visibility.

Growing Utilization from Wind Energy Sector

Blade lengths now exceed 100 meters for land-based turbines, and only carbon fiber delivers stiffness without penalty weight. Although SGL Carbon logged a 35.2% sales dip in 2023 due to inventory corrections, its long-term supply pacts with turbine OEMs keep the growth route intact. Fiberline’s profile deal with Nordex for Delta4000 models illustrates how specialized suppliers piece together multi-year volume programs.

Expansion of High-Performance Sporting Goods

Athletic footwear brands mainstreamed carbon-plate running shoes. Carbitex secured expansion funding to quintuple 2025 sales, driven by demand from global shoe makers. Brooks Running and other brands embed thin carbon inserts for energy return gains. Recreational-vehicle and consumer-equipment firms echo this trend, broadening the North America carbon fiber market scope beyond heavy industries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Research and Development, and Capital Expenditure | -2.80% | North America-wide, concentrated in manufacturing centers | Long term (≥ 4 years) |

| Regulatory-Driven Supply Risk for Raw Materials | -1.90% | United States & Canada, with trade policy implications | Medium term (2-4 years) |

| Limited Recycling Infrastructure and quality variance | -1.40% | United States primarily, with emerging Canada initiatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory-Driven Supply Risk for Raw Materials

Critical-material reviews by the White House and the Canadian government signal heightened scrutiny of PAN precursor imports. Policy shifts, such as export-control lists or stricter environmental permits, could pinch supply and raise compliance costs for the North America carbon fiber market.

Limited Recycling Infrastructure and Quality Variance

Recycled fiber often shows inconsistent sizing and shorter fiber lengths, limiting aerospace uptake. Investment flows into regional recycling hubs, but uniform standards and scaled logistics remain under development[2]Vartega, “Recycled Carbon Fiber Technology Overview,” vartega.com .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: PAN Dominance Faces Cost Pressures

PAN commanded 91.20% of the North America carbon fiber market in 2025. The segment benefits from proven strength-to-weight ratios and well-understood supply chains. Petroleum-pitch and rayon, in contrast, are set to grow at an 18.25% CAGR because auto and construction buyers prioritize lower cost over ultimate tensile strength. Advanced Carbon Products LLC has developed a mesophase pitch carbon fiber precursor, offering a significant cost-saving opportunity compared to the conventional PAN-based production method.

Demand shifts favor suppliers that diversify precursor choice. Higher yield rates that exceed 70% for pitch versus 55% for PAN can cut per-kilogram costs when furnace energy remains constant. For mass-market uses such as pressure vessels or civil infrastructure, these economics make alternative precursors increasingly credible options.

By Type: Virgin Fiber Leadership Challenged by Recycling Innovation

Virgin fiber retained 75.40% share of the North America carbon fiber market size in 2025 because aerospace and defense require full traceability. Recycled fiber, however, is projected to post a 18.48% CAGR. Vartega reached mechanical properties comparable to virgin fiber but at half the cost and 96-99% lower CO₂ footprint.

OEM acceptance of recycled intermediates is rising. Boeing’s use of KyronTEX sidewall panels shows that strict cabin-interior requirements can be met with reclaimed content. Automotive injection-molding compounds with recycled strands now cut finished-part cost by up to 30%, spurring volume adoption.

By Application: Composites Maintain Dual Leadership

Composite materials captured a 66.70% share and are also growing at an 18.10% CAGR, delivering both scale and momentum. Their leadership illustrates carbon fiber’s core value: enabling structures, not products. Automated fiber placement, rapid-cure resins, and closed-mold techniques shrink cycle times, broadening use in EV chassis, wind blades, and architectural retrofits.

Textile-grade fibers address 3-D woven preforms and braid sleeves for complex shapes, supplying segments such as marine and motorsports. Micro-electrode demand remains niche but validates fiber versatility. Catalysis fibers are used for high-surface-area reactors, yet volumes stay modest relative to structural composites.

By End-User Industry: Aerospace Leadership Faces Automotive Disruption

Aerospace and defense supplied 45.70% volume in 2025 thanks to long program cycles and stringent certification. Automotive, however, registers the fastest 18.05% CAGR as battery-electric platforms deploy carbon fiber to cut mass. Alternative-energy industries, including wind and hydrogen storage, further diversify outlets.

Construction agencies adopt carbon-fiber-reinforced polymer rebar to eliminate corrosion, lowering bridge life-cycle costs. Sporting-goods brands continue premium pricing for performance, offering attractive margins for specialty fiber runs and quick-turn fabrication.

Geography Analysis

The United States leads the North America carbon fiber market with a 62.90% share in 2025 and is projected to grow at an 17.60% CAGR to 2031. Federal designation of carbon fiber as a critical material spurs domestic furnace builds, while Hexcel and Toray expansions add 19,000 t of fresh yearly capacity. Defense and commercial aviation initiatives ensure baseline demand, whereas new mobility and wind-blade programs pull additional tonnage.

Canada follows with rising uptake in aerospace, hydrogen buses, and wind-turbine components. Research labs at the University of British Columbia advance bitumen-based fibers targeting a USD 12 kg cost to localize supply. Clean-tech investment credits and abundant hydroelectric power give Canadian producers a low-carbon advantage.

Mexico rounds out regional dynamics, leveraging USMCA access and competitive labor to host capacity such as Zoltek’s 13,000 t Guadalajara line. Aerospace clusters in Chihuahua now assemble complex aerostructures with imported and locally converted fiber. Smaller North American economies contribute niche volumes in marine and industrial equipment, helping solidify integrated supply chains across the continent.

Competitive Landscape

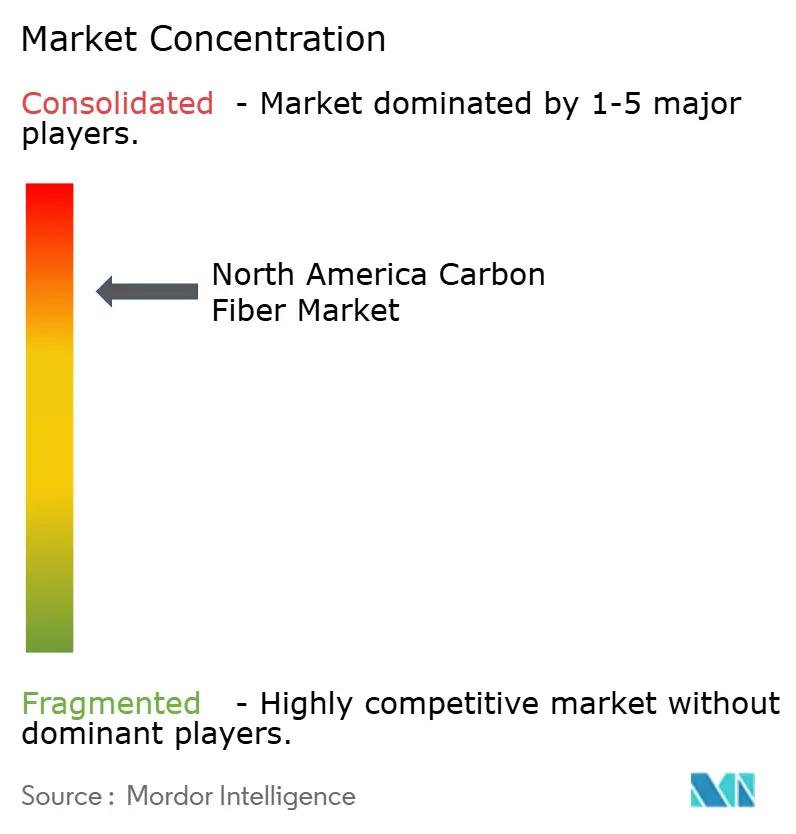

The North America carbon fiber market shows highly consolidated concentration because multimillion-dollar furnaces and proprietary know-how restrict new capacity. Hexcel, Toray, and SGL Carbon hold dominant positions, backed by long-term aerospace contracts and in-house precursor streams. Smaller innovators such as Vartega focus on recycling and low-cost pitch, targeting automotive and industrial clients.

Strategic moves emphasize vertical integration. Toray is adding 3,000 t capacity in South Carolina to supply hydrogen-tank filament-winding and pressure vessels. Collins Aerospace invests USD 200 million in carbon-carbon brakes, widening its aftermarket revenue base. Players deploy automated fiber placement and digital twins to raise throughput and cut scrap. Those that blend virgin, recycled and alternative-precursor lines position best for price volatility and sustainability reporting.

Supply-chain resilience measures include sourcing backup PAN strands, renewable electricity contracts and lifecycle certification. Firms that pair value-added processing with regionally proximate customers reduce logistics risk. Overall, the strategic landscape favors incumbents that continuously refresh technology and extend beyond a single sector reliance.

North America Carbon Fiber Industry Leaders

Hexcel Corporation

Mitsubishi Chemical Carbon Fiber and Composites Inc.

SGL Carbon

Syensqo

Toray Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Hexcel Corporation has introduced the HexTow IM9 24K continuous carbon fiber, offering the aerospace industry a lightweight, strong, and durable material designed to meet the demands of advanced composite applications.

- July 2023: Toray Composite Materials America, Inc. has announced plans to substantially expand its carbon fiber facility in Spartanburg, South Carolina. The 30,000-square-foot expansion is expected to enhance Toray’s carbon fiber production capacity by 3,000 metric tons annually, beginning in 2025.

North America Carbon Fiber Market Report Scope

Carbon fiber is a high-strength synthetic fiber composed mainly of carbon atoms. It is known for its exceptional strength-to-weight ratio, stiffness, and chemical resistance, which makes it a popular material in various industries. Carbon fiber is produced through a series of processes involving the conversion of carbon-rich precursors.

The North American carbon fiber market is segmented by raw material, type, application, end-user industry, and geography. By raw material, the market is segmented into polyacrylonitrile (PAN), petroleum pitch, and rayon. By type, the market is segmented into virgin fiber (VCF) and recycled carbon fiber (RCF). The applications of carbon fiber comprise composite materials, textiles, microelectrodes, and catalysis. By end-user industry, the market is segmented into aerospace and defense, alternative energy, automotive, construction and infrastructure, sporting goods, and other end-user industries (marine and maritime). The report also covers the market size and forecasts for the carbon fiber market in three countries across North America. For each segment, the market sizing and forecasts were made based on volume (tons).

By Raw Material

| Polyacrylonitrile (PAN) |

| Peroleum Pitch and Rayon |

By Type

| Virgin Carbon Fiber (VCF) |

| Recycled Carbon Fiber (RCF) |

By Application

| Composite Materials |

| Textiles |

| Micro-electrodes |

| Catalysis |

By End-user Industry

| Aerospace and Defense |

| Alternative Energy |

| Automotive |

| Construction and Infrastructure |

| Sporting Goods |

| Other End-user Industries (Marine and Maritime) |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Raw Material | Polyacrylonitrile (PAN) |

| Peroleum Pitch and Rayon | |

| By Type | Virgin Carbon Fiber (VCF) |

| Recycled Carbon Fiber (RCF) | |

| By Application | Composite Materials |

| Textiles | |

| Micro-electrodes | |

| Catalysis | |

| By End-user Industry | Aerospace and Defense |

| Alternative Energy | |

| Automotive | |

| Construction and Infrastructure | |

| Sporting Goods | |

| Other End-user Industries (Marine and Maritime) | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the projected CAGR for the North America carbon fiber market between 2026 and 2031?

The market is expected to expand at a 16.74% CAGR, rising from 71.1 kilotons in 2026 to 154.01 kilotons by 2031.

Which end-user industry currently consumes the most carbon fiber in North America?

Aerospace and defense leads with a 45.70% share of 2025 demand, thanks to ongoing aircraft production and defense modernization.

Why are recycled carbon fibers gaining momentum?

Recycled fibers offer up to 50% cost savings and a 96-99% cut in CO₂ emissions compared with virgin material, meeting automaker and wind-energy sustainability targets.

How significant is the United States within regional demand?

The United States accounts for 62.90% of 2025 volume and is also the fastest-growing geography at an 17.60% CAGR through 2031.

Which raw-material precursor is growing fastest, and why?

Petroleum-pitch and rayon precursors are forecast to grow at an 18.25% CAGR, as lower costs attract automotive and construction applications where ultra-high strength is not mandatory.

Page last updated on: